Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SunCoke Energy, Inc. | d419419d8k.htm |

Credit Suisse

Global Credit Products

Conference

October 2012

Exhibit 99.1 |

Mark

Newman Senior Vice President &

Chief Financial Officer |

Safe Harbor

Statement Safe Harbor Statement

Some of the information included in this presentation contains “forward-looking

statements” (as defined in Section 27A of the

Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as

amended). Such forward-looking statements are based on management’s beliefs

and assumptions and on information currently available. Forward-looking statements

include the information concerning SunCoke’s possible or assumed future results of operations, the planned Master

Limited Partnership, business strategies, financing plans, competitive position, potential

growth opportunities, potential operating performance improvements, the effects of

competition and the effects of future legislation or regulations. Forward-looking

statements include all statements that are not historical facts and may be identified by the

use of forward-looking terminology such as the words “believe,”

“expect,”

“plan,”

“intend,”

“anticipate,”

“estimate,”

“predict,”

“potential,”

“continue,”

“may,”

“will,”

“should”

or the negative of these terms or similar expressions. Forward-looking statements involve

risks, uncertainties and assumptions. Actual results may differ materially from those

expressed in these forward-looking statements. You should not put undue reliance on

any forward-looking statements. In accordance with the safe harbor provisions of the

Private Securities Litigation Reform Act of 1995, SunCoke has included in its filings

with the Securities and Exchange Commission cautionary language identifying important factors (but not necessarily all the

important factors) that could cause actual results to differ materially from those expressed

in any forward-looking statement made by SunCoke. For more information concerning

these factors, see SunCoke's Securities and Exchange Commission filings. All

forward-looking statements included in this presentation are expressly qualified in their

entirety by such cautionary statements. SunCoke does not have any intention or

obligation to update publicly any forward-looking statement (or its associated cautionary

language) whether as a result of new information or future events or after the date of this

presentation, except as required by applicable law.

This presentation includes certain non-GAAP financial measures intended to supplement, not

substitute for, comparable GAAP measures. Reconciliations of non-GAAP financial

measures to GAAP financial measures are provided in the Appendix at the end of the

presentation. Investors are urged to consider carefully the comparable GAAP measures and the reconciliations to those

measures provided in the Appendix, or on our website at www.suncoke.com.

CS

Global

Credit

Conference

-

October

2012

3 |

About

SunCoke About SunCoke

Largest independent producer of

metallurgical coke in the Americas

Coke is an essential ingredient in blast

furnace production of steel

Cokemaking business generates

~85% of Adjusted EBITDA

(1)

5.9 million tons of capacity in six

facilities; 5 in U.S. and 1 in Brazil

2012 U.S. coke production is expected

to be in excess of 4.3 million tons

Coal mining operations represents

~15% of Adjusted EBITDA

(1)

High quality mid-vol. metallurgical coal

reserves in Virginia and West Virginia

2012 coal production expected to be

1.6 million tons

CS

Global

Credit

Conference

-

October

2012

4

(1)

For a definition and reconciliation of Adjusted EBITDA, please see appendix.

|

Blast Furnaces

and Coke 5

1 short ton

of hot metal (NTHM)

Top Gas

CS Global Credit Conference -

October 2012

Blast furnaces are the most

efficient and proven method

of reducing iron oxides

into liquid iron

Coke is a vital material to

blast furnace steel making

We believe stronger, larger

coke is becoming more

important as blast furnaces

seek to optimize fuel needs

BEST IN CLASS in lbs/ST

Iron

burden

Iron ore/

pellets

Scrap

3100

198

30

600

Flux

Fuel

Coke

Limestone

BEST IN CLASS in lbs/ST

Fuel

Nat Gas

Coal

Up to

80-120

Up to

120-180

Most efficient blast

furnaces require

800-900 lbs/NTHM

of fuel to produce

a ton of hot metal |

More than

doubled capacity since 2006 with four new plants

Only company to design, build and

operate new greenfield developments

in U.S. in more than a decade

Supply about 20% of U.S. and Canada

coke needs

(1)

Secure, long-term take-or-pay

contracts with leading steelmakers

Customers include ArcelorMittal, U.S.

