Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Approach Resources Inc | d403149d8k.htm |

INVESTOR

PRESENTATION

AUGUST / SEPTEMBER 2012

Exhibit 99.1 |

Forward Looking-Statements

2

Cautionary Statements Regarding Oil & Gas Quantities

This presentation contains forward-looking statements within the meaning of Section 27A of the

Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All statements, other

than statements of historical facts, included in this presentation that address activities, events or

developments that the Company expects, believes or anticipates will or may occur in the future are

forward-looking statements. Without limiting the generality of the foregoing, forward-looking

statements contained in this presentation specifically include the expectations of management regarding

plans, strategies, objectives, anticipated financial and operating results of the Company, including as

to the Company’s Wolffork shale resource play, estimated resource potential and recoverability

of the oil and gas, estimated reserves and drilling locations, capital expenditures, typical well

results, and well profiles, type curve, and production and operating expenses guidance included in the

presentation. These statements are based on certain assumptions made by the Company based on

management's experience and technical analyses, current conditions, anticipated future

developments and other factors believed to be appropriate and believed to be reasonable by management.

When used in this presentation, the words “will,” “potential,” “believe,” “intend,” “expect,”

“may,” “should,” “anticipate,” “could,” “estimate,”

“plan,” “predict,” “project,” “target,” “profile,” “model” or their negatives, other similar expressions or the statements that include those words, are

intended to identify forward-looking statements, although not all forward-looking statements

contain such identifying words. Such statements are subject to a number of assumptions, risks and

uncertainties, many of which are beyond the control of the Company, which may cause actual results to

differ materially from those implied or expressed by the forward-looking statements. In

particular, careful consideration should be given to the cautionary statements and risk factors

described in the Company's most recent Annual Report on Form 10-K and Quarterly Report on

Form 10-Q. Any forward-looking statement speaks only as of the date on which such

statement is made and the Company undertakes no obligation to correct or update any forward-looking

statement, whether as a result of new information, future events or otherwise, except as required by

applicable law. The Securities and Exchange Commission (“SEC”) permits oil and gas companies, in their

filings with the SEC, to disclose only proved, probable and possible reserves that meet the SEC’s

definitions for such terms, and price and cost sensitivities for such reserves, and prohibits

disclosure of resources that do not constitute such reserves. The Company uses the terms “estimated

ultimate recovery” or “EUR,” reserve or resource “potential,” and other

descriptions of volumes of reserves potentially recoverable through additional drilling or recovery techniques that the SEC’s

rules may prohibit the Company from including in filings with the SEC. These estimates are by their

nature more speculative than estimates of proved, probable and possible reserves and accordingly

are subject to substantially greater risk of being actually realized by the Company.

EUR estimates, potential drilling locations and resource potential estimates have not been risked by

the Company. Actual locations drilled and quantities that may be ultimately recovered from the

Company’s interest may differ substantially from the Company’s estimates. There is no

commitment by the Company to drill all of the drilling locations that have been attributed these quantities.

Factors affecting ultimate recovery include the scope of the Company’s ongoing drilling program,

which will be directly affected by the availability of capital, drilling and production costs, availability of

drilling and completion services and equipment, drilling results, lease expirations, regulatory

approval and actual drilling results, as well as geological and mechanical factors Estimates of unproved

reserves, type/decline curves, per well EUR and resource potential may change significantly as

development of the Company’s oil and gas assets provides additional data.

Type/decline curves, estimated EURs, resource potential, recovery factors and well costs represent

Company estimates based on evaluation of petrophysical analysis, core data and well logs, well

performance from limited drilling and recompletion results and seismic data, and have not been

reviewed by independent engineers. These are presented as hypothetical recoveries if assumptions

and estimates regarding recoverable hydrocarbons, recovery factors and costs prove correct. The Company

has very limited production experience with these projects, and accordingly, such estimates may

change significantly as results from more wells are evaluated. Estimates of resource potential and EURs do not constitute reserves, but constitute estimates of contingent resources

which the SEC has determined are too speculative to include in SEC filings. Unless otherwise noted, IRR

estimates assume NYMEX forward-curve oil and gas pricing and Company-generated EUR and

decline curve estimates based on Company drilling and completion cost estimates that do not include land, seismic or G&A costs.

|

Notes: Proved reserves and acreage as of 6/30/2012. All Boe and Mcfe calculations

are based on a 6 to 1 conversion ratio. Enterprise value is equal to market

capitalization

using

the

closing

share

price

of

$27.73

per

share

on

8/23/2012,

plus

net

debt

as

of

6/30/2012.

Company Overview

•

Enterprise value $1.1 BN

•

High quality reserve base

83.7 MMBoe proved reserves, 37% PD

99% Permian Basin

•

Permian core operating area

166,000 gross (146,000 net) acres

500+ MMBoe gross, unrisked resource

potential

2,900+ drilling and recompletion opportunities

•

Oil-driven, high margin production

2Q’12 Production 7.7 MBoe/d, 65% oil & NGLs

2Q’12 Revenue mix 64% oil, 25% NGLs and

11% natural gas

3

AREX OVERVIEW

ASSET OVERVIEW |

AREX

2Q’12 Highlights 4

•

Oil

growth

key

contributor

to

total

production

growth

•

Production totaled 7.7 MBoe/d, up 16% and 7% over 2Q’11 and 1Q’12,

respectively •

Oil growth up 120% over 2Q’11 and 20% over 1Q’12

•

Oil

growth

key

contributor

to

total

reserves

growth

at

MY’12

•

Estimated proved reserves total 83.7 MMBoe, up 9% and 25% over YE’11 and

MY’11 proved reserves, respectively

•

Oil proved reserves total 23.5 MMBbls, increasing 30% and 132% over YE’11 and

MY’11 proved reserves, respectively

•

Horizontal Wolfcamp delivering strong results

•

Strong

well

performance

from

horizontal

Wolfcamp

“B”

in

Project

Pangea

•

Encouraging

well

performance

from

horizontal

Wolfcamp

“A”

