Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - ASSOCIATED BANC-CORP | d441275d8k.htm |

| EX-99.2 - NEWS RELEASE DATED NOVEMBER 13, 2012 - ASSOCIATED BANC-CORP | d441275dex992.htm |

Associated Banc-Corp

Investor Presentation

Bank of America Merrill Lynch

Banking & Financial Services Conference

November 14, 2012

Exhibit 99.1 |

Forward-Looking Statements

Important

note

regarding

forward-looking

statements:

1

Statements made in this presentation which are not purely historical are forward-looking

statements, as defined in the Private Securities Litigation Reform Act of 1995. This includes

any statements regarding management’s plans, objectives, or goals for future operations,

products or services, and forecasts of its revenues, earnings, or other measures of

performance. Such forward-looking statements may be identified by the use of words

such as “believe”, “expect”, “anticipate”, “plan”,

“estimate”, “should”, “will”, “intend”, “outlook”,

or similar expressions. Forward-looking statements are based on current management

expectations and, by their nature, are subject to risks and uncertainties. Actual results may

differ materially from those contained in the forward-looking statements. Factors

which may cause actual results to differ materially from those contained in such

forward-looking statements include those identified in the company’s most recent Form

10-K and subsequent SEC filings. Such factors are incorporated herein by reference. |

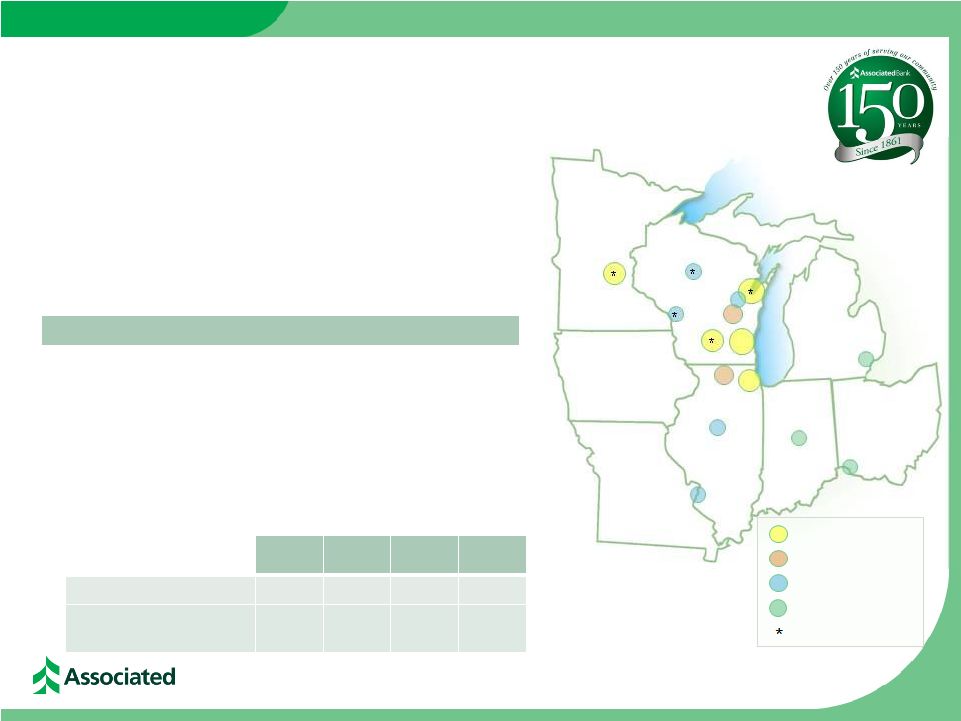

•

Top 50, publicly traded, U.S. bank holding company

•

$23 billion in assets; largest bank headquartered in Wisconsin

–

Over 250 banking offices serving over 150 communities

–

#1 mortgage originator in Wisconsin

–

#1

SBA

lender

in

Wisconsin

Leading Midwest Banking Franchise

1

3

FDIC market share data 6/30/12;

4

Experian State of Credit Survey 2012; FDIC market share data 6/30/12;

5

Source: U.S. BLS, State: Sept. 2012, US: Oct. 2012;

6

Source: FRB Chicago Midwest Manufacturing Index, Sept. 2012.

Operating in Attractive Midwest Markets

WI

MN

IL

U.S.

Unemployment

Rate

4

7.3%

5.8%

8.8%

7.9%

ASBC Deposits

($ in billions)

$11.5

$1.5

$3.7

$16.7

La Crosse

Green Bay

Peoria

Chicago

Madison

Rockford

Neenah

St. Louis

Milwaukee

Wausau

Appleton

Minneapolis

Indianapolis

Cincinnati

Detroit

2

2

1

•

5

of

the

top

10

cities

in

the

U.S

with

highest

credit

score

in

footprint

4

•

WI

&

MN

continue

to

show

above

average

employment

levels

5

•

Midwest

Manufacturing

output

is

up

8.5%

YoY

(vs.

3.5%

nationally)

6

•

Midwest

Machinery

output

is

up

8.1%

YoY

(vs.

