Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended June 30, 2012

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-16073

UNWIRED PLANET, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 94-3219054 | |

| State or other jurisdiction of incorporation or organization |

(I.R.S. Employer Identification No.) | |

| 2100 Seaport Blvd. Redwood City, California | 94063 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code

(650) 480-8000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, $0.001 Par Value | The NASDAQ Stock Market LLC (NASDAQ Global Select Market) |

Securities registered pursuant to section 12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer x | |

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) |

Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act): Yes ¨ No x

The aggregate market value of the voting stock held by non-affiliates of the registrant was approximately $134,990,661 as of December 31, 2011 based upon the closing sale price on the NASDAQ Global Select Market reported for such date. Shares of Common Stock held by each officer and director have been excluded in that such persons may be deemed to be affiliates. Shares of Common Stock held by other persons, including persons who own more than 5% of the outstanding shares of common stock, have not been excluded in that such persons are not deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

There were 90,311,159 shares of the registrant’s Common Stock issued and outstanding as of August 31, 2012.

DOCUMENTS INCORPORATED BY REFERENCE

The following documents, or portions thereof, are incorporated by reference into the following parts of this Form 10-K:

Proxy Statement for the 2012 Annual Meeting of Stockholders—Part III, Items 10, 11, 12, 13 and 14.

Table of Contents

| Page | ||||||

| PART I |

||||||

| Item 1. |

1 | |||||

| Item 1A. |

4 | |||||

| Item 1B. |

12 | |||||

| Item 2. |

12 | |||||

| Item 3. |

12 | |||||

| Item 4. |

14 | |||||

| PART II |

||||||

| Item 5. |

15 | |||||

| Item 6. |

16 | |||||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

17 | ||||

| Item 7A. |

31 | |||||

| Item 8. |

32 | |||||

| Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

34 | ||||

| Item 9A. |

34 | |||||

| Item 9B. |

34 | |||||

| PART III |

||||||

| Item 10. |

35 | |||||

| Item 11. |

35 | |||||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

35 | ||||

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

36 | ||||

| Item 14. |

36 | |||||

| PART IV |

||||||

| Item 15. |

37 | |||||

| 38 | ||||||

Table of Contents

Forward-Looking Statements

In addition to historical information, this Annual Report on Form 10-K (“Annual Report”) contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”). These forward-looking statements are based upon current expectations and beliefs of our management and are subject to numerous risks and uncertainties, including economic and market variables. Words such as “expects”, “intends”, “plans”, “believes”, “estimates” and similar expressions identify such forward-looking statements. Forward-looking statements include, among other things, statements regarding our ability to successfully realize the value of our intellectual property, our success in litigation and enforcement actions, the information and expectations concerning our future financial performance and potential or expected growth in the markets which relate to our intellectual property, business strategy, projected plans and objectives, the regulatory environment related to our business and our intellectual property, anticipated cost savings from restructurings, and our estimates with respect to future operating results. These forward-looking statements are merely predictions, not historical facts, and are subject to risks and uncertainties that could cause actual results to differ materially from those indicated in the forward-looking statements. These risks and uncertainties include our ability to realize the value of our patents, the uncertainty of our business model, the risks associated with patent litigation, the uncertainty of the regulatory environment, our ability to acquire patents, our ability to retain management and key personnel, and the other risks discussed below in “Item 1A. Risk Factors.” The occurrence of the events described above or in “Item 1A. Risk Factors” below could harm our business, results of operations and financial condition. These forward-looking statements are made as of the date of this Annual Report and we undertake no obligation to revise or publicly release the results of any revision to these forward-looking statements. Readers should carefully review the risk factors described below and in any subsequently filed reports.

PART I

Unwired Planet, Inc. (referred to as “Unwired Planet”, “our”, “we” or “us”) is an intellectual property and technology licensing company. Over the years, we have amassed a patent portfolio of approximately 200 issued United States and foreign patents and approximately 75 pending applications, many of which are considered formative to mobile communications and span smart devices, cloud technologies and unified messaging.

Unwired Planet, formerly known as Openwave Systems Inc., was incorporated in 1994 as a Delaware corporation, and we completed our initial public offering in June 1999. Our principal executive offices are located at 2100 Seaport Boulevard, Redwood City, CA 94063. Our telephone number is (650) 480-8000. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to the Securities Exchange Act of 1934, are available free of charge through our website at www.unwiredplanet.com, as soon as reasonably practicable after we file or furnish such material with the Securities and Exchange Commission (SEC). Information contained on our website is not incorporated by reference to this Annual Report.

Unwired Planet is focused on pursuing a multi-pronged strategy to realize the value of our patent portfolio, which ranges from direct licensing or sale of our patents, litigation, joint ventures, and partnering with one or more intellectual property specialists. We generate revenue by licensing our patented innovations and technologies to companies that develop mobile communications software infrastructure or hardware and/or develop mobile communications products. Our goal is to continue to create additional licensing opportunities.

1

Table of Contents

Background

Our company began in 1994 as Libris, Inc. and quickly became known as Unwired Planet. In 1999, Unwired Planet acquired Apiion, Ltd. of Belfast, Ireland and changed its name to Phone.com. After acquiring several high-tech startup companies and merging with Software.com in 2001, we changed our name to Openwave Systems, Inc., focusing on the development and delivery of mobile and fixed broadband software infrastructure to a global base of communication service providers.

In January 2012, we announced the pursuit of strategic alternatives to divest our product businesses and narrow our focus on our intellectual property business. On February 1, 2012, we sold our location business to Persistent Telecom Solutions Inc. (“Persistent”), a wholly-owned subsidiary of Persistent Systems Ltd., a leader in software product development. On April 30, 2012, we completed the sale of our mediation and messaging product businesses to Openwave Mobility, Inc. (formerly, OM1, Inc., “Openwave Mobility”), a portfolio company of Marlin Equity Partners, a private investment firm.

Unwired Planet is now solely focused on a multi-pronged intellectual property strategy that includes, among other things, licensing and, when necessary, litigation to protect the value of its patent portfolio. In May 2012, we officially changed our name back to Unwired Planet, a name which recalls the formative years when many of our foundational mobile communication patents were filed, and began trading on NASDAQ under the new symbol: UPIP.

Target Licensees

In October 2010, we signed our first licensing agreement with Mobixell/724, and in November 2011 we announced a licensing deal with Microsoft that covers our portfolio of approximately 200 patents.

In August 2011, we filed a complaint with the International Trade Commission (“ITC”) in Washington, DC, against Apple Inc. (“Apple”) and Research In Motion Limited in order to protect our intellectual property that pertains to how mobile devices connect to the Internet. We also simultaneously filed a similar complaint in federal district court in Delaware. We believe that these large companies should pay us to use the technologies that we invented—particularly in light of the substantial revenue these companies have earned from devices that we believe use our patented technology.

Intellectual Property Focus

Unwired Planet established many of the foundational patents that allow mobile devices to connect to the Internet. Over the years, we have amassed a patent portfolio of approximately 200 issued United States and foreign patents and approximately 75 pending applications, many of which are considered foundational to mobile communications.

