Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - FIFTH THIRD BANCORP | d441376d8k.htm |

©

Fifth Third Bank | All Rights Reserved

Bank of America Merrill Lynch

Banking & Financials Conference

Daniel T. Poston

Executive Vice President & Chief Financial Officer

November 14, 2012

Refer to earnings release dated October 18, 2012

and 10-Q dated November 7, 2012 for further information

Exhibit 99.1 |

2

©

Fifth Third Bank | All Rights Reserved

A strong franchise showing momentum

Strong results underscored by

continued loan growth, solid fee

income, expense control, and ongoing

improvement in credit metrics

Traditional banking model moderate

risk profile and strong execution

contribute to above average returns

New product offerings consistent with

our mission, our customer value

proposition, and regulatory reform

Return capital from robust internal

capital generation through

appropriate dividend payout and

share repurchase plans

Current and forecasted fully phased-in

pro-forma capital ratios would

substantially exceed new fully

phased-in well-capitalized minimums

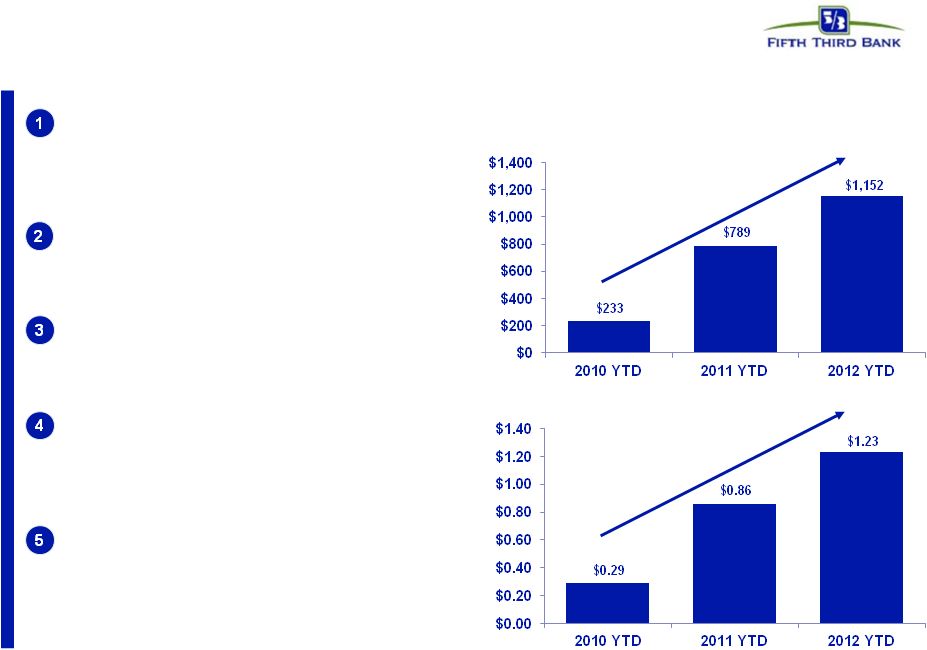

Earnings Growth

Net income available to common shareholders ($MM)

Diluted EPS |

3

©

Fifth Third Bank | All Rights Reserved

•

Continued strong loan production

–

Rates on loan originations lower but loan

interest income stable

•

Continue to provide customers with products /

solutions they find valuable

•

Careful management of liability costs

–

Disciplined pricing on deposits

–

Continued evaluation of term liabilities and

capital instruments

•

Strong mortgage banking results

•

Mortgage risks manageable

–

Typical quarterly mortgage repurchase cost

~$20MM

–

No mortgage securitizations outstanding

•

Strong profitability and capital in excess of fully

phased-in

Basel

III

standards

today

–

Believe we are well positioned to maintain

strong capital while providing meaningful

distributions to shareholders*

Environment characterized by low growth

expectations and low interest rates

•

Prolonged low-rate environment, coupled

with modest economic growth

•

Lower securities reinvestment yields on

portfolio cash flows

•

Strong deposit flows

•

Competitive dynamics

•

Elevated mortgage refinance activity

•

Firms facing significant costs related to

mortgage securitizations, GSE

repurchases, private label mortgage

repurchases

•

Higher capital standards; limitations on

dividend payout ratios; capital building

beyond targeted / required levels

•

Economic uncertainty including fiscal

cliff and impact on business activity;

concerns about European financial

system

Fifth Third is well-positioned to deal with current environmental

challenges Characteristics of current environment

Fifth Third’s response / position

* Subject to 2013 Comprehensive Capital Analysis & Review final rules; subject

to Board of Directors and regulatory approval. •

Low exposure to European banks (see slide 22) |

4

©

Fifth Third Bank | All Rights Reserved

NII results reflect continued moderate NIM

pressure offset by balance sheet growth

* Represents purchase accounting adjustments included in net interest income.

