Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - PEABODY ENERGY CORP | btu8k20120906.htm |

Exhibit 99.1

Energizing The World One BTU At A Time

Barclays Energy Conference

Gregory H. Boyce Chairman and Chief Executive Officer

September 6, 2012

Peabody Energy

Statement on Forward-Looking Information Peabody Energy

Some of the following information contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, as amended, and is intended to come within the safe-harbor protection provided by those sections. Our forward-looking statements are based on numerous assumptions that the company believes are reasonable, but they are open to a wide range of uncertainties and business risks that may cause actual results to differ materially from expectations as of Sept. 6, 2012. These factors are difficult to accurately predict and may be beyond the company's control. The company does not undertake to update its forward-looking statements. Factors that could affect the company's results include, but are not limited to: global supply and demand for coal, including the seaborne thermal and metallurgical coal markets; price volatility, particularly in higher-margin products and in our trading and brokerage businesses; impact of alternative energy sources, including natural gas and renewables; global steel demand and the downstream impact on metallurgical coal prices; impact of weather and natural disasters on demand, production and transportation; reductions and/or deferrals of purchases by major customers and ability to renew sales contracts; credit and performance risks associated with customers, suppliers, contract miners, co-shippers, and trading, banks and other financial counterparties; geologic, equipment, permitting and operational risks related to mining; transportation availability, performance and costs; availability, timing of delivery and costs of key supplies, capital equipment or commodities such as diesel fuel, steel, explosives and tires; integration of Macarthur Coal Limited (PEA-PCI) operations; successful implementation of business strategies; negotiation of labor contracts, employee relations and workforce availability; changes in postretirement benefit and pension obligations and their funding requirements; replacement and development of coal reserves; availability, access to and the related cost of capital and financial markets; effects of changes in interest rates and currency exchange rates (primarily the Australian dollar); effects of acquisitions or divestitures; economic strength and political stability of countries in which we have operations or serve customers; legislation, regulations and court decisions or other government actions, including, but not limited to, new environmental and mine safety requirements and changes in income tax regulations, sales-related royalties or other regulatory taxes; litigation, including claims not yet asserted; and other risks detailed in the company's reports filed with the Securities and Exchange Commission (SEC). The use of “Peabody,” “the company,” and “our” relate to Peabody, its subsidiaries and majority-owned affiliates.

Adjusted EBITDA is defined as income from continuing operations before deducting net interest expense, income taxes, asset retirement obligation expense, depreciation, depletion and amortization and amortization of basis difference associated with equity method investments. Adjusted EBITDA, which is not calculated identically by all companies, is not a substitute for operating income, net income or cash flow as determined in accordance with United States generally accepted accounting principles. Management uses Adjusted EBITDA as a key measure of operating performance and also believes it is a useful indicator of the company's ability to meet debt service and capital expenditure requirements.

Adjusted Income from Continuing Operations and Adjusted Diluted EPS are defined as income from continuing operations and diluted earnings per share excluding the impact of the remeasurement of foreign income tax accounts. Management has included these measures because, in management's opinion, excluding such impact is a better indicator of the company's ongoing effective tax rate and diluted earnings per share, and is therefore more useful in comparing the company's results with prior and future periods.

9/6/12

2

Peabody Positioned for Success in Challenging Market Conditions Peabody Energy

Peabody's long-term coal market view remains favorable Strong growth for global met and thermal coal Solid growth for PRB and Illinois Basin regions

Near-term view is cautious given decline in global commodity demand and pricing caused by recession in Europe, sluggish U.S. growth and eased expansion in China

We are responding to macro conditions by further reducing capital spending, deferring early-stage expansion projects, reducing growth volumes and continuing to aggressively manage costs

3

Peabody Responding to Near-Term Market Conditions Peabody Energy

Completing late-stage development projects Deferring future growth projects until economy strengthens

Reducing 2012 capital to $1.0 billion - $1.1 billion Capex midpoint $250 million below original 2012 target Expect 2013 capital at or below 2012 levels

Slowing pace of Australia volume growth

Closing Air Quality Mine in Indiana due to market conditions

Aggressively managing cost structure

Focusing on optimizing cash flows and reducing debt

4

Global Coal Markets

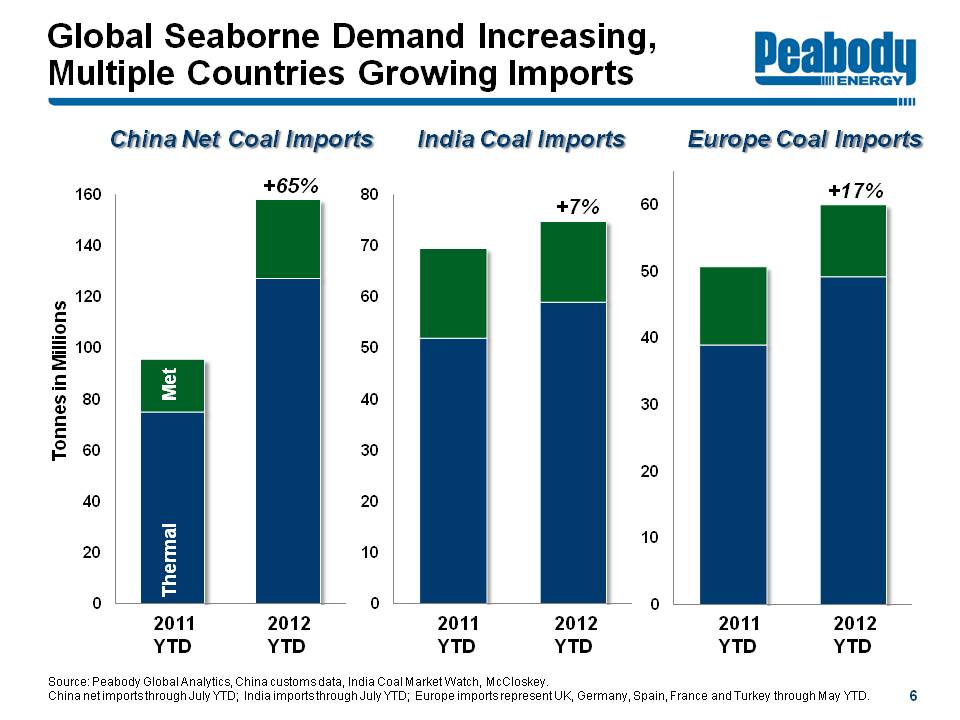

Global Seaborne Demand Increasing, Multiple Countries Growing Imports Peabody Energy

China Coal Imports Tonnes in Millions Thermal Met 0 20 40 60 80 100 120 140 160 2011 2012 +65%

India Coal Imports 0 10 20 30 40 50 60 70 80 2011 2012 +7%

Europe Coal Imports 0 10 20 30 40 50 60 2011 2012 +17%

Source: Peabody Global Analytics, China customs data, India Coal Market Watch, McCloskey.

China net imports through July YTD; India imports through July YTD; Europe imports represent UK, Germany, Spain, France and Turkey through May YTD.

6

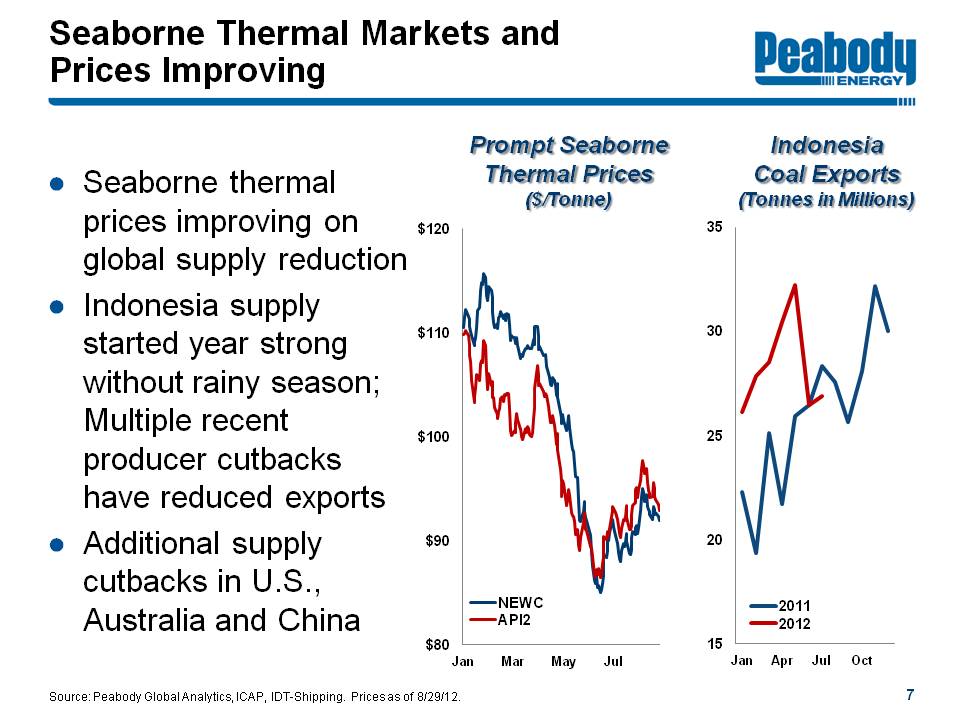

Seaborne Thermal Markets Improving, Prices Showing Strength Peabody Energy

Seaborne thermal prices improving on global supply reduction

Indonesia supply started year strong without rainy season; Multiple recent producer cutbacks have reduced exports