Unwired Planet’s founding team was among the first to consider and solve the technical and practical problems of accessing useful data on mobile devices, such as the Internet, user data and access to a variety of personal and enterprise applications, solutions for which are reflected in our earliest patents. Developing and deploying these groundbreaking solutions led to a robust and continuous pattern of creativity and innovation in mobility. Inventors at Unwired Planet focused on many forms of data and improved ways in which this data could be transferred, accessed, secured and used, both from the perspective of a mobile device and from the perspective of networks and servers communicating with mobile devices.

2

Table of Contents

For example, Unwired Planet and its subsidiaries invented in the areas of wireless push and broadcast, device provisioning and application access, messaging, location services, advertising, mobile payments, fleet management, authentication and privacy. Unwired Planet contributed fundamental principles to the marketplace of ideas upon which today’s mobile industry is built, with broad contributions benefiting wireless network operators, smartphone manufacturers, cloud service providers and essentially all mobile application developers.

Operating Environment and Trends

A licensing strategy requires other parties to be reasonable and willing to work out a fair royalty arrangement. In fact, many of these parties have teams in place precisely for the purpose of delaying or avoiding such a royalty discussion. Our potential licensees’ willingness and ability to pay reasonable royalties is, in part, affected by the number of patents infringed by a particular licensee product, the concentration of the holders of those patents, the licensee’s cost of licensing those patents, and the profitability of the infringing product.

Reasonable royalties for our patented inventions are best secured through negotiated license agreements thereby avoiding the uncertainties of litigation. Obtaining reasonable royalties for the use of our patents is generally dependent upon:

| • | Demonstrating infringement of claimed inventions; |

| • | Defeating arguments that our patents are invalid or unenforceable; and |

| • | Providing data supporting the royalties we are seeking. |

Some of the companies that we believe use our patented technology may not voluntarily enter into license agreements. As a result, we have developed abilities to plan, execute and sustain litigation campaigns and enforcements to protect our patent portfolio.

Competition

We believe that our principal competition for our patents may come from our prospective licensees, some of whom are evaluating and developing products based on technologies that they contend or may contend will not require a license from us. These companies include but are not limited to: communication service providers, handset manufacturers, software providers using mobile communications and mobile product companies. To the extent that these companies perceive there is no requirement to pay Unwired Planet royalties, or to the extent other factors influence the industry, our licensees and prospective licensees may adopt and promote alternative technologies. Even to the extent we determine that such alternative technologies infringe our patents, there can be no assurance that we would be able to negotiate agreements that would result in royalties being paid to us without litigation, which could be costly and the results of which would be uncertain. Litigation has been, and may continue to be, required to enforce and protect our intellectual property rights.

Employees

As of June 30, 2012, we had 37 employees. We anticipate a further reduction in our headcount once we complete the performance of services under the Transition Services Agreement (“TSA”) we entered into with Openwave Mobility, the buyer of the mediation and messaging product lines.

3

Table of Contents

Financial Information about Geographic Areas

For Unwired Planet’s financial information about geographic areas, please see Note 5 to the Consolidated Financial Statements included in this Annual Report on Form 10-K.

Our business is subject to a number of risks, many of which are described below. If any of the events described in these risks factors actually occur, our business, financial condition or results of operations could be materially and adversely affected, which would likely have a corresponding impact on the value of our common stock. Further, the risk factors described below could cause actual results to differ materially from the results contemplated by the forward-looking statements contained in this report. These risk factors should be reviewed carefully.

Risks Related to Our Business

Our efforts to realize the value of our patents may not be successful, which may lead to expensive and time-consuming litigation.

We rely on patent laws to protect our intellectual property or proprietary rights, although we believe that other factors such as the technological and creative skills of our personnel are also essential to maintaining a technology leadership position. We also rely on trademark law to protect the value of our corporate brand and reputation. In addition, we have divested our product businesses and intend to take actions to realize the value of our patent portfolio by pursuing patent licensing agreements and/or litigation. These efforts may not result in additional revenues, and may also result in counter-claims of non-infringement or invalidity being raised by third parties.

Despite our efforts to license and protect our intellectual property and proprietary rights, unauthorized parties may copy or otherwise obtain and use our technology or trademarks. Effectively policing and enforcing our intellectual property is time consuming and costly, and the steps taken by us may not prevent infringement of our intellectual property or proprietary rights and trademarks, particularly in foreign countries where in many instances the local laws or legal systems do not offer the same level of protection as in the United States.

We have brought legal action against Apple Inc. and Research In Motion in our efforts to realize the value of our patents, which may be expensive and time-consuming and may lead to outcomes and counterclaims against us that may have an adverse effect on our business.

We have filed a complaint with the ITC in Washington, DC, with Apple Inc. (“Apple”), Research In Motion Ltd. and Research In Motion Corp. as proposed respondents, requesting that the ITC bar Apple and the Research In Motion entities from importing into the United States their products, including smart devices and tablet computers, that infringe our patents cited in the complaint. The complaint alleges that Apple and RIM infringe upon four of our patents that cover technology that gives consumers access to the Internet from their mobile devices. We also filed a similar complaint against Apple and RIM in the federal district court of Delaware, asserting the same claims and seeking an injunction and damages. These lawsuits may be time consuming and costly, and result in the significant diversion of management’s attention. Further, as is typical in lawsuits like these, Apple and RIM have asserted counterclaims challenging the validity of our patents. Although we believe that our position is well founded, intellectual property litigation is uncertain, and if we are not able to prevail on our claims, our ability to collect royalties from our patents will be substantially undermined.

4

Table of Contents

We may become involved in litigation proceedings related to our former customers.

We have retained certain ongoing liabilities with respect to indemnification claims related to our former customers that were initiated prior to the closing of the sale of our Messaging and Mediation product businesses to Openwave Mobility and the sale of our location product business to Persistent Telecom Solutions. Although we have not elected to do so in the past, we may elect to seek a license or otherwise settle outstanding claims of infringement. Any litigation related to such indemnification claims could be costly and time consuming and could divert our management and key personnel from our intellectual property strategy and our business operations. The complexity of the technology involved increases the risks associated with intellectual property litigation. Royalty or licensing arrangements, if required, may not be available on terms acceptable to us, if at all. Any infringement claim successfully asserted against us by one of our former customers which arose prior to the closing of the sale of our Messaging and Mediation product business or the sale of our location products for which we have retained liability could result in costly litigation as well as the payment of substantial damages or an injunction.

Our revenues may be unpredictable, and this may harm our financial condition.

Our business strategy to realize the value of our patent portfolio, which may include acquiring patents and patent applications, is expected to be unpredictable and volatile with respect to revenues in future periods. Our patent portfolio includes 200 issued U.S. and foreign patents and 75 pending patent applications and covers technologies used in a wide variety of industries. Acquisitions of additional intellectual property may expand and diversify our revenue generating opportunities. However, due to the nature of a licensing business and uncertainties regarding the amount and timing of the receipt of license and other fees from licensees or potential infringers, stemming primarily from uncertainties regarding the outcome of enforcement actions, the growth rates of our existing licensees and certain other factors, our revenues may vary significantly from quarter to quarter, which could make our business difficult to manage, adversely affect our business and operating results, cause our quarterly results to fall below market expectations and adversely affect the market price of our common stock.

Focusing our business model on realizing the value of our intellectual property is a relatively recent initiative and may not result in anticipated benefits.

