Attached files

| file | filename |

|---|---|

| 8-K - ROSETTA RESOURCES INC 8-K 11-27-2012 - NBL Texas, LLC | form8k.htm |

Exhibit 99.1

REDEFINED

BUILDING VALUE IN UNCONVENTIONAL RESOURCES

Investor Presentation

NOVEMBER 2012

Forward-Looking Statements and Terminology Used

2

Forward-Looking Statements and Terminology Used (cont.)

3

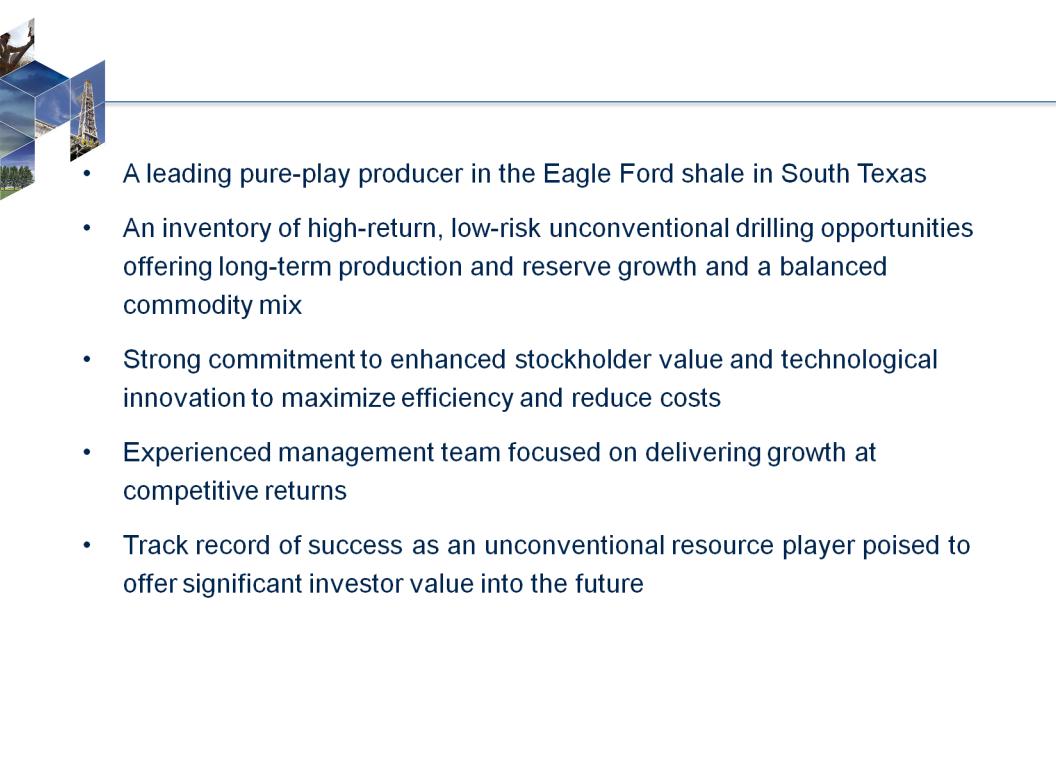

Company Profile

4

• Leverage high-graded asset base

• Strengthen position as a leading pure Eagle Ford shale player

• Develop and convert inventory of over 500 MMBoe with 15 years of drilling opportunities

