Attached files

| file | filename |

|---|---|

| 8-K - 8-K - OGLETHORPE POWER CORP | a2211941z8-k.htm |

Exhibit 99.1

|

|

Third Quarter 2012 Investor Briefing November 26, 2012 |

|

|

Participants Tom Smith President and Chief Executive Officer Mike Price Executive Vice President and Chief Operating Officer Betsy Higgins Executive Vice President and Chief Financial Officer |

|

|

3 Notice to Recipients Risk Factors and Forward Looking Statements Certain of the statements made by representatives of Oglethorpe Power Corporation (An Electric Membership Corporation) (“Oglethorpe”) during the course of this presentation that are not historical facts are forward-looking statements. Although Oglethorpe believes that the assumptions underlying these statements are reasonable, you are cautioned that such forward-looking statements are inherently uncertain and involve necessary risks that may affect Oglethorpe’s business prospects and performance, causing actual results to differ from those discussed during this presentation. When considering forward-looking statements, you should keep in mind risk factors and other cautionary statements included in Oglethorpe’s SEC filings. Any forward-looking statements made are subject to all the risks and uncertainties, many of which are beyond management’s control, as described in Oglethorpe’s SEC filings. Should one or more of these risks or uncertainties occur, or should underlying assumptions prove incorrect, Oglethorpe’s actual results and plans could differ materially from those expressed in any forward-looking statements. Oglethorpe undertakes no obligation to publicly update any forward-looking statements, whether as a result of new information or future events. This electronic presentation is provided as of November 26, 2012. If you are viewing this presentation after that date, there may have been events that occurred subsequent to such date that would have a material adverse effect on the information that was presented, and Oglethorpe has not undertaken any obligation to update this electronic presentation. |

|

|

4 Overview of Oglethorpe Power Corporation Business Members Ratings Not-for-profit Georgia electric membership corporation. One of the largest electric cooperatives in the United States. Owns or leases approximately 7,075 MW of generation capacity. Operates or schedules another 1,287 MW on behalf of the Members. 2012 new system peak of 9,351 MW. Wholesale electric power provider for 39 distribution cooperatives in Georgia (the “Members”). Take or pay, joint and several Wholesale Power Contracts through December 2050. Allows for recovery of all costs, including debt service. Senior Secured Ratings: Baa1 / A / A (all stable) Short-term Ratings: P-2 / A-1 / F1 Financial 2011 revenues of approximately $1.4 billion. Total assets of approximately $8.2 billion. |

|

|

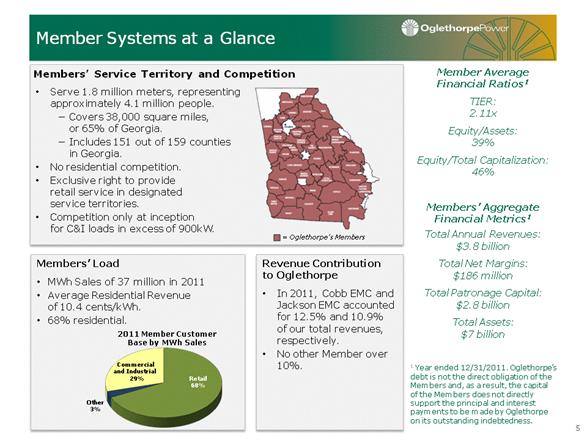

Members’ Load MWh Sales of 37 million in 2011 Average Residential Revenue of 10.4 cents/kWh. 68% residential. Serve 1.8 million meters, representing approximately 4.1 million people. Covers 38,000 square miles, or 65% of Georgia. Includes 151 out of 159 counties in Georgia. No residential competition. Exclusive right to provide retail service in designated service territories. Competition only at inception for C&I loads in excess of 900kW. 5 Member Systems at a Glance = Oglethorpe’s Members Members’ Service Territory and Competition Member Average Financial Ratios1 TIER: 2.11x Equity/Assets: 39% Equity/Total Capitalization: 46% Members’ Aggregate Financial Metrics1 Total Annual Revenues: $3.8 billion Total Net Margins: $186 million Total Patronage Capital: $2.8 billion Total Assets: $7 billion 1 Year ended 12/31/2011. Oglethorpe’s debt is not the direct obligation of the Members and, as a result, the capital of the Members does not directly support the principal and interest payments to be made by Oglethorpe on its outstanding indebtedness. 2011 Member Customer Base by MWh Sales Commercial and Industrial 29% Retail 68% Other 3% Revenue Contribution to Oglethorpe In 2011, Cobb EMC and Jackson EMC accounted for 12.5% and 10.9% of our total revenues, respectively. No other Member over 10%. |

