Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT - AMERICAN ELECTRIC POWER CO INC | d438470d8k.htm |

47th EEI

Financial Conference

Handout

Phoenix, AZ

November 12-13, 2012

Exhibit 99.1 |

2

Investor Relations Contacts

Chuck Zebula

Treasurer

SVP Investor Relations

614-716-2800

cezebula@aep.com

“Safe Harbor”

Statement under the Private

Securities Litigation Reform Act of 1995

Bette Jo Rozsa

Managing Director

Investor Relations

614-716-2840

bjrozsa@aep.com

Julie Sherwood

Director

Investor Relations

614-716-2663

jasherwood@aep.com

Sara Macioch

Analyst

Investor Relations

614-716-2835

semacioch@aep.com

This presentation contains forward-looking statements within the meaning of Section 21E of the

Securities Exchange Act of 1934. Although AEP and each of its Registrant Subsidiaries

believe that their expectations are based on reasonable assumptions, any such statements may be

influenced by factors that could cause actual outcomes and results to be materially different

from those projected. Among the factors that could cause actual results to differ materially from those in the forward-looking statements are: the economic climate and growth in, or

contraction within, our service territory and changes in market demand and demographic patterns,

inflationary or deflationary interest rate trends, volatility in the financial markets, particularly

developments affecting the availability of capital on reasonable terms and developments impairing our

ability to finance new capital projects and refinance existing debt at attractive rates, the

availability and cost of funds to finance working capital and capital needs, particularly during

periods when the time lag between incurring costs and recovery is long and the costs are

material, electric load, customer growth and the impact of retail competition, particularly in Ohio,

weather conditions, including storms, and our ability to recover significant storm restoration

costs through applicable rate mechanisms, available sources and costs of, and transportation for,

fuels and the creditworthiness and performance of fuel suppliers and transporters,

availability of necessary generating capacity and the performance of our generating plants, our

ability to resolve cost-related issues regarding I&M’s Donald C. Cook Nuclear Plant Unit 1

restoration and outage through warranty, insurance and the regulatory process, our ability to

recover increases in fuel and other energy costs through regulated or competitive electric rates,

our ability to build or acquire generating capacity, and transmission line facilities (including our

ability to obtain any necessary regulatory approvals and permits) when needed at acceptable

prices and terms and to recover those costs (including the costs of projects that are cancelled)

through applicable rate cases or competitive rates, new legislation, litigation and government

regulation including oversight of nuclear generation, energy commodity trading and new or heightened

requirements for reduced emissions of sulfur, nitrogen, mercury, carbon, soot or particulate

matter and other substances or additional regulation of fly ash and similar combustion products that could impact the continued operation and cost recovery of our plants and

related assets, evolving public perception of the risks associated with fuels used before,

during and after the generation of electricity, including nuclear fuel, a reduction in the federal

statutory tax rate could result in an accelerated return of deferred federal income taxes to

customers, timing and resolution of pending and future rate cases, negotiations and other

regulatory decisions including rate or other recovery of new investments in generation, distribution

and transmission service and environmental compliance, resolution of litigation, our ability

to constrain operation and maintenance costs, our ability to develop and execute a strategy

based on a view regarding prices of electricity, coal, natural gas and other energy-related

commodities, , prices and demand for power that we generate and sell at wholesale, changes in

technology, particularly with respect to new, developing or alternative sources of generation,

our ability to recover through rates or market prices any remaining unrecovered investment in

generating units that may be retired before the end of their previously projected useful lives,

volatility and changes in markets for electricity, natural gas, and other energy-related

commodities, changes in utility regulation, including the implementation of ESPs and the transition to

market and expected legal separation for generation in Ohio and the allocation of costs within

regional transmission organizations, including PJM and SPP, our ability to successfully manage

negotiations with stakeholders and obtain regulatory approval to terminate or amend the

Interconnection Agreement, changes in the creditworthiness of the counterparties with whom we

have contractual arrangements, including participants in the energy trading market, actions of rating

agencies, including changes in the ratings of our debt, the impact of volatility in the capital

markets on the value of the investments held by our pension, other postretirement benefit plans, captive insurance entity and nuclear decommissioning trust and the impact on future

funding requirements, accounting pronouncements periodically issued by accounting standard-setting

bodies and other risks and unforeseen events, including wars, the effects of terrorism

(including increased security costs), embargoes, cyber security threats and other catastrophic events.

