Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Vantage Drilling CO | d406643d8k.htm |

Vantage Drilling Company

Barclays CEO Energy Conference

New York, New York

September 5, 2012

Exhibit 99.1 |

Some of the statements in this presentation constitute forward-looking

statements. Forward-looking statements relate to

expectations,

beliefs,

projections,

future

plans

and

strategies,

anticipated

events

or

trends

and

similar

expressions

concerning matters that are not historical facts. The forward looking

statements contained in this presentation involve risks and uncertainties as

well as statements as to: •

our limited operating history;

•

availability of investment opportunities;

•

general volatility of the market price of our securities;

•

changes in our business strategy;

•

our ability to consummate an appropriate investment opportunity within given time

constraints; •

availability of qualified personnel;

•

changes in our industry, interest rates, the debt securities markets or the

general economy; •

changes in governmental, tax and environmental regulations and similar

matters; •

changes in generally accepted accounting principles by standard-setting

bodies; and •

the degree and nature of our competition.

The forward-looking statements are based on our beliefs, assumptions and

expectations of our future performance, taking into account all information

currently available to us. These beliefs, assumptions and expectations can change as a result

of many possible events or factors, not all of which are known to us or are within

our control. If a change occurs, our business, financial condition,

liquidity and results of operations may vary materially from those expressed in our forward-

looking statements.

Forward-Looking Statements

2 |

Symbol:

VTG (NYSE AMEX)

Location:

HQ

–

Houston;

Operations

–

Singapore;

Marketing

–

Dubai

Market Cap:

<

$450 million ($1.54 per share)

Book Value:

<

$700 million ($2.40 per share)

Enterprise Value:

<

$2.5 billion

Employees:

> 1,000

Contract Backlog:

$2.8 billion

Owned Fleet:

4 Ultra-Premium Jackups (operating in SE Asia & West Africa)

1 Ultra-Deepwater Drillship (operating offshore India)

1 Ultra-Deepwater Drillship (undergoing final acceptance testing in GOM)

1

Ultra-Deepwater

Drillship

(under

construction

–

May

2013

delivery)

Managed Fleet:

1

Ultra-Deepwater

Drillship

(under

construction

–

Q1/Q2

2013

delivery)

Corporate Overview

3 |

•

Aquamarine Driller

contract extended for an additional year at $153,400 per day, adding approximately

$56 million of backlog (prior contract at $132,000).

•

Sapphire Driller

awarded additional contracts at $165,000 per day net of taxes through the middle

of 2013, adding approximately $34.5 million to backlog (prior contract at

$120,000). •

Acquisition of Titanium Explorer

in April 2012. Undergoing customer acceptance testing with expected contract

commencement end of September 2012.

•

Ultra-deepwater

rates

rising,

providing

excellent

contracting

opportunity

for

Tungsten

Explorer

(2

Quarter 2013

delivery).

•

Platinum Explorer

has achieved impressive utilization –

–

First

12

months

of

operation

–

92.4%

utilization

–

Completed

1

Quarter

2012

@ 99.0%

utilization

–

Completed 2

Quarter 2012 @ 99.0% utilization

Recent Developments

4

nd

st

nd |

•

Premium high-specification drilling units, including four jackup rigs and three drillships

•

Vantage’s modern rigs are capable of drilling to deeper depths and possess enhanced operational

efficiency and technical capabilities, resulting in higher utilization, dayrates and

margins •

Total

costs

of

owned

fleet

of

four

jackups,

the

Platinum

Explorer

drillship

and

the

Titanium

Explorer

of

approximately

$2.6

billion

(<

$3.2

billion

upon

delivery/completion

of

Tungsten

Explorer)

•

Highly successful track record of managing, constructing, marketing and operating offshore drilling

units •

Deep in-house technical team of engineers and construction personnel overseeing complex

construction projects

•

All newbuilds delivered on budget and on time

•

Jackup fleet has experienced approx. 99% of productive time for Vantage’s first 42 months in

operation •

Significant long-term cash flow visibility

•

Contract backlog of approximately $2.7 billion with industry leading E&P Companies.