• Expand production base with about 11% of inventory developed

• Successfully execute business plan

• Grow total production and liquids volumes

• Lower overall cost structure and improve margins

• Capture firm transportation and processing capacity

• Test future growth opportunities

• Evaluate previously untested Eagle Ford acreage

• Continue testing optimal Eagle Ford well spacing

• Pursue new growth targets through blend of acquisitions and new ventures

• Financial strength and flexibility

• Low leverage

• Sizable liquidity

• Active hedging program

Company Strategy

5

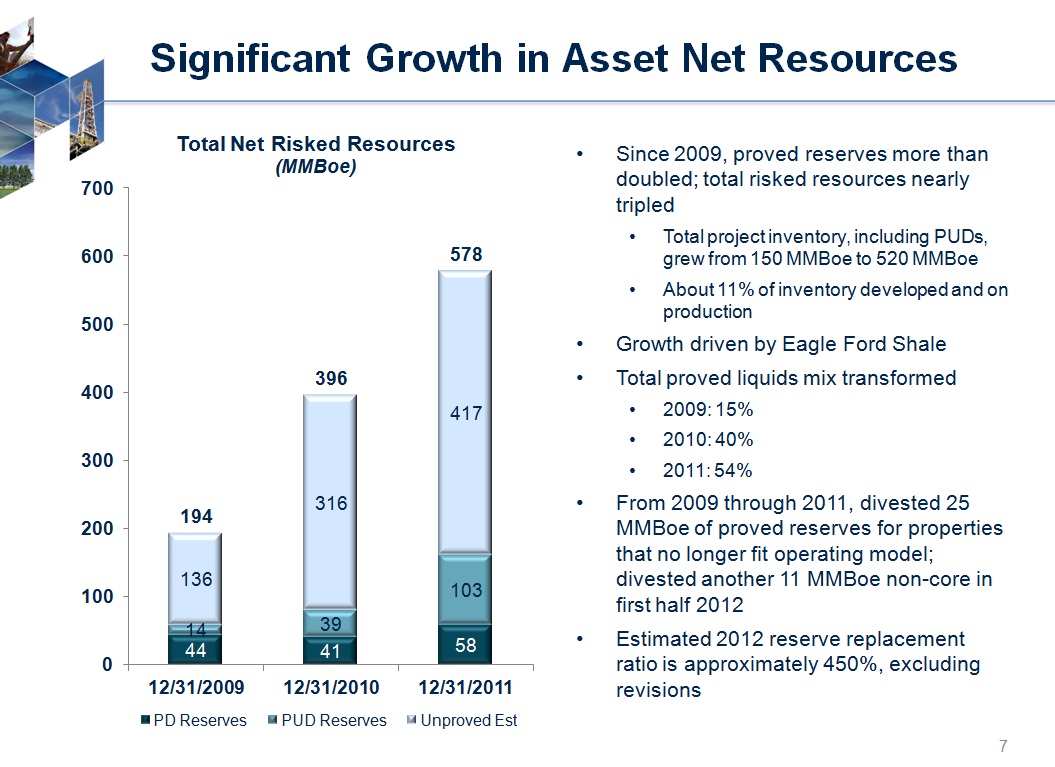

6

% Liquids: 14 19 24 29 33 46 51 49 52 59 60 64 62

% Oil: 5 7 10 12 15 18 19 22 22 24 30

8

Nov 7, 2012

Guidance

39 - 44

9

Includes capitalized interest and other corporate costs

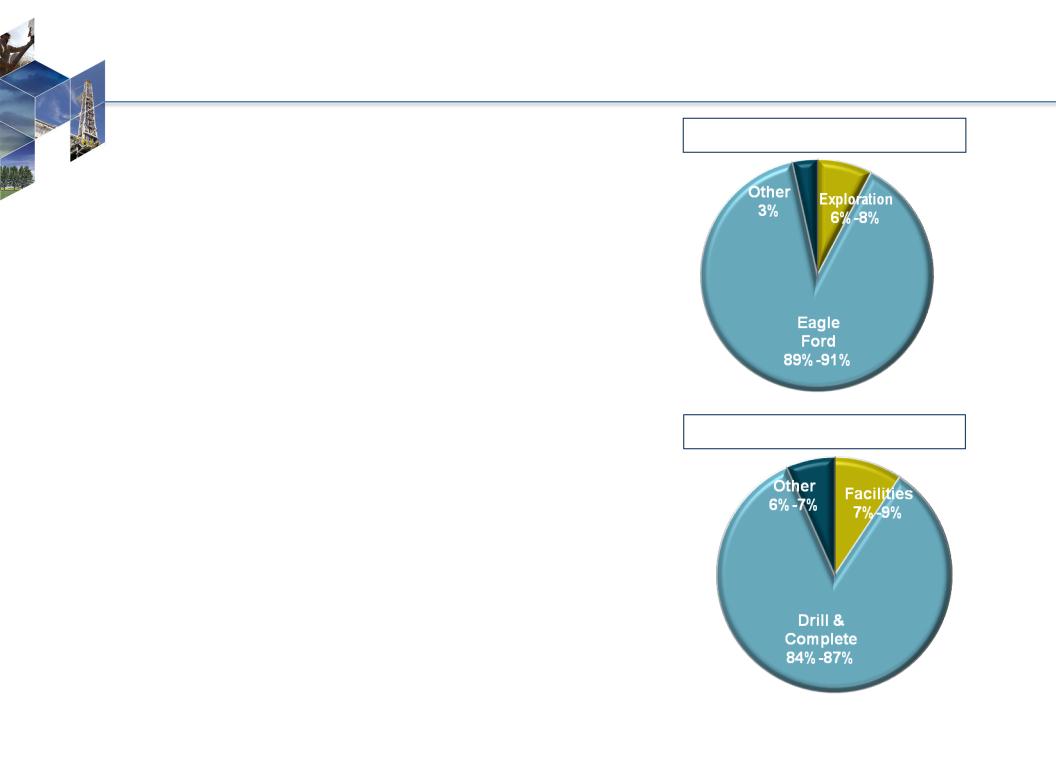

By Region

By Region

By Category

By Category

2012E Capital: $660-$680 Million

10

• Run four- to five-rig program in Eagle Ford area

• Approximately 60 completions for year

• 43 Eagle Ford completions thru September

• Estimate 15 to 20 Eagle Ford completions in 4Q

• Liquids-rich development

• Additional focus on Karnes Trough area and Briscoe

Ranch

Ranch

• Capital range dependent on timing of--

• Drilling two exploratory wells outside Eagle Ford

• Several land acquisitions

• Facilities construction for 2013 Eagle Ford expansion

• WI share of drilling 12 outside-operated Eagle Ford

wells in 4Q (Rosetta WI share approximately 7%)

wells in 4Q (Rosetta WI share approximately 7%)

• Fund base capital program from internally-

generated cash flow supplemented by borrowings

under current credit facility and divestitures

generated cash flow supplemented by borrowings

under current credit facility and divestitures

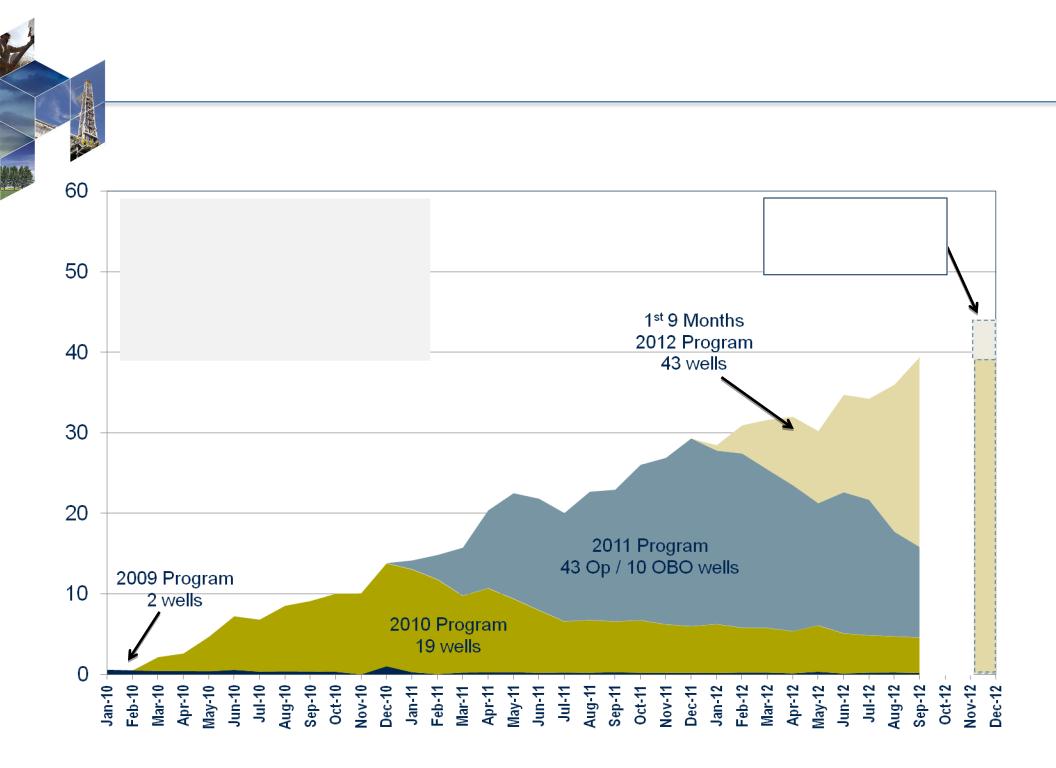

Eagle Ford Growth Profile

11

Eagle Ford production averaged

36.5 MBoe/d during 3Q 2012

36.5 MBoe/d during 3Q 2012

• 60.3% total liquids

• 29.8% oil / 30.5% NGLs

MBoe/d

Exit Rate Guidance

(As of 11/7/2012)

39 - 44 MBoe/d

Top 20 Eagle Ford Operators

% of Eagle Ford Shale Production

Gross Boe/d per Well

12

Top 20 Eagle Ford Operators include APC, BHP, CHK, COP, CRK, CRZO, EP, EOG, GeoSouthern, Lewis, MRO, MUR, PVA, PXD, PXP, ROSE, SFY, SM, TLM, XOM.

