Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - FIRST HORIZON CORP | d382051d8k.htm |

Exhibit 99.1

SECOND QUARTER 2012

FINANCIAL SUPPLEMENT

If you need further information, please contact:

Aarti Bowman, Investor Relations

901-523-4017

aagoorha@firsthorizon.com

TABLE OF CONTENTS

| Page | ||||

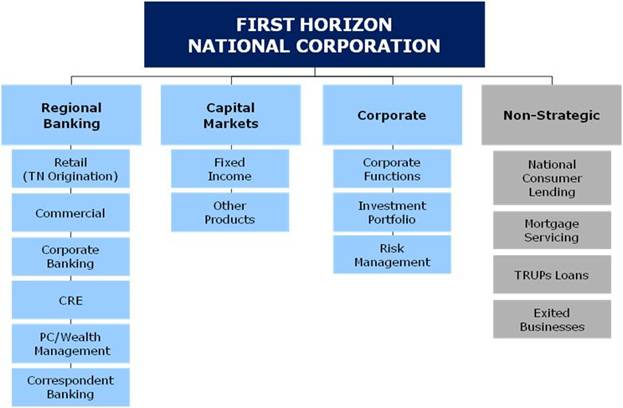

| First Horizon National Corporation Segment Structure |

3 | |||

| Performance Highlights |

4 | |||

| Charges for Restructuring, Repositioning, & Efficiency Initiatives |

6 | |||

| Consolidated Results |

||||

| Income Statement |

||||

| Summary Results |

7 | |||

| Income Statement |

8 | |||

| Other Income and Other Expense |

9 | |||

| Balance Sheet |

||||

| Period End Balance Sheet |

10 | |||

| Average Balance Sheet |

11 | |||

| Net Interest Income |

12 | |||

| Average Balance Sheet: Yields and Rates |

13 | |||

| Mortgage Servicing Rights |

14 | |||

| Business Segment Detail |

||||

| Segment Highlights |

15 | |||

| Regional Banking |

16 | |||

| Capital Markets |

17 | |||

| Corporate |

18 | |||

| Non-Strategic |

19 | |||

| Capital Highlights |

20 | |||

| Asset Quality |

||||

| Asset Quality: Consolidated |

21 | |||

| Asset Quality: Regional Banking and Corporate |

23 | |||

| Asset Quality: Non-Strategic |

24 | |||

| Rollforwards of Nonperforming Loans and ORE Inventory and Commercial Loans - Portfolio Metrics |

25 | |||

| Consumer Loans - Portfolio Metrics |

26 | |||

| Non-GAAP to GAAP Reconciliation |

27 | |||

| Glossary of Terms |

28 | |||

Other Information

This financial supplement contains forward-looking statements involving significant risks and uncertainties. A number of important factors could cause actual results to differ materially from those in the forward-looking information. Those factors include general economic and financial market conditions, including expectations of and actual timing and amount of interest rate movements including the slope of the yield curve, competition, customer and investor responses to these conditions, ability to execute business plans, geopolitical developments, recent and future legislative and regulatory developments, natural disasters, and items mentioned in this financial supplement and in First Horizon National Corporation’s (“FHN”) most recent press release, as well as critical accounting estimates and other factors described in FHN’s recent filings with the SEC. FHN disclaims any obligation to update any such factors or to publicly announce the result of any revisions to any of the forward-looking statements included herein or therein to reflect future events or developments.

Use of Non-GAAP Measures

Certain ratios are included in this financial supplement that are non-GAAP, meaning they are not presented in accordance with generally accepted accounting principles (“GAAP”) in the U.S. FHN’s management believes such ratios are relevant to understanding the capital position and results of the Company. The non-GAAP ratios presented in this financial supplement are tangible common equity to tangible assets, tangible book value per common share, tier 1 common to risk weighted assets, adjusted tangible common equity to risk weighted assets, and net interest margin adjusted for fully taxable equivalent (“FTE”). These ratios are reported to FHN’s management and Board of Directors through various internal reports. Additionally, disclosure of non-GAAP capital ratios provides a meaningful base for comparability to other financial institutions as demonstrated by their use by the various banking regulators in reviewing the capital adequacy of financial institutions. Non-GAAP measures are not formally defined by GAAP or codified in the federal banking regulations, and other entities may use calculation methods that differ from those used by FHN. Tier 1 capital is a regulatory term and is generally defined as the sum of core capital (including common equity and instruments that can not be redeemed at the option of the holder) adjusted for certain items under risk based capital regulations. Also a regulatory term, risk weighted assets includes total assets adjusted for credit risk and is used to determine capital ratios. Refer to the tabular reconciliation of non-GAAP to GAAP measures and presentation of the most comparable GAAP items on page 27 of this financial supplement.