Steel and AK Steel

Cokemaking operations are

strategically located in proximity to

customers’

facilities

The Leading Independent Cokemaker

The Leading Independent Cokemaker

SunCoke

Cokemaking Capacity

(In thousands of tons)

6

(1)

Source: Company estimates

2006

2007

2008

2009

2010

2011

Jewell Coke

(Virginia)

Indiana Harbor

(Indiana)

Haverhill I

(Ohio)

Vitória

(Brazil)

Haverhill II

(Ohio)

Granite City

(Illinois)

Middletown

(Ohio)

2,490

4,190

4,740

5,390

5,390

5,940

CS

Global

Credit

Conference

-

October

2012 |

SunCoke’s

Heat Recovery SunCoke’s Heat Recovery

Cokemaking Technology

Cokemaking Technology

CS

Global

Credit

Conference

-

October

2012

7

Industry leading environmental

signature

Leverage negative pressure

technology to substantially reduce

hazardous emissions

Convert waste heat into steam

and electrical power

Generate about 9 MW of electric

power per 110,000 tons of

annual coke production

Meet stringent U.S. EPA

Maximum Achievable Control

Technology standard

Traditional by-product cokemaking

methods have significant

environmental impacts |

SunCoke’s

Value Proposition SunCoke’s Value Proposition

Provide an assured supply of coke to steelmakers

Larger, stronger coke for improved blast furnace performance

Demonstrated sustained 15% -

20% turndown capability

High quality coke with cheaper coal blends

–

Burn

loss

vs.

by-product

Capital preservation and lower capacity cost per ton;

particularly relative to greenfield investment

Stringent U.S. regulatory environment

Power prices and reliability versus value of coke oven gas and

by-product "credits"

High Quality

& Reliable

Coke Supply

Turndown

Flexibility

Coal

Flexibility

Capital

Efficiency

& Flexibility

Environment

/Economic

Trade-offs

CS Global Credit Conference -

October 2012

8 |

Key Contract

Provisions Key Contract Provisions

CS

Global

Credit

Conference

-

October

2012

9

Take-or-Pay

Fixed Fee

Coal Cost

Operating

Costs

Transportation

& Taxes

–

We are obligated to deliver a minimum quantity of coke annually

Represents profit and return on capital

Customers must take all our production up to a maximum or

pay contract price for amount not taken

–

Fixed fee is fixed for life of contract

Cost of coal is passed-through subject to achieving a

contracted coal-to-coke yield standard

Operating costs are passed-through based on annually

negotiated budget or a fixed budget adjusted for inflation

These costs are passed-through |

Master Limited

Partnership Master Limited Partnership

Filed S-1 on August 8, 2012

–

Amended S-1 on September 14, 2012

Expected Assets/Structure

–

At closing of offering, MLP expected

to own approximately a 60% interest

in Haverhill and Middletown

–

SXC to own General Partner, incentive

distribution rights and a portion of

the partnership units

Proceeds to SXC

–

Expected uses will include paying

down debt, funding expansion and

other general corporate purposes

CS

Global

Credit

Conference

-

October

2012

10

Middletown Operations

Haverhill Operations |

Q1 & Q2 2012

Earnings Overview Results driven by strong Coke business

performance

Middletown startup has been a success

Continued improvement at Indiana Harbor

Strong operations at other facilities

Coal action plan progressing

Difficult demand/price environment

Taking action to reduce high cash

production costs

Achieved improved sequential quarter

performance

Strong liquidity position

Generated $66 million of free cash flow

(2)

in

first half 2012

Cash balance of $190 million and virtually

undrawn revolver of $150 million

(1)

For a definition and reconciliation of Adjusted EBITDA, please see the appendix.

(2)

For a definition and reconciliation of free cash flow, please see the appendix.

CS

Global

Credit

Conference

-

October

2012

11

$0.17

$0.24

$0.32

$0.32

2011

2012

Q1

Q2

Earnings Per Share

(diluted)

$26.6

$55.8

$37.7

$65.5

2011

2012

Q1

Q2

Adjusted EBITDA

(1)

(in millions) |

Domestic Coke

Business Summary Domestic Coke Business Summary

(Jewell Coke & Other Domestic Coke)

(Jewell Coke & Other Domestic Coke)

CS

Global

Credit

Conference

-

October

2012

12

(Tons in thousands)

($ in millions, except per ton amounts)

(1)

For a definition of EBITDA and Adjusted EBITDA/Ton and reconciliations, please see the

appendix. (2)

Includes Indiana Harbor contract billing adjustment of $6.0 million, net of NCI, and

inventory (3)

Includes a $2.4 million, net of NCI, charge related to coke inventory reduction and a $1.3

million, net of NCI, lower cost or market adjustment on pad coal inventory and

lower coal-to-coke yields related to the startup at Middletown.

