Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - TIAA FSB Holdings, Inc. | d395019d8k.htm |

EverBank Financial Corp

Raymond James Bank Conference

August 14, 2012

Exhibit 99.1 |

Disclaimer

THIS PRESENTATION HAS BEEN PREPARED BY EVERBANK FINANCIAL CORP ("EVERBANK"

OR THE “COMPANY”) SOLELY FOR INFORMATIONAL PURPOSES BASED ON ITS

OWN INFORMATION, AS WELL AS INFORMATION FROM PUBLIC SOURCES. THIS PRESENTATION HAS BEEN PREPARED

TO ASSIST INTERESTED PARTIES IN MAKING THEIR OWN EVALUATION OF EVERBANK AND DOES

NOT PURPORT TO CONTAIN ALL OF THE INFORMATION THAT MAY BE RELEVANT. IN

ALL CASES, INTERESTED PARTIES SHOULD CONDUCT THEIR OWN INVESTIGATION AND ANALYSIS OF

EVERBANK AND THE DATA SET FORTH IN THIS PRESENTATION AND OTHER INFORMATION PROVIDED

BY OR ON BEHALF OF EVERBANK. EXCEPT AS OTHERWISE INDICATED, THIS

PRESENTATION SPEAKS AS OF THE DATE HEREOF. THE DELIVERY OF THIS PRESENTATION SHALL NOT,

UNDER ANY CIRCUMSTANCES, CREATE ANY IMPLICATION THAT THERE HAS BEEN NO CHANGE IN

THE AFFAIRS OF THE COMPANY AFTER THE DATE HEREOF.

CERTAIN OF THE INFORMATION CONTAINED HEREIN MAY BE DERIVED FROM INFORMATION

PROVIDED BY INDUSTRY SOURCES. EVERBANK BELIEVES THAT SUCH INFORMATION

IS ACCURATE AND THAT THE SOURCES FROM WHICH IT HAS BEEN OBTAINED ARE RELIABLE. EVERBANK

CANNOT GUARANTEE THE ACCURACY OF SUCH INFORMATION, HOWEVER, AND HAS NOT

INDEPENDENTLY VERIFIED SUCH INFORMATION. THIS PRESENTATION MAY CONTAIN

CERTAIN FORWARD-LOOKING STATEMENTS AS DEFINED IN THE PRIVATE SECURITIES LITIGATION REFORM

ACT

OF

1995.

WORDS

SUCH

AS

“OUTLOOK,”

“BELIEVES,”

“EXPECTS,”

“POTENTIAL,”

“CONTINUES,”

“MAY,”

“WILL,”

“COULD,”

“SHOULD,”

“SEEKS,”

“APPROXIMATELY,”

“PREDICTS,”

“INTENDS,”

“PLANS,”

“ESTIMATES,”

“ANTICIPATES”

OR THE NEGATIVE VERSION OF THOSE WORDS OR OTHER

COMPARABLE WORDS ARE INTENDED TO IDENTIFY FORWARD-LOOKING STATEMENTS BUT ARE

NOT THE EXCLUSIVE MEANS OF IDENTIFYING SUCH STATEMENTS. THESE

FORWARD-LOOKING STATEMENTS ARE NOT HISTORICAL FACTS, AND ARE BASED ON CURRENT EXPECTATIONS,

ESTIMATES AND PROJECTIONS ABOUT THE COMPANY’S INDUSTRY, MANAGEMENT’S

BELIEFS AND CERTAIN ASSUMPTIONS MADE BY MANAGEMENT, MANY OF WHICH, BY THEIR

NATURE, ARE INHERENTLY UNCERTAIN AND BEYOND THE COMPANY’S CONTROL. ACCORDINGLY, YOU

ARE CAUTIONED THAT ANY SUCH FORWARD-LOOKING STATEMENTS ARE NOT GUARANTEES OF

FUTURE PERFORMANCE AND ARE SUBJECT TO CERTAIN RISKS, UNCERTAINTIES AND

ASSUMPTIONS THAT ARE DIFFICULT TO PREDICT. ALTHOUGH THE COMPANY BELIEVES THAT THE

EXPECTATIONS REFLECTED IN SUCH FORWARD-LOOKING STATEMENTS ARE REASONABLE AS OF

THE DATE MADE, EXPECTATIONS MAY PROVE TO HAVE BEEN MATERIALLY DIFFERENT FROM

THE RESULTS EXPRESSED OR IMPLIED BY SUCH FORWARD-LOOKING STATEMENTS. UNLESS

OTHERWISE REQUIRED BY LAW, EVERBANK ALSO DISCLAIMS ANY OBLIGATION TO UPDATE ITS

VIEW OF ANY SUCH RISKS OR UNCERTAINTIES OR TO ANNOUNCE PUBLICLY THE RESULT

OF ANY REVISIONS TO THE FORWARD-LOOKING STATEMENTS MADE IN THIS PRESENTATION. INTERESTED

PARTIES SHOULD NOT PLACE UNDUE RELIANCE ON ANY FORWARD-LOOKING STATEMENT AND

SHOULD CONSIDER THE UNCERTAINTIES AND RISKS DISCUSSED UNDER ITEM 1A.

