Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SunCoke Energy, Inc. | d385485d8k.htm |

| EX-99.1 - PRESS RELEASE - SunCoke Energy, Inc. | d385485dex991.htm |

Q2 2012

Earnings Conference Call

July 26, 2012

Exhibit 99.2 |

Safe Harbor

Statement Safe Harbor Statement

This slide presentation should be reviewed in conjunction with SunCoke’s

Second Quarter 2012 earnings release and conference call held on July 26,

2012 at 10:00 a.m. ET. Some

of

the

information

included

in

this

presentation

contains

“forward-looking

statements”

(as

defined

in

Section

27A

of

the Securities Act of 1933, as amended and Section 21E of the Securities Exchange

Act of 1934, as amended). Such forward-looking statements are based on

management’s beliefs and assumptions and on information currently available.

Forward-looking statements include the information concerning SunCoke’s

possible or assumed future results of operations, the planned Master Limited

Partnership, business strategies, financing plans, competitive position, potential

growth opportunities, potential operating performance improvements, the effects of

competition and the effects of future legislation or regulations.

Forward-looking statements include all statements that are not historical facts and may be

identified

by

the

use

of

forward-looking

terminology

such

as

the

words

“believe,”

“expect,”

“plan,”

“intend,”

“anticipate,”

“estimate,”

“predict,”

“potential,”

“continue,”

“may,”

“will,”

“should”

or the negative of these terms or similar expressions.

Forward-looking statements involve risks, uncertainties and assumptions.

Actual results may differ materially from those

expressed in these forward-looking statements. You should not put undue

reliance on any forward-looking statements. In accordance with the safe

harbor provisions of the Private Securities Litigation Reform Act of 1995, SunCoke has

included in its filings with the Securities and Exchange Commission cautionary

language identifying important factors (but not necessarily all the

important factors) that could cause actual results to differ materially from those expressed in any

forward-looking statement made by SunCoke. For more information concerning

these factors, see SunCoke's Securities and Exchange Commission

filings. All forward-looking statements included in this presentation

are expressly qualified in their entirety by such cautionary statements.

SunCoke does not have any intention or obligation to update publicly any

forward-looking statement (or its associated cautionary language) whether as a

result of new information or future events or after the date of this

presentation, except as required by applicable law. This presentation

includes certain non-GAAP financial measures intended to supplement, not substitute for, comparable

GAAP measures. Reconciliations of non-GAAP financial measures to GAAP financial

measures are provided in the Appendix at the end of the presentation.

Investors are urged to consider carefully the comparable GAAP measures and

the reconciliations to those measures provided in the Appendix, or on our website

at www.suncoke.com. SunCoke Energy Q2 2012 Earnings Conference Call

1 |

Q2 2012 Earnings

Overview Q2 2012 results of $0.32 per share driven

by strong Coke performance

•

Middletown startup has been a success

•

Continued improvement at Indiana

Harbor

•

Strong operations at other facilities

Coal action plan progressing

•

Improved sequential performance

•

Difficult demand/price environment

continues

Strong liquidity position

•

Generated significant free cash flow

•

Cash balance of $190 million and virtually

undrawn revolver of $150 million

Reaffirm expected 2012 Adjusted

EBITDA

(1)

of $250 million to $280 million

•

2012 free cash flow

(2)

is now expected to be

in excess of $100 million

(1)

For a definition and reconciliation of Adjusted EBITDA, please see the

appendix.

(2)

For a definition and reconciliation of free cash flow, please see the appendix.

SunCoke Energy Q2 2012 Earnings Conference Call

2

Earnings Per Share (diluted)

Adjusted EBITDA

(1)

(in millions)

$0.17

$0.24

$0.32

$0.32

2011

2012

Q1

Q2

$26.6

$55.8

$37.7

$65.5

2011

2012

Q1

Q2 |

MLP Update

MLP Update

•

Board approved formation of MLP

•

Expected Assets/Structure

–

A portion of our interests in

Haverhill and Middletown

–

SXC to own General Partner,

incentive distribution rights and a

portion of the partnership units

•

Proceeds to SXC

–

Expected uses will include paying

down debt, funding expansion and

other general corporate purposes

•

Timing

–

Expect to close no sooner than

fourth quarter 2012

•

Additional details will be in S-1

SunCoke Energy Q2 2012 Earnings Conference Call

3

Middletown Operations

Haverhill Operations |

Q2 2012 Financial

Results Q2 2012 Financial Results

Revenue up 22%

•

Middletown sold 146 thousand tons;

added $72.0 million to revenue

•

Higher average coal prices benefited

both Coke and Coal revenues

Adjusted EBITDA

(3)

increased 74%

•

Middletown contributed $14.0 million

•

Improved operations at Indiana Harbor

•

Yield/Cost improvement at Granite City

and other facilities

•

Coal results impacted by lower prices

and volumes in hi-vol./thermal

operations

•

Lower corporate costs

Earnings Per Share of $0.32

•

Reflects financing costs of standalone

capital structure

SunCoke Energy Q2 2012 Earnings Conference Call

4

($ in millions)

Q2'12

Q2'11

Domestic

Coke

Sales

Volume

1,074

927

147

Coal Sales Volumes

365

334

31

Revenue

460.9

$

377.9

$

83.0

$

Operating Income

42.8

$

21.5

$

21.3

$

Net Income Attributable to

Shareholders

22.7

$

22.5

$

0.2

$

Earnings Per Share

0.32

$

0.32

$

0.00

$

Coke Adjusted EBITDA

(1)

61.8

$

36.7

$

25.1

$

Coal Adjusted EBITDA

(2)

9.3

$

11.5

$

(2.2)

$

Corporate/Other

(5.6)

$

(10.5)

$

4.9

$

Adjusted EBITDA

(3)

65.5

$

37.7

$

27.8

$

Change

(1) Coke Adjusted EBITDA includes Jewell Coke, Other Domestic Coke and International

segments.