Additional supply cutbacks in U.S., Australia and China

Prompt Seaborne Thermal Prices ($/tonne) Jan Mar May July $80 $90 $100 $110 $120 NEWC API2

Indonesia Coal Exports (Million Metric Tonnes) Jan Apr Jul Oct 15 20 25 30 35 2011 2012

7

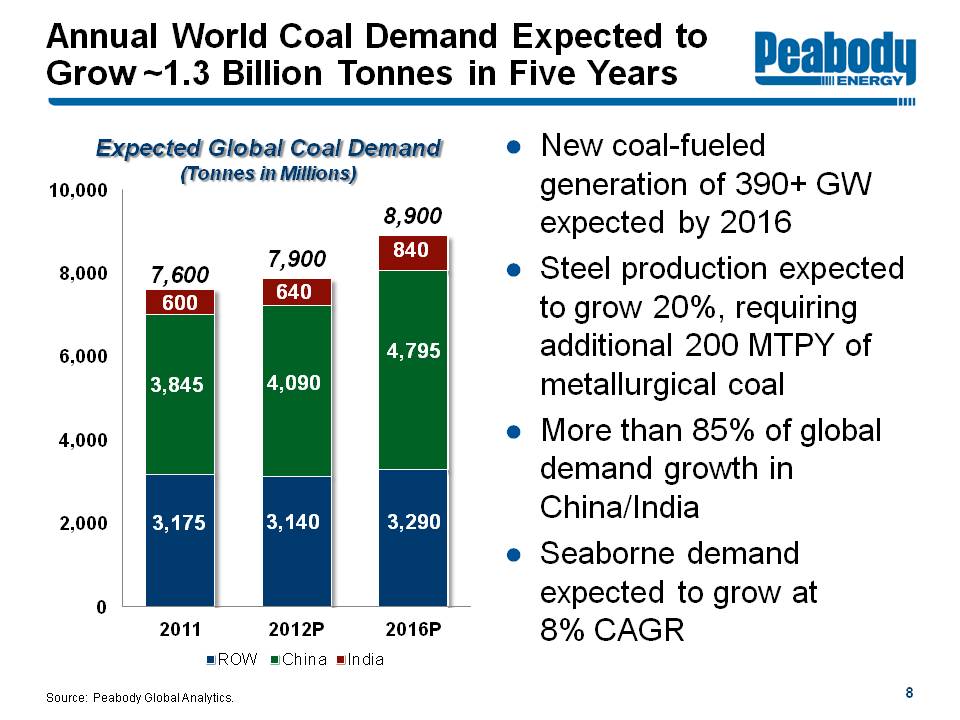

Annual World Coal Demand Expected to Grow ~1.3 Billion Tonnes in Five Years Peabody Energy

Expected Global Coal Demand (Million Tonnes) 0 2,000 4,000 6,000 8,000 10,000

2011 7,600 ROW 3,175 China 3,845 India 600

2012P 7,900 ROW 3,140 China 4,090 India 640

2016P 8,900 ROW 3,290 China 4,795 India 840

New coal-fueled generation of 390+ GW expected by 2016

Steel production expected to grow 20%, requiring additional 200 MTPY of metallurgical coal

More than 85% of global demand growth in China/India

Seaborne demand expected to grow at 8% CAGR

Source: Peabody Global Analytics.

8

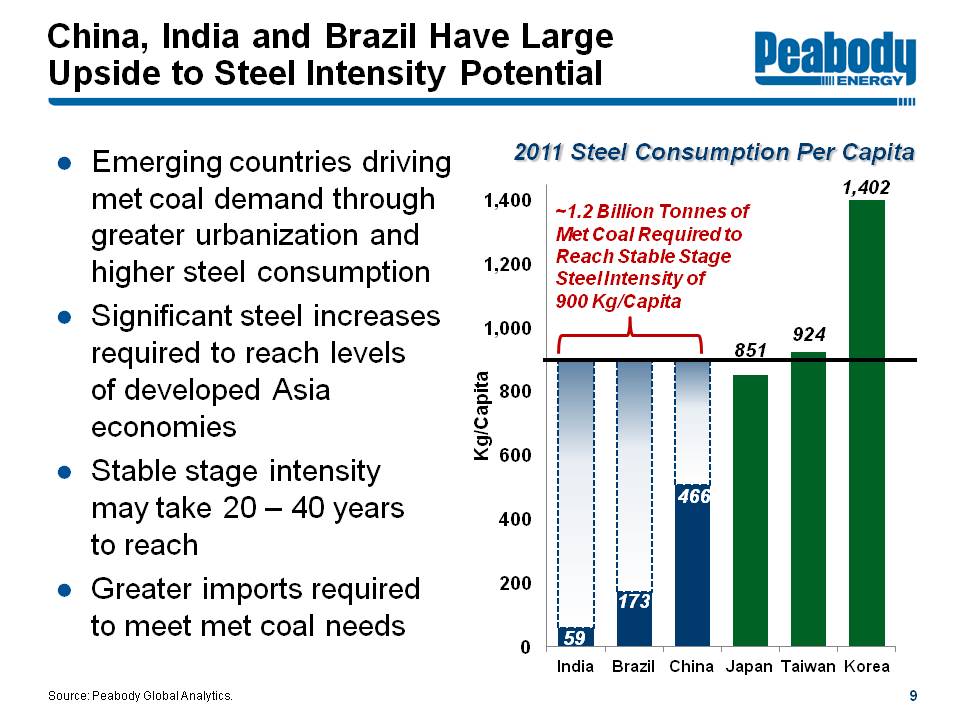

China, India and Brazil Have Large Upside to Steel Intensity Potential Peabody Energy

Emerging countries driving met coal demand through greater urbanization and higher steel consumption

Significant steel increases required to reach levels of developed Asia economies

Stable stage intensity may take 20 - 40 years to reach

Greater imports required to meet met coal needs

2011 Steel Consumption Per Capita Kg/Capita 0 200 400 600 800 1,000 1,200 1,400 India 59 Brazil 173 China 466 Japan 851 Taiwan 924 Korea 1,402 ~1.2 Billion Tonnes of Met Coal Required to Reach Stable Stage Steel Intensity of 900 Kg/Capita

Source: Peabody Global Analytics.

9

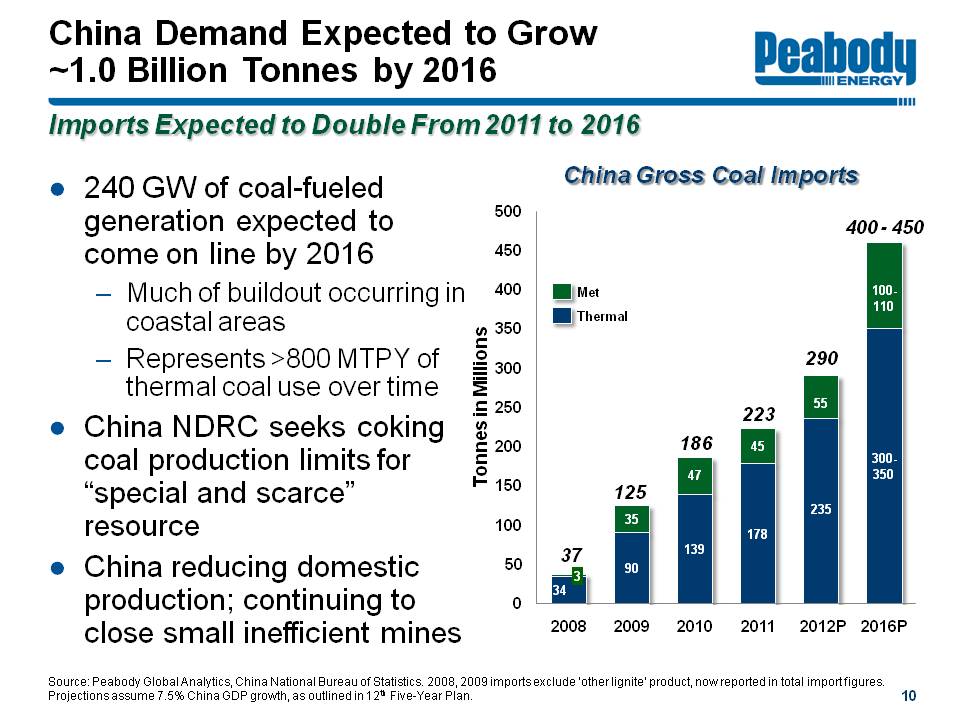

China Demand Expected to Grow ~1.0 Billion Tonnes by 2016 Peabody Energy

Imports Expected to Double From 2011 to 2016

240 GW of coal-fueled generation coming on line by 2016 Much of buildout occurring in coastal areas Represents >800 MTPY of thermal coal use over time

China NDRC seeks coking coal production limits for “special and scarce” resource

China reducing domestic production; continuing to close small inefficient mines

China Gross Coal Imports Tonnes in Millions 0 50 100 150 200 250 300 350 400 450 500 2008 37 Met 3 Thermal 34 2009 125 Met 35 Thermal 90 2010 186 Met 47 Thermal 139 2011 223 Met 45 Thermal 178 2012P 290 Met 55 Thermal 235 2016P 400 - 450 Met 100 - 110 Thermal 300 - 350

Source: Peabody Global Analytics, China National Bureau of Statistics. 2008, 2009 imports exclude 'other lignite' product, now reported in total import figures. Projections assume 7.5% China GDP growth, as outlined in 12th Five-Year Plan.