Strong performance driven by Middletown, Indiana Harbor and other operations

/Ton

/Ton

/Ton

(3)

/Ton

(2)

Domestic Coke Adjusted EBITDA

(1)

Per Ton

Domestic

Coke

Production

adjustment of $6.2 million, net of NCI, of which $3.1 million is attributable to Q3 2011. |

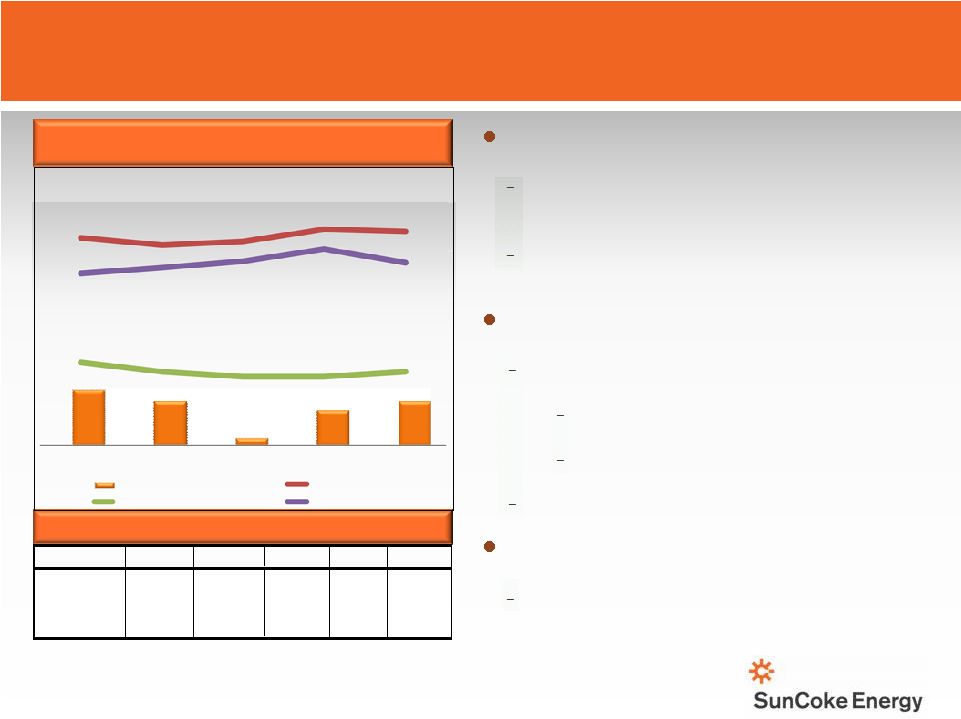

Coal Mining

Financial Summary Coal Mining Financial Summary

CS Global

Credit

Conference

-

October

2012

13

Coal Mining

Adjusted

EBITDA

(1)

and

Avg.

Sales

Price/Ton

(2)

Cash production costs increasing in face of

difficult demand/price environment

Pricing up modestly, reflecting strong mid-vol.

pricing/volumes, offset by weak hi-vol. and thermal

pricing/volumes

Cash costs up $11/ton, reflecting decreased mix and

higher costs of hi-vol. and thermal production

Coal action plan implemented in Q1 2012

gaining traction

Focus on most productive mines to reduce costs

delivered sequential quarter improvement

Cash cost per ton at Jewell decreased from

$161 in Q1 2012 to $143 in Q2 2012

Jewell reject rates improved from 68% in Q1

2012 to 66% in Q2 2012

Expect further cash cost reductions for 2013

Intend to maintain cash neutral position in

2012

Reduced capital spending in line with outlook

Coal Sales, Production and Purchases

-$50

$0

$50

$100

$150

Q2 '11

Q3 '11

Q4 '11

Q1 '12

Q2 '12

Coal Sales

334

371

363

373

365

Coal Producton

340

340

349

375

401

Purchased Coal

24

22

20

19

4

-$50

$0

$50

$100

$150

$200

($ in millions, except per ton amounts)

$11

$9

$2

$7

$9

$162

$155

$159

$171

$169

$34

$25

$20

$20

$25

$126

$132

$138

$151

$137

-$50

$0

$50

$100

$150

$200

Q2 '11

Q3 '11

Q4 '11(3)

Q1 '12

Q2 '12

Coal Adjusted EBITDA

Average Sales Price

Coal Adj EBITDA / ton

Coal Cash Cost / ton

(1)

For a definition and a reconciliation of Adjusted EBITDA, please see the appendix.

(2)

Average Sales Price is the weighted average sales price for all coal sales volumes, including

sales to affiliates and sales to Jewell Coke.