(2) Coal Adjusted EBITDA includes Coal Mining segment. In Q1 ’12, internal

coal transfer price mechanism changed to reflect Jewell Coke contract price; prior year

periods adjusted to reflect this change.

(3) For a definition and reconciliation of Adjusted EBITDA, please see appendix. |

Adjusted

EBITDA Adjusted EBITDA

(1)

(1)

Bridge –

Bridge –

Q2 2011 to Q2 2012

Q2 2011 to Q2 2012

SunCoke Energy Q2 2012 Earnings Conference Call

5

Quarter’s performance led by strong Coke business results

(1)

(2)

($ in millions)

$37.7

$65.5

$14.0

$5.1

$1.2

$4.8

$4.9

($2.2)

Q2 2011

Adjusted

EBITDA (1)

Middletown

Indiana

Harbor

(excluding one-time

items) (2)

Indiana

Harbor one-time

items (2)

Coke Business

(Jewel/Haverhill/

Granite City/Int'l)

Coal Mining

Corporate

Costs

Q2 2012

Adjusted

EBITDA (1)

Total improvement of

$6.3 million

For a definition and reconciliation of Adjusted EBITDA, please see the appendix.

One-time items that impacted Indiana Harbor performance in Q2 2011 included $1.2 million

($0.8 million net of noncontrolling interests) due to lower cost or market

adjustment on coke inventory purchased to meet projected production shortfall.

|

EPS Bridge

– EPS Bridge –

Q2 2011 to Q2 2012

Q2 2011 to Q2 2012

SunCoke Energy Q2 2012 Earnings Conference Call

6

EPS reflects strength of cokemaking business

offset by financing costs for standalone capital structure

(1)

$0.32

$0.32

$0.35

$0.06

($0.03)

($0.08)

($0.23)

($0.07)

Q2 2011 EPS

(Diluted)

Adjusted

EBITDA(1)

Coke business

Adjusted

EBITDA(1)

Corporate Costs

Adjusted

EBITDA(1)

Coal Mining

Depreciation,

Depletion

& Amortization

Financing Costs

Taxes

Q2 2012 EPS

(Diluted)

Reflects:

Q2 2012 interest expense: $12.0m

Q2 2011 interest income from affiliate: $5.7m

For a definition and reconciliation of Adjusted EBITDA, please see the appendix. |

Domestic Coke Business Summary

Domestic Coke Business Summary

(Jewell Coke & Other Domestic Coke)

(Jewell Coke & Other Domestic Coke)

SunCoke Energy Q2 2012 Earnings Conference Call

7

(Tons in thousands)

($ in millions, except per ton amounts)

Strong quarter for domestic coke profitability driven by

Middletown, Indiana Harbor and other operations

Domestic Coke Production

Domestic Coke Adjusted EBITDA

(1)

Per Ton

(1)

For a definition of EBITDA and Adjusted EBITDA/Ton and reconciliations, please see the

appendix.

(2)

Includes Indiana Harbor contract billing adjustment of $6.0 million, net of NCI, and

inventory adjustment of $6.2 million, net of NCI, of which $3.1 million is

attributable to Q3 2011.

(3)

Includes a $2.4 million, net of NCI, charge related to coke inventory reduction and a $1.3

million, net of NCI, lower cost or market adjustment on pad coal inventory and

lower coal-to-coke yields related to the startup at Middletown.

|

Domestic Coke

Business Outlook Domestic Coke Business

Outlook ($ in millions, except as noted)

Estimated

Low

Estimated

High

Domestic Coke Adjusted EBITDA

(1)

Per Ton

$55

$60

Annual Domestic Coke Sales Volumes (in millions of tons)

x 4.3

x 4.4

Domestic Coke Adjusted EBITDA

(1)

$237

$264

Less: Ongoing Capital Expenditures

($35)

($35)

Annual Domestic Coke Adjusted EBITDA

(1)

less Ongoing

Capital Expenditures

$202

$229

Illustrative Liquidity Ratios for Domestic Coke Business

Estimated

Estimated

Net Debt

(2)

to Adjusted EBITDA

(1)

2.7x

2.3x

Interest Coverage

(3)

4.6x

5.2x

(1)

For a definition and reconciliation of Adjusted EBITDA, please see the appendix.

(2)

Net Debt represents Total Debt less cash balance at end of period. Net Debt provides a

perspective on the Company's overall debt position. Net Debt was calculated by subtracting our

6/30/2012 cash balance of $190.0 million from our Total Debt of $724.9 million on 6/30/2012.

