Attached files

| file | filename |

|---|---|

| 8-K - U.S. CONCRETE, INC. 8-K - U.S. CONCRETE, INC. | usconcrete8k.htm |

Investor Presentation

November 15, 2012

Three Part Advisors, LLC

2012 Southwest IDEAS Conference

November 15, 2012

Three Part Advisors, LLC

2012 Southwest IDEAS Conference

Forward-Looking Statements

Certain statements provided in this presentation, including those that express a belief, expectation or

intention and those that are not of historical fact, are forward-looking statements within the meaning of

Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These

statements involve a number of risks and uncertainties and are intended to qualify for the safe harbors from

liability established by the Private Securities Litigation Reform Act of 1995. These risks and uncertainties may

cause actual results to differ materially from expected results and are described in detail in filings made by

U.S. Concrete, Inc. (the Company) with the Securities and Exchange Commission, including the

Companys Annual Report on Form 10-K for the year ended December 31, 2011 and subsequent Quarterly

Reports.

The forward-looking statements speak only as of the date of this presentation. Investors are cautioned not to

rely unduly on them. Many of these forward-looking statements are based on expectations and assumptions

about future events that may prove to be inaccurate. The Companys management considers these

expectations and assumptions to be reasonable, but they are inherently subject to significant business,

economic, competitive, regulatory and other risks, contingencies and uncertainties, most of which are difficult

to predict and many of which are beyond the Companys control. The Company undertakes no obligation to

update these statements unless required by applicable securities laws.

Certain statements provided in this presentation, including those that express a belief, expectation or

intention and those that are not of historical fact, are forward-looking statements within the meaning of

Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These

statements involve a number of risks and uncertainties and are intended to qualify for the safe harbors from

liability established by the Private Securities Litigation Reform Act of 1995. These risks and uncertainties may

cause actual results to differ materially from expected results and are described in detail in filings made by

U.S. Concrete, Inc. (the Company) with the Securities and Exchange Commission, including the

Companys Annual Report on Form 10-K for the year ended December 31, 2011 and subsequent Quarterly

Reports.

The forward-looking statements speak only as of the date of this presentation. Investors are cautioned not to

rely unduly on them. Many of these forward-looking statements are based on expectations and assumptions

about future events that may prove to be inaccurate. The Companys management considers these

expectations and assumptions to be reasonable, but they are inherently subject to significant business,

economic, competitive, regulatory and other risks, contingencies and uncertainties, most of which are difficult

to predict and many of which are beyond the Companys control. The Company undertakes no obligation to

update these statements unless required by applicable securities laws.

Company Overview

Ready-mixed concrete

4.3 million cubic yards in 2011

101 fixed and 13 portable concrete plants

Leading market position in 4 regions

Company Overview

Top 10 Producer of

Ready-Mixed Concrete in the U.S.

Page 4

Aggregates

7 aggregate and sand and gravel operations

1 recycle aggregate facility

4.3 million cubic yards in 2011

101 fixed and 13 portable concrete plants

Leading market position in 4 regions

Company Overview

Top 10 Producer of

Ready-Mixed Concrete in the U.S.

Page 4

Aggregates

7 aggregate and sand and gravel operations

1 recycle aggregate facility

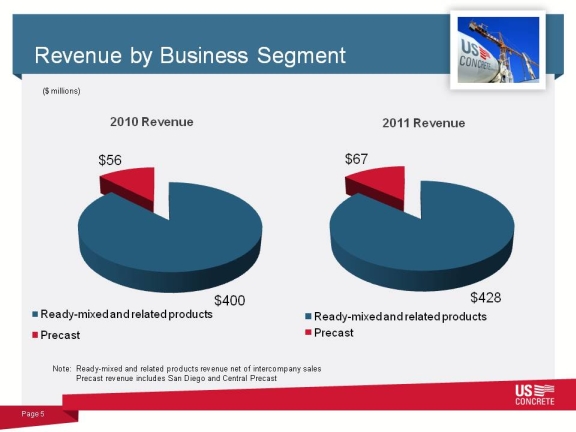

Revenue by Business Segment

$56

2010 Revenue 2011 Revenue

$67

($ millions)

$400

Ready-mixed and related products

Precast

Page 5

$428

Ready-mixed and related products

Precast

Note: Ready-mixed and related products revenue net of intercompany sales

Precast revenue includes San Diego and Central Precast

$56

2010 Revenue 2011 Revenue

$67

($ millions)

$400

Ready-mixed and related products

Precast

Page 5

$428

Ready-mixed and related products

Precast

Note: Ready-mixed and related products revenue net of intercompany sales

Precast revenue includes San Diego and Central Precast

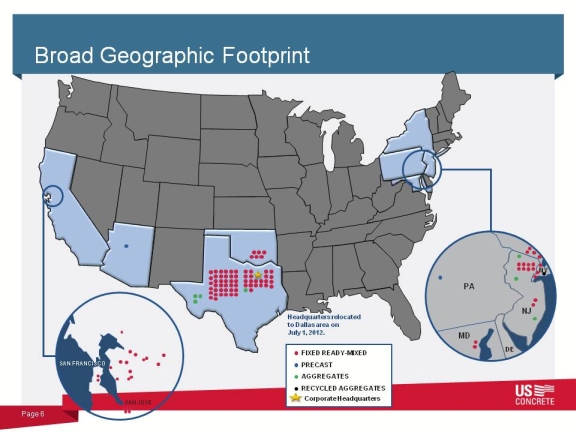

Broad Geographic Footprint

SAN FRANCISCO

SAN JOSE

MD

NJ

DE

NY

PA

Page 6

Headquarters relocated

to Dallas area on

July 1, 2012.

FIXED READY-MIXED

PRECAST

AGGREGATES

RECYCLED AGGREGATES

Corporate Headquarters

SAN FRANCISCO

SAN JOSE

MD

NJ

DE

NY

PA

Page 6

Headquarters relocated

to Dallas area on

July 1, 2012.