^ Estimate; funding (DDAs + interest-bearing liabilities); liabilities

attributed to fixed or floating using terms and expected beta

Fixed / Floating Portfolio

•

3Q12 NII included $10MM of non-recurring benefits (4

bps positive impact to NIM)

•

NIM pressure created by low rate environment, higher

prepayment speeds, repricing in securities and loan

portfolios, and modest natural asset sensitivity, but

overall is expected to be manageable

•

Spreads on new originations of variable rate assets

consistent with historical spreads

Interest-Earning

Assets

Funding^

Fixed

~55-60%

NII and NIM (FTE)

($MM)

Loans

50%

Loans

33%

Investment

Portfolio 3%

Trend: fixed rate loan origination coupons

relative to fixed portfolio weighted avg

Larger portfolio repricing effects

–

Emphasis on variable rate C&I lending

•

Coupons on new fixed rate loan originations

converging with portfolio average coupons

•

Current trends have pressured net interest income

levels, but expect to mitigate much of impact with

continued loan growth and liability management

Investment

Portfolio

14% |

5

©

Fifth Third Bank | All Rights Reserved

Balance sheet growth mitigates rate environment

•

Core deposit to loan ratio of 99% consistent with

3Q11

–

DDAs up 15% year-over-year

–

Consumer average transaction deposits up 5%

year-over-year

–

Commercial average transaction deposits up

10% year-over-year

Average loan growth ($B)^

Average core deposit growth ($B)

83

79

82

78

^ Excludes loans held-for-sale

Note: Numbers may not sum due to rounding

80

81

82

82

83

•

Growth driven by C&I and residential mortgage

loans; portfolios in run-off mode are of moderate

size

–

Commercial line utilization stable at 32%;

potential source of future growth

•

CRE portfolio continues to run-off, with modest

selective current origination volume

•

Managing auto volumes to ensure appropriate

returns; spread pressure due to competition

•

Branch mortgage refi product has FICO over 780,

LTV ~60% and avg. term ~15 years while yielding

above market rates due to process convenience

82

•

Short-term wholesale borrowings represent only

7% of total funding |

6

©

Fifth Third Bank | All Rights Reserved

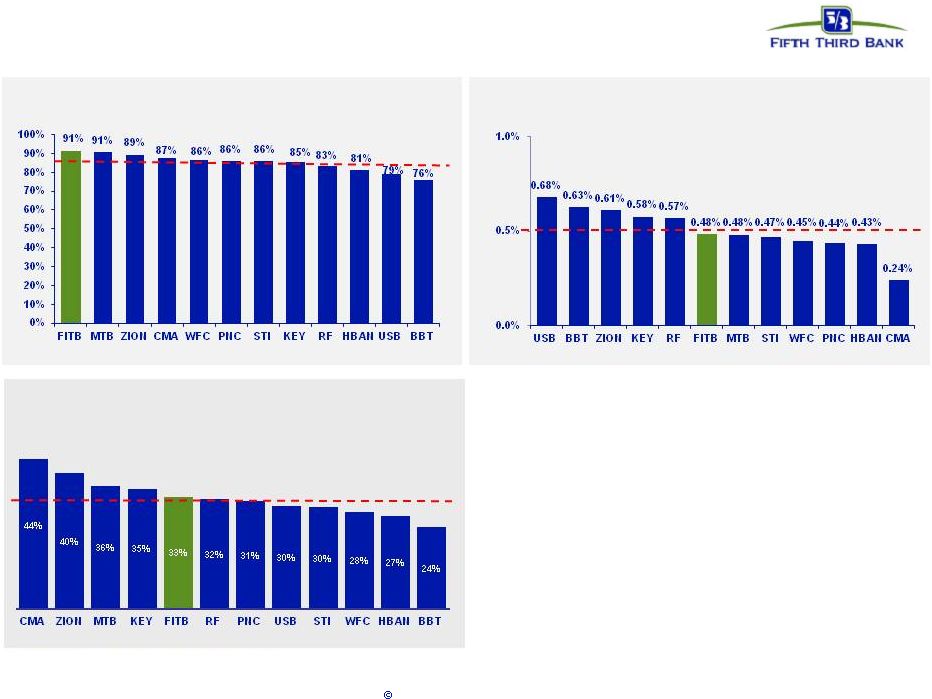

Strength in C&I loan growth

C&I Loans/Average Assets*^

C&I Spread to 1-month LIBOR

Peer average: 24%

Continued demand in large corporate and mid-

corporate space

Reduction in portfolio yields driven by mix shift

toward higher-quality loans, portfolio effects of

repricing, and pressure on new origination yields

C&I loans as a percent of total commercial loans

was 71% at 3Q12 versus peer average of 63%

C&I production continues to be broad based across

industries and sectors

—

Strength in manufacturing and healthcare

industries

—

Launch of Energy Lending vertical expected to

contribute to future growth in C&I

C&I spreads remain stable

C&I Portfolio^ ($B)

^ Presented on an average basis; Excluding held-for-sale loans. Source: SNL Financial and Company

Reports. Peer average includes: BBT, CMA, HBAN, KEY, MTB, PNC, RF, STI, USB, WFC, and ZION

* ZION & BBT exclude government guaranteed loans; ZION presented as end of period data. |

7

Fifth Third Bank | All Rights Reserved

Strong revenue and profit generation

Source: SNL Financial and Company Reports. Peer median includes: BBT, CMA, HBAN,

KEY, MTB, PNC, RF, STI, USB, WFC, and ZION ^ Excludes

$3MM,

$10MM,

$46MM,

and

$56MM

positive

valuation

adjustment

on

the

Vantiv

warrant

and

put

option

in

3Q11,

4Q11,

1Q12, and 2Q12, respectively, and a $16 million negative

valuation adjustment on the Vantiv warrant in 3Q12, as well as $115MM in gains from

Vantiv's IPO and $34MM charge related to Vantiv's debt refinancing in 1Q12. *

Non-GAAP measure. See Reg. G reconciliation in the Appendix to the presentation.