(3)

Interest coverage is Adjusted EBITDA divided by expected 2012 interest expense of $44 million,

net of amortization of issuance, discount and other fees. All figures are

estimates based on current expectations for domestic coke business (Jewell Coke and Other Domestic Coke segments); for example

purposes only

•

Expect

domestic

coke

Adjusted

EBITDA

(1)

per

ton

to

be

$55

-

$60

for

balance

of

2012

•

Based on current sentiment, 2012 coke sales volume expected to be in middle of range

SunCoke Energy Q2 2012 Earnings Conference Call

8 |

SunCoke

Energy

Q2

2012

Earnings

Conference

Call

9

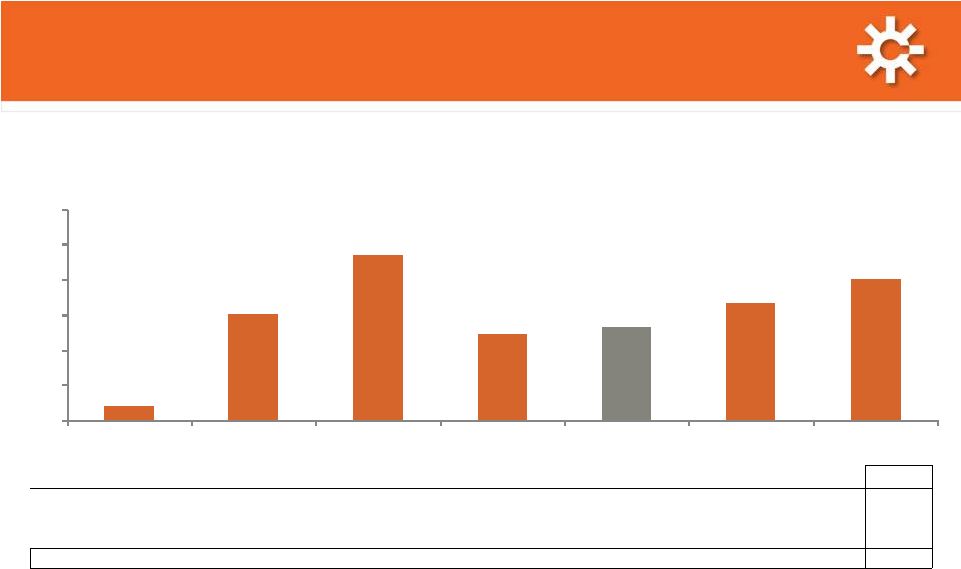

Pretax Return on Invested Capital (ROIC)

Pretax Return on Invested Capital (ROIC)

Pretax ROIC, ex-Middletown prior 2012

(1)(2)

Q1 2011

Q2 2011

Q3 2011

Q4 2011

2011

Q1 2012

Q2 2012

Total Domestic Coke (Includes Jewell Coke and Other Domestic Coke)

2%

15%

23%

12%

13%

17%

20%

International Coke

10%

7%

20%

120%

36%

0%

7%

Coal Mining

46%

28%

21%

(5%)

23%

11%

17%

Total SunCoke (Including Corp./Other)

4%

11%

16%

8%

10%

13%

17%

2%

15%

23%

12%

17%

20%

13%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Q1 2011

Q2 2011

Q3 2011

Q4 2011

2011

Q1 2012

Q2 2012

Pretax ROIC

(1)

for Domestic Coke

excluding Middletown prior to 2012

(2)

(3)

(3)

(4)

1)

For a definition of Pretax ROIC and reconciliations, please see the appendix. Pretax ROIC is

calculated as Adjusted Pretax Operating Income divided by average invested capital

(stockholders’ equity plus total debt net of cash and cash equivalents); for a reconciliation of

Adjusted Pretax Operating Income to Adjusted EBITDA, please see appendix

2)

This table excludes Middletown assets up to and including Q4 2011. At the end of Q4 2011,

identifiable assets included in Other Domestic Coke attributable to Middletown were $402.8m

(prior to Q4 2011, Middletown was included in the Corporate and Other segment); see historical segment detail in public filings for additional detail.

3)

Includes Indiana Harbor contract billing adjustment of $6.0 million, net of NCI, and inventory

adjustment of $6.2 million, net of NCI, of which $3.1 million is attributable to Q3 2011.

4)

Includes a $2.4 million, net of NCI, charge related to a coke inventory reduction and a $1.3 million,

net of NCI, lower cost or market adjustment on pad coal inventory and $4.0

million of non-recurring costs and lower coal-to-coke yields related to the startup at

Middletown. |

Q2

'11 Q3 '11

Q4 '11

Q1 '12

Q2 '12

Coal Sales

334

371

363

373

365

Coal Producton

340

340

349

375

401

Purchased Coal

24

22

20

19

4

$11

$9

$2

$7

$9

$162

$155

$159

$171

$167

$34

$25

$20

$20

$25

$126

$132

$138

$151

$137

-$50

$0

$50

$100

$150

$200

Q2 '11

Q3 '11

Q4 '11(3)

Q1 '12

Q2 '12

Coal Adjusted EBITDA

Average Sales Price

Coal Adj EBITDA / ton

Coal Cash Cost / ton

Coal Mining Financial Summary

Coal Mining Financial Summary

SunCoke Energy Q2 2012 Earnings Conference Call

10

Coal Mining Adjusted EBITDA

(1)

and Avg. Sales

Price/Ton

(2)

