Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Home Federal Bancorp, Inc. of Louisiana | form8k.htm |

Exhibit 99.1

1st Quarter Performance Update

December 2012

Forward Looking Statements

2

u This document contains forward-looking statements as that term is defined in the Private Securities

Litigation Reform Act of 1995. Forward-looking statements can be identified by the fact that they

do not relate strictly to historical or current facts. They often include words like “believe,”

“expect,” “anticipate,” “estimate” and “intend” or future or conditional verbs such as “will,”

“would,” “should,” “could” or “may.” We undertake no obligation to update any forward-looking

statements.

Litigation Reform Act of 1995. Forward-looking statements can be identified by the fact that they

do not relate strictly to historical or current facts. They often include words like “believe,”

“expect,” “anticipate,” “estimate” and “intend” or future or conditional verbs such as “will,”

“would,” “should,” “could” or “may.” We undertake no obligation to update any forward-looking

statements.

u These forward-looking statements include, but are not limited to:

u statements of goals, intentions and expectations;

u statements regarding prospects and business strategy;

u statements regarding asset quality and market risk; and

u estimates of future costs, benefits and results.

u Any of the forward-looking statements that we make in this communication and in other public

statements may turn out to be wrong because of inaccurate assumptions we might make or because

of other factors that we cannot foresee. Because of these and other uncertainties, our actual future

results may be materially different from the results indicated by these forward-looking statements

and you should not rely on such statements.

statements may turn out to be wrong because of inaccurate assumptions we might make or because

of other factors that we cannot foresee. Because of these and other uncertainties, our actual future

results may be materially different from the results indicated by these forward-looking statements

and you should not rely on such statements.

1st Quarter Highlights

► Continued execution and implementation of strategic initiatives drove another strong quarter

► Net income of $939,000 for the three months ended September 30, 2012 ($0.35 fully diluted EPS) driven by

stronger net interest income and mortgage banking income

stronger net interest income and mortgage banking income

► Quarterly net income increased 17% over the three month period ended September 30, 2011

► Net interest margin expanded to 4.08% for the three months ended September 30, 2012, up from 3.69%

for the same period last year

for the same period last year

► Significant growth opportunities in the commercial sector

► Commercial banking team has been successful in generating both loans and low cost deposits

► Superior asset quality profile as of September 30, 2012

► No non-performing assets

► No net charge-offs in the past twelve quarters

► Significant capital levels

► Tangible common equity to tangible assets ratio of 18.1%

► Effective use of capital management tools

► Maintained $0.06 per share quarterly cash dividend (MRQ payout ratio of 17%)

► Repurchased 306,360 shares of stock since 2nd step conversion as of September 30, 2012

► Fully funded Recognition and Retention Plan with purchase of 77,808 shares

► Strong aftermarket performance since the 2nd step conversion in December 2010

► Stock up approximately 76% since the 2nd step transaction*

3

* As of November 30, 2012.