We announced the divestiture of our products business in April 2012 and are focusing our efforts on realizing the value of our intellectual property. We have a limited operating history and a limited track record with respect to our intellectual property strategy, which could make it difficult to evaluate our current business and future prospects. We have encountered and will continue to encounter risks and difficulties frequently experienced by companies with evolving business strategies. If we do not manage these risks successfully, our business and operating results will be adversely affected. In addition, our intellectual property strategy may have other adverse consequences, such as employee attrition, the loss of employees with valuable knowledge or expertise or a negative impact on employee morale. Our strategy may place increased demands on our personnel and could adversely affect our ability to attract and retain talent, and to perform our accounting, finance and administrative functions. We may not realize all of the anticipated benefits of our prior or any future strategies.

We have a history of losses and we may not be able to achieve or maintain consistent profitability.

We have a history of losses and may not be able to maintain consistent profitability. Except for fiscal 2006, we have incurred annual net losses since our inception. As of June 30, 2012, we had an accumulated deficit of approximately

5

Table of Contents

$3.1 billion, which includes approximately $2.1 billion of goodwill amortization and impairment. We expect to continue to spend significant amounts to execute our intellectual property initiatives, which may not generate significant revenue in future periods. Our prospects must be considered in light of the risks, expenses, delays and difficulties frequently encountered by companies with business strategies similar to ours.

If we are unable to substantially utilize our net operating loss carryforwards, our financial results will be adversely affected.

As of June 30, 2012, we had net operating loss, or NOL, carryforwards for U.S. federal and state income tax purposes of approximately $1.6 billion and $601.8 million, respectively. Under Section 382 of the Internal Revenue Code, a corporation that undergoes an “ownership change” may be subject to limitations on its ability to utilize its pre-change NOLs to offset future taxable income. In general, an ownership change occurs if the aggregate stock ownership of certain stockholders (generally 5% stockholders, applying certain look-through and aggregation rules) increases by more than 50% over such stockholders’ lowest percentage ownership during the testing period (generally three years). Purchases of our common stock in amounts greater than specified levels, which will be beyond our control, could create a limitation on our ability to utilize our NOLs for tax purposes in the future. Although we have taken steps to preserve our ability to utilize our NOLs, such efforts may not be successful. Limitations imposed on our ability to utilize NOLs could cause U.S. federal and state income taxes to be paid earlier than would be paid if such limitations were not in effect and could cause such NOLs to expire unused, in each case reducing or eliminating the benefit of such NOLs. Furthermore, we may not be able to generate sufficient taxable income to utilize our NOLs before they expire. If any of these events occur, we may not derive some or all of the expected benefits from our NOLs. In addition, at the state level there may be periods during which the use of NOLs is suspended or otherwise limited, which would accelerate or may permanently increase state taxes owed.

If we are unable to successfully maintain or license existing patents or develop and acquire new patents and patent applications, our ability to generate revenues could be substantially impaired.

Our ability to compete in the future will depend on our continued efforts and success in licensing existing patents, including maintaining and prosecuting our patents properly, and may include acquiring new patents and patent applications with licensing and enforcement opportunities. While we expect for the foreseeable future to have sufficient liquidity and capital resources to maintain the level of maintenance and/or acquisitions necessary, various factors may require us to have greater liquidity and capital resources than we currently expect. If we are unable to successfully maintain and license our existing patents and acquire new patents and patent applications, our ability to generate revenues could be substantially impaired and our business and financial condition could be materially harmed.

Our success may depend in part upon our ability to retain the best legal counsel to represent us in patent enforcement litigation.

The success of our intellectual property licensing business may depend upon our ability to retain the best legal counsel to prosecute patent infringement litigation. As our patent enforcement actions increase, it may become more difficult to find the best legal counsel to handle all of our cases because many of the best law firms may have a conflict of interest that prevents their representation of us.

6

Table of Contents

In connection with patent enforcement actions that we may conduct, a court may rule that we have violated certain statutory, regulatory, federal, local or governing rules or standards, which may expose us to certain material liabilities.

In connection with any of our patent enforcement actions, it is possible that a defendant may request and/or a court may rule that we have violated statutory authority, regulatory authority, federal rules, local court rules, or governing standards relating to the substantive or procedural aspects of such enforcement actions. In such event, a court may issue monetary sanctions against us or award attorney’s fees and/or expenses to a defendant(s), which could be material, and if we are required to pay such monetary sanctions, attorneys’ fees and/or expenses, such payment could materially harm our operating results and our financial position.

Our exposure to uncontrollable outside influences, including new legislation and court rulings or actions by the United States Patent and Trademark Office, could adversely affect our ability to execute on our patent strategy and licensing initiatives and our results of operations.

We may spend a significant amount of resources to enforce existing and any newly acquired patents. If new legislation, regulations or rules are implemented either by Congress, the U.S. Patent and Trademark Office, or USPTO, or the courts that impact the patent application process, the patent enforcement process or the rights of patent holders, these changes could negatively affect our expenses and revenue. For example, new rules regarding the burden of proof in patent enforcement actions could significantly increase the cost of any enforcement actions, and new standards or limitations on liability for patent infringement could negatively impact our revenue derived from such enforcement actions.

In addition, it is difficult to predict the outcome of patent enforcement litigation at the trial level and the amount of time it may take to complete an enforcement action. It is often difficult for juries and trial judges to understand complex patents and patent applications, and as a result, there is a higher rate of successful appeals in patent enforcement litigation than more standard business litigation. Such appeals are expensive and time consuming, resulting in increased costs and delayed revenue. Although we intend to diligently pursue enforcement litigation, we cannot predict with significant reliability the decisions made by juries and trial courts.

Our acquisitions of patents and patent applications may be time consuming, complex and costly, which could adversely affect our operating results.

Our acquisitions of patents and patent applications may be time consuming, complex and costly to consummate. We may utilize many different transaction structures in our acquisitions and the terms of the acquisition agreements may be very heavily negotiated. As a result, we may incur significant operating expenses during the negotiations even where the acquisition is ultimately not consummated. In addition, as a result of any future acquisitions, we might need to issue additional equity securities, spend our cash or incur debt or assume significant liabilities, any of which could adversely affect our business and results of operations. Even if we successfully acquire particular patents, there is no guarantee that we will generate sufficient revenue related to those patents to offset the acquisition costs. While we intend to conduct confirmatory due diligence on the patents we are considering for acquisition, we may acquire patents from a seller who does not have proper title to those assets. In those cases, we may be required to spend significant resources to defend our interests in the patents and, if we are not successful, our acquisition may be invalid, in which case we could lose part or all of our investment in the patents.

7

Table of Contents

We may be unable to effectively manage future growth, if any, that we may achieve.

As a result of our efforts to control costs through restructurings and otherwise, our ability to effectively manage and control any future growth may be limited. To manage any growth, our management must continue to improve our operational, information and financial systems, procedures and controls and expand, train, retain and manage our employees. If our systems, procedures and controls are inadequate to support our operations, any expansion could decrease or stop, and investors may lose confidence in our operations or financial results. If we are unable to manage growth effectively, our business and operating results could be adversely affected, and any failure to develop and maintain adequate internal controls could cause the trading price of our shares to decline substantially.

Compliance with laws, rules and regulations relating to corporate governance and public disclosure may result in additional expenses.