3.7%

nationally)

6

Based on 2011 number of funded mortgage loans per HMDA data; ² Based on 2011 FY number of funded SBA loans;

>$1bn

deposits

>$500m

deposits

>$200m

deposits

Commercial

offices

Top

10

credit

score

4

3

3

3 |

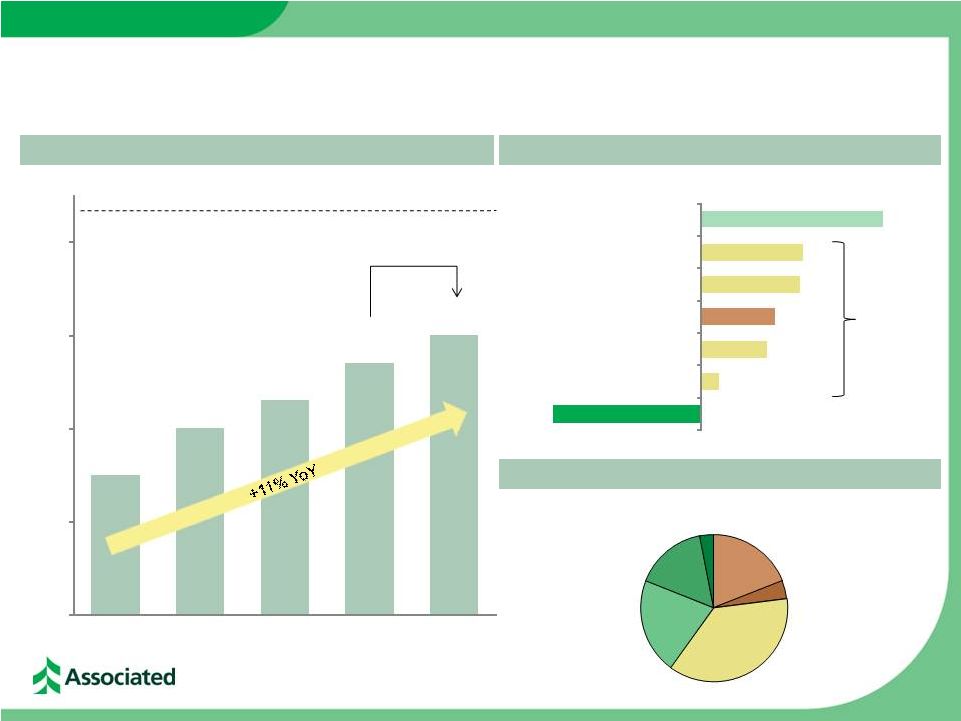

Third

Quarter 2012 Highlights •

Net income available to common shareholders of $45 million or $0.26 per

share •

Return on Tier 1 Common Equity of 9.7%, compared to 7.8% a year ago

Solid Quarterly Performance

Net Income

&

ROT1CE

Loan Growth

Net Interest Income

&

Net Interest Margin

•

Total loans of $15.0 billion were up $267 million, or 2% from the end of the prior

quarter –

Loan balances have increased by $1.5 billion, or 11%, from a year ago

Capital

•

Capital ratios remain very strong with a Tier 1 Common Equity ratio of

12.01% •

Current

capital

levels

are

well

in

excess

of

“well-capitalized”