|

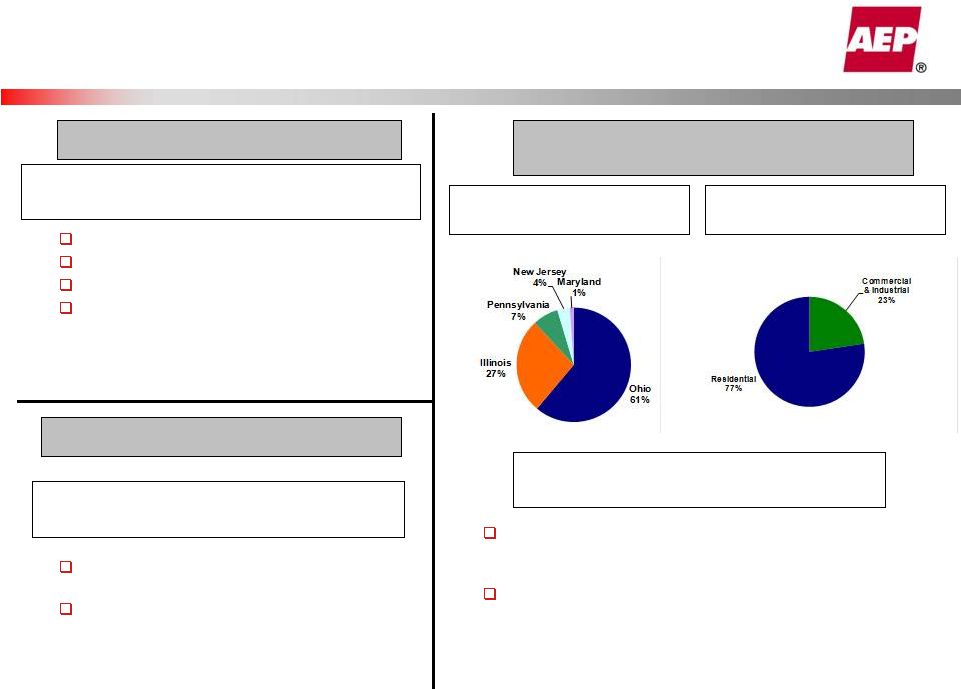

3

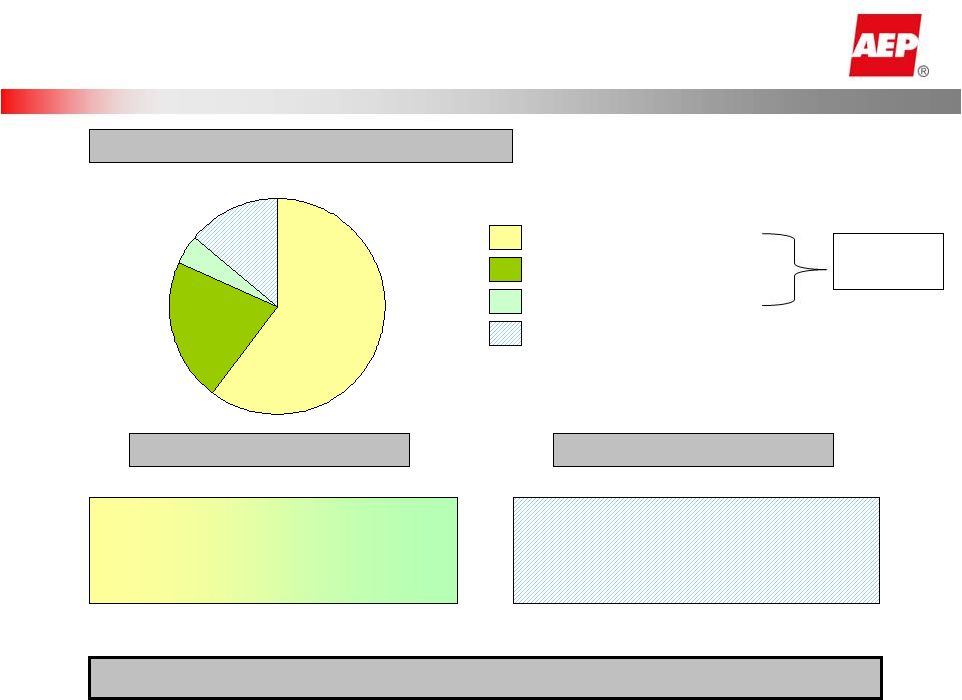

$2.4B,

4%

$33.1B,

61%

$7.6B,

14%

$11.7B,

21%

Projected YE 2014, TOTAL ASSETS

Prudently invest capital for customers

Allocate capital with ROE emphasis

Platform grows earnings 4-6%

Build competitive platform

Manage risks to match regulated profile

Well-positioned generation assets

86% of AEP’s assets are rate regulated

Competitive Objectives

Vertically Integrated Utilities

Competitive Segment

Transcos and Joint Ventures

Wires Only Utilities

86% Rate

Regulated

Regulated Objectives

Framing up the Business: Segment Assets |

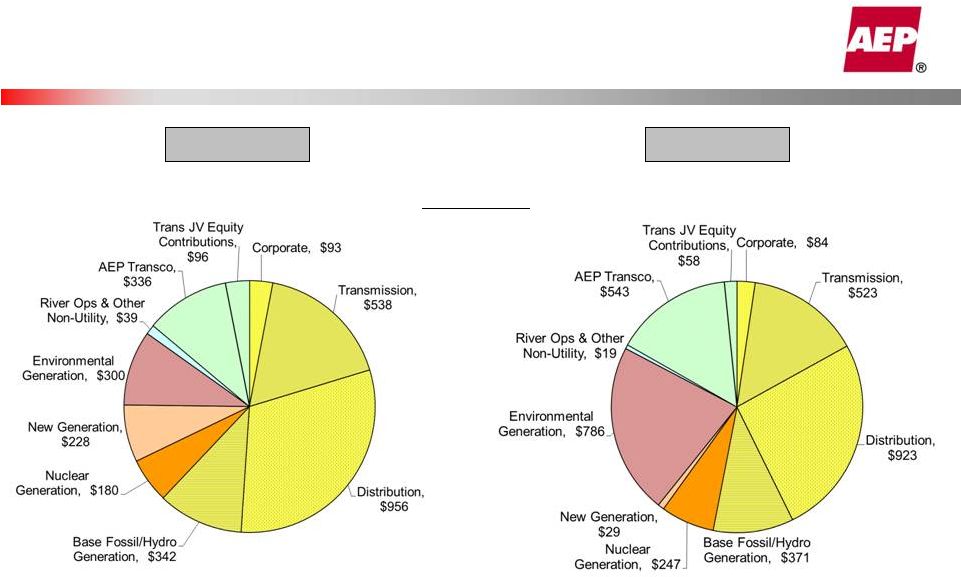

4

$1.3

$2.6

$4.1

$5.3

$0.4

$0.8

$1.0

$1.3

$0.9

$1.7

$2.3

$2.1

$4.3

$6.8

$8.9

$0.4

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

$10

2012E

2013E

2014E

2015E

Regulated Business Growth

Cumulative Change in Regulated Net PP&E

Vertically Integrated Utilities

D and G rate adjustments via base

rate cases with certain tracker

mechanisms for environmental and

reliability investments. T Rate

recovery via trackers in TN, VA, MI.

Others in base rates. ROEs range

from 10.0% to 10.9%.

Transcos

Transcos: Rate recovery via

FERC formula rates. ROEs

11.49% (PJM) / 11.20% (SPP)

Note: 2012 annual regulated depreciation is $1.1B; Transmission

JV investments, other than

Transource, are not reflected above as the ventures are not consolidated on

AEP’s financial statements

2011 Net Regulated PP&E = $32B

6.3% CAGR in Net Regulated PP&E

Wires Companies

TX Wires and Ohio Power Wires.

Rate recovery via trackers or

TCOS in OH and TX. ROEs

range from 9.96% to 11.49%.