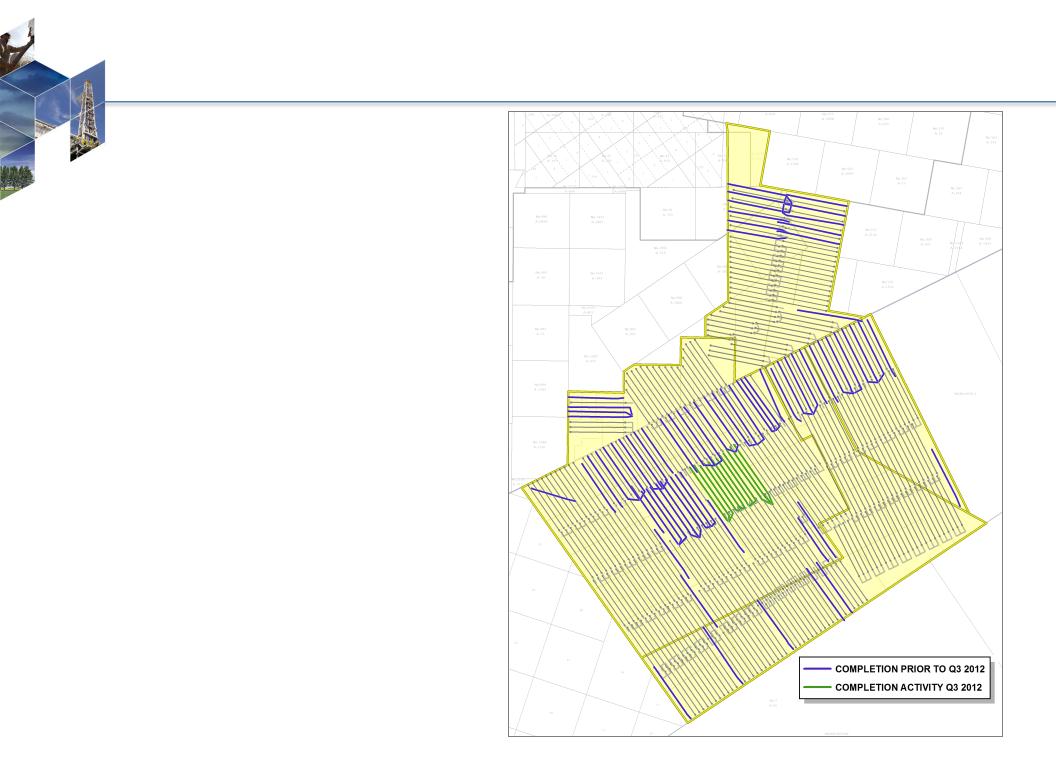

Gates Ranch

13

Summary

• 26,500 net acres in Webb County

• 84 completions as of 9/30/2012

• 1Q & 2Q 2012: 16 completions

• 3Q 2012: 12 completions

• 344 well locations remaining under current

55-acre spacing assumptions

55-acre spacing assumptions

Average Well Characteristics

• Well Costs: $7.5 - $8.0 million

• Spacing: 475 feet apart or 55 acres

• Composite EUR: 1.67 MMBoe

• F&D Costs: $4.65/Boe

• Condensate Yield = 64 Bbls/MMcf

• NGL Yield = 100 Bbls/MMcf

• Shrinkage = 20%

• Mix: Oil 23%, NGLs 32%

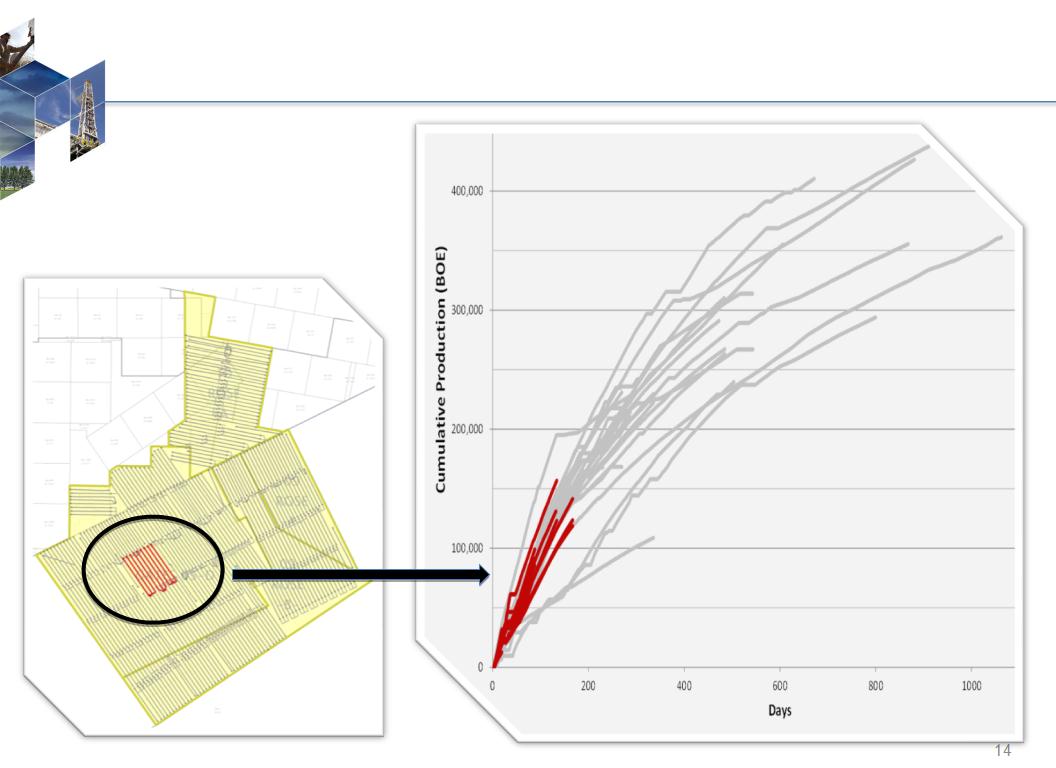

Well Performance on 55 acres

Wells spaced at 55 acres compared to similar offsetting wells spaced at 100 acres

Wells spaced at 55 acres compared to similar offsetting wells spaced at 100 acres

These 9 wells are our largest

continuous group of producing wells

that are spaced on 55 acres

continuous group of producing wells

that are spaced on 55 acres

These 9 wells are performing in line

with comparable offsetting wells

that were drilled and completed

early in the development of the area

and spaced on 100 acres …

with comparable offsetting wells

that were drilled and completed

early in the development of the area

and spaced on 100 acres …

Composite Type Curve - 1.7 MMBoe

(23% Oil / 32% NGLs)

South Type Curve - 1.9 MMBoe

North Type Curve - 1.4 MMBoe

Gates Ranch Well Performance - North and South Areas

15

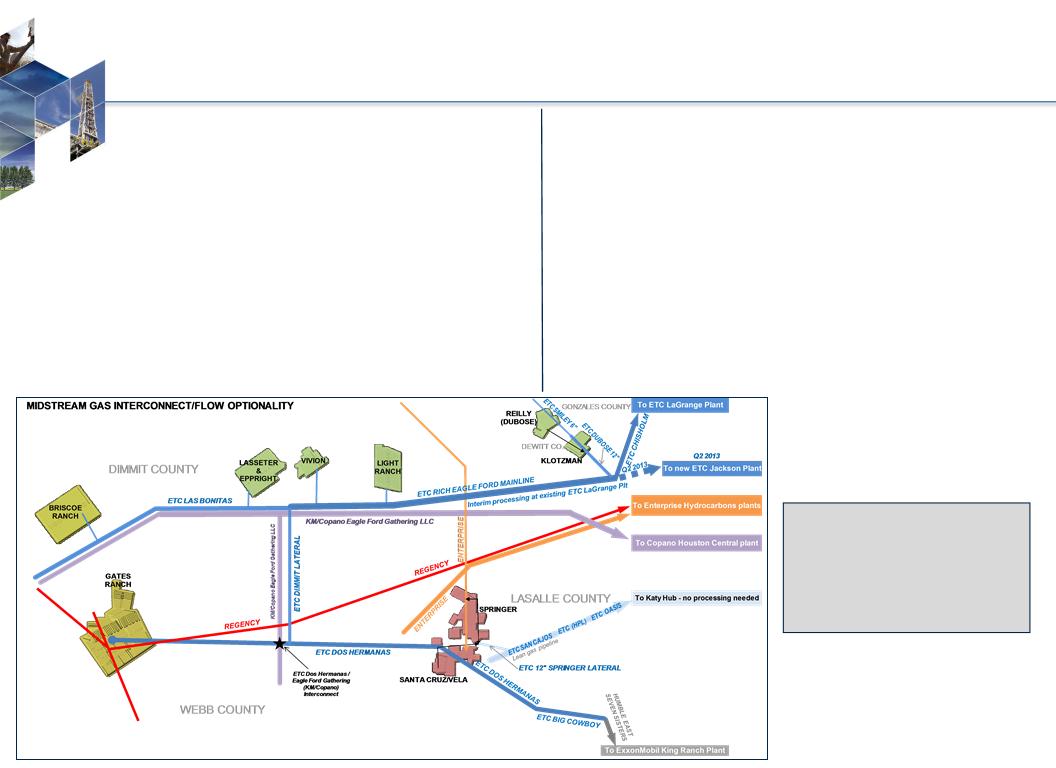

Eagle Ford Multiple Takeaway Options

16

Gas Transportation Capacity

Firm gross wellhead gas takeaway

• 195 MMcf/d today

• 245 MMcf/d in April 2013

Four processing options - Gathering (Plant)

• Regency (Enterprise Plants)

• Energy Transfer “ETC” Dos Hermanas (King Ranch)

• Eagle Ford Gathering (Copano Houston Central)

• ETC Rich Eagle Ford Mainline (LaGrange/Jackson)

Net 3-stream takeaway increases with higher

contribution of oil-weighted volumes

contribution of oil-weighted volumes

Oil Transportation Capacity

Gates Ranch, Briscoe Ranch and Central Dimmit Co.