pilot

wells

in

Pangea

West |

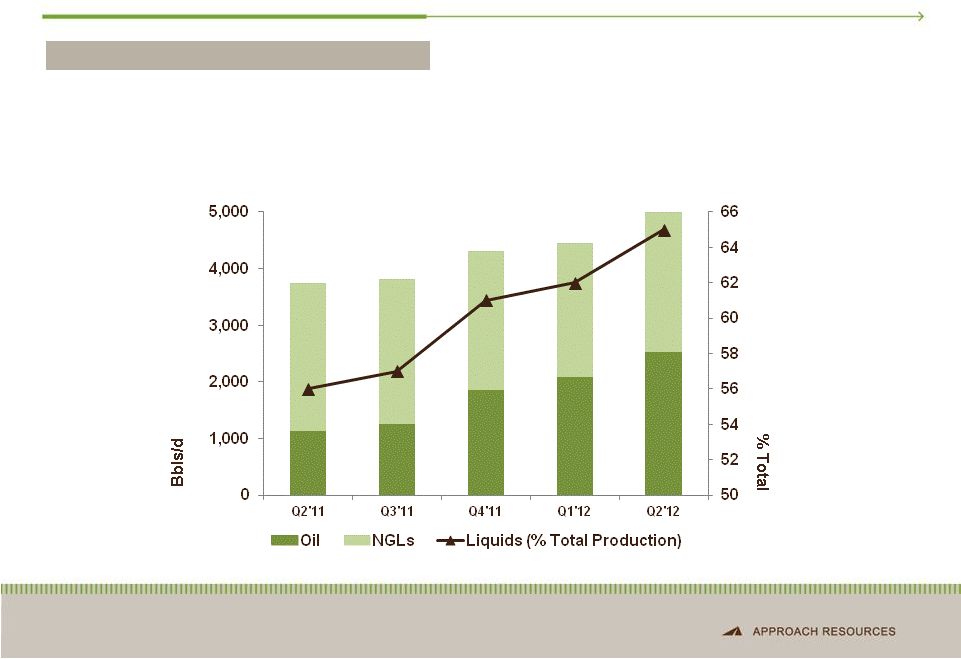

Quarterly Liquids Production

5

2Q’12 LIQUIDS PRODUCTION

•

2Q’12 Liquids production up 33% over 2Q’11

65% total production volumes

•

2Q’12 Oil production up 120% over 2Q’11

28% total production volumes |

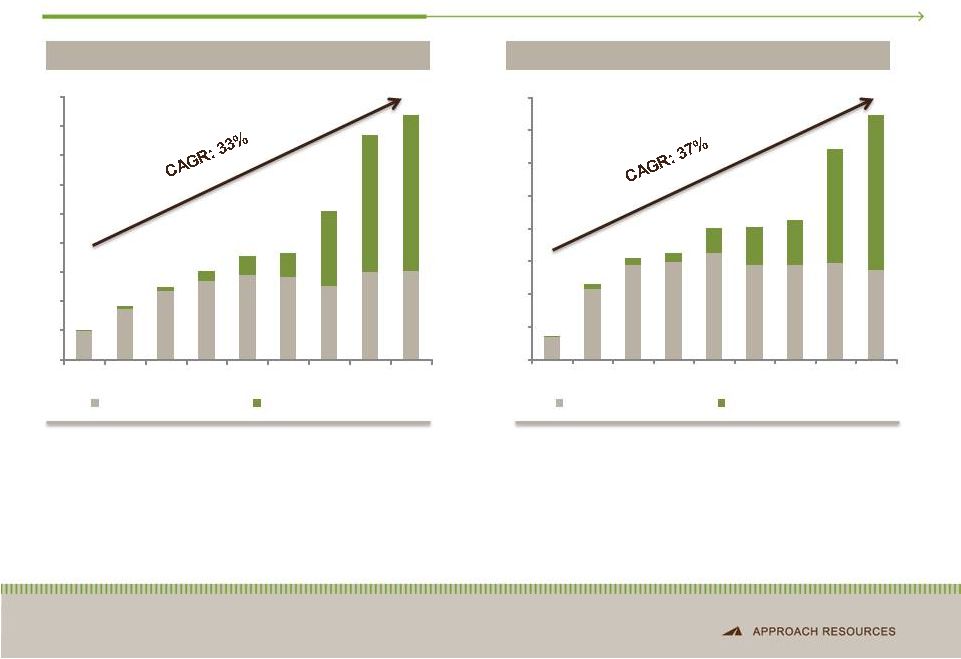

Track

Record of Reserve and Production Growth •

MY’12 reserves up 25% YoY and 9% over YE’12

Oil reserves up 33% to 23.5 MMbbls

•

Wolfcamp Shale key contributor to reserve growth

500+ MMBoe gross, unrisked resource potential

6

RESERVE GROWTH

PRODUCTION GROWTH

•

2011 production increased 50% YoY

•

Targeting 28% production growth in 2012

•

Strong liquids production growth

2012E production 65% liquids

0

10

20

30

40

50

60

70

80

90

2004

2005

2006

2007

2008

2009

2010

2011

MY'12

Natural Gas (MMBoe)

Oil & NGLs (MMbbls)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2004

2005

2006

2007

2008

2009

2010

2011

MY'12

Natural Gas (MBoe/d)

Oil & NGLs (Mbbls/d) |

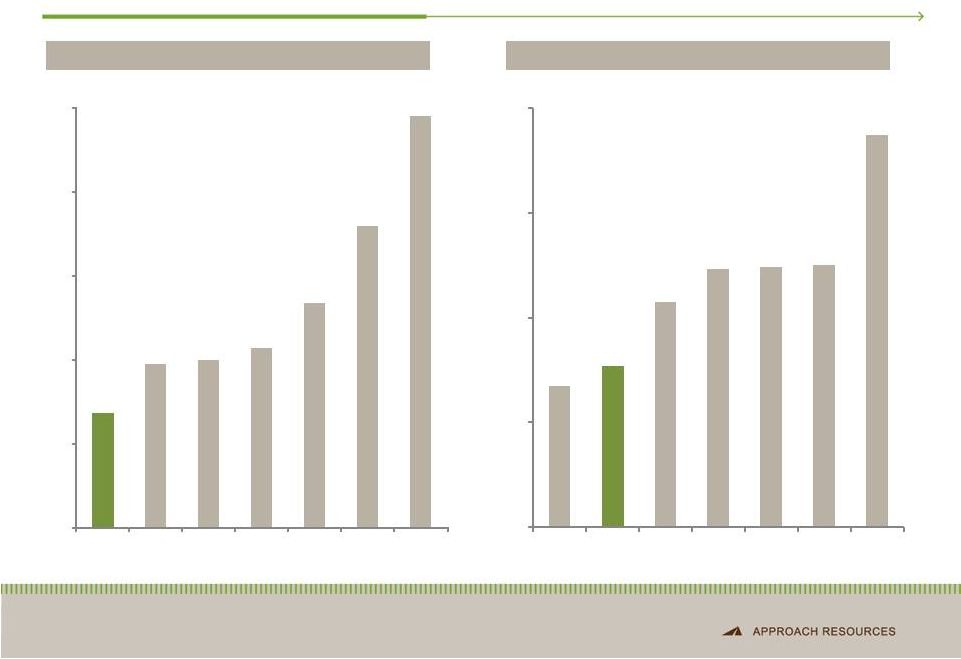

Low-Cost Operator

7

3-YR AVERAGE F&D COSTS ($/BOE)

2Q’12 LIFTING COSTS ($/BOE)

Notes: Oil weighted peers include BRY, CXO, KOG, LPI, NOG, OAS. Data based on SEC

filings and J.S. Herold data. 3-YR F&D costs represent drill-bit F&D

costs (drill-bit F&D costs defined as Exploration and Development Costs

divided by Reserve Extensions & Discoveries and Revisions less Production). Lifting

costs defined as lease operating expense plus taxes other than income and gathering