(3)

Q4 2011 Adjusted EBITDA inclusive of Black Lung Liability charge of $3.4 million and

OPEB expense allocation of $1.8 million. |

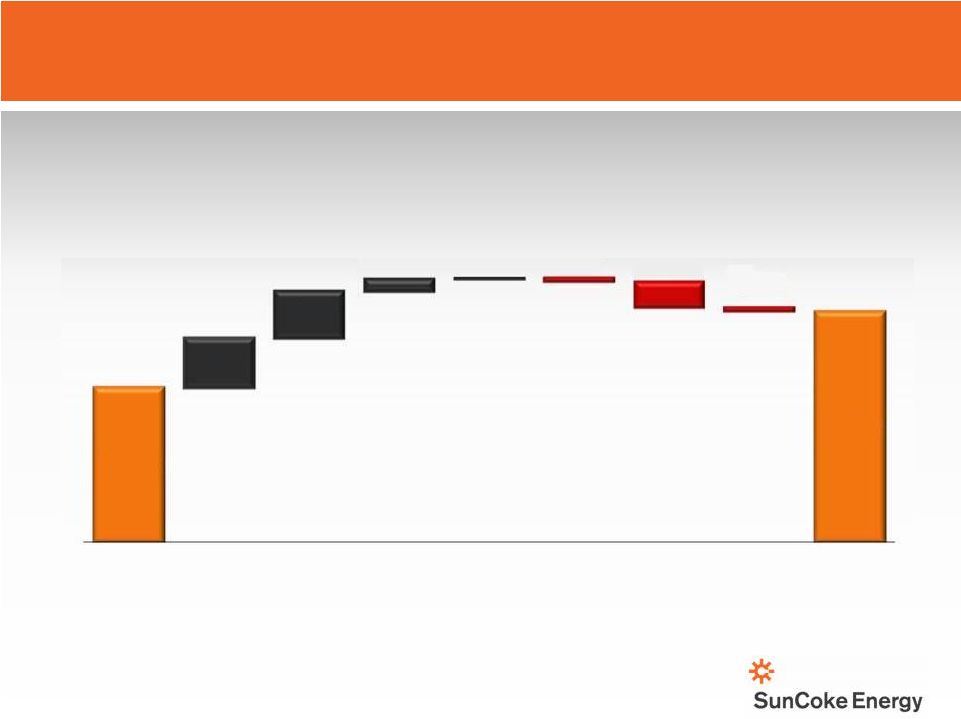

First Half 2012

Sources & Uses of Cash First Half 2012 Sources & Uses of Cash

14

Liquidity position and credit metrics improving;

free

cash

flow

(1)

was

$66

million

in

first

half

2012

($ in millions)

(1)

For a definition and reconciliation of free cash flow, please see appendix.

CS

Global

Credit

Conference

-

October

2012

$127.5

$40.6

$38.6

$10.0

$0.3

$190.0

($2.8)

($20.7)

($3.5)

Q4 2011

Cash

Balance

1H 2012

Net Income

Depreciation,

Depletion &

Amortization

Deferred

Taxes

Changes in

Working

Capital

Other

Capital

Expenditures

Cash used in

financing

activities

Q2 2012

Cash

Balance |

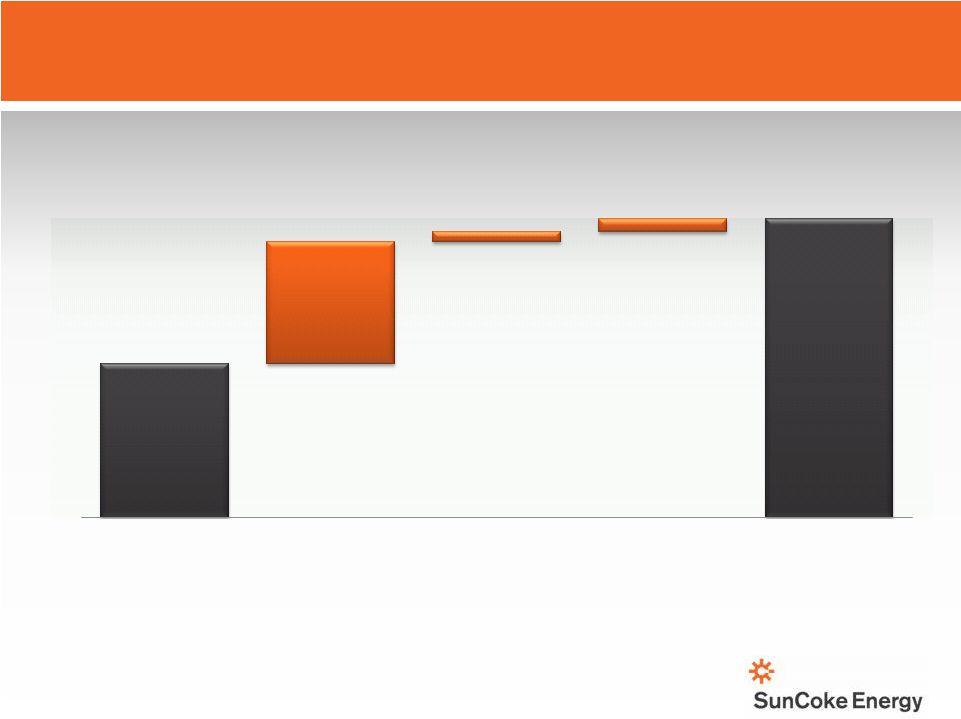

2012 Adjusted

EBITDA 2012 Adjusted EBITDA

(1)