Growth in regulated PP&E supports overall earnings growth of 4-6%

|

5

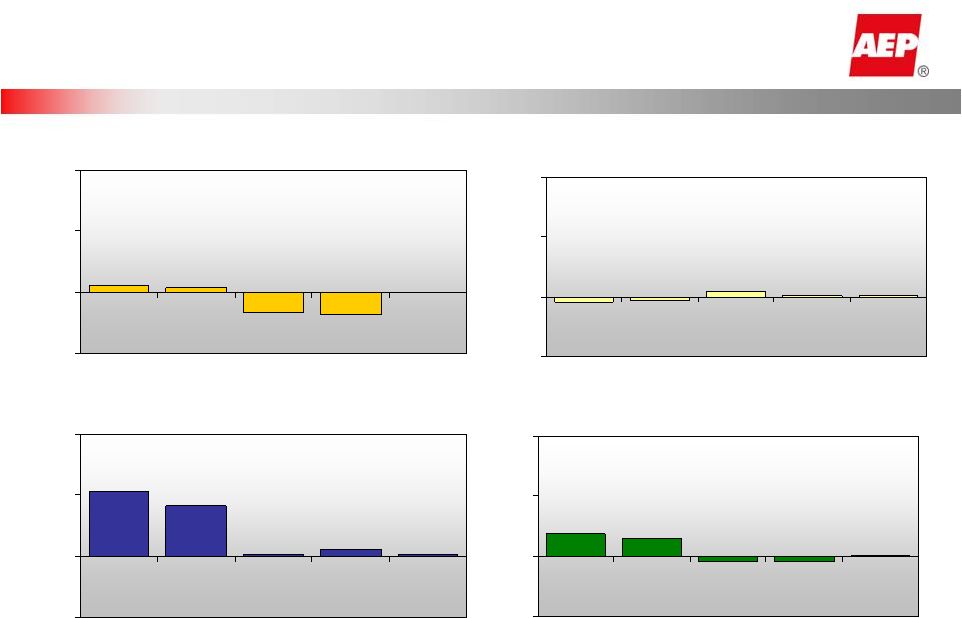

0.1%

-0.4%

-0.4%

1.5%

1.9%

-5%

0%

5%

10%

2010A

2011A

YTD12

2012E

2013E

0.6%

0.4%

-1.7%

-1.9%

0.0%

-5%

0%

5%

10%

2010A

2011A

YTD12

2012E

2013E

-0.4%

-0.3%

0.5%

0.1%

0.1%

-5%

0%

5%

10%

2010A

2011A

YTD12

2012E

2013E

5.3%

4.1%

0.2%

0.6%

0.2%

-5%

0%

5%

10%

2010A

2011A

YTD12

2012E

2013E

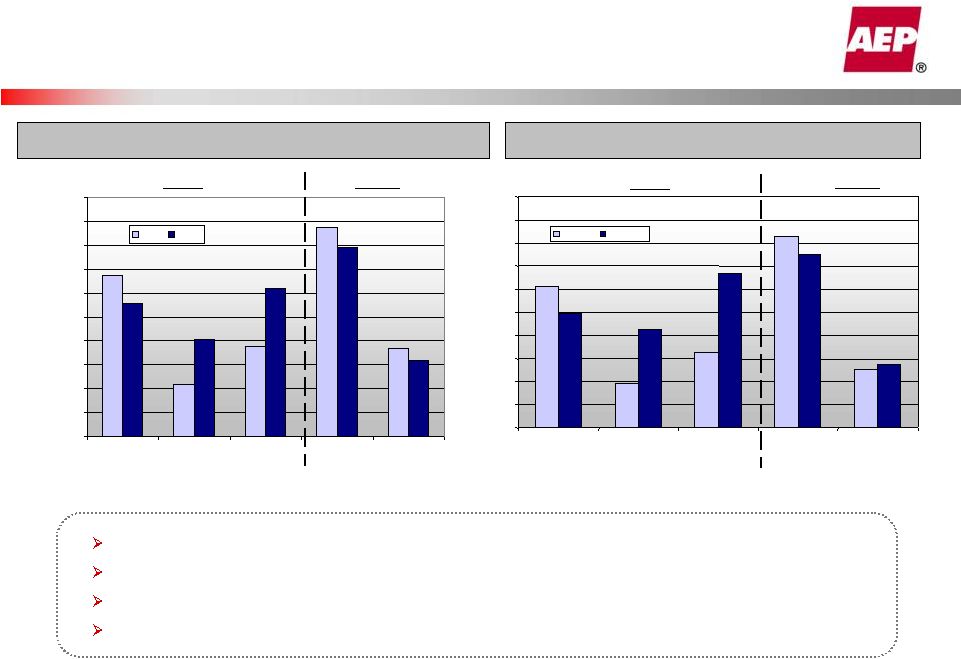

AEP Residential Normalized GWh Sales

%Change vs. Prior Year

AEP Commercial Normalized GWh Sales

%Change vs. Prior Year

AEP Industrial Normalized GWh Sales

%Change vs. Prior Year

AEP Total Normalized GWh Sales

%Change vs. Prior Year

Note: Charts reflect connected load and exclude firm wholesale load & Buckeye

Power backup load. Normalized Retail Load Trends |

6

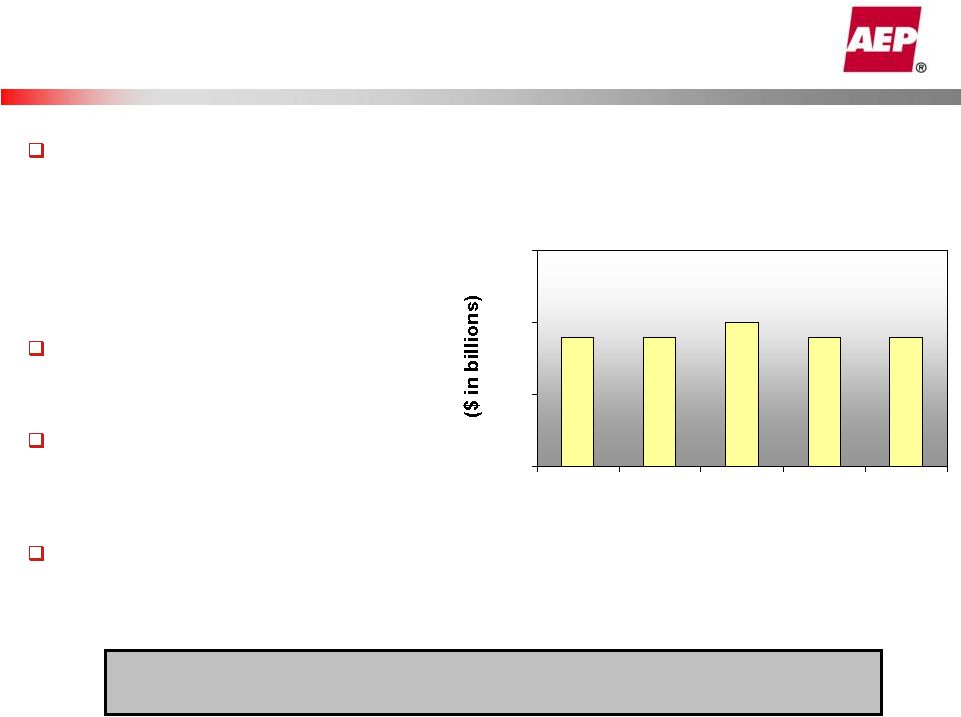

O&M Discipline

Organizational and process

optimization evaluation, including five

‘deep dive’