Federal securities laws, rules and regulations, as well as NASDAQ rules and regulations, require companies to maintain extensive corporate governance measures, impose comprehensive reporting and disclosure requirements, set strict independence and financial expertise standards for audit and other committee members and impose civil and criminal penalties for companies and their chief executive officers, chief financial officers and directors for securities law violations. These laws, rules and regulations and the interpretation of these requirements are evolving, and we are making investments to evaluate current practices and to continue to achieve compliance. As a result, our compliance programs have increased and will continue to increase general and administrative expenses and have diverted and will continue to divert management’s time and attention from revenue-generating activities. Further, in July 2010, Congress enacted the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) which includes various provisions requiring the Securities and Exchange Commission to adopt new rules and regulations with respect to enhanced investor protection, corporate governance and executive compensation. We expect the Dodd-Frank Act and the rules and regulations promulgated thereunder to increase our legal and financial compliance costs and to make some activities more time consuming and costly.

As we reduce our management and other personnel in connection with and following the sale of our businesses, our remaining management team and other personnel may face increased demands and we may not be able to operate our business effectively, execute on our business objectives or comply with the laws and regulations applicable to us.

In connection with the sale of our businesses, we have and will continue to reduce our personnel, including members of management. As a result, future members of management and our personnel may face significant demands in order to operate our business. If our management is unable to effectively operate our business and pursue our business objectives as a result of the reduction in personnel and other resources, our results of operations could suffer and the market price of our stock could decline.

As a public company, we are subject to the Exchange Act, the Sarbanes-Oxley Act, the Dodd-Frank Act, the listing requirements of NASDAQ and other applicable securities rules and regulations requiring us to, among other things, satisfy certain corporate governance requirements, file periodic reports with respect to our business and operating results and maintain effective disclosure controls and procedures and internal control over financial reporting. Our management and other personnel currently do, and will continue to, devote a substantial amount of time and resources to ensure that we comply with these requirements. However, with the reduction in personnel due to the sale of our businesses, the demands on our management and other personnel will increase and their time and attention may

8

Table of Contents

be diverted. We may need to hire more employees in the future or engage outside consultants to ensure that we are able to comply with these requirements, which will increase our costs and expenses. If we are not able to comply with the requirements of the rules and regulations applicable to us in a timely manner, we could be subject to sanctions or investigations by the SEC or other regulatory authorities, which would require additional financial and management resources, and our investors may not have access to timely information.

We face litigation risks that could have a material adverse effect on our company.

We may be the subject of private or government actions. For example, in the past we have been the subject of several shareholder derivative lawsuits relating to our past option grants and practices. Litigation may be time-consuming, expensive and disruptive to normal business operations, and the outcome of litigation is difficult to predict. The defense of these lawsuits may result in significant expense and a diversion of management’s time and attention from the operation of our business, which could impede our ability to achieve our business objectives and an unfavorable outcome may have a material adverse effect on our business, financial condition and results of operations. Additionally, any amount that we may be required to pay to satisfy a judgment or settlement of litigation may not be covered by insurance. Under our charter and the indemnification agreements that we have entered into with our officers and directors, we are required to indemnify, and advance expenses to them in connection with their participation in proceedings arising out of their service to us. There can be no assurance that any of these payments will not be material.

Our revolving credit facility with Silicon Valley Bank contains restrictive covenants that limit our discretion in the operation of our business, which could have a materially adverse effect on our business, financial condition and results of operations.

In January 2009, we entered into a $40.0 million secured revolving credit facility with Silicon Valley Bank, as subsequently amended, which contains numerous restrictive covenants that require us to comply with and maintain specified financial tests and ratios, thereby restricting our ability to:

| • | Incur debt; |

| • | Incur liens; |

| • | Redeem or prepay subordinated debt; |

| • | Make acquisitions of businesses or entities to sell specified assets; |

| • | Make investments, including loans, guarantees and advances; |

| • | Make capital expenditures beyond a specified threshold; |

| • | Engage in transactions with affiliates; |

| • | Pay dividends or limit the amount of stock repurchases; and |

| • | Enter into specified restrictive agreements. |

Our ability to comply with covenants contained in our credit agreement may be affected by events beyond our control, including prevailing economic, financial and industry conditions.

9

Table of Contents

Our current credit agreement is secured by a pledge of all of our assets. If we were to default under our current credit agreement, including a default of our financial covenants, and were unable to obtain a waiver or an amendment for such a default, the lender would have a right to foreclose on our assets in order to satisfy our obligations, if any, under the current credit agreement and could require us to put up cash collateral for any outstanding letter of credit balances. Any such action on the part of the lender against us could have a materially adverse impact on our business, financial condition and results of operations. On January 23, 2012, we entered into an amendment to extend the maturity of the secured revolving credit facility to February 28, 2012 and reduce the amount of the line of credit facility from $40.0 million to $25.0 million. On April 12, 2012, we entered into an amendment to extend the maturity of the secured revolving credit facility to April 28, 2013 and set minimum EBITDA levels. On May 4, 2012, we entered into an amendment to reduce the amount of the line of credit from $25.0 million to $18.0 million, delete the Borrowing Base requirement, delete the minimum EBITDA covenant, delete the fee on undrawn amounts, and modify the Liquidity Coverage Ratio definition.

If we are unable to extend the maturity of the secured revolving credit facility for an additional twelve month period, our business could be adversely affected.

We depend on recruiting and retaining key management with patent and intellectual property experience.

Our performance depends on attracting and retaining key management and other employees with the requisite expertise. In particular, our future success depends in part on the continued service of our employees, including key executives. Competition for qualified personnel in the San Francisco Bay Area in which we are located is significant. We believe that there are only a limited number of persons with the requisite skills to serve in many of our key positions, and it is generally difficult to hire and retain these persons. Furthermore, it may become more difficult to hire and retain key persons as a result of our past restructurings, any future restructurings, and our past stock performance. Competitors may in the future attempt to recruit our employees. In the event of turnover within key positions, integration of new employees will require additional time and resources, which could adversely affect our business plan. If we are unable to attract or retain qualified personnel, our business could be adversely affected.

Risks Related to Owning Our Common Stock

Our quarterly operating results may fluctuate significantly as a result of factors outside of our control, which could cause the market price of our common stock to decline.

We expect our revenues and operating results to vary from quarter to quarter. As a consequence, our operating results in any single quarter may not meet the expectations of securities analysts and investors, which could cause the price of our common stock to decline. Our licensing revenue is difficult to forecast and is likely to fluctuate from quarter to quarter.