($ in millions, except per ton amounts)

Q2 2012 Adjusted EBITDA

(1)

declined YoY to

$9.3 million

•

Pricing up modestly, reflecting strong mid-vol.

pricing/volumes, offset by weak

hi-vol. & thermal pricing/volumes

•

Cash costs up $11/ton, reflecting decreased mix

and higher costs of hi-vol. & thermal production

(mid-vol. costs up slightly)

Coal action plan gaining traction

•

Cash cost per ton decreased from Q1 2012

Intend to maintain cash neutral position in

Coal Sales, Production and Purchases

•

Jewell underground cash cost per ton was $143

in Q2 2012 vs. $161 in Q1 2012, and $139 in Q2

2011

•

Jewell reject rates were 66% in Q2 2012,

improved from 68% in Q1 2012 and 67% in Q2

2011

•

Expect further cash cost reductions for 2013

(1)

For a definition and a reconciliation of Adjusted EBITDA, please see the appendix.

(2)

Average Sales Price is the weighted average sales price for all coal sales volumes, including

sales to affiliates and sales to Jewell Coke.

(3)

Q4 2011 Adjusted EBITDA inclusive of Black Lung Liability charge of $3.4 million and

OPEB expense allocation of $1.8 million.

2012 |

Q2 2012 Sources

& Uses of Cash Q2 2012 Sources & Uses of Cash

SunCoke Energy Q2 2012 Earnings Conference Call

11

Liquidity position and credit metrics improving;

free cash flow

(1)

was $66 million in first half 2012

($ in millions)

(1)

For a definition and reconciliation of free cash flow, please see appendix.

$113.6

$24.0

$20.2

$40.1

$190.0

$5.6

($0.1)

($11.2)

($2.2)

Q1 2012

Cash

Balance

Q2 2012

Net Income

Depreciation,

Depletion &

Amortization

Deferred

Taxes

Changes in

Working

Capital

Other

Capital

Expenditures

Cash used in

financing

activities

Q2 2012

Cash

Balance

Primary changes vs. Q1 2012:

Accounts receivable: +$24.8m

Accrued liabilities: +$9.9m

Interest payable: +$7.8m

Inventory: ($5.7m) |

Strategies for

Enhancing Shareholder Value Strategies for Enhancing Shareholder Value

12

SunCoke Energy Q2 2012 Earnings Conference Call

Maintain focus on details

and discipline of coke and

coal mining operations

Sustain and enhance top

quartile safety

performance and ability to

meet environment

standards

Leverage operating know-

how and technology to

continuously improve

yields and operating costs

Domestic

Continue permitting

efforts for next

potential U.S. facility

Explore opportunities to

make strategic

investments in existing

capacity

International

Execute India entry and

pursue follow-on

growth

Coke MLP

Execute plan to place a

portion of our

cokemaking assets into

an MLP structure

Coal

Optimize operations

and investments to

enhance long-term

strategic flexibility

Operational

Excellence

Grow The Coke

Business

Strategically Optimize

Assets |

Updated 2012

Guidance Updated 2012 Guidance

Metric

Expected 2012 Outlook

Adjusted EBITDA

(1)

$250 million –

$280 million

EPS* (at 22% tax rate)

$1.30 –

$1.65

Capital Expenditures &

Investments

Approximately $85 million

Free Cash Flow

(2)

$100 million +

Cash Tax Rate

10% –

15%

Effective Tax Rate

20% –

24%

Corporate Costs

$30 million –

$35 million

Coke Production

In excess of 4.3 million tons

Coal Production

Approximately 1.6 million tons

SunCoke Energy Q2 2012 Earnings Conference Call

13

(1) For a definition and reconciliation of Adjusted EBITDA, please see the appendix.

(2) For a definition of Free Cash Flow and reconciliation, please see the appendix.

*Diluted |

Questions |

Appendix

|

Definitions

SunCoke Energy Q2 2012 Earnings Conference Call

16

for sales discounts and the deduction of income attributable to non-controlling interests in our

Indiana Harbor cokemaking operations. EBITDA reflects sales discounts included as a

reduction in sales and other operating revenue. The sales discounts represent the sharing with

our customers of a portion of nonconventional fuels tax credits, which reduce our income tax expense. However, we

believe that our Adjusted EBITDA would be inappropriately penalized if these discounts were treated as

a reduction of EBITDA since they represent sharing of a tax benefit which is not included in

EBITDA. Accordingly, in computing Adjusted EBITDA, we have added back these sales discounts.

Our Adjusted EBITDA also reflects the deduction of income attributable to noncontrolling interest in our

Indiana Harbor cokemaking operations. EBITDA and Adjusted EBITDA do not represent and should not

be considered alternatives to net income or operating income under United States generally

accepted accounting principles (GAAP) and may not be comparable to other similarly titled

measures of other businesses. Management believes Adjusted EBITDA is an important measure of the operating

performance of the Company’s assets and is indicative of the Company’s ability to generate

cash from operations.