2

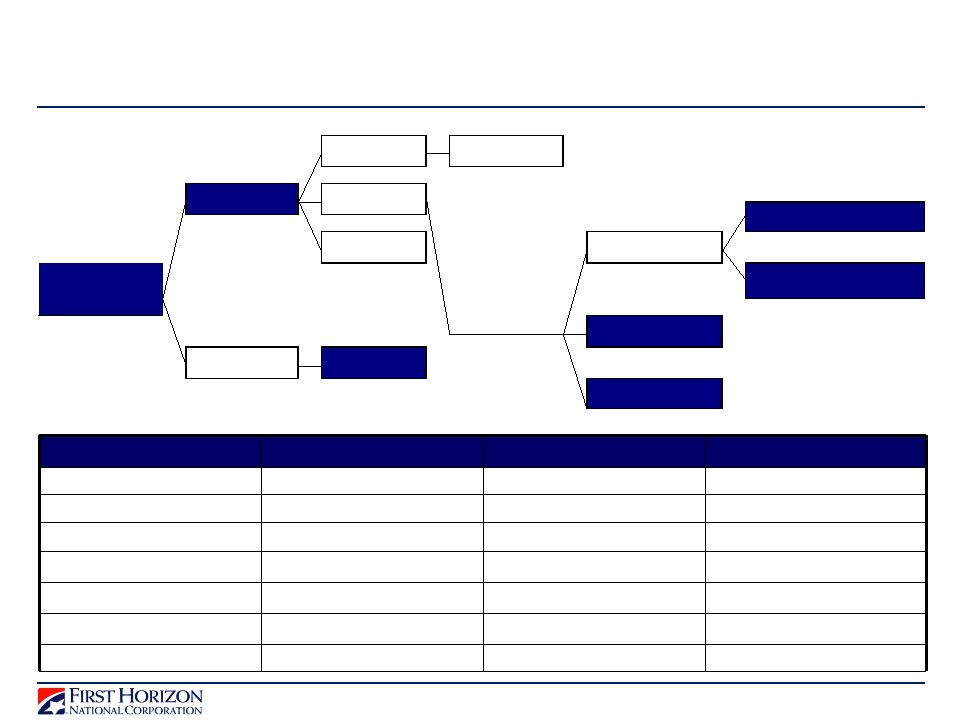

| FIRST HORIZON NATIONAL CORPORATION SEGMENT STRUCTURE |

|

Regional Banking

| • | Traditional lending and deposit taking, investments, financial planning, trust services, asset management, and cash management |

| • | Correspondent banking which provides credit, depository, and other banking related services to other financial institutions |

Capital Markets

| • | Fixed income sales, trading, and strategies for institutional clients in the U.S. and abroad |

| • | Other capital markets products such as portfolio advisory, derivatives, and loan trading |

Corporate

| • | Executive management, enterprise-wide risk management, corporate, finance, corporate communications, low income housing activities, legal functions and funding for the corporation including any impact from balance sheet positioning |

| • | Various charges related to restructuring, repositioning, and efficiency initiatives |

Non-Strategic

| • | Wind-down businesses that include: |

| • | National consumer lending loan portfolios |

| • | Trust preferred loan portfolio |

| • | Legacy mortgage servicing |

| • | Exited businesses such as First Horizon Msaver, Inc. (“Msaver”), First Horizon Insurance, Inc. (“FHI”), and Highland Capital Management Corporation (“Highland Capital”) and associated restructuring, repositioning, and efficiency charges |

3

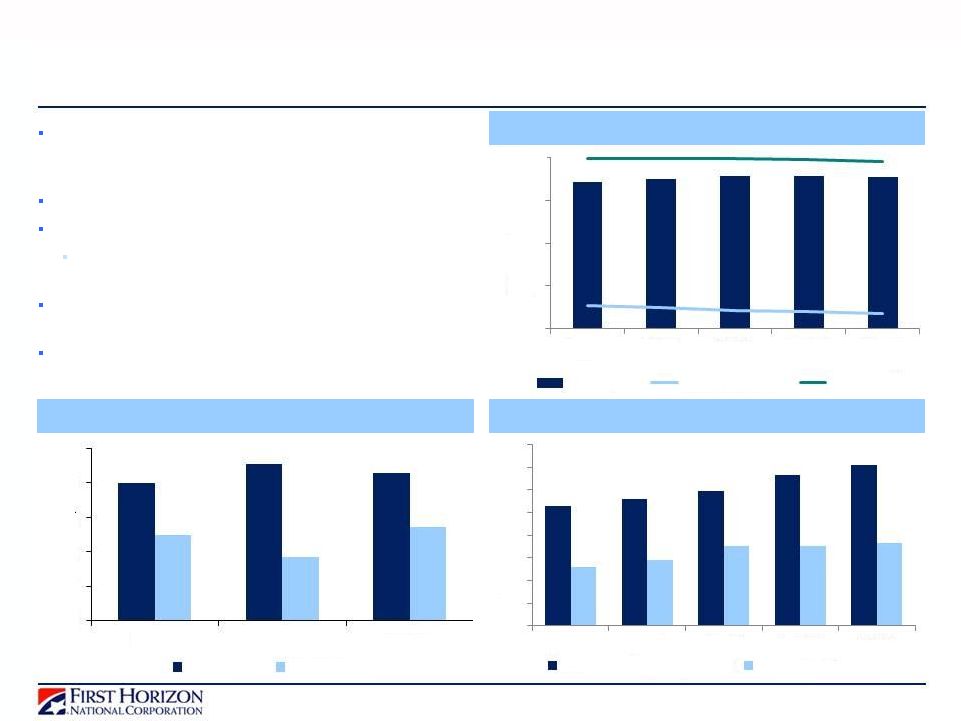

PERFORMANCE HIGHLIGHTS

Summary of Second Quarter 2012 Significant Items

(Millions)

| Segment | Item | Income Statement | Amount | Comments | ||||

| Non Strategic | Repurchase Provision | Noninterest Expense: Repurchase and foreclosure provision | $(250.0) million | Pre-tax charge related to repurchase obligations for mortgage loans (see discussion under Non-strategic section) | ||||

| Non Strategic | Legal Expense | Noninterest Expense: Other | $(22.0) million | Pre-tax loss accrual related to pending legal matters | ||||

| Non Strategic | Investment Security Gain |

Noninterest Income: Security Gains/Losses | $5.1 million | Pre-tax gain on the sale of venture capital investment | ||||

(Second Quarter 2012 vs. First Quarter 2012)

Consolidated

• Net loss available to common shareholders was $124.8 million, or $.50 loss per diluted share, compared to net income of $30.5 million, or $.12 per diluted share in first quarter

• Net interest income (“NII”) increased slightly in second quarter to $172.7 million; The net interest margin (“NIM”) increased to 3.16 percent from 3.12 percent

• The increase in NII is primarily attributable to an increase in commercial loan fees coupled with lower funding costs