regulatory

benchmarks

•

Existing capital levels are already above proposed Basel III capital levels

Deposit Growth

•

Average deposits increased by $565 million, or 4%, during the quarter

–

Deposit balances are up $1.2 billion, or 8%, from a year ago

•

Net interest income increased by $2 million from the second quarter to $156

million –

Net interest margin of 3.26%

3 |

•

Continue to examine options for acquisitions while maintaining discipline in

pricing of any transaction •

Branch consolidation transactions with cost take-out opportunities provide

greater value in current environment •

Focused on transactions with lower tangible book value dilution and

shorter-term earn back period Capital Management Priorities and Plans

•

Focus remains on funding organic loan growth across the footprint

•

Supporting business growth initiatives and ongoing capital investments

4

1) Funding Organic Growth

2) Paying a Competitive Dividend

4) Buybacks and Redemptions

•

Completed the redemption of all $180 million of outstanding Trust preferred

securities in the past 45 days •

Announced $125 million share repurchase program to strategically

return capital to shareholders

3) Non-organic Growth Opportunities

•

Increasing quarterly dividend to $0.08/share, effective December

15

–

60% higher dividend than previous $0.05/share |

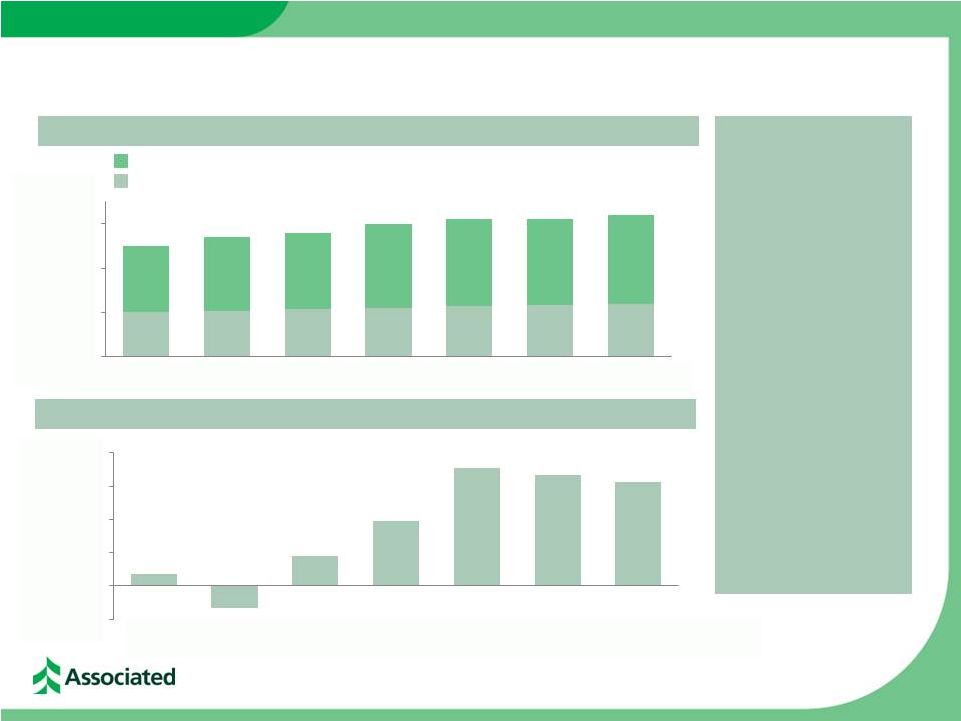

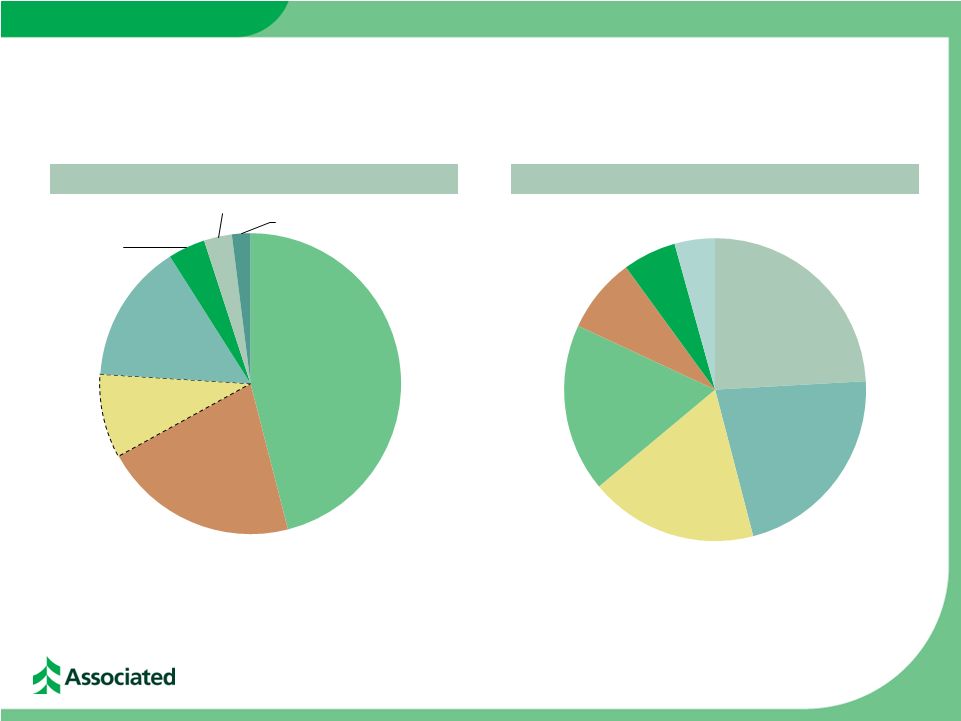

Loan

Portfolio Growth and Composition Total Loans of $15.0 billion at September 30,

2012 3Q 2012 Net Loan Growth of $267 million

Total Loans ($ in billions)

+2% QoQ

Peak Loans (4Q 2008) $16.3 billion

Loan Mix –

3Q 2012

($ balances in millions)

* General commercial loan growth presented here is net of (i.e. reduced by) $75

million Home Equity & Installment

Commercial Real Estate*

Residential Mortgage

Power & Utilities

Oil & Gas

Mortgage Warehouse

General Commercial Loans*

Total

Commercial

Loans

+3% QoQ

of loans which were migrated from investor CRE to owner-occupied during

Q3. * CRE growth shown above is inclusive of the $75 million that was

migrated as referenced above. 5

($101)