“RISK FACTORS” OF EVERBANK’S QUARTERLY REPORT ON FORM

10-Q AND IN ANY OF EVERBANK’S SUBSEQUENT FILINGS WITH THE

SECURITIES AND EXCHANGE COMMISSION. 2 |

Company Overview |

EverBank Overview

Strong Returns

High Growth

Low Risk

Acquired in 1994

and headquartered

in Jacksonville, FL

$15.0bn in assets,

$10.8bn in deposits &

$1.2bn shareholders’

equity as of June 30,

2012

Initial public offering on

May 3, 2012

$1.4bn market

capitalization

(1)

Nationwide banking

franchise

Unique, diversified

business model

Robust asset

generation

capabilities

Scalable, low cost

deposit platform

Disciplined risk

management

Cohesive, long

tenured management

team

(1) Market capitalization as of 8.8.2012 close

4 |

Pending Acquisition of GE Capital’s Business Property Lending

Acquired MetLife Bank’s warehouse finance business

Completion of Initial Public Offering

Acquired online

deposit franchise

2000

-

2003

Mortgage Lending

and Servicing

2004

-

2007

Expansion of

Deposit Strategy

2008

-

2012

Addition of Diversified

Asset Generation

Evolution and Growth

Adopted EverBank name

Acquired NetBank mortgage assets

Growth capital infusion

Acquired Tygris

FDIC-Assisted Acquisition of Bank of Florida

$ 16.9

Pro Forma for Pending

BPL Acquisition

5 |

Best

of Both Online and Branch Banking Models Strong Asset Generation

Quality Deposit Mix

High Customer Retention

Geographic Diversity

Low

“Fully-Loaded”

Expenses

Ability to Quickly Scale

EverBank

Online Banks

Regional

Branch Banks

6 |

7

EverBank’s Business Strategy

San Francisco Area

Los Angeles Area

Houston, TX

Denver, CO

Dallas, TX

Atlanta, GA

St Louis, MO

Direct Bank

Chicago, IL

Branch

Presence

Jacksonville, FL

Northern VA

-

Loan Production Office

-

Business Headquarters

-

Corporate Headquarters

Bethesda, MD

Deliver high value products and

services to self-directed customers

through a variety of channels

Target mass affluent and small business

segments

Key wealth markets nationwide

Continue integrating core product

offering

Deposits

Jumbo lending

Commercial finance

Commercial lending

Expand long-term into complimentary

product lines

Brokerage

Wealth management

Parsippany, NJ

ECF

EVER Deposits

EVER Lending

EVER Deposits & Lending

Strategic Plan

Deposits and Lending by County / Business Locations

7

Deposits

Residential

Lending

Commercial

Finance

Commercial

Lending

Brokerage

Services

Wealth

Management

Developed

In Development |

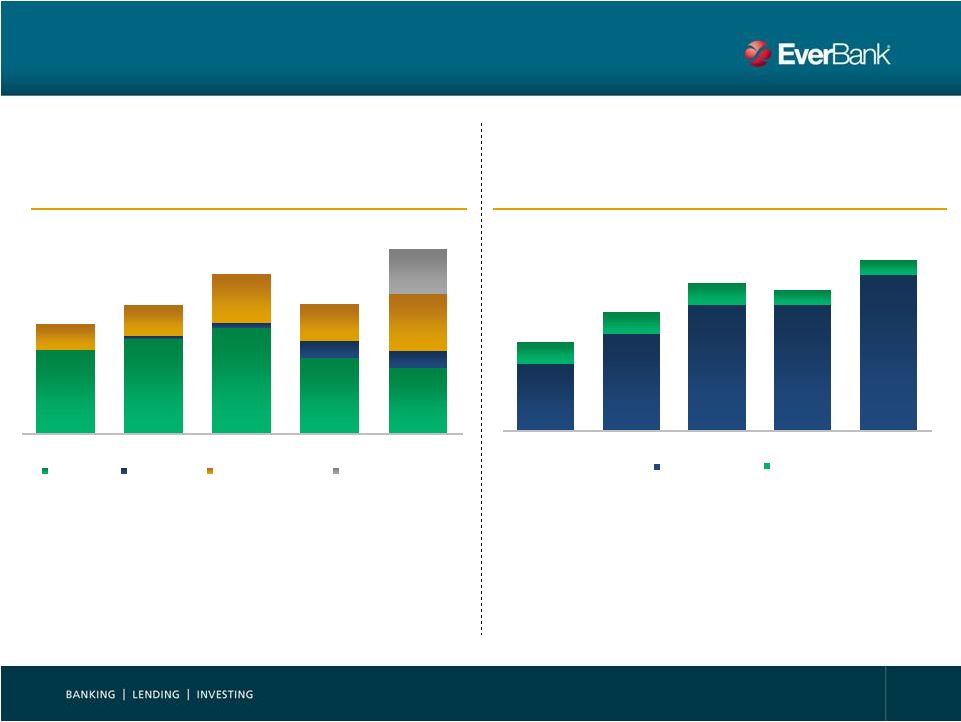

Diversified Asset Generation

Retained Asset Generation ($mm)

Mortgage Production Volume ($bn)

422

495

617

501

714

1.2

1.6

2.0

1.9

2.3

Secondary

Retained

8

76%

74%

66%

58%

35%

2%

3%

13%

9%

24%

24%

31%

29%

31%

25%

2Q11

3Q11

4Q11

1Q12

2Q12

Residential

Commercial

Commercial finance

Warehouse finance

0.9

1.3

1.7

1.7

2.1

0.3

0.3

0.3

0.2

0.2

2Q11

3Q11

4Q11

1Q12

2Q12 |

9

Retained Asset Generation

(1)

Represents Q2 2012 annualized

(2)

Key transaction assumption

Pending BPL Acquisition Enhances Asset Generation

Diversifies and expands existing asset generation capabilities

$2.9bn

$0.5bn

$3.4bn

(2)

