Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - NAUTILUS, INC. | d418657d8k.htm |

October

2012 Charting the Course

to Profitable Growth

Exhibit 99.1 |

Safe Harbor

Statement This presentation includes forward-looking statements

(statements which are not historical facts) within the meaning of the Private

Securities Litigation Reform Act of 1995, including statements concerning the

Company's prospects, resources, capabilities, current or future financial

trends or operating results, demand for the Company's objectives, expectations, products, future plans for introduction

of new products and the anticipated outcome of new business initiatives. Factors

that could cause Nautilus, Inc.'s actual results to differ materially

from

these

forward-looking

statements

include

our

ability

to

acquire

inventory

from

sole

source

foreign

manufacturers

at

acceptable

costs,

within

timely

delivery

schedules

and

that

meet

our

quality

control

standards,

availability

and

price

of

media

time

consistent with our cost and audience profile parameters, a decline in consumer

spending due to unfavorable economic conditions in one or more of our

current or target markets, an adverse change in the availability of credit for our customers who finance their

purchases, our ability to pass along vendor raw material price increases and

increased shipping costs, our ability to effectively develop, market and

sell future products, our ability to protect our intellectual property, and the introduction of competing products. Additional

assumptions, risks and uncertainties are described in detail in our registration

statements, reports and other filings with the Securities and Exchange

Commission, including the "Risk Factors" set forth in our Annual Report on Form 10-K, as supplemented by our

quarterly reports on Form 10-Q. Such filings are available on our website or at

www.sec.gov. You are cautioned that such statements are

not

guarantees

of

future

performance

and

that

actual

results

or

developments

may

differ

materially

from

those

set

forth

in

the

forward-looking statements. We undertake no obligation to publicly update or

revise forward-looking statements to reflect subsequent events or

circumstances. Unless otherwise indicated, all information regarding our

operating results pertain to continuing operations. 2

|

Plans and strategies are in place to deliver…

Nautilus Fall 2012 Update -

Highlights

•

The Business has been successfully transformed into a simplified, much

more focused and profitable, growth oriented model

•

Significant momentum on key initiatives which began last year are starting

to pay dividends

•

Stepped up new product development efforts are getting traction

Pipeline of new launches starting Q3 2012 through 2013

•

Operating expense controls and leverage potential are evident

First half operating ratio was 42.7% of sales versus 45.2% last year

•

Balance sheet is well positioned to support business growth

All remaining debt paid off in March 2012

Cash balance at $16.1M as of June 2012

3

growth

above the industry average

profitability

in

line

with

top

consumer

durables

companies |

Nautilus Fall

2012 Update Recent Financial Performance Improvement

Recent Business Initiative Results

Objectives and Strategies for the Future

Themes of Execution

Summary

Other Background Information

Nautilus Business Profile

Historical Perspective

4 |

Business Model

Transformation Complex

Lack of Focus

Significant Infrastructure

Globally

Years of Financial Losses

Weak Balance Sheet

Simplified

Focused on Home Use

Markets

Lean Operations

Strong Balance Sheet

2007

2007

2012

2012

5

Remain Simplified; but with

stepped up product innovation

and brand utilization

Remain Focused; but with more

diversified product lines

Continue; but with even greater

leverage

of

current

infrastructure

Continue; building towards

higher operating margin

Maintain and Build; utilize to

improve shareholder value

GOAL

GOAL

Profitable and Positioned

for Further Improvement |

Recent Financial

Performance Improvement * Remaining debt was paid off in March 2012 ($5.5M)

6

METRIC

YOY First Half 2012

Last Twelve Months -

Q2 2012

•

Revenue

Growth

increased

–

Direct

–

Retail

+ 9.4%

+ 10.9%

+ 8.1%

+ 7.4%

+ 10.1%

+ 3.6%

•

Gross Margin

Direct

Retail

+ 110 bps

+ 230 bps

-

100

bps

+ 10 bps

+ 150 bps

-

310 bps

•

Operating

Expense

ratio

Improved

45.2% to 42.7%

44.9% to 40.5%

•

June Cash net of debt

improved

$16.1M vs

$9.6M Last

Year

*

---

•

Income from Continuing Operations

increased

Loss of $1.1M to gain of

$2.2M

Loss of $1.5M to gain of $5.7M

improved |

Operating Income

Progress Continuing Operations Only

*2012 LTM results shown are for the last twelve month’s actual performance which includes