(1)

Outlook

Outlook

($ in millions)

CS

Global

Credit

Conference

-

October

2012

15

(1)

For a definition of Adjusted EBITDA and reconciliation of Adjusted EBITDA, please see the

appendix. Strong U.S. cokemaking business expected to

2011

Adjusted

EBITDA (1)

Coke Business

Coal Mining

Corporate

Costs

Estimated

2012 Adjusted

EBITDA (1)

drive

increase

in

Adjusted

EBITDA

in

2012

$141

$95 -

$110

$5 -

$15

$9 -

$14

$250 -

$280

(1) |

Strategies for

Enhancing Shareholder Value Strategies for Enhancing Shareholder Value

16

CS

Global

Credit

Conference

-

October

2012

Operational

Excellence

•

Maintain focus on details

and discipline of coke and

coal mining operations

•

Sustain and enhance top

quartile safety

performance and ability to

meet environment

standards

•

Leverage operating know-

how and technology to

continuously improve

yields and operating costs

Grow The Coke

Business

•

U.S. & Canada

Continue permitting

efforts for next potential

U.S. facility

•

Explore opportunities to

make strategic

investments in existing

capacity

•

International

•

Execute India entry and

pursue follow-on growth

Strategically Optimize

Assets

•

Coke MLP

•

Execute plan to place a

portion of our

cokemaking assets into

an MLP structure

•

Coal

•

Optimize operations and

investments to enhance

long-term strategic

flexibility

• |

CS

Global

Credit

Conference

-

October

2012

Source: CRU, The Annual Outlook for Metallurgical Coke 2012.

Replace aging coke batteries operated by integrated steel producers

Source: CRU, The Annual Outlook for Metallurgical Coke 2012

51% of coke capacity is at facilities >30 years old

U.S. and Canada Opportunity

U.S. and Canada Opportunity

17

Total 2011 Coke Demand: 19.5 million tons

Integrated

Integrated

Steel

Steel

Producers

Producers

63%

63%

SunCoke

18%

DTE

5%

Other Merchant

Other Merchant

& Foundry

& Foundry

6%

6%

Imports

Imports

8%

8%

Average Age

%

of U.S. & Canada

coke production

9

37

27%

24%

Aging Cokemaking Facilities

SunCoke

U.S. &

Canada

(excl SXC)

30-40 years

40+ years

U.S. & Canada Coke Supply |

Coke Price

Comparison Coke Price Comparison

18

SunCoke’s coke is competitive on price, quality and reliability, providing us the

opportunity to displace imported coke

Source:

World

Price

(DTC),

Coke

Market

Report,

CRU

and

company

estimates

CS

Global

Credit

Conference

-

October

2012

U.S. and Canada Coke Imports

Representative

Delivered

Coke

Prices

-

$/ton

Chinese 40% Export Tax Premium (Tariff)

Chinese Coke Price

SunCoke Price -

Contracted Coal Price Differential

SunCoke Coke Price @ Spot Coal Price

1

Includes approx. $50/ton freight and approx. $40/ton handling loss

for shipping to Great Lakes region

2

Includes approx. $45/ton freight and approx. $30/ton handling loss

for shipping to Great Lakes region

$348

$48

$331

$402

$127

Other Domestic Coke

Ukrainian

Coke (2)

Chinese

Coke (1)

$396

$331

4.5

4.8

3.2

5.2

0.9

2.0

2.0

2.0

1.8

1.6

1.5

1.7

Imports

SunCoke sales volumes

2005

2006

2007

2008

2009

2010

2011

2012E

2013E

2014E

2015E

2016E

Based on July 2012 prices

$529 |

Sources: CRU, The Annual Outlook for

Metallurgical Coke 2011, CIA World Factbook.