FIXED READY-MIXED

PRECAST

AGGREGATES

RECYCLED AGGREGATES

Corporate Headquarters

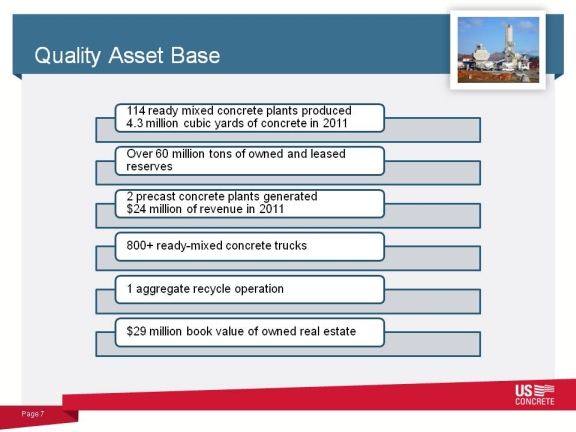

Quality Asset Base

114 ready mixed concrete plants produced

4.3 million cubic yards of concrete in 2011

Over 60 million tons of owned and leased

reserves

2 precast concrete plants generated

$24 million of revenue in 2011

Page 7

800+ ready-mixed concrete trucks

1 aggregate recycle operation

$29 million book value of owned real estate

114 ready mixed concrete plants produced

4.3 million cubic yards of concrete in 2011

Over 60 million tons of owned and leased

reserves

2 precast concrete plants generated

$24 million of revenue in 2011

Page 7

800+ ready-mixed concrete trucks

1 aggregate recycle operation

$29 million book value of owned real estate

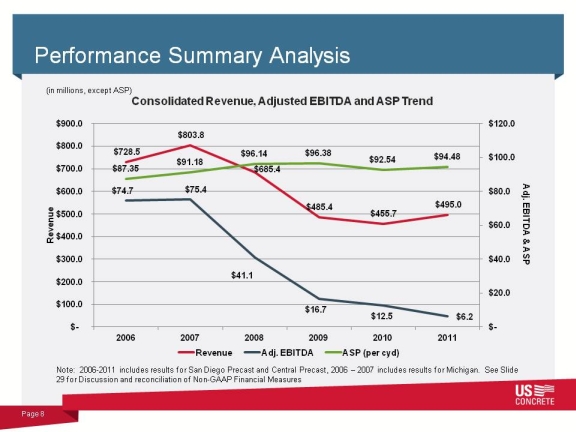

Performance Summary Analysis

$728.5

$803.8

$685.4

$485.4

$455.7

$495.0

$74.7 $75.4

$87.35

$91.18

$96.14 $96.38

$92.54 $94.48

$80.0

$100.0

$120.0

$500.0

$600.0

$700.0

$800.0

$900.0

Adj. EBITDA & ASP

Revenue

Consolidated Revenue, Adjusted EBITDA and ASP Trend

(in millions, except ASP)

$41.1

$16.7

$12.5 $6.2

$-

$20.0

$40.0

$60.0

$-

$100.0

$200.0

$300.0

$400.0

2006 2007 2008 2009 2010 2011

Revenue Adj. EBITDA ASP (per cyd)

Page 8

Note: 2006-2011 includes results for San Diego Precast and Central Precast, 2006 2007 includes results for Michigan. See Slide

29 for Discussion and reconciliation of Non-GAAP Financial Measures

$728.5

$803.8

$685.4

$485.4

$455.7

$495.0

$74.7 $75.4

$87.35

$91.18

$96.14 $96.38

$92.54 $94.48

$80.0

$100.0

$120.0

$500.0

$600.0

$700.0

$800.0

$900.0

Adj. EBITDA & ASP

Revenue

Consolidated Revenue, Adjusted EBITDA and ASP Trend

(in millions, except ASP)

$41.1

$16.7

$12.5 $6.2

$-

$20.0

$40.0

$60.0

$-

$100.0

$200.0

$300.0

$400.0

2006 2007 2008 2009 2010 2011

Revenue Adj. EBITDA ASP (per cyd)

Page 8

Note: 2006-2011 includes results for San Diego Precast and Central Precast, 2006 2007 includes results for Michigan. See Slide

29 for Discussion and reconciliation of Non-GAAP Financial Measures

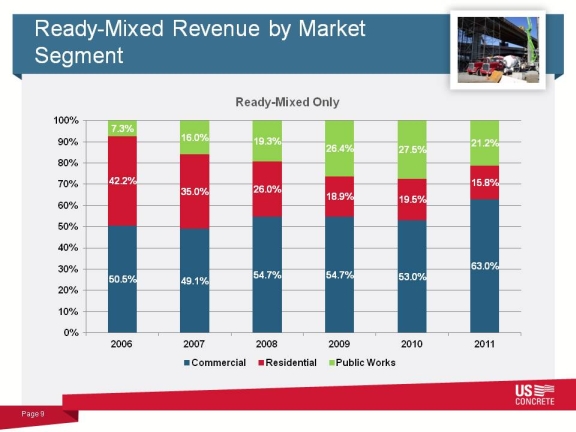

Ready-Mixed Revenue by Market

Segment

Ready-Mixed Only

42.2%

35.0% 26.0%

18.9% 19.5%

15.8%

7.3%

16.0% 19.3%

26.4% 27.5%

21.2%

60%

70%

80%

90%

100%

Page 9

50.5% 49.1%

54.7% 54.7% 53.0%

63.0%

0%

10%

20%

30%

40%

50%

2006 2007 2008 2009 2010 2011

Commercial Residential Public Works

Segment

Ready-Mixed Only

42.2%

35.0% 26.0%

18.9% 19.5%

15.8%

7.3%

16.0% 19.3%

26.4% 27.5%

21.2%

60%

70%

80%

90%

100%

Page 9

50.5% 49.1%

54.7% 54.7% 53.0%

63.0%

0%

10%

20%

30%

40%

50%

2006 2007 2008 2009 2010 2011

Commercial Residential Public Works

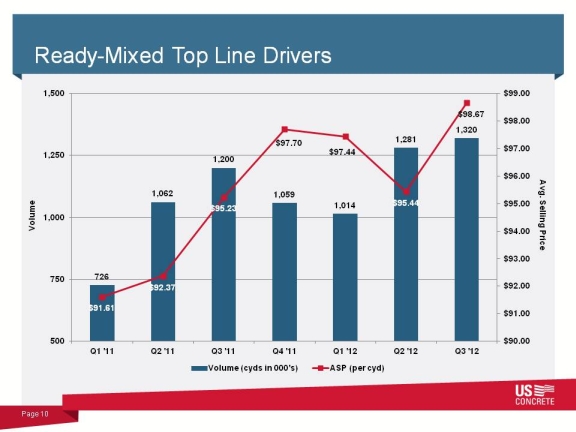

Ready-Mixed Top Line Drivers

1,062

1,200

1,059

1,014

1,281

1,320

$95.23

$97.70

$97.44

$95.44

$98.67

$95.00

$96.00

$97.00

$98.00

$99.00

1,000

1,250

1,500

Avg. Selling Price

Volume

726

$91.61

$92.37

$90.00

$91.00

$92.00

$93.00

$94.00

500

750

Q1 '11 Q2 '11 Q3 '11 Q4 '11 Q1 '12 Q2 '12 Q3 '12

Volume (cyds in 000's) ASP (per cyd)