(1) |

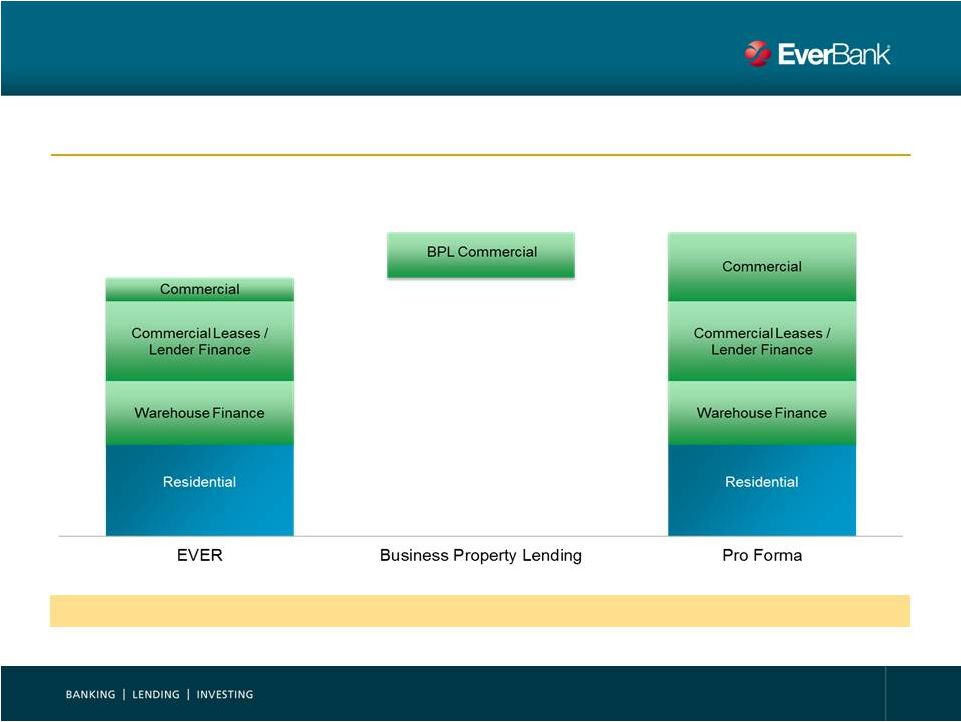

10

Transaction increases commercial loan concentration from 23% to 37%

Residential

Commercial

Pending BPL Acquisition Diversifies Loan Portfolio

Pro Forma

EVER

Business Property Lending

Total: $10.9bn

Total: $2.4bn

Total: $13.3bn |

11

Source: AlixPartners study

(1)

Percentage of U.S. households who used branch banking channel within the last

year Online and Mobile Banking Trends

Online

banking

channel

market

share

has

grown

to

43%

vs.

a

decline

to

62%

for

branch

banking

Bank Channel Usage as a % of U.S. Households

91%

19%

Branch Banking

(1)

Mobile Banking

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

11

Online Banking |

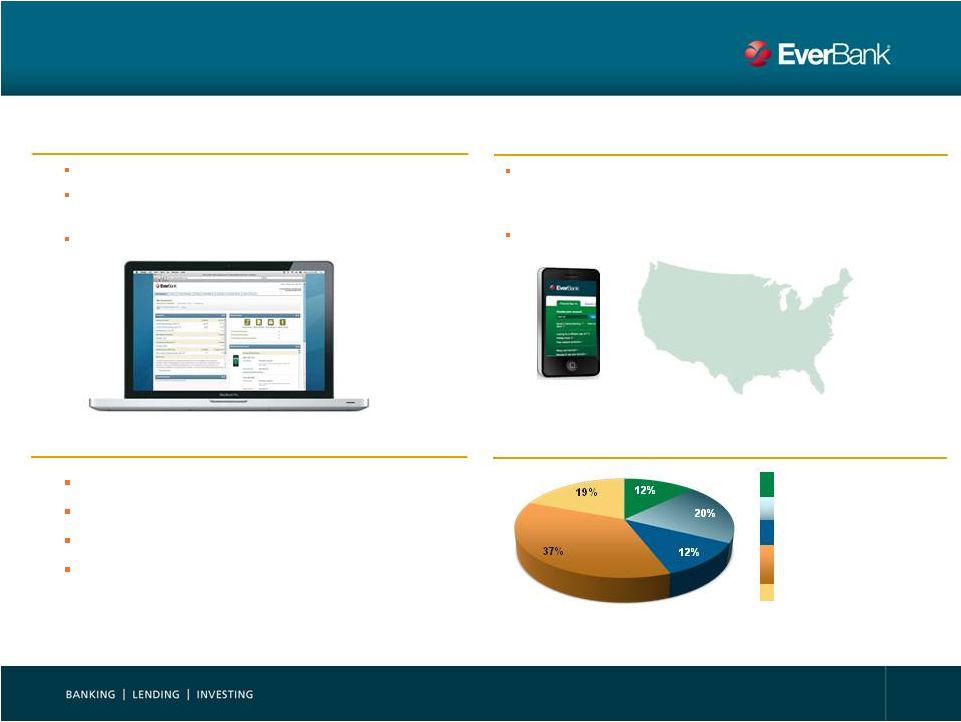

Value Proposition Yields

Attractive Customer Base Internal and external account aggregation

Analysis and reporting across financial life: investing,

spending, budgeting, tracking alerts

Bill pay and electronic transfers

Mobile, Online, 24 Hour Phone Support, No Fee ATM,

Imaging / Remote Deposit, Direct Deposit, Select

Financial Centers, Mail

ATM fee rebates

474,000 ATMs

Noninterest-bearing

Checking

MMDA & Savings

Global Market

Time Deposits

111,178 households, 222,763 accounts

Average deposits per household: $78,283

54% household income > $75,000

46%

household

net

worth

(1)