$12

$45

$50

$67

$69

$125

$13.5

$14.0

$14.3

$14.7

$15.0

$12.0

$13.0

$14.0

$15.0

$16.0

3Q 2011

4Q 2011

1Q 2012

2Q 2012

3Q 2012

CRE Investor

19%

Construction

4%

Commercial

& Business

Lending

37%

Res Mtg

21%

Home Equity

16%

Consumer

3% |

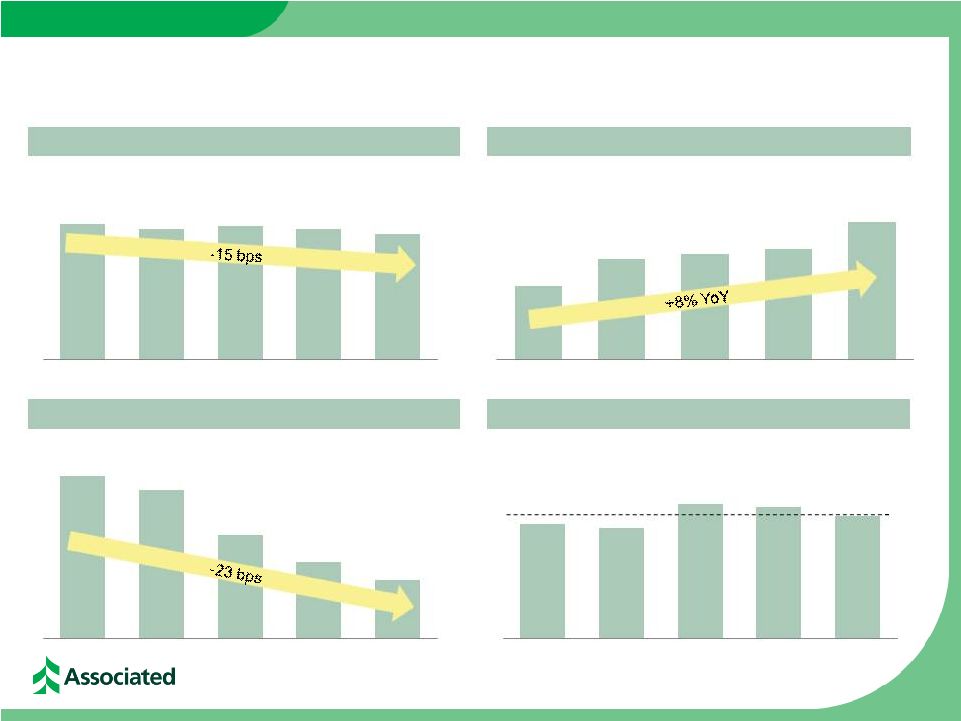

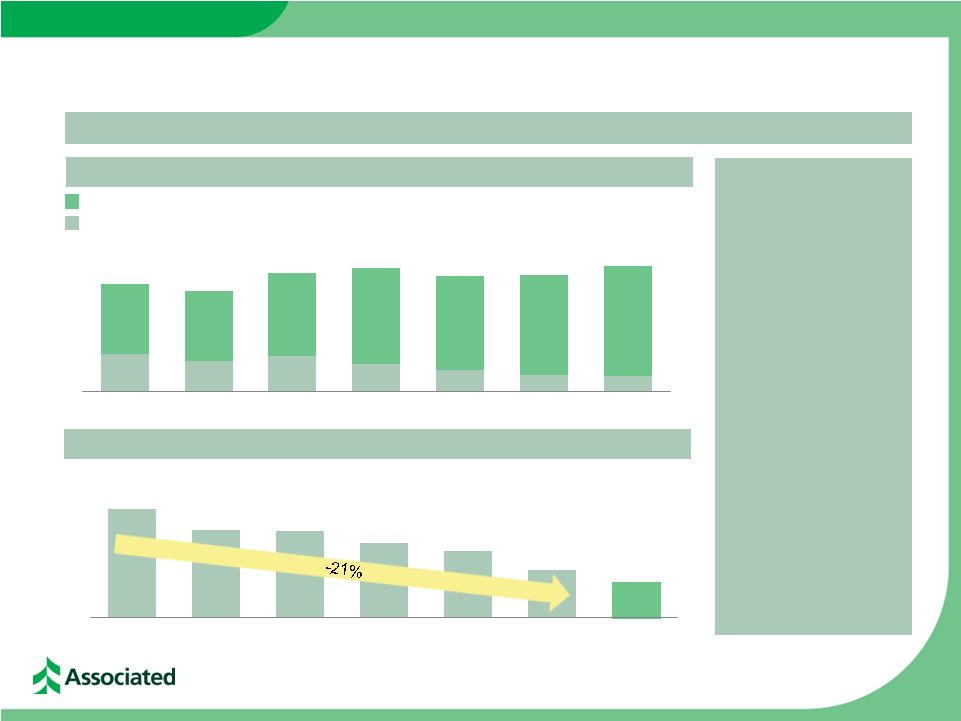

Managing the Cost of Funds & Margin

Yield on Interest-earning Assets

Cost of Interest-bearing Deposits

Average Deposits

Net Interest Margin

($ balances in billions)

6

FY2011:

3.26%

3.88%

3.81%

3.85%

3.80%

3.73%

$14.4

$14.9

$15.0

$15.1

$15.6

0.56%

0.53%

0.43%

0.37%

0.33%

3Q 2011

4Q 2011

1Q 2012

2Q 2012

3Q 2012

3.23%

3.21%

3.31%

3.30%

3.26%

3Q 2011

4Q 2011

1Q 2012

2Q 2012

3Q 2012

3Q 2011

4Q 2011

1Q 2012

2Q 2012

3Q 2012

3Q 2011

4Q 2011

1Q 2012

2Q 2012

3Q 2012 |

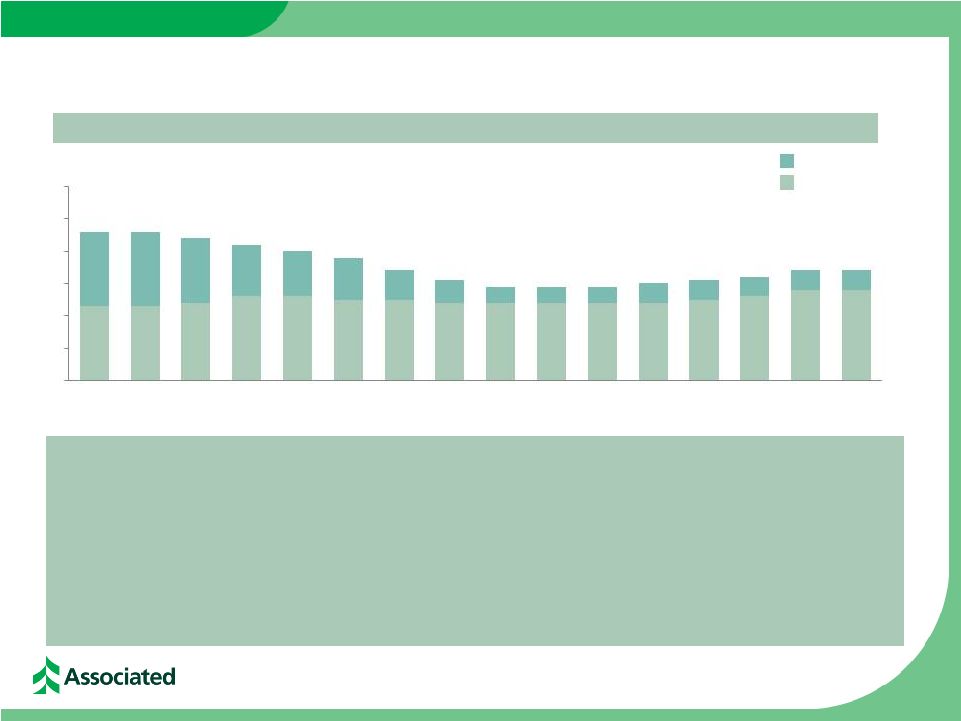

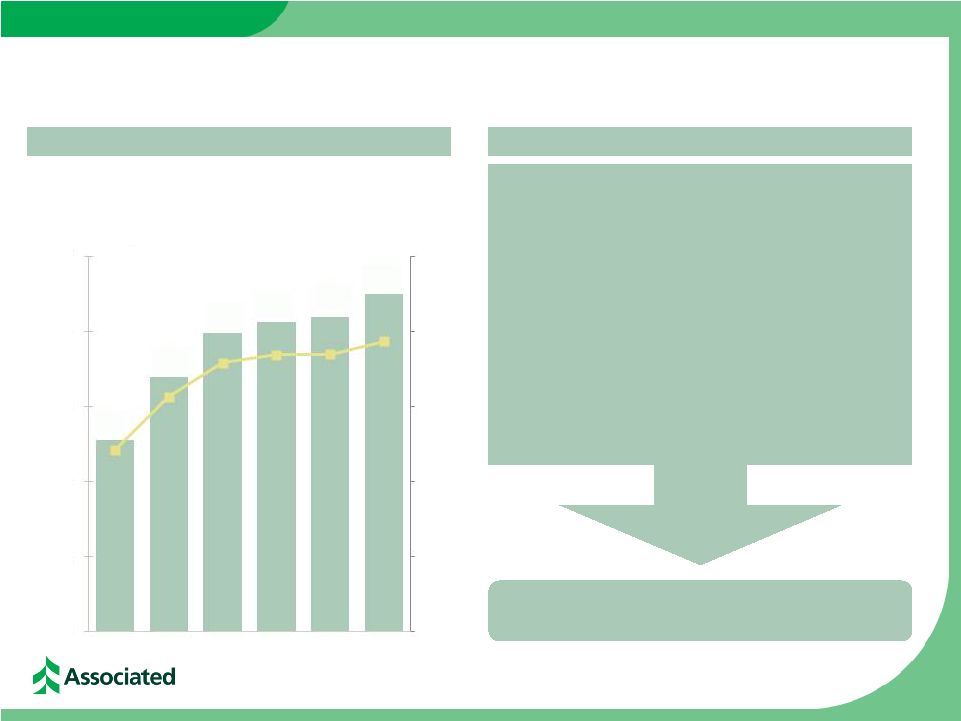

Rebuilding Commercial & Business Lending Portfolio

($ in billions)

7

Highlights

•

Over the past two years we have restored our C&I

lending efforts

•

Competitive disruptions in our markets continue to

provide opportunity for growth into 2013 •

Manufacturing sector remains the cornerstone of our

C&I lending efforts

•

Specialized lending portfolios continue to grow from a

small base

$5.7

$5.5

$5.4

$5.0

$4.7

$4.3

$4.2

$4.2

$4.2

$4.1

$4.3

$4.5

$4.9

$4.9

$5.3

$5.5

$3.5

$4.0

$4.5

$5.0

$5.5

$6.0

4Q

2008

1Q

2009

2Q

2009

3Q

2009

4Q

2009

1Q

2010

2Q

2010

3Q

2010

4Q

2010

1Q

2011

2Q

2011

3Q

2011

4Q

2011

1Q

2012

2Q

2012

3Q

2012

Manufacturing

19%

Other 18%

Finance and

Insurance 12%

Wholesale

Trade 10%

Real

Estate

9%

Retail Trade

7%

Oil & Gas 6%

Health Care and

Social Assistance

5%

Power &

Utilities 5%

Professional,

Scientific, and

Technical Services

4%

Rental and

Leasing Services

4%

Transportation and

Warehousing 2%

CB&L

Loans

by

Industry

–

3Q

2012

Commercial & Business Lending Loans |

Rebuilding Commercial Real Estate Lending Portfolio

($ in billions)