1,062

1,200

1,059

1,014

1,281

1,320

$95.23

$97.70

$97.44

$95.44

$98.67

$95.00

$96.00

$97.00

$98.00

$99.00

1,000

1,250

1,500

Avg. Selling Price

Volume

726

$91.61

$92.37

$90.00

$91.00

$92.00

$93.00

$94.00

500

750

Q1 '11 Q2 '11 Q3 '11 Q4 '11 Q1 '12 Q2 '12 Q3 '12

Volume (cyds in 000's) ASP (per cyd)

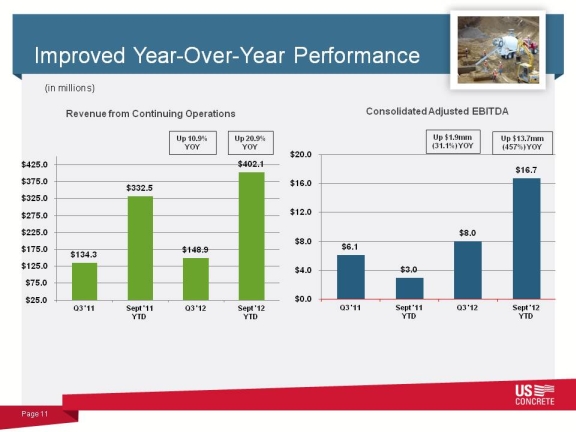

Improved Year-Over-Year Performance

Up $13.7mm

(457%) YOY

Up $1.9mm

(31.1%) YOY

(in millions)

Consolidated Adjusted EBITDA

$332.5

$402.1

$275.0

$325.0

$375.0

$425.0

Up 20.9%

YOY

Up 10.9%

YOY

Revenue from Continuing Operations

$6.1

$3.0

$8.0

$0.0

$4.0

$8.0

Q3 '11 Sept '11

YTD

Q3 '12 Sept '12

YTD

Up $13.7mm

(457%) YOY

Up $1.9mm

(31.1%) YOY

(in millions)

Consolidated Adjusted EBITDA

$332.5

$402.1

$275.0

$325.0

$375.0

$425.0

Up 20.9%

YOY

Up 10.9%

YOY

Revenue from Continuing Operations

$6.1

$3.0

$8.0

$0.0

$4.0

$8.0

Q3 '11 Sept '11

YTD

Q3 '12 Sept '12

YTD

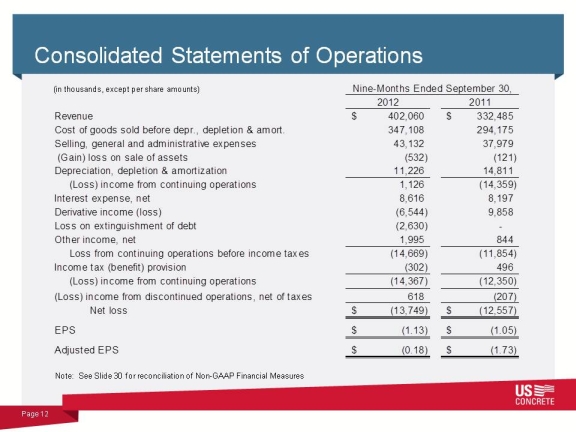

Consolidated Statements of Operations

2012 2011

Revenue $ 402,060 $ 332,485

Cost of goods sold before depr., depletion & amort. 347,108 294,175

Selling, general and administrative expenses 43,132 37,979

(Gain) loss on sale of assets (532) (121)

Depreciation, depletion & amortization 11,226 14,811

(Loss) income from continuing operations 1,126 (14,359)

Interest expense, net 8,616 8,197

Derivative income (loss) (6,544) 9,858

(in thousands, except per share amounts) Nine-Months Ended September 30,

Page 12

Loss on extinguishment of debt (2,630) -

Other income, net 1,995 844

Loss from continuing operations before income taxes (14,669) (11,854)

Income tax (benefit) provision (302) 496

(Loss) income from continuing operations (14,367) (12,350)

(Loss) income from discontinued operations, net of taxes 618 (207)

Net loss $ (13,749) $ (12,557)

EPS $ (1.13) $ (1.05)

Adjusted EPS $ (0.18) $ (1.73)

Note: See Slide 30 for reconciliation of Non-GAAP Financial Measures

2012 2011

Revenue $ 402,060 $ 332,485

Cost of goods sold before depr., depletion & amort. 347,108 294,175

Selling, general and administrative expenses 43,132 37,979

(Gain) loss on sale of assets (532) (121)

Depreciation, depletion & amortization 11,226 14,811

(Loss) income from continuing operations 1,126 (14,359)

Interest expense, net 8,616 8,197

Derivative income (loss) (6,544) 9,858

(in thousands, except per share amounts) Nine-Months Ended September 30,

Page 12

Loss on extinguishment of debt (2,630) -

Other income, net 1,995 844

Loss from continuing operations before income taxes (14,669) (11,854)

Income tax (benefit) provision (302) 496

(Loss) income from continuing operations (14,367) (12,350)

(Loss) income from discontinued operations, net of taxes 618 (207)

Net loss $ (13,749) $ (12,557)

EPS $ (1.13) $ (1.05)

Adjusted EPS $ (0.18) $ (1.73)

Note: See Slide 30 for reconciliation of Non-GAAP Financial Measures

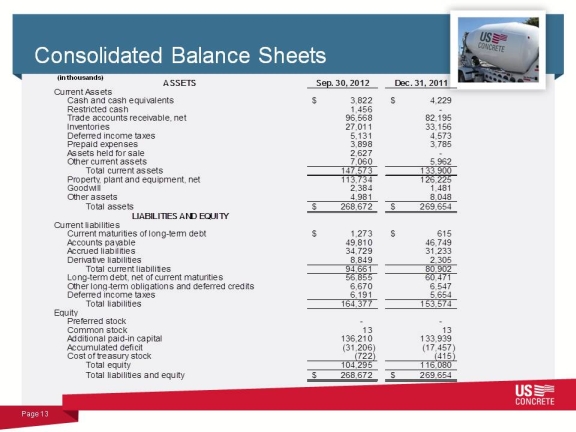

Consolidated Balance Sheets

(in thousands)