>

$250,000

(1)

Based on reported household net worth; excludes 17% of households that do not report household net

worth One Stop, Integrated Financial Portal

Convenient Access: 24 x 365

Attractive Nationwide Customer Base

2Q12 Deposit Composition

12 |

(1)

Based

on

Bank

of

America’s

Deposit

Banking

segment

2011

average

Non-Interest

Expense

to

Average

Deposits;

NIE

reduced

by

15

bps

for

estimated

agency

fees

(2)

Non-interest expense from direct and retail banking operations, excluding agency fees and corporate

overhead allocation costs (3)

Calculated

as

annual

deposit

interest

expense

divided

by

average

balance

of

deposits;

includes

non-interest

bearing

deposits

(4)

Aggregate FDIC financial information

Low All-In Cost of Deposits

Deposit Interest Expense

(3)

Non-Interest Expense as a % of

Deposits

“All-in”

Cost of Deposits

13 |

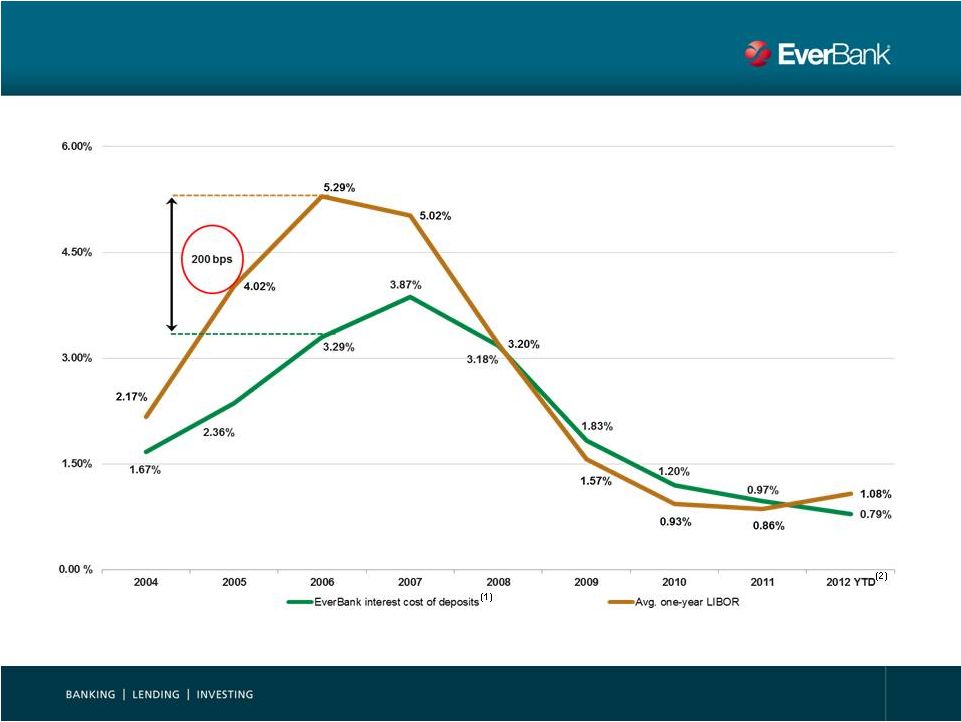

Deposit Pricing Lags in Rising Rate Environment

(1)

Calculated

as

annual

deposit

interest

expense

divided

by

average

balance

of

deposits;

includes

non-interest

bearing

deposits;

YTD

(2)

EverBank interest cost of deposits for year to date June 30, 2012; Average

one-year LIBOR represents the average of December 31, 2011, March, 31, 2012 and June 30, 2012

14 |

15

Strong, Stable Deposit Base

(1)

Compound

annual

retention

rate

for

balances

of

non-CD

bank

accounts

existing

at

June

30,

2012,

calculated

from

initial

year

end

to

June

30,

2012

(2)

Average account balance for non-CD bank accounts existing at each point in time,

shown from initial year end to June 30, 2012 Compound

Annual

Retention

Rate

(1)

Average

Balance

of

Accounts

Existing

at

Each

Period

(2)

Vintage

High Customer Deposit Retention

Loyal Customers with Growing Balances

98%

97%

97%

96%

2004

2005

2006

2007

$10,000

$20,000

$30,000

$40,000

$50,000

2005

2006

2007

2008

2009

2010

2011

2012

YTD

2005

2006

2007

2008

2009

2010

2011

15 |

16

History of Attractive Acquisitions

Business Property Lending

$2.4bn assets

$3.1bn servicing rights

Warehouse Finance

$351mm assets

$1.4bn assets

$1.2bn deposits

$780mm assets

$425mm growth capital

$340mm deposits

Size

(1)

Target

(1)

Net of any purchase accounting adjustments, figures are rounded

Disciplined approach has yielded attractive strategic and growth acquisitions |

Pending Acquisition of Business Property Lending, Inc.

