Attached files

| file | filename |

|---|---|

| EX-23.1 - Pershing Gold Corp. | q1100891_ex23-1.htm |

| EX-21.1 - Pershing Gold Corp. | q1100891_ex21-1.htm |

As filed with the Securities and Exchange Commission on December 6, 2012.

SEC File No. 333-179073

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

______________________

FORM S-1/A

(Amendment No. 3)

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

____________________

PERSHING GOLD CORPORATION

(Exact name of registrant as specified in its charter)

|

Nevada

|

1000

|

26-0657736

|

|

(State or other jurisdiction of

incorporation or organization)

|

(Primary Standard Industrial

Classification Code Number)

|

(I.R.S. Employer Identification No.)

|

1658 Cole Boulevard

Building 6-Suite 210

Lakewood, CO 80401

(877) 705-9357

(Address, including zip code, and telephone number,

including area code, of registrant’s principal executive offices)

Stephen Alfers

President and Chief Executive Officer

1658 Cole Boulevard

Building 6-Suite 210

Lakewood, CO 80401

(877) 705-9357

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

Harvey J. Kesner, Esq.

61 Broadway, 32nd Floor

New York, New York 10006

Telephone: (212) 930-9700

Fax: (212) 930-9725

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

(Check one):

|

Large accelerated filer

|

o

|

Accelerated filer

|

o

|

|

Non-accelerated filer

|

o

|

Smaller reporting company

|

x

|

|

(Do not check if a smaller reporting company)

|

CALCULATION OF REGISTRATION FEE

|

Title of Each Class of Securities to be Registered

|

Amount to be Registered (1)

|

Proposed Maximum

Offering Price per Share

|

Proposed Maximum

Aggregate Offering Price

|

Amount of

Registration Fee

|

|

Common stock, par value $.0001 per share (2)

|

91,324,590

|

$0.35(3)

|

$31,963,606.50

|

$4,359.84*

|

|

Common stock, par value $.0001 per share underlying warrants

|

914,688

|

$0.35(3)

|

$320,140.80

|

$43.67*

|

|

Total

|

92,239,278

|

$0.35(3)

|

$32,283,747.30

|

$4,403.51*

|

|

(1)

|

Pursuant to Rule 416 (b) under the Securities Act, the shares of common stock offered hereby also include an indeterminate number of additional shares of Common stock as may from time to time become issuable by reason of stock splits or stock dividends.

|

|

(2)

|

The shares of common stock will be offered under the secondary offering prospectus relating to resales by the selling stockholders of the shares of common stock issued to such selling stockholders.

|

|

(3)

|

Estimated solely for the purpose of calculating the registration fee, and based upon the average of the bid and ask price of the registrant’s common stock as reported on the OTC Markets’ OTCQB on December 4, 2012, in accordance with Rule 457(c) under the Securities Act.

|

*Previously Paid

THE REGISTRANT HEREBY AMENDS THIS REGISTRATION STATEMENT ON SUCH DATE OR DATES AS MAY BE NECESSARY TO DELAY ITS EFFECTIVE DATE UNTIL THE REGISTRANT SHALL FILE A FURTHER AMENDMENT WHICH SPECIFICALLY STATES THAT THIS REGISTRATION STATEMENT SHALL THEREAFTER BECOME EFFECTIVE IN ACCORDANCE WITH SECTION 8(a) OF THE SECURITIES ACT OF 1933 OR UNTIL THE REGISTRATION STATEMENT SHALL BECOME EFFECTIVE ON SUCH DATE AS THE COMMISSION, ACTING PURSUANT TO SAID SECTION 8(a), MAY DETERMINE.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED DECEMBER 6, 2012

92,239,278 Shares

PERSHING GOLD CORPORATION

Common Stock

_________________

This prospectus relates to the sale by the selling stockholders identified in this prospectus of up to 92,239,278 shares of our common stock, par value $0.0001 per share, which includes 914,688 shares of common stock issuable upon the exercise of outstanding warrants. On July 22, 2011 we agreed to file this registration statement under the Securities Act of 1933 to register the 76,095,215 shares of our common stock issued to Continental Resources Group, Inc. (“Continental”), which is expected to distribute such registered shares to its shareholders as part of its plan of liquidation. Continental owns 76,095,215 shares, or approximately 28.54% of our issued and outstanding common stock. Additional shares registered hereunder are being registered pursuant to registration obligations with the holders.

The prices at which the selling stockholders may sell shares will be determined by the prevailing market price for the shares or in privately negotiated transactions. We will not receive any proceeds from the sale of these shares by the selling stockholders. All expenses of registration incurred in connection with this offering are being borne by us, but all selling and other expenses incurred by the selling stockholders will be borne by the selling stockholders.

Our common stock is quoted on the regulated quotation service of the OTC Markets’ OTCQB under the symbol “PGLC.OB”. On December 5, 2012, the last reported sale price of our common stock as reported on the OTCQB was $0.35 per share.

Investing in our common stock is highly speculative and involves a high degree of risk. You should carefully consider the risks and uncertainties in the section entitled “Risk Factors” beginning on page 4 of this prospectus before making a decision to purchase our stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2012

TABLE OF CONTENTS

|

Page

|

|

|

1

|

|

|

4

|

|

|

4

|

|

|

4

|

|

|

13

|

|

|

13

|

|

|

14

|

|

|

24

|

|

|

34

|

|

|

36

|

|

|

41

|

|

|

46

|

|

|

47

|

|

|

48

|

|

|

51

|

|

|

52

|

|

|

52

|

|

|

52

|

|

|

53

|

|

|

F-1

|

You should rely only on the information contained in this prospectus. We have not authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not making an offer to sell these securities in any jurisdiction where an offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

The following summary highlights information contained elsewhere in this prospectus. It may not contain all the information that may be important to you. You should read this entire prospectus carefully, including the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operation,” and our historical financial statements and related notes included elsewhere in this prospectus. As used in this prospectus, unless otherwise specified, references to the “Company,” “we,” “our” and “us” refer to Pershing Gold Corporation and, unless otherwise specified, its subsidiaries.

Overview

We are a gold and precious metals exploration company pursuing exploration and development opportunities primarily in Nevada. We are currently focused on exploration at our Relief Canyon properties in Pershing County in northwestern Nevada. None of our properties contain proven and probable reserves, and all of our activities on all of our properties are exploratory in nature. To date, we have not generated any revenues from our mining operations.

For the year ended December 31, 2011, we reported a net loss of approximately ($24.6) million. We reported a net loss of approximately ($5.1) million for the quarter ended September 30, 2012 and approximately ($45.6) million for the nine months ended September 30, 2012. We expect to incur significant losses into the foreseeable future and our monthly “burn rate” for general and administrative costs (including all employee salaries, public company expenses and consultants) is approximately $500,000. Our monthly burn rate for all costs during each month of the fourth quarter 2012 is expected to be approximately $700,000 (including exploration and facilities recommissioning). We will need to obtain additional funding to fund operations and exploration beginning in January 2013.