|

|

2012 Capacity and Energy (a) Includes Oglethorpe and Smarr EMC resources. Capacity reflects planning capacity. Member Sales Member & Non-Member Sales Energy(a) 12 Months Ending 9/30/2012 6 Rocky Mountain Pumped Storage Hydro Sewell Creek Energy Facility Chattahoochee Energy Facility Hawk Road Energy Facility Plant Wansley Talbot Energy Facility Hartwell Energy Facility Plant Vogtle Plant Hatch Doyle Generating Plant Smarr Energy Facilitiy Plant Scherer Thomas A. Smith Energy Facility 2012 Capacity(a) Gas Nuclear Coal Hydro |

|

|

Oglethorpe’s Generation and Power Supply Resources (a) These capacity amounts are the amounts used for 2012 summer reserve planning purposes. (b) Each of the Members, other than Flint, has designated Oglethorpe to schedule its energy allocation from SEPA. The Members’ total allocation is 618 MW, of which Oglethorpe schedules 562 MW. 7 Resource Fuel Type Oglethorpe Ownership Share Operator Summer Planning Reserve Capacity (MW) (a) 2011 Average Capacity Factor License Expiration (if applicable) Oglethorpe Owned/Leased: Plant Hatch 2 Nuclear 30% Southern Nuclear 527 88% 2034 & 2038 Plant Vogtle 2 Nuclear 30% Southern Nuclear 689 93% 2047 & 2049 Plant Scherer 2 Coal 60% Georgia Power 1,010 65% - Plant Wansley 2 Coal 30% Georgia Power 523 52% - Chattahoochee Energy Facility - CC 1 Gas 100% Siemens 470 46% - Thomas A. Smith Energy Facility - CC 2 Gas 100% Oglethorpe 1,250 28% - Doyle I, LLC Generating Plant - CTs 5 Gas 100% Doyle I, LLC 348 5% - Hawk Road Energy Facility - CTs 3 Gas 100% Oglethorpe 486 0.5% - Hartwell Energy Facility - CTs 2 Gas/Oil 100% Oglethorpe 298 8% - Talbot Energy Facility - CTs 6 Gas/Oil 100% Oglethorpe 656 5% - Rocky Mountain Pumped Storage Hydro 3 Hydro 74.61% Oglethorpe 817 15% 2027 Subtotal 30 7,074 Member Owned/Oglethorpe Operated: Smarr / Sewell Creek - CTs 6 Gas/Oil - Oglethorpe 725 2% - Member Contracted/Oglethorpe Scheduled: Southeastern Power Administration (SEPA) (b) - Hydro - 562 - - Grand Total 36 8,361 # Units |

|

|

Operations Highlights Mike Price Executive Vice President and Chief Operating Officer |

|

|

9 Historical Load Member Demand Requirements Member Energy Requirements (MW) Percent Change (Million MWh) Percent Change 6.1% 0.8% 10.4% 3.9% 2.8% -0.3% -3.7% -5.3% Note: The data is at the Members’ delivery points (net of system losses). While Flint EMC was not a Member from 2006 through 2009, Flint EMC data is included in all years. Highest Summer Peak (2012) = 9351 MW Highest Winter Peak (2010) = 8462 MW -2.0% 9.1% 0.1% -5.4% Days ≥ 90° Days ≥ 95° Days ≥ 100° 50 24 9 39 4 38 4 84 19 53 13 3.9% 3.7% (Forecasted) 27 11 3 |