Interests. Management believes Free Cash Flow information enhances an investor’s understanding of

a business’ ability to generate cash. Free Cash Flow does not represent and should

not be considered an alternative to net income or cash flows from operating activities as

determined under GAAP and may not be comparable to other similarly titled measures of other businesses.

attributable to non-controlling interests divided by average invested capital (stockholders’

equity plus total debt net of cash and cash equivalents). We use Pretax ROIC as one

measure of how effectively we deploy capital and make multi-year investment decisions. It

is also used as a long-term performance measure under certain of our incentive compensation

plans. Pretax ROIC is not a measure of financial performance under generally accepted

accounting principles, and may not be comparable to other similarly titled measures used by

other companies. Pretax ROIC should not be considered in isolation or as an alternative to net earnings as an indicator of

performance. We define segment level Pretax ROIC as Adjusted EBITDA less depreciation expense

plus net income attributable to non-controlling interests divided by average allocated

invested capital. Average allocated invested capital for each respective

segment is calculated pro-rata based on the segment level identifiable assets for the period as

disclosed in our public filings.

•

Adjusted

EBITDA

represents

earnings

before

interest,

taxes,

depreciation,

depletion

and

amortization

(“EBITDA”)

adjusted

•

Adjusted

EBITDA/Ton

represents

Adjusted

EBITDA

divided

by

tons

sold.

•

Free

Cash

Flow

equals

cash

from

operations

less

cash

used

in

investing

activities

less

cash

distributions

to

non-controlling

•

Pretax

Return

on

Invested

Capital

(ROIC)

is

defined

as

Adjusted

EBITDA

less

depreciation

expense

plus

net

income |

Reconciliations

SunCoke Energy Q2 2012 Earnings Conference Call

17

$ in millions

Q2 2012

Q1 2012

FY 2011

Q4 2011

Q3 2011

Q2 2011

Q1 2011

FY 2010

Adjusted Pro Forma Operating Income

151.5

Add: Pro Forma impact of ArcelorMittal settlement

51.0

Subtract: Legal and settlement charges related to ArcelorMittal Settlement

and Indiana Harbor Arbitration

(16.3)

Adjusted Operating Income

46.6

37.1

80.4

14.9

33.5

24.6

7.4

186.2

Net Income (Loss) attributable to Noncontrolling Interest

1.3

(0.3)

(1.7)

(0.5)

3.4

1.6

(6.2)

7.1

Subtract: Depreciation Expense

(20.2)

(18.4)

(58.4)

(16.0)

(14.7)

(14.7)

(13.0)

(48.2)

Adjusted EBITDA

65.5

55.8

140.5

31.4

44.8

37.7

26.6

227.3

Subtract: Depreciation, depletion and amortization

(20.2)

(18.4)

(58.4)

(16.0)

(14.7)

(14.7)

(13.0)

(48.2)

Subtract: Financing expense, net

(11.8)

(12.0)

(1.4)

(7.1)

(3.3)

4.5

4.5

19.0

Subtract: Income Tax

(7.0)

(5.3)

(7.2)

2.9

(5.1)

(1.9)

(3.1)

(46.9)

Subtract: Sales Discount

(3.8)

(3.2)

(12.9)

(3.2)

(3.5)

(3.1)

(3.1)

(12.0)

Add: Net Income attributable to NCI

1.3

(0.3)

(1.7)

(0.5)

3.4

1.6

(6.2)

7.1

Net Income

24.0

16.6

58.9

7.5

21.6

24.1

5.7

146.3

Reconciliations

from

Adjusted

Operating

Income

and

Adjusted

EBITDA

to

Net

Income |

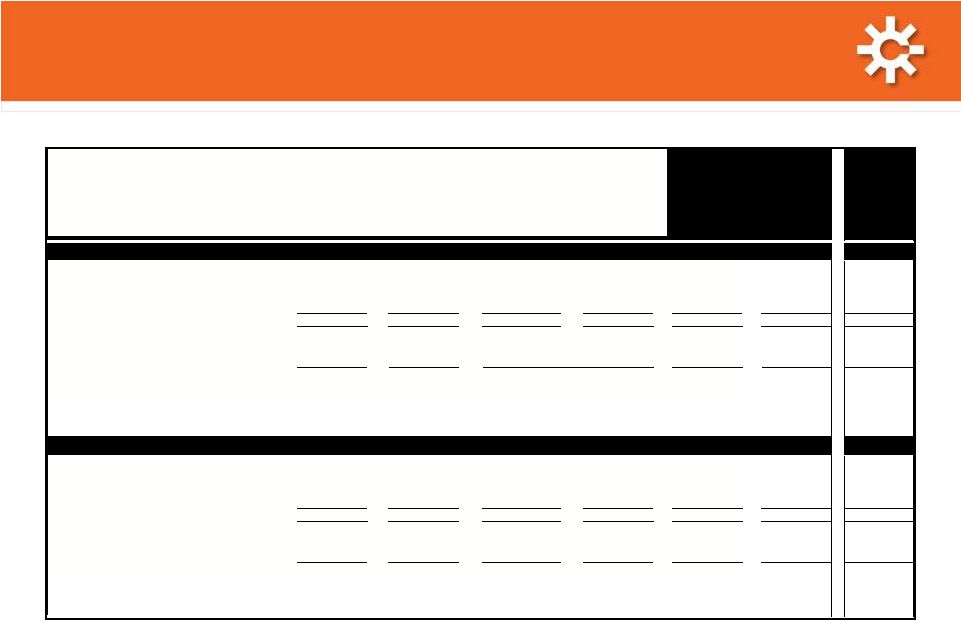

Reconciliations

SunCoke Energy Q2 2012 Earnings Conference Call

18

$ in millions, except per ton data

Jewell Coke

Other

Domestic

Coke

International

Coke

Jewell Coal

Corporate

Combined

Domestic

Coke

Q2 2012

Adjusted EBITDA

12.5

48.6

0.7

9.3

(5.6)