Business Strategy

Our business strategy is to acquire and advance precious metals exploration properties. We seek properties with known mineralization that are in an advanced stage of exploration and have previously undergone some drilling but are under-explored, which we believe we can advance quickly to increase value. We are currently focused on exploration on the Relief Canyon properties, commencing mining at Relief Canyon Mine, and recommissioning the Relief Canyon gold processing facility. We acquired the former Relief Canyon Mine property in August 2011, which includes a processing plant that could be used in mining operations. We began an exploration drilling program in 2011 that we plan to continue. We expanded our Relief Canyon property position in 2012 significantly with the acquisition of approximately 22,000 acres of unpatented mining claims and other property interests in the Pershing Pass area. We refer to our combined land position of approximately 25 square miles along the Humboldt Range, both north and south of the Relief Canyon Mine area as the “Relief Canyon expansion properties”. We refer to the Relief Canyon Mine property and Relief Canyon expansion properties collectively as the “Relief Canyon properties”. We continue drilling to expand the Relief Canyon Mine deposit and aim to obtain a National Instrument 43-101 technical report during the first quarter of 2013.

Our 2012 exploration program is nearly complete. We spent approximately $4.8 million on exploration activities during the nine months ended September 30, 2012 and anticipate spending approximately $0.4 million for the remainder of 2012. We will require external funding not only to pursue our exploration program but also to maintain our operations beginning in 2013. Our forecasted total costs for exploration in 2013 are $3.6 million.

In addition to our exploration program, we are preparing to recommission the gold processing facility on the Relief Canyon Mine site, which is currently in a care and maintenance status. We expect the cost to recommission the facility will be approximately $2.6 million, and our goal is to have it recommissioned by the end of 2013.

Our estimated total cost for 2013 of exploration, permitting, landholding, facilities recommissioning and general and administrative is approximately $13 million, which includes the 2013 exploration and recommissioning amounts described above, and in more detail below.

We intend to continue to acquire additional mineral targets in Nevada and elsewhere in locations where we believe we have the potential to quickly expand and advance known mineralization and the potential to discover new deposits. We will require external funding to pursue our exploration programs. There is no assurance we will be able to raise capital on acceptable terms or at all.

If, through our exploration program, we discover an area that may be able to be profitably mined for gold, we would focus most of our activities on determining whether that is feasible, including further delineation of the location, size and economic feasibility of a potential orebody. If our efforts are successful, we anticipate that we would seek additional capital through debt or equity financing to fund further development, or that we would sell or lease the rights to mine to a third party or enter into joint venture or other arrangements. There is no assurance that we could obtain additional capital or a willing third party.

1

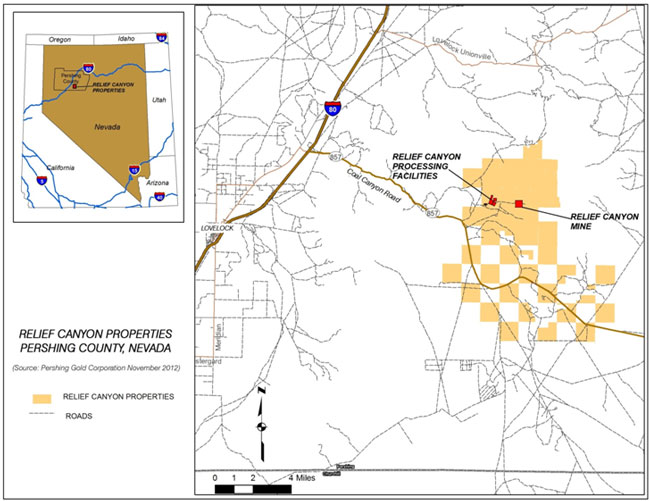

Relief Canyon Properties

The Relief Canyon properties contain approximately 24,000 acres and are comprised of approximately 1,000 unpatented mining claims, 118 millsites and private lands. We commenced our Phase I drilling program at the Relief Canyon Mine property in September 2011; this program was designed to test conceptual targets as well as the continuity and grade of mineralized zones found by previous operators.

We have three initiatives at our Relief Canyon properties:

1. Relief Canyon Mine

The main objective of the Company is to expand the existing deposit and commence mining at the existing Relief Canyon Mine. We completed the final phase of drilling for 2012 with an additional 83 holes comprising approximately 27,300 feet. This drilling was on land adjacent to the current deposit in order to extend and upgrade the existing deposit. We have drilled a total of 123 drill holes comprising approximately 58,000 feet at Relief Canyon Mine. We are also completing baseline geologic mapping of the mine pits.

We spent approximately $4.3 million on exploration activities at the Relief Canyon Mine during the nine months ended September 30, 2012 and anticipate spending approximately $0.4 million for the remainder of 2012. Our exploration plan for 2013 is to continue to concentrate our resources on the Relief Canyon Mine in order to refine our understanding of the deposit. We currently estimate that full year 2013 exploration costs at Relief Canyon Mine will be approximately $3.0 million. This amount is subject to change and also subject to receiving adequate external financing. If we do not receive adequate financing we will have to curtail our exploration and also delay or cancel commencement of mining at Relief Canyon Mine.

Our target is to produce gold in 2014 from newly mined ore, gold-bearing materials on the dumps, and/or toll ores from other properties. The reopening of the Relief Canyon Mine is dependent on obtaining sufficient external funding, the receipt of permits, and expansion of the deposit as a result of our exploration efforts above the water table. Additional permitting will be needed to mine the deposit below the water table. There is no guarantee that we will produce gold in 2014 or at all.

2. Relief Canyon Expansion Properties

We are conducting generative exploration on the Relief Canyon expansion properties. In 2012, we generated targets through surface sampling, mapping, and geophysics at three specific projects in our Relief Canyon expansion properties: Pershing Pass, Pershing Packard, and South Relief. These areas are shown on our map on page 26.

Through November 2012 we drilled four holes comprising approximately 3,000 feet and performed soil sampling, and geochemical and geophysical testing to identify new drill-ready targets. This cost approximately $500,000. Approximately $50,000 of the remainder of the 2012 exploration budget is expected to be spent at the Relief Canyon expansion properties. Our exploration plan for 2013 is to continue to generate targets for future exploration – our goal is to generate four drill-ready targets per year. We currently estimate that full year 2013 exploration costs will be $600,000. This amount would decrease if we do not receive adequate financing, or increase if we have very good exploration results and receive adequate financing. If we do not receive adequate external financing we will have to curtail, postpone or cancel exploration activities.

Because the Relief Canyon expansion properties are at an early stage of exploration, it will take at least several years to perform sufficient exploration to determine whether these properties contain mineable reserves that could be put into production in the future. Exploration costs in future years may increase or decrease depending on results and available funding.

We consider expenditures on our Relief Canyon expansion properties to have a lower priority than expenditures on the Relief Canyon Mine property. If we do not receive adequate funding, we would reduce, postpone or cancel expenditures at our Relief Canyon expansion properties before reducing, postponing or cancelling exploration activity at Relief Canyon Mine.

3. Recommissioning Relief Canyon Processing Facility

In June 2012 we began to prepare the Relief Canyon heap leach processing facility for recommissioning. The Relief Canyon processing facility was completed in 2008, is fully permitted, and is currently in a care and maintenance status.