and transportation expense. $8.20

$11.71

$11.98

$12.84

$16.06

$21.57

$29.40

$0

$6

$12

$18

$24

$30

AREX

Peer 1

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6

$8.04

$9.23

$12.85

$14.73

$14.89

$14.96

$22.43

$0

$6

$12

$18

$24

Peer 1

AREX

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6 |

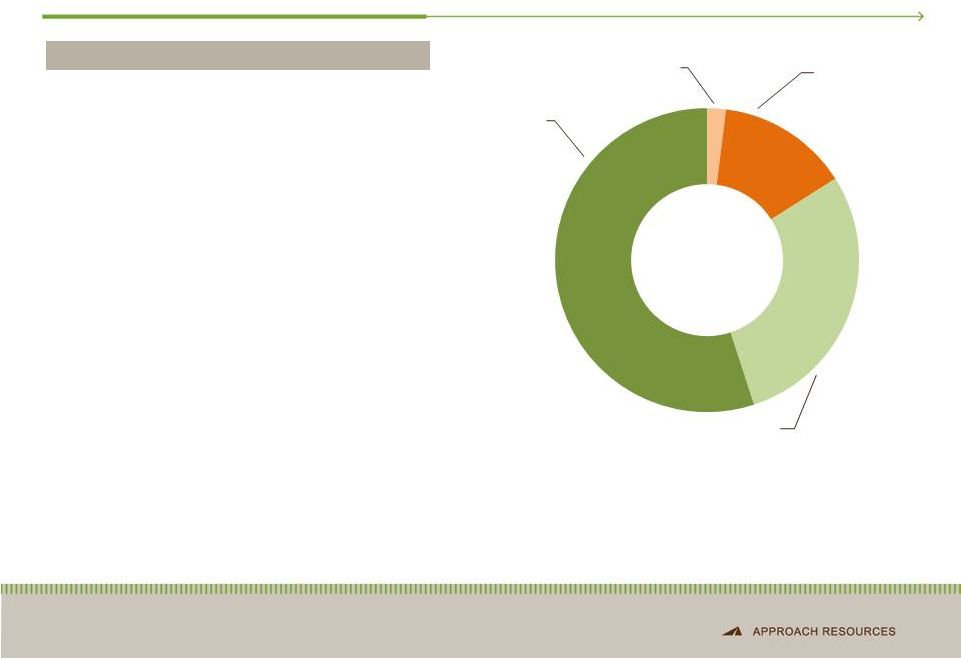

2012

Capital Program 8

•

Horizontal Wolfcamp

2 horizontal rigs

Beginning development program of B zone

Testing A & C zones

•

Vertical Clearfork & Wolfcamp

1 vertical rig and recompletion program

•

Infrastructure & Equipment

Upfront investments to prepare for large-scale field

development

-

Lower drilling and completion costs

-

Transportation for growing crude production

•

Acreage –

Strategic, bolt-on additions

•

Targeting 28% production growth

2012

production

guidance

2.9

MMBoe

–

3.1

MMBoe

2012 PROGRAM OVERVIEW

2012 Capital Program $260 MM

2%

14%

29%

55%

Horizontal

Wolfcamp

Acreage

Infrastructure &

Equipment

Vertical Wolffork &

Recompletions |

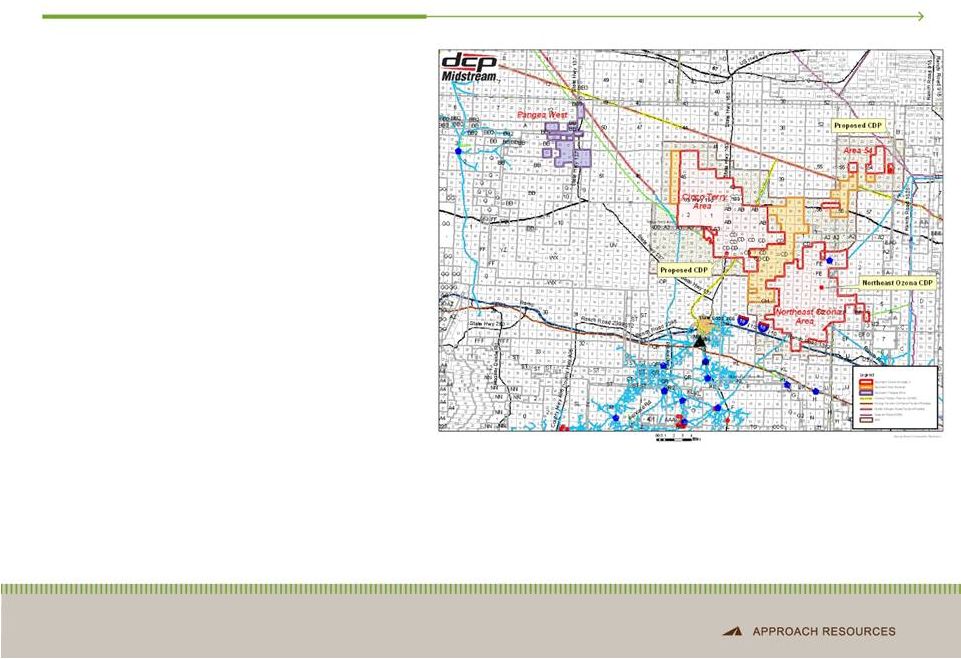

Major

Infrastructure in Place 9

•

Gas Processing –

DCP

•

Gas Processing –

WTG

•

NGL Pipeline

CP Chemical EZ Line to Mont Belvieu

Sand Hills Pipeline will provide new capacity for

NGLs to Mont Belvieu (initial capacity 200

MBbls/d; expected to be operational for

Permian Basin barrels in 3Q’13)

•

Oil Transportation

WTG Benedum Gas Plant (current capacity 110

MMcf/d)

Ozona Gas Plant (current capacity 120 MMcf/d)

SW Ozona Gas Plant (current capacity 100

MMcf/d)