65.5

61.1

Subtract: Depreciation, depletion and amortization

(1.3)

(13.7)

(0.1)

(4.3)

(0.8)

(20.2)

(15.0)

Add (Subtract): Net (Income) loss attributable

to noncontrolling interests

1.3

1.3

1.3

Adjusted Pre-Tax Operating Income

11.2

36.2

0.6

5.0

(6.4)

46.6

47.4

Adjusted EBITDA

12.5

48.6

0.7

9.3

(5.6)

65.5

61.1

Sales Volume (thousands of tons)

170

892

358

373

1,062

Adjusted EBITDA per Ton

73.5

54.5

2.0

24.9

57.5

Average

Allocated

Invested

Capital

(1)

50.9

892.7

36.6

117.7

NMF

1,097.9

943.6

Annualized Quarterly Pretax ROIC

88%

16%

7%

17%

NMF

17%

20%

Q1 2012

Adjusted EBITDA

15.0

40.1

0.1

7.4

(6.8)

55.8

55.1

Subtract: Depreciation, depletion and amortization

(1.3)

(12.6)

(0.1)

(4.1)

(0.3)

(18.4)

(13.9)

Add (Subtract): Net (Income) loss attributable

to noncontrolling interests

(0.3)

(0.3)

(0.3)

Adjusted Pre-Tax Operating Income

13.7

27.2

-

3.3

(7.1)

37.1

40.9

Adjusted EBITDA

15.0

40.1

0.1

7.4

(6.8)

55.8

55.1

Sales Volume (thousands of tons)

186

892

358

373

1,078

Adjusted EBITDA per Ton

80.6

45.0

0.3

19.8

51.1

Average

Allocated

Invested

Capital

(1)

53.3

928.2

41.0

119.6

NMF

1,142.1

981.5

Annualized Quarterly Pretax ROIC

103%

12%

0%

11%

NMF

13%

17%

Reconciliations from Adjusted EBITDA to Adjusted Pre-Tax Operating Income

|

Reconciliations

SunCoke Energy Q2 2012 Earnings Conference Call

19

$ in millions, except per ton data

Jewell Coke

Other

Domestic

Coke

International

Coke

Jewell Coal

Corporate

Combined

Domestic

Coke

FY 2011

Adjusted EBITDA

46.1

89.4

13.7

35.5

(44.2)

140.5

135.5

Subtract: Depreciation, depletion and amortization

(4.9)

(38.7)

(0.2)

(12.9)

(1.7)

(58.4)

(43.6)

Add (Subtract): Net (Income) loss attributable

to noncontrolling interests

(1.7)

(1.7)

(1.7)

Adjusted Pre-Tax Operating Income

41.2

49.0

13.5

22.6

(45.9)

80.4

90.2

Adjusted EBITDA

46.1

89.4

13.7

35.5

(44.2)

140.5

135.5

Sales Volume (thousands of tons)

702

3,068

1,442

1,454

3,770

Adjusted EBITDA per Ton

65.7

29.1

9.5

24.4

35.9

Average Allocated Invested Capital

52.8

627.8

37.4

99.8

NMF

817.8

680.6

Pretax ROIC

78%

8%

36%

23%

NMF

10%

13%

Q4 2011

Adjusted EBITDA

10.6

21.3

10.2

2.5

(13.2)

31.4

31.9

Subtract: Depreciation, depletion and amortization

(1.2)

(10.6)

(0.1)

(3.7)

(0.4)

(16.0)

(11.8)

Add (Subtract): Net (Income) loss attributable

to noncontrolling interests

(0.5)

(0.5)

(0.5)

Adjusted Pre-Tax Operating Income

9.4

10.2

10.1

(1.2)

(13.6)

14.9

19.6

Adjusted EBITDA

10.6

21.3

10.2

2.5

(13.2)

31.4

31.9

Sales Volume (thousands of tons)

166

837

295

363

1,003

Adjusted EBITDA per Ton

63.9

25.4

34.6

6.9

31.8

Average Allocated Invested Capital

46.7

594.0

33.7

105.6

NMF

779.9

640.6

Annualized Quarterly Pretax ROIC

81%

7%

120%

-5%

NMF

8%

12%

Reconciliations from Adjusted EBITDA to Adjusted Pre-Tax Operating Income

|

Reconciliations

Reconciliations

SunCoke Energy Q2 2012 Earnings Conference Call

20

$ in millions, except per ton data

Jewell Coke

Other

Domestic

Coke

International

Coke

Jewell Coal

Corporate

Combined

Domestic

Coke

Q3 2011

Adjusted EBITDA

13.9

34.3

1.7

9.2

(14.3)

44.8

48.2

Subtract: Depreciation, depletion and amortization

(1.2)

(9.9)