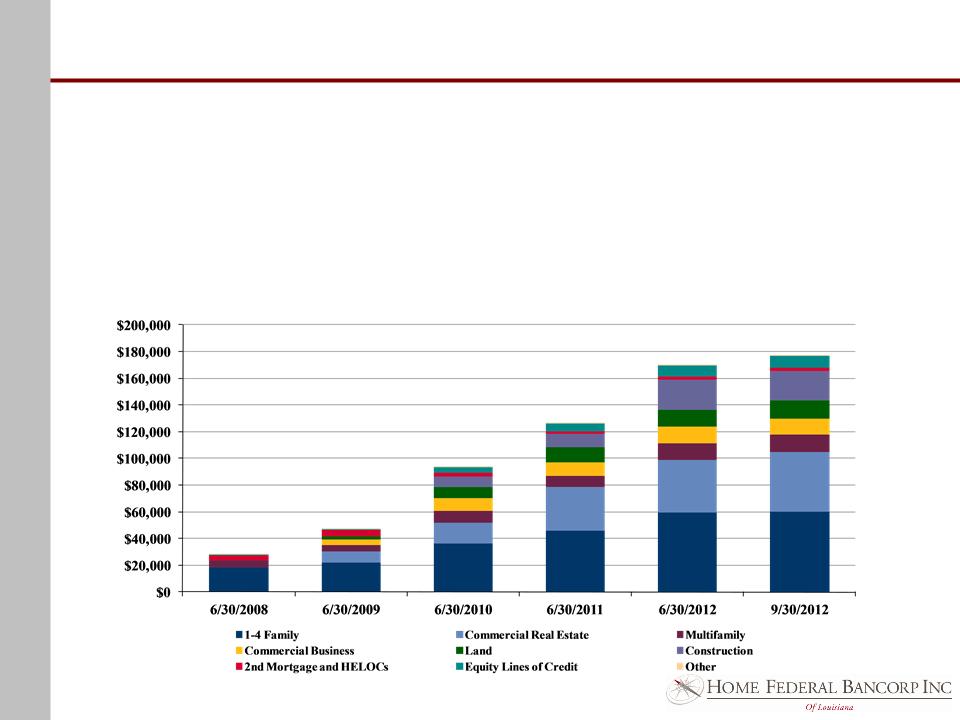

Continued Loan Growth

► Commercial lending initiatives have resulted in significant loan portfolio growth and diversification

► New commercial lending staff was able to rapidly generate quality loans through borrowers with which the lending staff

has strong historical relationships

has strong historical relationships

► 73% net loan growth since June 30, 2010

► Additional lenders have been added to the staff

► Substantially all loans originated in primary market of Shreveport and Bossier

► $9.2 million loans held for sale as of September 30, 2012 due to significant mortgage origination business

4

Dollars in thousands

Source: Company filings.

Note: Loan composition does not include loans held for sale.

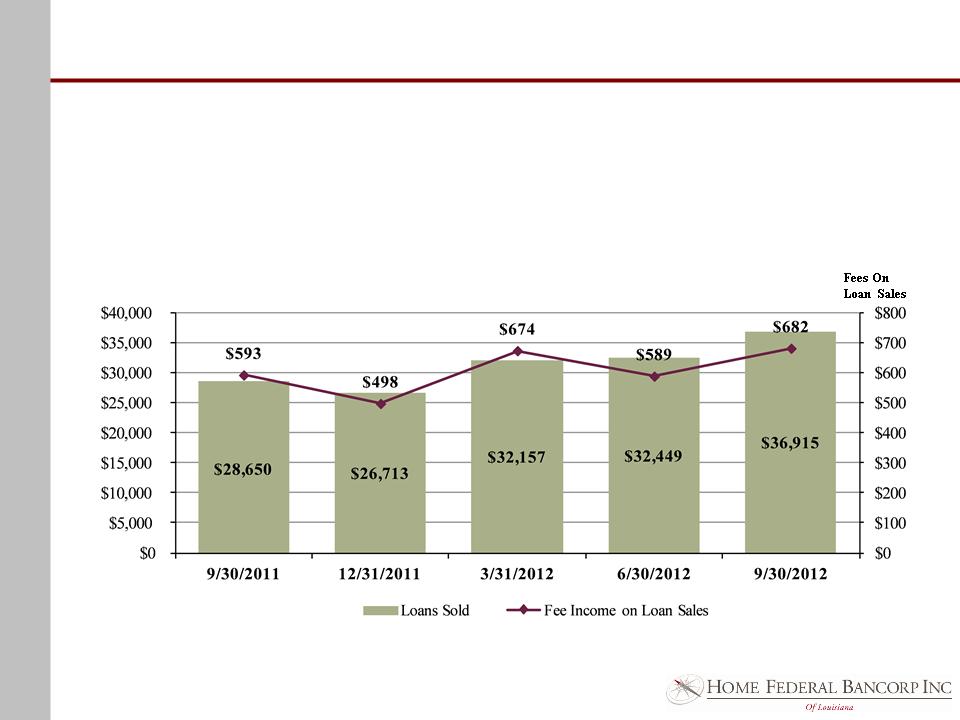

Mortgage Banking Growth

► Mortgage banking originations, loan sales, and gains on loan sales continue to be strong

► Sold $120.0 million 1-4 family residential loans, during the year ended June 30, 2012

► Sell most fixed rate owner occupied mortgage loan originations to manage interest rate risk

► Quarterly gain on loan sales of $682,000 for the three months ended September 30, 2012 is an all-time

high

high

5

Dollars in thousands

Loans Sold

Source: Company filings.

