Attached files

| file | filename |

|---|---|

| 8-K - 8-K - STONERIDGE INC | v326609_8k.htm |

| EX-99.1 - EXHIBIT 99.1 - STONERIDGE INC | v326609_ex99-1.htm |

1 Stoneridge, Inc . Earnings Release Presentation October 24, 2012 Exhibit 99.2

Statements in this presentation that are not historical facts (including, but not limited to, 2012 net sales guidance) are forward - looking statements, which involve risks and uncertainties that could cause actual events or results to differ materially from those expressed or implied by the statements. Important factors that may cause actual results to differ materially from those in the forward - looking statements include, among other factors, the loss or bankruptcy of a major customer; the costs and timing of facility closures, business realignment or similar actions; a significant change in medium - and heavy - duty truck, automotive or agricultural and off - highway vehicle production; our ability to achieve cost reductions that offset or exceed customer - mandated selling price reductions; a significant change in general economic conditions in any of the various countries in which Stoneridge operates; labor disruptions at Stoneridge’s facilities or at any of Stoneridge’s significant customers or suppliers; the ability of suppliers to supply Stoneridge with parts and components at competitive prices on a timely basis; the amount of Stoneridge’s indebtedness and the restrictive covenants contained in the agreements governing its indebtedness, including its asset - based credit facility and senior secured notes; customer acceptance of new products; capital availability or costs, including changes in interest rates or market perceptions; the failure to achieve successful integration of any acquired company or business; the occurrence or non - occurrence of circumstances beyond Stoneridge’s control; and the items described in “Risk Factors” and other uncertainties or risks discussed in Stoneridge’s periodic and current reports filed with the Securities and Exchange Commission. Important factors that could cause the performance of the commercial vehicle and automotive industry to differ materially from those in the forward - looking statements include factors such as (1) continued economic instability or poor economic conditions in the United States and global markets, (2) changes in economic conditions, housing prices, foreign currency exchange rates, commodity prices, including shortages of and increases or volatility in the price of oil, (3) changes in laws and regulations, (4) the state of the credit markets, (5) political stability, (6) international conflicts and (7) the occurrence of force majeure events. Forward Looking Statements

Forward Looking Statements ( con’t ) These factors should not be construed as exhaustive and should be considered with the other cautionary statements in Stoneridge’s filings with the Securities and Exchange Commission. Forward - looking statements are not guarantees of future performance; Stoneridge’s actual results of operations, financial condition and liquidity, and the development of the industry in which Stoneridge operates may differ materially from those described in or suggested by the forward - looking statements contained in this presentation. In addition, even if Stoneridge’s results of operations, financial condition and liquidity, and the development of the industry in which Stoneridge operates are consistent with the forward - looking statements contained in this presentation, those results or developments may not be indicative of results or developments in subsequent periods. This presentation contains time - sensitive information that reflects management’s best analysis only as of the date of this presentation. Any forward - looking statements in this presentation speak only as of the date of this presentation, and Stoneridge undertakes no obligation to update such statements. Comparisons of results for current and any prior periods are not intended to express any future trends or indications of future performance, unless expressed as such, and should only be viewed as historical data. Stoneridge does not undertake any obligation to publicly update or revise any forward - looking statement as a result of new information, future events or otherwise, except as otherwise required by law.