We plan to amend the permits for this facility to authorize processing of ores from sites outside of Relief Canyon Mine and to add a gold recovery (strip) circuit. If there are delays in obtaining the permit to leach ores from other sites, we would only be able to leach ores from the Relief Canyon Mine. If we make a future discovery of mineable reserves at the Relief Canyon expansion properties, we would seek an amendment to the permits for the Relief Canyon processing facility to expand the capacity of the leach pad and ponds to accommodate additional ore. If there are delays in obtaining the permit to add the gold recovery system, we would sell gold-loaded carbon to another facility that would recover/strip the gold.

2

In order to recommission the facility, from now through the end of 2013 we anticipate our activities will include construction on the site such as building a lab facility and core shack, engineering, design and construction of the pollution control devices for the strip circuit, improving the computer system, and purchasing equipment such as crusher repair parts and start up supplies like lime and cyanide. Once recommissioned and amended permits received, the Relief Canyon heap leach processing facility would be available to process newly mined ores from the Relief Canyon Mine, previously leached heaps, gold-bearing waste rocks on existing waste rock dumps, as well as materials from other mines. We expect the total cost to recommission the facility will be approximately $2.6 million, and our goal is to have it recommissioned by the end of 2013. If we are unable to raise adequate external funding we would reduce or cancel this recommissioning activity.

We consider expenditures on recommissioning the Relief Canyon processing facility to have a lower priority than expenditures on Relief Canyon Mine. If we do not receive adequate funding, we would reduce, postpone or cancel expenditures at our Relief Canyon processing facility before reducing, postponing or cancelling exploration activity Relief Canyon Mine.

Events Subsequent to September 30, 2012

Director and Management Changes

In November 2012, we appointed Alex Morrison to our board of directors. In addition, further to Pershing’s decision to bring its finance and accounting function inside the company, we designated Eric Alexander, our Vice President of Finance and Controller, as principal financial officer and principal accounting officer. The board of directors accepted the resignations of Adam Wasserman as Chief Financial Officer and David Rector as Treasurer, Vice President of Administration and Finance and member of the board of directors. Mr. Rector will remain as an employee of the Company to assist with transition matters and other projects until the end of 2012.

Private Placement

On December 3, 2012, we completed a private offering of common stock to accredited investors, including one of our directors, in which we sold an aggregate of 9,469,548 shares of common stock and warrants for the purchase of 3,787,819 shares of common stock for an aggregate purchase price of $3,124,950. The purchase price for one share of common stock and a warrant to acquire 0.40 of a share of common stock was $0.33. The warrants are exercisable immediately at an exercise price of $0.50 per share and will expire on December 7, 2015.

Property Disposition

In order to focus our efforts on the Relief Canyon properties, in May 2012, we sold our North Battle Mountain Mineral Prospect and Red Rock Mineral Prospect gold exploration properties, and all of our uranium exploration properties.

Financial Results

We reported a net loss of approximately ($24.6) million for the year ended December 31, 2011 as compared to a net loss of approximately ($2.0) million for the period from February 10, 2010 (inception) to December 31, 2010. We reported a net loss of approximately ($45.6) million for the nine months ended September 30, 2012 as compared to a net loss of approximately ($20.3) million for the nine months ended September 30, 2011. We expect to incur significant losses into the foreseeable future and our monthly “burn rate” for general and administrative costs (including all employee salaries, public company expenses and consultants) is approximately $500,000. Our monthly burn rate for all costs during each month of the fourth quarter 2012 is expected to be $700,000 (including exploration and facilities recommissioning). We will spend approximately $5.2 million on exploration in 2012, and our estimated exploration costs for 2013 are approximately $3.6 million. If we are unable to raise external funding, and eventually generate significant revenues from our claims and properties, we will not be able to earn profits or continue operations. We have no production history upon which to base any assumption as to the likelihood that we will prove successful, and it is uncertain that we will generate any operating revenues or ever achieve profitable operations. If we are unsuccessful in addressing these risks, our business will most likely fail.

Corporate Information

We were incorporated in Nevada on August 2, 2007 under the name “Excel Global, Inc.” and operated as a web-based service provider and consulting company. On September 27, 2010, we changed our name to “The Empire Sports & Entertainment Holdings Co.” and commenced the promotion and production of sports and entertainment events as our sole line of business which we operated until September 1, 2011 when we exited the sports and entertainment business. We began acquiring mining exploration properties in May 2011, and on May 16, 2011, we changed our name to “Sagebrush Gold Ltd.” and on February 27, 2012 to “Pershing Gold Corporation” due to our focus on exploration for gold in Pershing County, Nevada.

Our principal executive offices are located at 1658 Cole Boulevard, Building 6-Suite 210, Lakewood, CO 80401 and our telephone number is 877-705-9357.

3

|

Common stock offered by the selling stockholders:

|

92,239,278 shares, consisting of 76,095,215 shares issued to Continental in connection with the purchase of substantially all of its assets, 15,229,375 shares subject to registration rights obligations of the Company and 914,688 shares of common stock underlying warrants to purchase shares of the Company’s common stock which are subject to certain registration rights obligations.

|

|

|

Common stock outstanding before this offering:

|

266,592,027 (1)

|

|

|

Common stock outstanding after this offering

|

267,506,715 (2)

|

|

|

Use of proceeds:

|

We will not receive any proceeds from the sale of shares in this offering by the selling stockholders.

|

|

|

OTC Bulletin Board symbol:

|

PGLC.OB

|

|

|

Risk factors:

|

You should carefully consider the information set forth in this prospectus and, in particular, the specific factors set forth in the “Risk Factors” section beginning on page 4 of this prospectus before deciding whether or not to invest in shares of our common stock.

|

|

(1) The number of outstanding shares before the offering is based upon 266,592,027 shares outstanding as of December 3, 2012 and excludes:

|

|

| • |

35,298,000 shares of common stock issuable upon the exercise of outstanding options; and

|

| • |

16,255,779 shares of common stock issuable upon the exercise of outstanding warrants.

|

|

(2) The number of outstanding shares after the offering is based upon 266,592,027 shares outstanding as of December 3, 2012 and 914,688 shares of common stock offering for resale hereunder upon exercise of certain outstanding warrants and excludes:

|

|

| • |

35,298,000 shares of common stock issuable upon the exercise of outstanding options; and

|

| • |

15,341,091 shares of common stock issuable upon the exercise of outstanding warrants.

|

This prospectus contains forward-looking statements. The use of any statements containing the words “anticipate,” “intend,” “believe,” “estimate,” “project,” “expect,” “plan,” “should” or similar expressions are intended to identify such statements. Such statements include statements regarding our expectations, hopes, beliefs or intentions regarding the future, including but not limited to statements regarding our financing, market, strategy, competition, development plans (including acquisitions and expansion), revenues, operations, and compliance with applicable laws. Forward-looking statements involve certain risks and uncertainties, and actual results may differ materially from those discussed in any such statement. Factors that could cause actual results to differ materially from such forward-looking statements include, but are not limited to, risks and uncertainties related to: anticipated expenditures and costs in our operations; planned exploration activities and the anticipated outcome of such exploration activities; our ability to obtain financing to fund our estimated expenditure and capital requirements; the establishment and estimates of mineral reserves and resources; the grade of mineral reserves and resources; plans and anticipated timing for obtaining permits and licenses for our properties; anticipated liquidity to meet expected operating costs and capital requirements; estimates of environmental liabilities; factors expected to impact our results of operations; and risks related to development, bonding, permitting, construction, other activities related to mine development; significant increases or decreases in gold prices; metallurgy, processing, access, availability of materials, equipment, supplies and water; results of pending and future feasibility studies; and other factors, many of which are beyond our control, including those additional risks as described in the following section “Risk Factors”. All forward-looking statements in this document are made as of the date hereof, based on information available to us as of the date hereof, and we assume no obligation to update any forward-looking statement.