Factors that may lead to significant fluctuation in our operating results include, but are not limited to:

| • | restructuring or impairment charges we may take; |

| • | the timing of the receipt of periodic license fee payments; |

| • | fluctuations in the net number of active licensees period to period; |

10

Table of Contents

| • | costs related to acquisitions, alliances, licenses and other efforts to expand our operations; |

| • | the timing of payments under the terms of any license agreements into which we may enter; |

| • | expenses related to, and the timing and results of, patent filings and other enforcements proceedings relating to intellectual property rights; |

| • | revenue recognition and other accounting policies; |

| • | the perceived relevance and value in our existing patent asset portfolio by existing or potential licensees; |

| • | changes in and timing of new governmental, statutory and industry association laws, regulations, procedures or requirements; |

| • | fluctuations in currency exchange rates; and |

| • | industry and economic conditions, including competitive pressures or conditions that affect the intellectual property risk and management of existing or potential licensees. |

Our operating results could be impacted by the amount and timing of operating costs and capital expenditures relating to our business and our ability to accurately estimate and control costs. Most of our expenses, such as compensation for current employees and lease payments for facilities and equipment, are largely fixed. In addition, our expense levels are based, in part, on our expectations regarding future revenues. As a result, any shortfall in revenues relative to our expectations could cause significant changes in our operating results from period to period. In this regard, our bookings may not be indicative of revenue that will be recognized in current or subsequent periods. Due to the foregoing factors, we believe period-to-period comparisons of our historical operating results may be of limited use. In any event, we may be unable to meet our internal projections or the projections of securities analysts and investors. If we are unable to do so, we expect that, as in the past, the trading price of our stock may fall dramatically.

Provisions of our corporate documents and Delaware law may discourage an acquisition of our business, which could affect our stock price.

Our charter and bylaws may inhibit changes of control that are not approved by our Board of Directors. In particular, our certificate of incorporation includes provisions for a classified Board of Directors, authorizes the Board of Directors to issue preferred stock without stockholder approval, prohibit cumulative voting in director elections and prohibits stockholders from taking action by written consent. Further, our bylaws include provisions that prohibit stockholders from calling special meetings and require advance notice for stockholder proposals or nomination of directors. We are also subject to Section 203 of the Delaware General Corporation Law, which generally prevents a person who becomes the owner of 15 percent or more of the corporation’s outstanding voting stock from engaging in specified business combinations for three years unless specified conditions are satisfied. These provisions could have the effect of delaying or preventing changes in control or management.

Our stock price has been and is likely to continue to be volatile and you may not be able to resell shares of our common stock at or above the price you paid, if at all.

The trading price of our common stock has experienced wide fluctuations due to the factors discussed in this risk factors section and elsewhere in this Annual Report. In addition, the stock market in general has, and the NASDAQ Global Market and technology companies in particular have, experienced extreme price and volume fluctuations. These trading prices and valuations may not be sustainable. These broad market and industry factors may decrease the

11

Table of Contents

market price of our common stock, regardless of our actual operating performance. In addition, in the past, following periods of volatility in the overall market and the market price of a company’s securities, securities class action litigation has often been instituted against companies that experienced such volatility. This litigation, if instituted against us, regardless of its outcome, could result in substantial costs and a diversion of our management’s attention and resources.

Item 1B. Unresolved Staff Comments.

None.

Our principal office is located in Redwood City, California, where we lease approximately 144,000 square feet under a sublease agreement that terminates on June 29, 2013. We also have other facility leases in other locations in the United States, including our former headquarters which comprises approximately 283,000 square feet and which is currently under a sublease that expires April 29, 2013. The future lease payments, net of sublease income, for our former headquarters is included in accrued restructuring costs in our consolidated balance sheet.

We believe that our facilities are sufficient for our purposes for the foreseeable future.

Simmonds v. Credit Suisse Group, et al.

On October 3, 2007, Vanessa Simmonds, a purported stockholder of Unwired Planet, filed suit in the U.S. District Court for the Western District of Washington (“Western District Court”) against Credit Suisse Group, Bank of America Corporation, and JPMorgan Chase & Co., the lead underwriters of our initial public offering in June 1999, alleging violations of Section 16(b) of the Exchange Act, 15 U.S.C. § 78p(b). The complaint seeks to recover from the lead underwriters any “short-swing profits” obtained by them in violation of Section 16(b). The suit names us as a nominal defendant, contains no claims against us, and seeks no relief from us. Simmonds filed an Amended Complaint on February 25, 2008 (the “Amended Complaint”), naming as defendants Credit Suisse Securities (USA), Robertson Stephens, Inc., J.P. Morgan Securities, Inc., and again naming Bank of America Corporation. The Amended Complaint asserts substantially similar claims as those set forth in the initial complaint.

On March 12, 2009, the Western District Court entered its judgment in the case and granted the moving issuers’ motion to dismiss, finding plaintiff’s demand letters were insufficient to put the issuers on notice of the claims asserted against them. The Western District Court also granted the underwriters’ motion to dismiss as to the claims arising from the non-moving issuers’ IPOs, finding plaintiff’s claims were time-barred under the applicable statute of limitations.

Following an appeal to the United States Court of Appeals for the Ninth Circuit (the “Ninth Circuit”), on December 2, 2010, the Ninth Circuit affirmed the Western District Court’s decision to dismiss the moving issuers’ cases on the grounds that plaintiff’s demand letters were insufficient to put the issuers on notice of the claims asserted against them and further ordered that the dismissals be made with prejudice. The Ninth Circuit, however, reversed and remanded the Western District Court’s decision on the underwriters’ motion to dismiss as to the claims arising from the non-moving issuers’ IPOs, finding plaintiff’s claims were not time-barred under the applicable statute of

12

Table of Contents

limitations. In remanding, the Ninth Circuit advised the non-moving issuers and underwriters to file in the Western District Court the same challenges to plaintiff’s demand letters that moving issuers had filed.

On January 18, 2011, the Ninth Circuit denied all petitions for rehearing and petitions for rehearing en banc. On January 25, 2011, the Ninth Circuit granted the underwriters’ motion to stay the issuance of the mandate and ordered that the mandate in the cases involving the non-moving issuers be stayed for ninety days pending the filing of a petition for writ of certiorari in the United States Supreme Court. On January 26, 2011, the Ninth Circuit granted the appellant’s motion and ruled that the mandate in all cases is stayed for ninety days pending the appellant’s filing of a petition for writ of certiorari in the United States Supreme Court. On April 5, 2011, the plaintiff filed a Petition for Writ of Certiorari with the United States Supreme Court seeking reversal of the Ninth Circuit’s December 2, 2010 decision. On April 15, 2011, underwriter defendants filed a Petition for Writ of Certiorari with the United States Supreme Court seeking reversal of the Ninth Circuit’s December 2, 2010 decision relating to the statute of limitations issue.

On June 27, 2011, the United States Supreme Court denied Simmonds’ petition regarding the demand issue and granted the underwriters’ position relating to the statute of limitations issue. Oral argument in that case was held on November 29, 2011. On March 26, 2012, the Supreme Court vacated the Ninth Circuit’s holding that petitioner’s claims were not time barred, and remanded the cases to the District Court for proceedings consistent with the Supreme Court’s opinions.

On June 7, 2012, the mandate of the Ninth Circuit was formally entered. On June 11, 2012, Plaintiffs voluntarily dismissed the case with prejudice as to the adequacy-of-the-pre-suit demand issue, and without prejudice as to all other issues.

No amount has been accrued as of June 30, 2012, as a loss is not considered probable or reasonably estimable.

In the Matter of Certain Devices of Mobile Communication

On August 31, 2011, we filed a complaint with the International Trade Commission (“ITC”) in Washington, DC, with Apple Inc. (“Apple”), Research In Motion Ltd. and Research In Motion Corp. as proposed respondents, requesting that the ITC bar Apple and the Research In Motion entities (“RIM”) from importing into the United States their products, including smart devices and tablet computers, that infringe certain of our patents. The complaint alleges that Apple and RIM infringe upon four of our patents that cover technology that, among other things, give consumers access to the Internet from their mobile devices. The ITC matter is currently scheduled for substantive hearing commencing October 15, 2012, though dates in a legal proceeding are always subject to change at the discretion of the presiding judge.