• The increase in NIM is largely due to a decline in excess cash held at the Fed and an increase in commercial loan fees which were partially offset by a lower yielding securities portfolio

• Noninterest income (including security gains) was $158.9 million in second quarter, a decrease of $43.5 million from first quarter

• Decrease primarily driven by lower fixed income revenue within capital markets in second quarter and a decline in mortgage banking income within the non-strategic segment

• Provision expense was $15.0 million in second quarter compared to $8.0 million in first quarter

• Noninterest expense was $527.2 million in second quarter compared to $322.0 million in first quarter

• Increase primarily driven by an increase to the repurchase and foreclosure provision

• These increases were partially offset by a decline in personnel costs within capital markets commensurate with lower fixed income revenue

• Period-end loans were $16.2 billion for the second quarter compared to $16.0 billion in first quarter; average loan balances were $16.0 billion for both quarters

• The increase in the period-end loan portfolio is primarily driven by the increase in loans to mortgage companies and real estate installment loans, partially offset by continued run-off within the non-strategic portfolios

• Average core deposits decreased slightly to $15.6 billion in second quarter, period-end decreased 5% to $15.5 billion

Regional Banking

• Net interest income increased $1.1 million in second quarter

• Increase in NII primarily attributable to higher commercial loan fees in second quarter

• Provision was $4.8 million in second quarter compared to a provision credit of $7.4 million in prior quarter

• Commercial reserve levels reflect continued stabilization of the commercial portfolio; slight increase in the level of consumer reserves

• Period-end loans increased $380.8 million to $12.0 billion primarily due to an increase in loans to mortgage companies and real estate installment loans

• Noninterest income increased to $64.8 million in second quarter from $59.9 million in first quarter

• Deposit fee income increased primarily due to seasonality in non-sufficient funds (“NSF”) fee structure

• Second quarter includes $1.8 million gain related to the sale of a branch

• Noninterest expense increased to $142.4 million in second quarter from $139.4 million in prior quarter

Capital Markets

• Fixed income revenues declined to $68.2 million in second quarter from $98.6 million in first quarter

• Fixed income average daily revenue (“ADR”) was $1.1 million in second quarter compared to $1.6 million in first quarter

• Noninterest expense decreased to $60.9 million in second quarter from $80.3 million in prior quarter

• Variable compensation costs decreased consistent with the decrease in fixed income ADR

Corporate

• NII was negative $4.1 million in second quarter compared to negative $4.7 million in first quarter

• Noninterest income (including securities gains) was $3.8 million in second quarter compared to $9.3 million in prior quarter

• Decline primarily resulting from lower deferred compensation income due to market conditions and is mirrored by a reduction in deferred compensation expense

• Noninterest expense decreased to $19.4 million in second quarter from $22.5 million in prior quarter

• The decline in deferred compensation expense was partially offset by an increase in restructuring costs, primarily severance

4

PERFORMANCE HIGHLIGHTS (continued)

(Second Quarter 2012 vs. First Quarter 2012)

Non-Strategic

• NII decreased $.9 million to $24.0 million in second quarter due to the continued contraction of loan portfolios

• Provision expense decreased to $10.2 million in second quarter from $15.4 million in prior quarter due to continued stabilization and runoff of the consumer portfolio

• Noninterest income (including securities gains) decreased to $15.3 million in second quarter from $26.5 million in prior quarter primarily due to a decline in mortgage banking income

• Positive net hedging results decreased to $1.8 million in second quarter from $9.1 million in prior quarter

• Mortgage banking was also negatively affected by a decline in servicing fees and adjustment made as a result of contingencies related to prior servicing sales

• Decline in mortgage banking income was partially offset by a $5.1 million gain on sale of a venture capital investment

• Noninterest expense increased to $304.5 million in second quarter from $79.8 million in prior quarter

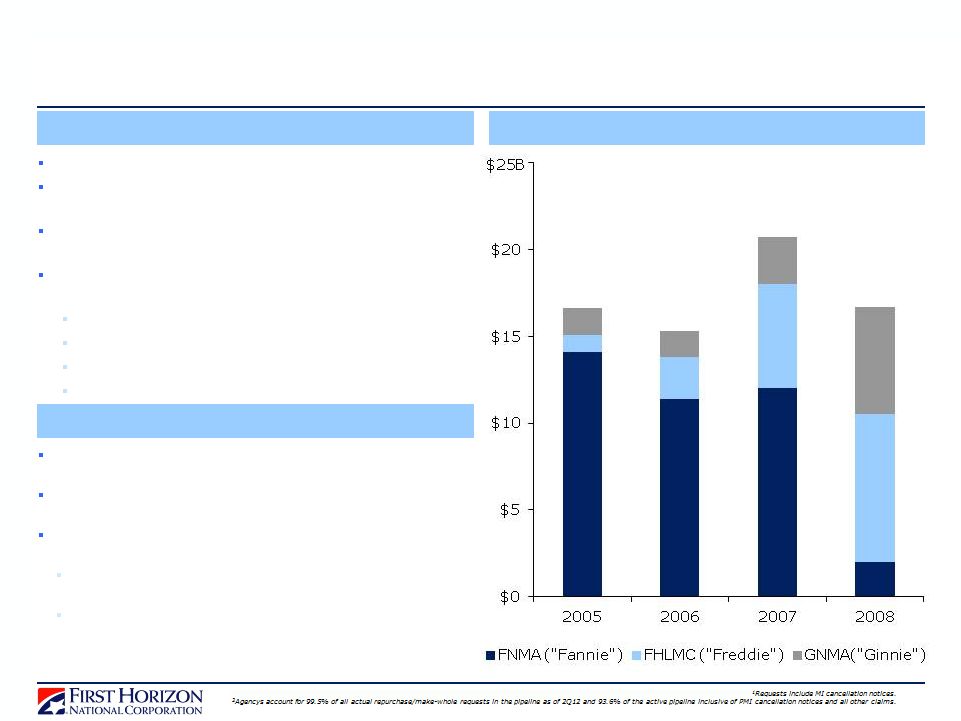

• Provisioning for repurchase and foreclosure losses was $250.0 million in second quarter compared to $49.3 million in first quarter