Investing in our common stock involves a high degree of risk. Before investing in our common stock you should carefully consider the following risks, together with the financial and other information contained in this prospectus. If any of the following risks actually occurs, our business, prospects, financial condition and results of operations could be adversely affected. In that case, the trading price of our common stock would likely decline and you may lose all or a part of your investment.

RISKS RELATING TO OUR BUSINESS

We have no proven or probable reserves on our properties and we do not know if our properties contain any gold or other minerals that can be mined at a profit.

The properties on which we have the right to explore for gold and other minerals are not known to have any deposits of gold or other minerals which can be mined at a profit (as to which there can be no assurance). Whether a gold or other mineral deposit can be mined at a profit depends upon many factors. Some but not all of these factors include: the particular attributes of the deposit, such as size, grade and proximity to infrastructure; operating costs and capital expenditures required to start mining a deposit; the availability and cost of financing; the price of the gold or other mineral which is highly volatile and cyclical; and government regulations, including regulations relating to prices, taxes, royalties, land use, importing and exporting of minerals and environmental protection. We are also obligated to pay production royalties on certain of our mining activities, including a net smelter royalty of 2% on production from our Relief Canyon Gold assets acquired during 2011, which would increase our costs of production and make our ability to operate profitably more difficult.

4

We are an exploration stage company and have only recently commenced exploration activities on our claims. We reported a net loss for the year ended December 31, 2011 and subsequent quarters to date, and expect to incur operating losses for the foreseeable future.

Our evaluation of our Relief Canyon properties are primarily based on historical exploration data. In addition, our exploration programs are in their early stages. Accordingly, we are not yet in a position to estimate expected amounts of minerals, yields or values or evaluate the likelihood that our business will be successful. We have not earned any revenues from mining operations. The likelihood of success must be considered in light of the problems, expenses, difficulties, complications and delays encountered in connection with the exploration of the mineral properties that we plan to undertake. These potential problems include, but are not limited to, unanticipated problems relating to exploration, and additional costs and expenses that may exceed current estimates. Prior to completion of our exploration stage, we anticipate that we will incur increased operating expenses without realizing any revenues. We reported a net loss of approximately ($24.6) million for the year ended December 31, 2011 as compared to a net loss of approximately ($2.0) million for the period from February 10, 2010 (inception) to December 31, 2010. We reported a net loss of approximately ($5.1) million for the quarter ended September 30, 2012 and approximately ($45.6) million for the nine months ended September 30, 2012. We expect to incur significant losses into the foreseeable future and our monthly “burn rate” for general and administrative costs (including all employee salaries, public company expenses and consultants) is approximately $500,000. Our monthly burn rate for all costs during each month of the fourth quarter 2012 is expected to be approximately $700,000 (including exploration and facilities recommissioning). We will spend approximately $5.2 million on exploration in 2012, and our estimated exploration costs for 2013 are $3.6 million. Our estimated facility recommissioning costs for 2013 are $2.6 million. If we are unable to raise external funding, and eventually generate significant revenues from our claims and properties, we will not be able to earn profits or continue operations. We have no production history upon which to base any assumption as to the likelihood that we will prove successful, and it is uncertain that we will generate any operating revenues or ever achieve profitable operations. If we are unsuccessful in addressing these risks, our business will most likely fail.

Exploring for gold and other minerals is inherently speculative, involves substantial expenditures, and is frequently non-productive.

Mineral exploration (currently our only business), and gold exploration in particular, is a business that by its nature is very speculative. There is a strong possibility that we will not discover gold or any other minerals which can be mined or extracted at a profit. Even if we do discover gold or other deposits, the deposit may not be of the quality or size necessary for us or a potential purchaser of the property to make a profit from actually mining it. Few properties that are explored are ultimately developed into producing mines. Unusual or unexpected geological conditions, fires, flooding, explosions, cave-ins, landslides and the inability to obtain suitable or adequate machinery, equipment or labor are just some of the many risks involved in mineral exploration programs and the subsequent development of gold deposits.

The mining industry is capital intensive and we may be unable to raise necessary funding.

We estimate that we will require approximately $2.1 million to operate and explore during the fourth quarter of 2012. These expenses include approximately $1.5 million for general and administrative costs, $400,000 for exploration, and $175,000 for permitting and property maintenance costs. Our estimated total cost for 2013 for exploration, permitting, landholding, facilities recommissioning and for general and administrative costs is approximately $13 million. We will need to obtain additional funding to fund operations and exploration. We may be unable to secure additional financing on terms acceptable to us, or at all. Our inability to raise additional funds on a timely basis could prevent us from achieving our business objectives and could have a negative impact on our business, financial condition, results of operations and the value of our securities. If we raise additional funds by issuing additional equity or convertible debt securities, the ownership of existing stockholders may be diluted and the securities that we may issue in the future may have rights, preferences or privileges senior to those of the current holders of our common stock. Such securities may also be issued at a discount to the market price of our common stock, resulting in possible further dilution to the book value per share of common stock. If we raise additional funds by issuing debt, we could be subject to debt covenants that could place limitations on our operations and financial flexibility.

Unanticipated problems or delays in recommissioning our gold processing facility may negatively affect our operations.

If our processing facility recommissioning plans are threatened or delayed because we are unable to finance it or for other reasons, our business may experience a substantial setback. Prolonged problems may fatally threaten the commercial viability of our planned facilities. Moreover, the occurrence of significant unforeseen conditions or events in connection with the processing facility may require us to re-examine the thoroughness of our due diligence and planning processes. Any change to management’s evaluation of the viability of the project could have a material adverse effect on our business, consolidated financial condition or results of operations.

5

Projected recommissioning and financing costs for the processing facility may also increase to a level that would make these facilities too expensive to recommission or unprofitable to operate. Currently we expect the total cost to recommission the facility will be approximately $2.6 million. Contractors, engineering firms, construction firms and equipment suppliers also receive requests and orders from other companies and, therefore, we may not be able to secure their services or products on a timely basis or on acceptable financial terms. We may suffer significant delays or cost overruns as a result of a variety of factors, such as increases in the prices or materials, permitting delays, shortages of workers or materials, transportation constraints, adverse weather, equipment failures, fires, damage to or destruction of property and equipment, environmental damage, unforeseen difficulties or labor issues, any of which could delay or prevent us from commencing operations. Any of these factors could have a material adverse effect on our business, consolidated financial conditions or results of operations.