Sep. 30, 2012 Dec. 31, 2011

Current Assets

Cash and cash equivalents $ 3,822 $ 4,229

Restricted cash 1,456 -

Trade accounts receivable, net 96,568 82,195

Inventories 27,011 33,156

Deferred income taxes 5,131 4,573

Prepaid expenses 3,898 3,785

Assets held for sale 2,627 -

Other current assets 7,060 5,962

Total current assets 147,573 133,900

Property, plant and equipment, net 113,734 126,225

Goodwill 2,384 1,481

Other assets 4,981 8,048

Total assets $ 2 68,672 $ 269,654

ASSETS

LIABILITIES AND EQUITY

Page 13

Current liabilities

Current maturities of long-term debt $ 1,273 $ 615

Accounts payable 49,810 46,749

Accrued liabilities 34,729 31,233

Derivative liabilities 8,849 2,305

Total current liabilities 94,661 80,902

Long-term debt, net of current maturities 56,855 60,471

Other long-term obligations and deferred credits 6,670 6,547

Deferred income taxes 6,191 5,654

Total liabilities 164,377 153,574

Equity

Preferred stock - -

Common stock 13 13

Additional paid-in capital 136,210 133,939

Accumulated deficit (31,206) (17,457)

Cost of treasury stock (722) (415)

Total equity 104,295 116,080

Total liabilities and equity $ 2 68,672 $ 269,654

(in thousands)

Sep. 30, 2012 Dec. 31, 2011

Current Assets

Cash and cash equivalents $ 3,822 $ 4,229

Restricted cash 1,456 -

Trade accounts receivable, net 96,568 82,195

Inventories 27,011 33,156

Deferred income taxes 5,131 4,573

Prepaid expenses 3,898 3,785

Assets held for sale 2,627 -

Other current assets 7,060 5,962

Total current assets 147,573 133,900

Property, plant and equipment, net 113,734 126,225

Goodwill 2,384 1,481

Other assets 4,981 8,048

Total assets $ 2 68,672 $ 269,654

ASSETS

LIABILITIES AND EQUITY

Page 13

Current liabilities

Current maturities of long-term debt $ 1,273 $ 615

Accounts payable 49,810 46,749

Accrued liabilities 34,729 31,233

Derivative liabilities 8,849 2,305

Total current liabilities 94,661 80,902

Long-term debt, net of current maturities 56,855 60,471

Other long-term obligations and deferred credits 6,670 6,547

Deferred income taxes 6,191 5,654

Total liabilities 164,377 153,574

Equity

Preferred stock - -

Common stock 13 13

Additional paid-in capital 136,210 133,939

Accumulated deficit (31,206) (17,457)

Cost of treasury stock (722) (415)

Total equity 104,295 116,080

Total liabilities and equity $ 2 68,672 $ 269,654

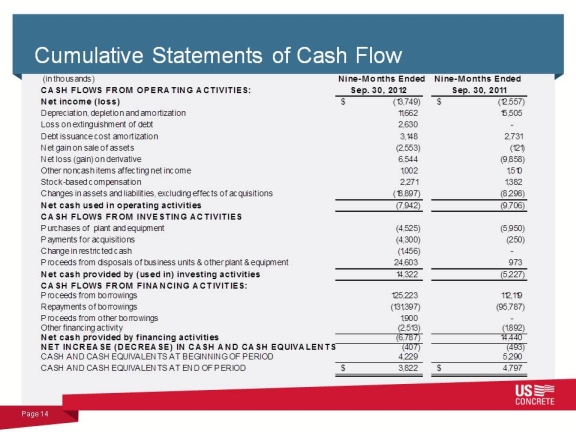

Cumulative Statements of Cash Flow

(in thousands) Nine-Months Ended Nine-Months Ended

CASH F LOWS FROM OP ERAT ING ACT IVIT IES: Sep. 30, 2012 Sep. 30, 2011

Net income ( lo ss) $ (13,749) $ (12,557)

Depreciation, depletion and amortization 11,662 15,505

Loss on extinguishment of debt 2,630 -

Debt issuance cost amortization 3,148 2,731

Net gain on sale of assets (2,553) (121)

Net loss (gain) on derivative 6,544 (9,858)

Other noncash items affecting net income 1,002 1,510

Stock-based compensation 2,271 1,382

Changes in assets and liabilities, excluding effects of acquisitions ( 18,897) (8,298)

Net cash used in o perat ing act ivit ies (7,942) (9,706)

CASH F LOWS FROM INVEST ING ACT IVIT IES

Page 14

Purchases of plant and equipment (4,525) (5,950)

Payments for acquisitions (4,300) (250)

Change in restricted cash (1,456) -

Proceeds from disposals of business units & other plant & equipment 24,603 973

Net cash pro vided by (used in) invest ing act ivit ies 14,322 (5,227)

CASH F LOWS FROM F INANCING ACT IVIT IES:

Proceeds from borrowings 125,223 112,119

Repayments of borrowings (131,397) (95,787)

Proceeds from other borrowings 1,900 -

Other financing activity (2,513) (1,892)

Net cash pro vided by f inancing act ivit ies (6,787) 14,440

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENT S (407) (493)

CASH AND CASH EQUIVALENTS AT BEGINNING OF PERIOD 4,229 5,290

CASH AND CASH EQUIVALENTS AT END OF PERIOD $ 3,822 $ 4,797

(in thousands) Nine-Months Ended Nine-Months Ended

CASH F LOWS FROM OP ERAT ING ACT IVIT IES: Sep. 30, 2012 Sep. 30, 2011

Net income ( lo ss) $ (13,749) $ (12,557)

Depreciation, depletion and amortization 11,662 15,505

Loss on extinguishment of debt 2,630 -

Debt issuance cost amortization 3,148 2,731

Net gain on sale of assets (2,553) (121)

Net loss (gain) on derivative 6,544 (9,858)

Other noncash items affecting net income 1,002 1,510

Stock-based compensation 2,271 1,382

Changes in assets and liabilities, excluding effects of acquisitions ( 18,897) (8,298)

Net cash used in o perat ing act ivit ies (7,942) (9,706)

CASH F LOWS FROM INVEST ING ACT IVIT IES

Page 14

Purchases of plant and equipment (4,525) (5,950)

Payments for acquisitions (4,300) (250)

Change in restricted cash (1,456) -

Proceeds from disposals of business units & other plant & equipment 24,603 973

Net cash pro vided by (used in) invest ing act ivit ies 14,322 (5,227)

CASH F LOWS FROM F INANCING ACT IVIT IES:

Proceeds from borrowings 125,223 112,119

Repayments of borrowings (131,397) (95,787)

Proceeds from other borrowings 1,900 -

Other financing activity (2,513) (1,892)

Net cash pro vided by f inancing act ivit ies (6,787) 14,440

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENT S (407) (493)