Company owned and third-party oil hauling

trucks |

Infrastructure & Equipment Projects

10

•

Safely and securely transport water across Project Pangea and Pangea West

and reduce truck traffic

•

Reduce time and money spent on water hauling and disposal

•

Replace rental equipment and contractors with Company-owned and operated

equipment and personnel

•

Reduce money spent on flowback operations

•

Facilitate large-scale field development

•

Reduce fresh water use

•

Reduce water costs

•

Efficiently transport crude oil to market and reduce inventory

•

Reduce oil differential

Purchasing and installing water

transfer equipment

Drilling and/or converting SWD

wells

Purchasing and installing flowback

equipment

Securing water supply

Testing non-potable water and

recycling flowback water

Installing crude takeaway lines

Purchased oil hauling trucks

PROJECTS

BENEFITS

Infrastructure and equipment projects are key to large-scale field

development and to reducing D&C costs and

monthly LOE |

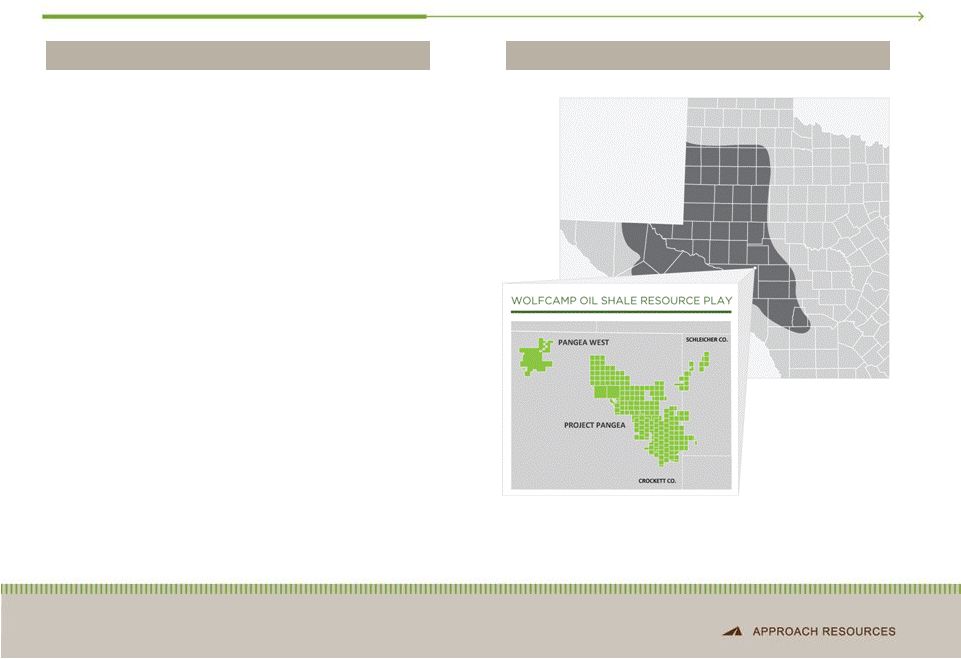

AREX

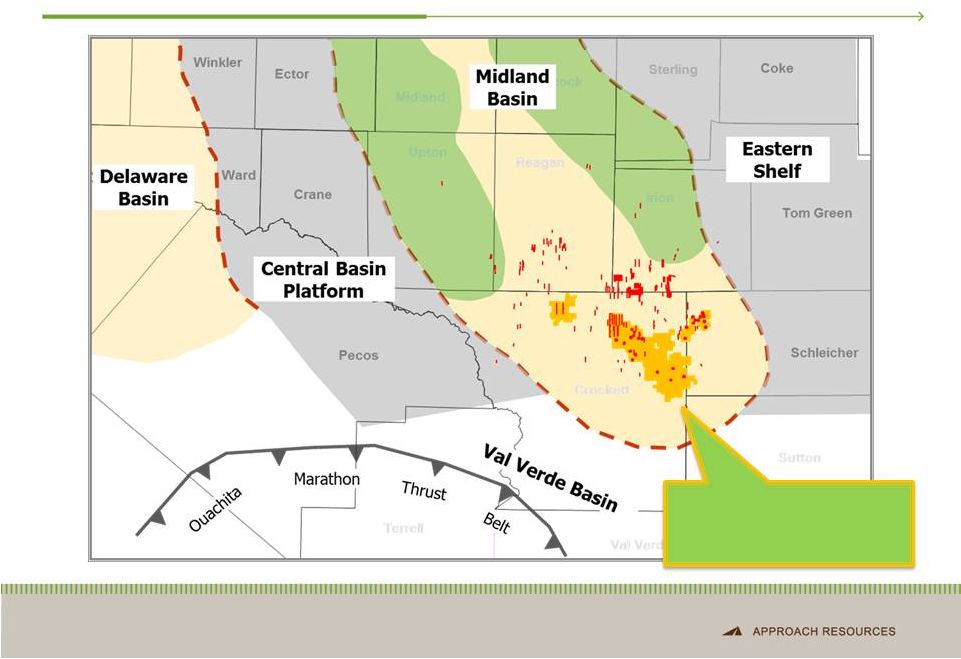

Wolfcamp Play Favorably Located in the S. Midland Basin 11

Wolfcamp / Wolffork Oil

Shale Resource Play |

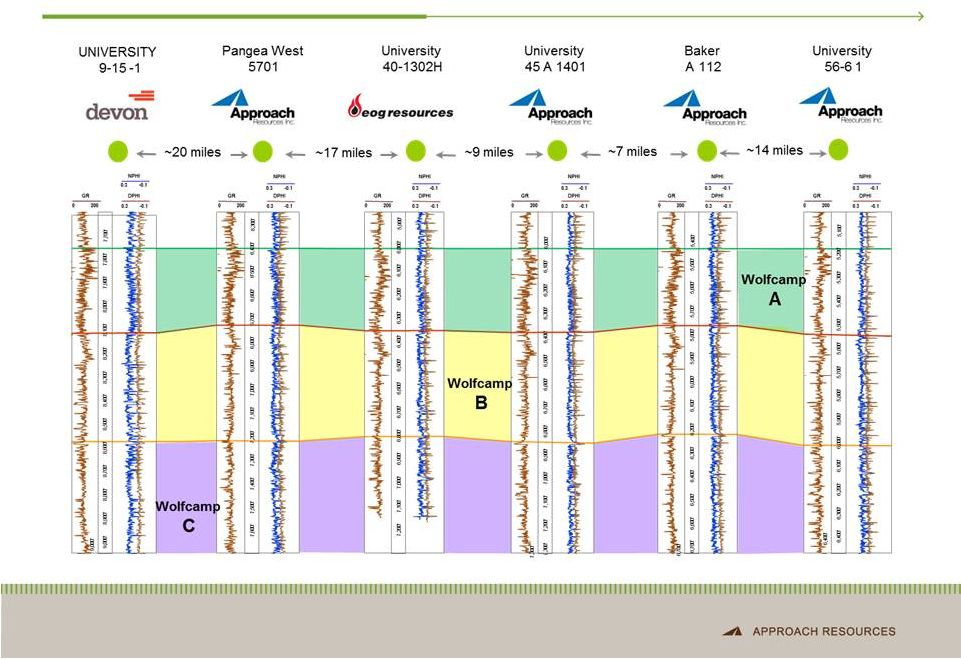

12

Wolfcamp Oil Shale Play –

Widespread, Thick, Consistent & Repeatable |

AREX

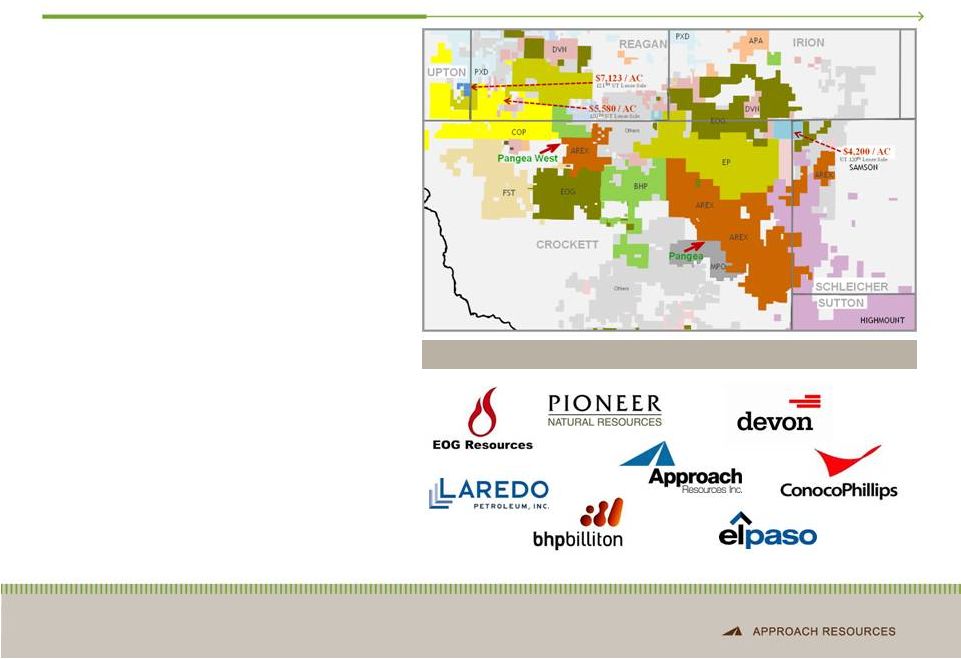

Wolfcamp Oil Shale Resource Play 13

ACTIVE PARTICIPANTS IN THE PLAY

Large, primarily contiguous acreage position

Liquids-rich, multiple pay zones

166,000 gross (146,000 net) acres

Low acreage cost ~$500 per acre

2,900+ drilling and recompletion opportunities

Transitioning Wolfcamp B to development

Testing multiple horizontal laterals targeting

Testing tighter well spacing

Preparing field for large-scale development

Broad industry participation de-risking play

41 Horizontal Wolfcamp rigs as of July 2012

Average peak IP rate of 807 Boe/d in 2Q’12

Average lateral well length of ~7,100 ft.