• The repurchase liability for first lien mortgage loans increased to $360.5 million in second quarter from $161.2 million in first quarter

• Second quarter provision reflects a change in estimate of FHN’s repurchase obligations for alleged breaches of reps and warranties related to mortgage loans sold to Fannie and Freddie

• Change in estimate reflects significant new information from Fannie including loans currently selected for review; information supporting anticipated future selections (primarily from seriously delinquent and liquidated loan pools); and asset quality statistics for loans sold to Fannie (primarily loans no longer serviced by FHN)

• Data utilized to extrapolate probable incurred losses related to loans sold to Freddie; Ginnie loans were not included in the extrapolation

• Unless GSE repurchase practices or outcomes change significantly, FHN expects that the mortgage repurchase reserve established as of the end of the second quarter will be sufficient for losses resulting from current pending and projected repurchase requests from Fannie and Freddie

• Active pipeline increased to $430.6 million from $380.3 million in prior quarter

• Repurchase/make whole requests were $363.4 million as of the end of second quarter and primarily relate to requests from Fannie/Freddie

• Cumulative average rescission rates ranging between 45 percent and 55 percent with cumulative average loss severities ranging between 50 percent and 60 percent

• Second quarter includes a $22.0 million loss accrual related to pending legal matters

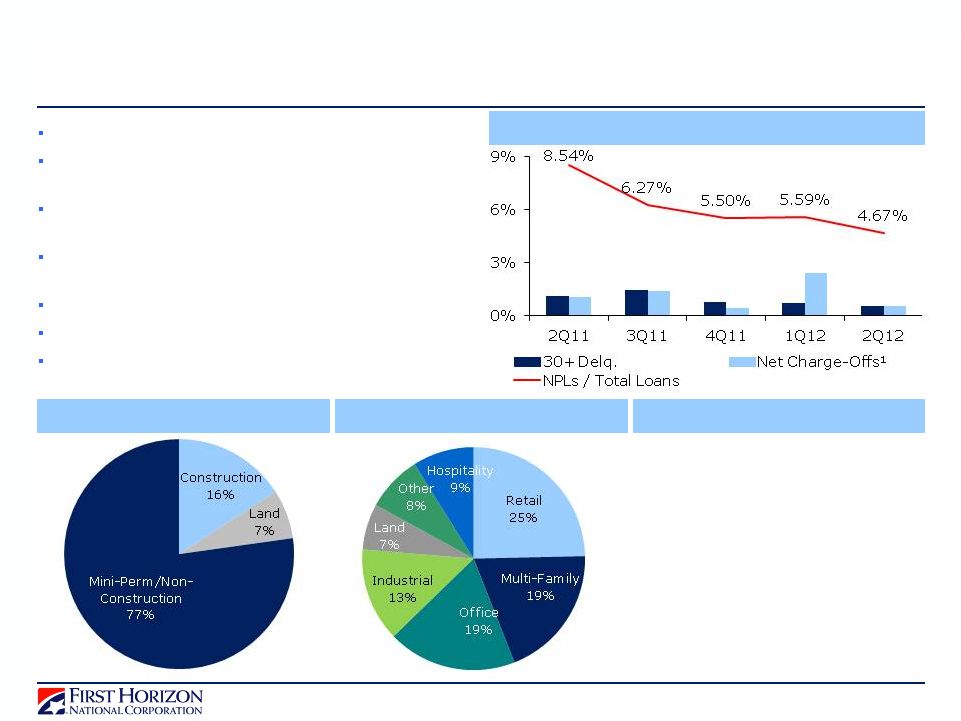

Asset Quality

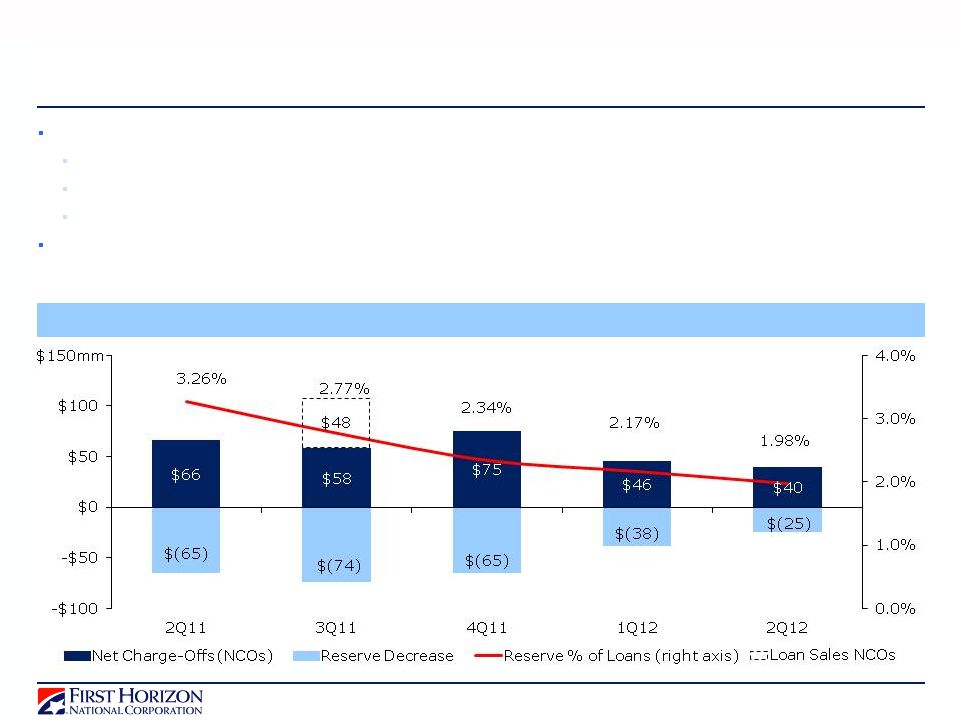

• Allowance as a percentage of loans ratio decreased to 198 basis points from 217 basis points in prior quarter