July 2011 through June 2012 Results of Restructuring

and Focus on Consumer

Market

7

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

2008

2009

2010

2011

2012 LTM*

Operating Income / Loss

(% of Net Revenue) |

Operating Income

Progress Continuing Operations -

Quarterly results are unaudited

8

Operating Income / Loss by Quarter

-$5.0

-$4.0

-$3.0

-$2.0

-$1.0

$0.0

$1.0

$2.0

$3.0

$4.0

'09

'10

'11

'12

-16.0

-14.0

-12.0

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

'09

'10

'11

'12

-3.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

'09

'10

'11

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

'09

'10

Q4

Q3

Q2

Q1

'11 |

Recent Business

Initiative Results – Significant Momentum

•

Top line growth and margin improvement from new products

New line of TCs, CBR, Retail items introduced in 2011 / 2012

•

Milestone consumer and brand research study completed

Setting brand strategy; improved product positioning

Filtering and better targeting of new products

Focus licensing opportunities

•

Increased new product development resources have been put in place

Advanced Development Group created

New disciplines to enhance product innovation

•

New product pipeline filling for 2013 and beyond

Back

half

2012

planned

launches

include

DVD

program,

more

Retail

items,

digital

caloric

tracking device

•

Secured back half 2012 price increases to help mitigate product cost pressures

•

Significantly advanced diversification of supply base and negotiated more

favorable payment terms

First Half 2012

9 |

Recent

Business

Initiative

Results

(cont.)

•

Placements secured with new Retail customers

•

Cost improvement initiatives being institutionalized

Focus on products, processes, and services

•

Remaining debt was paid off in March ($5.5M)

•

Organizational progress:

New CFO (Linda Pearce) joined in August this year

Significant talent added throughout R&D

Move to lower cost office completed in August

Redesigned incentive plan for better alignment with performance to long term goals

First Half 2012

Significant momentum on key initiatives begun last year

and we are beginning to harvest gains from those efforts

10 |

New Product

Development Progress – Stepped up pace

•

In

2012

we

have

launched

several

new

products

(many

shown

below)

with

more

on the way:

Coming in Q4:

DVD Workout Program

and a Digital Caloric Tracking Device

Schwinn AD6 Airdyne

Bowflex 445 Dumbbells

Schwinn A40 and 425 Elliptical

Schwinn 520 Recumbent Elliptical

CoreBody Reformer

Creative Refresh

11 |

Brand Research

Findings – Significant Opportunity

•

In early 2012 we

engaged in a large

nationwide survey of

attitudes and

behaviors toward

fitness across all

geographic, age,

gender, and income

demographics

•

We confirmed that

we hold industry

leading brands, and

also gained valuable

insights into

consumer attitudes

toward modalities,

desired goals, and

shopping

preferences

1,500+ respondents

maintaining journals of

activity and answering

questions regarding

fitness equipment

modalities and brands

12

1,500+ respondents

maintaining journals of

activity and answering

questions regarding

fitness equipment

modalities and brands

Bowflex ranks #1 in

awareness

Nautilus and Schwinn also

rank near top of awareness

Universal is untapped

opportunity

All brands ranked at the top

of the industry for quality,

durability, and company

reputation

Bowflex: Innovative, Quick

and Proven Results

Nautilus: Serious Fitness

Schwinn: Quality Cardio

Differentiated brands allow

greater market flexibility

Unique consumer segments

•

•

•

•

•

•

•

•

•

and product opportunities for

each brand

Roadmap established to drive

licensing direction

•

Recognized

Brands

Desired

Attributes

Market

Opportunities |

Objectives and

Strategies – Getting to the Goal

STRATEGIES/METRICS

How we grow and compete

Added core competencies

How we do what we do

The scorecard

13

KEY

ELEMENTS

Business Strategies

Operational Capabilities

Organizational

Financials

Plans to achieve the desired business profile

are being implemented

OUR

EXPECTATIONS

FOR

THE

FUTURE |

Business

Strategy for the Future –

Ideal State

•

New products focus / diversified product line offering

Expanded cardio and alternative fitness

Stabilized and growing strength business

•

Brands further developed via internal marketing and licensing

•

Expanded International sales; growth on a paced, low risk basis

Represents <1% today

•

Expanded Licensing opportunities to extend brand building and increase

royalty stream

•

Further built-in resilience to consumer credit environment via product

diversification

•

Maximized shareholder return including optimal use of cash

•

Achieved desired level of Organizational Excellence

Culture of improvement, innovation, and execution

14 |

Targeted

Financial Objectives – Potential for the Future

•

Revenue growth pace approximating 9% / year for both Retail and Direct

Direct: Keeping current pace a low double digit / year

Retail: Slower start but achieving 8-9 % / year as we continue to execute and the

consumer spending environment improves

•

Gross margin improvement of 3-4% points

Retail:

Turnaround

trend

expected

to

begin

second

half

2012

and

build

from

there

over

the

longer

term

Direct: Further modest gains possible

•

Operating expense: Greater leverage is possible 1-3% points

S&M investment for new product launches is mostly scalable

Gradual continued R&D investment

Investment in brand development

Operating income range approximating 7-10% (versus 2% in 2011) *

* Excludes oppty’s / changes in licensing royalty stream

15

Although we are not yet positioned to identify precise timeframes for achievement

of our objectives, we believe that with continued execution of our

strategy we can deliver long term financial performance in-line with

top performing peers |

Levers to

Generate Growth and Increased Profitability Unique

Multi-Channel

Business Model

Capabilities

Cost

Opportunities in

Supply Chain

Strongest Brands

in the Industry

(Including #1)

Balance Sheet

Provides

Flexibility

for Growth

Re-invigorated New

Product Development and

Diversification

Strong

Company

Culture

Overhead

Structure is Highly

Leverage-able

Very Efficient

Working Capital

Model

Significant

Licensing

Royalty

Stream

Low Market

Share in Retail

Un-penetrated

International

Markets

16 |

Revenue

Growth

Margin

Improvements

Operating

Expense

New Product Pipeline

(more, and more diverse)

Brand Leverage

Increased Retail Share

International

Increased Licensing

Supply Chain Efficiencies

Cost Improvements

Leveraging Overhead Structure

Marketing and Media Efficiency

Strong Company Culture

(continuous improvement)