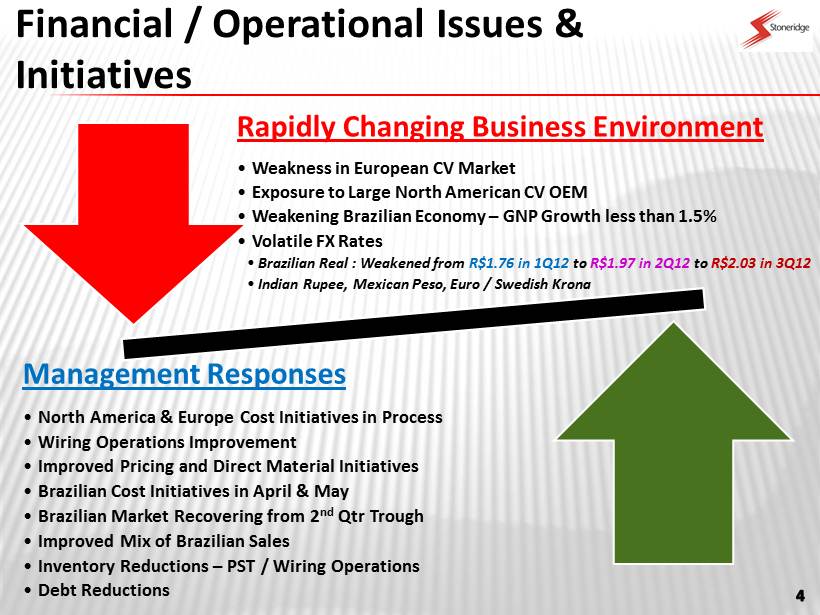

Financial / Operational Issues & Initiatives Rapidly Changing Business Environment • Weakness in European CV Market • Exposure to Large North American CV OEM • Weakening Brazilian Economy – GNP Growth less than 1.5% • Volatile FX Rates • Brazilian Real : Weakened from R$1.76 in 1Q12 to R$1.97 in 2Q12 to R$2.03 in 3Q12 • Indian Rupee, Mexican Peso, Euro / Swedish Krona Management Responses • North America & Europe Cost Initiatives in Process • Wiring Operations Improvement • Improved Pricing and Direct Material Initiatives • Brazilian Cost Initiatives in April & May • Brazilian Market Recovering from 2 nd Qtr Trough • Improved Mix of Brazilian Sales • Inventory Reductions – PST / Wiring Operations • Debt Reductions

3Q11 SRI Core PST Ops PST PPA SRI $ % Net Sales 195.9 175.5 43.8 0.0 219.3 23.4 11.9% Total Cost of Goods Sold 158.4 142.0 25.7 0.3 168.0 9.6 6.1% Gross Profit 37.5 33.5 18.0 (0.3) 51.2 13.8 36.8% Gross Margin % 19.1% 19.1% 41.2% 23.4% Total Selling, General & Admin 30.5 29.1 14.2 1.3 44.6 14.2 46.5% SGA % to Sales 15.5% 16.6% 32.3% 20.4% Operating Income 7.0 4.4 3.9 (1.7) 6.6 (0.4) (5.5)% Operating Margin % 3.6% 2.5% 8.9% 3.0% 3Q12 SRI Variance Sales, Gross Profit, & Op Income – 3Q11 vs 3Q12 175.5 142.0 33.5 29.1 4.4 43.8 26.1 17.7 15.5 2.2 0% 20% 40% 60% 80% 100% Sales COGS GP SGA Op Income Core PST

2Q12 SRI Core PST Ops PST PPA SRI $ % Net Sales 234.3 175.5 43.8 0.0 219.3 (15.0) (6.4)% Total Cost of Goods Sold 180.6 142.0 25.7 0.3 168.0 (12.6) (7.0)% Gross Profit 53.7 33.5 18.0 (0.3) 51.2 (2.4) (4.5)% Gross Margin % 22.9% 19.1% 41.2% 23.4% Total Selling, General & Admin 52.0 29.1 14.2 1.3 44.6 (7.4) (14.3)% SGA % to Sales 22.2% 16.6% 32.3% 20.4% Operating Income 1.6 4.4 3.9 (1.7) 6.6 5.0 309.0% Operating Margin % 0.7% 2.5% 8.9% 3.0% 3Q12 SRI Variance Sales, Gross Profit, & Op Income – 2Q12 vs 3Q12 175.5 142.0 33.5 29.1 4.4 43.8 26.1 17.7 15.5 2.2 0% 20% 40% 60% 80% 100% Sales COGS GP SGA Op Income Core PST

2Q12 vs 3Q12 EPS Bridge PST Impacts SRI Core TOTAL Volume 0.05 (0.26) (0.21) Mix / Direct Material 0.03 0.04 0.07 FX 0.05 0.00 0.05 SGA Drop / Cost Reduction 0.00 0.14 0.14 PST Cost Reduct / Purchase Acctg 0.10 0.00 0.10 TOTAL 0.23 (0.08) 0.15 0.02 0.10 0.14 0.05 0.07 (0.21) (0.13) 3Q12 Actual EPS PST Cost Reduct / Purchase Acctg SGA Drop / Cost Reduction FX Mix / Direct Material Volume 2Q12 Actual EPS