10

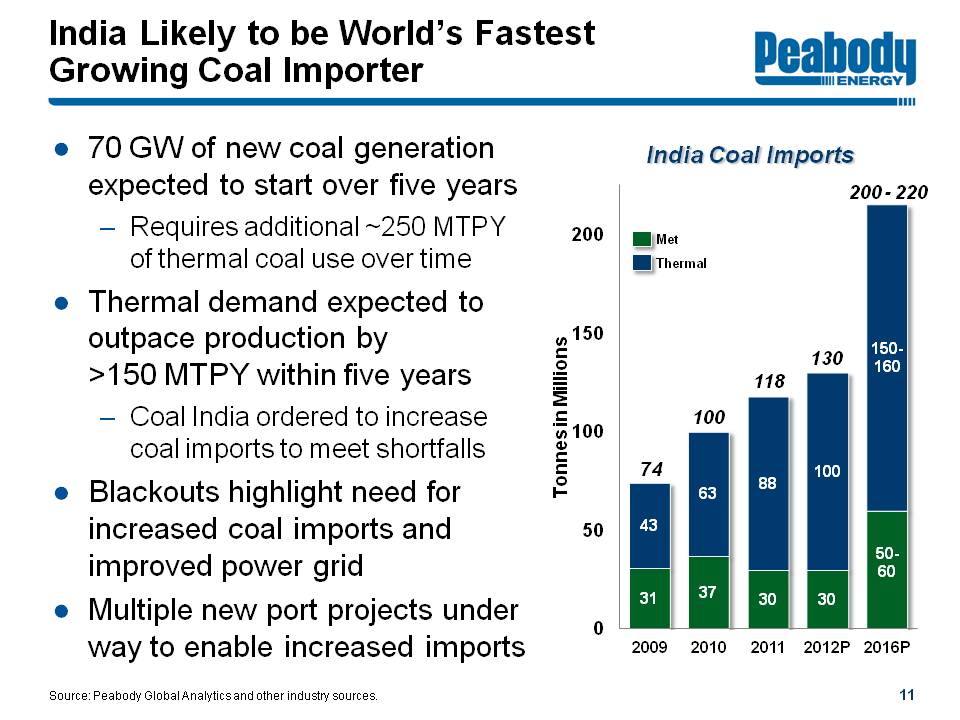

India Likely to be World's Fastest Growing Coal Importer Peabody Energy

70 GW of new coal generation expected to start over five years Requires additional ~250 MTPY of thermal coal use over time

Thermal demand expected to outpace production by >150 MTPY within five years Coal India ordered to increase coal imports to meet shortfalls

Blackouts highlight need for increased coal imports and improved power grid

Multiple new port projects under way to enable increased imports

India Coal Imports Tonnes in Millions 0 50 100 150 200

2009 74 Met 31 Thermal 43 2010 100 Met 37 Thermal 63 2011 115 Met 30 Thermal 85 2012P 130 Met 30 Thermal 100 2016P 200 - 220 Met 50 - 60 Thermal 150 - 160

Source: Peabody Global Analytics and other industry sources.

11

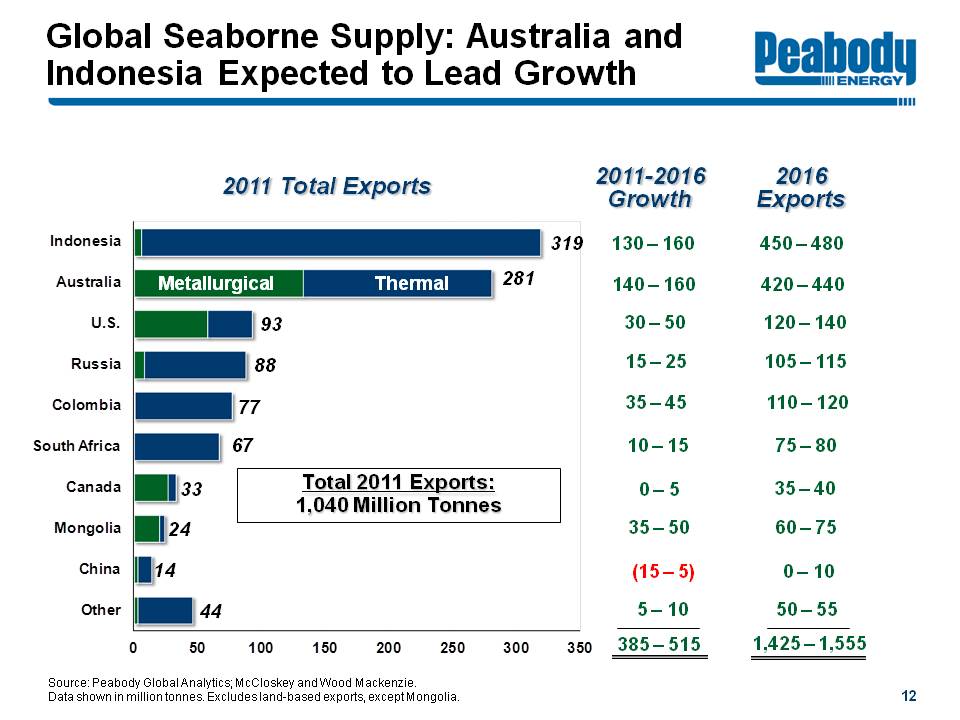

Global Seaborne Supply: Australia and Indonesia Expected to Lead Growth Peabody Energy

2011 Total Exports Metallurgical Thermal 0 50 100 150 200 250 300 350

Indonesia 319 Australia 281 U.S. 93 Russia 88 Colombia 77 South Africa 67 Canada 33 Mongolia 24 China 14 Other 46 Total 2011 Exports: 1,040 Million Tonnes

2011-2016 Growth 385 - 515 Indonesia 130 - 160 Australia 140 - 160 U.S. 30 - 50 Russia 15 - 25 Colombia 35 - 45 South Africa 10 - 15 Canada 0 - 5 Mongolia 35 - 50 China (15) - (5) Other 5 - 10

2016 Exports 1,425 - 1,555 Indonesia 450 - 580 Australia 420 - 440 U.S. 120 - 140 Russia 105 - 115 Colombia 110 - 120 South Africa 75 - 80 Canada 35 - 40 Mongolia 60 - 75 China 0 - 10 Other 50 - 55

Source: Peabody Global Analytics; McCloskey and Wood Mackenzie. Data shown in million tonnes. Excludes land-based exports, except Mongolia.

12

Australia Coal: Multiple Advantages Over Other Regions Peabody Energy

Supplies 60% of world's seaborne metallurgical coal

Major competitive advantage with mines close to port; Ports close to high-growth markets

Largest exporter of high-CV thermal coal

Peabody's Australian margins greater than average U.S. peer margins

Australian coal assets earn valuations significantly higher than U.S. counterparts

13

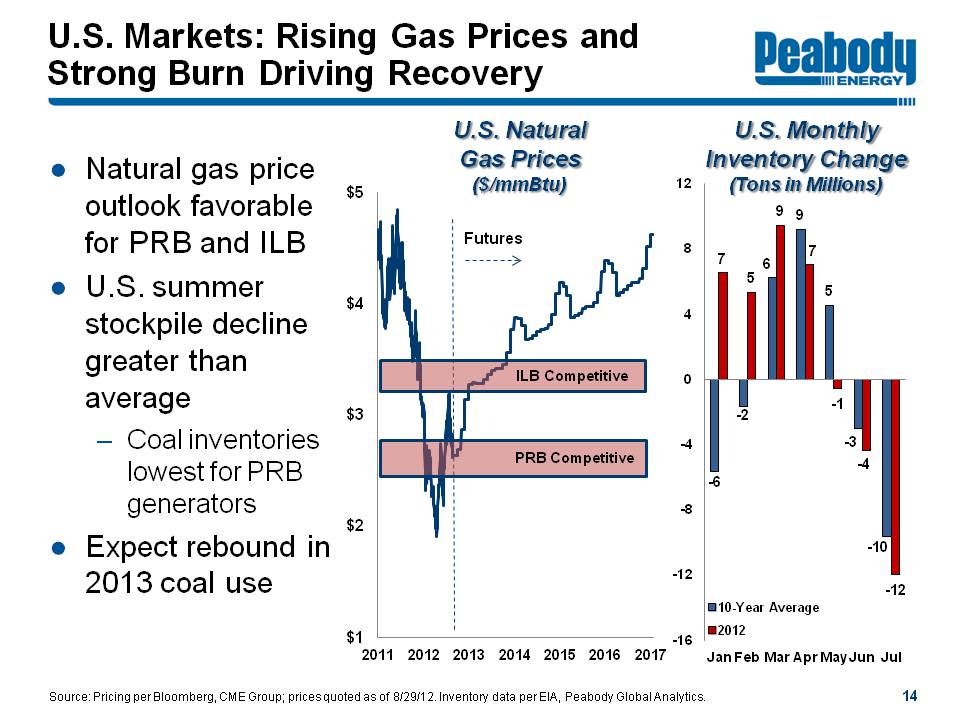

U.S. Markets: Rising Gas Prices and Strong Burn Driving Recovery Peabody Energy

Natural Gas Prices Favorable for PRB and ILB

U.S. stockpile decline greater than average Coal inventories lowest for PRB generators