• Second quarter allowance reflects continued stabilization of loan portfolios and improving asset quality metrics

• Provision expense increased to $15.0 million during second quarter from $8.0 million in prior quarter

• Annualized net charge-offs decreased to 101 basis points of average loans from 116 basis points in prior quarter

• Net charge-offs were $40.0 million in second quarter compared to $46.3 million in prior quarter

• Commercial net charge-offs were flat at $11.0 million in second quarter

• Consumer net charge-offs were $29.0 million in second quarter, a $6.6 million decline from prior quarter

• Nonperforming assets (“NPAs”) decreased 8.69 percent from prior quarter; NPA ratio declined to 232 basis points from 256 basis points

• Foreclosed assets declined as disposition activity more than offset new inflow

• Troubled debt restructurings (“TDRs”) were $478.1 million at the end of second quarter compared with $429.6 million prior quarter

• Commercial Portfolio:

• Reserves decreased $13.4 million from prior quarter primarily driven by the C&I portfolio within the regional bank

• Reserve levels reflect continued aggregate improvement of the portfolio as upgrades outpaced downgrades

• Some upgrades within the TRUPs and bank stock portfolio; the lowest tier borrowers remain stressed and are closely monitored

• Consumer Portfolio:

• Reserves decreased $11.5 million in second quarter from $180.4 million in first quarter driven by consumer real estate portfolio within the non-strategic segment

• Balances of consumer real estate loans increased within the regional banking segment, partially offsetting runoff from the non-strategic portfolios

• Performance of the home equity portfolio improved in second quarter; 30+ delinquency rates decreased to 129 basis points from 142 basis points in prior quarter

• Reserves for the Permanent Mortgage portfolio decreased $3.5 million; Allowance to loans increased to 3.77 percent from 3.62 percent

• The decrease in reserves was driven by lower delinquencies as 30+ delinquency declined to 149 basis points from 216 basis points in the prior quarter

• The decline was mitigated by an increase in TDR reserves in second quarter

Taxes

• Second quarter includes approximately $7 million of positive effect from permanent tax credits

• Permanent credits primarily relate to affordable housing credits, life insurance, and tax-exempt interest

Capital and Liquidity

• Paid $0.01 per share dividend July 1, 2012

• Increased stock repurchase program to $200 million; repurchased shares costing $36.9 million in second quarter

• Repurchased shares costing $44.5 million in prior quarter

• Volume weighted average price for all share repurchases under the stock repurchase program of $8.28 per share (before $.03 per share broker commission)

• Capital ratios (regulatory capital ratios estimated based on period-end balances)

• 8.13% for tangible common equity to tangible assets

• 13.10% for Tier 1

• 15.94% for Total Capital

• 10.63% for Tier 1 Common

5

CHARGES FOR RESTRUCTURING, REPOSITIONING, & EFFICIENCY INITIATIVES

Quarterly, Unaudited

| (Thousands) | 2Q12 | 1Q12 | 4Q11 | 3Q11 | 2Q11 | |||||||||||||||

| By Income Statement Impact |

||||||||||||||||||||

| Noninterest income |

||||||||||||||||||||

| All other income and commissions (a) |

$ | (2,287 | ) | $ | — | $ | — | $ | 1,200 | $ | — | |||||||||

| Gain on divestiture |

— | 200 | — | — | — | |||||||||||||||

| Noninterest expense |

||||||||||||||||||||

| Employee compensation, incentives, and benefits |

2,191 | (152 | ) | 3,760 | 2,128 | 7,511 | ||||||||||||||

| Occupancy |

(219 | ) | 44 | 39 | 1,031 | 59 | ||||||||||||||

| Legal and professional fees |

— | 15 | (27 | ) | — | — | ||||||||||||||

| All other expense |

12 | 5 | 220 | 74 | 9,026 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total gain/(loss) before income taxes |

(4,271 | ) | 288 | (3,992 | ) | (2,033 | ) | (16,596 | ) | |||||||||||

| Income/(loss) from discontinued operations (b) |

485 | (96 | ) | (84 | ) | 8,951 | 441 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net impact resulting from restructuring, repositioning, and efficiency initiatives |

$ | (3,786 | ) | $ | 192 | $ | (4,076 | ) | $ | 6,918 | $ | (16,155 | ) | |||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (a) | Reflects adjustment due to contingencies associated with prior mortgage servicing sales. |

| (b) | Includes amounts related to Msaver, First Horizon Insurance, and Highland Capital. |

6

CONSOLIDATED SUMMARY RESULTS

Quarterly, Unaudited

| 2Q12 Change vs. | ||||||||||||||||||||||||||||

| (Dollars in thousands, except per share data) | 2Q12 | 1Q12 | 4Q11 | 3Q11 | 2Q11 | 1Q12 | 2Q11 | |||||||||||||||||||||

| Income Statement Highlights |

||||||||||||||||||||||||||||

| Net interest income |

$ | 172,675 | $ | 171,929 | $ | 178,877 | $ | 176,340 | $ | 172,860 | * | * | ||||||||||||||||

| Noninterest income |

153,842 | 202,113 | 180,993 | 185,725 | 187,592 | (24 | )% | (18 | )% | |||||||||||||||||||

| Securities gains/(losses), net |

5,065 | 328 | 203 | 35,162 | 1 | NM | NM | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total revenue |

331,582 | 374,370 | 360,073 | 397,227 | 360,453 | (11 | )% | (8 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Noninterest expense |