CASH AND CASH EQUIVALENTS AT BEGINNING OF PERIOD 4,229 5,290

CASH AND CASH EQUIVALENTS AT END OF PERIOD $ 3,822 $ 4,797

Industry Overview

$18.5

$30.0

$20.0

$40.0

$60.0

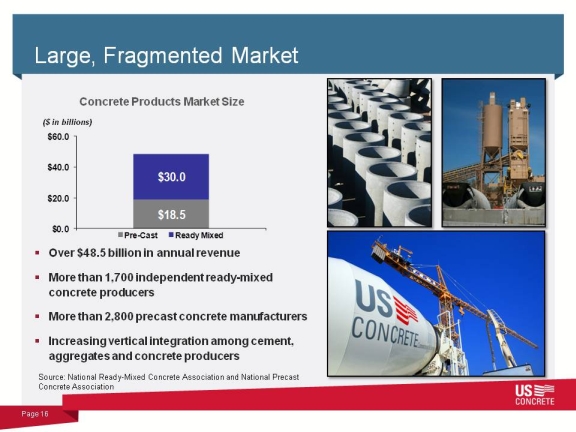

Large, Fragmented Market

Concrete Products Market Size

($ in billions)

$0.0

Pre-Cast Ready Mixed

Over $48.5 billion in annual revenue

More than 1,700 independent ready-mixed

concrete producers

More than 2,800 precast concrete manufacturers

Increasing vertical integration among cement,

aggregates and concrete producers

Page 16

Source: National Ready-Mixed Concrete Association and National Precast

Concrete Association

$30.0

$20.0

$40.0

$60.0

Large, Fragmented Market

Concrete Products Market Size

($ in billions)