500+ MMBoe gross, unrisked resource

500+ MMBoe gross, unrisked resource

potential

Early-stage development

mode

the Wolfcamp A and C

Note: Number of Horizontal Wolfcamp rigs per PXD July 2012 investor presentation. Average peak IP

rate and average lateral well length based on public disclosure from AREX, EOG, PXD. |

AREX

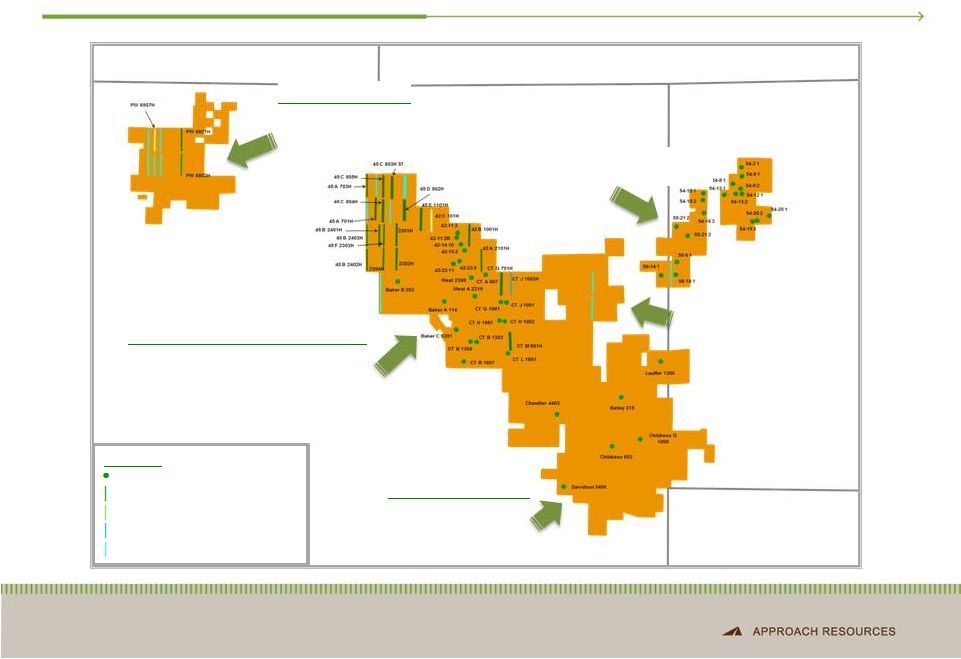

Wolfcamp Play – Activity Map

14

Pangea West

North & Central Pangea

South Pangea

•

18,000 gross acres

•

2 horizontal pilot wells with encouraging

results

Schleicher

Crockett

Irion

Reagan

•

3D Seismic planning underway

•

Targeting horizontal pilot well in

4Q’12

•

Interpreting newly acquired

3D seismic

•

Targeting horizontal pilot

well in 4Q’12

•

59,000 gross acres

•

Continuing

completion design

improvement

•

89,000 gross acres

•

Continuing horizontal and vertical

development

•

Continuing refining completion designs

Sutton

Legend

Vertical Producer

HZ Producer

HZ –

Waiting on Completion

HZ –

Drilling

HZ –

Permit |

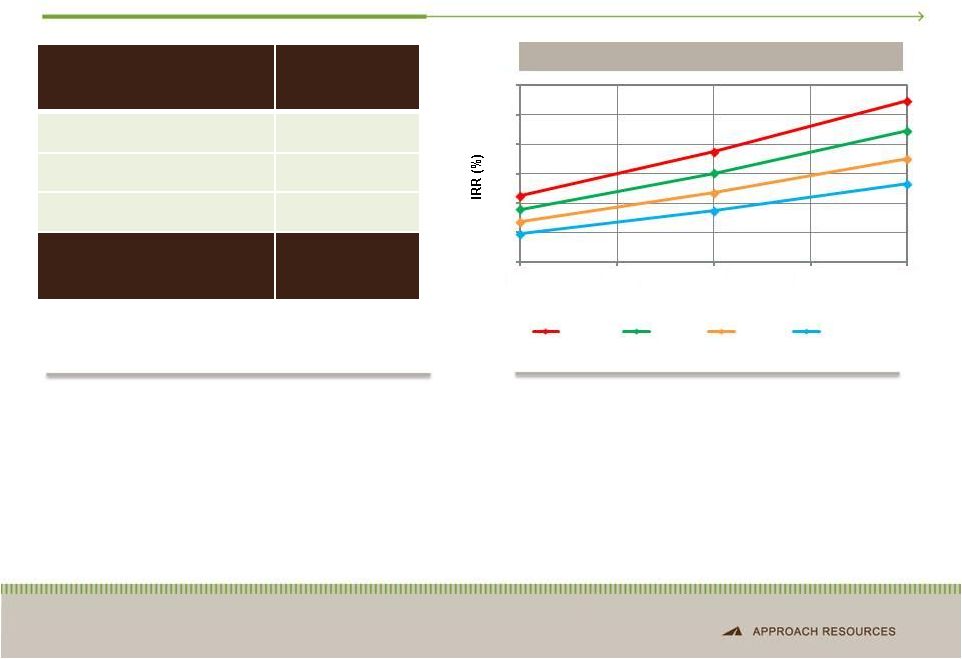

Horizontal Wolfcamp Economics

15

BTAX IRR SENSITIVITIES

•

Horizontal drilling improves recoveries and

returns

•

Multiple, stacked horizontal targets

•

7,000’+ lateral length

•

~80% of EUR made up of oil and NGLs

•

2 horizontal rigs running in Project Pangea /

Pangea West

•

Improving IPs and liquids ratio driving higher

returns

•

Recent well results range from 634 BOEPD to

1,310 BOEPD, made up of 84% to 97% liquids

•

875 BOEPD initial IP for Univ. 45 A 703H, made up of

85% oil and 93% total liquids

•

612 BOEPD and 539 BOEPD average 30-day and

60-day rates, respectively, for Univ. 45 A 703H

Notes: Potential locations based on 1,000-feet spacing between each horizontal

well. Economics assume NYMEX gas strip 2/2012 and NGL price based on 50% WTI

oil price. 0

10

20

30

40

50

60

350

400

450

500

550

Well EUR (MBoe)

$100 / bbl

$90 / bbl

$80 / bbl

$70 / bbl

Play Type

Horizontal

Wolfcamp

Avg. EUR

450 MBoe

Targeted Well Cost

$5.5 MM

Potential Locations

500

Gross Resource

Potential

225 MMBoe |

Recent Well Results

16

Note: IP mix based on 24 hr.-IP rates.

IP

MIX

–

LAST

10

HZ

B

WELLS

24 HR.-

IP –

LAST 10 HZ B WELLS

Completion

date

Well name

IP

(Boe/d)

Oil

(Bbl/d)

NGL

(Bbl/d)

Gas

(Mcfe/d)

IP %

Liquids

No. of

stages

Lateral

length

(ft.)