We are a junior exploration company with no operating mining activities and we may never have any mining activities in the future.

Our business is exploring for gold and, to a lesser extent, other minerals. If we discover commercially exploitable gold or other deposits, we will not be able to make any money from mining activities unless the gold or other deposits are actually mined, or we sell our interest. Accordingly, we will need to seek additional capital through debt or equity financing, find some other entity to mine our properties or operate our facilities on our behalf, enter into joint venture or other arrangements with a third party, or sell or lease the property our rights to mine to third parties. Mine development projects typically require a number of years and significant expenditures during the development phase before production is possible. Such projects could experience unexpected problems and delays during development, construction and mine start-up. Mining operations in the United States are subject to many different federal, state and local laws and regulations, including stringent environmental, health and safety laws. If and when we assume operational responsibility for mining on our properties, it is possible that we will be unable to comply with current or future laws and regulations, which can change at any time. It is possible that changes to these laws will be adverse to any potential mining operations. Moreover, compliance with such laws may cause substantial delays and require capital outlays in excess of those anticipated, adversely affecting any potential mining operations. Our future mining operations, if any, may also be subject to liability for pollution or other environmental damage. It is possible that we will choose to not be insured against this risk because of high insurance costs or other reasons.

We have a short operating history, have only lost money and may never achieve any meaningful revenue.

We acquired all of our property interests during the past 15 months. Our operating history consists of starting our exploration activities. We have no income-producing activities from mining or exploration. We have already lost money because of the expenses we have incurred in acquiring the rights to explore on our property and conducting our exploration activities. Exploring for gold and other minerals or resources is an inherently speculative activity. There is a strong possibility that we will not find any commercially exploitable gold or other deposits on our property. Because we are an exploration company, we may never achieve any meaningful revenue.

We must make annual lease payments, advance royalty and royalty payments and claim maintenance payments or we will lose our rights to our property.

We are required under the terms of our property interests to make annual lease payments starting in 2014 and advance royalty and royalty payments each year. We are also required to make annual claim maintenance payments to the U.S. Bureau of Land Management (“BLM”) and pay a fee to Pershing County in order to maintain our rights to explore and, if warranted, to develop our unpatented mining claims. If we fail to meet these obligations, we will lose the right to explore for gold and other minerals on our property. Our total estimated annual property maintenance costs payable to the BLM for all of the unpatented mining claims and millsites in the Relief Canyon area in 2012 are approximately $160,000, which will remain approximately the same unless we acquire or dispose of some unpatented mining claims. Our total annual costs payable to county authorities is approximately $12,000. Our lease payments, advance royalty and royalty payments and claim maintenance payments are described above under “Business and Properties”.

Our business is subject to extensive environmental regulations which may make exploring, mining or related activities prohibitively expensive, and which may change at any time.

All of our operations are subject to extensive environmental regulations which can substantially delay exploration and make exploration expensive or prohibit it altogether. We may be subject to potential liabilities associated with the pollution of the environment and the disposal of waste products that may occur as the result of exploring and other related activities on our properties, including our plan to process gold at our processing facility. We may have to pay to remedy environmental pollution, which may reduce the amount of money that we have available to use for exploration or other activities, and adversely affect our financial position. If we are unable to fully remedy an environmental problem, we might be required to suspend operations or to enter into interim compliance measures pending the completion of the required remedy. If a decision is made to mine our properties and we retain any operational responsibility for doing so, our potential exposure for remediation may be significant, and this may have a material adverse effect upon our business and financial position. We have not purchased insurance for potential environmental risks (including potential liability for pollution or other hazards associated with the disposal of waste products from our exploration activities) and such insurance may not be available to us on reasonable terms or at a reasonable price. All of our exploration and, if warranted, development activities may be subject to regulation under one or more local, state and federal environmental impact

6

analyses and public review processes. It is possible that future changes in applicable laws, regulations and permits or changes in their enforcement or regulatory interpretation could have significant impact on some portion of our business, which may require our business to be economically re-evaluated from time to time. These risks include, but are not limited to, the risk that regulatory authorities may increase bonding requirements beyond our financial capability. Inasmuch as posting of bonding in accordance with regulatory determinations is a condition to the right to operate under all material operating permits, increases in bonding requirements could prevent operations even if we are in full compliance with all substantive environmental laws. We have been required to post substantial bonds under various laws relating to mining and the environment and may in the future be required to post further bonds to pursue additional activities. For example, we must provide BLM and the Nevada Division of Environmental Protection Bureau of Mining Regulation and Reclamation (“NDEP”) additional financial assurance (reclamation bonds) to guarantee reclamation of any new surface disturbance required for drill roads, drill sites, or mine expansion. We have provided BLM and NDEP a reclamation bond in the amount of approximately $4.6 million that covers both the exploration and mining features at the Relief Canyon Mine property, including the three open-pit mines and associated waste rock disposal areas, the mineral processing facilities, ancillary facilities, and the exploration roads and drill pads. Our preliminary estimate of the likely amount of additional financial assurance to conduct exploration is approximately $190,000. Our preliminary estimate of the likely amount of additional financial assurance to recommence mining operations is $75,000. See “Business and Properties – Relief Canyon Properties – Environmental Permitting Requirements” for additional information regarding our environmental permitting budget. We may be unable or unwilling to post such additional bonds which could prevent us from realizing any commercial mining success or commencing mining activities.

The government licenses and permits which we need to explore on our property may take too long to acquire or cost too much to enable us to proceed with exploration. In the event that we discover commercially exploitable deposits, we may face substantial delays and costs associated with securing the additional government licenses and permits which we will need to mine on our property which could preclude our ability to develop the mine. We are also seeking to amend the permit for our existing gold processing facility, which may be delayed.

Exploration activities usually require the granting of permits from various governmental agencies. For example, exploration drilling on unpatented mining claims requires a permit to be obtained from the United States Bureau of Land Management, which may take several months or longer to grant the requested permit. Depending on the size, location and scope of the exploration program, additional permits may also be required before exploration activities can be undertaken. Prehistoric or Indian grave yards, threatened or endangered species, archeological sites or the possibility thereof, difficult access, excessive dust and important nearby water resources may all result in the need for additional permits before exploration activities can commence. In addition, we are seeking amendments to our permits for our gold processing facility, in order to leach ores from other sites, and to add a gold recovery (stripping) system to the facility. If there are delays in obtaining the permit to leach ores from other sites, we would only be able to leach ores from the Relief Canyon Mine. If we make a future discovery of mineable reserves at the Relief Canyon expansion properties, we would seek an amendment to the permits for the Relief Canyon processing facility to expand the capacity of the leach pad and ponds to accommodate additional ore. If there are delays in obtaining the permit to add the gold recovery system, we would sell gold-loaded carbon to another facility that would recover/strip the gold. We estimate the cost of amending these permits will be less than $10,000. As with all permitting processes, there is the risk that unexpected delays and excessive costs may be experienced in obtaining required permits. The needed permits may not be granted, or may be granted in an acceptable timeframe or cost too much. Delays in or our inability to obtain necessary permits will result in unanticipated costs, which may result in serious adverse effects upon our business.