Expect rebound in 2013 coal use

U.S. Natural Gas Prices ($/mmBtu)

$1 $2 $3 $4 $5 2011 2012 2013 2014 2015 2016 2017 ILB Competitive PRB Competitive

U.S. Monthly Inventory Change Tons in Millions -16 -12 -8 -4 0 4 8 12 Jan 10-Year Average -6 2012 7 Feb 10-Year Average -2 2012 5 Mar 10-Year Average 6 2012 9 Apr 10-Year Average 9 2012 7 May 10-Year Average 5 2012 -1 Jun 10-Year Average -3 2012 -7 Jul 10-Year Average -10 2012 -12

Source: Pricing per Bloomberg, CME Group; prices quoted as of 8/29/12. Inventory data per EIA, Peabody Global Analytics.

14

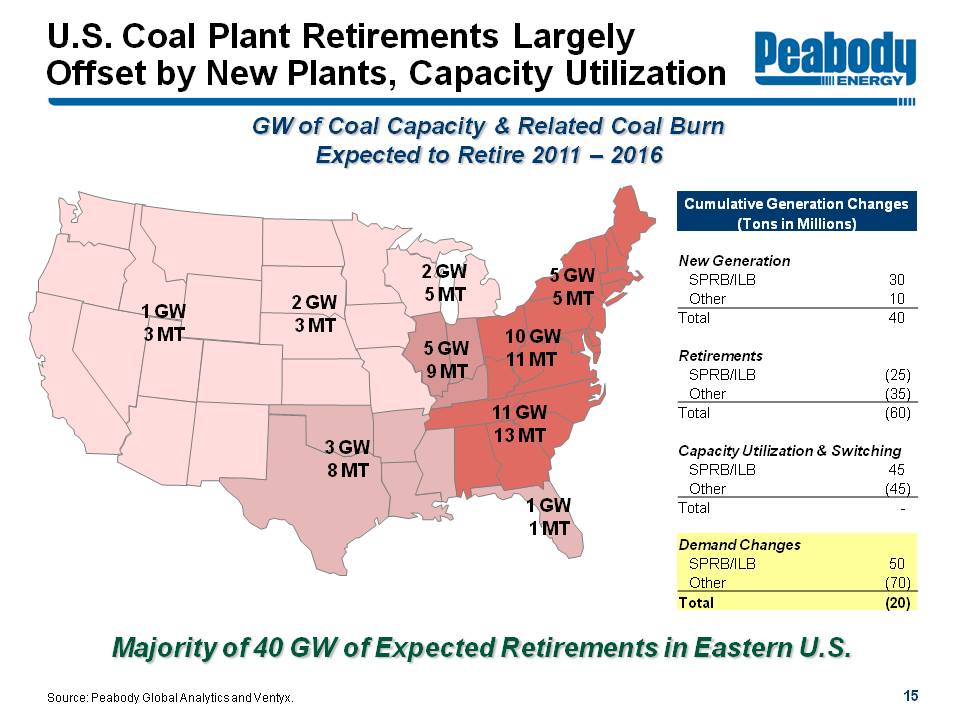

U.S. Coal Plant Retirements Largely Offset by New Plants, Capacity Utilization Peabody Energy

GW of Coal Capacity & Related Coal Burn Retiring 2011 - 2016

1 GW 3 MT 2 GW 3 MT 3 GW 8 MT 2 GW 5 MT 5 GW 9 MT 10 GW 11 MT 5 GW 5 MT 11 GW 13 MT 1 GW 1 MT

Cumulative Generation Changes Million Tons

New Generation SPRB / ILB 30 Other 10 Total New Gen 40

Retirements SPRB / ILB (25) Other (35) Total Retirements (60)

Capacity Utilization & Switching SPRB / ILB 45 Other (45) Total Cap./Switch -

Total SPRB / ILB 50 Other (70) Total Change (20)

Majority of 40 GW of Expected Retirements in Eastern U.S.

Source: Peabody Global Analytics and Ventyx.

15

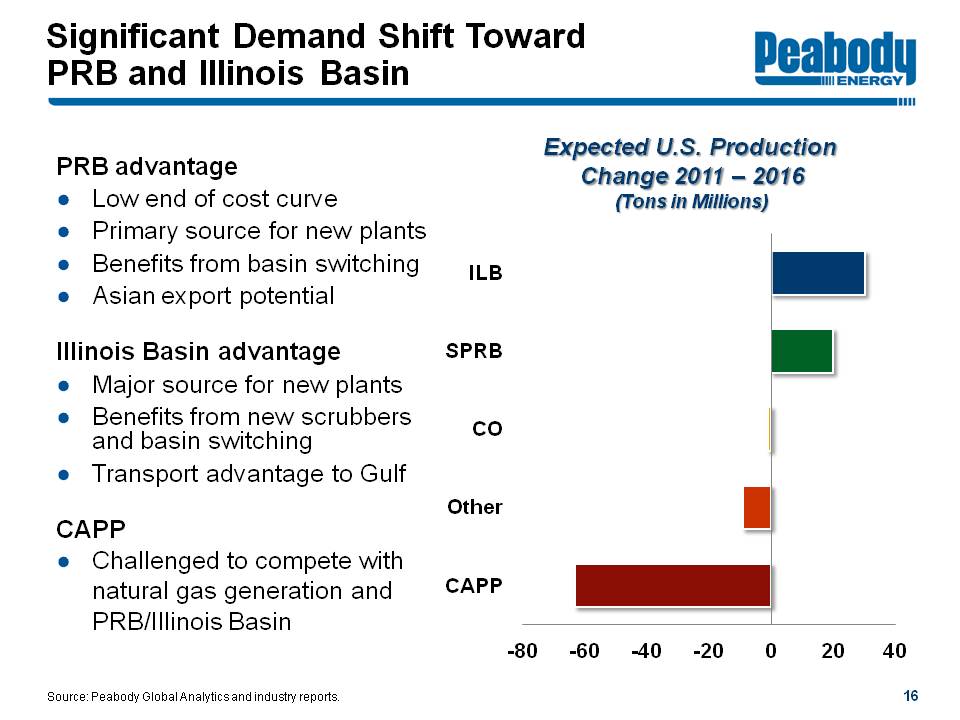

Significant Demand Shift Towards PRB and Illinois Basin Peabody Energy

PRB advantage Low end of cost curve Primary source for new plants Benefits from basin switching Asian export potential

Illinois Basin advantage Major source for new plants Benefits from new scrubbers and basin switching Transport advantage to Gulf

CAPP Challenged to compete with natural gas generation and PRB/Illinois Basin

Expected U.S. Production Change 2011 - 2016P (Tons in Millions)

ILB SPRB CO Other CAPP -80 -60 -40 -20 0 20 40

Source: Peabody Global Analytics and industry reports.

16

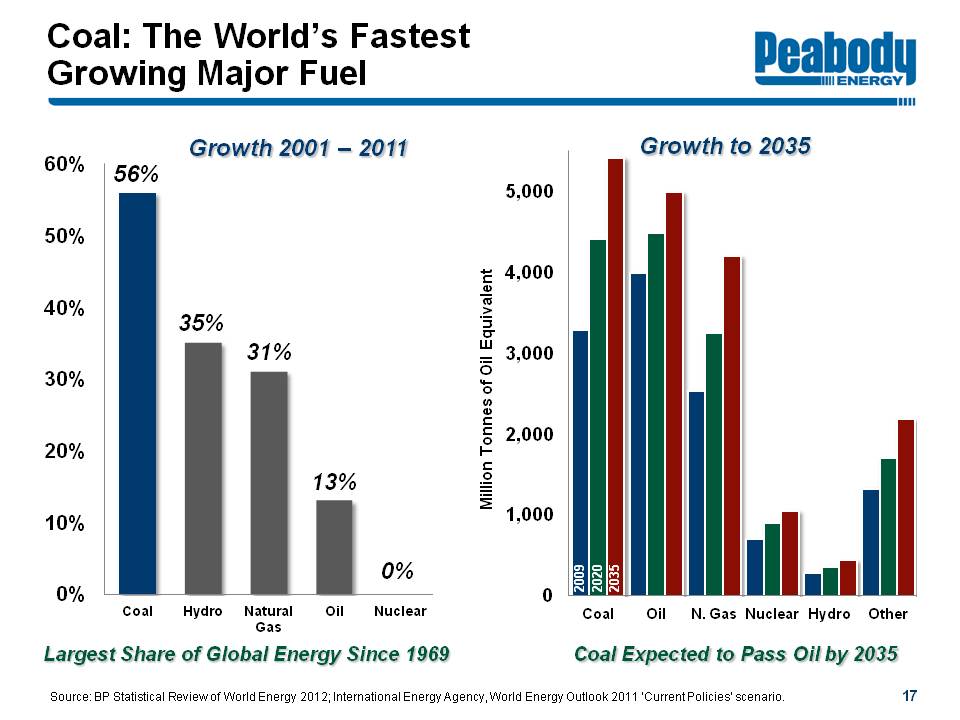

Coal: The World's Fastest Growing Major Fuel Peabody Energy

Growth 2001 - 2011 0% 10% 20% 30% 40% 50% 60%

Coal 56% Hydro 35% Natural Gas 31% Oil 13% Nuclear 0%

Largest Share of Global Energy Since 1969

Growth to 2035 Million Tonnes of Oil Equivalent 0 1,000 2,000 3,000 4,000 5,000

Coal 2009 2020 2035 Oil N. Gas Nuclear Hydro Other

Coal Expected to Pass Oil by 2035

Source: BP Statistical Review of World Energy 2012; International Energy Agency, World Energy Outlook 2011 'Current Policies' scenario.