B Bench:

May 2012

University 45 A #703H

875

743

73

354

93%

29

7,672

Mar 2012

University 45 F #2304H

1,111

840

150

729

89%

28

7,641

Mar 2012

University 45 F #2303H

634

481

84

412

89%

30

7,999

Feb 2012

University 45 C #805H

676

441

130

632

84%

28

7,849

Feb 2012

University 45 C #804H

892

823

38

185

97%

35

7,811

Dec 2011

University 45 E #1101H

687

632

30

147

96%

35

7,712

Dec 2011

University 45 F #2302H

1,136

986

83

404

94%

28

7,698

Dec 2011

University 45 F #2301H

1,310

1,136

96

467

94%

34

7,749

Sep 2011

University 45 C #803H

1,044

931

57

335

95%

23

7,358

Sep 2011

University 45 B #2401H

811

582

116

677

86%

23

7,613

Sep 2011

University 45 D #902H

798

611

95

552

88%

23

7,770

Jun 2011

University 45 A #701H

694

613

41

237

94%

21

6,859

May 2011

CT G #701H

328

168

81

473

76%

23

7,609

Apr 2011

University 42-21 #1H

316

132

93

543

71%

21

7,037

Mar 2011

CT M #901H

171

51

61

355

65%

15

5,377

A Bench:

Jun 2012

Pangea West #6601H

461

388

40

196

93%

29

7,742

Jun 2012

Pangea West #6602H

494

391

57

278

91%

28

7,828

C Bench:

Nov 2011

University 42 B #1001H

541

324

120

584

82%

28

7,769

HZ WOLFCAMP WELL RESULTS

Boe/d

Average: 918 Boe/d

Average: 82% oil |

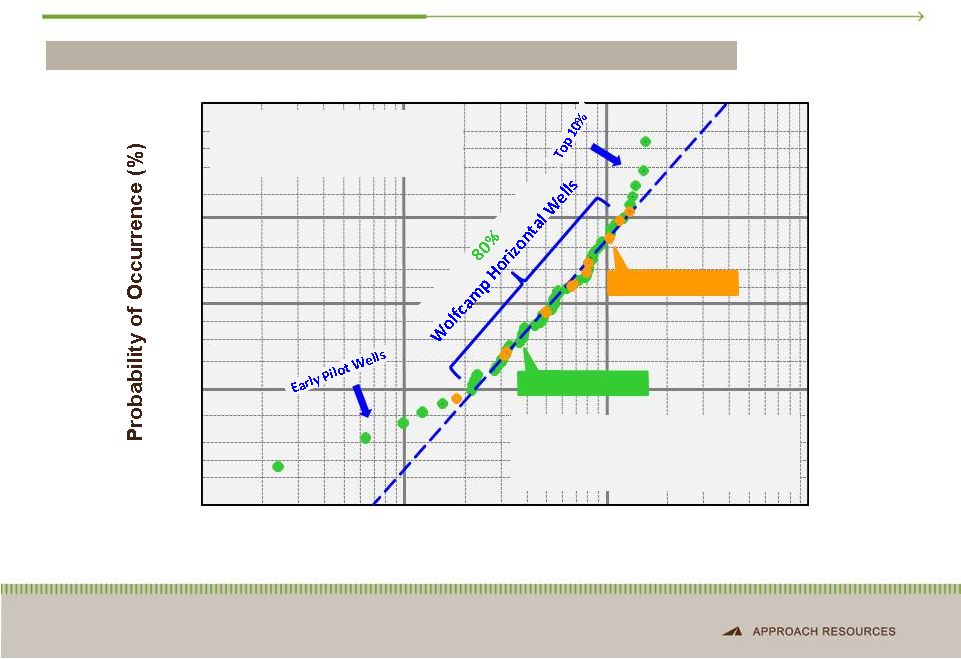

Distribution of IP Rates –

Horizontal Wolfcamp Wells

WOLFCAMP

OIL

SHALE

RESOURCE

PLAY

–

SOUTHERN

MIDLAND

BASIN

17

10%

50%

90%

10.0

100

1,000

10,000

Initial Daily Production Rate (BOEPD)