•

Work experience includes a strong customer mix including:

(1)

PVEP Phu Quy Petroleum Operating Co. Ltd. is a joint venture interest between PetroVietnam Exploration

Production Corp. and Total E&P Vietnam. Company Highlights

5

Premium Fleet

Proven Operational

Track

Record

Significant

Contract Coverage

with

High Quality

Counterparties

–

Level of efficiency is “best in class”

–

Total, ENI, Petrobras, ONGC, Petronas Cargali, PTT Thailand, Pearl Energy, Bowleven,

Foxtrot (1)

International, Phu Quy

, and Salamander. |

•

Successful construction management arrangements for ultra-deepwater

drillships, including completed

Aker

drillships

and

SeaDragon

semisubmersible

projects

and

ongoing

Dalian Developer

project.

•

Provided Vantage with significant engineering expertise and experience in Korean,

Chinese and Singaporean shipyards.

•

Management team with extensive experience; average of 29 years in the drilling

industry •

Includes international and domestic public company experience with

industry-leading peers involving numerous acquisitions and debt and

equity financings. •

Experienced

operating

and

technical

personnel

with

highest

level

of expertise.

Company Highlights (Cont’d)

6

Experienced

Construction

Supervision and

Management and

Operational Team

Arrangements

Management |

Owned Assets

•

Delivered On-Time, On-

Budget -

December 2008

•

Hired by Financial Institution to provide shipyard oversight

following bid process

•

Largest drillship in the world currently under construction

•

Vessel will include oil storage and multi-purpose

capabilities

•

Delivery Q2 2013

•

3

newbuild project at DSME

•

Leverages shipyard experience

•

Favorable costs and delivery

schedule

•

Delivery Q2 2013

Tungsten Explorer

Premium Owned Fleet with a Proven Operational

Track Record

7

•

2 Successful newbuild at

DSME

•

Delivery April 2012

•

On Contract by Q4 2012

Construction Management Projects

Dalian Developer

Newbuild Ultra-Premium Marine Pacific Class 375 Jackups

Emerald Driller

Sapphire Driller

Aquamarine Driller

Topaz Driller

Platinum Explorer

Ultra-Deepwater 12,000 ft Drillships

•

Delivered On-Time, On-

Budget -

November 2010

•

Delivered On-Time, On-

Budget -

July 2009

•

Delivered On-Time, On-

Budget -

December 2009

•

Delivered On-Time, On-

Budget -

September 2009

Titanium Explorer

Ultra-Deepwater Drillship

nd

rd |

Business Strategy

8

•

Customer demand for new high-specification units supported by:

–

Need for rigs well-suited for drilling through deep and complex formations and

drilling horizontally –

Enhanced efficiency providing faster drilling and moving times

–

Improved safety features and lower downtime for maintenance

•

Long-term

drillship

contracts

for

Platinum

Explorer

(5

years)

and

Titanium

Explorer

(8 years)