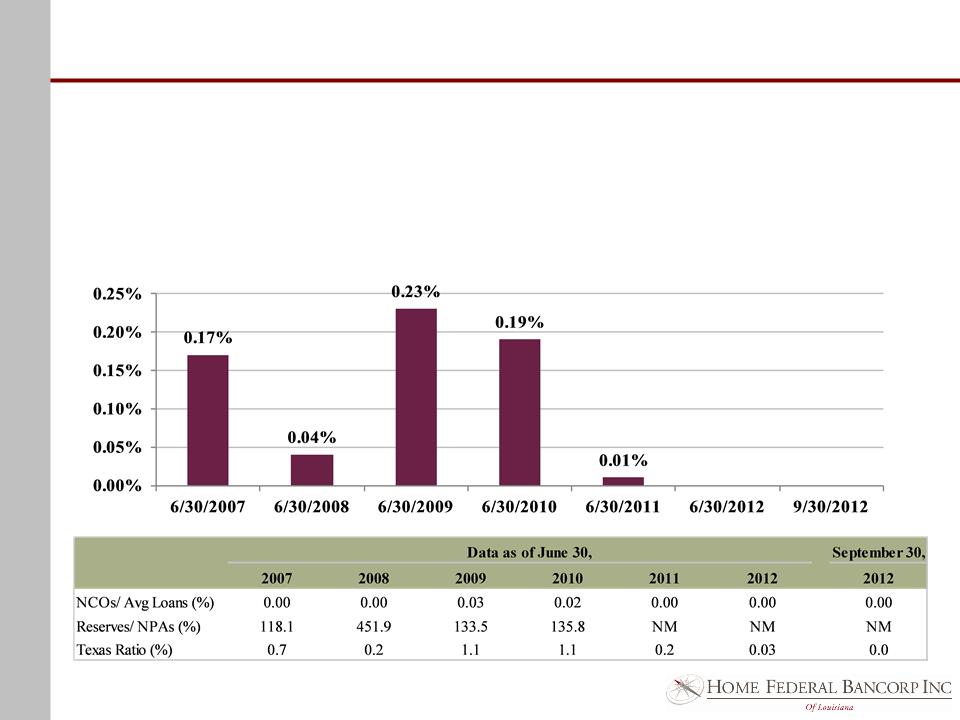

Strong Asset Quality

► Home Federal’s credit profile has fared significantly better than its peers

► As a result of Home Federal’s disciplined underwriting standards, there were no non-performing assets

at September 30, 2012

at September 30, 2012

► Since 2009 new commercial lending policies, procedures and systems have been established

► Third party commercial loan review conducted annually

► File review conducted monthly

Source: Company filings, SNL Financial.

Non-performing assets include TDRs and loans 90+ days past due.

Texas Ratio defined as (non-performing assets) / (tangible equity and loan loss reserve).