areas of focus

–

Finance & Accounting

–

Information Technology

–

Procurement/Supply Chain

–

Generation

–

Organizational Effectiveness

Benefits evaluation to align AEP’s

benefits with other companies in the

sector

Analysis complete in the fourth

quarter of 2012 including

development of an integrated plan

and a roadmap for implementation

Management will discuss the results

with the financial community in the

first quarter of 2013

Utility Operations O&M

$3.4

$3.4

$3.5

$2.5

$3.0

$3.5

$4.0

2009A

2010A

2011A

2012E

2013E

Utility Operations O&M expected to remain essentially flat from

2012 to 2013

2012/2013 O&M range

of $3.3 -

3.4B |

7

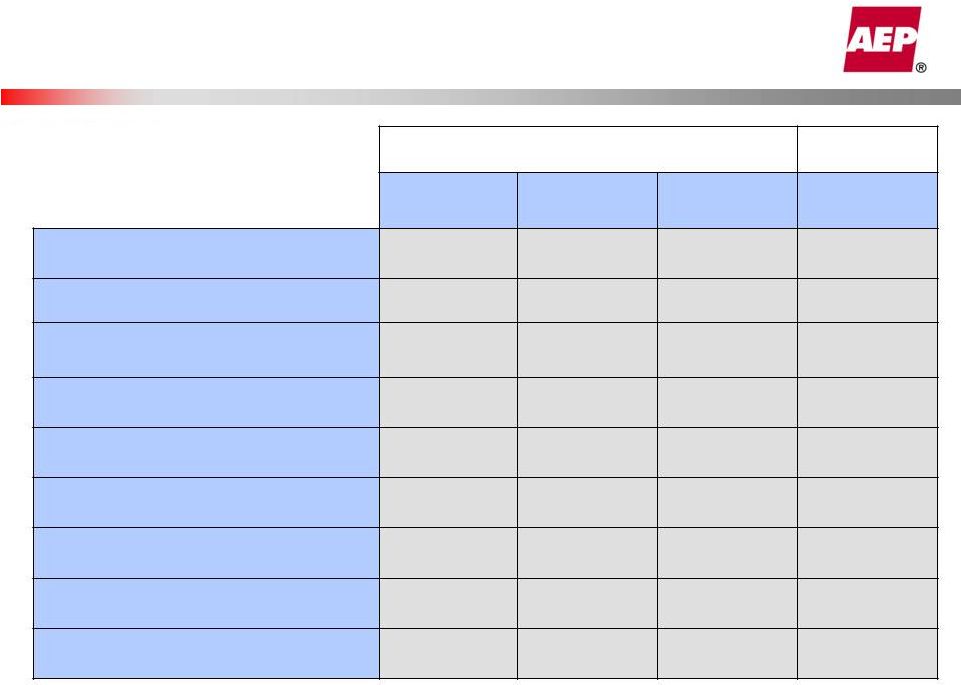

Pending Rate Changes

SWEPCO –

Louisiana: Formula Rate Plan

Filed a request for a 4 year extension of its formula rate update plan, to

include years 2011-

2014. This would encompass recovery for Stall and Turk.

Status:

Docket U-32220;

Staff testimony will be filed November 9, 2012,

Company rebuttal due November 20, hearings scheduled for November 28-

29, and approval is expected in January 2013.

$ in millions

Company

I&M - Indiana

Request

Intervenor Testimony

Rate increase

$140.4

$28

Rate base/investment

$2,391.6

$2,324.5

Return on equity

11.15%

9.20%

Equity component

42.67%

41.956%

Status:

Docket No. 44075. Case filed on September 23, 2011. Hearing on

Case in Chief held February 20 - March 2, 2012. Intervenor testimony filed April

27, 2012. Rebuttal testimony filed May 25, 2012. Hearing held in June 2012.

Anticipate order in 2012.

$ in millions

SWEPCO -

Texas

Company Request

Intervenor/Staff

Testimony

Rate increase

$83.1

n/a

Rate base/investment

$1,199.3

Return on equity

11.25%

Equity component

49.10%

Status:

Docket No. 40443. Case filed on July 27, 2012. Intervenor testimony

due December 10, 2012. Staff testimony due December 17, 2012. Hearing

begins February 3, 2013. Order expected in May 2013, with rates going into

effect retroactive to January 29, 2013. |

8

Transmission Investment Opportunities

Transmission Operations

Capital/JV Equity and EPS Forecast

Transcos

–

11.49% (PJM) / 11.20% (SPP)

ETT

–

9.96%

Prairie

Wind

–

12.8%

2013 Transco

Capital/JV

Contributions

-

$601M

($ in millions)

Authorized ROEs

Ohio, $308

Other

Transcos, $7

Oklahoma,

$100

Joint

Ventures,

$58

Indiana/

Michigan,

$128

Remain on-track to meet investment goals

$432

$601

$716

$718

$0.08

$0.28

$0.14

$0.35

$0

$100

$200

$300

$400

$500

$600

$700

$800

2012E

2013E

2014E

2015E

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

$0.40

$0.45

$0.50

Transco Capital/JV Equity Contributions

EPS Contribution |

9

YTD Sept 2012 Billed Load

(4,793 GWh)

Off-System Sales & Competitive Business

Update

Competitive Retail

(included in Generation & Marketing Segment)

River Operations

Off-System Sales

Sept 30, 2012 Customers

(148,000 customers)

Recent results challenged by economy,

drought and river conditions

Management focused on export

opportunities (coal), and fleeting

infrastructure improvements

CRES

Capacity

Revenues:

$50

–

70M

Trading & Marketing: $45 –

55M

Physical volumes: 35 –

37 GWh

Future results dependent on natural gas

price/heat rate expansion

Retail marketing continues to focus on efforts in Ohio and

our

PJM

footprint

–

to

date,

over

61%

of

competitive

retail

sales volumes are in Ohio

Since October 2011, retail sales under contract increased

by over 60%, up to nearly 14 million MWh

2012 vs. 2013

estimated

growth

of

$0.02

-

$0.04/share

2012 vs. 2013

estimated

decline

of

$(0.03)

-

$(0.05)/share

2012 vs. 2013

estimated

growth

of

$0.01

-

$0.03/share |

10

2012 vs. 2013 Earnings Drivers

Retail Gross Margin:

Normalized Retail Load

(0.04)

(0.06)

Weather

(0.03)

(0.03)

Ohio Customer Switching and Capacity

(2)

( ? )

( ? )

Rate Changes

0.42

0.44

Off-System Sales Margin

(0.05)

(0.03)

Utility O&M Expense

(0.04)

(0.02)

Depreciation Expense

(0.15)

(0.14)

AFUDC and Effective Tax Rate

(0.23)

(0.22)

Interest Expense

0.08

0.09

Transmission Operations

0.06

0.06

River Operations

0.02

0.04

Generation and Marketing

0.01

0.03

EPS Based on 487MM Shares

(1) Preliminary EPS range reflects approximate ranges for key drivers. Not intended

to be a complete year-over-year reconciliation. (2) Unfavorable Ohio

switching impact expected for 2013 vs. 2012; assumption to be provided at 1Q13 analyst meeting

42% switched; 6% in queue as of September 2012

Primarily SWEPCO (Turk), Ohio, Indiana and APCo related rate activity

Preliminary EPS Range

(1)