527,177 | 321,994 | 312,036 | 322,708 | 344,455 | 64 | % | 53 | % | |||||||||||||||||||

| Provision for loan losses |

15,000 | 8,000 | 10,000 | 32,000 | 1,000 | 88 | % | NM | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Income/(loss) before income taxes |

(210,595 | ) | 44,376 | 38,037 | 42,519 | 14,998 | NM | NM | ||||||||||||||||||||

| Provision/(benefit) for income taxes |

(88,178 | ) | 10,570 | (526 | ) | 8,367 | (4,167 | ) | NM | NM | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Income/(loss) from continuing operations |

(122,417 | ) | 33,806 | 38,563 | 34,152 | 19,165 | NM | NM | ||||||||||||||||||||

| Income/(loss) from discontinued operations, net of tax |

487 | (435 | ) | (752 | ) | 4,828 | 3,671 | NM | (87 | )% | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net income/(loss) |

(121,930 | ) | 33,371 | 37,811 | 38,980 | 22,836 | NM | NM | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net income attributable to noncontrolling interest |

2,844 | 2,844 | 2,871 | 2,875 | 2,844 | * | * | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net income/(loss) available to common shareholders |

$ | (124,774 | ) | $ | 30,527 | $ | 34,940 | $ | 36,105 | $ | 19,992 | NM | NM | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Common Stock Data |

||||||||||||||||||||||||||||

| Diluted EPS from continuing operations |

$ | (0.50 | ) | $ | 0.12 | $ | 0.13 | $ | 0.12 | $ | 0.06 | NM | NM | |||||||||||||||

| Diluted EPS |

$ | (0.50 | ) | $ | 0.12 | $ | 0.13 | $ | 0.14 | $ | 0.08 | NM | NM | |||||||||||||||

| Diluted shares (thousands) |

249,104 | 255,369 | 260,372 | 262,803 | 262,756 | (2 | )% | (5 | )% | |||||||||||||||||||

| Period-end shares outstanding (thousands) |

248,810 | 252,667 | 257,468 | 263,619 | 263,699 | (2 | )% | (6 | )% | |||||||||||||||||||

| Cash dividends declared per share |

$ | 0.01 | $ | 0.01 | $ | 0.01 | $ | 0.01 | $ | 0.01 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Balance Sheet Highlights (Period-End) |

||||||||||||||||||||||||||||

| Total loans, net of unearned income (Restricted—$ .1 billion) (a) |

$ | 16,185,763 | $ | 15,971,330 | $ | 16,397,127 | $ | 16,241,402 | $ | 16,061,646 | 1 | % | 1 | % | ||||||||||||||

| Total deposits |

16,117,443 | 16,935,170 | 16,213,009 | 15,698,255 | 15,896,027 | (5 | )% | 1 | % | |||||||||||||||||||

| Total assets (Restricted—$ .1 billion) (a) |

25,492,955 | 25,678,969 | 24,789,384 | 25,571,469 | 25,054,066 | (1 | )% | 2 | % | |||||||||||||||||||

| Total liabilities (Restricted—$ .1 billion) (a) |

22,978,549 | 23,004,796 | 22,104,747 | 22,828,239 | 22,372,684 | * | 3 | % | ||||||||||||||||||||

| Total equity |

2,514,406 | 2,674,173 | 2,684,637 | 2,743,230 | 2,681,382 | (6 | )% | (6 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Asset Quality Highlights |

||||||||||||||||||||||||||||

| Allowance for loan losses (Restricted—$ 6.0 million) (a) |

$ | 321,051 | $ | 346,016 | $ | 384,351 | $ | 449,645 | $ | 524,091 | (7 | )% | (39 | )% | ||||||||||||||

| Allowance / period-end loans |

1.98 | % | 2.17 | % | 2.34 | % | 2.77 | % | 3.26 | % | ||||||||||||||||||

| Net charge-offs |

$ | 39,965 | $ | 46,335 | $ | 75,294 | $ | 106,446 | $ | 66,037 | (14 | )% | (39 | )% | ||||||||||||||

| Net charge-offs (annualized) / average loans |

1.01 | % | 1.16 | % | 1.84 | % | 2.65 | % | 1.67 | % | ||||||||||||||||||

| Non-performing assets (NPA) (b) |

$ | 466,873 | $ | 511,320 | $ | 521,161 | $ | 582,572 | $ | 747,860 | (9 | )% | (38 | )% | ||||||||||||||

| NPA % (b) (c) |

2.32 | % | 2.56 | % | 2.57 | % | 3.02 | % | 4.09 | % | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Key Ratios & Other |

||||||||||||||||||||||||||||

| Return on average assets (annualized) (d) |

(1.96 | )% | 0.53 | % | 0.60 | % | 0.62 | % | 0.37 | % | ||||||||||||||||||

| Return on average common equity (annualized)(e) |

(21.06 | )% | 5.15 | % | 5.69 | % | 5.90 | % | 3.36 | % | ||||||||||||||||||

| Net interest margin(f) (g) |

3.16 | % | 3.12 | % | 3.23 | % | 3.23 | % | 3.20 | % | ||||||||||||||||||

| Fee income to total revenue(h) |

47.12 | % | 54.03 | % | 50.29 | % | 51.30 | % | 52.04 | % | ||||||||||||||||||

| Efficiency ratio(i) |

161.45 | % | 86.08 | % | 86.71 | % | 89.13 | % | 95.56 | % | ||||||||||||||||||

| Book value per common share |

$ | 8.92 | $ | 9.42 | $ | 9.28 | $ | 9.29 | $ | 9.05 | ||||||||||||||||||

| Tangible book value per common share(g) |

$ | 8.28 | $ | 8.78 | $ | 8.66 | $ | 8.68 | $ | 8.43 | ||||||||||||||||||

| Adjusted tangible common equity to risk weighted assets(g) |

9.96 | % | 10.79 | % | 10.73 | % | 11.09 | % | 11.05 | % | ||||||||||||||||||

| Full time equivalent employees |

4,619 | 4,629 | 4,718 | 4,812 | 5,036 | * | (8 | )% | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

NM - Not meaningful

* Amount is less than one percent.