Purchase Price Accounting Expense [Non Cash] (millions) Q1 Q2 Q3 Q4 Full Year 2012 COGS / DM Inventory Write Up $1.8 $1.4 $0.0 $0.0 $3.2 COGS / Depreciation – Fixed Asset Write Up $0.4 $0.3 $0.3 $0.3 $1.3 SGA / Amortized Intangibles $1.0 $1.1 $1.4 $1.7 $5.2 TOTAL $3.2 $2.8 $1.7 $2.0 $9.7 Q1 Q2 Q3 E Q4 E 2012 E Impact on Op Margin 1.22% 1.20% 0.78% 0.85% 1.03% Impact on EPS $(0.06) $(0.05) $(0.03) $(0.04) $(0.18)

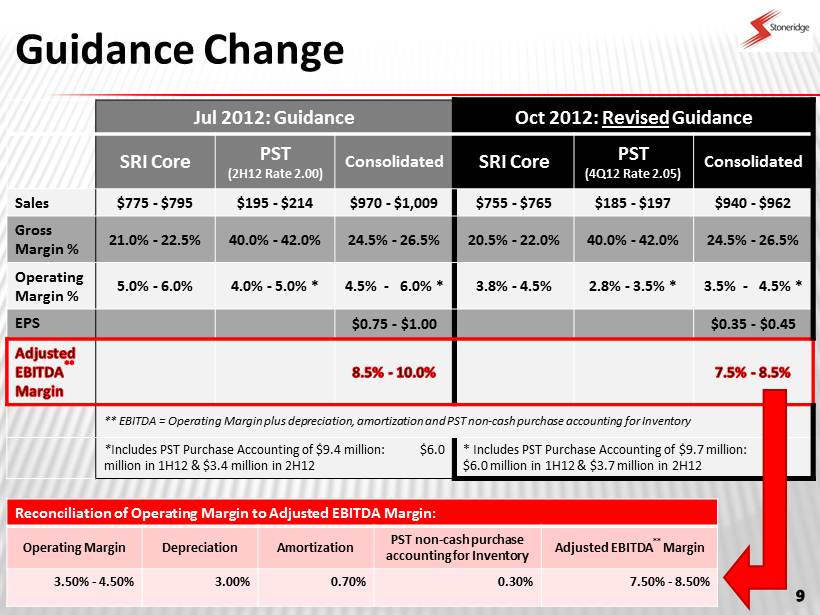

Guidance Change Jul 2012: Guidance Oct 2012: Revised Guidance SRI Core PST (2H12 Rate 2.00) Consolidated SRI Core PST (4Q12 Rate 2.05) Consolidated Sales $775 - $795 $195 - $214 $970 - $1,009 $755 - $765 $185 - $197 $940 - $962 Gross Margin % 21.0% - 22.5% 40.0% - 42.0% 24.5% - 26.5% 20.5% - 22.0% 40.0% - 42.0% 24.5% - 26.5% Operating Margin % 5.0% - 6.0% 4.0% - 5.0% * 4.5% - 6.0% * 3.8% - 4.5% 2.8% - 3.5% * 3.5% - 4.5% * EPS $0.75 - $1.00 $0.35 - $0.45 ** EBITDA = Operating Margin plus depreciation, amortization and PST non - cash purchase accounting for Inventory * Includes PST Purchase Accounting of $9.4 million: $6.0 million in 1H12 & $3.4 million in 2H12 * Includes PST Purchase Accounting of $9.7 million: $6.0 million in 1H12 & $3.7 million in 2H12 Reconciliation of Operating Margin to Adjusted EBITDA Margin: Operating Margin Depreciation Amortization PST non - cash purchase accounting for Inventory Adjusted EBITDA ** Margin 3.50% - 4.50% 3.00% 0.70% 0.30% 7.50% - 8.50%