• Plains Crude Gathering - Firm gathering capacity of

25,000 Bbls/d to Gardendale hub with up to 60,000 Bbls

storage; started operation in April 2012

25,000 Bbls/d to Gardendale hub with up to 60,000 Bbls

storage; started operation in April 2012

• Access to truck and rail loading and pipeline

connections

connections

Karnes Trough

• Rosetta-owned oil truck-loading facility began operation

in late July 2012

in late July 2012

• Trucking readily available

Pricing assumptions included in Appendix

Well-positioned to move

new production to

market with access to

multiple midstream

service providers

new production to

market with access to

multiple midstream

service providers

17

|

Area

|

Window

|

Net

Acreage |

|

Gates Ranch

|

Liquids

|

26,500

|

|

Non-Gates Ranch

|

Liquids

|

23,500

|

|

Encinal Area

|

Dry Gas

|

15,000

|

|

TOTAL

|

|

65,000

|

18

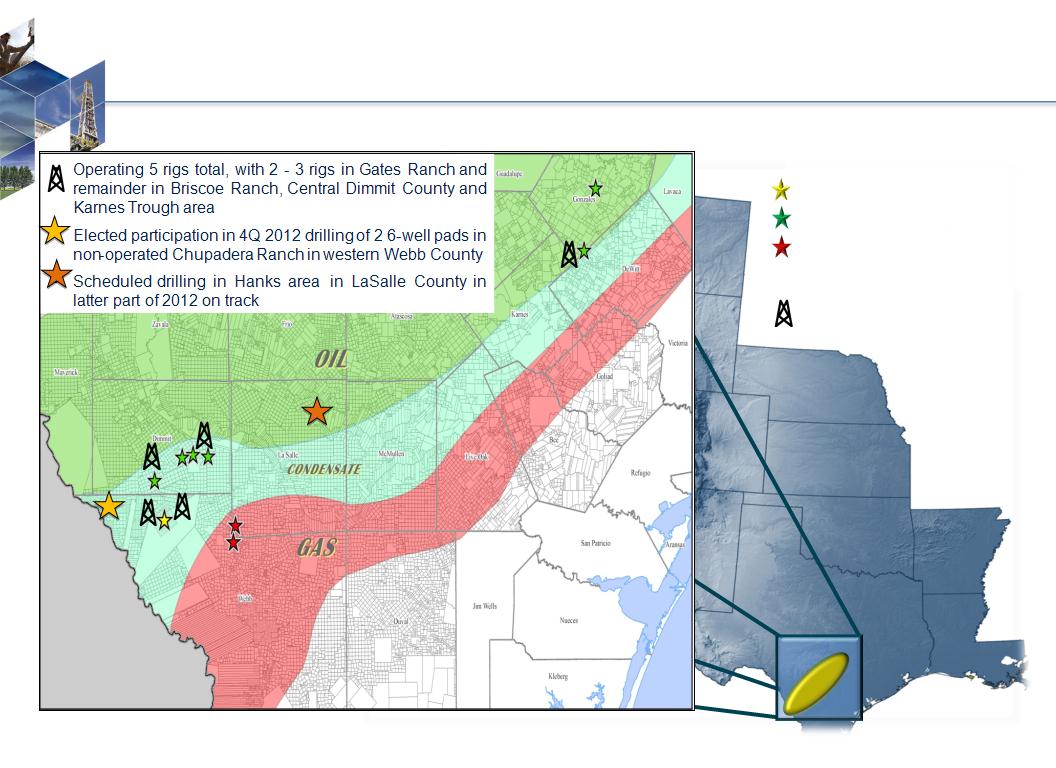

Eagle Ford Shale Activity

Current Drilling Activity Area

19

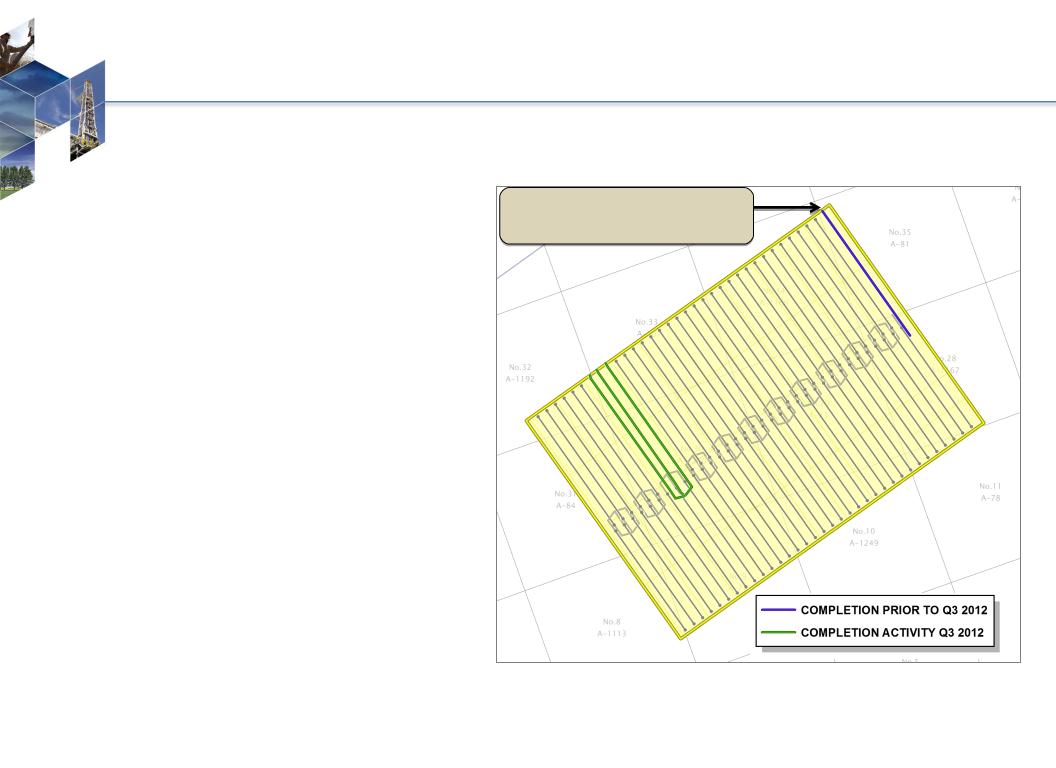

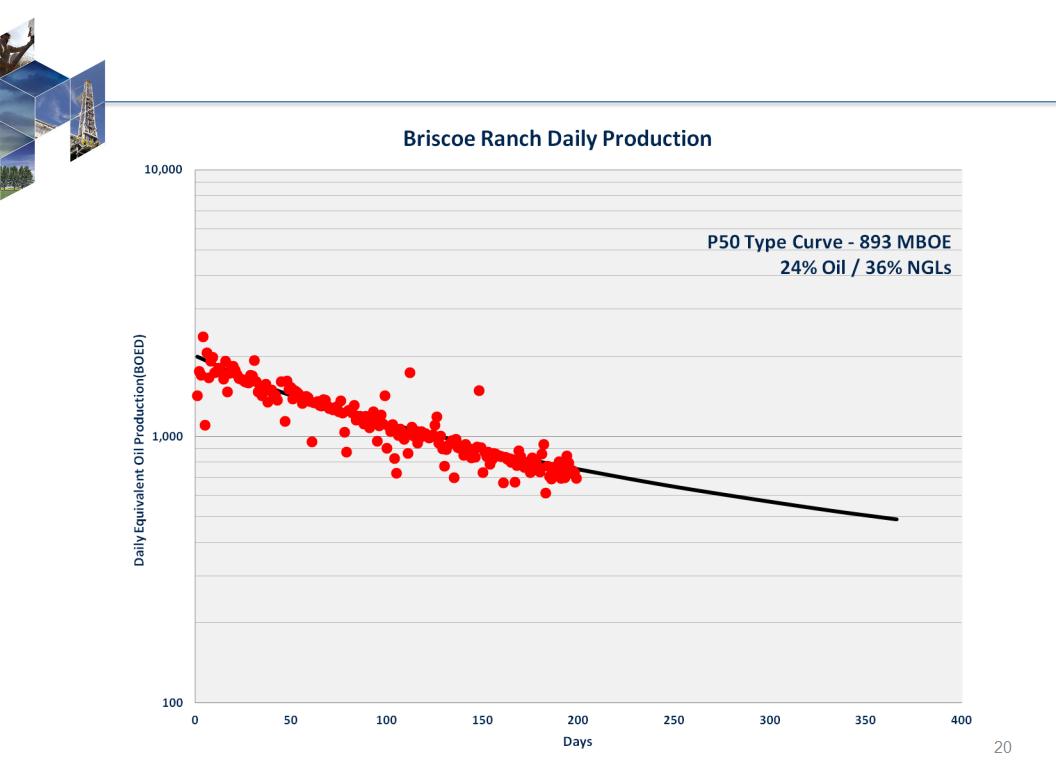

Briscoe Ranch

Summary

• 3,545 net acres in southern Dimmit

County

County

• 4 completions as of 9/30/2012

• 3Q 2012: 3 completions

• 64 well locations remaining

Average Well Characteristics