India Opportunity

India Opportunity

19

India

India

Steel/Coke

Steel/Coke

Market

Market

•

•

Committed to

Committed to

India entry

India entry

strategy

strategy

–

–

Discussing

Discussing

opportunities in

opportunities in

India

India

–

–

Targeting

Targeting

potential entry by

potential entry by

early 2013

early 2013

Growing Steel

Market

Coke supply

Deficit

Active

Merchant

Market

Electric Power

Deficit

Projected to be 3rd largest

steel market by 2020

Blast furnace to play a critical

role in growth

Importing approximately

2 million tons annually

Coke capacity investment lags

steel investment

3.5 million tons merchant

production or 13% of total

17 active merchant

coke producers

10% -

20% short power

Average wholesale price >$80

mwh (2x U.S. rate)

CS

Global

Credit

Conference

-

October

2012 |

QUESTIONS

QUESTIONS

CS Global Credit Conference -

October 2012

20 |

Appendix

|

Definitions

CS

Global

Credit

Conference

-

October

2012

22

• Adjusted EBITDA represents earnings before interest, taxes, depreciation,

depletion and amortization (“EBITDA”) adjusted for sales discounts and the

deduction of income attributable to non-controlling interests in our Indiana Harbor

cokemaking operations. EBITDA reflects sales discounts included as a reduction in sales and other

operating revenue. The sales discounts represent the sharing with our customers of a portion

of nonconventional fuels tax credits, which reduce our income tax expense. However, we

believe that our Adjusted EBITDA would be inappropriately penalized if these discounts

were treated as a reduction of EBITDA since they represent sharing of a tax benefit

which is not included in EBITDA. Accordingly, in computing Adjusted EBITDA, we have added back

these sales discounts. Our Adjusted EBITDA also reflects the deduction of income attributable

to noncontrolling interest in our Indiana Harbor cokemaking operations. EBITDA and

Adjusted EBITDA do not represent and should not be considered alternatives to net

income or operating income under United States generally accepted accounting principles

(GAAP) and may not be comparable to other similarly titled measures of other businesses.

Management believes Adjusted EBITDA is an important measure of the operating performance of

the Company’s assets and is indicative of the Company’s ability to generate

cash from operations. •

Adjusted EBITDA/Ton

represents Adjusted EBITDA divided by tons sold.

•

Free Cash Flow

equals cash from operations less cash used in investing activities less cash distributions to

non- controlling interests. Management believes Free Cash Flow information

enhances an investor’s understanding of a business’

ability to generate cash. Free Cash Flow does not represent and should not be

considered an alternative to net income or cash flows from operating activities as

determined under GAAP and may not be comparable to other similarly titled measures of

other businesses. |

Reconciliations

CS

Global

Credit

Conference

-

October

2012

23

$ in millions

Q2 2012

Q1 2012

FY 2011

Q4 2011

Q3 2011

Q2 2011

Q1 2011

Adjusted Operating Income

46.6

37.1

80.4

14.9

33.5

24.6

7.4

Net Income (Loss) attributable to Noncontrolling Interest

1.3

(0.3)

(1.7)

(0.5)

3.4

1.6

(6.2)

Subtract: Depreciation Expense

(20.2)

(18.4)

(58.4)

(16.0)

(14.7)

(14.7)

(13.0)

Adjusted EBITDA

65.5

55.8

140.5

31.4

44.8

37.7

26.6

Subtract: Depreciation, depletion and amortization

(20.2)

(18.4)

(58.4)

(16.0)

(14.7)

(14.7)

(13.0)

Subtract: Financing expense, net

(11.8)

(12.0)

(1.4)

(7.1)

(3.3)

4.5

4.5

Subtract: Income Tax

(7.0)

(5.3)

(7.2)

2.9

(5.1)

(1.9)

(3.1)

Subtract: Sales Discount

(3.8)

(3.2)

(12.9)

(3.2)

(3.5)

(3.1)

(3.1)

Add: Net Income attributable to NCI

1.3

(0.3)

(1.7)

(0.5)

3.4

1.6

(6.2)

Net Income

24.0

16.6

58.9

7.5

21.6

24.1

5.7

Reconciliations

from

Adjusted

Operating

Income

and

Adjusted

EBITDA

to

Net

Income |

Reconciliations

CS

Global

Credit

Conference

-

October

2012

24

$ in millions, except per ton data

Jewell Coke

Other

Domestic

Coke

International

Coke

Jewell Coal

Corporate

Combined

Domestic

Coke

Q2 2012

Adjusted EBITDA

12.5

48.6

0.7

9.3

(5.6)

65.5

61.1

Subtract: Depreciation, depletion and amortization

(1.3)

(13.7)

(0.1)

(4.3)

(0.8)

(20.2)

(15.0)

Add (Subtract): Net (Income) loss attributable

to noncontrolling interests

1.3

1.3

1.3

Adjusted

Pre-Tax

Operating

Income

11.2

36.2

0.6

5.0

(6.4)