|

|

New AP1000 units will be adjacent to existing two units at Vogtle site. Experienced developer and operator, Southern Nuclear. Favorable EPC contract with experienced contractors, Westinghouse and Stone & Webster (Contractor) which includes parent guarantees. 30% share or 660 MW of 2,200 MW total capacity from additional units. Georgia Power, MEAG and City of Dalton are other co-owners. Oglethorpe’s share is fully subscribed by its Members. $4.2 billion estimated total cost to Oglethorpe (including AFUDC). 10 Vogtle Units 3 & 4 Project Highlights Conceptual Drawing of Vogtle Units 3 & 4 Georgia Power 45.7% Oglethorpe Power 30.0% MEAG 22.7% Dalton Utilities 1.6% |

|

|

11 Vogtle Units 3 & 4 Capital Expenditures $1.5 billion spent through 9/30/2012 Actuals Forecasts 2005 2017 2016 2015 2014 2013 2012 2011 2010 2009 2006 2007 2008 MAY 2005 Development Agreement MAR 2008 Filed Combined Construction Operating License (COL) with NRC DEC 2011 DCD Final Rule Effective APR 2006 Definitive Agreements MAY 2010 Signed DOE Conditional Term Sheet 2017 Unit 4 in Service AUG 2006 Filed Early Site Permit (ESP) with NRC AUG 2009 NRC Issuance of ESP/LWA 2016 Unit 3 in Service AUG 2011 NRC Staff Completed Work on FSER for both AP1000 DCD and COL FEB 2012 COLs Issued Early 2013 Projected Start of DOE Funding |

|

|

Budget Based on August 2012 project budget, the Oglethorpe budget projection for Vogtle Units 3 and 4 remains $4.2 billion. Schedule The current project schedule is based on November 2016 and 2017 commercial operation dates (CODs) for the units. Co-owners are evaluating whether maintaining scheduled CODs of 2016 and 2017 is in the best interest of their members/customers. Recent Claims The EPC contract provides for both informal and formal dispute resolution procedures. Currently the co-owners and the Contractors are involved in litigation with respect to two claims that were not resolved through the formal dispute resolution process: One claim relates to the responsibility for backfill costs. Another claim relates to costs resulting from certain design changes and design certification/license issuance delay. Budget, Schedule and Recent Claims 12 |

|

|

Received Unit 4 condenser Completed fabrication of Unit 3 reactor vessel Completed Unit 3 turbine building foundation Completed fabrication of Unit 3 containment vessel bottom head Completed fabrication of module CR10 (cradle for containment vessel) Completed Unit 3 cooling tower foundation and ring beam Performed nuclear island basemat test pour Construction Progress Unit 4 Condenser Delivery Unit 3 Turbine Island 13 |

|

|

14 Nuclear Island Basemat Test Pour |

|

|

15 Containment Vessel |

|

|

16 Upcoming Construction Unit 3 rebar, embeds, basemat concrete Dec 2012 Receive reactor vessel Dec 2012 Set CR10 (cradle for containment vessel) Q1 2013 Ship & receive turbine generator, accumulator tanks, heat exchanger, core make-up tanks, reactor coolant piping Q1 2013 Set Containment vessel bottom head (Unit 3) Q2 2013 Ship & receive steam generators, pressurizer, spent fuel storage racks Q2 2013 |

|

|

Plant Vogtle Conceptual Drawing of Vogtle Units 3 & 4 Georgia Power 45.7% Oglethorpe Power 30.0% MEAG 22.7% Dalton Utilities 1.6% 17 |

|

|

Financial Highlights Betsy Higgins Executive Vice President and Chief Financial Officer |