Business Acquired

Business Property Lending division from GE Capital

Provides loans on essential use properties owned or leased by small

and mid-sized companies

Includes commercial loan origination and servicing business

$2.44bn of high-quality top performing loans

Servicing rights on additional $3.1bn of securitized business loans

108 employees, including senior management team

Purchase Price

$2.51bn cash for the stock of a subsidiary of GE Capital, includes

$70.5mm premium and generates $40mm goodwill

Required Approvals

Regulatory and other customary approvals

Expected Closing Date

Fourth Quarter 2012

Attractive Deal

Economics

Immediately accretive to EPS

(low double digit %)

Accretive to ROE by ~100bps

Minimal impact on TBV

Low Risk

High quality loan portfolio

Turn-key platform

Strong pro forma capital and

liquidity

17

Strategic Value

Accelerates strategic growth plan

Diversifies balance sheet

Complements distribution in key

markets |

Second Quarter 2012 Results |

Adjusted

Earnings

Per

Share

(1)

Financial Highlights

(1)

Represents

adjusted

diluted

earnings

per

common

share

from

continuing

operations

for

2007-YTD;

2003-2006

represents

adjusted

basic

earnings

per

common

share

from

continuing

operations.

Calculated

using

adjusted

net

income

attributable

to

the

Company

from

continuing

operations;

2012

adjusted

EPS

calculation

includes

$4.5mm

and

$1.1mm

cash

dividends

paid

to

Series

A

and

Series

B

Preferred

shareholders in Q1 and Q2, respectively; a reconciliation of non-GAAP financial

measures can be found in the appendix (2)

Q2 YTD adjusted return on average equity for banks $5-25bn in assets represents

annualized Q1 metric; Q2 YTD metrics unavailable Adjusted

Return

on

Average

Equity

(2)

2Q12 Capital Ratios

Tangible Book Value Per Share

19 |

20

Key

Highlights

–

2Q12

Note: A reconciliation of non-GAAP financial measures can be found in the

appendix Earnings

Execution of

Strategic Goals

$714mm retained organic asset generation

Total loans up $1.1bn, or 11%, LQ to $10.9bn

Deposits up $0.3bn, or 2%, LQ to $10.8bn

Core NIM up 1bp LQ to 3.53% (Reported NIM of 3.86%)

Closed acquisition of warehouse finance business from MetLife

Completed Initial Public Offering

Executed definitive agreements to acquire Business Property

Lending from GE Capital

Adjusted EPS of $0.33, up 18% linked quarter (LQ)

GAAP EPS of $0.09, up 13% LQ

Balance Sheet

and NIM Growth

Solid Capital

Ratios

Improving Credit

Quality

TCE / TA: 7.8%

Tier 1 leverage (bank): 8.3%

Total risk-based (bank): 15.8%

Adjusted non-performing assets were 1.46% of total assets, down 17bps

LQ

Net charge-offs were 0.34% of average loans held for investment, down

31bps LQ |

Stock

Price Performance Note:

Peer

group

consists

of

AF,BOH,

BOKF,

CYN,

FHN,

FRC,

HBHC,

HCBK,

IBKC,

NYB,

SBNY

and

VLY

EVER Return Since IPO

80

85

90

95

100

105

110

115

120

125

5/2

5/9

5/16

5/23

5/30

6/6

6/13

6/20

6/27

7/4

7/11

7/18

7/25

8/1

8/8

EVER

Peer Avg

KRE

19.7%

(5.0)%

(2.3)%

21 |

Why

Invest in EverBank High-performing,

strong-growth,

low-risk national

bank franchise

Robust asset

generation

capabilities coupled

with attractive, low-

cost deposit engine

Ability to achieve

earnings growth in a

variety of economic

cycles

Proven ability to

capitalize on market

opportunities

Scalable operating

platforms and

distribution channels

Management team

with long-term track

record of success

22 |

Appendix |

Loans

Strong Returns

High Growth

Low Risk

End of Period Loans ($mm)

End of period loans up $1.1bn, or 11%, LQ and

$3.3bn, or 44%, YoY

Residential loans up 5% LQ and 40% YoY

Commercial loans up 49% LQ and 63% YoY

Lease financing receivables up 12% LQ and 43% YoY

Loan growth driven by strong organic origination activity

in all asset classes and the closing of warehouse

finance acquisition

Loan yield on average loans HFI of 5.11% down 34

bps linked quarter

Decrease in excess accretion and addition of short-

term, variable rate warehouse finance loans

Loans HFI Composition ($mm)

6,767

6,198

6,442

7,245

7,708

Quarter Highlights

7,559

7,990

9,167

9,776

10,887

2Q11

3Q11

4Q11

1Q12

2Q12

Residential

Commercial

Commercial Finance

Warehouse Finance

2Q11

3Q11

4Q11

1Q12

2Q12

Loans HFI

Loans HFS

Average Loan HFI Yield

24 |

8,910

9,029

8,956

9,139

9,214

915

1,127

1,455

1,305

1,463

1.04%

0.94%

0.82%

0.81%

0.77%

2Q11

3Q11

4Q11

1Q12

2Q12

Interest-bearing

Noninterest-bearing

Cost of deposits

Deposits

Strong Returns

High Growth

Low Risk

Average Deposits and Rates ($mm)

Average deposits up $232.6mm, or 2%, LQ and

$850.9mm, or 9%, YoY

Noninterest-bearing deposits up 12% LQ and 60% YoY

Checking deposits up 1% LQ and 4% YoY

Global market deposits down 3% LQ and 4% YoY

MMDA & savings deposits up 2% LQ and 6% YoY

Time deposits down 1% LQ and up 1% YoY

Cost of deposits declined 4 bps linked quarter and

27 bps year over year to 0.77%

Over 70% of CD book will mature in the next 12 months

9,825

10,156

10,411

10,443

10,676

Quarter Highlights

Note: Cost of deposits shown above represents interest expense paid on deposits over

average total deposits 13%

25 |

26

113

111

115

116

125

2Q11

3Q11

4Q11

1Q12

2Q12

4.22%

3.98%

3.94%

3.97%

3.86%

Net Interest Income

Net Interest Income ($mm)