Revenue

^

/ Avg. Int. Earning Assets

PPNR

^*

/ Avg. Int. Earning Assets

3Q12 returns strong relative to peers

NII / Total Assets

Noninterest Income^ / Total Assets

•

Business mix provides higher than average

diversity among spread and fee revenues (40+%

of revenue)

•

Relatively strong margin and relatively high fee

income contribution drives strong revenue and

PPNR generation profitability despite sluggish

economy

•

Income from ownership in Vantiv $25MM in

3Q12 (full year 2011 quarterly avg ~$14MM,

despite selling ~10% in 1Q12)

6.33%

5.82%

6.18%

6.02%

6.00%

6.25%

ROAA

ROAE

2.50%

1.86%

2.29%

2.31%

2.31%

2.13%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3Q11

4Q11

1Q12

2Q12

3Q12

3Q12

Peer Median

3.65%

3.67%

3.61%

3.56%

3.56%

3.58%

2.68%

2.15%

2.57%

2.46%

2.69%

2.42%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

3Q11

4Q11

1Q12

2Q12

3Q12

3Q12

Peer Median

1.23%

1.20%

1.28%

FITB

Peer Median

ROAA

Adjusted ROAA^

10.4%

10.1%

10.9%

FITB

Peer Median

ROAE

Adjusted ROAE^

©

Fifth Third Bank | All Rights Reserved |

8

Strong mortgage banking results

•

Record origination fees and gain on

loan sales in 3Q12

•

Highest ranking among all servicers

and peer groups in Fannie Mae’s

2011 STAR

TM

Program for servicing

performance

Looking forward:

•

Stronger originations / deliveries in

4Q12 vs 3Q12

–

Results should remain robust

while rates remain low

•

Gain on sale margins benefitting

from:

–

Strong demand

–

Industry capacity constraints

–

Strong mortgage-backed securities

pricing

•

HARP 2.0 originations expected to

remain similar percentage of total

originations in 4Q12 vs 3Q12

Mortgage originations and gain-on-sale margins*

Mortgage Banking Revenue ($MM)

* Gain-on-sale margin represents margin on loans originated for sale.

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

$0

$1

$2

$3

$4

$5

$6

$7

$8

3Q11

4Q11

1Q12

2Q12

3Q12

Originations for sale

Originations HFI

Margins*

($B)

119

152

174

183

226

59

58

61

63

62

(34)

(47)

(46)

(41)

(48)

34

(7)

15

(22)

(40)

3Q11

4Q11

1Q12

2Q12

3Q12

Orig fees and gains on loan sales

Gross servicing fees

Servicing rights amortization

MSR valuation adjustments

$178

$200

$183

$156

$204

©

Fifth Third Bank | All Rights Reserved |

9

©

Fifth Third Bank | All Rights Reserved

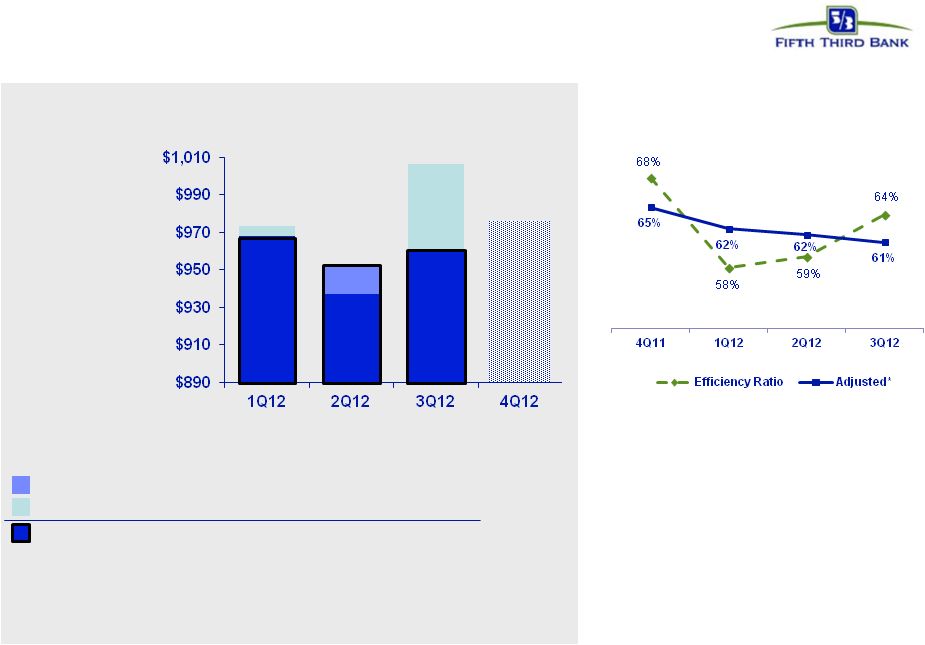

Disciplined expense management

•

Expect similar adjusted efficiency ratio in

4Q12; target mid-50% in normalized

environment (with higher interest rate

environment)

2012 expense trend ($MM)

* Non-recurring items described on page 18 in the appendix to this

presentation. Reported expense

Increasing expense

Non-recurring items*:

Adjusted expense

Decreasing expense

$973

$937

$1,006

$23

$17

$5

($28)

($2)

($50)