Comments

East and Ohio down 0.3%; West and Texas up 0.8%

Normal weather assumption

Recovery from drought-impacted operations in 2012

Growth in Competitive Retail

Lower CRES payments and trading; increased physical sales

Includes new operations and effect of repositioning effort

Higher base depreciation; Ohio units depreciated to retirement date

Primarily due to Turk In-Service in December 2012

Debt retirements

Growth in ETT and Transcos |

11

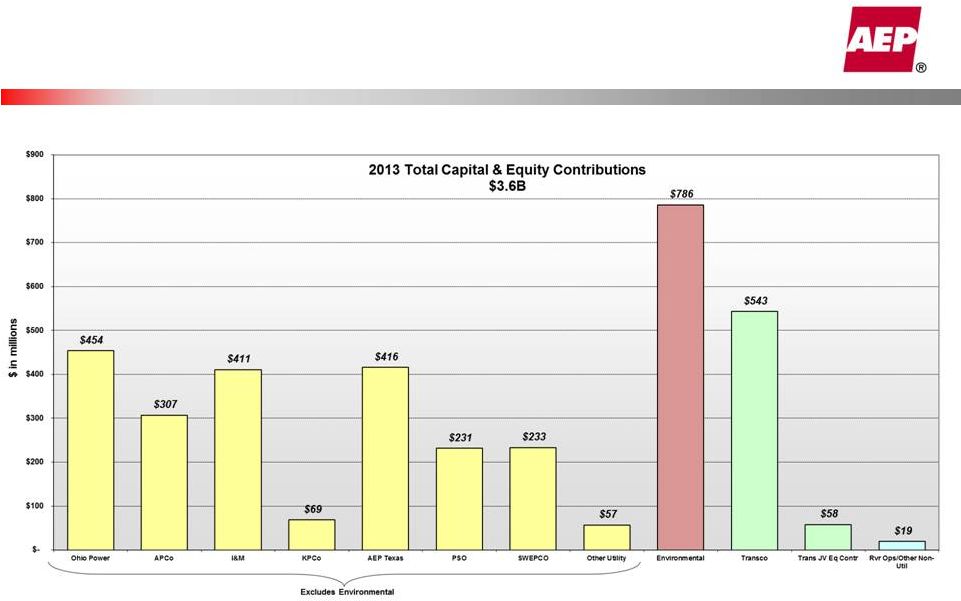

2012 and 2013 Capital & Equity

Contributions

2012: $3.1B

2013: $3.6B

$ in millions |

12

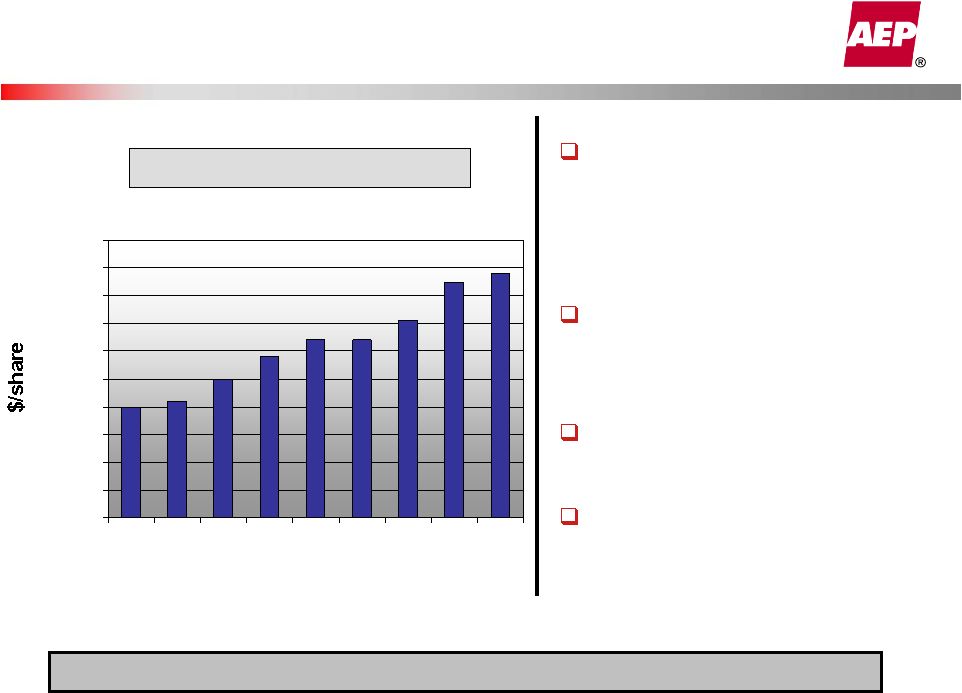

Dividend History and Policy

$1.88

$1.85

$1.71

$1.64

$1.64

$1.58

$1.40

$1.42

$1.50

$1.00

$1.10

$1.20

$1.30

$1.40

$1.50

$1.60

$1.70

$1.80

$1.90

$2.00

2004

2005

2006

2007

2008

2009

2010

2011

2012

Dividend history since 2004

Dividend statistics

-

Current yield -

4.5%

-

Current

quarterly

payment

-

$0.47/share

-

Current

payout

ratio

-

about

60%

-

Growth of 3.8% per annum since 2004

-

Paid 409 consecutive quarters

Recent dividend increases

-

June 2010 –

2.4% increase

-

December

2010

–

9.5%

increase

-

December

2011

–

2.2%

increase

Dividend level supported by

regulated operations earnings

Consolidated dividend payout

ratio target of 50-60%

AEP

is

committed

to

dividend

component

of

total

shareholder

return |

13

Preliminary 2013 Cash Flows

Ohio distribution deferred assets ($300M)

and WV ENEC balance ($400M)

Credit facility established at the parent

level to fund Ohio Power maturities

during the corporate separation transition

Dividend Reinvestment Plan expected to

produce $100M

Balance sheet remains stable at mid-50%

debt to capitalization ratio

$ in millions

2013E

Cash from Operations

3,800

Cash from Securitization

700

Capital & JV Equity Contributions

(3,600)

Other Investing Activities

(215)

Common Dividends

(915)

Excess (Required) Capital

(230)

Financing ($ in millions)

2013E

Excess (Required) Capital

(230)

Debt Maturities (Senior Notes, PCRBs)

(1,649)

Securitzation Amortizations

(300)

Change in STD/Change in Cash

0

Interim Credit Facility*

1,000

Equity Issuances (DRP)

100

Debt Capital Market Needs (New) **

(1,079)

* Interim credit facility range $1.0 - $1.2B (see slide 15)