Openwave Systems Inc. v. Apple Inc., Research in Motion Ltd, and Research in Motion Corp.

On August 31, 2011, we filed a complaint in the Federal District Court for the District of Delaware against Apple and RIM, again alleging that Apple and RIM products infringe certain of our patents, seeking among other things a declaration that our patents cited in the complaint have been infringed by Apple and RIM and that these patents are valid and enforceable, damages as a result of the infringement, and an injunction against further infringement. This action is stayed pending the outcome of the ITC case. This matter is stayed pending October 15, 2012.

13

Table of Contents

From time to time, we may be involved in litigation or other legal proceedings, including those noted above, relating to or arising out of its day-to-day operations or otherwise. Litigation is inherently uncertain, and we could experience unfavorable rulings. Should we experience an unfavorable ruling, there exists the possibility of a material adverse impact on its financial condition, results of operations, cash flows or on its business for the period in which the ruling occurs and/or in future periods.

Indemnification claims

Prior to the sale of our product businesses, our software license and services agreements generally included a limited indemnification provision for claims from third parties relating to our intellectual property. In connection with the sale of our product businesses, we retain certain ongoing liabilities with respect to indemnification claims related to our former customers that were initiated prior to the sale of the Location business line and the Messaging and Mediation product businesses. As of June 30, 2012, no amount is accrued for indemnifications as there were no existing claims where a loss is considered probable. Historically, costs related to these indemnification provisions have been infrequent and we are unable to estimate the maximum potential impact of these indemnification provisions on its future results of operations.

Three of our licensees are seeking indemnification from us under their respective license agreements in connection with being named as defendants in two matters pending in the United States District Court for the Eastern District of Texas captioned Unified Messaging Solutions, Inc. v. Google, et al. (Civil Action No. 6:11cv00464) and Unified Messaging Solutions, Inc. v. Facebook, et al. (Civil Action No. 6:11cv00120 (the “Actions”). Plaintiff in the Actions alleges that the licensees’ web-based communication services infringe patents allegedly owned by the plaintiff and the licensees claim that their web-based services are comprised of products licensed from us. We have assumed the defense on behalf of two of the licensees. With respect to the third, the licensee is conducting its own defense and has requested that we indemnify it for one-third of its defense costs and any damages awarded.

As of June 30, 2012, no amount is accrued for indemnifications as there were no existing claims where a loss is considered probable. Historically, costs related to these indemnification provisions have been infrequent and we are unable to estimate the maximum potential impact of these indemnification provisions on its future results of operations.

Item 4. Mine Safety Disclosures.

Not applicable.

14

Table of Contents

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Price Range of Common Stock

Our common stock is listed for quotation on the NASDAQ Global Select Market under the symbol “UPIP.” The following table sets forth the reported high and low closing sales prices for our common stock for the fiscal periods indicated.

| Stock price by quarter |

High | Low | ||||||

| Fiscal year ended June 30, 2012: |

||||||||

| First quarter |

$ | 2.50 | $ | 1.26 | ||||

| Second quarter |

$ | 1.77 | $ | 1.46 | ||||

| Third quarter |

$ | 2.61 | $ | 1.65 | ||||

| Fourth quarter |

$ | 3.10 | $ | 2.15 | ||||

| Fiscal year ended June 30, 2011: |

||||||||

| First quarter |

$ | 2.14 | $ | 1.59 | ||||

| Second quarter |

$ | 2.43 | $ | 1.68 | ||||

| Third quarter |

$ | 2.58 | $ | 1.98 | ||||

| Fourth quarter |

$ | 2.43 | $ | 2.02 | ||||

Holders

As of August 31, 2012 there were 335 holders of record of our common stock. Because many of our shares of common stock are held by brokers and other institutions on behalf of stockholders, we are unable to estimate the total number of stockholders represented by these record holders.

Dividend Policy

Our policy has been to retain future earnings for reinvestment in our business, and accordingly, we have not paid cash dividends other than a special one-time cash dividend paid in June 2007, and we do not anticipate paying cash dividends in the foreseeable future. Further, our line of credit restricts our ability to pay dividends.

15

Table of Contents

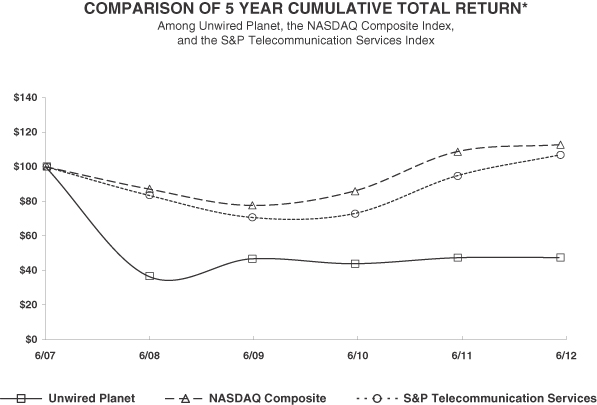

Performance Graph

The information contained in the Performance Graph shall not be deemed to be “soliciting material” or “filed” with the SEC or subject to the liabilities of Section 18 of the Exchange Act, except to the extent that we specifically incorporate it by reference into a document filed under the Securities Act or the Exchange Act.

The following graph compares the cumulative total stockholder return on our common stock, the NASDAQ Composite Index, and the S&P Telecommunication Services Index. The graph assumes that $100 was invested in our common stock, the NASDAQ Composite Index and the S&P Telecommunication Services Index on June 30, 2007, and calculates the return quarterly through June 30, 2012. The stock price performance on the following graph is not necessarily indicative of future stock price performance.

*$100 invested on 6/30/07 in stock or index, including reinvestment of dividends.

Fiscal year ending June 30.

Copyright© 2012 S&P, a division of The McGraw-Hill Companies Inc. All rights reserved.

Item 6. Selected Financial Data.

The following selected financial data should be read in conjunction with our consolidated financial statements and related notes thereto and with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this Annual Report.