• Well Costs: $7.5 - $8.0 million

• Spacing: 425 feet apart or 50 acres

• Condensate Yield: 76 Bbls/MMcf

• NGL Yield: 121 Bbls/MMcf

• Shrinkage: 23%

Future Activity

• Planned full development activity will last

well into 2016

well into 2016

*Seven-day stabilized rate

Discovery Well Initial Rate* - 10/2011

1,990 Boe/d, 68% Liquids

(850 Bo/d, 490 B/d NGLs, 3,900 Mcf/d)

Briscoe Ranch Type Curve

21

Karnes Trough Area

SUMMARY

• 1,900 net acres; located in oil window

• 10 total completions as of 9/30/2012

• 1Q 2012: 2 completions

• 2Q 2012: 7 completions

• 12 well locations remaining

• Well Costs: $8.5 - $9.0 million

• Activity planned through 2013

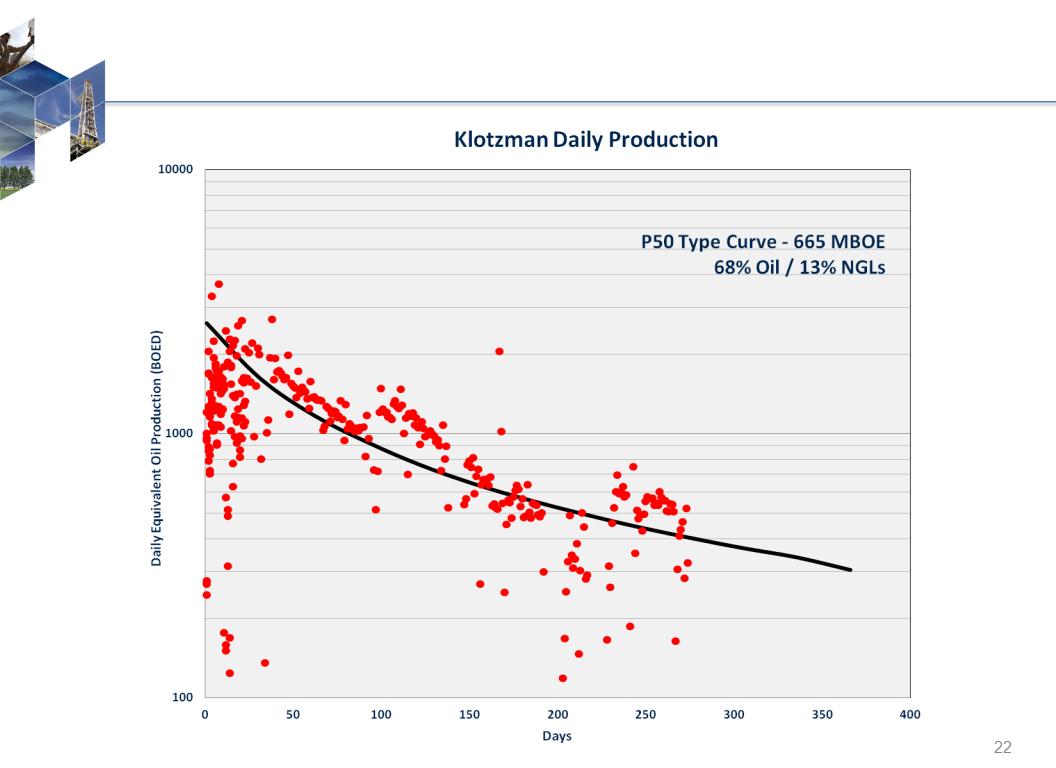

Klotzman (Dewitt County)

• 8 total completions as of 9/30/2012

• 1Q 2012: 1 completions

• 2Q 2012: 6 completions

• Rosetta-owned oil truck terminal started

operation in late July

operation in late July

Reilly (Gonzales County)

• 2 completions as of 9/30/2012

• 1Q 2012: 1 completion

• 2Q 2012: 1 completion

*Seven-day stabilized rate

Klotzman 1H

Discovery Well Initial Rate* - 11/2011

3,033 Boe/d, 81% Oil

(2,450 Bo/d, 250 B/d NGLs, 2,000 Mcf/d)

Adele Dubose 1H

Delineation Well Initial Rate* - 2/2012

1,463 Boe/d, 76% Oil

(1,109 Bo/d, 153 B/d NGLs, 1,200 Mcf/d)