•

Marketing

Tungsten

Explorer

with

focus

on

project

term

of

3-5

years

•

Jackups operating on contracts with multi-year term

•

Negotiating multi-year extension for Emerald Driller

•

$2.7 billion in contract backlog mitigates cyclical oil and gas industry

risk •

Focused on expanding relationships with national oil companies, major oil

companies, large independents and super-regionals (generally longer

contract duration) •

Strong

existing

relationships

have

contributed

to

large

existing

backlog

and

repeat business

with

customers

•

Organic growth through attractive shipyard orders

•

Growth through acquisitions of assets and other offshore drilling companies

•

Both deepwater and jackups attractive; however current conditions favor

ultra-deepwater Capitalize on Customer

Demand for High-

Specification Units

Focus on Long-term

Contracts

Expand Key Industry

Relationships

Pursue Expansion

Opportunities |

Vantage Offices

Managed Rigs

Country of Operation

Worldwide Operations

9

Houston

Dubai

Singapore

Contract: Petrobras

Titanium Explorer

U.S. GOM

Sapphire Driller

Contract: Foxtrot

Ivory Coast

Contract: ONGC

Platinum Explorer

India

Contract: PTT

Emerald Driller

Thailand

Aquamarine Driller

Contract: Petronas

Carigaili

Malaysia

Topaz Driller

Contract: Total

Malaysia

Owned Rigs |

Strong Customer Relationships

10

Key Customers |

•

Faster drilling times

•

Faster moving times

•

Increased volumes of consumable liquids and

drilling fluids

•

Reduced boat runs and non-productive time

•

Improved pipe handling and offline capability

•

Fast preloading time for all tanks

•

75’

x 30’

cantilever reach substantially greater

than the industry average

•

Pipe decks allow increased storage capacity

•

Premium drilling package:

•

3 x 2200HP mud pumps

•

Integrated diverter system

•

18-¾’’

BOP system and 4 rams

•

High-capacity, high efficiency –

5 x CAT 3516 B

Diesel engines

Ultra-Premium Jackup Fleet

11

Emerald

Driller

Sapphire

Driller

Topaz

Driller

Aquamarine

Driller

World

class

assets

achieving

world

class

performance

Fleet

productive

time

approximately

99%

since

inception

Quarterly Financial Performance

Increased Operational Efficiency and

Improved Technical Capability: |

(1)

Average

drilling

revenue

per

day

is

based

on

the

total

estimated

revenue

divided

by

the

minimum

number

of

days

committed

in

a

contract.

Unless

otherwise

noted,

the

total

revenue

includes

any

mobilization

and

demobilization

fees

and

other

contractual

revenues

associated

with

the

drilling

services.

(2)

The drilling revenue per day includes the achievement of the 12.5% bonus

opportunity, but excludes mobilization revenues and revenue escalations included in the contract.

Fleet Status –

Average Drilling Revenue/Day

12

Ownership

2012

2013

2014

Rig

%

Q1

Q2

Q3

Q4

Q1

Q2

Q4

Q1

Q2

Q3

Q4

Jackups

Emerald Driller

100%

$130K

Sapphire Driller

100%

$120K (net of taxes)

$165K (net)

$165K (net)

$175 (net)

Aquamarine Driller

100%

$132K

$153K

Topaz Driller

100%

$187K (includes upgrades and mobilization)

$135K

Drillships

Platinum Explorer

100%

$590.5K (5 years)

Titanium Explorer

100%

$572K (8 years)

(2)

Tungsten Explorer

100%

Contracted

Option

Commisioning /

Construction

Contract

Mobilization /

(1)