16

Table of Contents

The following table sets forth selected Consolidated Statements of Operations and Consolidated Balance Sheet data, revised to reflect Musiwave, Client and the product operations as discontinued operations, for fiscal 2012, 2011, 2010, 2009 and 2008 (in thousands, except per share data):

| Fiscal Year ended June 30, | ||||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||

| Selected Consolidated Statements of Operations Data: |

||||||||||||||||||||

| Total revenues |

$ | 15,050 | $ | 4,019 | $ | — | $ | — | $ | — | ||||||||||

| Total operating expenses |

24,020 | 11,356 | 11,901 | 13,718 | 10,487 | |||||||||||||||

| Operating loss from continuing operations |

(8,970 | ) | (7,337 | ) | (11,901 | ) | (13,718 | ) | (10,487 | ) | ||||||||||

| Net income (loss) from continuing operations |

(8,150 | ) | (8,105 | ) | (11,929 | ) | (24,081 | ) | (6,846 | ) | ||||||||||

| Discontinued operations: |

||||||||||||||||||||

| Net income (loss) from discontinued operations, net of tax |

(27,577 | ) | (17,379 | ) | 1,556 | (63,795 | ) | (51,206 | ) | |||||||||||

| Gain on sale of discontinued operations |

50,294 | (9,764 | ) | 4,516 | 2,000 | 36,190 | ||||||||||||||

| Total income (loss) from discontinued operations |

22,717 | (27,143 | ) | 6,072 | (61,795 | ) | (15,016 | ) | ||||||||||||

| Net income (loss) |

$ | 14,567 | $ | (35,248 | ) | $ | (5,857 | ) | $ | (85,876 | ) | $ | (21,862 | ) | ||||||

| Basic and diluted net income (loss) per share: |

||||||||||||||||||||

| Continuing operations |

$ | (0.09 | ) | $ | (0.10 | ) | $ | (0.14 | ) | $ | (0.29 | ) | $ | (0.09 | ) | |||||

| Discontinued operations |

$ | 0.26 | $ | (0.32 | ) | $ | 0.07 | $ | (0.75 | ) | $ | (0.18 | ) | |||||||

| Basic and diluted net income (loss) per share |

$ | 0.17 | $ | (0.42 | ) | $ | (0.07 | ) | $ | (1.04 | ) | $ | (0.27 | ) | ||||||

| Shares used in computing basic and diluted net income (loss) |

86,354 | 84,577 | 83,500 | 82,956 | 82,465 | |||||||||||||||

| As of June 30, | ||||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||

| Selected Consolidated Balance Sheets Data: |

||||||||||||||||||||

| Cash, cash equivalents and restricted cash and short-term investments |

$ | 83,569 | $ | 81,213 | $ | 106,146 | $ | 109,082 | $ | 224,851 | ||||||||||

| Long-term investments and restricted cash and investments |

9,423 | 15,630 | 13,222 | 17,618 | 52,419 | |||||||||||||||

| Total assets |

97,493 | 147,817 | 188,609 | 208,367 | 504,744 | |||||||||||||||

| Convertible subordinated debt, net |

— | — | — | — | 149,842 | |||||||||||||||

| Total stockholders’ equity |

$ | 68,629 | $ | 42,945 | $ | 72,759 | $ | 72,696 | $ | 154,015 | ||||||||||

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion should be read in conjunction with the consolidated financial statements and notes included elsewhere in this Annual Report. The following discussion contains forward-looking statements that reflect our plans, estimates and beliefs. Our actual results could differ materially from those discussed in the forward-looking statements. Factors that could cause or contribute to these differences include, but are not limited to, those discussed below and those listed in the Risk Factor section contained above in Item 1A.

Since our inception in 1994, Unwired Planet and its predecessor companies have invested in and patented certain intellectual property for the mobile internet industry, some of which we believe are foundational in allowing mobile devices to connect to the Internet.

On January 12, 2012, we announced our pursuit of strategic alternatives for our product operations. On February 1, 2012, we announced the sale of our location product operations to Persistent Systems for a purchase price of $6.0 million. On April 30, 2012, we sold the mediation and messaging product operations to Openwave Mobility for a

17

Table of Contents

purchase price of $49.6 million. We accounted for the sale of the location product line and the sale of the mediation and messaging product lines as a discontinued operation. Accordingly, the condensed consolidated financial statements have been revised for all periods presented to reflect the location, mediation and messaging businesses as discontinued operations. Unless noted otherwise, the following discussions pertain to our continuing operations.

The pursuit of strategic alternatives was designed to allow us to focus on realizing the value of our intellectual property. For example, on August 31, 2011, we announced we had filed complaints against Apple Inc. and Research In Motion Limited in order to protect our intellectual property pertaining to how mobile devices connect to the Internet. This litigation is ongoing. During the first quarter of fiscal 2012, we entered into a license agreement with a third-party whereby we licensed rights to all of our patents for a fee of $15.0 million which was received during the second quarter of fiscal 2012. Additionally, during the first quarter of fiscal 2011 we licensed a number of patents to a competitor which generated $4.0 million in patent revenue for the period. As we execute our licensing plans, we anticipate the related revenue in future periods to be unpredictable and volatile. Additionally, legal costs associated with our efforts to license and protect our intellectual property and proprietary rights could be material in any given period, and are unpredictable and volatile. Effectively policing and enforcing our intellectual property is time consuming and costly. In addition, there can be no assurance that any ongoing or future litigation will be successful.

Critical Accounting Policies and Judgments

We believe that there are several accounting policies that are critical to understanding our business and prospects for our future performance, as these policies affect the reported amounts of revenue and other significant areas that involve management’s judgment and estimates. These significant accounting policies are:

| • | Classification among continuing and discontinued operations; |

| • | Revenue recognition; |

| • | Stock-based compensation; |

| • | Valuation of investments; and |

| • | Restructuring-related assessments. |

These policies, and our procedures related to these policies, are described in detail below. In addition, please refer to the Notes to Consolidated Financial Statements for further discussion of our accounting policies.

Classification among continuing and discontinued operations

Due to the sale of our remaining product businesses in 2012, we have presented financial results for the product businesses in discontinued operations. As the majority of costs related to employees and operations in the past related to our product operations, we identified costs we considered to be related to the ongoing intellectual property business for presentation in continuing operations. Costs we identified as relating to continuing operations include costs related to all personnel dedicated to our patent initiatives, including external legal fees and support personnel. Additionally, certain general and administrative costs were included, which are equivalent to the resources we expect to have on an ongoing basis after our transition to an intellectual property business. This includes costs related to our CEO and CFO, as well as accounting, information systems, and support personnel. All compensation, benefits, stock-based compensation and restructuring costs, if any, associated with these positions were included in ongoing operations. Additionally, we included costs related to being a public company, such as external audit costs,

18

Table of Contents

costs associated with the Sarbanes-Oxley Act, board of directors fees, SEC filings and NASDAQ fees. Facilities and information technology costs were allocated based upon the percentage of headcount of the employees assumed to be working primarily for the intellectual property business. Restructuring costs related to facilities remained in continuing operations, as we have retained the related liabilities. All other historical costs were classified as discontinued operations as they were considered necessary to support the product business.

.

Revenue Recognition

We recognize revenue from the licensing of our intellectual property when the following fundamental criteria are met: (i) persuasive evidence of an arrangement exists, (ii) delivery has occurred, (iii) the sales price is fixed or determinable, and (iv) collection of resulting receivables is reasonably assured. To date, revenue from upfront payments from licensees for the licensing of our patents has been recognized when the arrangement is mutually signed, since there has been no delivery or future performance obligation and the other three criteria are met upon signing the arrangement. When patent licensing arrangements include royalties for future sales of the licensees’ products using our licensed patented technology, revenue is recognized when the royalty report is received from the licensee, at which time the fixed and determinable criteria is met.

Stock-based Compensation

Stock-based compensation is recorded utilizing the fair value recognition provisions of accounting guidance, which requires the use of judgment and estimates in performing multiple calculations. We have estimated the expected volatility as an input into the Black-Scholes-Merton valuation formula when assessing the fair value of options granted. Our estimate of volatility was based upon the historical volatility experienced in our stock price, as well as implied volatility in market traded options on our common stock when appropriate. During fiscal 2012, 2011 and 2010, implied volatility was not utilized in our valuation of options granted due to the lack of option contracts with a strike price similar to our stock option grants. To the extent volatility of our stock price increases in the future, our estimates of the fair value of options granted in the future could increase, thereby increasing stock-based compensation expense in future periods. Our expected term of options granted is derived from actual post-vesting option cancellation and exercise experience, as well as the average midpoint between vesting and the contractual term for outstanding options.