17

Peabody's Global Platform

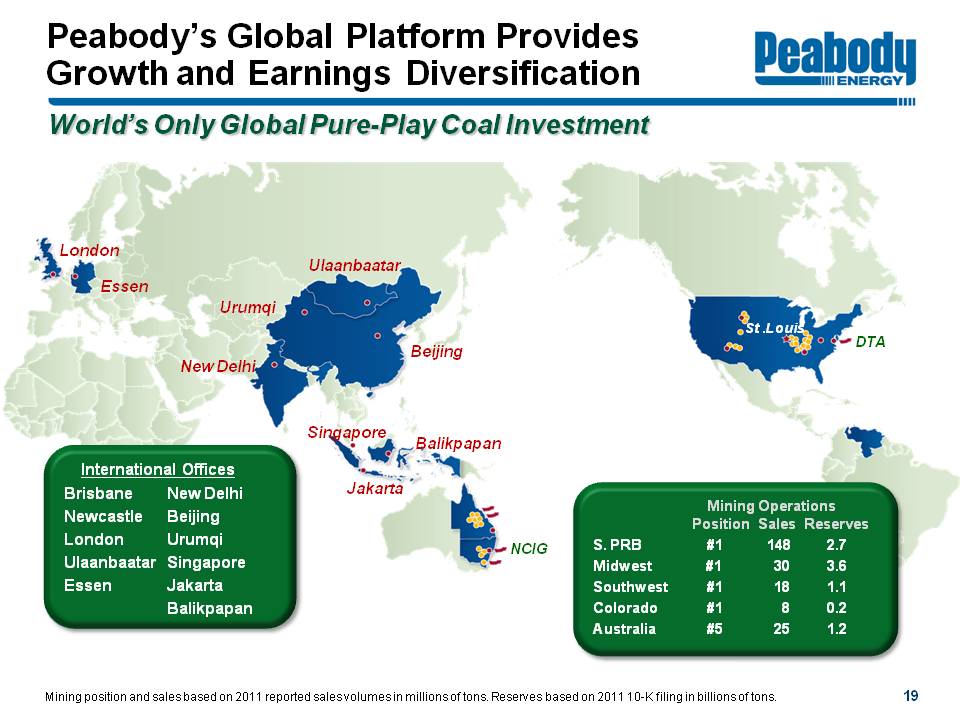

Peabody's Global Platform Provides Growth and Earnings Diversification Peabody Energy

World's Only Global Pure-Play Coal Investment

London Essen New Delhi Urumqi Ulaanbaatar Beijing Singapore Jakarta Balikpapan NCIG St. Louis DTA

International Offices Brisbane Newcastle London Ulaanbaatar Essen New Delhi Beijing Urumqi Singapore Jakarta Balikpapan

Mining Operations Position Sales Reserves

S. PRB #1 148 2.7 Midwest #1 30 3.6 Southwest #1 18 1.1 Colorado #1 8 0.2 Australia #5 25 1.2

Mining position and sales based on 2011 reported sales volumes in millions of tons. Reserves based on 2011 10-K filing in billions of tons.

19

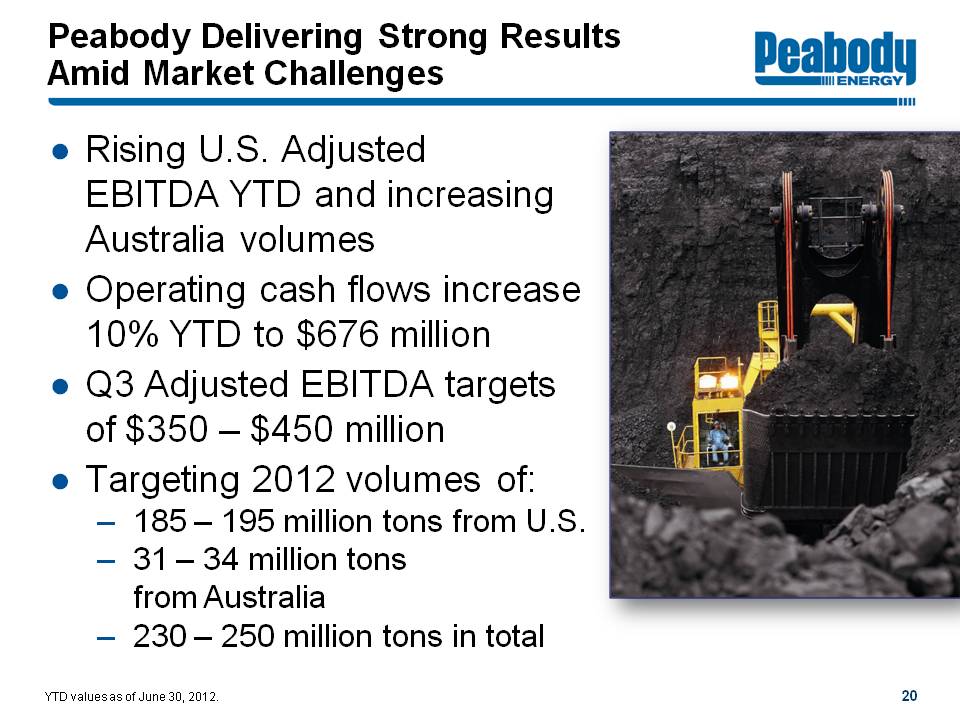

Peabody Delivering Strong Results Amid Market Challenges Peabody Energy

Rising U.S. Adjusted EBITDA YTD and increasing Australia volumes

Operating cash flows increase 10% YTD to $676 million

Q3 Adjusted EBITDA targets of $350 - $450 million

Targeting 2012 volumes of: 185 - 195 million tons from U.S. 31 - 34 million tons from Australia 230 - 250 million tons in total

YTD values as of June 30, 2012.

20

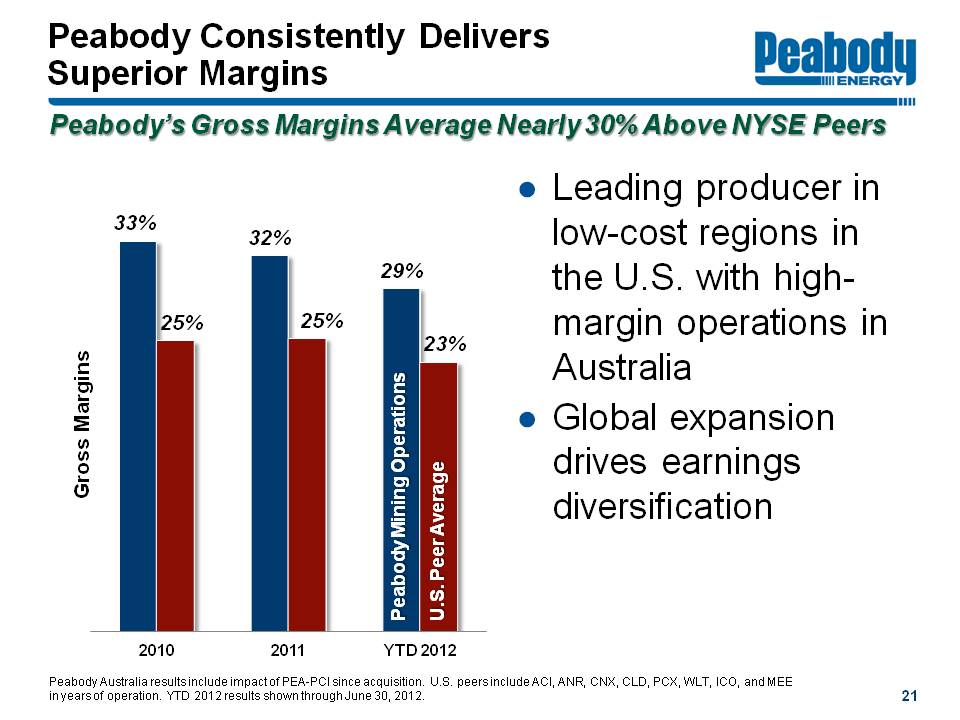

Peabody Consistently Delivers Superior Margins Peabody Energy

Peabody's Gross Margins Average Nearly 30% Above NYSE Peers

Gross Margins 2010 33% 25% 2011 32% 25% YTD 2012 29% 23%

Peabody Mining Operations U.S. Peer Average

Leading producer in low-cost regions in the U.S. with high-margin operations in Australia

Global expansion drives earnings diversification

Peabody Australia results include impact of PEA-PCI since acquisition. U.S. peers include ACI, ANR, CNX, CLD, PCX, WLT, ICO, and MEE in years of operation. YTD 2012 results shown through June 30, 2012.