$0.0

Pre-Cast Ready Mixed

Over $48.5 billion in annual revenue

More than 1,700 independent ready-mixed

concrete producers

More than 2,800 precast concrete manufacturers

Increasing vertical integration among cement,

aggregates and concrete producers

Page 16

Source: National Ready-Mixed Concrete Association and National Precast

Concrete Association

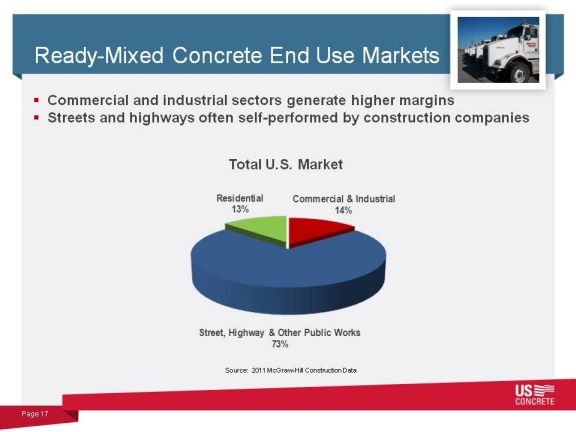

Ready-Mixed Concrete End Use Markets

Total U.S. Market

Residential

13%

Commercial & Industrial

14%

Commercial and industrial sectors generate higher margins

Streets and highways often self-performed by construction companies

Page 17

Source: 2011 McGraw-Hill Construction Data

Street, Highway & Other Public Works

73%

Total U.S. Market

Residential

13%

Commercial & Industrial

14%

Commercial and industrial sectors generate higher margins

Streets and highways often self-performed by construction companies

Page 17

Source: 2011 McGraw-Hill Construction Data

Street, Highway & Other Public Works

73%

Company Strategy and Focus

Our Mission, Values and Principles

Mission

Our Mission

is to become

the preferred

provider of

ready-mix Core Values

Safety

Integrity

Operational

Excellence

Sustainability

Operating Principles

Innovation

Quality

Productivity

Customer

Resource

concrete and

aggregate

products in

selective

markets we

serve

Environmental

Stewardship

Page 19

The Strategic Plan supports the Companys Mission and Core Values and

is tied to its Operating Principles and annual incentive plan

Mission

Our Mission

is to become

the preferred

provider of

ready-mix Core Values

Safety

Integrity

Operational

Excellence

Sustainability

Operating Principles

Innovation

Quality

Productivity

Customer

Resource

concrete and

aggregate

products in

selective

markets we

serve

Environmental

Stewardship

Page 19

The Strategic Plan supports the Companys Mission and Core Values and

is tied to its Operating Principles and annual incentive plan

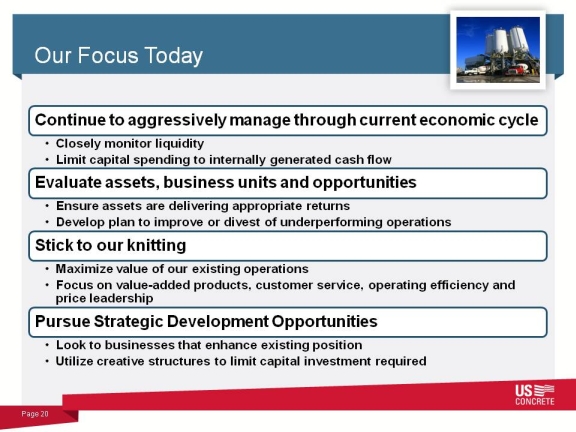

Our Focus Today

Continue to aggressively manage through current economic cycle

Closely monitor liquidity

Limit capital spending to internally generated cash flow

Evaluate assets, business units and opportunities

Ensure assets are delivering appropriate returns

Develop plan to improve or divest of underperforming operations

Stick to our knitting

Maximize value of our existing operations

Focus on value-added products, customer service, operating efficiency and

price leadership

Pursue Strategic Development Opportunities

Look to businesses that enhance existing position

Utilize creative structures to limit capital investment required

Page 20

Continue to aggressively manage through current economic cycle

Closely monitor liquidity

Limit capital spending to internally generated cash flow

Evaluate assets, business units and opportunities

Ensure assets are delivering appropriate returns

Develop plan to improve or divest of underperforming operations

Stick to our knitting

Maximize value of our existing operations

Focus on value-added products, customer service, operating efficiency and

price leadership

Pursue Strategic Development Opportunities

Look to businesses that enhance existing position

Utilize creative structures to limit capital investment required

Page 20

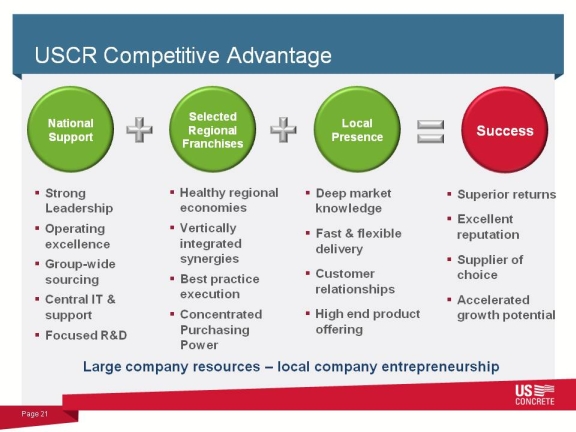

USCR Competitive Advantage

Strong

Leadership

Healthy regional

economies

Deep market

knowledge

Superior returns

Excellent

National

Support

Selected

Regional

Franchises

Local

Presence Success

Operating

excellence

Group-wide

sourcing

Central IT &

support

Focused R&D

Page 21

Vertically

integrated

synergies

Best practice

execution

Concentrated

Purchasing

Power

Fast & flexible

delivery

Customer

relationships

High end product

offering

reputation

Supplier of

choice

Accelerated

growth potential

Large company resources local company entrepreneurship

Strong

Leadership

Healthy regional

economies

Deep market

knowledge

Superior returns

Excellent

National

Support

Selected

Regional

Franchises

Local

Presence Success

Operating

excellence

Group-wide

sourcing

Central IT &

support

Focused R&D

Page 21

Vertically

integrated

synergies

Best practice

execution

Concentrated

Purchasing

Power

Fast & flexible

delivery

Customer

relationships

High end product

offering

reputation

Supplier of

choice

Accelerated

growth potential

Large company resources local company entrepreneurship

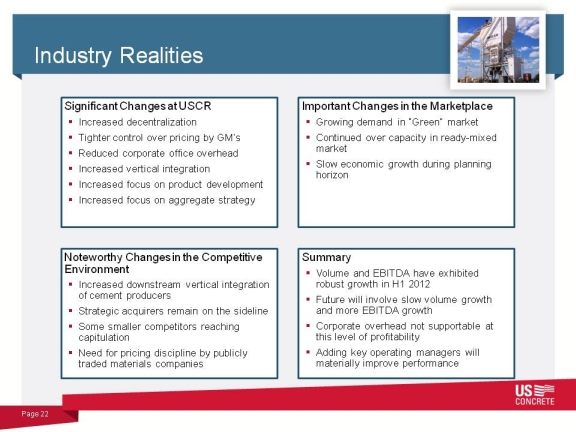

Industry Realities

Significant Changes at USCR

Increased decentralization

Tighter control over pricing by GMs

Reduced corporate office overhead

Increased vertical integration

Increased focus on product development

Increased focus on aggregate strategy

Important Changes in the Marketplace

Growing demand in Green market

Continued over capacity in ready-mixed

market

Slow economic growth during planning

horizon

Noteworthy Changes in the Competitive

Environment

Increased downstream vertical integration

of cement producers

Strategic acquirers remain on the sideline

Some smaller competitors reaching

capitulation

Need for pricing discipline by publicly

traded materials companies

Summary

Volume and EBITDA have exhibited

robust growth in H1 2012

Future will involve slow volume growth

and more EBITDA growth

Corporate overhead not supportable at

this level of profitability

Adding key operating managers will

materially improve performance

Page 22

Significant Changes at USCR

Increased decentralization

Tighter control over pricing by GMs

Reduced corporate office overhead

Increased vertical integration

Increased focus on product development

Increased focus on aggregate strategy

Important Changes in the Marketplace

Growing demand in Green market

Continued over capacity in ready-mixed

market

Slow economic growth during planning

horizon

Noteworthy Changes in the Competitive

Environment

Increased downstream vertical integration

of cement producers

Strategic acquirers remain on the sideline

Some smaller competitors reaching

capitulation

Need for pricing discipline by publicly

traded materials companies

Summary

Volume and EBITDA have exhibited

robust growth in H1 2012

Future will involve slow volume growth

and more EBITDA growth

Corporate overhead not supportable at

this level of profitability

Adding key operating managers will

materially improve performance

Page 22

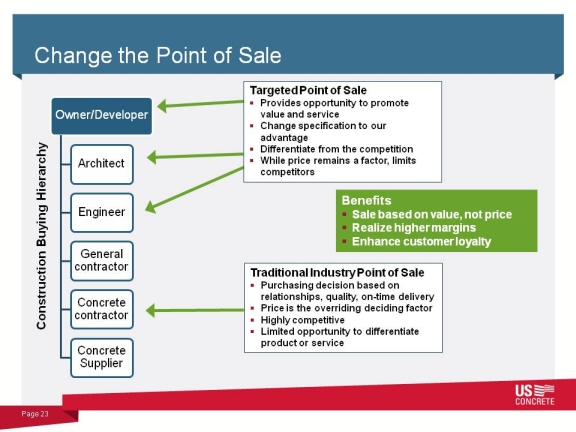

Change the Point of Sale

Owner/Developer

Architect

Engineer

Construction Buying Hierarchy

Targeted Point of Sale

Provides opportunity to promote

value and service

Change specification to our

advantage

Differentiate from the competition

While price remains a factor, limits

competitors

Benefits

Sale based on value, not price

General

contractor

Concrete

contractor

Concrete

Supplier

Page 23

Realize higher margins

Enhance customer loyalty

Traditional Industry Point of Sale

Purchasing decision based on

relationships, quality, on-time delivery

Price is the overriding deciding factor

Highly competitive

Limited opportunity to differentiate

product or service

Owner/Developer

Architect

Engineer

Construction Buying Hierarchy

Targeted Point of Sale

Provides opportunity to promote

value and service

Change specification to our

advantage

Differentiate from the competition

While price remains a factor, limits

competitors

Benefits

Sale based on value, not price

General

contractor

Concrete

contractor

Concrete

Supplier

Page 23

Realize higher margins

Enhance customer loyalty

Traditional Industry Point of Sale

Purchasing decision based on

relationships, quality, on-time delivery

Price is the overriding deciding factor

Highly competitive

Limited opportunity to differentiate

product or service

Sustainable Development Today

Sustainable construction is

not a passing fad

Membership in the U.S.

Green building Council has

increased from fewer than

100 to over 18,000 in the past

decade

Over 155,000 building

Page 24

U.S. Concrete, Inc.

professionals are LEED

certified

Demand for green building

materials is forecasted to

grow at an accelerated rate

Sustainable construction is

not a passing fad

Membership in the U.S.