Valuation of Investments

As of June 30, 2012 and June 30, 2011, $2.2 million and $4.4 million, respectively, in auction rate securities (“ARS”), recorded in long-term investments on the consolidated balance sheet, were considered illiquid based upon lack of recent auction results. We estimated the fair value of these auction rate securities based on: (1) financial standing of the issuer; (2) size of position held and the liquidity of the market; (3) contractual restrictions on disposition; (4) pending public offering with respect to the financial instrument; (5) pending reorganization activity affecting the financial instrument; (6) reported prices and the extent of the public trading in similar financial instruments of the issuer or comparable companies; (7) ability of the issuer to obtain required financing; (8) changes in the economic conditions affecting the issuer; (9) a recent purchase of the sale of a security of the issuer; (10) pricing by other dealers in similar securities; (11) financial statements of any underlying ARS portfolio investments; (12) successful auction/early redemption; (13) failing auctions until maturity; or (14) default and the estimated cash flows for each scenario. Other factors are considered, such as interest rate effects, liquidity, trinomial probabilities, recovery rates, value of the investments held by the issuer and the financial condition and credit ratings of the issuer, insurers, and parent companies, as applicable. Assumptions of probabilities of default, probabilities of passing auction,

19

Table of Contents

and probabilities of earning the maximum rate for each period are based upon the risks, the underlying investments collateralizing the ARS, the maturity date of the ARS, the maximum rate of the ARS and current market conditions, and third party professional judgment. We recorded other-than-temporary and realized losses in the consolidated statements of operations of $1.1 million and $1.7 million during fiscal 2011 and 2010, respectively, related to these securities. There were no other-than-temporary and realized losses in the consolidated statements of operations during fiscal 2012.

Restructuring–related Assessments

Our critical accounting policy and judgment as it relates to restructuring-related assessments includes our estimate of facility costs. To determine the facility costs, which consist of the loss after our cost recovery efforts from subleasing a building, some estimates were made related to: (1) the time period over which the relevant building would remain vacant; (2) sublease terms; and (3) sublease rates, including common area charges. The facility cost is an estimate that may be adjusted in the future upon triggering events (such as changes in estimates of time and rates to sublease, based upon current market conditions, or changes in actual sublease rates).

Summary of Operating Results for Fiscal 2012, 2011 and 2010

Revenues

We generate patent revenue, which is derived from licensing our intellectual property.

To date our patent revenues have been from two licensees, as shown in the following table:

| % of Total Revenue Fiscal Year Ended June 30, |

||||||||||||

| 2012 | 2011 | 2010 | ||||||||||

| Microsoft |

100 | % | — | — | ||||||||

| Mobixell Networks |

— | 100 | % | — | ||||||||

The following table presents the key revenue information for fiscal 2012, 2011 and 2010, respectively (dollars in thousands):

| Fiscal Year ended June 30, | Percent Change FY 2012 from FY 2011 |

Percent Change FY 2011 from FY 2010 |

||||||||||||||||||

| 2012 | 2011 | 2010 | ||||||||||||||||||

| Revenues: |

||||||||||||||||||||

| Patents |

$ | 15,050 | $ | 4,019 | $ | — | 274 | % | N/A | |||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Total revenues |

$ | 15,050 | $ | 4,019 | $ | — | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Percent of revenues: |

||||||||||||||||||||

| Patents |

100 | % | 100 | % | N/A | |||||||||||||||

|

|

|

|

|

|||||||||||||||||

| Total revenues |

100 | % | 100 | % | N/A | |||||||||||||||

|

|

|

|

|

|||||||||||||||||

Patents Revenues

During the first quarter of fiscal 2012, we entered into a license agreement with Microsoft whereby we licensed them rights to all of our patents for a fee of $15.0 million which was received during the second quarter of fiscal 2012. During the first quarter of fiscal 2011, we entered into a license agreement for a fee of $4.0 million plus future royalties from domestic sales of products and related services covered under the patent license after September 22, 2010.

20

Table of Contents

Our patent initiative was approved by our Board of Directors in fiscal 2011, thus there are no patent revenues in fiscal 2010.

Operating Expenses

The following table represents operating expenses for fiscal 2012, 2011 and 2010, respectively (dollars in thousands):

| Fiscal Year ended June 30, | ||||||||||||||||||||

| 2012 | Percent Increase (Decrease) |

2011 | Percent Increase (Decrease) |

2010 | ||||||||||||||||

| Sales and marketing expense |

$ | 614 | 100 | % | $ | — | N/A | $ | — | |||||||||||

| Patent initiative expense |

13,089 | 285 | % | 3,398 | 1145 | % | 273 | |||||||||||||

| General and administrative |

7,651 | 33 | % | 5,732 | -19 | % | 7,079 | |||||||||||||

| Restructuring and other costs |

2,666 | 20 | % | 2,226 | -51 | % | 4,549 | |||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Total operating expenses |

$ | 24,020 | 112 | % | $ | 11,356 | -5 | % | $ | 11,901 | ||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Percent of revenues |

||||||||||||||||||||

| Sales and marketing |

4 | % | N/A | N/A | ||||||||||||||||

| Patent initiative expense |

87 | % | 85 | % | N/A | |||||||||||||||

| General and administrative |

51 | % | 143 | % | N/A | |||||||||||||||

Sales and marketing expense

Sales and marketing expenses include salary and benefit expenses and travel expenses for our marketing personnel, as well as any commissions related to our patent revenues. Sales and marketing expenses also include the costs of public relations, promotional materials and other market development programs.

The $0.6 million of sales and marketing expense incurred during fiscal 2012 primarily consists of commissions of $0.4 million incurred during the first quarter of fiscal 2012 in connection with the patent deal signed in that quarter, as well as $0.2 million in marketing expense incurred during the fourth quarter of fiscal 2012. Prior to fiscal 2012, patent revenues were not subject to a commission plan and our marketing activities were related to the discontinued operations.

Patent initiative expenses

Patent initiative expenses include legal and consulting costs related to defending or asserting our patents, as well as labor costs for employees engaged in these activities on a full-time basis.

During the fiscal year ended June 30, 2012, patent initiative expenses increased by 285% compared with the prior year. This increase is primarily due to a $9.3 million increase in legal expenses associated with patent litigation, which includes legal fees supporting the ITC case filed and announced in August 2011. Additionally, there was an increase of approximately $0.4 million related to labor and associated costs as the resources allocated to the patent department increased.

During the fiscal year ended June 30, 2011, we incurred approximately $3.4 million in patent initiative expenses. The Board of Directors approved our patent strategy during fiscal 2011, and as such the only comparable charges in fiscal 2010 relate to labor and associated costs.

21

Table of Contents

General and administrative expenses

General and administrative expenses consist principally of salary and benefit expenses, travel expenses, and facility costs for our finance, legal, information services and executive personnel. General and administrative expenses also include outside accounting and legal fees.