46.6

47.4

Adjusted EBITDA

12.5

48.6

0.7

9.3

(5.6)

65.5

61.1

Sales Volume (thousands of tons)

170

892

358

373

1,062

Adjusted EBITDA per Ton

73.5

54.5

2.0

24.9

57.5

Q1 2012

Adjusted EBITDA

15.0

40.1

0.1

7.4

(6.8)

55.8

55.1

Subtract: Depreciation, depletion and amortization

(1.3)

(12.6)

(0.1)

(4.1)

(0.3)

(18.4)

(13.9)

Add (Subtract): Net (Income) loss attributable

to noncontrolling interests

(0.3)

(0.3)

(0.3)

Adjusted Pre-Tax Operating Income

13.7

27.2

-

3.3

(7.1)

37.1

40.9

Adjusted EBITDA

15.0

40.1

0.1

7.4

(6.8)

55.8

55.1

Sales Volume (thousands of tons)

186

892

358

373

1,078

Adjusted EBITDA per Ton

80.6

45.0

0.3

19.8

51.1

Reconciliations from Adjusted EBITDA to Adjusted Pre-Tax Operating Income

|

Reconciliations

25

$ in millions, except per ton data

Jewell Coke

Other

Domestic

Coke

International

Coke

Jewell Coal

Corporate

Combined

Domestic

Coke

Q4 2011

Adjusted EBITDA

10.6

21.3

10.2

2.5

(13.2)

31.4

31.9

Subtract: Depreciation, depletion and amortization

(1.2)

(10.6)

(0.1)

(3.7)

(0.4)

(16.0)

(11.8)

Add (Subtract): Net (Income) loss attributable

to noncontrolling interests

(0.5)

(0.5)

(0.5)

Adjusted

Pre-Tax Operating Income

9.4

10.2

10.1

(1.2)

(13.6)

14.9

19.6

Adjusted EBITDA

10.6

21.3

10.2

2.5

(13.2)

31.4

31.9

Sales Volume (thousands of tons)

166

837

295

363

1,003

Adjusted EBITDA per Ton

63.9

25.4

34.6

6.9

31.8

Q3 2011

Adjusted EBITDA

13.9

34.3

1.7

9.2

(14.3)

44.8

48.2

Subtract: Depreciation, depletion and amortization

(1.2)

(9.9)

-

(3.3)

(0.3)

(14.7)

(11.1)

Add (Subtract): Net (Income) loss attributable

to noncontrolling interests

3.4

3.4

3.4

Adjusted

Pre-Tax Operating Income

12.7

27.8

1.7

5.9

(14.6)

33.5

40.5

Adjusted EBITDA

13.9

34.3

1.7

9.2

(14.3)

44.8

48.2

Sales Volume (thousands of tons)

191

777

373

371

968

Adjusted EBITDA per Ton

72.8

44.1

4.6

24.8

49.8

Reconciliations from Adjusted EBITDA to Adjusted Pre-Tax Operating Income

CS

Global

Credit

Conference

-

October

2012 |

Reconciliations

$ in millions, except per ton data

Jewell Coke

Other

Domestic

Coke

International

Coke

Jewell Coal

Corporate

Combined

Domestic

Coke

Q2 2011

Adjusted EBITDA

10.6

25.3

0.8

11.5

(10.5)

37.7

35.9

Subtract: Depreciation, depletion and amortization

(1.4)

(9.6)

(0.1)

(3.2)

(0.4)

(14.7)

(11.0)

Add (Subtract): Net (Income) loss attributable

to noncontrolling interests

1.6

1.6

1.6

Adjusted Pre-Tax Operating Income

9.2

17.3

0.7

8.3

(10.9)

24.6

26.5

Adjusted EBITDA

10.6

25.3

0.8

11.5

(10.5)

37.7

35.9

Sales Volume (thousands of tons)

170

757

412

334

927

Adjusted EBITDA per Ton

62.4

33.4

1.9

34.4

38.7

Q1 2011

Adjusted EBITDA

11.0

8.5

1.0

12.3

(6.2)

26.6

19.5

Subtract: Depreciation, depletion and amortization

(1.1)

(8.6)

-

(2.7)

(0.6)

(13.0)

(9.7)

Add (Subtract): Net (Income) loss attributable

to noncontrolling interests

(6.2)

(6.2)

(6.2)

Adjusted Pre-Tax Operating Income

9.9

(6.3)

1.0

9.6

(6.8)

7.4

3.6

Adjusted EBITDA

11.0

8.5

1.0

12.3

(6.2)

26.6

19.5

Sales Volume (thousands of tons)