Green building Council has

increased from fewer than

100 to over 18,000 in the past

decade

Over 155,000 building

Page 24

U.S. Concrete, Inc.

professionals are LEED

certified

Demand for green building

materials is forecasted to

grow at an accelerated rate

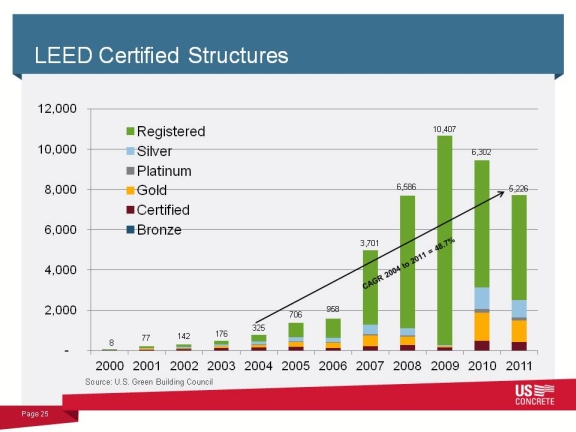

LEED Certified Structures

6,586

10,407

6,302

8,000 5,226

10,000

12,000

Registered

Silver

Platinum

Gold

Certified

8

77 142 176

325

706

958

3,701

-

2,000

4,000

6,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Bronze

Page 25

Source: U.S. Green Building Council

6,586

10,407

6,302

8,000 5,226

10,000

12,000

Registered

Silver

Platinum

Gold

Certified

8

77 142 176

325

706

958

3,701

-

2,000

4,000

6,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Bronze

Page 25

Source: U.S. Green Building Council

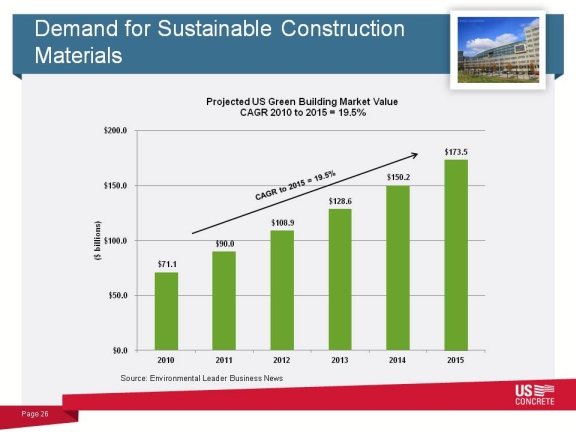

Demand for Sustainable Construction

Materials

$128.6

$150.2

$173.5

$150.0

$200.0

Projected US Green Building Market Value

CAGR 2010 to 2015 = 19.5%

Page 26

$71.1

$90.0

$108.9

$0.0

$50.0

$100.0

2010 2011 2012 2013 2014 2015

($ billions)

Source: Environmental Leader Business News

Materials

$128.6

$150.2

$173.5

$150.0

$200.0

Projected US Green Building Market Value

CAGR 2010 to 2015 = 19.5%

Page 26

$71.1

$90.0

$108.9

$0.0

$50.0

$100.0

2010 2011 2012 2013 2014 2015

($ billions)

Source: Environmental Leader Business News

Benefits of Our Sustainable Strategy

Increase product demand

Sustainable demand to grow at a higher rate

Increase revenue and profit per yard

Higher priced value-added products drive margins

Reduce raw material cost per yard

Lower cost of cement alternatives

Differentiate Company from competition

Cement companies remain focused on core cement

Create competitive advantage

First mover offering solution to owners

Page 27

Increase product demand

Sustainable demand to grow at a higher rate

Increase revenue and profit per yard

Higher priced value-added products drive margins

Reduce raw material cost per yard

Lower cost of cement alternatives

Differentiate Company from competition

Cement companies remain focused on core cement

Create competitive advantage

First mover offering solution to owners

Page 27

Conclusions

Short-term actions will provide organic growth through 2014 despite

no meaningful economic recovery

Execute an extremely disciplined regional price leadership strategy

Refocus efforts on improved aggregate tactical operational plan

Aggressively restructure business into more decentralized model

More local ownership of results

Think like owners/entrepreneurial spirit

Smaller corporate staff in full facilitation/support role

Pursue aggressive R&D efforts to develop and market Green

products.

Seek out value added, bolt-on acquisitions in existing markets and

potential divestitures in underperforming segments.

Page 28

Short-term actions will provide organic growth through 2014 despite

no meaningful economic recovery

Execute an extremely disciplined regional price leadership strategy

Refocus efforts on improved aggregate tactical operational plan

Aggressively restructure business into more decentralized model

More local ownership of results

Think like owners/entrepreneurial spirit

Smaller corporate staff in full facilitation/support role

Pursue aggressive R&D efforts to develop and market Green

products.

Seek out value added, bolt-on acquisitions in existing markets and

potential divestitures in underperforming segments.

Page 28

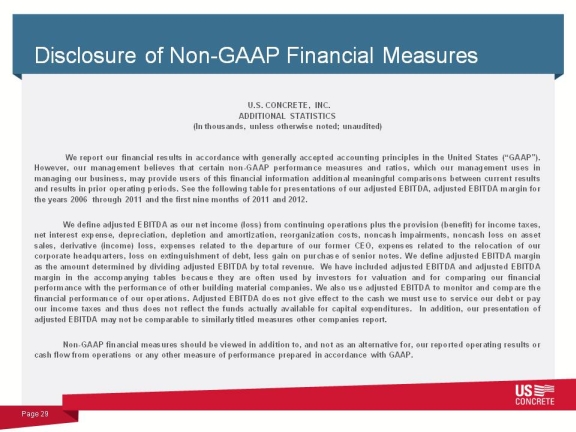

Disclosure of Non-GAAP Financial Measures

U.S. CONCRETE, INC.

ADDITIONAL STATISTICS

(In thousands, unless otherwise noted; unaudited)

We report our financial results in accordance with generally accepted accounting principles in the United States (GAAP).

However, our management believes that certain non-GAAP performance measures and ratios, which our management uses in

managing our business, may provide users of this financial information additional meaningful comparisons between current results

and results in prior operating periods. See the following table for presentations of our adjusted EBITDA, adjusted EBITDA margin for

the years 2006 through 2011 and the first nine months of 2011 and 2012.

We define adjusted EBITDA as our net income (loss) from continuing operations plus the provision (benefit) for income taxes,

net interest expense, depreciation, depletion and amortization, reorganization costs, noncash impairments, noncash loss on asset

sales, derivative (income) loss, expenses related to the departure of our former CEO, expenses related to the relocation of our

corporate headquarters, loss on extinguishment of debt, less gain on purchase of senior notes. We define adjusted EBITDA margin

as the amount determined by dividing adjusted EBITDA by total revenue. We have included adjusted EBITDA and adjusted EBITDA

margin in the accompanying tables because they are often used by investors for valuation and for comparing our financial

performance with the performance of other building material companies. We also use adjusted EBITDA to monitor and compare the

financial performance of our operations. Adjusted EBITDA does not give effect to the cash we must use to service our debt or pay

our income taxes and thus does not reflect the funds actually available for capital expenditures. In addition, our presentation of

adjusted EBITDA may not be comparable to similarly titled measures other companies report.

Non-GAAP financial measures should be viewed in addition to, and not as an alternative for, our reported operating results or

cash flow from operations or any other measure of performance prepared in accordance with GAAP.

Page 29

U.S. CONCRETE, INC.

ADDITIONAL STATISTICS

(In thousands, unless otherwise noted; unaudited)

We report our financial results in accordance with generally accepted accounting principles in the United States (GAAP).