Generating Long Term EPS Growth

17 |

•

Deliver short term improvements while building for the future

–

Build in sustainable improvements

•

Exploit

our

competitive

advantages

in

brands,

product

quality

and

innovation,

marketing

expertise,

and

customer

loyalty

•

Diagnose, plan, deploy, and course correct when necessary

–

Create culture of optimization and search out opportunities

•

Tight controls on operating expense and working capital

Themes of Execution

18

These underlying themes of execution will enable us to

advance our initiatives with pace |

Summary

•

We have built a strong foundation for execution of our strategies to achieve

the ideal state and to realize the potential in the business

•

Management team is focused on key strategies and initiatives to deliver the

mid-term financial objectives

•

Additional

underpinnings

to

support

our

longer

term

strategy

for

growth

are

being implemented in 2012 / 2013

Product development and diversification

Brand development and penetration, including licensing

Cost structure and operational capabilities

Organizational Excellence

•

Always mindful of return to shareholders via EPS growth and capital

allocation

19

The potential is there, the plan is clear, the trajectory is good

|

Summary

– Long Term EPS Growth Potential

20

Strong EPS growth / year

Operating Expense Leverage 1-3 pts lower

Gross Margin Improvement 3-4 pts higher

Revenue Growth –

Sustaining 9-10% / year

Operating Income @ 7-10% and increasing at double digit pace

+

Cash generation

We are focused on delivering value to our shareholders through sustained EPS

growth. By executing our strategies, we expect to deliver strong EPS

growth over the long term. |

Nautilus

Business Profile Historical Perspective

21 |

Nautilus Cardio

Product Lines TreadClimber by Bowflex

Schwinn Fitness

Nautilus

CoreBody Reformer

22 |

Nautilus

Strength Product Lines Bowflex / Nautilus

SelectTech Dumbbells

Bowflex Revolution and Rod Based

Home Gyms

Universal Strength Accessories

Bowflex BodyTower

23 |

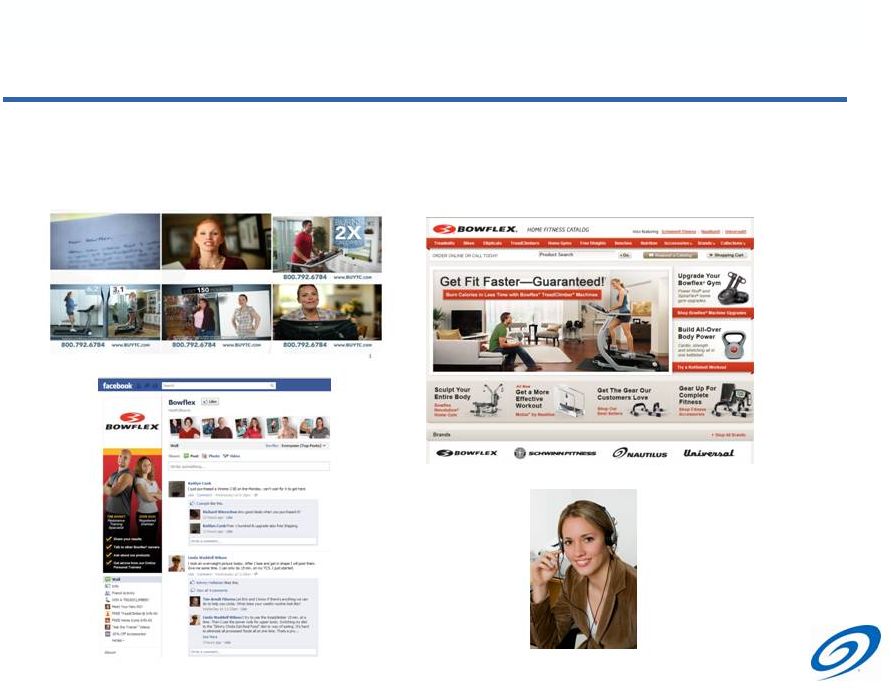

•

Direct to Consumer

–

Our direct to consumer business utilizes television and online advertising, in

addition to social media, to drive sales via our websites and call center

Consumer Reach -

Direct

24 |

Consumer Reach

– Retail

•

Retail

–

Distributes products via multiple third-party retailers located in the US and

Canada, as well as through leading e-commerce sites such as Amazon.com

25 |

Nautilus

History •

Revenues peaked at $ 680M* in 2006, however profitability was eroding, cash dwindling

and debt was rising

•

Economic downturn in 2008 / 2009 negatively affected consumer discretionary purchases

•

Commercial and Pearl Izumi businesses divested in 2008 / 2009 and largely eliminated

debt while shoring up the balance sheet

•

Restructured in 2009-2010 to focus on the consumer market

Direct to consumer via TV / Internet

Retail via both traditional store placement and leading e-commerce sites

*Includes income from discontinued and continuing operations

26

1986:

Founded as

Bowflex of

America

1993:

DRTV

marketing

begins

1999:

Acquired

Nautilus Inc -

expansion

into

commercial

clubs

2001:

Acquired

Schwinn Fitness

and entered

retail market

2005:

Acquired

Pearl iZumi

with plans to

expand into

fitness apparel

market

2006:

Peak

revenues

as sales

exceed

$600M

2008:

Sold Pearl

iZumi

business

2009:

Divested

commercial

brands via sale

and licensing

agreements

2010:

Restructured

to focus on

consumer

markets

2011:

Achieved

annual

profitability for

first time since

2006 |

Revenue and

Income from both Discontinued and Continuing Operations *2012 LTM results shown are for

the last twelve month’s actual performance which includes July 2011 through June 2012

27

Net Income Progress

($100)

($80)

($60)

($40)

($20)

$0

$20

$40

$0

$100

$200

$300

$400

$500

$600

$700

$800

2005

2006

2007

2008

2009

2010

2011

2012 LTM*

Net Revenue

Net Income / (Loss)

$631

$680

$569

$439

$264

$181

$181

$188

$23

$29

($56)

($91)

($53)

($23)

$1

$5

Revenue and Net Income

($ Millions) |

|