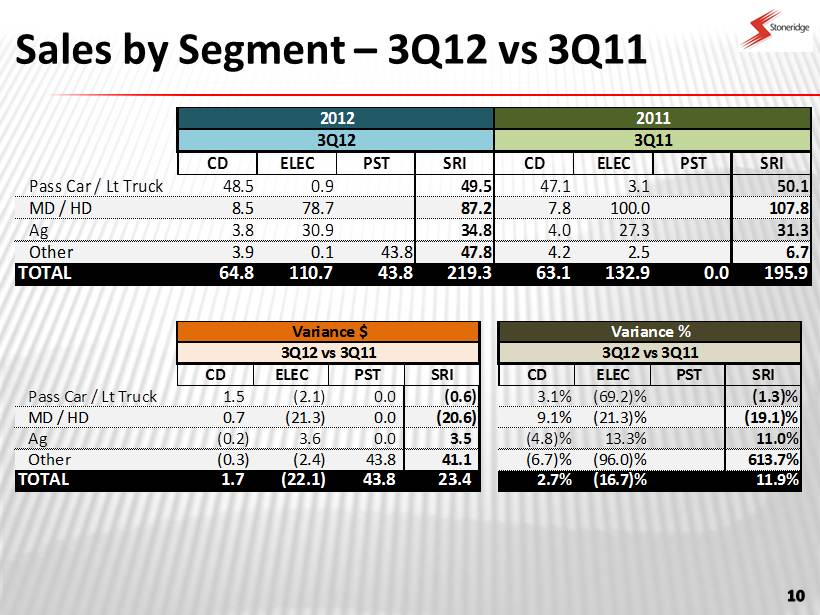

Sales by Segment – 3Q12 vs 3Q11 CD ELEC PST SRI CD ELEC PST SRI Pass Car / Lt Truck 48.5 0.9 49.5 47.1 3.1 50.1 MD / HD 8.5 78.7 87.2 7.8 100.0 107.8 Ag 3.8 30.9 34.8 4.0 27.3 31.3 Other 3.9 0.1 43.8 47.8 4.2 2.5 6.7 TOTAL 64.8 110.7 43.8 219.3 63.1 132.9 0.0 195.9 201120123Q12 3Q11 CD ELEC PST SRI CD ELEC PST SRI Pass Car / Lt Truck 1.5 (2.1) 0.0 (0.6) 3.1% (69.2)% (1.3)% MD / HD 0.7 (21.3) 0.0 (20.6) 9.1% (21.3)% (19.1)% Ag (0.2) 3.6 0.0 3.5 (4.8)% 13.3% 11.0% Other (0.3) (2.4) 43.8 41.1 (6.7)% (96.0)% 613.7% TOTAL 1.7 (22.1) 43.8 23.4 2.7% (16.7)% 11.9% Variance $3Q12 vs 3Q11 Variance %3Q12 vs 3Q11

Sales by Segment – 3Q12 vs 2Q12 CD ELEC PST SRI CD ELEC PST SRI Pass Car / Lt Truck 48.5 0.9 49.5 51.4 1.2 0.0 52.6 MD / HD 8.5 78.7 87.2 8.3 91.9 0.0 100.2 Ag 3.8 30.9 34.8 4.4 32.5 0.0 36.8 Other 3.9 0.1 43.8 47.8 4.5 1.7 38.5 44.7 TOTAL 64.8 110.7 43.8 219.3 68.6 127.3 38.5 234.3 3Q12 2Q12 2012 CD ELEC PST SRI CD ELEC PST SRI Pass Car / Lt Truck (2.9) (0.3) 0.0 (3.2) (5.6)% (21.7)% (6.0)% MD / HD 0.2 (13.2) 0.0 (13.0) 2.5% (14.3)% (12.9)% Ag (0.5) (1.5) 0.0 (2.1) (12.4)% (4.7)% (5.6)% Other (0.6) (1.6) 5.3 3.1 (12.9)% (94.1)% 13.8% 7.0% TOTAL (3.8) (16.6) 5.3 (15.1) (5.5)% (13.0)% 13.8% (6.4)% 3Q12 vs 2Q12 Variance $ Variance % 3Q12 vs 2Q12

Cost Initatives / Benefits $ millions 1Q12 2Q12 3Q12 4Q12 FY 2012 Costs NA Wiring 0.0 0.0 (0.7) (0.4) (1.1) NA / European Instrumentation 0.0 0.0 (0.3) 0.0 (0.3) PST (0.3) (1.3) 0.0 0.0 (1.6) TOTAL (0.3) (1.3) (1.0) (0.4) (3.0) Benefits NA Wiring 0.0 0.0 0.7 1.1 1.8 NA / European Instrumentation 0.0 0.0 0.0 0.4 0.4 PST 0.0 0.0 2.2 2.2 4.4 TOTAL 0.0 0.0 2.9 3.7 6.6 NET (0.3) (1.3) 1.9 3.3 3.6