However, our management believes that certain non-GAAP performance measures and ratios, which our management uses in

managing our business, may provide users of this financial information additional meaningful comparisons between current results

and results in prior operating periods. See the following table for presentations of our adjusted EBITDA, adjusted EBITDA margin for

the years 2006 through 2011 and the first nine months of 2011 and 2012.

We define adjusted EBITDA as our net income (loss) from continuing operations plus the provision (benefit) for income taxes,

net interest expense, depreciation, depletion and amortization, reorganization costs, noncash impairments, noncash loss on asset

sales, derivative (income) loss, expenses related to the departure of our former CEO, expenses related to the relocation of our

corporate headquarters, loss on extinguishment of debt, less gain on purchase of senior notes. We define adjusted EBITDA margin

as the amount determined by dividing adjusted EBITDA by total revenue. We have included adjusted EBITDA and adjusted EBITDA

margin in the accompanying tables because they are often used by investors for valuation and for comparing our financial

performance with the performance of other building material companies. We also use adjusted EBITDA to monitor and compare the

financial performance of our operations. Adjusted EBITDA does not give effect to the cash we must use to service our debt or pay

our income taxes and thus does not reflect the funds actually available for capital expenditures. In addition, our presentation of

adjusted EBITDA may not be comparable to similarly titled measures other companies report.

Non-GAAP financial measures should be viewed in addition to, and not as an alternative for, our reported operating results or

cash flow from operations or any other measure of performance prepared in accordance with GAAP.

Page 29

Reconciliation of Non-GAAP Financial

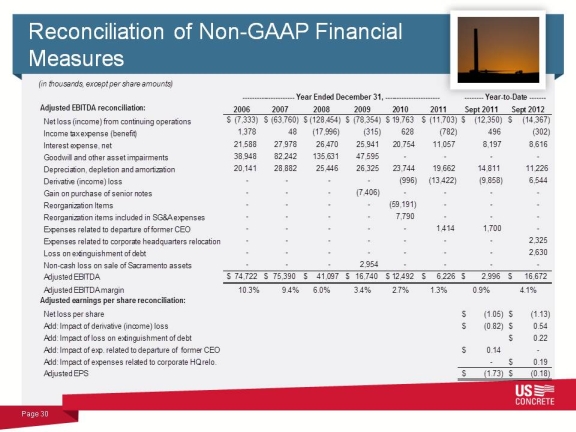

Measures

(in thousands, except per share amounts)

Adjusted EBITDA reconciliation: 2006 2007 2008 2009 2010 2011 Sept 2011 Sept 2012

Net loss (income) from continuing operations $ (7,333) $ (63,760) $ (128,454) $ (78,354) $ 19,763 $ (11,703) $ (12,350) $ (14,367)

Income tax expense (benefit) 1,378 48 (17,996) (315) 628 (782) 496 (302)

Interest expense, net 21,588 27,978 26,470 25,941 20,754 11,057 8,197 8,616

Goodwill and other asset impairments 38,948 82,242 135,631 47,595 - - - -

Depreciation, depletion and amortization 20,141 28,882 25,446 26,325 23,744 19,662 14,811 11,226

Derivative (income) loss - - - - (996) (13,422) (9,858) 6,544

Gain on purchase of senior notes - - - (7,406) - - - -

Reorganization Items - - - - (59,191) - - -

Reorganization items included in SG&A expenses - - - - 7,790 - - -

---------------------- Year Ended December 31, ----------------------- -------- Year-to-Date -------

Page 30

Expenses related to departure of former CEO - - - - - 1,414 1,700 -

Expenses related to corporate headquarters relocation - - - - - - - 2,325

Loss on extinguishment of debt - - - - - - - 2,630

Non-cash loss on sale of Sacramento assets - - - 2,954 - - - -

Adjusted EBITDA $ 74,722 $ 75,390 $ 41,097 $ 16,740 $ 12,492 $ 6,226 $ 2,996 $ 16,672

Adjusted EBITDA margin 10.3% 9.4% 6.0% 3.4% 2.7% 1.3% 0.9% 4.1%

Adjusted earnings per share reconciliation:

Net loss per share $ (1.05) $ (1.13)

Add: Impact of derivative (income) loss $ (0.82) $ 0.54

Add: Impact of loss on extinguishment of debt $ 0.22

Add: Impact of exp. related to departure of former CEO $ 0.14 -

Add: Impact of expenses related to corporate HQ relo. - $ 0.19

Adjusted EPS $ (1.73) $ (0.18)

Measures

(in thousands, except per share amounts)

Adjusted EBITDA reconciliation: 2006 2007 2008 2009 2010 2011 Sept 2011 Sept 2012

Net loss (income) from continuing operations $ (7,333) $ (63,760) $ (128,454) $ (78,354) $ 19,763 $ (11,703) $ (12,350) $ (14,367)

Income tax expense (benefit) 1,378 48 (17,996) (315) 628 (782) 496 (302)

Interest expense, net 21,588 27,978 26,470 25,941 20,754 11,057 8,197 8,616

Goodwill and other asset impairments 38,948 82,242 135,631 47,595 - - - -

Depreciation, depletion and amortization 20,141 28,882 25,446 26,325 23,744 19,662 14,811 11,226

Derivative (income) loss - - - - (996) (13,422) (9,858) 6,544

Gain on purchase of senior notes - - - (7,406) - - - -

Reorganization Items - - - - (59,191) - - -

Reorganization items included in SG&A expenses - - - - 7,790 - - -

---------------------- Year Ended December 31, ----------------------- -------- Year-to-Date -------

Page 30

Expenses related to departure of former CEO - - - - - 1,414 1,700 -

Expenses related to corporate headquarters relocation - - - - - - - 2,325

Loss on extinguishment of debt - - - - - - - 2,630

Non-cash loss on sale of Sacramento assets - - - 2,954 - - - -

Adjusted EBITDA $ 74,722 $ 75,390 $ 41,097 $ 16,740 $ 12,492 $ 6,226 $ 2,996 $ 16,672

Adjusted EBITDA margin 10.3% 9.4% 6.0% 3.4% 2.7% 1.3% 0.9% 4.1%

Adjusted earnings per share reconciliation:

Net loss per share $ (1.05) $ (1.13)

Add: Impact of derivative (income) loss $ (0.82) $ 0.54

Add: Impact of loss on extinguishment of debt $ 0.22

Add: Impact of exp. related to departure of former CEO $ 0.14 -

Add: Impact of expenses related to corporate HQ relo. - $ 0.19

Adjusted EPS $ (1.73) $ (0.18)

Investor Presentation

November 15, 2012

Three Part Advisors, LLC

2012 Southwest IDEAS Conference

November 15, 2012

Three Part Advisors, LLC

2012 Southwest IDEAS Conference