Industry Wells

AREX Wells

99%

1%

Available Data = 65 HZ Wells

P50 ~ 504 BOEPD

Majority Completed Last 12 Months

Many factors affect IPs, including learning curve, number of frac

stages, fluid type and amount, proppant amount, pumping rate,

lateral landing point and fracture density

Data from public domain and company IR presentations |

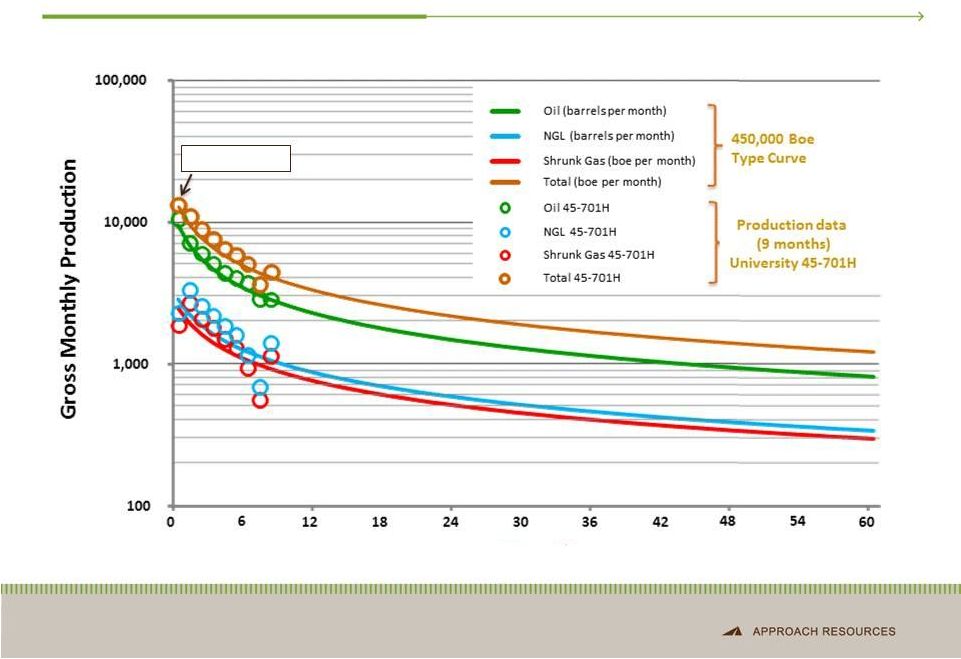

Horizontal Wolfcamp –Type Curve

18

Month

IP 694 BOEPD |

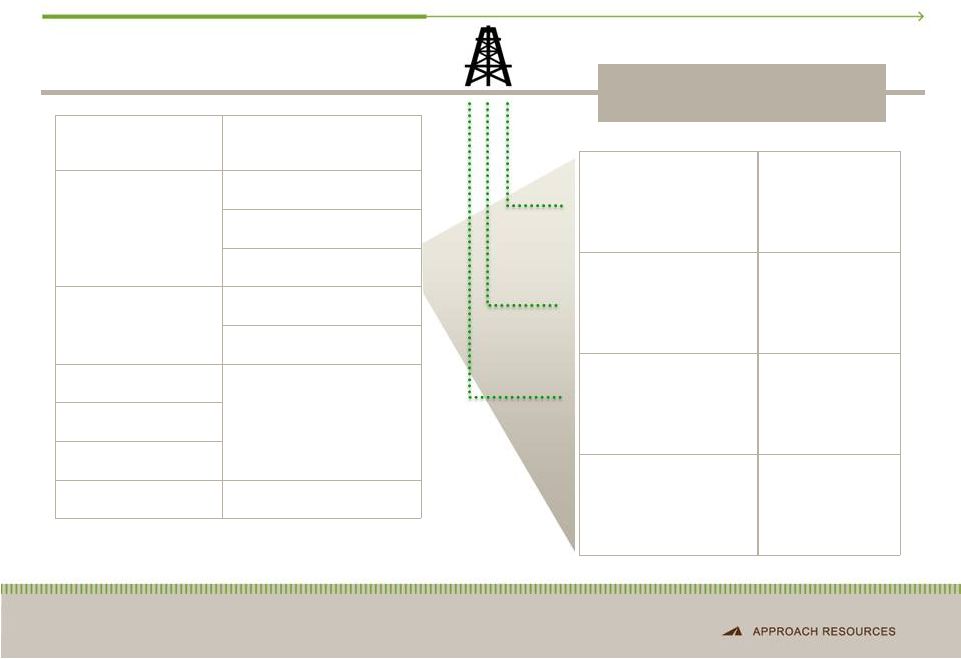

Horizontal Wolfcamp Targets

19

SYSTEM

STRATIGRAPHIC

UNIT

Permian

Clearfork/Spraberry

Dean

Wolfcamp

Pennsylvanian

Canyon

Strawn

Mississippian

Devonian

Silurian

Ordovician

Ellenburger

WOLFCAMP A

WOLFCAMP B

WOLFCAMP C

WOLFCAMP D

Pilot

Transitioning to

Development

Pilot –

Recent

Results

Encouraging

Under Evaluation

POTENTIAL HORIZONTAL

WOLFCAMP TARGETS |

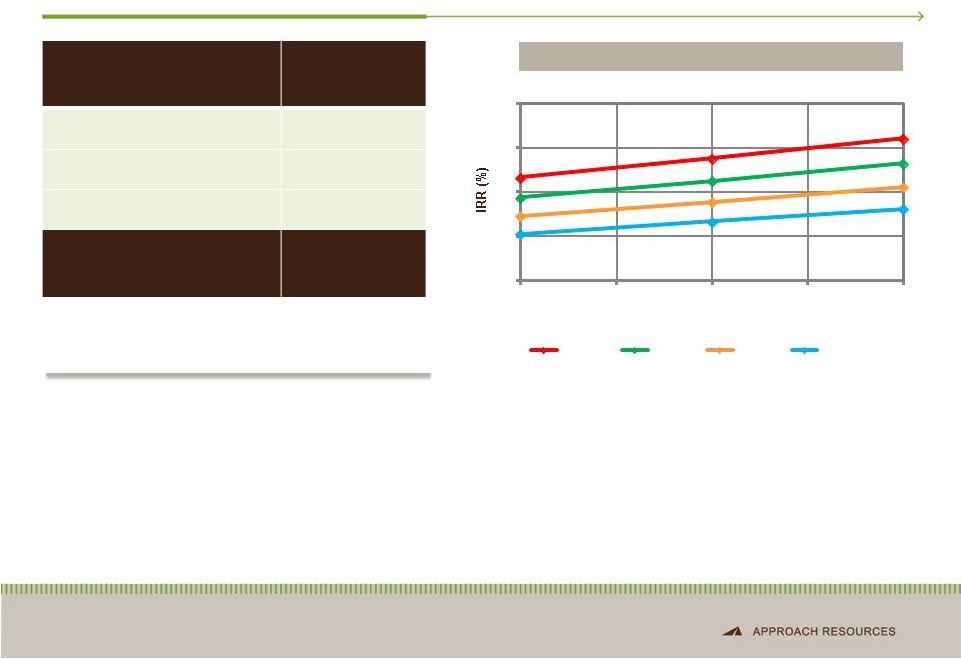

Vertical Clearfork & Wolfcamp (“Wolffork”) Economics

20

BTAX IRR SENSITIVITIES

•

Vertical pilot program in development mode

•

190 BOEPD average IP for 12 recent vertical

Wolffork wells (73% liquids), 5 of which

averaged 300 BOEPD

Notes: Potential locations based on 20-acre spacing. Economics assume

NYMEX gas strip 2/2012 and NGL price based on 50% WTI oil price. 0

10

20

30

40

100

105

110

115

120

Well EUR (MBoe)

$100 / bbl

$90 / bbl

$80 / bbl

$70 / bbl

Play Type

Vertical

Wolffork

Gross Resource

Potential

200+ MMBoe

Avg. EUR

Targeted Well Cost

Potential Locations

110 MBoe

$1.2 MM

1,825 |

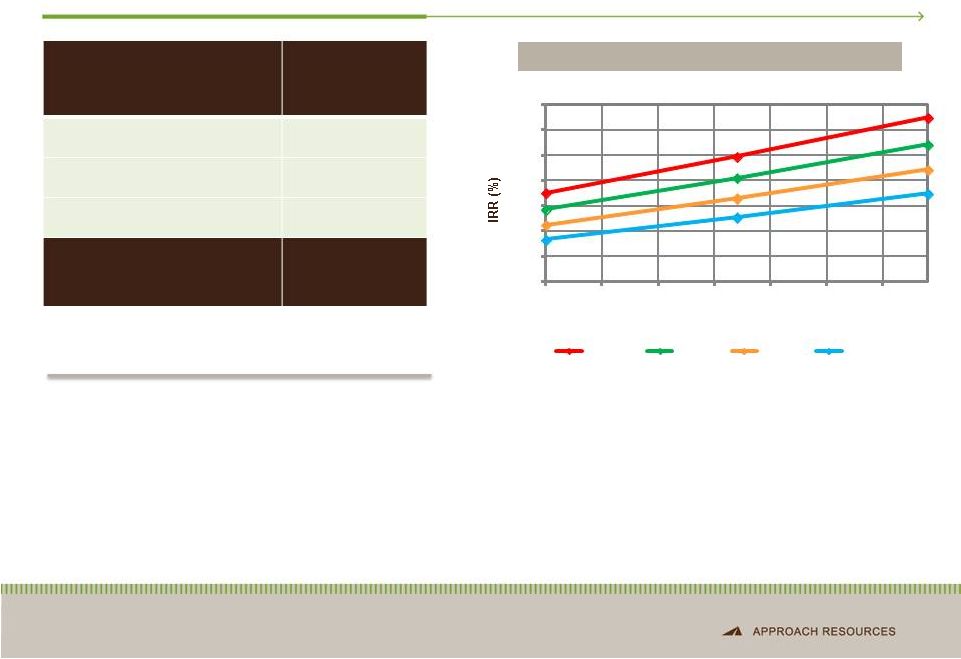

Vertical Wolffork Recompletion Economics

21

BTAX IRR SENSITIVITIES

•

186 BOEPD average IP for 9 recent vertical

Wolffork recompletions (78% liquids)

•

Recent recompletion IPs include 315 and 250

BOEPD IPs from two recompletions,

respectively

Notes: Potential locations based on 20 to 40-acre spacing. Economics

assume NYMEX gas strip 2/2012 and NGL price based on 50% WTI oil price.