-

(3.3)

(0.3)

(14.7)

(11.1)

Add (Subtract): Net (Income) loss attributable

to noncontrolling interests

3.4

3.4

3.4

Adjusted Pre-Tax Operating Income

12.7

27.8

1.7

5.9

(14.6)

33.5

40.5

Adjusted EBITDA

13.9

34.3

1.7

9.2

(14.3)

44.8

48.2

Sales Volume (thousands of tons)

191

777

373

371

968

Adjusted EBITDA per Ton

72.8

44.1

4.6

24.8

49.8

Average Allocated Invested Capital

53.5

636.2

34.8

115.1

NMF

839.6

689.7

Annualized Quarterly Pretax ROIC

95%

17%

20%

21%

NMF

16%

23%

Q2 2011

Adjusted EBITDA

10.6

25.3

0.8

11.5

(10.5)

37.7

35.9

Subtract: Depreciation, depletion and amortization

(1.4)

(9.6)

(0.1)

(3.2)

(0.4)

(14.7)

(11.0)

Add (Subtract): Net (Income) loss attributable

to noncontrolling interests

1.6

1.6

1.6

Adjusted Pre-Tax Operating Income

9.2

17.3

0.7

8.3

(10.9)

24.6

26.5

Adjusted EBITDA

10.6

25.3

0.8

11.5

(10.5)

37.7

35.9

Sales Volume (thousands of tons)

170

757

412

334

927

Adjusted EBITDA per Ton

62.4

33.4

1.9

34.4

38.7

Average Allocated Invested Capital

57.9

648.2

39.7

117.7

NMF

863.4

706.1

Annualized Quarterly Pretax ROIC

64%

11%

7%

28%

NMF

11%

15%

Reconciliations from Adjusted EBITDA to Adjusted Pre-Tax Operating Income

|

Reconciliations

Reconciliations

SunCoke Energy Q2 2012 Earnings Conference Call

21

$ in millions, except per ton data

Jewell Coke

Other

Domestic

Coke

International

Coke

Jewell Coal

Corporate

Combined

Domestic

Coke

Q1 2011

Adjusted EBITDA

11.0

8.5

1.0

12.3

(6.2)

26.6

19.5

Subtract: Depreciation, depletion and amortization

(1.1)

(8.6)

-

(2.7)

(0.6)

(13.0)

(9.7)

Add (Subtract): Net (Income) loss attributable

to noncontrolling interests

(6.2)

(6.2)

(6.2)

Adjusted Pre-Tax Operating Income

9.9

(6.3)

1.0

9.6

(6.8)

7.4

3.6

Adjusted EBITDA

11.0

8.5

1.0

12.3

(6.2)

26.6

19.5

Sales Volume (thousands of tons)

175

697

362

386

872

Adjusted EBITDA per Ton

62.9

12.2

2.8

31.9

22.4

Average Allocated Invested Capital

56.0

645.6

41.4

83.8

NMF

826.9

701.7

Annualized Quarterly Pretax ROIC

71%

-4%

10%

46%

NMF

4%

2%

FY 2010

Adjusted EBITDA

123.9

78.5

15.0

24.0

(14.1)

227.3

202.4

Add (Subtract): Pro Forma impact of

ArcelorMittal settlement

(69.0)

18.0

(51.0)

(51.0)

Add (Subtract): Legal and settlement charges

related to ArcelorMittal Settlement and

Indiana Harbor Arbitration

3.6

12.7

16.3

16.3

Proforma Adjusted EBITDA

58.5

109.2

15.0

24.0

(14.1)

192.6

167.7

Subtract: Depreciation, depletion and amortization

(4.4)

(35.0)

(0.1)

(7.7)

(1.0)

(48.2)

(39.4)

Add (Subtract): Net (Income) loss attributable

to noncontrolling interests

7.1

7.1

7.1

Adjusted Pro Forma Operating Income

54.1

81.3

14.9

16.3

(15.1)

151.5

135.4

Adjusted EBITDA

58.5

109.2

15.0

24.0

(14.1)

192.6

167.7

Sales Volume (thousands of tons)

721

2,917

-

1,277

3,638

Adjusted EBITDA per Ton

81.1

37.4

18.8

46.1

Average Allocated Invested Capital

58.5

691.6

42.5

51.4

NMF

844.0

750.1

Pretax ROIC

92%

12%

35%

32%

NMF

18%

18%

Reconciliations from Adjusted EBITDA to Adjusted Pre-Tax Operating Income

|

SunCoke Energy Q2 2012 Earnings Conference Call

22

Pretax Return on Invested Capital Reconciliation,

$MM

Consolidated Sun Coke Energy

Q2 2012

Q1 2012

2011

Q4 2011

Q3 2011

Q2 2011

Q1 2011

2010

Adjusted Pre-Tax Operating Income

(1)

46.6

37.1

80.4

14.9

33.5

24.6

7.4

151.5

Invested Capital

Q1 2012

(2)

Q1 2012

(2)

2011

Q4 2011

Q3 2011

Q2 2011

Q1 2011

2010

Debt

$724.9

$725.7

$726.4

$726.4

$697.8

$794.7

$715.7

$655.3

Equity

535.4

513.3

559.9

559.9

604.5

457.3

433.4

429.3

Cash

(190.0)