$968

$952

$961

Managing expenses carefully in response to revenue

environment; continuous process of expense evaluation

Efficiency ratio trend

–

Current impact of credit costs on

revenue and expenses; impact of

regulatory reforms (e.g., debit

interchange) not fully mitigated

–

Reflects below-capacity balance sheet

and lower revenue than we expect and

can support longer term |

10

©

Fifth Third Bank | All Rights Reserved

Credit trends continue to improve

with strong reserve coverage levels

Source: SNL Financial and Company Reports. Data as of 3Q12. HFI NPLs exclude loans

held-for-sale and also exclude covered assets for BBT, USB, and ZION

* HBAN, KEY, PNC, USB, WFC include the implementation of newly issued 3Q12 OCC

guidance which requires write-down of performing consumer loans restructured in bankruptcy to

collateral value. The light blue section indicates the additional charge-offs

due to this guidance. Continued

decline

in

problem

assets

and

corresponding

decline

in

charge-offs

combined

with strong reserves on an absolute and relative basis

NPLs / Loans

Peer average: 1.6%

Loan loss reserves / Loans

Peer average: 2.0%

Net charge-off ratio

Peer average: 0.9%

Reserves / NPLs

Peer average: 131% |

11

Fifth Third Bank | All Rights Reserved

Capital management philosophy

* Subject to Board of Directors and regulatory approval

Organic growth opportunities

•

Support growth of core banking franchise

•

Continued loan growth despite sluggish

economy

Strategic opportunities

*

•

Prudently evaluate franchise including

increasing density in core markets via

disciplined acquisitions or selective de

novos

•

Expect future acquisition opportunities

although activity remains muted in near-term

•

Attain top 3 market position in 65% of

markets or more longer term

Return to more normal dividend policy*

•

Strong levels of profitability would support

higher dividend than current level

•

Move towards levels more consistent with

Fed’s near-term payout ratio guidance of

30%

•

Quarterly dividend increased to $0.10 in

3Q12

Repurchases / Redemptions

*

•

Common share repurchases to limit and

manage growth of excess capital levels

Expect capital philosophy to remain consistent

pending evaluation of results in 2013 CCAR process

Capital Deployment

Capital Return

–

Manage capital in light of regulatory

environment, other alternatives,

maintenance of desired / required buffers,

stock price

–

$600MM of potential repurchases through

1Q13 ($350MM ASR completed in October;

$125MM ASR entered into in November)

•

Redeemed $1.4bn in TruPS in 3Q12 |

12

©

Fifth Third Bank | All Rights Reserved

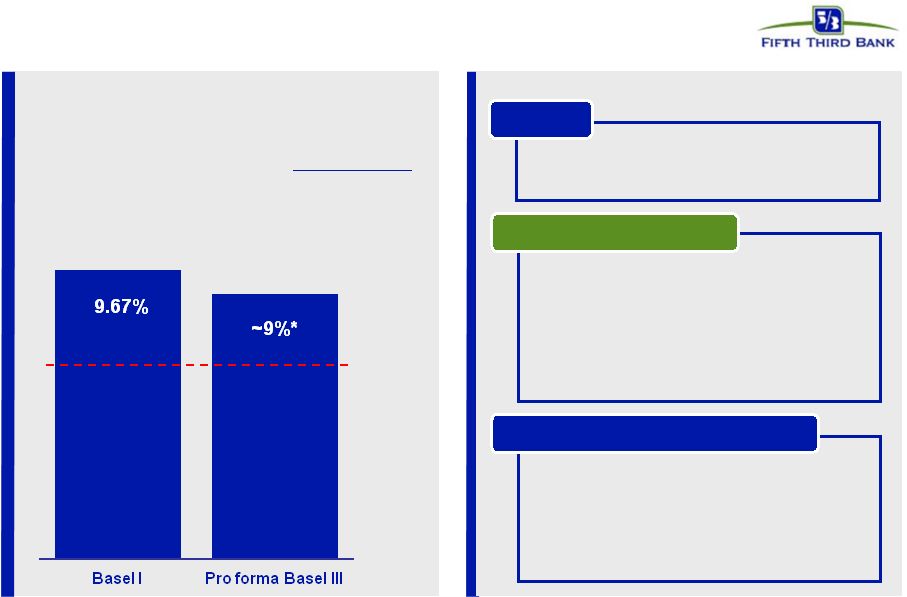

Capital position remains strong

* The pro forma Tier I common equity ratio is management’s estimate based upon

its current interpretation of the three draft Federal Register notices proposing enhancements to regulatory

capital requirements published in June 2012. The actual impact to the

Bancorp’s Tier I common equity ratio may change significantly due to further clarification of the agencies proposals or

revisions to the agencies final rules, which remain subject to public

comment. Proposed new U.S. capital standards would have manageable impact, if

adopted Primary Basel III Adjustments*

Proposed

fully

phased in

buffered

minimum

of 7.0%

Basel III Impacts

•

3Q12 Tier 1 common equity ratio of

9.67% under Basel I

Current

•

Capital impact increase primarily

from inclusion of AOCI

•

RWA increase primarily from 1-4

family senior and junior lien

residential mortgages,

commitments under one year

Estimated NPR Impact

•

Pro forma 3Q12 Tier 1 common

equity ratio of ~9%* under Basel III

•

Does not include the effect of any

mitigating actions Fifth Third may

take

Pro forma Tier 1 Common Equity

NPR Capital Impact

~45 bps +/-

NPR RWA Impact

~(110 bps) +/-

Total Tier 1

Change ~(65 bps) +/-

Tier 1 Common Equity |

13

©

Fifth Third Bank | All Rights Reserved

Fifth Third’s balance sheet and business model

relatively advantaged under new capital standards

Fifth Third’s capital position already well in excess of any established

standards, likely standards, and most peers 5.0%

7.0%

4.5%

Unofficial CCAR supervisory reference minimum

3Q12 Pro forma Tier 1 common / RWA

U.S. proposed Basel III**

3Q12 Tier 1 common / RWA

Basel I

2019 Basel III buffered minimum

2015 Basel III minimum

Not disclosed

High

7%

range

Source: SNL Financial and company reports (financial data as of 3Q12).