6

Non-Performing Assets / Total Assets

0.00%

0.00%

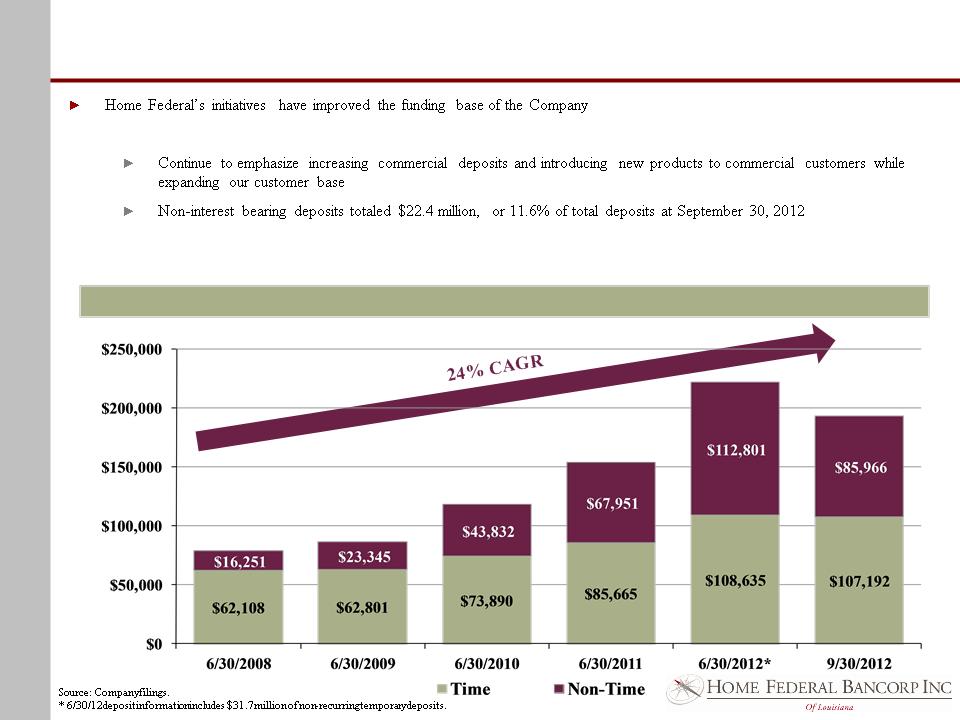

Deposit Base

► Total deposits have grown 147% since June 30, 2008

► Established relationship pricing at the bank level

► Deposits are comprised of local relationships

7

Deposit Growth

Dollars in thousands

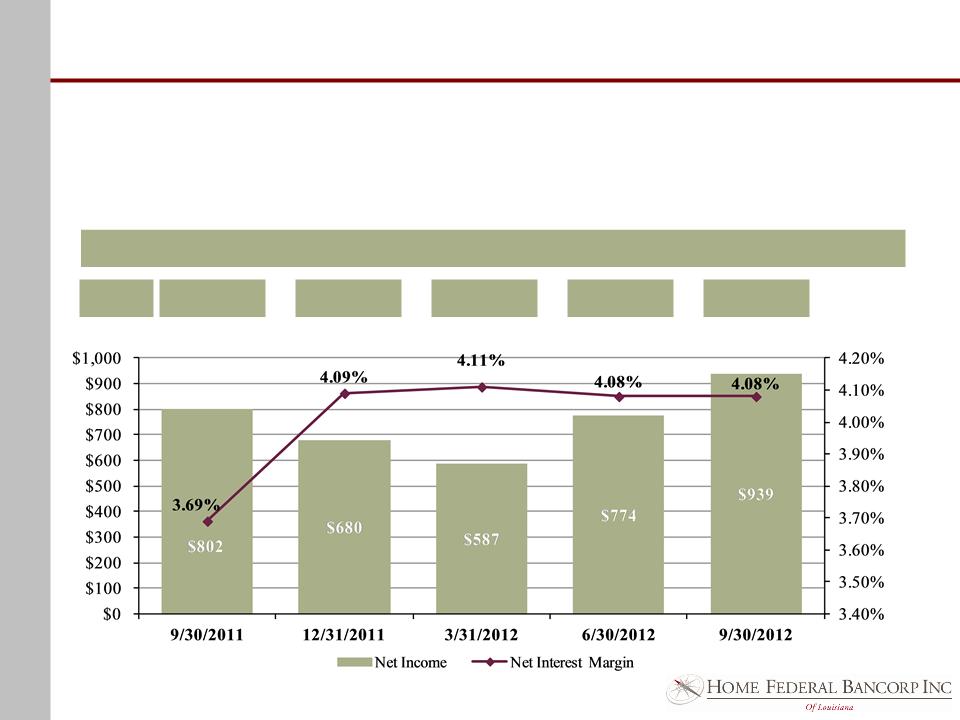

► As the loan and deposit mix has changed, net interest margin and earnings have improved

► Earnings should continue to benefit from increased commercial lending efforts

► Home Federal has experienced significant mortgage originations, which has provided meaningful non-interest

income

income

Strong, Consistent Financial Performance

8

Net Interest Margin Expansion & Quarterly Net Income

Dollars in thousands

$0.28

$0.23

$0.21

$0.28

$0.35

EPS*

Source: Company filings.

*Represents fully-diluted earnings per share.