Klotzman Type Curve

23

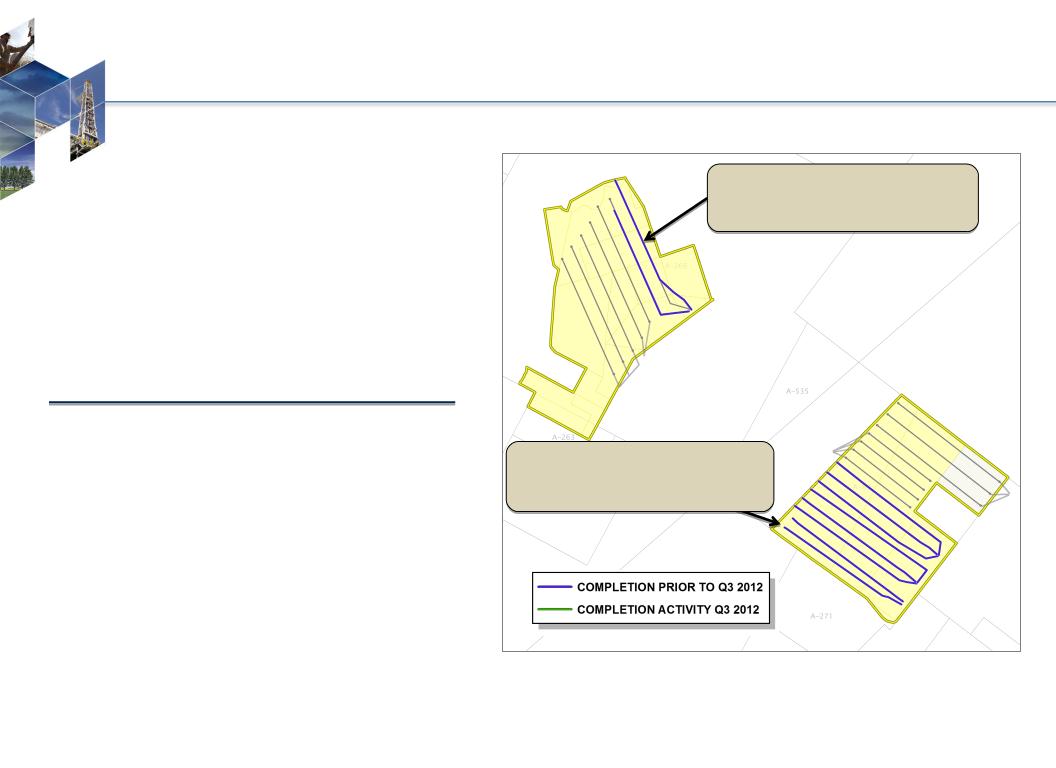

Central Dimmit County Area

Summary

• 8,100 net acres in Dimmit County

• 5 completions as of 9/30/2012

• 2Q 2012: 2 completions

• 3Q 2012: 1 completion

• 122 well locations remaining

• Well Costs: $7.5 - $8.0 million

Light Ranch

• 3 total completions as of 9/30/2012

• 2Q 2012: 2 completions

Vivion

• 1 completion as of 9/30/2012

Lasseter & Eppright

• 1 completion as of 9/30/2012

• 3Q 2012: 1 completion (discovery)

*Seven-day stabilized rate

Light Ranch 1H

Discovery Well Initial Rate* - 10/2010

987 Boe/d, 78% Liquids

(510 Bo/d, 260 B/d NGLs, 1,300 Mcf/d)

Vivion 1H

Discovery Well Initial Rate* - 9/2011

680 Boe/d, 89% Liquids

(506 Bo/d, 102 B/d NGLs, 436 Mcf/d)

Lasseter & Eppright 1

Discovery Well Initial Rate* - 9/2012

1,228 Boe/d, 76% Liquids

(667 Bo/d, 262 B/d NGLs, 1,792 Mcf/d)

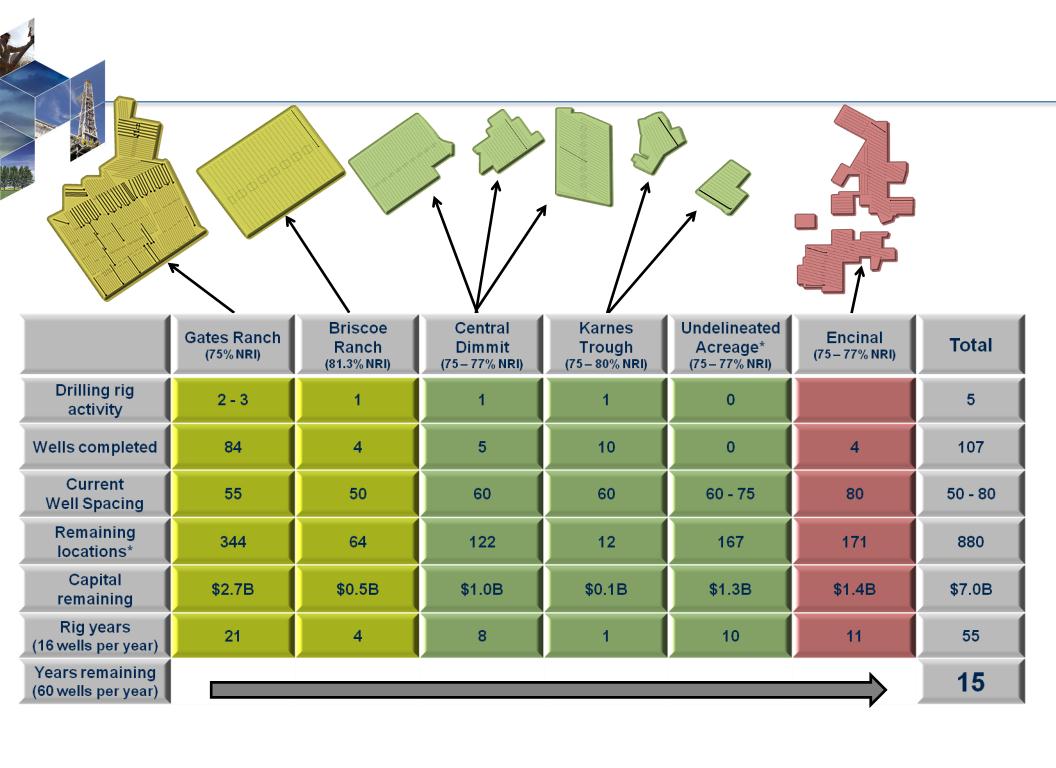

Eagle Ford Inventory

+/- 880 net wells remaining as of 9/30/2012

+/- 880 net wells remaining as of 9/30/2012

* Denotes roughly 10,000 net acres in the liquids window of the play in Webb (~3,000), LaSalle (~3,500), and Gonzales (~3,000) counties.