Highlights

•

Over

the

past

several

years

we

have

refocused

our

CRE

efforts

to

emphasize

in-footprint

and

lower

risk

asset

classes

•

Commercial

real

estate

lending

balances

bottomed

out

in

2010

and

have

grown

by

$500

million

since

early

2011,

•

We see continued opportunity to grow commercial real estate in the Upper Midwest

given current market and pricing •

We have added commercial real estate LPO teams in Michigan, Indiana, and Ohio to

provide better regional Commercial Real Estate Lending Loans

8

Construction

CRE

$4.6

$4.6

$4.4

$4.2

$4.0

$3.8

$3.4

$3.1

$2.9

$2.9

$2.9

$3.0

$3.1

$3.2

$3.4

$3.4

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

4Q

2008

1Q

2009

2Q

2009

3Q

2009

4Q

2009

1Q

2010

2Q

2010

3Q

2010

4Q

2010

1Q

2011

2Q

2011

3Q

2011

4Q

2011

1Q

2012

2Q

2012

3Q

2012

however they remain $1.2 billion below peak at 4Q 2008

dynamics

diversification to the portfolio |

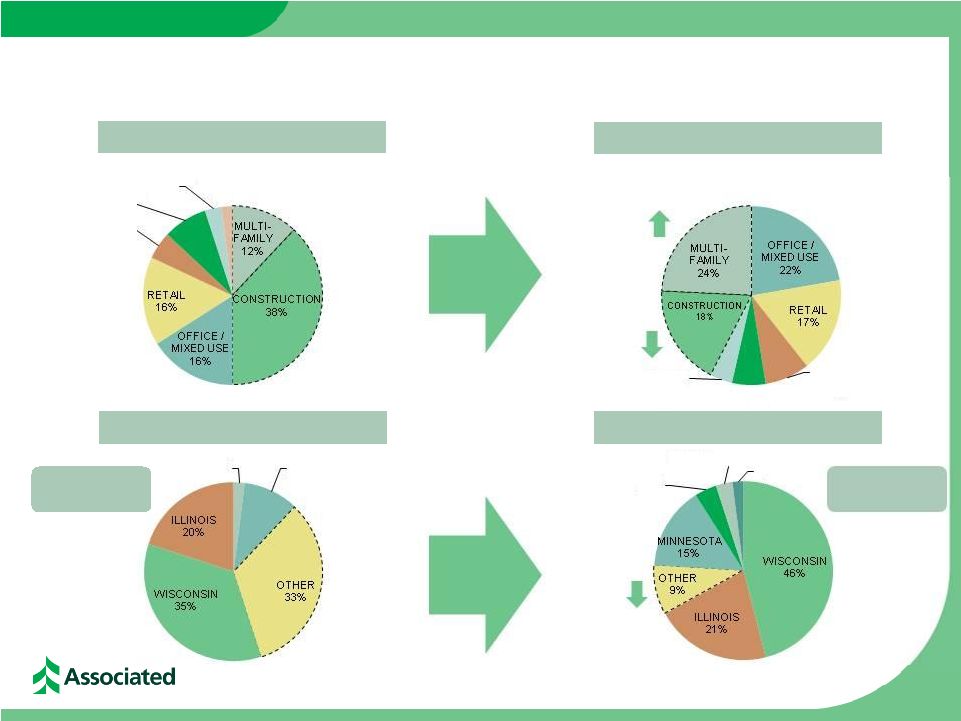

Refocused Commercial Real Estate Activities

9

CRE

/

Construction

–

3Q

2009

CRE

/

Construction

–

3Q

2012

CRE

/

Construction

–

3Q

2009

CRE

/

Construction

–

3Q

2012

67%

“In-footprint”

INDUSTRIAL

5%

OTHER

8%

HOTEL /

MOTEL

3%

SINGLE

FAMILY /

CONDO

2%

INDUSTRIAL

OTHER

HOTEL /

MOTEL

4%

8%

6%

OHIO

4%

MISSOURI

3%

INDIANA

2%

91%

“In-footprint”

MISSOURI

2%

MINNESOTA

10% |

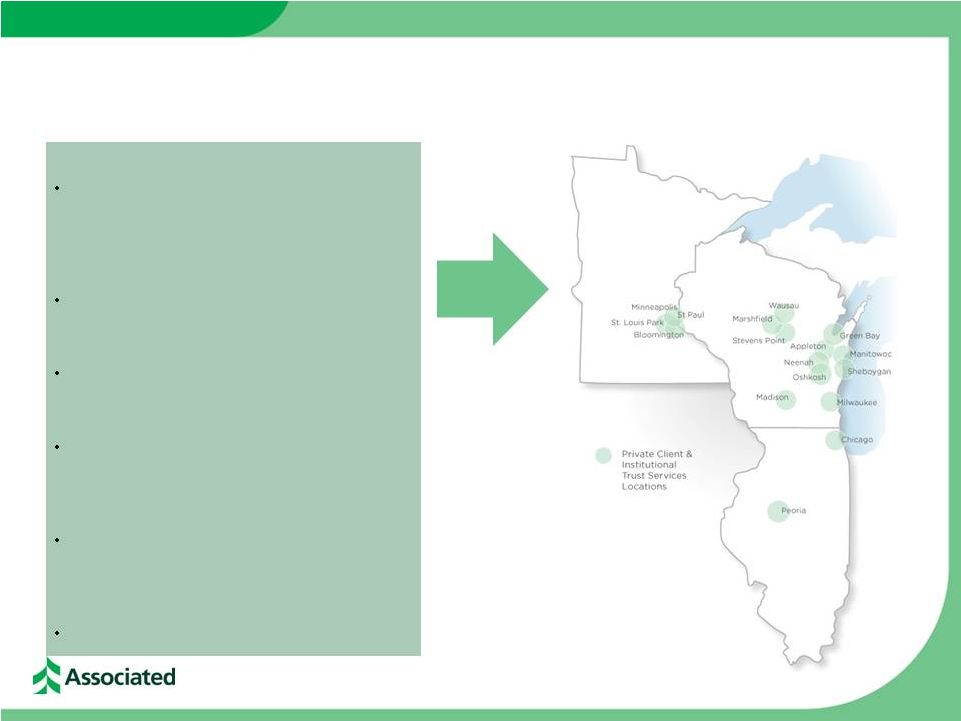

Enhanced Private Client & Institutional Services

10

Hired new Director of Trust (based in

Milwaukee) & Director of Private Banking

(based in Chicago) in order to drive business

growth

New hire strategy focused on team lift-outs

across the footprint (Minneapolis & Chicago)

Created dedicated Private Banking credit team

led by an experienced credit manager

Product and service enhancements for affluent

client base and specialty niches (law &

accounting firm partners)

Strengthening cross-line partnerships between

Trust, Private Banking, Insurance & Commercial

Banking

Over $6.2 billion of assets under management

Highlights |

Strong Mortgage Banking Business

11

Residential Mortgage Loan Portfolio

($ in billions)

Net Mortgage Banking Revenues

($ in millions)

Highlights

•

•

•

•

15-year fixed

Hybrid ARMs (3/5/7)

$2.5

$2.7

$2.8

$3.0

$3.1

$3.1

$3.2

$0.0

$1.0

$2.0

$3.0

1Q 2011

2Q 2011

3Q 2011

4Q 2011

1Q 2012

2Q 2012

3Q 2012

$2

-$3

$5

$10

$18

$17

$16

-$5

$0

$5

$10

$15

$20

1Q 2011

2Q 2011

3Q 2011

4Q 2011

1Q 2012

2Q 2012

3Q 2012

Opened new channels

and expanded into

additional markets

Retaining primarily

hybrid ARMs on balance

sheet as well as ~$1.2

billion of 15-year fixed

product

Selling substantially all

30-year production

Associated remains the

#1 mortgage lender in

Wisconsin (by units &

dollar volume) |

Refinement of Branch Strategy

12

($ in billions)