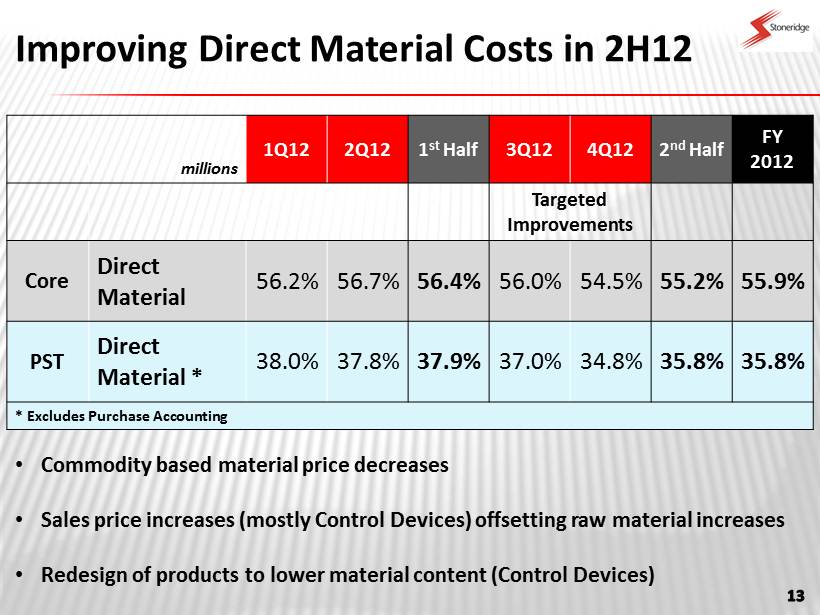

Improving Direct Material Costs in 2H12 millions 1Q12 2Q12 1 st Half 3Q12 4Q12 2 nd Half FY 2012 Targeted Improvements Core Direct Material 56.2% 56.7% 56.4% 56.0% 54.5% 55.2% 55.9% PST Direct Material * 38.0% 37.8% 37.9% 37.0% 34.8% 35.8% 35.8% * Excludes Purchase Accounting • Commodity based material price decreases • Sales price increases (mostly Control Devices) offsetting raw material increases • Redesign of products to lower material content (Control Devices)

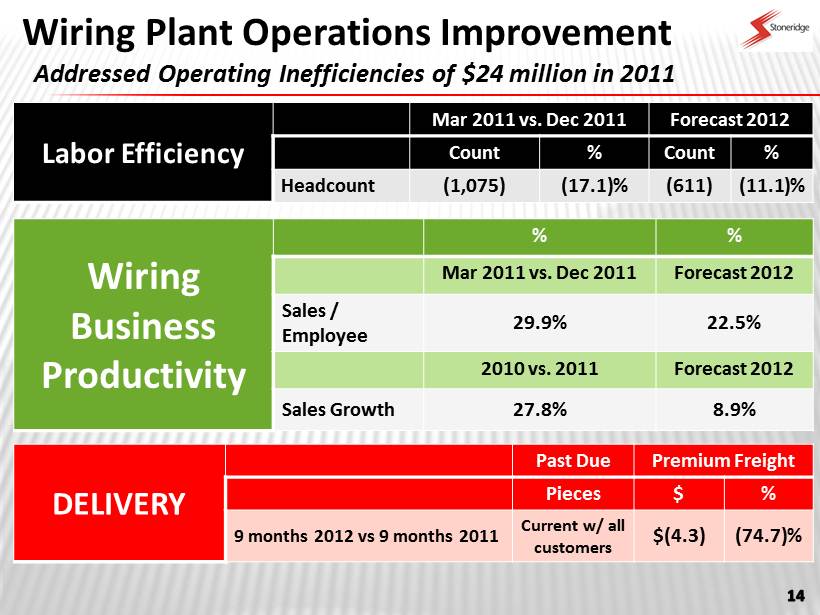

Wiring Plant Operations Improvement Addressed Operating Inefficiencies of $24 million in 2011 DELIVERY Past Due Premium Freight Pieces $ % 9 months 2012 vs 9 months 2011 Current w/ all customers $(4.3) (74.7)% Labor Efficiency Mar 2011 vs. Dec 2011 Forecast 2012 Count % Count % Headcount (1,075) (17.1)% (611) (11.1)% Wiring Business Productivity % % Mar 2011 vs. Dec 2011 Forecast 2012 Sales / Employee 29.9% 22.5% 2010 vs. 2011 Forecast 2012 Sales Growth 27.8% 8.9%