** New Debt Capital Market Needs for 2013 will be refined based

on timing, form and approval of corporate separation and asset

transfers |

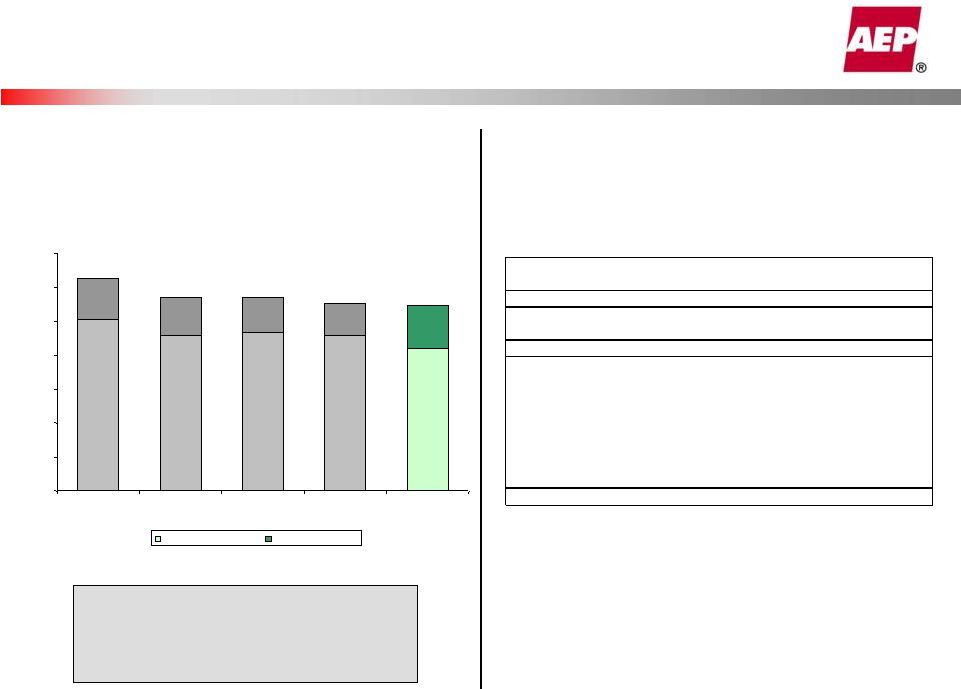

14

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

2008A

2009A

2010A

2011A

3Q2012

Short/Long Term Debt

Securitization Debt

Capitalization & Liquidity

Liquidity Summary (09/30/2012)

62.5%

57.2%

57.0%

55.3%

54.6%

Total Debt / Total Capitalization

Balance sheet remains

stable at mid-50% debt to

capitalization ratio

Liquidity Summary

(unaudited)

Actual

($ in millions)

Amount

Maturity

Revolving Credit Facility

1,750

$

Jul-16

Revolving Credit Facility

1,500

Jun-15

Total Credit Facilities

3,250

Plus

Cash & Cash Equivalents

443

Less

Commercial Paper Outstanding

(520)

Letters of credit issued

(132)

Net available Liquidity

3,041

$

|

15

Ohio Power Recapitalization

(1)

Senior note retirements include the 2013 maturities of $750M, potential to call an

additional $225M of senior notes, intercompany note of $200M and 2014

maturity of $225M. (2)

AEP

plans

to

fund

the

retirements

with

a

combination

of

a

sizeable

term

loan

($1.0

-

$1.2B),

securitization

proceeds, short-term debt and/or cash on hand. The term loan will be

paid with proceeds from permanent financing for AEP Generation

Resources. (3)

Pollution control bond retirements include 2013 mandatory tenders and the

potential to call additional bonds. (4)

$296M of pollution control bonds will remain at Ohio Power but become the

financial responsibility of AEP Generation Resources.

(5)

Further reduction of unsecured debt outstanding may occur once securitization of

the deferred fuel balance from ESP1 occurs (current balance of $536M at

9/30/12). Outstanding Debt

9/30/2012

Debt

Retirements

Ohio Power

Company

Senior Notes

3,350

(1,400)

(1,2)

1,950

Pollution Control Bonds

518

(222)

(2,3)

296

(4)

Debt Outstanding

3,868

2,246

(5) |

16

Securitization Update

Legislation was signed into law in March 2012 with both

the WV Commission and Consumer Advocate office

support for securitization for the large deferred fuel

balances at Appalachian Power.

In June, all parties settled on approximately $312M as

the deferred ENEC balance; however, there are other

items that are included in the application for a total of

approximately $415M, exclusive of financing costs.

The filing for the Financing Order was made in August

2012 and we expect to issue the securitization bonds in

the

1

st

quarter

2013.

In December 2011, the governor signed a bill that allows

Ohio’s electric utilities to utilize securitization as a financing

tool for certain utility assets. AEP Ohio has two separate

securitization opportunities.

Distribution Regulatory Assets

–

In December 2011, the PUCO ordered OPCo to implement

a new rider, the Deferred Asset Recovery Rider (DARR), to

collect certain distribution-related deferred costs, which

meet the requirements for securitization under the new law.

–

OPCo filed its financing application with the PUCO in July

2012 requesting an issuance amount of up to $320M. We

expect

to

issue

the

securitization

bonds

in

the

1

st

quarter

2013.

Deferred

Fuel Regulatory Asset

–

The deferred fuel balance from the 2009-2011 ESP is

currently

being

collected

from

September

2012

–

August

2018.

–

This asset also meets the requirements for securitization,

once a final, nonappealable order is obtained, which we

anticipate in the second half of 2013.

–

The September 30, 2012 deferral balance was $536M.

West Virginia

Ohio |

17

Liability Management (parent debt)

On

December

14,

2012,

AEP,

Inc.

will

repay

the

full

$242,775,000

outstanding

principal balance of its 5.25% Series D Senior Notes (CUSIP: 025537AE1), issued

on May 20, 2003 with a maturity of June 1, 2015 together with accrued

interest and a make-whole premium.

On

December

19,

2012,

AEP,

Inc.

will

repay

the

full

$315,000,000

outstanding

principal balance of its 8.75% Junior Subordinated Debentures (CUSIP: 02557T208),

issued March 20, 2008 with a maturity of March 1, 2063 together with accrued

interest and a make-whole premium.

AEP plans to repay the premium and notes outstanding with typical financings

available to the company ---

such as those available as short-term (commercial

paper and credit facilities) and long-term markets (senior notes at AEP

parent). In the fourth quarter of 2012, pre-tax expenses for the

transaction are expected to be approximately $50M. For 2013 and 2014,

the pre-tax interest savings is expected to be greater than $30M in each

year. |

18

Credit Metrics

* Moody’s/S&P/Fitch ** Includes securitization debt

Trailing Twelve Months 09/30/2012

FFO Interest

Coverage

FFO to Debt

GAAP Debt to

Capitalization

Credit

Ratings*

American Electric Power Company

4.75

19.9%

54.6%

Baa2/BBB/BBB

Appalachian Power Company

3.41

12.6%

56.0%

Baa2/BBB/BBB

Indiana Michigan Power Company

4.79

21.7%

53.8%

Baa2/BBB/BBB

Kentucky Power Company

3.70

18.1%

53.5%

Baa2/BBB/BBB

Ohio Power Company

5.37

24.7%

45.4%

Baa1/BBB/A-

Public Service Company of Oklahoma

7.34

35.7%

50.3%

Baa1/BBB/BBB+

Southwestern Electric Power Company

5.02

24.3%

50.7%

Baa3/BBB/BBB

AEP Texas Central Company

4.90

24.4%

82.4%**

Baa2/BBB/A-

AEP Texas North Company

5.26

21.9%

55.3%

Baa2/BBB/A- |

19

Diversification Supports System Results

Jurisdiction

Authorized Rate

Base

Authorized ROE

9/30/12 Pro-forma Earned

ROE

AEP Ohio - Distribution

$1,912MM

10.20%

AEP Ohio - Transmission

$952MM

11.49%

APCo-Virginia

$2,172MM

10.90%

APCo-West Virginia

$2,428MM

10.00%

KPCo-Kentucky

$995MM

10.50%

11.20%

I&M-Indiana

$2,000MM

10.50%

I&M-Michigan

$663MM

10.20%

PSO-Oklahoma

$1,706MM

10.15%

14.01%

SWEPCO-Louisiana

$649MM

10.57%

SWEPCO-Arkansas

$612MM

10.25%

SWEPCO-Texas

$665MM

10.33%

TCC-Texas

$1,566MM

9.96%

13.62%

TNC-Texas

$530MM

9.96%

12.47%

* - AEP Ohio ROE represents G, T, and D operations

Note: Pro-forma Earned ROEs adjust GAAP results by eliminating any material

nonrecurring items, represent a 12-month rolling calculation and

are not weather normalized 10.23% *

9.49%

7.73%

11.70% |

20

AEP Ohio Regulatory Update

Capacity order received July 2, 2012;