|

|

Income Statement Excerpts Margins for Interest ratio is calculated on an annual basis and is determined by dividing Oglethorpe’s Margins for Interest by Interest Charges, both as defined in Oglethorpe’s First Mortgage Indenture. The Indenture obligates Oglethorpe to establish and collect rates that, subject to any necessary regulatory approvals, are reasonably expected to yield a Margins for Interest ratio equal to at least 1.10x for each fiscal year. In addition, the Indenture requires a showing of Oglethorpe’s having met this requirement for certain historical periods as a condition for issuing additional obligations under the Indenture. Oglethorpe increased its Margins for Interest ratio to 1.12x for 2009 and to 1.14x for 2010, 2011 and 2012, above the minimum 1.10x ratio required by the Indenture. Oglethorpe’s Board of Directors will continue to evaluate margin coverage throughout the Vogtle construction period and may chose to further increase, or decrease, the Margins for Interest ratio in the future. 19 Key Point: Through September net margin equates to 122% of targeted annual margin ($39.4 million to achieve 1.14 MFI). This is typical for Oglethorpe and consistent with management’s practice of budgeting conservatively and making adjustments to the budget (typically toward the end of the year) to match actual expenses plus margin. December 31, ($ in thousands) 2012 2011 2011 2010 2009 Statement of Revenues and Expenses: Operating Revenues: Sales to Members $944,481 $947,130 $1,224,238 $1,292,667 $1,144,012 Sales to Non-Members 99,842 134,977 166,040 1,478 1,249 Operating Expenses 857,296 890,592 1,152,458 1,054,896 921,139 Other Income 46,659 31,447 44,264 43,651 42,728 Net Interest Charges (185,545) (183,726) (244,347) (249,167) (240,460) Net Margin $48,141 $39,236 $37,737 $33,733 $26,390 Margins for Interest Ratio (a) n/a n/a 1.14x 1.14x 1.12x Sales to Members Average Power Cost (cents/kWh) 5.75 6.15 6.25 5.71 5.67 MWh Sold 16,422,271 15,401,272 19,574,145 22,644,790 20,191,657 Year Ended September 30, Nine Months Ended |

|

|

Balance Sheet Excerpts (a) The equity ratio is less than that of many investor-owned utilities, as is typical for many wholesale G&T coops, because Oglethorpe operates on a not-for-profit basis and has a significant amount of authority to set and change rates to ensure sufficient cost recovery to produce margins to meet financial coverage requirements. The equity ratio is calculated, pursuant to Oglethorpe’s First Mortgage Indenture, by dividing patronage capital and membership fees by total capitalization plus long-term debt due within one year (Total Long-Term Debt and Equities in the table above). Oglethorpe has no financial covenant that requires it to maintain a minimum equity ratio; however, a covenant in the Indenture restricts distributions of equity (patronage capital) to its Members if its equity ratio is below 20%. Oglethorpe also has a covenant in a credit agreement that currently requires a minimum total patronage capital of $575 million. 20 September 30, ($ in thousands) 2012 2011 2010 Balance Sheet Data: Assets: Electric Plant: Net Plant in Service $3,988,451 $4,007,281 $3,570,522 CWIP 2,108,896 1,784,264 1,195,475 Nuclear Fuel 295,761 284,205 249,563 Total Electric Plant $6,393,108 $6,075,750 $5,015,560 Deposit on Rocky Mountain Transaction $42,932 $132,048 $123,573 Cash and Cash Equivalents $437,810 $443,671 $672,212 Total Assets $8,243,502 $8,078,829 $6,997,062 Capitalization: Patronage Capital and Membership Fees $681,830 $633,689 $595,952 Accumulated Other Comprehensive Loss 1,488 618 (469) Subtotal $683,318 $634,307 $595,483 Long-term Debt and Obligations under Capital Leases 5,731,965 5,709,706 4,836,415 Obligation under Rocky Mountain Transactions 42,932 132,048 123,573 Long-term Debt and Capital Leases due within one year 169,282 172,818 170,947 Total Long-Term Debt and Equities $6,627,497 $6,648,879 $5,726,418 Equity Ratio (a) 10.3% 9.5% 10.4% December 31, |