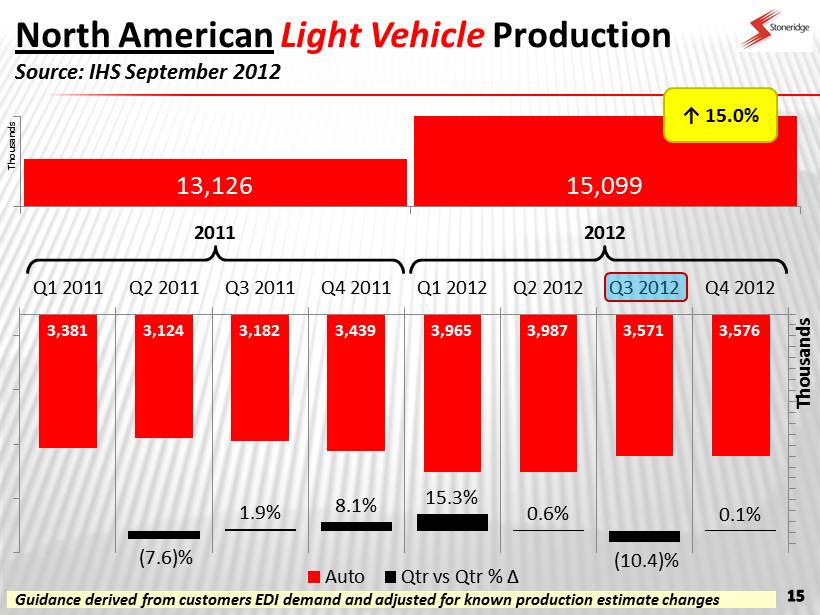

13,126 15,099 2011 2012 Thousands North American Light Vehicle Production Source: IHS September 2012 3,381 3,124 3,182 3,439 3,965 3,987 3,571 3,576 (7.6)% 1.9% 8.1% 15.3% 0.6% (10.4)% 0.1% Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Thousands Auto Qtr vs Qtr % ∆ ↑ 15.0% Guidance derived from customers EDI demand and adjusted for known production estimate changes

166,998 185,327 2011 2012 N.A. Medium Duty Truck Production Source: LMC September 2012 (previous JD Power) 40,135 44,760 41,834 40,269 48,200 49,903 43,778 43,446 11.5% (6.5)% (3.7)% 19.7% 3.5% (12.3)% (0.8)% Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 NA N.A. Qtr vs Qtr % ∆ ↑ 11.0% Guidance derived from customers EDI demand and adjusted for known production estimate changes

255,488 284,033 2011 2012 N.A. Heavy Duty Truck Production Source: LMC September 2012 (previous JD Power) 51,501 60,569 68,482 74,936 77,779 78,298 64,355 63,601 17.6% 13.1% 9.4% 3.8% 0.7% (17.8)% (1.2)% Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 NA N.A. Qtr vs Qtr % ∆ ↑ 11.2% Guidance derived from customers EDI demand and adjusted for known production estimate changes

334,357 298,078 2011 2012 W Europe Heavy Duty Truck Production Source: LMC September 2012 (previous JD Power) 83,415 82,813 76,569 91,560 78,118 78,641 65,077 76,242 (0.7)% (7.5)% 19.6% (14.7)% 0.7% (17.2)% 17.2% Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Europe Europe Qtr vs Qtr % ∆ ↓ (10.9)% Guidance derived from customers EDI demand and adjusted for known production estimate changes

FX Assumptions for 4Q12 USD / BRL 2.05 USD / MXN 13.25 EUR / USD 1.23 Copper $4.00 / pound

Debt / Net Debt (millions USD) 4Q11 1Q12 2Q12 3Q12 E 2012 F Total Debt $267.1 $253.2 $244.9 Net Debt $188.4 $210.2 $205.8 Total Debt / EBITDA 3.5 x 1 2.75 x 2 ABL Balance $38.0 $31.0 $25.0 $11.0 $0.0 Brazil Debt $54.1 $47.2 $43.8 $35.0 $32.2 EBITDA = Operating Income + Depreciation + Amortization + Purchase Accounting Direct Material 1 Proforma for PST Debt and EBITDA 2 Based on Average Guidance Level