The value of our property is subject to volatility in the price of gold and any other deposits we may seek or locate.

Our ability to obtain additional and continuing funding, and our profitability if and when we commence mining operations or sell our rights to mine, will be significantly affected by changes in the market price of gold and other mineral deposits. Gold and other minerals’ prices fluctuate widely and are affected by numerous factors, all of which are beyond our control. The price of gold may be influenced by:

|

•

|

fluctuation in the supply of, demand and market price for gold;

|

|

|

•

|

mining activities of our competitors;

|

|

|

•

|

sale or purchase of gold by central banks and for investment purposes by individuals and financial institutions;

|

|

|

•

|

interest rates;

|

|

|

•

|

currency exchange rates;

|

|

|

•

|

inflation or deflation;

|

|

|

•

|

fluctuation in the value of the United States dollar and other currencies;

|

|

|

•

|

global and regional supply and demand, including investment, industrial and jewelry demand; and

|

|

|

•

|

political and economic conditions of major gold or other mineral-producing countries.

|

7

The price of gold and other minerals have fluctuated widely in recent years, and a decline in the price of gold or other minerals could cause a significant decrease in the value of our property, limit our ability to raise money, and render continued exploration and development of our property impracticable. If that happens, then we could lose our rights to our property or be compelled to sell some or all of these rights. Additionally, the future development of our mining properties beyond the exploration stage is heavily dependent upon the level of gold prices remaining sufficiently high to make the development of our property economically viable.

Our property title may be challenged. We are not insured against any challenges, impairments or defects to our mining claims or title to our other properties.

Our property is comprised primarily of unpatented lode mining claims and millsites located and maintained in accordance with the federal General Mining Law of 1872. Unpatented lode mining claims and millsites are unique U.S. property interests and are generally considered to be subject to greater title risk than other real property interests because the validity of unpatented mining claims and millsites is often uncertain. This uncertainty arises, in part, out of the complex federal and state laws and regulations with which the owner of an unpatented mining claim or millsite must comply in order to locate and maintain a valid claim. If we discover mineralization that is close to the claim boundaries, it is possible that some or all of the mineralization may occur outside the boundaries. In such a case we would not have the right to extract those minerals. The uncertainty resulting from not having a title search or having the claims surveyed on our properties leaves us exposed to potential title defects. Defending any challenges to our property title would be costly, and may divert funds that could otherwise be used for exploration activities and other purposes. For example, on February 7, 2012, the Company obtained a copy of a complaint filed in the United States District Court for the Southern District of New York (the “Complaint”) entitled Relief Gold Group, Inc., v Sagebrush Gold Ltd, Gold Acquisition Corp. (“GAC”), Barry C. Honig, and David S. Rector (12 civ 0952). Relief Gold alleges various causes of action including breach of contract, intentional interference with contract, intentional interference with prospective business relationship/economic relations, misappropriation of trade secrets and unjust enrichment, related to the Company’s acquisition on August 30, 2011 of the assets of the Relief Canyon Mine pursuant to Chapter 11 of the Bankruptcy Code. Relief Gold seeks money damages and to enjoin Sagebrush, Honig, Rector and GAC from exercising its rights and privileges gained or acquired as a result of any alleged unlawful conduct, including any management rights over GAC or the assets acquired by GAC as a result of the alleged wrongful conduct of the other defendants. Relief Gold further seeks to disgorge the profits, benefits and any other advantages gained by reason of the alleged unlawful conduct.

In addition, unpatented lode mining claims and millsites are always subject to possible challenges by third parties or contests by the federal government, which, if successful, may prevent us from exploiting our discovery of commercially extractable gold. Challenges to our title may increase our costs of operation or limit our ability to explore on certain portions of our property. We are not insured against challenges, impairments or defects to our property title.

Possible amendments to the General Mining Law could make it more difficult or impossible for us to execute our business plan.

In recent years, the U.S. Congress has considered a number of proposed amendments to the General Mining Law, as well as legislation that would make comprehensive changes to the law. Although no such legislation has been adopted to date, there can be no assurance that such legislation will not be adopted in the future. If adopted, such legislation could, among other things, (i) adopt the limitation on the number of millsites that a claimant may locate, discussed below, (ii) impose time limits on the effectiveness of plans of operation that may not coincide with mine life, (iii) impose more stringent environmental compliance and reclamation requirements on activities on unpatented mining claims and millsites, (iv) establish a mechanism that would allow states, localities and Native American tribes to petition for the withdrawal of identified tracts of federal land from the operation of the General Mining Law, (v) allow for administrative determinations that mining would not be allowed in situations where undue degradation of the federal lands in question could not be prevented, and (vi) impose royalties on gold and other mineral production from unpatented mining claims or impose fees on production from patented mining claims. Further, it could have an adverse impact on earnings from our operations, could reduce estimates of any reserves we may establish and could curtail our future exploration and development activity on our unpatented claims.

Our ability to conduct exploration, development, mining and related activities may also be impacted by administrative actions taken by federal agencies. With respect to unpatented millsites, for example, the ability to use millsites and their validity has been subject to greater uncertainty since 1997. In November of 1997, the Secretary of the Interior (appointed by President Clinton) approved a Solicitor’s Opinion which concluded that the General Mining Law imposed a limitation that only a single five-acre millsite may be claimed or used in connection with each associated and valid unpatented or patented lode mining claim. Subsequently, however, on October 7, 2003, the new Secretary of the Interior (appointed by President Bush) approved an Opinion by the Deputy Solicitor which concluded that the mining laws do not impose a limitation that only a single five-acre millsite may be claimed in connection with each associated unpatented or patented lode mining claim. Current federal regulations do not include the millsite limitation. There can be no assurance, however, that the Department of the Interior will not seek to re-impose the millsite limitation at some point in the future.

8

In addition, a consortium of environmental groups has filed a lawsuit in the United District Court for the District of Columbia against the Department of the Interior, the Department of Agriculture, the Bureau of Land Management, or BLM, and the USFS, asking the court to order the BLM and USFS to adopt the five-acre millsite limitation. That lawsuit also asks the court to order the BLM and the USFS to require mining claimants to pay fair market value for their use of the surface of federal lands where those claimants have not demonstrated the validity of their unpatented mining claims and millsites. If the plaintiffs in that lawsuit were to prevail, that could have an adverse impact on our ability to use our unpatented millsites for facilities ancillary to our exploration, development and mining activities, and could significantly increase the cost of using federal lands at our properties for such ancillary facilities.

Market forces or unforeseen developments may prevent us from obtaining the supplies and equipment necessary to explore for gold and other minerals.

Gold exploration and mineral exploration in general, is a very competitive business. Competitive demands for contractors and unforeseen shortages of supplies and/or equipment could result in the disruption of our planned exploration activities. Current demand for exploration drilling services, equipment and supplies is robust and could result in suitable equipment and skilled manpower being unavailable at scheduled times for our exploration program. Fuel prices are extremely volatile as well. We will attempt to locate suitable equipment, materials, manpower and fuel if sufficient funds are available. If we cannot find the equipment and supplies needed for our various exploration programs, we may have to suspend some or all of them until equipment, supplies, funds and/or skilled manpower become available. Any such disruption in our activities may adversely affect our exploration activities and financial condition.