* Data sourced form SNL Financial 2Q12. In 2Q12, HBAN stated Basel III Tier 1 common ratio

would be negatively impacted by approximately 150 basis points. ** Note: Fifth

Third’s pro forma Tier I common equity ratio is management’s estimate based upon its current interpretation of the three draft Federal Register notices proposing

enhancements to regulatory capital requirements published in June 2012. The actual impact to

the Bancorp’s Tier I common equity ratio may change significantly due to further

clarification of the agencies proposals or revisions to the agencies final rules, which

remain subject to public comment. Not adjusted for potential mitigation efforts. ^

CMA 3Q12 earnings call stated “Tier 1 capital ratio is estimated to be comfortably above the new 8.5% regulatory standard”.

|

14

Fifth Third Bank | All Rights Reserved

Well-positioned for the future

•

Fifth Third monitors liquidity at the Holding Company over a 24-month period,

and manages liquidity based on the coverage of contractual obligations

without accessing the capital markets or receiving dividends from the Bank entity

•

Fifth Third has completely exited all crisis-era government support

programs Superior capital and liquidity position

•

NCOs of 0.75%; 3.1x reserves / annualized NCOs

•

Substantial reduction in exposure to CRE since 1Q09; relatively low CRE exposure

versus peers •

Very low relative exposure to areas of concern, e.g. European financials, mortgage

repurchase risk Proactive approach to risk management

•

Traditional commercial banking franchise built on customer-oriented localized

operating model •

Strong market share in key markets with focus on further improving density

•

Fee income ~43% of total revenue

Diversified traditional banking platform

•

PPNR has remained strong throughout the credit cycle

•

PPNR substantially exceeds annual net charge-offs (364% PPNR / NCOs^ in

3Q12) •

1.2% ROAA; 13% return on average tangible common equity^

Industry leader in earnings power

^ Non-GAAP measure. See Reg. G reconciliation in the Appendix to the

presentation. –

Fifth Third is one of the few large banks that have no TLGP-guaranteed debt to refinance in

2012 |

15

©

Fifth Third Bank | All Rights Reserved

Cautionary statement

This

report

contains

statements

that

we

believe

are

“forward-looking

statements”

within

the

meaning

of

Section

27A

of

the

Securities

Act

of

1933, as amended, and Rule 175 promulgated thereunder, and Section 21E of the

Securities Exchange Act of 1934, as amended, and Rule 3b-6 promulgated

thereunder. These statements relate to our financial condition, results of operations, plans, objectives, future

performance

or

business.

They

usually

can

be

identified

by

the

use

of

forward-looking

language

such

as

“will

likely

result,”

“may,”

“are

expected to,”

“is anticipated,”

“estimate,”

“forecast,”

“projected,”

“intends to,”

or may include other similar words or phrases such as

“believes,”

“plans,”

“trend,”

“objective,”

“continue,”

“remain,”

or

similar

expressions,

or

future

or

conditional

verbs

such

as

“will,”

“would,”

“should,”

“could,”

“might,”

“can,”

or similar verbs. You should not place undue reliance on these statements, as they

are subject to risks and uncertainties,

including

but

not

limited

to

the

risk

factors

set

forth

in

our

most

recent

Annual

Report

on

Form

10-K.

When

considering

these

forward-looking statements, you should keep in mind these risks and

uncertainties, as well as any cautionary statements we may make. Moreover,

you should treat these statements as speaking only as of the date they are made and based only on information then actually

known to us.

There are a number of important factors that could cause future results to differ

materially from historical performance and these forward- looking

statements. Factors that might cause such a difference include, but are not limited to: (1) general economic conditions and

weakening in the economy, specifically the real estate market, either nationally or

in the states in which Fifth Third, one or more acquired entities and/or the

combined company do business, are less favorable than expected; (2) deteriorating credit quality; (3) political

developments, wars or other hostilities may disrupt or increase volatility in

securities markets or other economic conditions; (4) changes in the interest

rate environment reduce interest margins; (5) prepayment speeds, loan origination and sale volumes, charge-offs and loan

loss provisions; (6) Fifth Third’s ability to maintain required capital levels

and adequate sources of funding and liquidity; (7) maintaining capital

requirements may limit Fifth Third’s operations and potential growth; (8) changes and trends in capital markets; (9) problems

encountered by larger or similar financial institutions may adversely affect the

banking industry and/or Fifth Third; (10) competitive pressures

among

depository

institutions

increase

significantly;

(11)

effects

of

critical

accounting

policies

and

judgments;

(12)

changes

in

accounting policies or procedures as may be required by the Financial Accounting

Standards Board (FASB) or other regulatory agencies; (13)

legislative

or

regulatory

changes

or

actions,

or

significant

litigation,

adversely

affect

Fifth

Third,

one

or

more

acquired

entities

and/or

the

combined

company

or

the

businesses

in

which

Fifth

Third,

one

or

more

acquired

entities

and/or

the

combined

company

are

engaged,

including

the

Dodd-Frank

Wall

Street

Reform

and

Consumer

Protection

Act;

(14)

ability

to

maintain

favorable

ratings

from

rating

agencies;

(15)

fluctuation

of

Fifth

Third’s

stock

price;

(16)

ability

to

attract

and

retain

key

personnel;

(17)

ability

to

receive

dividends

from

its

subsidiaries;