|

|

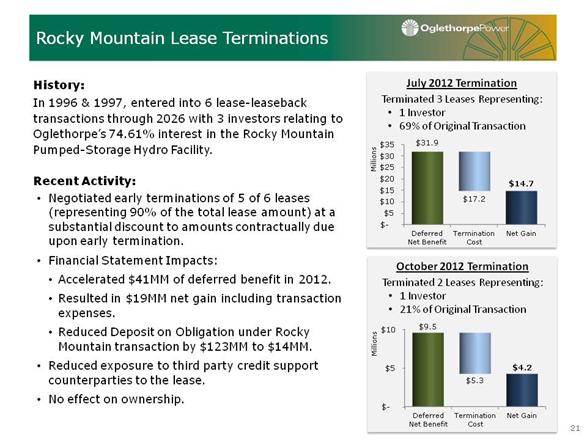

21 Rocky Mountain Lease Terminations October 2012 Termination Terminated 2 Leases Representing: 1 Investor 21% of Original Transaction July 2012 Termination Terminated 3 Leases Representing: 1 Investor 69% of Original Transaction History: In 1996 & 1997, entered into 6 lease-leaseback transactions through 2026 with 3 investors relating to Oglethorpe’s 74.61% interest in the Rocky Mountain Pumped-Storage Hydro Facility. Recent Activity: Negotiated early terminations of 5 of 6 leases (representing 90% of the total lease amount) at a substantial discount to amounts contractually due upon early termination. Financial Statement Impacts: Accelerated $41MM of deferred benefit in 2012. Resulted in $19MM net gain including transaction expenses. Reduced Deposit on Obligation under Rocky Mountain transaction by $123MM to $14MM. Reduced exposure to third party credit support counterparties to the lease. No effect on ownership. |

|

|

Signed conditional term sheet with DOE in May 2010. DOE loan guarantee targets 70% of eligible project costs, not to exceed $3.057 billion. All-in pricing expected to be favorable relative to taxable capital markets. Will be secured under Oglethorpe’s First Mortgage Indenture on parity with other secured debt. Final approval subject to negotiation of definitive agreements, due diligence by DOE and satisfaction of other conditions. There can be no assurance that DOE will ultimately issue loan guarantee to Oglethorpe. Projected start of DOE funding is early 2013. Any costs not funded by DOE will be financed through taxable bonds (have already issued $1.15 billion of taxable bonds and plan an additional taxable issuance in late 2012 that is partially Vogtle related). 22 DOE Loan Guarantees for Vogtle 3 & 4 |

|

|

23 RUS Loan Status Total Amount Outstanding of All RUS Guaranteed Loans: $2.2 billion Purpose/Use of Proceeds Approved Advanced (to date) Remaining Amount Approved Loans General Improvements $ 92,000,000 $ 45,685,619 $ 46,314,381 General & Environmental Improvements $ 441,522,000 $ 392,367,936 $ 49,154,064 General & Environmental Improvements $ 310,228,000 $ 117,878,134 $ 192,349,866 Hawk Road Energy Facility $ 203,100,000 $ 106,648,215 $ 96,451,785 General Improvements1 $ 127,703,000 $ - $ 127,703,000 Thomas A. Smith Energy Facility2 $ 492,610,000 $ - $ 492,610,000 $ 1,667,163,000 $ 662,579,904 $ 1,004,583,096 1 Anticipate loan will close and begin funding in Q1 2013 2 Anticipate loan will close and fully fund in Q1 2013 |

|

|

24 Bank Credit Facilities Term of Facilities Closed on a 2-year $150 million unsecured line of credit which replaced the existing $150 million secured line. Syndicated facility with CoBank as Administrative Agent. Completed the liquidity restructuring plan started in 2011. Bank of America, N.A. (Admin. Agent) 210 $ CoBank 150 $ SunTrust Bank 130 $ Wells Fargo Bank 125 $ Royal Bank of Canada 110 $ Bank of Montreal 100 $ Bank of Tokyo - Mitsubishi 100 $ Mizuho 80 $ JPMorgan Chase 60 $ Fifth Third Bank 50 $ Goldman Sachs Bank 50 $ US Bank 50 $ PNC Bank 40 $ Chang Hwa Commercial Bank 10 $ |