21

Peabody U.S. Platform: Continued Focus on Success at Low End of Cost Curve Peabody Energy

Current-year U.S. position fully priced since late 2011 70% - 75% priced for 2012 based on 2012 production levels

Continued operational focus on cost containment: reducing overtime, use of contractors, discretionary spending

Closure of Air Quality Mine in Q3 2012 1.2 MTPY of sales; among Peabody's highest-cost U.S. mines

Lowering 2013 capital for Twentymile Sage Creek and Gateway North extensions while matching new volumes with current production profile

Unpriced position as of June 30, 2012. Air Quality sales based on 2011 reported sales volumes.

22

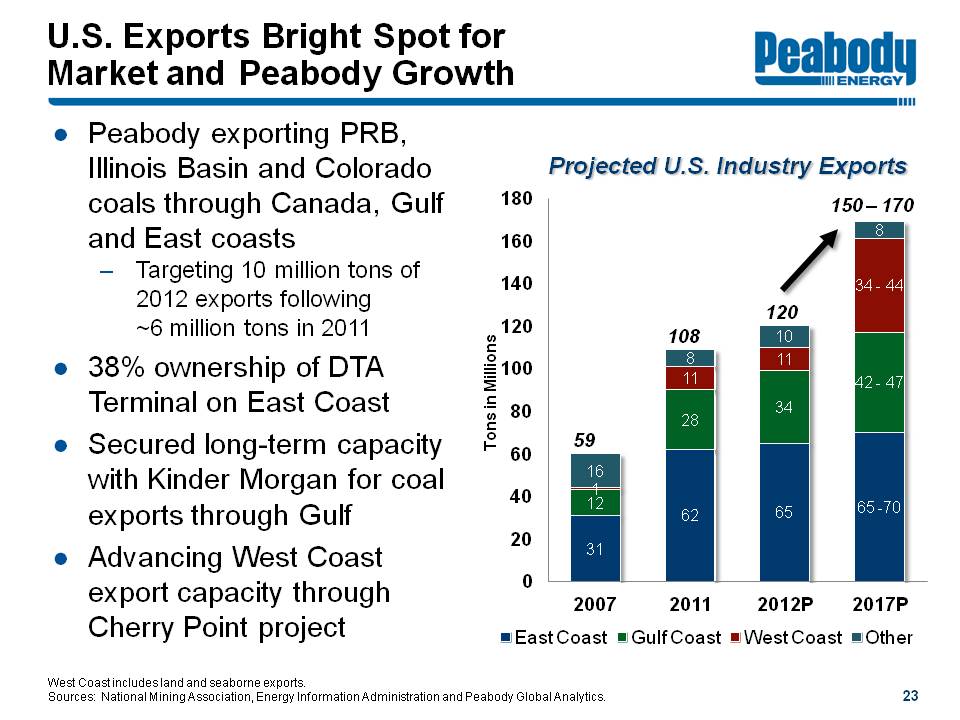

U.S. Exports Bright Spot for Market and Peabody Growth Peabody Energy

Peabody exporting PRB, Illinois Basin and Colorado coals through Canada, Gulf and East coasts Targeting 10 million tons of 2012 exports following ~6 million tons in 2011

38% ownership of DTA Terminal on East Coast

Secured long-term capacity with Kinder Morgan for coal exports through Gulf

Advancing West Coast export capacity through Cherry Point project

Projected U.S. Exports Million Tons 0 20 40 60 80 100 120 140 160 180

2007 59 East Coast 31 Gulf Coast 12 West Coast 1 Other 16

2011 108 East Coast 62 Gulf Coast 28 West Coast 11 Other 8

2012P 120 East Coast 65 Gulf Coast 34 West Coast 11 Other 10

2017P 150 - 170 East Coast 65 - 70 Gulf Coast 42 - 47 West Coast 34 - 44 Other 8

West Coast includes land and seaborne exports.

Sources: National Mining Association, Energy Information Administration and Peabody Global Analytics.

23

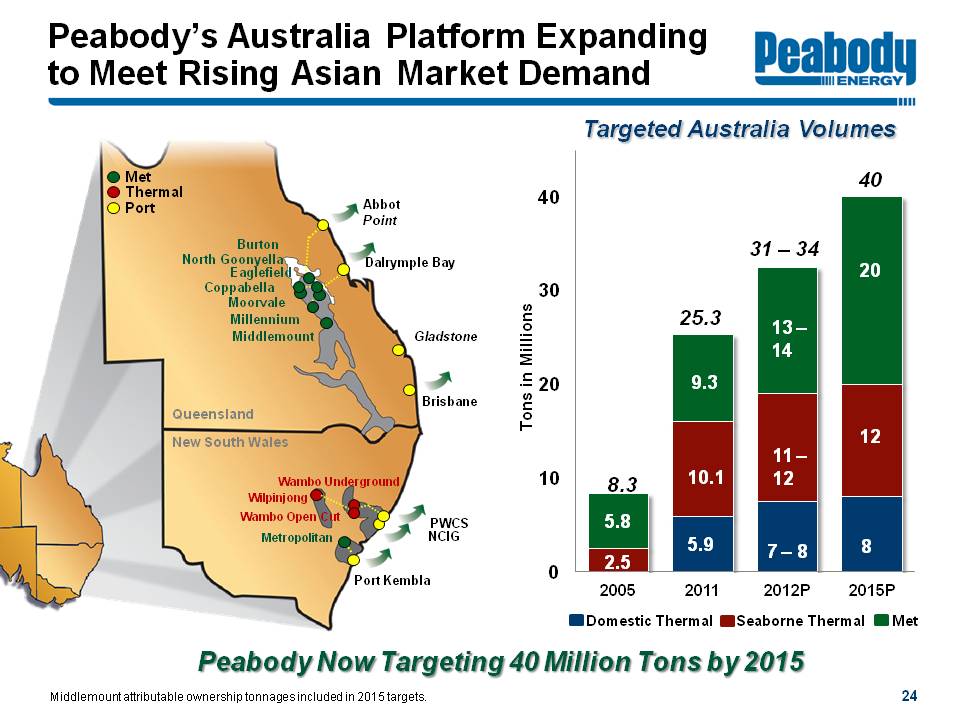

Peabody's Australia Platform Expanding to Meet Rising Asian Market Demand

Met Thermal Port

Queensland Burton North Goonyella Eaglefield Coppabella Moorvale Millennium Middlemount Abbot Point Dalrymple Bay Gladstone Brisbane

New South Wales Wambo Underground Wilpinjong Wambo Open Cut Metropolitan PWCS NCIG Port Kembla

Targeted Australia Volumes Tons in Millions 0 10 20 30 40

2005 2.5 5.8 8.3 2011 5.9 10.1 9.3 25.3 2012P 7 - 8 11 - 12 13 - 14 31 - 34 2015P 8 12 20 40

Domestic Thermal Seaborne Thermal Met

Peabody Now Targeting 40 Million Tons by 2015

Middlemount attributable ownership tonnages included in 2015 targets.

24

Conversion to Owner Operator on Target at Millennium and Wilpinjong Mines Peabody Energy

Moving Additional ~40% of Australia Production to Owner-Operator

15% - 20% cost improvement overcomes other cost pressures

Increased control over mining

Sharing best practices from other Peabody operations

~75% of Australian production to be owner operated upon transition in April 2013

Flexibility to lease some equipment needs to reduce capital outlay

Evaluation under way for other operations

25

Peabody Advancing Late-Stage Projects to Completion Peabody Energy

Wilpinjong expansion completed on time and on budget Expanded BTU's lowest-cost Australia thermal mine capacity by 30% to ~13 MTPY

Millennium expansion near completion Doubling mine capacity to ~3 - 4 MTPY Includes SHCC/PCI and adding HCC to mine mix

Burton widening/extension nearing completion Moving to new HCC mining area in Q3 Extends mine life and expands production

North Goonyella longwall top coal caving technology to add HQHCC volumes

Eaglefield co-development extending mine life, HQHCC production

Middlemount permit received for eventual increase to 4 MTPY (100% basis)

26

Re-Evaluating Future Project Portfolio to Match Market Demand Peabody Energy

Metropolitan modernization under way; expansion targeted for 2014 - 15 at higher volumes

Codrilla Mine development deferred Mine to add 2 - 3 MTPY (attributable ownership) to LV PCI platformUndergoing drilling and added value engineering