(18)

potentially

dilutive

effect

of

future

acquisitions

on

current

shareholders’

ownership

of

Fifth

Third;

(19)

effects

of

accounting

or

financial

results

of

one

or

more

acquired

entities;

(20)

difficulties

from

the

separation

of

or

the

results

of

operations

of

Vantiv,

LLC from Fifth Third; (21) loss of income from any sale or potential sale of

businesses that could have an adverse effect on Fifth Third’s earnings

and future growth; (22) ability to secure confidential information through the use of computer systems and telecommunications

networks; and (23) the impact of reputational risk created by these developments on

such matters as business generation and retention, funding and

liquidity. You

should

refer

to

our

periodic

and

current

reports

filed

with

the

Securities

and

Exchange

Commission,

or

“SEC,”

for

further

information

on other factors, which could cause actual results to be significantly different

from those expressed or implied by these forward-looking statements.

|

16

Fifth Third Bank | All Rights Reserved

Appendix |

17

Fifth Third Bank | All Rights Reserved

Core funded balance sheet and pricing discipline

•

Deposit-rich core funding mix supports

relatively low cost of funds

–

High percentage of funding base in low cost

transaction deposits and noninterest-

bearing DDA accounts

–

Low reliance on wholesale funding

SOURCE: SNL Financial and Company Reports. Data as of 3Q12

Transaction deposits defined as DDA, NOW and Savings/MMDA accounts; Cost of Funds

defined as interest incurred on interest-bearing liabilities as a percentage of average noninterest-bearing deposits and interest-

bearing liabilities; Transaction deposits/Total deposits presented on an average

basis; DDA/Total deposits presented on end-of-period basis. Transaction

Deposits / Total Deposits Peer average

85%

Cost of Funds

Peer average

0.51%

DDA/Total Deposits

Peer average

32% |

18

Fifth Third Bank | All Rights Reserved

PPNR trend

•

PPNR of $568MM down 11% from 2Q12 levels and

8% from prior year

•

Adjusted PPNR of $593MM, including positive

adjustments totaling $25MM, down 1% sequentially

and 7% year-over-year

—

Including 3Q12 mortgage repurchase reserve

build, PPNR of $617MM

Efficiency ratio

PPNR reconciliation

Pre-tax pre-provision earnings*

($ in millions)

Income before income taxes (U.S. GAAP) (a)

Add: Provision expense (U.S. GAAP) (b)

PPNR (a) + (b)

Adjustments

to

remove

(benefit)

/

detriment^:

In

noninterest

income:

Vantiv IPO gain

Vantiv debt refinancing

Valuation of 2009 Visa total return swap

Vantiv warrants & puts

Valuation of bank premises moved to HFS

Litigation reserve additions in revenue

Sale of certain Fifth Third funds

Securities (gains) / losses

In

noninterest

expense:

Debt extinguishment (gains) / losses

Non-income tax related assessment resolution

Sale of certain Fifth Third funds

Termination of certain borrowing & hedging transactions

Severance expense

FDIC insurance expense

Gain on sale of affordable housing

Litigation reserve additions in expense

Adjusted PPNR

Credit-related

items^^:

In noninterest income

In noninterest expense

Credit-adjusted PPNR**

3Q11

4Q11

1Q12

2Q12

3Q12

$530

$418

$603

$565

$503

87

55

91

71

65

$617

$473

$694

$636

$568

-

-

(115)

-

-

-

-

34

-

-

17

54

19

11

1

(3)

(10)

(46)

(56)

16

-

-

-

17

-

-

-

-

6

-

-

-

-

-

(13)

(26)

(5)

(9)

(3)

(2)

-

-

9

-

26

-

-

(23)

-

-

-

-

-

-

2

28

-

-

-

-

-

-

6

-

-

-

-

-

(9)

-

-

-

-

(8)

(5)

4

19

13

2

-

$637

$531

$582

$596

$593

25

33

14

17

14

45

44

34

40

59

$707

$608

$630

$653

$666

* Non-GAAP measure. See Reg. G reconciliation on pages 23 and 24.

** There are limitations on the usefulness of credit-adjusted PPNR, including the significant

degree to which changes in credit and fair value are integral, recurring components of the

Bancorp’s core operations as a financial institution. This measure has been included herein to

facilitate a greater understanding of the Bancorp’s financial condition. ^ Prior quarters

include similar adjustments. ^^ See page 19 for detailed breakout of credit-related

items. # 61% also excluding $22MM 3Q12 mortgage repurchase reserve build

|

19

Fifth Third Bank | All Rights Reserved

Credit-related costs

In noninterest income ($MM)

In noninterest expense ($MM)

Actual

($ in millions)

3Q11

4Q11

1Q12

2Q12

3Q12

Gain / (loss) on sale of loans

$3

$9

$5

$8

$2

Commercial loans HFS FV adjustment

(6)

(18)

(1)

(5)

(3)

Gain / (loss) on sale of OREO properties

(21)

(22)

(17)

(19)

(11)

Mortgage repurchase costs

(2)

(1)

(2)

(2)

(2)

Total credit-related revenue impact

($25)

($33)

($14)

($17)

($14)

Actual

($ in millions)

3Q11

4Q11

1Q12

2Q12

3Q12

Mortgage repurchase expense

$19

$18

$15

$18

$36

Provision for unfunded commitments

(10)

(6)

(2)

(1)

(2)

Derivative valuation adjustments

4

(5)

(4)

(0)

(2)