Non-maturity deposits

Time Deposits

Increasing Deposit Base while Optimizing Traditional Retail Network

Total Deposits & Customer Funding

$15.0

$14.0

$16.6

$17.2

$16.1

$16.3

$17.5

2Q 2007

2Q 2008

2Q 2009

2Q 2010

2Q 2011

2Q 2012

3Q 2012

Number of Branches

315

293

291

279

270

250

238

2Q 2007

2Q 2008

2Q 2009

2Q 2010

2Q 2011

2Q 2012

Pro

forma

-

Highlights

•

Deposits & customer

funding have grown by

$2.5 billion since 2007

•

At the same time, the

total branch count has

been reduced by over

20%

•

Announced plans to

consolidate an

additional 12 branches

in early 2013

•

Planned reformatting of

4 additional full-service

branches to lower cost

delivery channels

•

Focused on continually

evaluating efficiencies

of the branch network

and reviewing branch

delivery channels

|

Footprint Update

13

Example small-format teller line

Continuing To Invest In Our Branches While Optimizing Our Network

Completed the remodel,

relocation, or new

construction of over 30

branches in 2011

50 remodels planned in

2012; completed ~40

branches YTD 2012

YTD 2012 PPE expense

of $59 million includes

ongoing investments in

franchise

Consolidated 21

branches in 1H2012 and

sold three additional

outlying branches in

Jan. 2012

Example in-store remodel

Example small-format teller line

Example traditional remodel

Highlights

Consolidating HQ in

downtown Green Bay

Consolidating Chicago

commercial teams |

Continued Improvement in Credit Quality Indicators

($ in millions)

3Q 2011

4Q 2011

1Q 2012

2Q 2012

3Q 2012

Potential problem loans

$ 660

$ 566

$ 480

$ 410

$ 404

Nonaccruals

$ 403

$ 357

$ 327

$ 318

$ 278

Provision for loan losses

$ 4

$ 1

$ 0

$ 0

$ 0

Net charge offs

$ 30

$ 23

$ 22

$ 24

$ 18

ALLL/Total loans

2.96%

2.70%

2.50%

2.26%

2.11%

ALLL/Nonaccruals

99.09%

105.99%

108.93%

104.65%

113.29%

NPA/Assets

2.03%

1.82%

1.65%

1.62%

1.38%

Nonaccruals/Loans

2.99%

2.54%

2.29%

2.16%

1.86%

NCOs / Avg Loans

0.90%

0.64%

0.61%

0.65%

0.47%

14 |

Why

Associated 15

Net Income

Available to

Common

($ in millions)

Return on Tier 1

Common Equity

Reasons to Invest

Net Income Available to Common & ROT1CE

Management Team Focused on Creating

Long-Term Shareholder Value

•

Leading Midwest Bank Operating in

Attractive Markets

•

Core Organic Growth Opportunity

•

Disciplined Deposit Pricing & Stable Margin

•

Improving Credit Quality

•

Strong Capital Profile Above Basel III

Expectations & Opportunities for Capital

Deployment

•

Improving Earnings Profile

$26

$34

$40

$41

$42

$45

6.1%

7.8%

9.0%

9.2%

9.3%

9.7%

0.00%

2.50%

5.00%

7.50%

10.00%

12.50%

$0

$10

$20

$30

$40

$50

2Q 2011

3Q 2011

4Q 2011

1Q 2012

2Q 2012

3Q 2012 |

Associated

Banc-Corp will be the most admired Midwestern financial services company, distinguished by

sound, value-added financial solutions with personal service for our customers, built upon a

strong commitment to our colleagues and the communities we serve, resulting in exceptional value

for our shareholders. |

Appendix

17 |

18

3Q 2011

4Q 2011

1Q 2012

2Q 2012

3Q 2012

ASBC Capital Ratios

TCE /TA

8.77%

8.84%

9.01%

8.99%

8.91%

Leverage Ratio

9.62%

9.81%

10.03%

9.95%

9.99%

Tier 1 Common Ratio

12.44%

12.24%

12.49%

12.04%

12.01%

Tier 1 Ratio

14.35%

14.08%

14.33%

13.64%

13.57%

Total Capital Ratio

15.81%

15.53%

15.78%

15.08%

15.00%

ABNA Capital Ratios

Leverage Ratio

10.35%

10.56%

10.70%

10.85%

10.65%

Tier 1 Ratio

15.57%

15.23%

15.40%

14.92%

14.69%

Total Capital Ratio

16.84%

16.50%

16.67%

16.18%

15.95%

Maintaining a Strong Capital Profile |

High

Quality Investment Securities Portfolio Market Value Composition –

September 30, 2012

Investment Portfolio –

September 30, 2012

Portfolio Composition Ratings –

September 30, 2012

Risk –

Weighted Profile –

September 30, 2012

Credit Rating

Mkt Value (000’s)

% of Total

Govt & Agency

$ 3,559,632

79%

AAA

14,728

---

AA

778,184

17%

A

136,415

3%

BAA1, BAA2 & BAA3

14,237

---

BA1 & Lower and

Non-rated

14,725

---

TOTAL

$4,517,921

100%

Type

Mkt Value

(000’s)

% of Total

0% RWA

$ 80,684

2%

20% RWA

4,160,596

92%

50% RWA

25,855

1%

=>100% RWA

92,200

2%

Not subject to RW

158,586

3%

TOTAL

$4,517,921

100%

Type

Bk Value

(000’s)

Mkt Value

(000’s)

TEY

(%)

Duration

(Yrs)

Govt &

Agencies

$ 1,010

$ 1,011

0.30

1.88

MBS

2,043,149

2,134,182

3.37

2.47

CMOs

1,338,377

1,356,338

2.66

1.25

CMBS

71,965

74,725

2.70

7.37

Municipals

801,180

848,894

5.50

4.67

Corporates &

Other

101,525

102,771

1.79

1.12

TOTAL AFS

$4,357,206

$4,517,921

3.50

2.41

19

CMOs

30%

MBS

47%

Municipals

19%

CMBS

2%

Corporates

2% |

20

Consumer Loan Portfolios by Geography

(as of September 30, 2012)