rehearing order received October 17, 2012

ESP 1 fuel deferral (PIRR) order received

August 1, 2012; rehearing order received

October 3, 2012

ESP 2 order received August 8, 2012

Corporate separation order received

October 17, 2012

Rehearings for ESP and corporate separation

orders in process

Corporate separation filings at the FERC

made October 31, 2012 |

21

Corporate Separation Next Steps

Six filings made at FERC

on

October 31, 2012

Three FERC Section 203 Applications

Three FERC Section 205 Applications

Comments due November 30 and

December 17, 2012

Q4

2012

Post

Q4

2012

1/1/2014

Final Settlements and FERC Orders

Corporate Separation of Ohio Power

generation assets

Approval of Power Supply Agreement

between AEP Generation Resources and

Ohio Power

Approval of Power Coordination

Agreement among APCo, I&M and KPCo

(FRR and off-system sales)

Bridge Agreement (interim agreement to

address legacy off-system sales and FRR

obligations)

Transfer of Amos Unit 3 and Mitchell

Generating Facilities to APCo and KPCo

Summary of Key Requests in

FERC Filings:

Approximate Timeline

FERC Settlement Process with State

Commissions and Stakeholders

Execute process, achieve timeline

Corporate Separation rehearing process

complete at PUCO

Target

Q2/Q3

2013

Implementation |

Corporate Separation Transition

Competitive

Operations

Ohio

Power

Current: 2012 -

2013

Transition:

1Q 2014 to May 2015

Market:

post May 2015

Ohio generation remains in four-

company pool

Capacity Order Received

$188.88/MW-day

ESP 2 Order Received

Corporate Separation Order

received (PUCO)