OREO expense

7

8

5

5

6

Other problem asset related expenses

25

28

19

19

21

Total credit-related operating expenses

$45

$44

$34

$40

$59

Note: Numbers may not sum due to rounding |

20

Fifth Third Bank | All Rights Reserved

Continued improvement in credit trends

Peer average includes: BBT, CMA, HBAN, KEY, MTB, PNC, RF, STI, USB, WFC, and

ZION Source: SNL Financial and company filings. All ratios exclude loans

held-for-sale and covered assets for peers where appropriate. NPA

ratio vs. peers Net charge-off ratio vs. peers

Loans 90+ days delinquent % vs. peers

Loans 30-89 days delinquent % vs. peers

FITB credit metrics are in line with or better than peers

(7.5%)*

3.8%

before

credit

actions

5.0%*

2.3%

before credit

actions

(HFS transfer)

* 4Q08 NCOs included $800MM in NCOs related to commercial loans moved to held-for-sale; 3Q10

NCOs included $510MM in NCOs related to loans sold or moved to held-for-sale |

21

Fifth Third Bank | All Rights Reserved

Mortgage repurchase overview

3Q12 balances of outstanding claims decreased 24% from 2Q12

—

Within recent range of quarterly volatility

Virtually all sold loans and the majority of new claims relate to

agencies

—

99% of outstanding balance of loans sold

—

82% of current quarter outstanding claims

Majority of outstanding balances of the serviced for others

portfolio relates to origination activity in 2009 and later

Private claims and exposure relate to whole loan sales (no

outstanding first mortgage securitizations)

—

Preponderance of private sales prior to 2006

Repurchase Reserves* ($ in millions)

Outstanding Counterparty Claims ($ in millions)

3Q11

4Q11

1Q12

2Q12

3Q12

Beginning balance

$80

$69

$72

$71

$75

Net reserve additions

20

20

17

20

39

Repurchase losses

(31)

(17)

(17)

(16)

(15)

Ending balance

$69

$72

$71

$75

$99

* Includes reps and warranty reserve ($81MM) and reserve for loans sold with

recourse ($18MM) Note: Numbers may not sum due to rounding

Outstanding Balance of Sold Loans ($ in millions)

Fannie

Freddie

GNMA

Private

Total

2004 and Prior

$778

$3,500

$195

$307

$4,779

2005

274

1,151

49

130

1,605

2006

363

930

48

214

1,556

13%

2007

563

1,517

64

171

2,314

2008

714

1,207

519

-

2,441

2009

1,362

6,498

3,160

1

11,020

2010

3,015

6,768

2,744

-

12,527

2011

3,712

6,844

2,275

-

12,831

2012

3,858

6,830

2,671

-

13,359

Grand Total

$14,638

$35,246

$11,725

$823

$62,432

1.3%

2005-2008 vintages account for ~80% of total life to date

losses of $372MM from sold portfolio

$24MM increase in representation & warranty reserve

resulting from additional information received from

Freddie Mac regarding future mortgage file requests and

repurchase expectations |

22

©

Fifth Third Bank | All Rights Reserved

European Exposure

Total exposure includes funded and unfunded commitments, net of collateral; funded

exposure excludes unfunded exposure Peripheral Europe includes Greece,

Ireland, Italy, Portugal and Spain Other Europe includes European countries

not part of the Euro (primarily the United Kingdom and Switzerland) Data

above includes exposure to U.S. subsidiaries of Europe-domiciled companies

Note: Numbers may not sum due to rounding

•

International exposure primarily related to trade finance and financing activities of

U.S. companies with foreign parent or overseas activities of U.S.

customers •

No European sovereign exposure (total international sovereign exposure $3MM)

•

Total exposure to European financial institutions <$150MM

•

Total exposure to five peripheral Europe countries <$200MM

•

$878MM in funded exposure to Eurozone-related companies (~1% of total loan

portfolio) European Exposure

Total

Funded

Total

Funded

Total

Funded

Total

Funded

exposure

exposure

exposure

exposure

exposure

exposure

exposure

exposure

(amounts in $MM)

Peripheral Europe

-

-

15

-

152

119

167

119

Other Eurozone

-

-

74

74

1,382

759

1,456

833

Total Eurozone

-

-

89

74

1,534

878

1,623

952

Other Europe

-

-

42

32

879

492

921

524

Total Europe

-

-

132

106

2,413

1,369

2,545

1,475

Sovereigns

Financial Institutions

Non-Financial Entities

Total

Eurozone includes countries participating in the European common currency (Euro) |

23

Fifth Third Bank | All Rights Reserved

Regulation G Non-GAAP reconciliation

Fifth Third Bancorp and Subsidiaries

Regulation G Non-GAAP Reconcilation

$ and shares in millions

(unaudited)

September

June

March

December

September

2012

2012

2012

2011

2011

Income before income taxes (U.S. GAAP)

$503

$565

$603

$418

$530

Add:

Provision expense (U.S. GAAP)

65

71

91

55

87

Pre-provision net revenue (a)

568

636

694

473

617

Net income available to common shareholders (U.S. GAAP)

354

376

421

305

373

Add:

Intangible amortization, net of tax

2

2

3

3

3

Tangible net

income available to common shareholders 356

378

424

308

376

Tangible net income available to common

shareholders (annualized) (b) 1,416

1,520

1,705

1,222

1,492

Average Bancorp shareholders' equity (U.S. GAAP)

13,887

13,628

13,366

13,147

12,841

Less:

Average preferred stock

(398)

(398)

(398)

(398)

(398)

Average goodwill

(2,417)

(2,417)

(2,417)

(2,417)

(2,417)