(113.6)

(127.5)

(127.5)

(110.9)

(30.5)

(11.0)

(40.1)

Middletown

(402.8)

(402.8)

(387.6)

(346.1)

(286.7)

(242.2)

Invested Capital

$1,070.3

$1,125.4

$756.0

$756.0

$803.8

$875.4

$851.5

$802.4

Average Invested Capital*

$1,097.9

$1,142.1

$817.8

$779.9

$839.6

$863.4

$826.9

$844.0

Q2 2012

Q1 2012

2011

Q4 2011

Q3 2011

Q2 2011

Q1 2011

2010

Quarterly ROIC

17%

13%

8%

16%

11%

4%

Last Twelve Months' ROIC

10%

18%

*5 quarter average for 2011, two quarter average for each quarter, year-end average for

2010 Debt

Q2 2011

Q1 2011

2010

Interest receivable from affiliate

(3.6)

(1.8)

0.0

Notes receivable from affiliate

(289.0)

(289.0)

(289.0)

Advances from affiliate

1,087.3

1,006.5

944.3

Total Debt

794.7

715.7

655.3

(1) See Adjusted EBITDA and Pretax ROIC Reconciliation for respective periods, 2010 uses

Adjusted Pro Forma Operating Income

(2) Q1 2012 Average Invested Capital includes Middletown in both the beginning and ending of

quarter average (Q1 2012 and Q4 2011)

|

SunCoke Energy Q2 2012 Earnings Conference Call

23

Pretax Return on Invested Capital Reconciliation

Period ended

Jewell

Coke

Other

Domestic Coke

International

Coke

Coal

Mining

Corporate

and Other

Total

Identifiable Assets for

Allocating Invested Capital

Q2 2012

81.4

1,458.4

53.9

193.0

183.5

1,970.2

Q1 2012

83.9

1,440.2

64.6

189.1

141.1

1,918.9

Q4 2011, inc Middletown

81.6

1,440.8

62.7

182.1

174.6

1,941.8

Q4 2011

81.6

1,038.0

62.7

182.1

174.6

1,539.0

Q3 2011

77.7

990.6

52.7

178.3

192.3

1,879.2

Q2 2011

85.1

954.4

53.6

173.5

67.2

1,972.6

Q1 2011

82.6

922.6

61.2

167.3

48.9

1,860.1

2010

80.9

962.6

59.7

76.7

7.3

1,718.5

Percentage of

Invested Capital

Q2 2012

4.6%

81.6%

3.0%

10.8%

NMF

100.0%

Q1 2012

4.7%

81.0%

3.6%

10.6%

NMF

100.0%

Q4 2011, inc Middletown

4.6%

81.5%

3.5%

10.3%

NMF

100.0%

Q4 2011

6.0%

76.1%

4.6%

13.3%

NMF

100.0%

Q3 2011

6.0%

76.2%

4.1%

13.7%

NMF

100.0%

Q2 2011

6.7%

75.4%

4.2%

13.7%

NMF

100.0%

Q1 2011

6.7%

74.8%

5.0%

13.6%

NMF

100.0%

2010

6.9%

81.6%

5.1%

6.5%

NMF

100.0%

Allocated

Invested Capital

Q2 2012

48.8

873.6

32.3

115.6

-

1,070.3

Q1 2012

53.1

911.7

40.9

119.7

-

1,125.4

Q4 2011, inc Middletown

53.5

944.8

41.1

119.4

-

1,158.8

Q4 2011

45.2

575.1

34.7

100.9

-

756.0

Q3 2011

48.1

612.9

32.6

110.3

-

803.8

Q2 2011

58.8

659.6

37.0

119.9

-

875.4

Q1 2011

57.0

636.7

42.3

115.5

-

851.5

Note: This table excludes Middletown assets up to and including Q4 2011. At the end of Q4 2011,

identifiable assets included in Other Domestic Coke attributable to Middletown were $402.8m

(prior to Q4 2011, Middletown was included in the Corporate and Other segment); see historical segment detail in public filings for additional detail. |

(in

millions) 2012E

Low

2012E

High

Net Income

$98

$122

Depreciation, Depletion and Amortization

74

72

Total financing costs, net

48

46

Income tax expense

25

37

EBITDA

$245

$277

Sales discounts

11

10

Noncontrolling interests

(6)

(7)

Adjusted EBITDA

$250

$280

Estimated EBITDA Reconciliation

2012E Net Income to Adjusted EBITDA Reconciliation

SunCoke Energy Q2 2012 Earnings Conference Call

24 |

Free Cash Flow

Reconciliations 2012E Estimated Free Cash Flow Reconciliation

SunCoke Energy Q2 2012 Earnings Conference Call

25

(in millions)

1

st

Half

2012

Cash from operations

$ 86.7

Less cash used for investing activities

(20.7)

Less payments to minority interest

( -

)

Free Cash Flow

$ 66.0

(in millions)

2012

Cash from operations

In excess of

$ 189

Less cash used for investing activities

Approx.

(85)

Less payments to minority interest

Approx.

(4)

Free Cash Flow

In excess of

$ 100

First Half 2012 Free Cash Flow Reconciliation |

Media releases and SEC filings

are available on

www.suncoke.com

Investor Relations:

630-824-1907 |