Corporate

Separation filings at FERC

Mid 2013; Delivery begins under

initial 10% of load SSO auction

Grow Retail Business

Hedge Generation

Anticipated FERC approval of

corporate separation effective

1/1/2014 *

Pool agreement modified or

terminated *

Subsequent SSO auctions: 60%

of load on June 1, 2014 and 100%

of load on January 1, 2015

Remaining SSO load served by

AEP Generation Resources *

Ohio generation separated *

Serve remaining OPCo SSO load

via affiliate agreement *

Generation Resources receives

$188.88/MW-day capacity plus

Rate Stability Rider revenue from

Ohio Power

All capacity and energy

available for competitive

operations

SSO for remaining Ohio

Power customers at

auction price for

capacity and energy

* Subject to FERC approval

22 |

23

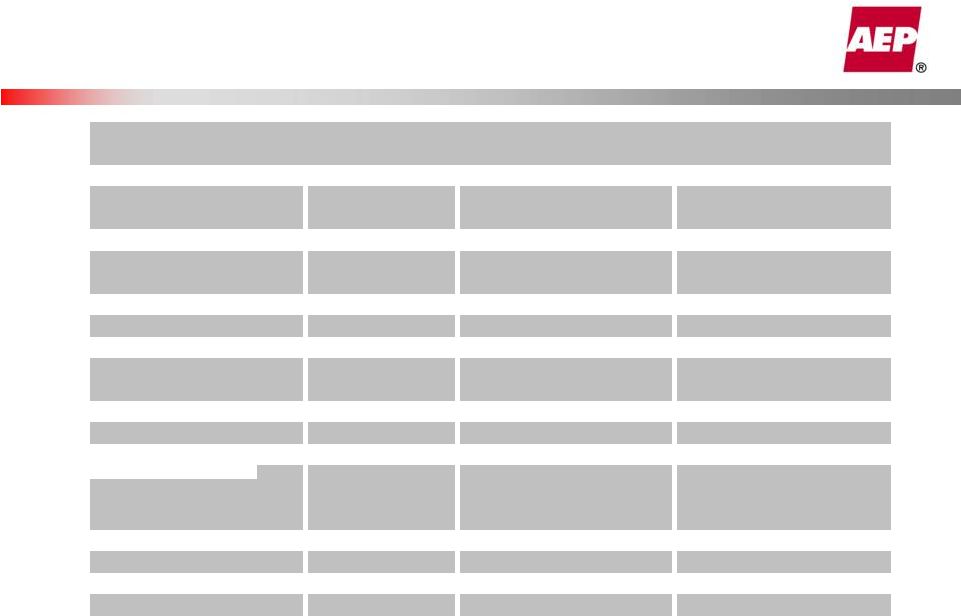

MATS Environmental Investments &

Retirements

Projected Plant Retirements through 2016

Potential Environmental Investments

ACI –

Activated Carbon Injection

DSI –

Dry Sorbent Injection

FGD –

Flue Gas Desulfurization

SCR –

Selective Catalytic Reduction

Operating

Company

Plant

MW

Expected

Retirement

Operating

Company

Plant

MW

Expected

Retirement

APCo

Glen Lyn 5

95

2015

AEP Ohio

Conesville 3

165

2012

Glen Lyn 6

240

2015

Muskingum River 1-4

840

2015

Clinch River 3

235

2015

Picway 5

100

2015

Sporn 1

150

2015

Sporn 2-4

300

2015

Sporn 3

150

2015

Kammer 1-3

630

2015

Kanawha River 1

200

2015

Beckjord

53

2015

Kanawha River 2

200

2015

Total MW

2,088

Total MW

1,270

KPCo

Big Sandy 1

278

2015

I&M

Tanners Creek 1

145

2015

Tanners Creek 2

145

2015

SWEPCO

Welsh 2

528

2014

Tanners Creek 3

205

2015

Total MW

495

PSO

Northeastern 4

465

2016

Total Retirements

5,124MW

=

Operating

Company

Plant

MW

Potential Type of

retrofit

Operating

Company

Plant

MW

Potential Type of

retrofit

AEP Ohio*

Conesville 5

400

ACI, DSI

PSO

Oklaunion

101

FGD upgrade, ACI

Conesville 6

400

ACI, DSI

Northeastern 3****

470

ACI, DSI, Baghouse

Muskingum River 5**

578

Refuel with Natural Gas

SWEPCO

Welsh 1

528

ACI, DSI

APCO

Clinch River 1***

242

Refuel with Natural Gas

Welsh 3

528

ACI, DSI

Clinch River 2***

242

Refuel with Natural Gas

Pirkey

580

FGD Upgrade

Dolet Hills

262

ACI, Baghouse

I&M

Tanners Creek 4

500

DSI, ACI

Flint Creek****

264

FGD, ACI

Rockport****

1,310

FGD, SCR

TNC

Oklaunion

377

FGD upgrade, ACI

KPCO

Big Sandy 2

800

under evaluation

Grand Total MW

7,582

* Assumes investment is able to clear the market

** Existing Coal Plant 585MW

*** Existing Coal Plant 235MW

**** Case on file, subject to regulatory approval |

24

37.6%

87.5%

36.5%

22.0%

67.3%

62.0%

31.7%

78.9%

40.6%

55.8%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

East Coal

East Gas

East Combined

Cycle

West Coal

West Gas

3Q11

3Q12

61.2%

82.7%

42.4%

25.3%

32.7%

19.0%

27.4%

74.9%

49.2%

66.9%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

East Coal

East Gas

East Combined

Cycle

West Coal

West Gas

YTD11

YTD12

Coal to Gas Switching

Overall generation from natural gas has increased over 50 percent

year-to-date East combined cycle statistics include the addition of

the Dresden Plant, which came on line in February 2012 45 days system

average coal inventory at September 30, 2012 Coal fully hedged for

2012; approximately 92% hedged for 2013 West

West

East

East

3rd Quarter 2011 vs. 2012 Capacity Factor

YTD 2011 vs. 2012 Capacity Factor |

25

Capacity Profile

AEP Generation Resources

Fleet Characteristics post 2014

ADVANTAGE

–

River served,

controlled coal and combined cycle

gas represent about 75% of

portfolio

COAL, CONTROLLED

Gavin

2,640

Cardinal

595

Zimmer

330

52%

Stuart

600

OVEC

434

Conesville 4

340

Conesville 5,6 (scrubber only)

800

13%

NATURAL GAS

Lawrenceburg

1,186

Waterford

840

23%

Darby

507

Muskingum River

578

12%

Hydro (Racine)

26

8,876

Combined Cycle, Baseload

Combustion Turbine/Steam, Peaking

River Served, Baseload

Rail/Truck Served, Intermediate

Coal Controlled

Coal Uncontrolled

MR5 Gas Conversion

Gas

Renewables

To Be Transferred

To Be Retired |

26

Pension & OPEB Estimates

Investment returns for our pension plan are

positive for the year, with gains in both the

equity and fixed income segments. OPEB

funds also show positive returns year to date.

AEP made a discretionary contribution of $100

million to the pension plan during the third

quarter of 2012 and plans to make an

additional $100 million discretionary

contribution in 2013.

We expect combined pension and OPEB costs

(O&M and capital) to increase by about $85M

from 2012 to 2013, depending on investment

results and interest rate changes during the

fourth quarter of 2012 and subject to results of

the benefits evaluation.

Estimates for costs and contributions are very

sensitive to changes in interest rates and

investment returns between now and year-end.

Pension Liability Funding

75%

74%

81%

88%

87%

70%

80%

90%

100%

2008

2009

2010

2011

3Q2012

2012

2013E

Pension Discount Rate

4.55%

4.10%

OPEB Discount Rate

4.75%

4.25%

Assumed Long Term

Rate of Return on Assets

7.25%

TBD |

27

2013 AEP System Capital |

28

East & West Normalized Retail Load Trends

East & West Normalized Retail Load Trends

-0.3%

-1.4%

-1.2%

0.7%

1.7%

-5%

0%

5%

10%

2010A

2011A

YTD12

2012E

2013E

East System Total Normalized GWh Sales

%Change vs. Prior Year

R: -0.3%

C: -

0.4%

I: -0.4%

0.8%

1.2%

1.0%

2.8%

2.1%

-5%

0%

5%

10%

2010A

2011A

YTD12

2012E

2013E

West System Total Normalized GWh Sales

%Change vs. Prior Year

R: 0.3%

C: 0.6%

I: 1.8%

Drivers

Weak customer growth

Aggressive DSM mandates

Coal mine curtailed production/closures

Aluminum pot line reductions

Growth in Shale Gas

Drivers

Demographic and Job Growth

Oil & Gas Expansions

Growth in Shale Gas

Auto plant shut down

Note: Charts reflect connected load and exclude firm wholesale load & Buckeye

Power backup load |

29

East Normalized Retail Load Trends

East Normalized Retail Load Trends

1.2%

3.2%

-2.1%

-2.4%

-2.7%

-5%

0%

5%

10%

2010A

2011A

YTD12

2012E

2013E

3.0%

0.2%

0.0%

-0.1%

-1.2%

-5%

0%

5%

10%

2010A

2011A

YTD12

2012E

2013E

AEP Ohio Normalized GWh Sales

%Change vs. Prior Year

I&M Normalized GWh Sales

%Change vs. Prior Year

R: -0.1%

C: 0.0%

I: 2.3%

R: 0.3%

C: -0.6%

I: -6.0%

R: -2.0%

C: -

1.2%

I: -0.5%

2.8%

0.1%

-0.7%

-1.7%

1.9%

-5%

0%

5%

10%

2010A

2011A

YTD12

2012E

2013E

R: 0.1%

C: 0.1%

I: 7.0%

APCo/Wheeling Normalized GWh Sales

%Change vs. Prior Year

1.4%

-2.6%

0.8%

-3.8%

-3.4%

-5%

0%

5%

10%

2010A

2011A

YTD12

2012E

2013E

Kentucky Power Normalized GWh Sales

%Change vs. Prior Year

R: -1.2%

C: 1.7%

I: 2.0%

Note: Charts reflect connected load and exclude firm wholesale load & Buckeye

Power backup load |

30

1.2%

-0.2%

1.9%

1.4%

-0.2%

-5%

0%

5%

10%

2010A

2011A

YTD12

2012E

2013E

West Normalized Retail Load Trends

West Normalized Retail Load Trends

4.9%

5.1%

0.3%

1.6%

0.4%

-5%

0%

5%

10%

2010A

2011A

YTD12

2012E

2013E

1.0%

1.7%

1.7%

3.2%

1.0%

-5%

0%

5%

10%

2010A

2011A

YTD12

2012E

2013E

PSO Normalized GWh Sales

%Change vs. Prior Year

SWEPCO Normalized GWh Sales

%Change vs. Prior Year

AEP Texas Normalized GWh Sales

%Change vs. Prior Year

R: -0.2%

C: -

0.7%

I: 0.1%

R: 1.2%

C: 1.7%

I: 1.8%

R: 0.1%

C: 0.5%

I: 3.1%

Note: Charts reflect connected load and exclude firm wholesale load

Note: 2010 increase due to economic recovery, 2011 due to acquisition of

VEMCO |