Certain previously reported amounts have been reclassified to agree with current presentation.

| (a) | Restricted balances parenthetically presented are as of June 30, 2012. |

| (b) | In 2Q12, the process for identifying current junior liens behind delinquent or modified first liens for nonaccrual status was refined. Q1 consumer NPLs have been represented to agree with Q2 presentation. |

| (c) | NPAs related to the loan portfolio over period-end loans plus foreclosed real estate and other assets. |

| (d) | Calculated using net income. |

| (e) | Calculated using net income available to common shareholders. |

| (f) | Net interest margin is computed using total net interest income adjusted for FTE. |

| (g) | Refer to the Non-GAAP to GAAP Reconciliation on page 27 of this financial supplement. |

| (h) | Ratio excludes securities gains/(losses). |

| (i) | Noninterest expense divided by total revenue excluding securities gains/(losses). |

7

CONSOLIDATED INCOME STATEMENT

Quarterly, Unaudited

| 2Q12 Change vs. | ||||||||||||||||||||||||||||

| (Thousands) | 2Q12 | 1Q12 | 4Q11 | 3Q11 | 2Q11 | 1Q12 | 2Q11 | |||||||||||||||||||||

| Interest income |

$ | 200,735 | $ | 201,503 | $ | 209,715 | $ | 208,360 | $ | 206,757 | * | (3 | )% | |||||||||||||||

| Less: interest expense |

28,060 | 29,574 | 30,838 | 32,020 | 33,897 | (5 | )% | (17 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net interest income |

172,675 | 171,929 | 178,877 | 176,340 | 172,860 | * | * | |||||||||||||||||||||

| Provision for loan losses (a) |

15,000 | 8,000 | 10,000 | 32,000 | 1,000 | 88 | % | NM | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net interest income after provision for loan losses |

157,675 | 163,929 | 168,877 | 144,340 | 171,860 | (4 | )% | (8 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Noninterest income: |

||||||||||||||||||||||||||||

| Capital markets |

74,913 | 106,743 | 87,756 | 99,557 | 77,921 | (30 | )% | (4 | )% | |||||||||||||||||||

| Mortgage banking |

9,889 | 23,341 | 18,008 | 12,751 | 32,101 | (58 | )% | (69 | )% | |||||||||||||||||||

| Deposit transactions and cash management (b) |

30,123 | 28,741 | 31,349 | 35,701 | 34,726 | 5 | % | (13 | )% | |||||||||||||||||||

| Trust services and investment management |

6,477 | 5,808 | 5,822 | 6,086 | 6,684 | 12 | % | (3 | )% | |||||||||||||||||||

| Brokerage management fees and commissions |

8,759 | 8,496 | 7,572 | 9,576 | 7,662 | 3 | % | 14 | % | |||||||||||||||||||

| Insurance commissions |

830 | 568 | 1,399 | 739 | 764 | 46 | % | 9 | % | |||||||||||||||||||

| Securities gains/(losses), net (c) |

5,065 | 328 | 203 | 35,162 | 1 | NM | NM | |||||||||||||||||||||

| Gain on divestiture |

— | 200 | — | — | — | NM | * | |||||||||||||||||||||

| Other |

22,851 | 28,216 | 29,087 | 21,315 | 27,734 | (19 | )% | (18 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total noninterest income |

158,907 | 202,441 | 181,196 | 220,887 | 187,593 | (22 | )% | (15 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Adjusted gross income after provision for loan losses |

316,582 | 366,370 | 350,073 | 365,227 | 359,453 | (14 | )% | (12 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Noninterest expense: |

||||||||||||||||||||||||||||

| Employee compensation, incentives, and benefits |

149,616 | 175,458 | 149,013 | 153,540 | 151,160 | (15 | )% | (1 | )% | |||||||||||||||||||

| Repurchase and foreclosure provision (d) |

250,000 | 49,256 | 45,033 | 52,791 | 24,563 | NM | NM | |||||||||||||||||||||

| Operations services |

9,477 | 9,127 | 10,601 | 11,978 | 13,907 | 4 | % | (32 | )% | |||||||||||||||||||

| Occupancy |

11,486 | 12,119 | 12,168 | 13,523 | 13,061 | (5 | )% | (12 | )% | |||||||||||||||||||

| Legal and professional fees |

8,417 | 6,067 | 12,708 | 18,132 | 20,451 | 39 | % | (59 | )% | |||||||||||||||||||

| FDIC premium expense |

6,801 | 6,336 | 5,504 | 5,904 | 8,839 | 7 | % | (23 | )% | |||||||||||||||||||

| Computer software |

9,960 | 9,465 | 9,507 | 8,689 | 8,375 | 5 | % | 19 | % | |||||||||||||||||||

| Contract employment and outsourcing (e) |

10,844 | 11,115 | 12,514 | 14,352 | 8,142 | (2 | )% | 33 | % | |||||||||||||||||||

| Equipment rentals, depreciation, and maintenance |

7,789 | 7,616 | 7,748 | 8,795 | 8,481 | 2 | % | (8 | )% | |||||||||||||||||||

| Foreclosed real estate |

1,908 | 4,170 | 4,793 | 4,691 | 5,803 | (54 | )% | (67 | )% | |||||||||||||||||||

| Communications and courier |

4,484 | 4,499 | 4,384 | 4,428 | 5,069 | * | (12 | )% | ||||||||||||||||||||

| Miscellaneous loan costs |

1,298 | 1,327 | 1,354 | 959 | 859 | (2 | )% | 51 | % | |||||||||||||||||||

| Amortization of intangible assets |

979 | 973 | 1,000 | 1,004 | 1,006 | 1 | % | (3 | )% | |||||||||||||||||||

| Other (f) (g) |

54,118 | 24,466 | 35,709 | 23,922 | 74,739 | NM | (28 | )% | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total noninterest expense |