Average intangible assets

(31)

(34)

(38)

(42)

(47)

Average tangible common equity

(c) 11,041

10,779

10,513

10,290

9,979

Total Bancorp shareholders' equity (U.S. GAAP)

13,718

13,773

13,560

13,201

13,029

Less:

Preferred stock

(398)

(398)

(398)

(398)

(398)

Goodwill

(2,417)

(2,417)

(2,417)

(2,417)

(2,417)

Intangible assets

(30)

(33)

(36)

(40)

(45)

Tangible common equity, including

unrealized gains / losses (d) 10,873

10,925

10,709

10,346

10,169

Less: Accumulated other comprehensive income / loss

(468)

(454)

(468)

(470)

(542)

Tangible common equity, excluding unrealized gains /

losses (e) 10,405

10,471

10,241

9,876

9,627

Total assets (U.S. GAAP)

117,483

117,543

116,747

116,967

114,905

Less:

Goodwill

(2,417)

(2,417)

(2,417)

(2,417)

(2,417)

Intangible assets

(30)

(33)

(36)

(40)

(45)

Tangible assets, including

unrealized gains / losses (f) 115,036

115,093

114,294

114,510

112,443

Less: Accumulated other comprehensive income / loss, before tax

(720)

(698)

(720)

(723)

(834)

Tangible assets, excluding unrealized gains / losses

(g) 114,316

114,395

113,574

113,787

111,609

Common shares outstanding (h)

897

919

920

920

920

Net charge-offs (i)

156

181

220

239

262

Ratios:

Return on average tangible common equity (b) / (c)

12.8%

14.1%

16.2%

11.9%

15.0%

Tangible common equity (excluding unrealized gains/losses) (e) / (g)

9.10%

9.15%

9.02%

8.68%

8.63%

Tangible common equity (including unrealized gains/losses) (d) / (f)

9.45%

9.49%

9.37%

9.04%

9.04%

Tangible book value per share (d) / (h)

12.12

11.89

11.64

11.25

11.05

Pre-provision net revenue / net charge-offs (a) / (i)

364%

351%

315%

198%

235%

For the Three Months Ended |

24

©

Fifth Third Bank | All Rights Reserved

Regulation G Non-GAAP reconciliation

Fifth Third Bancorp and Subsidiaries

Regulation G Non-GAAP Reconcilation

$ and shares in millions

(unaudited)

September

June

March

December

September

2012

2012

2012

2011

2011

Total Bancorp shareholders' equity (U.S. GAAP)

$13,718

$13,773

$13,560

$13,201

$13,029

Goodwill and certain other intangibles

(2,504)

(2,512)

(2,518)

(2,514)

(2,514)

Unrealized gains

(468)

(454)

(468)

(470)

(542)

Qualifying trust preferred securities

810

2,248

2,248

2,248

2,273

Other

38

38

38

38

20

Tier I capital

11,594

13,093

12,860

12,503

12,266

Less:

Preferred stock

(398)

(398)

(398)

(398)

(398)

Qualifying trust preferred securities

(810)

(2,248)

(2,248)

(2,248)

(2,273)

Qualifying noncontrolling interest in consolidated subsidiaries

(51)

(51)

(50)

(50)

(30)

Tier I common equity (a)

10,335

10,396

10,164

9,807

9,565

Risk-weighted assets, determined in accordance with

prescribed regulatory requirements

1

(b)

106,858

106,398

105,412

104,945

102,562

Ratio:

Tier I common equity (a) / (b)

9.67%

9.77%

9.64%

9.35%

9.33%

Basel III -

Estimated Tier 1 common equity ratio

September

2012

Tier 1 common equity (Basel I)

$10,333

Add:

Adjustment related to AOCI for AFS securities

507

Estimated Tier 1 common equity under Basel III rules

2

10,840

Estimated risk-weighted assets under Basel III rules

3

120,308

Estimated Tier 1 common equity ratio under Basel III rules

9.01%

(1)

(2)

(3)

For the Three Months Ended

Tier I common equity under Basel III includes the unrealized gains and losses for

AFS securities. Other adjustments include mortgage servicing rights and deferred tax assets subject to threshold

limitations and deferred tax liabilities related to intangible assets.

Key differences under Basel III in the calculation of risk-weighted assets

compared to Basel I include: (1) risk weighting for commitments under 1 year; (2) higher risk weighting for exposures to

residential

mortgage,

home

equity,

past

due

loans,

foreign

banks

and

certain

commercial

real

estate;

(3)

higher

risk

weighting

for

mortgage

servicing

rights

and

deferred

tax

assets

that

are

under

certain

thresholds

as

a

percent

of

Tier

I

capital;

(4)

incremental

capital

requirements

for

stress

VaR;

and

(5)

derivatives

are

differentiated

between

exchange

clearing

and

over-the-counter

and

the

50% risk-weight cap is removed. The estimated Basel III risk-weighted assets

are based upon the Bancorp’s interpretations of the three draft Federal Register notices proposing enhancements to

the regulatory capital requirements that were published in June of 2012. These

amounts are preliminary and subject to change depending on the adoption of final Basel III capital rules by the

Regulatory Agencies.

For the Three

Months Ended

Under the banking agencies’

risk-based capital guidelines, assets and credit equivalent amounts of

derivatives and off-balance sheet exposures are assigned to broad risk categories. The

aggregate dollar amount in each risk category is multiplied by the associated risk

weight of the category. The resulting weighted values are added together, along with the measure for market risk,

resulting in the Bancorp’s total risk-weighted assets.

|