0

10

20

30

40

50

60

70

76

81

86

91

96

101

106

Well EUR (MBoe)

$100 / bbl

$90 / bbl

$80 / bbl

$70 / bbl

Play Type

Vertical

Wolffork

Recompletion

Avg. EUR

93 MBoe

Targeted Well Cost

$0.75 MM

Potential Locations

190

Gross Resource

Potential

17+ MMBoe |

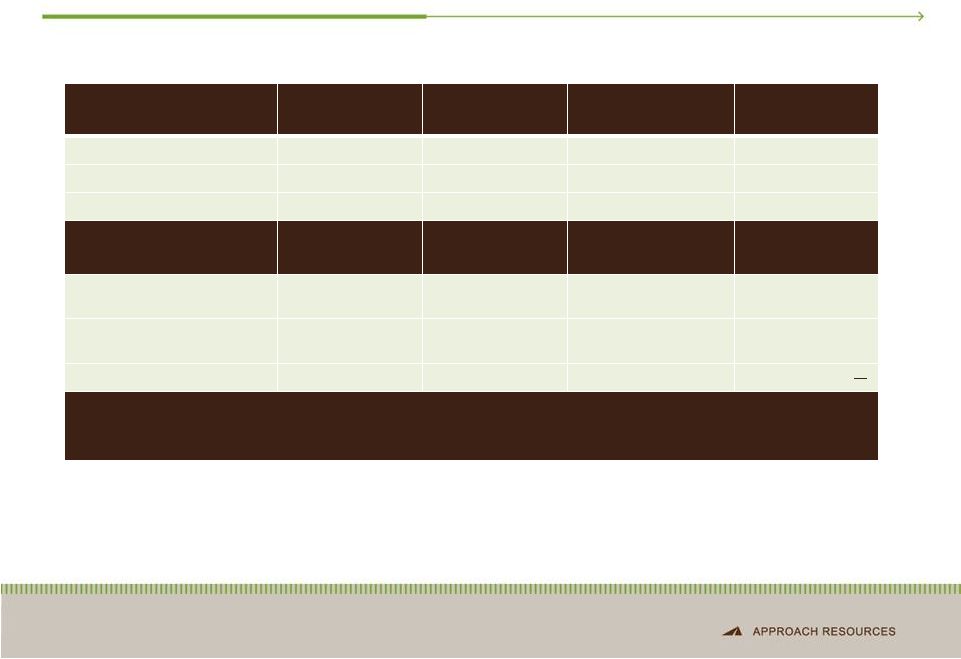

AREX

Drilling Targets & Resource Potential 22

PLAY TYPE

Horizontal

Wolfcamp

Vertical

Wolffork

Vertical Wolffork

Recompletion

Vertical Canyon

Wolffork

EUR (MBoe)

450

110

93

193

Targeted well cost ($MM)

$5.5

$1.2

$0.75

$1.5

Potential locations

500

1,825

190

440

GROSS RESOURCE

POTENTIAL (MMBoe)

225

200+

17+

85

Target

Wolfcamp

Clearfork,

Wolfcamp

Clearfork, Wolfcamp

Canyon, Clearfork,

Wolfcamp

Drilling depth (ft.)

7,000+ (lateral

length)

< 7,500

< 7,500

< 8,500

Activity (# of rigs)

2

1

2 -

4 recompl. / month

500+ MMBoe Total Gross Resource Potential

20+ Years of Drilling Inventory¹

Notes: Potential locations based on 1,000-feet spacing between each horizontal

well for Horizontal Wolfcamp, 20-acre spacing for Vertical Wolffork, 20 to 40-

acre spacing for Vertical Wolffork Recompletion and 40-acre spacing for Vertical

Canyon Wolffork. ¹

Assumes 24 horizontal and 35 vertical wells drilled per year.

|

Creating Value Through Growth

23

•

Concentrated geographic footprint in the Southern Midland Basin

•

Strong growth track record at competitive costs

•

Detailed technical evaluation led to discovery of significant growth

potential in the Wolfcamp / Wolffork oil shale resource play

•

Rigorous pilot program de-risked ~100,000 gross acres

•

Capital discipline for Wolfcamp / Wolffork program acceleration

|

Financial

NON-GAAP RECONCILIATIONS

Framework |

2012

Operating and Financial Guidance 25

2012 GUIDANCE

2012 Guidance

Production

Total (MBoe)

2,900 -

3,100

Percent Oil & NGLs

65%

Operating costs and expenses ($/per Boe)

Lease operating

$

5.50 –

6.50

Severance and production taxes

$

2.50 –

4.00

Exploration

$

4.00 –

5.00

General and administrative

$

7.00 –

8.00

Depletion, depreciation and amortization

$

15.00 –

18.00

Capital expenditures ($MM)

Approximately $260 |

Hedge Position

26

CURRENT HEDGE POSITION

Commodity and Time Period

Type

Volume

Price

Crude Oil

2012

Collar

700 Bbls/d

$85.00/Bbl -

$97.50/Bbl

2012

Collar

500 Bbls/d

$90.00/Bbl -

$106.10/Bbl

September

2012

–

December

2012

Collar

350 Bbls/d

$90.00/Bbl -

$102.30/Bbl

2013

Collar

650 Bbls/d

$90.00/Bbl -

$105.80/Bbl

2013

Collar

450 Bbls/d

$90.00/Bbl -

$101.45/Bbl

2014

Collar

550 Bbls/d

$90.00/Bbl -

$105.50/Bbl

Natural Gas Liquids

Natural

Gasoline

–

February

2012

–

December

2012

Swap

225 Bbls/d

$95.55/Bbl

Normal

Butane

–

March

2012

–

December

2012

Swap

225 Bbls/d

$73.92/Bbl

Natural Gas

2012

Call

230,000 MMBtu/month

$6.00/MMBtu

July 2012 –

December 2012

Swap

360,000 MMBtu/month

$2.70/MMBtu

•

Recently increased crude oil derivatives positions in 2012 (collar covering 350

Bbls/d) and 2013 (collar covering 450 Bbls/d):

|

Financial Strength

27

Liquidity

(unaudited)

is

calculated

by

adding

the

net

funds

available

under

our

revolving

credit

facility

and

cash

and

cash

equivalents.

We

use

liquidity as an indicator of the Company’s ability to fund development and

exploration activities. Liquidity has limitations, and can vary from year

to year for the Company and can vary among companies based on what is or is not

included in the measurement on a company’s financial statements.

Liquidity is provided in addition to, and not as an alternative for, and should be read in conjunction with, the information contained in

our financial statements prepared in accordance with GAAP (including the notes),

included in our SEC filings and posted on our website. The table below

summarizes our liquidity at June 30, 2012 (in thousands). Liquidity

(unaudited) June 30, 2012

Borrowing base

$

270,000

Cash and cash equivalents

402

Long-term debt

(145,400)

Unused letters of credit

(350)

Liquidity

$

124,652

Long-term

debt-to-capital

ratio

(unaudited)

is

calculated

as

of

June

30,

2012,

and

by

dividing

long-term

debt

(GAAP)

by

the

sum

of

total

stockholders’

equity (GAAP) and long-term debt (GAAP). We use the long-term

debt-to-capital ratio as a measurement of our overall financial

leverage. However, this ratio has limitations. This ratio can vary from

year-to-year for the Company and can vary among companies based on

what is or is not included in the ratio on a company’s financial statements.

This ratio is provided in addition to, and not as an alternative for, and

should be read in conjunction with, the information contained in

our financial statements prepared in accordance with GAAP (including the notes),

included in our SEC filings and posted on our website. The table below

summarizes our long-term debt-to-capital ratio at June 30, 2012 (in

thousands).

Long-term debt-to-capital (unaudited)

June 30, 2012

Long-term debt

$

145,400

Total stockholders’

equity

480,333

625,733

Long-term debt-to-capital

23.2% |

Contact

Information

MEGAN P. HAYS

Manager, Investor Relations & Corporate Communications

817.989.9000 x 2108

mhays@approachresources.com

www.approachresources.com |