Q3

Contract extension being negotiated for Emerald

(up to 3 years) |

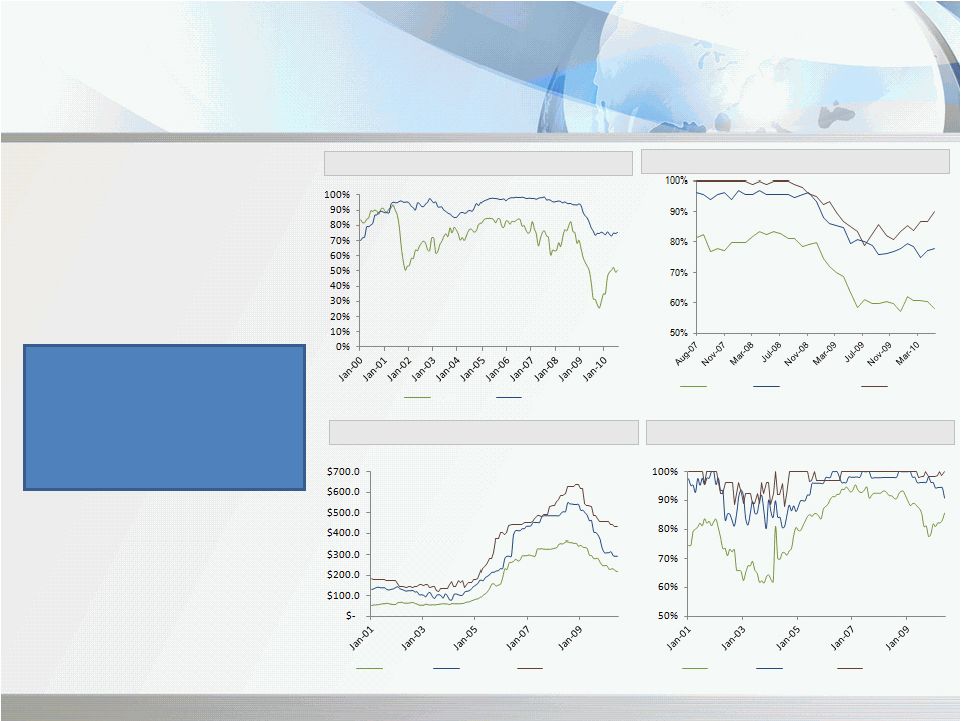

•

Premium jackups (350’

+ IC rigs)

and ultra-deepwater floater have

historically maintained

significantly higher utilization

levels

Source: Riglogix; ODS-PetroData.

Premium Asset Advantage

13

Recent leading edge

dayrates have reached

$170K for jackups and

$650K for ultra-deepwater

floaters

Global Jackup Utilization

International vs. GOM Jackup Utilization

Historical Floater Dayrates ($Thousands)

Historical Floater Utilization

GOM

Midwater

Deepwater

Ultradeepwater

Midwater

Deepwater

Ultra-Deepwater

<300 ft.

300 to 349 ft. IC

350+ ft IC

Rest of World |

•

Capabilities and age –

The current worldwide fleet is comprised mostly of older, inefficient rigs

Source: ODS-Petrodata

Global Jackup Fleet Distribution

Profile of Global Jackup Fleet

14

Age

Rigs

%

%

300+

200-299

<200

25 years or older

325

68%

58%

152

119

54

5 to 24 years

64

13%

11%

59

1

4

0 to 4 years

90

19%

16%

80

6

4

479

100%

291

126

62

2012 Deliveries

26

5%

24

2

0

2013 Deliveries

38

7%

37

1

0

2014 Deliveries

15

3%

13

2

0

558

100%

365

131

62

Age of Jackup Fleet

Water Depth (feet)

Despite 126 newbuild deliveries since 2003, majority of worldwide

jackup fleet remains older than 25 years

–

22% of today’s jackups are mat-supported and/or have less than 200ft of

water depth capability –

68% of today’s jackups are 25 years or older

–

As of March 2012 a total of 85 rigs were either stacked, cold stacked, or in an

accommodation mode without drilling contract –

How many will not return to service?

•

Age is a factor –

Demand is increasing for high-specification jackups. Many customers are

implementing age restrictions and new high-specification

requirements. MS

18

300'+ IC

151

MC

40

300'+ IC

9

250' IC

57

<300' IS

15

<250' IC

65

300' IC

131 |

Ultra-Deepwater Rig Supply is Increasing Significantly

Deepwater Exploration is a Young, Rapidly Growing Market

Demand is Likely to Exceed Rig Supply Despite Newbuilds

Source: ODS-Petrodata, DnB NOR

Global Deepwater Market

15

Recent fixtures

>$650,000 per day |

Balance Sheet

($Millions)

Financial Overview

16

Long-term

Debt matures

in 2015

First Call

option

February

2013

December 31,

December 31,

June 30,

2010

2011

2012

Cash and cash equivalents

120.4

$

110.0

$

123.7

$

Restricted cash

29.0

7.0

5.9

Trade receivables

50.2

100.9

78.2

Inventory

19.8

24.4

33.6

Prepaid expenses and other current assets

11.5

16.9

13.0

230.9

259.3

254.5

Property and equipment, net

1,718.1

1,805.1

2,648.2

Investment in joint venture

-

-

-

Other assets

54.2

58.2

86.4

2,003.2

$

2,122.5

$

2,989.1

$

Accounts payable and accrued liabilities

107.5

$

148.1

$

197.0

$

Short-term debt

8.6

-

-

Current maturities of long-term debt

-

-

-

116.1

148.1

197.0

Long–term debt

1,103.5

1,246.4

2,082.7

Other long term liabilities

13.5

29.8

20.1

Shareholders' Equity

Paid-in capital

854.8

860.8

865.2

Retained Earnings

(84.7)