Net interest income up $9.4mm, or 8%, LQ and

$12.1mm, or 11%, YoY

Average interest earning assets up 11% LQ and

22% YoY

Reported NIM declined 11 bps LQ and 36 bps YoY

to 3.86%

Core NIM rose 1 bp LQ to 3.53%

Core NIM

Quarter Highlights

Net Interest Income

Net Interest Margin

($mm)

4Q11

1Q12

2Q12

Average interest-earning assets

11,571

$

11,707

$

13,025

$

Net interest income

115

$

116

$

125

$

Reported NIM

3.94%

3.97%

3.86%

Net interest income

115

$

116

$

125

$

Less: Discount accretion from

Tygris acquisition

15

13

11

Adjusted net interest income

100

$

102

$

114

$

Core NIM

3.43%

3.52%

3.53% |

27

Banking and Wealth Management

Net interest income up $8.3mm, or 8%, LQ and

$9.7mm, or 9%, YoY due to loan growth

Provision for loan and lease losses down $5.3mm,

or 51%, LQ and $3.2mm, or 39% YoY due to credit

quality improvement

Credit-related expenses increased due to elevated

foreclosure activity related to our GNMA pool buyout

loans

Segment Earnings

Segment Highlights

($mm)

2Q11

1Q12

2Q12

Net interest income

105

$

107

$

115

$

Provision for loan and lease losses

(8)

(10)

(5)

Net interest income after provision

97

96

110

Noninterest income

16

25

26

Noninterest expense:

Credit-related expenses

6

8

14

All other noninterest expense

40

52

62

Pre-tax income

66

$

62

$

60

$

Adjustment items (pre-tax)

3

3

1

Adjusted pre-tax income

69

$

65

$

61

$ |

28

Mortgage Banking

Net interest income up $1.3mm, or 12%, LQ and

$2.3mm, or 24%, YoY

Noninterest income increased $11.3mm, or 30%,

YoY as a result of increased gain on sale activity

due to increased origination activity

Continued high volume of originations due to

historically low rates and HARP 2.0

Other credit-related expenses were down $7.8mm,

or 65%, LQ and $3.7mm, or 47%, YoY reflecting

positive credit trends

Segment Earnings

Segment Highlights

Key Metrics

($mm)

2Q11

1Q12

2Q12

Net interest income after provision

9

$

9

$

11

$

Noninterest income

37

48

49

Noninterest expense:

Foreclosure and OREO expense

4

3

3

Other credit-related expenses

8

12

4

All other noninterest expense

36

57

61

Pre-tax income (loss)

(2)

$

(15)

$

(8)

$

Adjustment items (pre-tax):

-

15

30

1

5

5

Adjusted pre-tax income (loss)

(1)

$

5

$

28

$

Increase in MSR valuation allowance

Transaction and non-recurring

regulatory related expense

2Q11

1Q12

2Q12

Mortgage lending volume

$1.2bn

$1.9bn

$2.3bn

Gain on sale margin

49bps

197bps

261bps

Servicing UPB

$56.9bn

$53.6bn

$53.3bn

Average servicing fee

31bps

31bps

30bps |

29

Corporate Services

GAAP loss of $34.4mm, up $5.7mm, or 20%, LQ

Adjusted loss of $29.9mm, up $2.8mm, or 10%, LQ

Noninterest expense increased due to regulatory,

infrastructure investments and Business Property

Lending diligence expenses

Segment Earnings

Segment Highlights

($mm)

2Q11

1Q12

2Q12

Net interest income

(2)

$

(1)

$

(2)

$

Noninterest expense

28

27

33

Pre-tax income (loss)

(29)

$

(29)

$

(34)

$

Adjustment items (pre-tax):

2

2

4

Adjusted pre-tax income

(27)

$

(27)

$

(30)

$

Memo:

FTE

480

520

541

Total Assets

(1)

/ FTE

26.1

$

26.5

$

27.8

$

Transaction and non-recurring

regulatory related expense

(1)

Ratio represents total company assets per Corporate Services FTE

|

Adjusted NPA / Total Assets

Note: A reconciliation of Non-GAAP financial measures can be found in the

appendix (1)

Tygris and Bank of Florida purchase-impaired loans and leases accounted for

under ASC 310-30 or by analogy Asset Quality

Adjusted NPA ratio

excludes loans and

leases with

enhanced credit

protection

(1)

Adjusted NPA / Total Assets Build

Highlights

NCO / Average Loans HFI

Adjusted non-performing assets to total assets

declined 17 bps LQ resulting from a $4.9mm, or

2.9%, decrease in non-performing loans

Net charge-offs to average loans HFI decreased 31

bps LQ to 0.34%

Allowance for loan and lease losses decreased

$0.9mm, or 1.1%, LQ as charge-offs of $6.6mm

exceeded provisions of $5.8mm

1.35%

1.46%

1.02%

0.65%

0.34%

2.73%

2.11%

1.86%

1.63%

1.46%

13.49%

(10.96)%

Regulatory NPAs /

Assets

Impact Ex. Govt

Insured Loans

Adjusted NPAs /

Assets

2009

2010

2011

1Q12

2Q12

2009

2010

2011

1Q12

2Q12

Impact Ex. Tygris

and Bank of

Florida

1.46%

(1.07)%

30 |

31

Mortgage Banking Drivers

Revenue vs. Amortization and Valuation

Allowance ($mm)