9

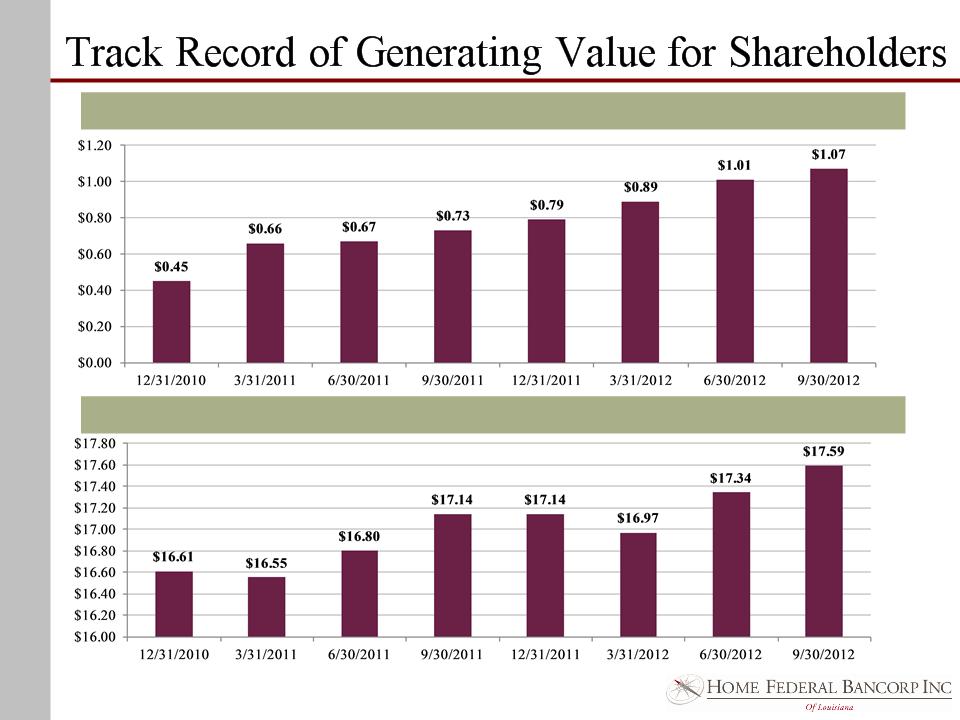

Trailing Twelve Months Earnings Per Share

Source: SNL Financial.

Tangible Book Value Per Share

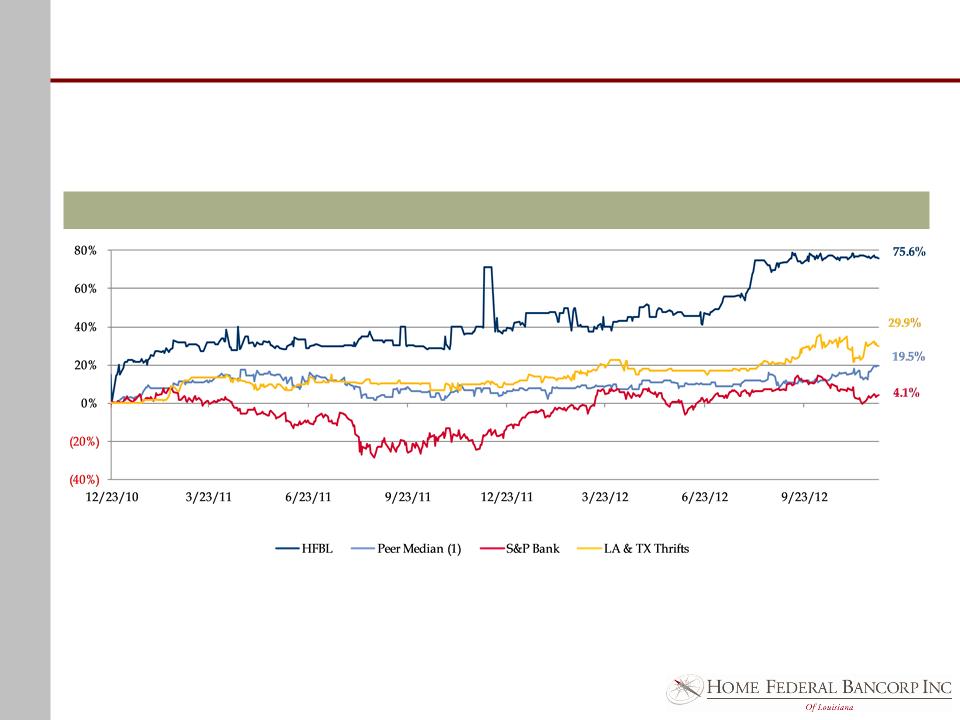

Stock Price Performance

10

► Home Federal Bancorp, Inc. of Louisiana stock has significantly outperformed peers,

Louisiana and Texas thrifts and the broad bank indices since its 2nd step transaction

Louisiana and Texas thrifts and the broad bank indices since its 2nd step transaction

Price Performance Since 12/23/10

Source: SNL Financial. Pricing data as of November 30, 2012.

Louisiana and Texas thrifts exclude MHCs and merger targets.

(1) Peers include nationwide thrifts with market capitalizations between $30 million and $50 million and assets less than $1 billion.

Concluding Thoughts

u Over the past several years we have strengthened our senior management

team, added seasoned commercial and residential lenders with strong

business ties within our primary market area.

team, added seasoned commercial and residential lenders with strong

business ties within our primary market area.

u We have also invested in new technologies which permit us to deliver state

of the art products and services to our customers.

of the art products and services to our customers.

u These investments, particularly our ability to attract and retain experienced

lenders, has permitted us to grow our bank profitably over the past several

years.

lenders, has permitted us to grow our bank profitably over the past several

years.

u We believe Home Federal is well positioned to continue to grow our assets,

deposits, customers and earnings over the next several years.

deposits, customers and earnings over the next several years.

11