Our directors and executive officers lack significant experience or technical training in exploring for precious and base metal deposits and in developing mines.

Our directors and executive officers lack significant experience or technical training in exploring for precious and base metal deposits and in developing mines. Accordingly, our management may not be fully aware of many of the specific requirements related to working within this industry. Their decisions and choices may not take into account standard engineering or managerial approaches that mineral exploration companies commonly use. Consequently, our operations, earnings, and ultimate financial success could suffer irreparable harm due to some of our management’s lack of experience in the mining industry.

We may not be able to maintain the infrastructure necessary to conduct exploration activities.

Our exploration activities depend upon adequate infrastructure. Reliable roads, bridges, power sources and water supply are important factors which affect capital and operating costs. Unusual or infrequent weather phenomena, sabotage, government or other interference in the maintenance or provision of such infrastructure could adversely affect our exploration activities and financial condition.

Our exploration activities may be adversely affected by the local climate or seismic events, which could prevent us from gaining access to our property year-round.

Earthquakes, heavy rains, snowstorms, and floods could result in serious damage to or the destruction of facilities, equipment or means of access to our property, or may otherwise prevent us from conducting exploration activities on our property. There may be short periods of time when the unpaved portion of the access road is impassible in the event of extreme weather conditions or unusually muddy conditions. During these periods, it may be difficult or impossible for us to access our property, make repairs, or otherwise conduct exploration activities on them.

RISKS RELATING TO OUR ORGANIZATION AND COMMON STOCK

We have relied on a certain stockholder to provide significant investment capital to fund our operations.

We have in the past relied on cash infusions primarily from Frost Gamma Investments Trust (“Frost Gamma”). During the year ended December 31, 2011, Frost Gamma provided approximately $5,000,000 to us to fund operations in consideration for the issuance of certain of our securities. Curtailment of cash investments by Frost Gamma could detrimentally impact our cash availability and our ability to fund its operations.

Our principal shareholder, officers and directors own a substantial interest in our voting stock and investors will have limited voice in our management.

Our principal shareholders Continental and Frost Gamma, as well as our officers and directors, in the aggregate beneficially own in excess of approximately 61.59% of our outstanding common stock, including shares of common stock issuable upon exercise or conversion within 60 days of the date of this filing. Currently, Continental owns 76,095,215 shares, or 28.54% of our common stock, and our officers and directors beneficially own 40,767,542 shares, or 14.49% of our common stock. Additionally, the holdings of our officers and directors may increase in the future upon vesting or other maturation of exercise rights under any of the convertible securities they may hold or in the future be granted or if they otherwise acquire additional shares of our common stock.

9

As a result of their ownership and positions, our principal shareholder, directors and executive officers collectively are able to influence all matters requiring shareholder approval, including the following matters:

|

|

•

|

election of our directors;

|

|

|

•

|

amendment of our articles of incorporation or bylaws; and

|

|

|

•

|

effecting or preventing a merger, sale of assets or other corporate transaction.

|

In addition, their stock ownership may discourage a potential acquirer from making a tender offer or otherwise attempting to obtain control of the Company, which in turn could reduce our stock price or prevent our shareholders from realizing a premium over our stock price.

The price disparities between the price of our common stock and the price of the common stock of our principal shareholder may cause insiders to trade in our common stock.

Our principal shareholder, Continental, owns 76,095,215 shares of our common stock and intends to distribute those shares to its shareholders subsequent to such time that the SEC declares the Registration Statement, of which this prospectus forms a part, effective. As a result of the price disparities that may arise from time to time between the price of our common stock and the price of the common stock of Continental, we believe that, from time to time, investors may seek to participate in transactions based upon these pricing disparities and buy, sell, short or hedge shares of our common stock or shares of common stock of Continental. Such transactions should not be viewed as indicative of the success of our business or of our future prospects. A member of our Board of Directors is a shareholder of Continental, and has stated that he may acquire or dispose of shares and undertake additional transactions in the outstanding securities of Continental.

Our director owns a significant stake in our principal shareholder, and as a result may be able to exert influence over this shareholder, which could result in a conflict of interest.

Currently, Continental, our principal shareholder, owns 76,095,215 shares, or 28.54%, of our common stock, which it intends to distribute to its shareholders as part of its plan of liquidation. Barry Honig, a member of our board of directors, is the largest shareholder of Continental and beneficially owns 12,194,236 shares, or 12.8%, of Continental. In addition, 3,535,000 shares of Continental are owned by various Uniform Transfer to Minor Act accounts for which Mr. Honig’s father is custodian for the benefit of Mr. Honig’s minor children. Mr. Honig exercises no investment or voting power and disclaims beneficial ownership of the shares owned by accounts for which his father is custodian. In addition, 150,000 shares are owned by Alan Honig. Although Mr. Barry Honig disclaims beneficial ownership of such shares, if aggregated, the percent of class represented by the aggregate amount beneficially owned and the excluded shares would be 16.69% of Continental’s issued and outstanding shares. Such amounts are excluded from Mr. Honig’s beneficial ownership amounts reported herein. We are subject to the reporting requirements of federal securities laws, and compliance with such requirements can be expensive and may divert resources from other projects, thus impairing our ability to grow.

We are subject to the information and reporting requirements of the Securities and Exchange Act of 1934, as amended (the “Exchange Act”), and other federal securities laws, including compliance with the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”).

The costs of preparing and filing annual and quarterly reports and other information with the Securities and Exchange Commission and furnishing audited reports to stockholders will cause our expenses to be higher than they would have been if we were privately held. These costs for the year ended December 31, 2011 were approximately $604,000 and we anticipate incurring costs relating to being a public company of $800,000 for the year ending December 31, 2012.

It may be time consuming, difficult and costly for us to develop, implement and maintain the internal controls and reporting procedures required by the Sarbanes-Oxley Act. We may need to hire additional financial reporting, internal controls and other finance personnel in order to develop and implement appropriate internal controls and reporting procedures.

If we fail to establish and maintain an effective system of internal control, we may not be able to report our financial results accurately or to prevent fraud. Any inability to report and file our financial results accurately and timely could harm our reputation and adversely impact the trading price of our common stock.

Effective internal control is necessary for us to provide reliable financial reports and prevent fraud. If we cannot provide reliable financial reports or prevent fraud, we may not be able to manage our business as effectively as we would if an effective control environment existed, and our business and reputation with investors may be harmed. As a result, our small size and any current internal control deficiencies may adversely affect our financial condition, results of operation and access to capital. Management has determined that our internal audit function is significantly deficient due to insufficient qualified resources to perform internal audit functions. During our assessment of the effectiveness of internal control over financial reporting as of December 31, 2011, management identified significant deficiency related to (i) our internal audit functions, and (ii) a lack of segregation of duties within accounting functions. Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with any policies and procedures may deteriorate.

10

Public company compliance may make it more difficult to attract and retain officers and directors.