Residential Mortgage Loans by State

Home Equity Loans by State

Approximately half of home equity

portfolio is in first-lien position

WISCONSIN

51%

ILLINOIS 32%

MINNESOTA

10%

MISSOURI

4%

OTHER 3%

WISCONSIN 71%

ILLINOIS 16%

MINNESOTA

11%

OTHER 2% |

21

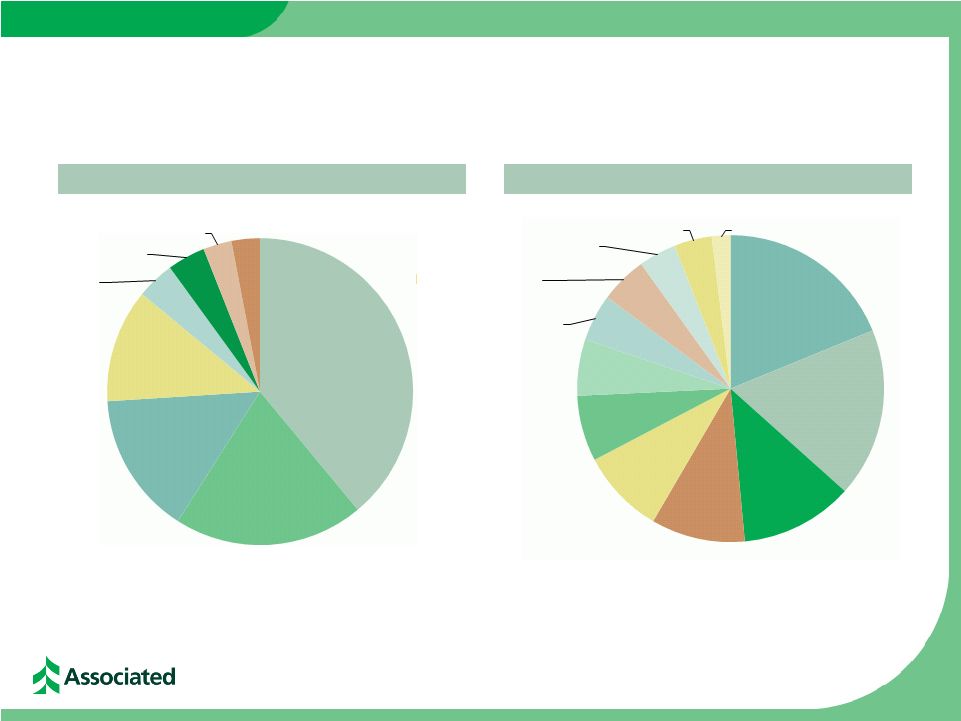

Commercial & Business Lending Loans

(as of September 30, 2012)

Commercial & Business Lending Loans by State

Commercial & Business Lending Loans by Industry

NEW YORK

4%

TEXAS 4%

NORTH

CAROLINA

3%

CALIFORNIA

3%

Health Care and

Social Assistance

5%

Power & Utilities 5%

Professional,

Scientific, and

Technical Services

4%

Rental and Leasing

Services 4%

Transportation and

Warehousing 2%

WISCONSIN

39%

ILLINOIS 20%

MINNESOTA

15%

OTHER 12%

Manufacturing 19%

Other 18%

Finance and

Insurance

12%

Wholesale

Trade 10%

Real Estate

9%

Retail Trade 7%

Oil & Gas 6% |

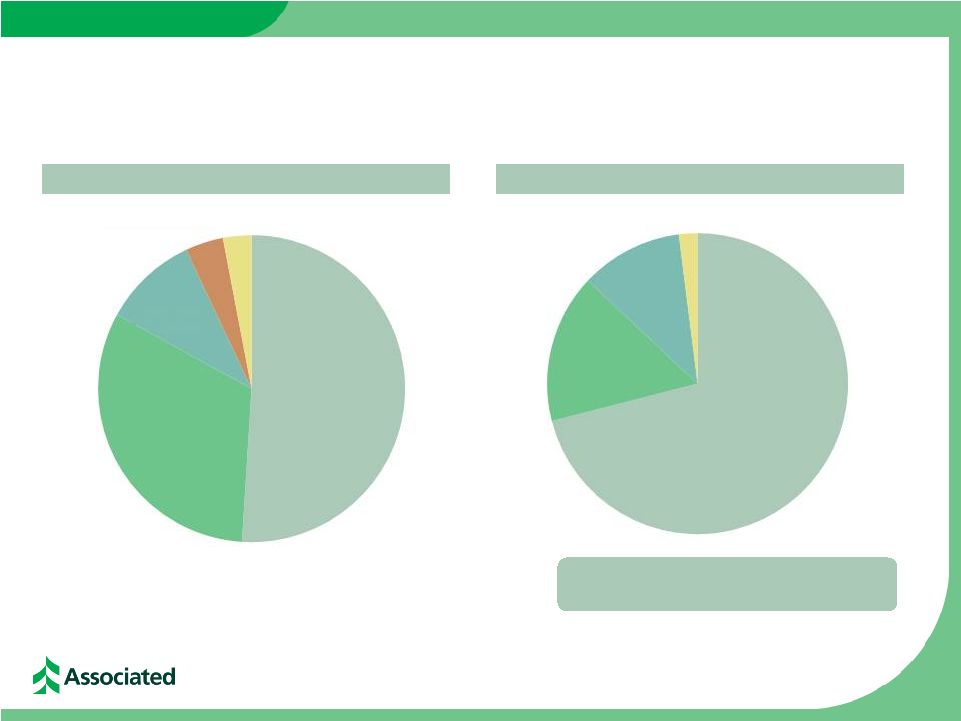

Commercial Real Estate Lending Loans

(as of September 30, 2012)

22

WISCONSIN

46%

ILLINOIS

21%

OTHER

9%

MINNESOTA

15%

OHIO

4%

MISSOURI

3%

INDIANA

2%

MULTI

FAMILY 24%

OFFICE/MIXED USE

22%

RETAIL 18%

CONSTRUCTION

18%

INDUSTRIAL 8%

OTHER 6%

HOTEL/MOTEL 4%

Commercial Real Estate Lending Loans by State

Commercial Real Estate Lending Loans by Collateral

- |