175

697

362

386

872

Adjusted EBITDA per Ton

62.9

12.2

2.8

31.9

22.4

Reconciliations from Adjusted EBITDA to Adjusted Pre-Tax Operating Income

CS

Global

Credit

Conference

-

October

2012

26 |

(in

millions) 2012E

Low

2012E

High

Net Income

$98

$122

Depreciation, Depletion and Amortization

74

72

Total financing costs, net

48

46

Income tax expense

25

37

EBITDA

$245

$277

Sales discounts

11

10

Noncontrolling interests

(6)

(7)

Adjusted EBITDA

$250

$280

Estimated EBITDA Reconciliation

2012E Net Income to Adjusted EBITDA Reconciliation

27

CS Global Credit Conference -

October 2012 |

Free Cash Flow

Reconciliations 2012E Estimated Free Cash Flow Reconciliation

CS

Global

Credit

Conference

-

October

2012

28

(in millions)

1

st

Half

2012

Cash from operations

$ 86.7

Less cash used for investing activities

(20.7)

Less payments to minority interest

( -

)

Free Cash Flow

$ 66.0

(in millions)

2012

Cash from operations

In excess of

$ 189

Less cash used for investing activities

Approx.

(85)

Less payments to minority interest

Approx.

(4)

Free Cash Flow

In excess of

$ 100

First Half 2012 Free Cash Flow Reconciliation |

Reference

|

SunCoke’s

Cokemaking Technology SunCoke’s Cokemaking Technology

30

CS

Global

Credit

Conference

-

October

2012

Our industry-leading cokemaking technology meets

U.S. EPA Maximum Achievable Control Technology (MACT) Standards |

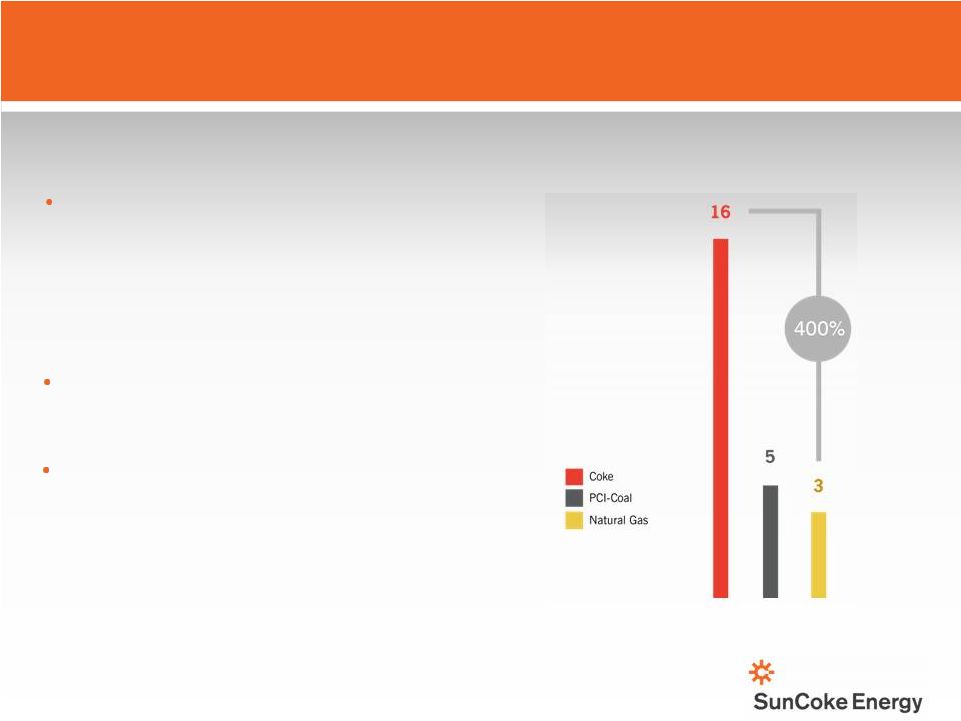

Natural Gas in

The Blast Furnace Impact of Low Natural Gas Prices

Natural gas cannot completely replace

coke in blast furnace

–

We estimate natural gas and other

injectants can replace up to about 30%

–

The less coke used the more important

the coke’s quality

Alternative technologies take time to

implement, require significant capital

commitments and are energy intensive

Coke oven gases produced by

integrated steelmakers’

own coke

ovens is less valuable in low cost

natural gas environment, potentially

impacting steelmakers’

future

reinvest/rebuild decisions

Blast Furnace Fuel Pricing

31

Source: CRU, SXC Analysis

US$/MMBtu

CS

Global

Credit

Conference

-

October

2012 |