The Sarbanes-Oxley Act and rules implemented by the Securities and Exchange Commission have required changes in corporate governance practices of public companies. As a public company, we expect these rules and regulations to increase our compliance costs in 2012 and beyond and to make certain activities more time consuming and costly. As a public company, we also expect that these rules and regulations may make it more difficult and expensive for us to obtain director and officer liability insurance and we may be required to accept reduced policy limits and coverage or incur substantially higher costs to obtain the same or similar coverage. As a result, it may be more difficult for us to attract and retain qualified persons to serve on our board of directors or as executive officers, and to maintain insurance at reasonable rates, or at all.

Because we became public by a reverse merger, we may not be able to attract the attention of major brokerage firms.

There may be risks associated with us becoming public through a “reverse merger.” Securities analysts of major brokerage firms may not provide coverage of us since there is no incentive to brokerage firms to recommend the purchase of our common stock. No assurance can be given that brokerage firms will, in the future, want to conduct any offerings on our behalf.

Our stock price may be volatile.

The market price of our common stock is likely to be highly volatile and could fluctuate widely in price in response to various factors, many of which are beyond our control, including the following:

| • |

results of operations and exploration efforts;

|

|

| • |

fluctuation in the supply of, demand and market price for gold;

|

|

| • |

our ability to obtain working capital financing;

|

|

| • |

additions or departures of key personnel;

|

|

| • |

limited “public float” in the hands of a small number of persons whose sales or lack of sales could result in positive or negative pricing pressure on the market price for our common stock;

|

|

| • |

our ability to execute our business plan;

|

|

| • |

sales of our common stock and decline in demand for our common stock;

|

|

| • |

regulatory developments;

|

|

| • |

economic and other external factors;

|

|

| • |

investor perception of our industry or our prospects; and

|

|

| • |

period-to-period fluctuations in our financial results.

|

In addition, the securities markets have from time to time experienced significant price and volume fluctuations that are unrelated to the operating performance of particular companies. These market fluctuations may also materially and adversely affect the market price of our common stock. As a result, you may be unable to resell your shares at a desired price.

We have not paid cash dividends in the past and do not expect to pay dividends in the future. Any return on investment may be limited to the value of our common stock.

We have never paid cash dividends on our common stock and do not anticipate doing so in the foreseeable future. The payment of dividends on our common stock will depend on earnings, financial condition and other business and economic factors affecting us at such time as our board of directors may consider relevant. If we do not pay dividends, our common stock may be less valuable because a return on your investment will only occur if our stock price appreciates.

There is currently a very limited trading market for our common stock and we cannot ensure that one will ever develop or be sustained.

Our shares of common stock are very thinly traded, only a small percentage of our common stock is available to be traded and is held by a small number of holders and the price, if traded, may not reflect our actual or perceived value. There can be no assurance that there will be an active market for our shares of common stock either now or in the future. The market liquidity will be dependent on the perception of our operating business, among other things. We may, in the future, take certain steps, including utilizing investor awareness campaigns, press releases, road shows and conferences to increase awareness of our business and any steps that we might take to bring us to the awareness of investors may require we compensate consultants with cash and/or stock. There can be no assurance that there will be any awareness generated or the results of any efforts will result in any impact on our trading volume. Consequently, investors may not be able to liquidate their investment or liquidate it at a price that reflects the value of the business and trading may be at an inflated price relative to the performance of our company due to, among other things, availability of sellers of our shares. If a market should develop, the price may be highly volatile. Because there may be a low price for our shares of common stock, many brokerage firms or clearing firms may not be willing to effect transactions in the securities or accept our shares for deposit in an account. Even if an investor finds a broker willing to effect a transaction in the shares of our common stock, the combination of brokerage commissions, transfer fees, taxes, if any, and any other selling costs may exceed the selling price. Further, many lending institutions will not permit the use of low priced shares of common stock as collateral for any loans.

11

We anticipate having our common stock continue to be quoted for trading on the OTC Bulletin Board or the OTCQB; however, we cannot be sure that such quotations will continue. As soon as is practicable, we anticipate applying for listing of our common stock on the NYSE MKT or other national securities exchange, assuming that we can satisfy the initial listing standards for such exchange. We currently do not satisfy the initial listing standards, and cannot ensure that we will be able to satisfy such listing standards or that our common stock will be accepted for listing on any such exchange. Should we fail to satisfy the initial listing standards of such exchanges, or our common stock is otherwise rejected for listing and remain listed on the OTC Bulletin Board or OTCQB or suspended from the OTC Bulletin Board or OTCQB, the trading price of our common stock could suffer and the trading market for our common stock may be less liquid and our common stock price may be subject to increased volatility.

Our common stock is deemed a “penny stock,” which would make it more difficult for our investors to sell their shares.

Our common stock is subject to the “penny stock” rules adopted under Section 15(g) of the Exchange Act. The penny stock rules generally apply to companies whose common stock is not listed on the NASDAQ Stock Market or other national securities exchange and trades at less than $4.00 per share, other than companies that have had average revenue of at least $6,000,000 for the last three years or that have tangible net worth of at least $5,000,000 ($2,000,000 if the company has been operating for three or more years). These rules require, among other things, that brokers who trade penny stock to persons other than “established customers” complete certain documentation, make suitability inquiries of investors and provide investors with certain information concerning trading in the security, including a risk disclosure document and quote information under certain circumstances. Many brokers have decided not to trade penny stocks because of the requirements of the penny stock rules and, as a result, the number of broker-dealers willing to act as market makers in such securities is limited. If we remain subject to the penny stock rules for any significant period, it could have an adverse effect on the market, if any, for our securities. If our securities are subject to the penny stock rules, investors will find it more difficult to dispose of our securities.

Offers or availability for sale of a substantial number of shares of our common stock may cause the price of our common stock to decline.

If our stockholders sell substantial amounts of our common stock in the public market or upon the expiration of any statutory holding period, under Rule 144, or upon expiration of lock-up periods applicable to outstanding shares, or issued upon the exercise of outstanding options or warrants, it could create a circumstance commonly referred to as an “overhang” and in anticipation of which the market price of our common stock could fall. The existence of an overhang, whether or not sales have occurred or are occurring, also could make more difficult our ability to raise additional financing through the sale of equity or equity-related securities in the future at a time and price that we deem reasonable or appropriate.

Exercise of options or warrants may result in substantial dilution to existing shareholders.

If the price per share of our common stock at the time of exercise of any options or warrants or conversion of any other convertible securities is in excess of the various exercise or conversion prices of such convertible securities, exercise or conversion of such convertible securities would have a dilutive effect on our common stock. As of the date hereof, we had reserved shares issuable upon exercise of (i) options to purchase 35,298,000 shares of our common stock and (ii) warrants to purchase 16,255,779 shares of our common stock. Further, any additional financing that we secure may require the granting of rights, preferences or privileges senior to those of our common stock and which result in additional dilution of the existing ownership interests of our common stockholders.

Our articles of incorporation allow for our board to create new series of preferred stock without further approval by our stockholders, which could adversely affect the rights of the holders of our common stock.