24

25

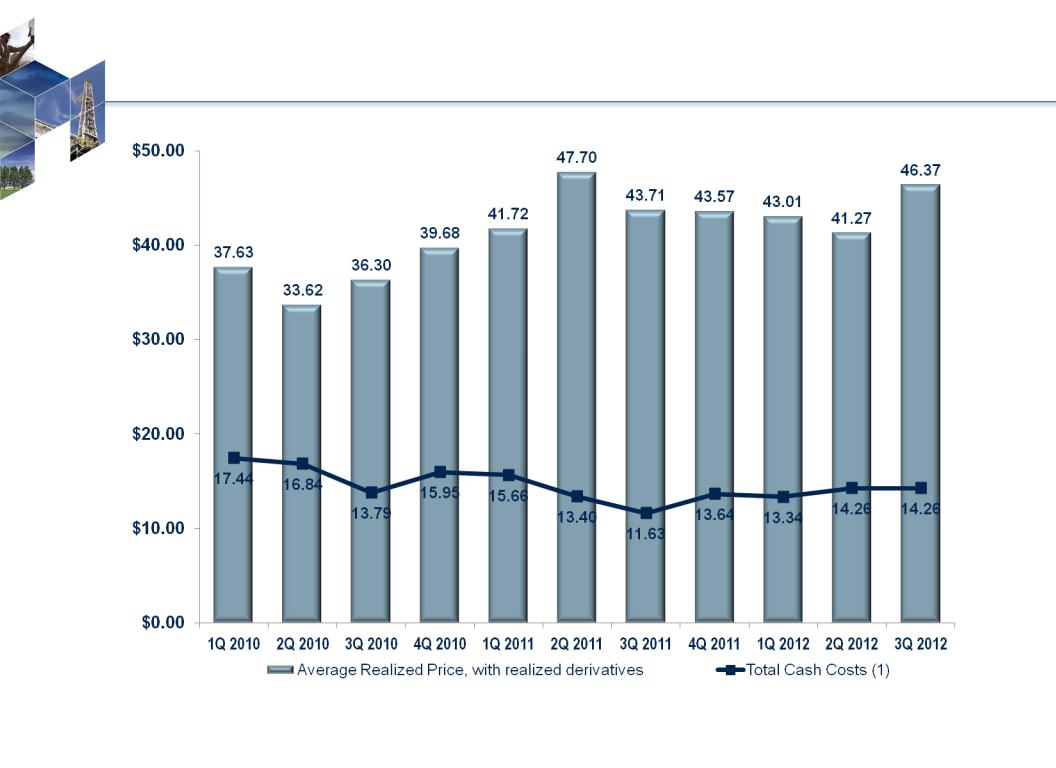

Margin Expansion

26

1. Total cash costs (a non-GAAP measure) is calculated as the sum of all average costs per Boe, excluding DD&A and stock-based compensation. Management believes this

presentation may be helpful to investors as it represents average cash costs incurred by our oil, NGL and natural gas producing activities. This measure is not intended to

replace GAAP statistics but rather to provide additional information that may be helpful in evaluating trends and performance.

presentation may be helpful to investors as it represents average cash costs incurred by our oil, NGL and natural gas producing activities. This measure is not intended to

replace GAAP statistics but rather to provide additional information that may be helpful in evaluating trends and performance.

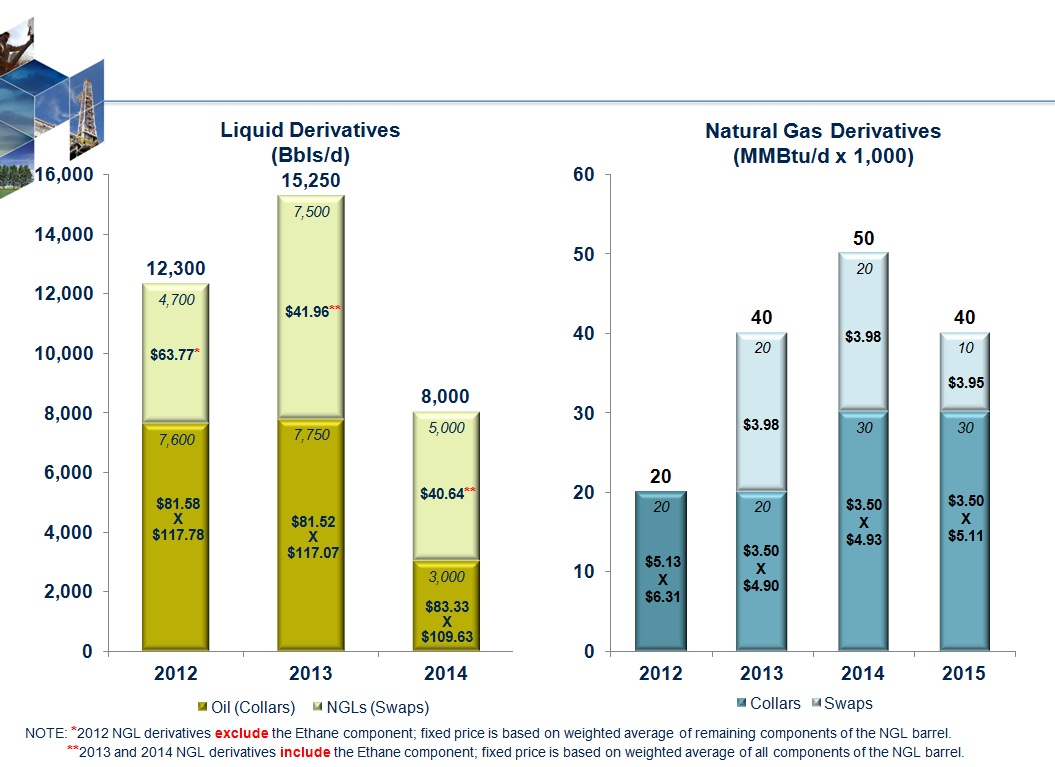

Commodity Derivatives Position - November 7, 2012

27

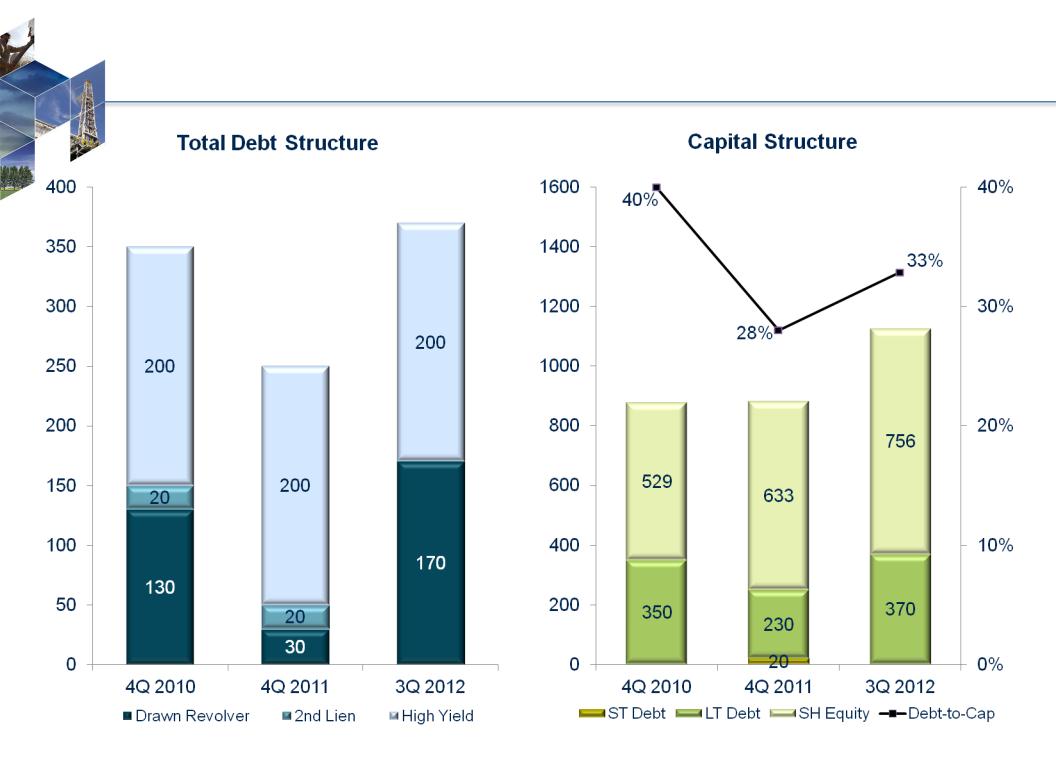

Debt and Capital Structure

350

250

883

879

28

370

1,126

Note: As of November 7, 2012, total debt is $370 million.