Wambo Open-Cut expansion now outside of planning horizon

27

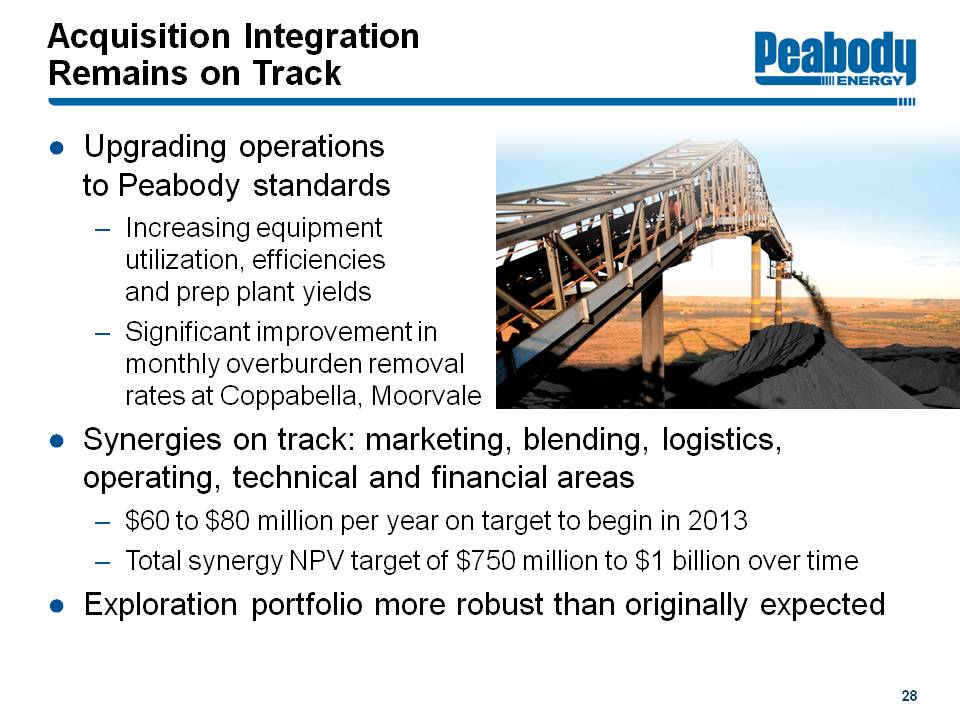

Acquisition Integration Remains on Track Peabody Energy

Upgrading operations to Peabody standards Increasing equipment utilization, efficiencies and prep plant yields Significant improvement in monthly overburden removal rates at Coppabella, Moorvale

Synergies on track: marketing, blending, logistics, operating, technical and financial areas $60 to $80 million per year on target to begin in 2013 Total synergy NPV target of $750 million to $1 billion over time

Exploration portfolio more robust than originally expected

28

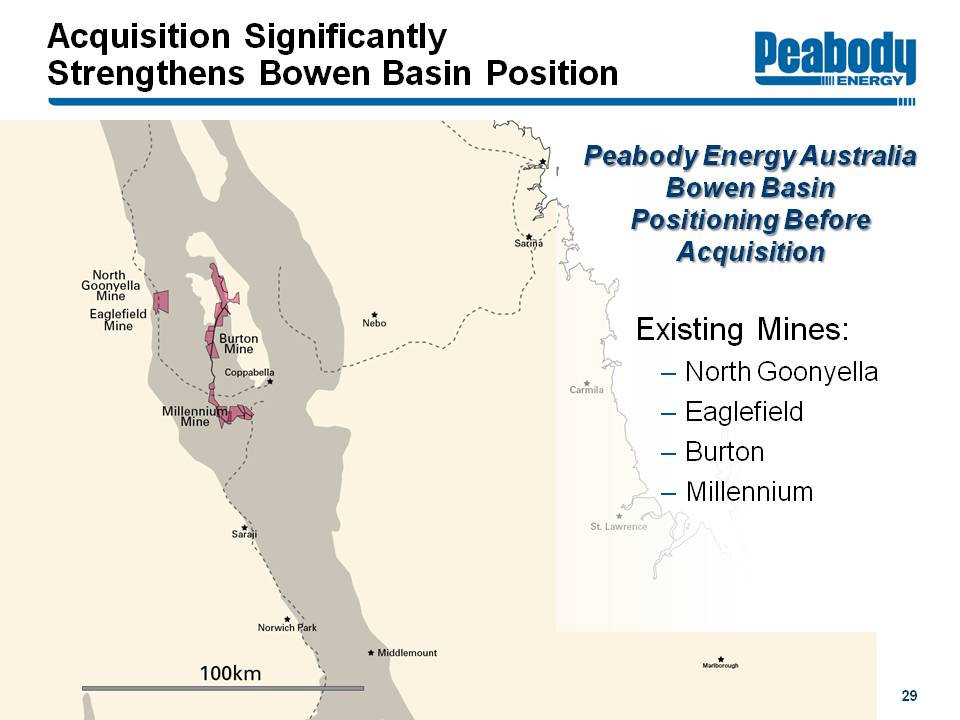

Acquisition Significantly Strengthens Bowen Basin Position Peabody Energy

Peabody Energy Australia Bowen Basin Positioning Before Acquisition

Existing Mines: North Goonyella Eaglefield Burton Millennium

North Goonyella Mine Eaglefield Mine Burton Mine Coppabella Nebo Millenium Mine Saraji Norwich Park Middlemount Sarina Carmila St. Lawrence Marlborough

100km

29

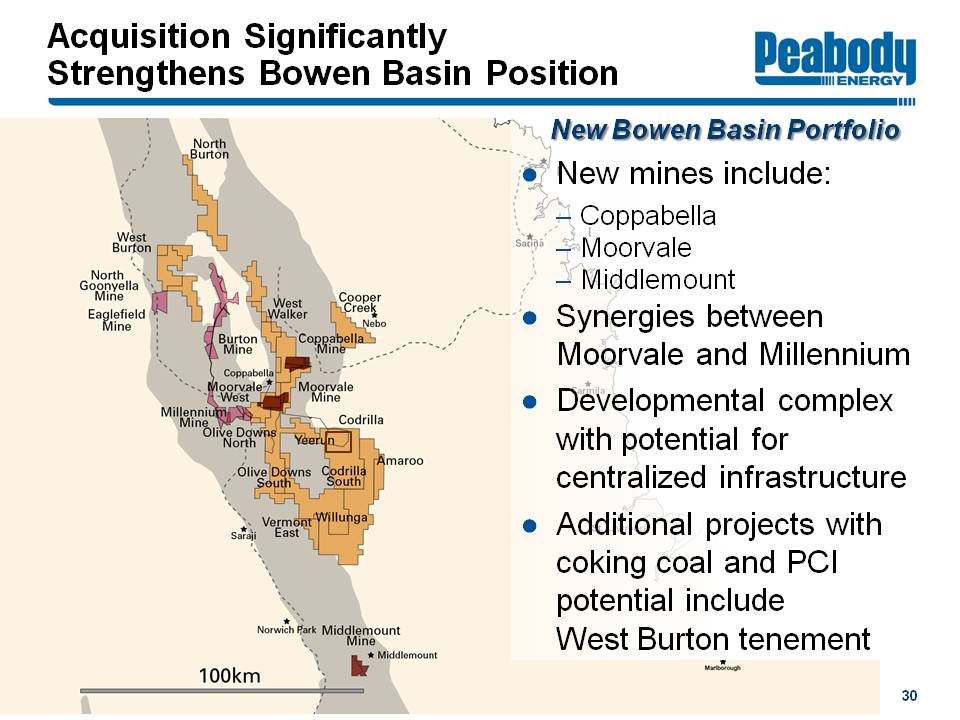

Acquisition Significantly Strengthens Bowen Basin Position Peabody Energy

New Bowen Basin Portfolio

New mines include: Coppabella Moorvale Middlemount

Synergies between Moorvale and Millennium

Developmental complex with potential for centralized infrastructure

Additional projects with coking coal and PCI potential include

West Burton tenement

100km

North Burton West Burton North Goonyella Mine Eaglefield Mine Burton Mine West Walker Cooper Creek Nebo Coppabella Mine Coppabella Moorvale West Moorvale Mine Millenium Mine Olive Downs North Olive Downs South Yeerun Codrilla Codrilla South Amaroo Vermont East Willunga Middlemount Mine Saraji Norwich Park Middlemount Sarina Carmila St. Lawrence Marlborough