|

|

25 Oglethorpe’s Available Liquidity as of November 8, 2012 Borrowings Detail $407.9 MM Vogtle Interim Financing $274.9 MM Thomas A. Smith Acquisition Interim Financing $252.9 MM Letter of Credit Support for VRDBs/Thomas A. Smith $100.2 MM Vogtle Interest Rate Hedging Represents 548 days of liquidity on hand. 0 500 1,000 1,500 2,000 Total Credit Facilities Less Borrowings Available Line Capacity Cash (Excluding $64.7 Million in RUS Cushion of Credit) Total Liquidity $1,925 - $1,036 $889 $312 $1,201 (Millions) |

|

|

Rate Structure Assures Recovery of All Costs + Margin Fixed costs: Members billed based on board-approved annual budget and budget revisions throughout the year, if necessary. Prior period adjustment mechanism covers any year-end shortfall below required 1.10 MFI (board approval not required). Energy costs: Actual costs are passed through. Monthly true-up of estimate vs. actual. Note: First Mortgage Indenture requires an MFI ratio of least 1.10x MFI coverage requirement of 1.10x under First Mortgage Indenture. Achieved 1.14x MFI for 2010 and 2011. Budget of 1.14x MFI for 2012. Formulary rate under Wholesale Power Contract. Designed to recover all costs, plus margin, without any further regulatory approval. Annual budget and rate adjustments to reflect budget changes are generally not subject to approval of RUS or any other regulatory authority. Changes to rate schedule are subject to RUS approval. (Budgeted) Margin Coverage 26 $16.9 $17.2 $17.7 $18.2 $19.1 $19.3 $26.4 $33.7 $37.7 $39.4 $0.0 $15.0 $30.0 $45.0 Net Margin (MM) |

|

|

27 Liquidity Margins for Interest Wholesale Power Cost Interim Financing Long Term Debt Balance Sheet Electric Plant Average Cost of Funds: 0.74% (dollars in millions) Secured LT Debt (09.30.2012): $5.5 billion Weighted Average Cost: 4.92% Equity ratio: 10.3% 2012 1.14 MFI September 30, 2012 September 30, 2012 Actuals Forecast Cost of Power Sales to Members Additional Member Collections (reflects collections from Members for future expenses associated with a major maintenance sinking fund as well as debt service adder) |

|

|

Completed to date in 2012: Letter of Credit and remarketing agent substitution for $43.445 million Monroe 2010A bonds (March). $32.38 million tax-exempt refinancing (April). Syndicated $150 million unsecured credit facility with CoBank (October). Upcoming: Up to $250 million taxable bond offering (4th Quarter). Potential DOE financing (Early 2013). $212 million tax-exempt bond refinancing (1st Quarter 2013). 28 Recent and Upcoming Financing Activity |

|

|

One of the largest electric cooperatives in the United States. Oglethorpe has long-term, take-or-pay, joint and several Wholesale Power Contracts with its Members through 2050. Primarily residential customer base — approximately 2/3 of Members’ MWh sales and operating revenue. Oglethorpe’s formulary rate structure assures cost recovery. Inputs to rate formula are not subject to any regulatory approval. Changes to formulary rate schedule are subject to RUS approval. Members are not subject to regulation for rate setting purposes. Strong liquidity position. Well diversified power supply portfolio. Substantial value in existing resources. Strong, consistent operational and financial performance. Strong emphasis on risk management and corporate compliance. 29 Oglethorpe is a Strong, Stable Credit |

|

|

A link to this presentation will be posted on Oglethorpe’s website www.opc.com. Oglethorpe’s SEC filings, including its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K are made available on its website. For additional information please contact: 30 Additional Information Name Title Email Address Phone Number Betsy Higgins Executive Vice President and Chief Financial Officer betsy.higgins@opc.com 770-270-7168 Tom Brendiar Director, Bank and Investor Relations tom.brendiar@opc.com 770-270-7173 Joe Rick Director, Capital Markets joe.rick@opc.com 770-270-7240 |