($MM)

($MM)

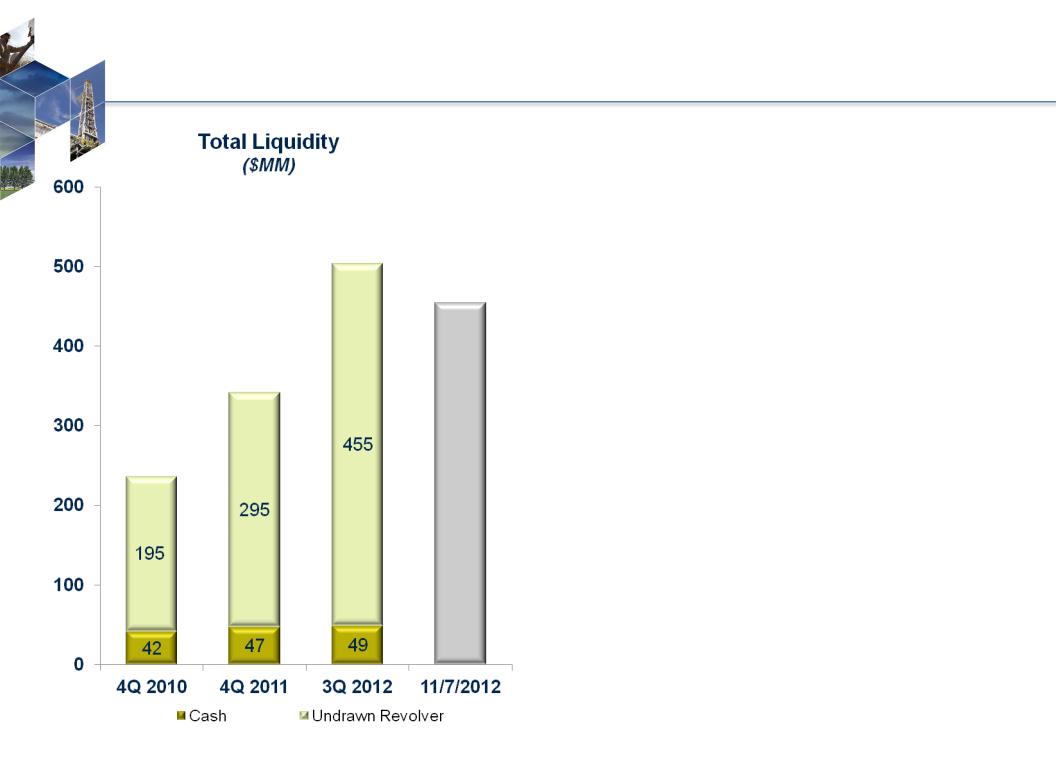

Adequate liquidity available to fund 2012

$660 - $680 million capital program

$660 - $680 million capital program

• Borrowing base raised in April, 2012

based on performance

based on performance

• $455 million of $625 million borrowing

base available as of November 7th

base available as of November 7th

• Lobo and Olmos divestiture ($90 million,

net proceeds collected as of September

30th)

net proceeds collected as of September

30th)

Liquidity

29

342

237

504

475

Asset Base High-Graded

• Focused on liquids-rich targets in Eagle Ford with significant project inventory

• Completed divestiture program; redeployed proceeds

Executing Business Plan

• Doubled proved reserves since 12/31/2010

• Increased Gates Ranch recoveries

• Sufficient firm take-away capacity

• Projected strong 2012 growth and exit rates

Testing Growth Opportunities

• Increased Gates Ranch well density

• Three discoveries in other Eagle Ford areas

• Pursue new growth targets through blend of acquisitions and new ventures

Financial Strength and Flexibility

• Debt-to-capitalization ratio at 33%

• Approximately $475 million in liquidity as of early November 2012

Summary

30

APPENDIX

31

|

|

|

2012 4th Quarter

|

|||

|

|

|

|

|||

|

$/BOE

|

|

|

|

|

|

|

Direct Lease Operating Expense

|

|

$ 2.40

|

-

|

$ 2.50

|

|

|

Insurance

|

|

0.05

|

-

|

0.06

|

|

|

Ad Valorem Tax

|

|

0.33

|

-

|

0.35

|

|

|

Treating and Transportation

|

|

4.00

|

-

|

4.10

|

|

|

Production Taxes

|

|

1.52

|

-

|

1.60

|

|

|

DD&A

|

|

11.50

|

-

|

12.05

|

|

|

G&A, excluding Stock-Based Compensation

|

|

3.35

|

-

|

3.50

|

|

|

Interest Expense

|

|

1.55

|

-

|

1.65

|

|

32

Fourth Quarter Expense Guidance

As of November 7, 2012

As of November 7, 2012

• Volumes and Product Mix

• Exit Rate 39 - 44 MBoe/d; 62 % total liquids

• 3Q 2012: 37.1 MBoe/d with 36.5 MBoe/d from Eagle Ford (Oil 30%, NGLs 30%)

• Averaged 41 MBoe/d in October 2012

• Treating & Transportation fees impacted by mix changes

• Crude Oil Pricing

• Should approximate WTI

• NGL pricing (Mount Belvieu Benchmark)

• Firm fractionation capacity

• Adjust for fractionation fees approximately $3 to $4 per barrel

• Adjust for reported 2012 derivative activity, excluding ethane

• Pricing estimates based on % of WTI not as correlative

4th Qtr Guidance - Framing For Quarterly Models

33

|

|

1st 9

Months 2012 |

2011

|

2010

|

|

Daily rate (MBoe/d)

|

34.8

|

27.6

|

22.9

|

|

Oil% / NGLs%

|

25% / 32%

|

18% / 26%

|

9% / 13%

|

|

|

$/Boe

|

$/Boe

|

$/Boe

|

|

Average realized price (without realized derivatives)

|

$41.89

|

$42.45

|

$32.98

|

|

Average realized price (with realized derivatives)

|

$43.66

|

$44.18

|

$36.85

|

|

Direct lease operating expense

|

$2.39

|

$2.72

|

$4.52

|

|

Workovers / Insurance / Ad valorem tax

|

0.70

|

0.75

|

1.58

|

|

Lease operating expense

|

$3.09

|

$3.47

|

$6.10

|

|

Treating and transportation

|

3.92

|

2.22

|

0.83

|

|

Production taxes

|

1.21

|

1.20

|

0.71

|

|

General and administrative costs¹

|

3.82

|

4.59

|

5.04

|

|

Interest expense

|

1.92

|

2.11

|

3.23

|

|

Total cash costs2

|

$13.96

|

$13.59

|

$15.91

|

|

Cash Margin2 (without realized derivatives)

|

$27.93

|

$28.86

|

$17.07

|

|

Cash Margin2 (with realized derivatives)

|

$29.70

|

$30.59

|

$20.94

|

Margin Improvement

34

1. Excludes stock-based compensation expense

2. Total cash costs (a non-GAAP measure) is calculated as the sum of all average costs per Boe, excluding DD&A and stock-based compensation. Cash Margin (a non-GAAP measure) is

calculated as the difference between average realized equivalent price and total cash costs. Management believes this presentation may be helpful to investors as it represents average

cash costs incurred by our oil, NGL and natural gas producing activities as compared to average realized price based on revenue generated. These measures are not intended to replace

GAAP statistics but rather to provide additional information that may be helpful in evaluating trends and performance.

calculated as the difference between average realized equivalent price and total cash costs. Management believes this presentation may be helpful to investors as it represents average

cash costs incurred by our oil, NGL and natural gas producing activities as compared to average realized price based on revenue generated. These measures are not intended to replace

GAAP statistics but rather to provide additional information that may be helpful in evaluating trends and performance.

REDEFINED

BUILDING VALUE IN UNCONVENTIONAL RESOURCES