Summary

Current low interest rate environment generates

positive long-term net economic value for our

mortgage business

June 30, 2012 mortgage servicing rights carrying

value reflects the significant decline in mortgage

rates at the end of the second quarter and the

success of the government’s HARP initiatives

An increase in expected refinance activity will

generate residential lending revenues over time,

while the non-cash MSR valuation allowance is

recorded immediately; we believe the residential

lending revenues will more than offset the increase

in prepayments

Amortization rate of 27% closely approximates the

actual payoff activity in the underlying portfolio of

approximately 24%

Valuation allowance is recoverable if rates rise and

refinance activity slows

Servicing fee income

Loan production and gain on sale income

Amortization

Addition to MSR valuation allowance

(23)

(28)

(29)

(34)

(21)

(19)

(15)

(30)

48

45

46

42

27

41

56

80

3Q11

4Q11

1Q12

2Q12 |

32

'04 - '05

'06 - '08

'09 - '12

Total

$2,357

$450

$18,241

$21,048

8,977

11,528

3,134

23,639

$11,334

$11,978

$21,374

$44,686

0.34%

1.89%

0.32%

0.77%

0.05%

0.57%

0.18%

0.26%

41%

40%

27%

37%

15%

21%

25%

23%

9%

45%

22%

35%

25%

50%

31%

44%

Life Time

Last 12 Months

Life Time

Last 12 Months

Loss Severity

Last 12 Months

Repurchase Rates

Request Rates

Life Time

Sold UPB ($mm)

Agency

Agency Aggregator

Total Sold UPB

Credit –

Originated Mortgage Repurchase Reserve

Reserve Trends

Summary Statistics by Vintage

Coverage ratio of 3.25 years

LTD realized losses of only 8bps for the whole portfolio and

expected total life-time realized losses of just 16bps

2006

–

2008

quality

of

production

was

strong

2006

–

2008

vintages

were

primarily

sold

to

the

large

agency

aggregators

Highlights

Reserve Rollforward

($mm)

2Q11

3Q11

4Q11

1Q12

2Q12

Pending Reserves -

BoP

$ 32.0

$ 33.2

$ 33.0

$ 32.0

$ 35.0

Provisions -

New Sales

0.5

0.0

0.1

0.4

0.3

Provisions -

Changes in

Existing Reserves

4.9

2.6

1.2

5.8

1.1

Charge Offs

(4.2)

(2.8)

(2.3)

(3.2)

(2.4)

Pending Reserves -

EoP

$ 33.2

$ 33.0

$ 32.0

$ 35.0

$ 34.0

10

11

13

Quarters of Coverage at

Trailing 4 Quarter Realized Loss Rate

Losses to date ($mm)

'04 -

'05

'06 -

'08

'09 -

'12

Total

Total Sold UPB

$11,334

$11,978

$21,374

$44,686

Total Sold Units

51,108

57,421

95,297

203,826

Request Rate

0.34%

1.89%

0.32%

0.77%

Requests Received

173

1,087

309

1,569

Pending Requests

20

251

38

312

Resolved Requests

153

836

271

1,257

Repurchase Rate

41%

40%

27%

37%

Repurchases

63

334

73

469

Average Loan size

221,770

208,597

224,293

219,238

Loss Severity

9%

45%

22%

35%

Losses Recognized

$1.2

$31.5

$3.7

$36.4

Losses Recognized (bps)

1.1

26.3

1.7

8.1 |

33

Annual

Targets

ROE

Net

Income

/

EPS

Growth

(2)

Dividend Payout Ratio

TCE/TA

Total Risk-Based Capital

Ratio

Asset Growth

Intermediate Financial Targets

3-Year Average

Historical Annual

Performance

(1)

Represents CAGR from 2008-2011

(2)

EPS on a diluted basis

(3)

Adjusted earnings and return metrics for continuing operations; a reconciliation of

non-GAAP financial measures can be found in the appendix 9% -

12%

23%

(1)

9% -

12%

66% / 39%

(1)(3)

10% -

13%

12%

(3)

~15%

N/A

7.0% -

7.5%

7.1%

12% -

14%

15.3% |

Non-GAAP Reconciliations

Adjusted Net Income

(1)

No material items gave rise to adjustments prior to the year ended December 31,

2010. Accordingly, for periods presented before the year ended December 31, 2010, we have not reflected

adjustments to net income attributable to the Company from continuing operations

calculated in accordance with GAAP 2Q 2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

GAAP net income from continuing operations

23.0

$

52.7

$

188.9

$

53.5

$

23.4

$

29.7

$

32.6

$

28.2

$

23.7

$

19.0

$

Bargain purchase gain on Tygris transaction

-

-

(68.1)

-

-

-

-

-

-

-

Gain on sale of investment securities due to portfolio repositioning

-

-

(12.3)

-

-

-

-

-

-

-

Gain on repurchase of trust preferred securities

-

(2.9)

(3.6)

-

-

-

-

-

-

-

Transaction and non-recurring regulatory related expense

10.0

16.8

6.0

-

-

-

-

-

-

-

Loss on early extinguishment of acquired debt

-

-

6.4

-

-

-

-

-

-

-

Decrease in fair value of Tygris indemnification asset

-

5.4

13.7

-

-

-

-

-

-

-

Increase in Bank of Florida non-accretable discount

2.6

3.0

3.8

-

-

-

-

-

-

-

Impact of change in ALLL methodology

-

1.2

-

-

-

-

-

-

-

-

Early adoption of TDR guidance and policy change

-

6.2

-

-

-

-

-

-

-

-

MSR impairment

28.1

24.5

-

-

-

-

-

-

-

-

Tax benefit (expense) related to revaluation of Tygris NUBILs

-

0.7

(7.8)