(162.6)

(175.8)

Accumulated other comprehensive loss

-

-

-

Total shareholders’

equity

770.2

698.2

689.4

2,003.2

$

2,122.5

$

2,989.1

$

Outstanding shares

289.7

291.2

292.4

Book value per share

2.66

$

2.40

$

2.36

$

|

EBITDA

Low

6.5x

Today’s

Peer Avg.

8.8x

Historical

Peer Avg.

11.6x

$400 million

$2.04

$4.91

$8.42

$450 million

$3.04

$6.29

$10.23

$500 million

$4.06

$7.66

$12.05

$550 million

$5.08

$9.04

$13.87

Implied

Values

–

EV/EBITDA

Source: Jefferies

Price to Book Value

Key Drivers Near Term –

•

Achieve high productive time on Platinum

Explorer •

Improving dayrate contract fixtures on jackups

•

Commencement of operations in US GOM for Titanium

Explorer •

Contract for the Tungsten Explorer

•

Refinance $2 billion debt in 2013

17

Significant Upside Valuation Potential

Peer Group (current)

Peer Group (2009-2010)

Peer Group (2005-2009)

VTG

140%

190%

300%

64% |

Historical Financial

Information ($ Millions)

Financial Overview

18

Achieved record Revenue and

Adjusted EBITDA in 1 Quarter 2012

Quarter Ended

Revenue

Adjusted EBITDA

$140.0

$120.0

$100.0

$80.0

$60.0

$40.0

$20.0

$0.0

$14.3

$6.4

$22.2

$9.5

$36.4

$14.2

$38.6

$58.3

$5.0

$25.3

$68.4

$24.6

$66.9

$21.3

$84.9

$16.9

$124.6

$42.8

$120.9

$49.7

$118.5

$44.8

$121.3

$47.3

$131.8

$60.3

$105.1

$50.9

3/31/2009

6/30/2009

9/30/2009

12/31/2009

3/31/2010

6/30/2010

9/30/2010

12/31/2010

3/31/2011

6/30/2011

9/30/2011

12/31/2011

3/31/2012

6/30/2012

st |

Reconciliation of Net Income (Loss) to Adjusted EBITDA

($Millions)

Appendix

19

3/31/2010

6/30/2010

9/30/2010

12/31/2010

3/31/2011

6/30/2011

9/30/2011

12/31/2011

3/31/2012

6/30/2012

Net income (loss)

6.0

$

(7.0)

$

(33.6)

$

(13.0)

$

(18.7)

$

(40.1)

$

(11.9)

$

(7.3)

$

(1.2)

$

(10.0)

$

Interest expense, net

8.0

13.3

13.9

14.1

41.5

39.3

37.1

37.5

36.8

36.2

Income tax provision (benefit)

2.3

8.4

2.8

5.5

2.9

7.8

2.0

(1.2)

5.8

6.1

Depreciation

7.5

8.4

8.8

8.8

16.1

16.0

16.0

16.4

16.6

16.4

Loss on debt extinguishment

-

-

24.0

-

-

25.2

-

-

-

-

Loss on acquisition of subsidiary

-

-

3.8

-

-

-

-

-

-

-

EBITDA

23.8

$

23.1

$

19.7

$

15.4

$

41.9

$

48.2

$

43.2

$

45.4

$

58.0

$

48.7

$

Share-based compensation expense

1.5

1.5

1.6

1.5

0.9

1.5

1.6

1.9

2.3

2.2

Adjusted EBITDA

25.3

$

24.6

$

21.3

$

16.9

$

42.8

$

49.7

$

44.8

$

47.3

$

60.3

$

50.9

$ |