30

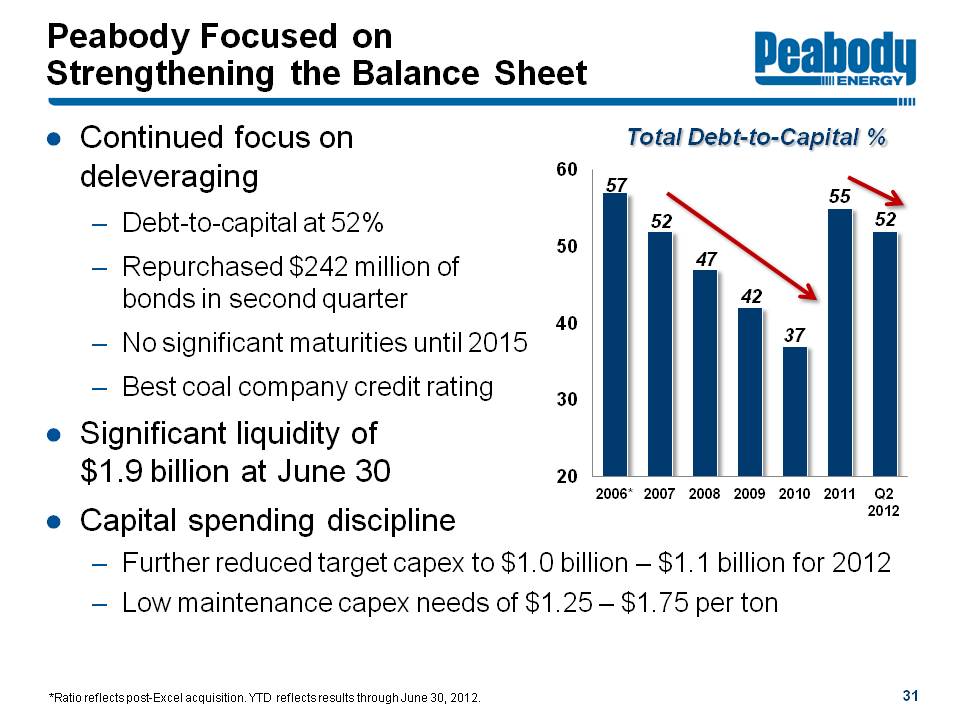

Peabody Focused on Strengthening the Balance Sheet Peabody Energy

Continued focus on deleveraging Debt-to-capital at 52% Repurchased $242 million of bonds in second quarter No significant maturities until 2015 Best coal company credit rating

Significant liquidity of $1.9 billion at June 30

Capital spending discipline Further reduced target capex to $1.0 billion - $1.1 billion for 2012 Low maintenance capex needs of $1.25 - $1.75 per ton

Total Debt-to-Capital % 20 30 40 50 60

2006* 57 2007 52 2008 47 2009 42 2010 37 2011 55 Q2 2012 52

*Ratio reflects post-Excel acquisition. YTD reflects results through June 30, 2012.

31

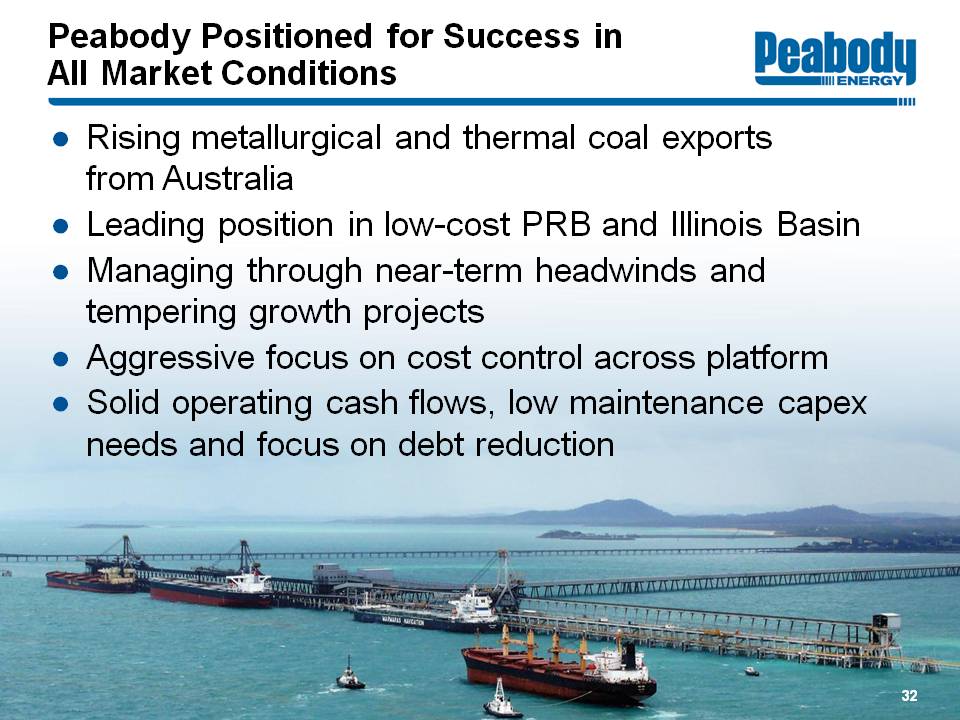

Peabody Positioned for Success in All Market Conditions Peabody Energy

Rising metallurgical and thermal coal exports from Australia

Leading position in low-cost PRB and Illinois Basin

Managing through near-term headwinds and tempering growth projects

Aggressive focus on cost control across platform

Solid operating cash flows, low maintenance capex needs and focus on debt reduction

32

Energizing The World One BTU At A Time

Barclays Energy Conference

Gregory H. Boyce Chairman and Chief Executive Officer

September 6, 2012

Peabody Energy

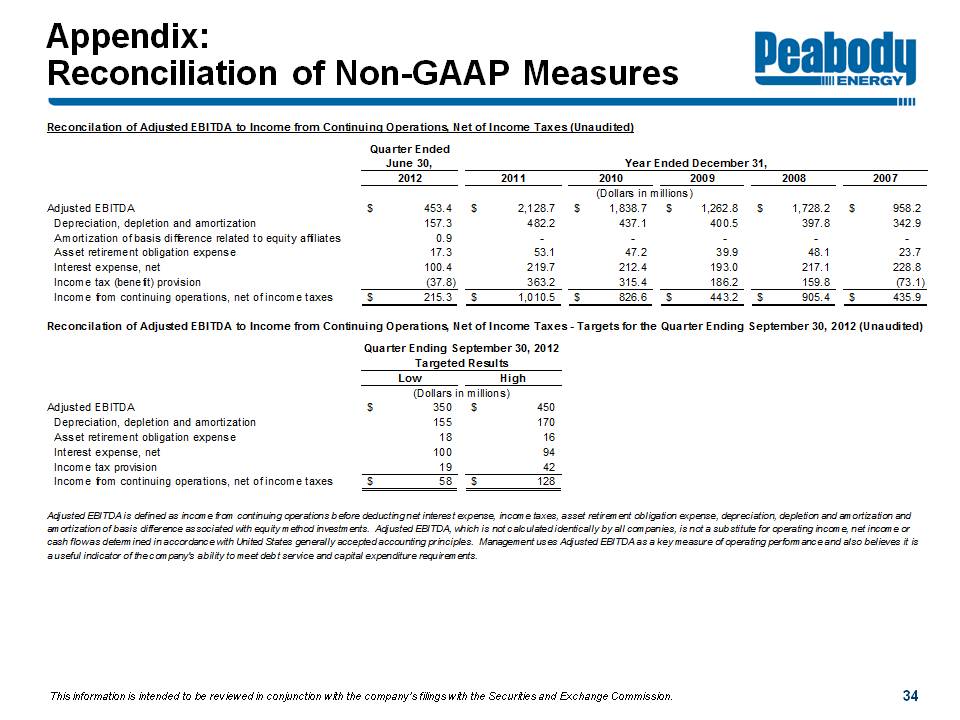

Appendix: Reconciliation of Non-GAAP Measures Peabody Energy

Reconciliation of Adjusted EBITDA to Income from Continuing Operations, Net of Income Taxes (Unaudited)

Quarter Ended June 30, 2012 Year ended December 31, 2011 2010 2009 2008 2007 (Dollars in Millions)

Adjusted EBITDA $453.4 $2,128.7 $1,838.7 $1,262.8 $1,728.2 $958.2

Depreciation, depletion and amortization 157.3 482.2 437.1 400.5 397.8 342.9

Amortization of basis difference related to equity affiliates 0.9 - - - - -

Asset retirement obligation expense 17.3 53.1 47.2 39.9 48.1 23.7

Interest expense, net 100.4 219.7 212.4 193.0 217.1 228.8

Income tax (benefit) provision (37.8) 363.2 315.4 186.2 159.8 (73.1)

Income from continuing operations, net of income taxes $215.3 $1,010.5 $826.6 $443.2 $905.4 $435.9

Reconciliation of Adjusted EBITDA to Income from Continuing Operations, Net of Income Taxes - Targets for the Quarter Ending September 30, 2012 (Unaudited)

Quarter Ending September 30, 2012 Targeted Results Low High (Dollars in Millions)

Adjusted EBITDA $350 $450

Depreciation, depletion and amortization 155 170

Asset retirement obligation expense 18 16

Interest expense, net 100 94

Income tax (benefit) provision 19 42

Income from continuing operations, net of income taxes $58 $128

Adjusted EBITDA is defined as income from continuing operations before deducting net interest expense, income taxes, asset retirement obligation expense, depreciation, depletion and amortization and amortization of basis difference associated with equity method investments. Adjusted EBITDA, which is not calculated identically by all companies, is not a substitute for operating income, net income or cash flow as determined in accordance with United States generally accepted accounting principles. Management uses Adjusted EBITDA as a key measure of operating performance and also believes it is a useful indicator of the company's ability to meet debt service and capital expenditure requirements.

This information is intended to be reviewed in conjunction with the company's filings with the Securities and Exchange Commission.

34