-

-

-

-

-

-

-

Adjusted net income from continuing operations

63.7

$

107.6

$

127.0

$

53.5

$

23.4

$

29.7

$

32.6

$

28.2

$

23.7

$

19.0

$

Three Months Ended

June 30,

March 31,

December 31,

September 30,

June 30,

(dollars in thousands)

2012

2012

2011

2011

2011

Net income

11,172

$

11,846

$

13,760

$

7,758

$

21,795

$

Transaction and non-recurring regulatory related expense, net of tax

6,143

3,884

4,331

4,751

2,136

Increase in Bank of Florida non-accretable discount, net of tax

463

2,135

2,208

298

-

Early adoption of TDR guidance and policy change, net of tax

-

-

-

-

1,561

MSR impairment, net of tax

18,684

9,389

11,638

12,824

-

Adjusted net income

36,462

$

27,254

$

31,937

$

25,631

$

25,492

$

34 |

Non-GAAP Reconciliations

Non-performing Assets (NPA)

June 30,

March 31,

December 31,

December 31,

December 31,

(dollars in thousands)

2012

2012

2011

2010

2009

Total non-accrual loans and leases

168,962

$

170,589

$

193,478

$

213,818

$

194,951

$

Accruing loans 90 days or more past due

1,800

5,119

6,673

1,754

1,362

Total non-performing loans (NPL)

170,762

175,708

200,151

215,592

196,313

Other real estate owned (OREO)

49,248

49,304

42,664

37,450

24,087

Total non-performing assets (NPA)

220,010

225,012

242,815

253,042

220,400

Troubled debt restructurings (TDR) less than 90 days past due

93,184

92,954

92,628

70,173

95,482

Total NPA and TDR

(1)

313,194

$

317,966

$

335,443

$

323,215

$

315,882

$

Total NPA and TDR

313,194

$

317,966

$

335,443

$

323,215

$

315,882

$

Government-insured 90 days or more past due still accruing

1,647,567

1,530,665

1,570,787

553,341

589,842

Bank of Florida loans accounted for under ASC 310-30:

90 days or more past due

140,797

146,379

149,743

195,425

-

OREO

20,379

22,852

19,456

19,166

-

Total regulatory NPA and TDR

2,121,937

$

2,017,862

$

2,075,429

$

1,091,147

$

905,724

$

Adjusted credit quality ratios excluding government-insured loans

and loans accounted for under ASC 310-30:

(1)

NPA to total assets

1.46%

1.63%

1.86%

2.11%

2.73%

Credit quality ratios including government-insured loans and loans

accounted for under ASC 310-30:

NPA to total assets

13.49%

13.97%

15.20%

8.50%

10.05%

(1)

We define non-performing assets, or NPA, as non-accrual loans, accruing

loans past due 90 days or more and foreclosed property. Our NPA calculation excludes government-

insured pool buyout loans for which payment is insured by the government. We

also exclude loans and foreclosed property acquired in the Bank of Florida acquisition accounted

for

under

ASC

310-30

because

as

of

June

30,

2012,

we

expected

to

fully

collect

the

carrying

value

of

such

loans

and

foreclosed

property.

35 |

36

June 30,

(dollars in thousands)

2012

Shareholders' equity

1,181,369

$

Less:

Goodwill

10,238

Intangible assets

6,700

Tangible common equity

1,164,431

$

Less:

Accumulated other comprehensive loss

(113,094)

Adjusted tangible common equity

1,277,525

$

Total assets

15,040,824

$

Less:

Goodwill

10,238

Intangible assets

6,700

Tangible assets

15,023,886

$

June 30,

March 31,

June 30,

(dollars in thousands)

2012

2012

2011

Shareholders' equity

1,263,687

$

1,099,404

$

1,130,104

$

Less:

Goodwill and other intangibles

(16,938)

(17,290)

(18,319)

Disallowed servicing asset

(36,650)

(40,783)

(31,927)

Disallowed deferred tax asset

(70,357)

(71,302)

(74,522)

Add:

Accumulated losses on securities and cash flow hedges

110,101

86,981

25,051

Tier 1 capital

1,249,843

1,057,010

1,030,387

Less:

Low-level recourse and residual interests

-

(20,424)

(19,079)

Add:

Allowance for loan and lease losses

77,393

78,254

80,419

Total regulatory capital

1,327,236

$

1,114,840

$

1,091,727

$

Adjusted total assets

15,022,729

$

13,731,482

$

12,438,222

$

Risk-weighted assets

8,424,290

7,311,556

6,648,103

Non-GAAP Reconciliations

Regulatory Capital (bank level)

Tangible Common Equity and Tangible Assets |

Non-GAAP Reconciliations

Tangible Common Equity

2Q 2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

GAAP shareholders equity

1,181

$

968

$

1,013

$

554

$

411

$

239

$

213

$

185

$

165

$

144

$

Less: Goodwill

10

10

10

0

0

2

0

0

0

0

Less: Other intangible assets

7

7

9

-

1

2

3

4

6

7

Tangible common equity

1,164

$

950

$

994

$

554

$

410

$

235

$

209

$

180

$

159

$

137

$

37 |