527,177 | 321,994 | 312,036 | 322,708 | 344,455 | 64 | % | 53 | % | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Income/(loss) before income taxes |

(210,595 | ) | 44,376 | 38,037 | 42,519 | 14,998 | NM | NM | ||||||||||||||||||||

| Provision/(benefit) for income taxes |

(88,178 | ) | 10,570 | (526 | ) | 8,367 | (4,167 | ) | NM | NM | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Income/(loss) from continuing operations |

(122,417 | ) | 33,806 | 38,563 | 34,152 | 19,165 | NM | NM | ||||||||||||||||||||

| Income/(loss) from discontinued operations, net of tax |

487 | (435 | ) | (752 | ) | 4,828 | 3,671 | NM | (87 | )% | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net income/(loss) |

(121,930 | ) | 33,371 | 37,811 | 38,980 | 22,836 | NM | NM | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net income attributable to noncontrolling interest |

2,844 | 2,844 | 2,871 | 2,875 | 2,844 | * | * | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net income/(loss) available to common shareholders |

$ | (124,774 | ) | $ | 30,527 | $ | 34,940 | $ | 36,105 | $ | 19,992 | NM | NM | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

NM - Not meaningful

* Amount is less than one percent.

Certain previously reported amounts have been reclassified to agree with current presentation.

| (a) | 3Q11 includes approximately $36 million of losses on sales of nonperforming loans. |

| (b) | Fees impacted by the Durbin Amendment which became effective in 4Q11 resulting in lower interchange income. |

| (c) | 2Q12 includes a $5.1 million gain on sale of venture capital investment; 3Q11 includes a $35.1 million gain associated with the sale of a portion of Visa Class B Shares. |

| (d) | 2Q12 includes $250.0 million charge to the repurchase and foreclosure provision primarily related to a revision in estimate based on new information received from a GSE. |

| (e) | Beginning in 3Q11, FHN transitioned to a new mortgage subservicer resulting in elevated base servicing costs. |

| (f) | 4Q11 includes an $8.3 million increase in derivative liabilities associated with prior sales of Visa shares related to the decline in the conversion ratio for Visa Class B shares. |

| (g) | 2Q12 includes $22.0 million loss accrual related to pending legal matters, $3.4 million in ancillary expenses associated with legacy mortgage wind-down activities, and $2.8 million related to the write-off of unrecoverable servicing advances; 2Q11 includes $36.7 million associated with a litigation settlement. |

8

OTHER INCOME AND OTHER EXPENSE

Quarterly, Unaudited

| 2Q12 Changes vs. | ||||||||||||||||||||||||||||

| (Thousands) | 2Q12 | 1Q12 | 4Q11 | 3Q11 | 2Q11 | 1Q12 | 2Q11 | |||||||||||||||||||||

| Other Income |

||||||||||||||||||||||||||||

| Bank owned life insurance |

$ | 4,659 | $ | 4,772 | $ | 4,764 | $ | 5,116 | $ | 4,920 | (2 | )% | (5 | )% | ||||||||||||||

| Bankcard income (a) |

5,705 | 5,615 | 7,259 | 5,258 | 5,151 | 2 | % | 11 | % | |||||||||||||||||||

| ATM interchange fees (b) |

2,669 | 2,556 | 2,655 | 3,709 | 3,791 | 4 | % | (30 | )% | |||||||||||||||||||

| Other service charges |

3,212 | 3,293 | 3,541 | 2,969 | 2,819 | (2 | )% | 14 | % | |||||||||||||||||||

| Electronic banking fees |

1,632 | 1,706 | 1,546 | 1,609 | 1,536 | (4 | )% | 6 | % | |||||||||||||||||||

| Letter of credit fees |

1,560 | 1,334 | 1,230 | 1,407 | 1,869 | 17 | % | (17 | )% | |||||||||||||||||||

| Deferred compensation (c) |

(1,020 | ) | 3,119 | 376 | (2,093 | ) | 221 | NM | NM | |||||||||||||||||||

| Other (d) |

4,434 | 5,821 | 7,716 | 3,340 | 7,427 | (24 | )% | (40 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total |

$ | 22,851 | $ | 28,216 | $ | 29,087 | $ | 21,315 | $ | 27,734 | (19 | )% | (18 | )% | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Other Expense |

||||||||||||||||||||||||||||

| Losses from litigation and regulatory matters (e) |

$ | 22,100 | $ | 153 | $ | 694 | $ | — | $ | 38,260 | NM | (42 | )% | |||||||||||||||

| Advertising and public relations |

3,153 | 4,250 | 4,965 | 4,571 | 3,558 | (26 | )% | (11 | )% | |||||||||||||||||||

| Low income housing expense |

4,214 | 4,608 | 5,974 | 4,712 | 4,973 | (9 | )% | (15 | )% | |||||||||||||||||||

| Other insurance and taxes |

3,130 | 3,199 | 3,395 | 3,352 | 3,507 | (2 | )% | (11 | )% | |||||||||||||||||||

| Travel and entertainment |

2,435 | 1,864 | 2,342 | 2,075 | 2,137 | 31 | % | 14 | % | |||||||||||||||||||

| Customer relations |

1,348 | 855 | 1,301 | 1,185 | 1,152 | 58 | % | 17 | % | |||||||||||||||||||

| Employee training and dues |

1,230 | 1,092 | 1,172 | 1,009 | 1,342 | 13 | % | (8 | )% | |||||||||||||||||||

| Supplies |

817 | 1,033 | 953 | 1,092 | 792 | (21 | )% | 3 | % | |||||||||||||||||||

| Bank examination costs |

800 | 799 | 1,127 | 1,138 | 1,117 | * | (28 | )% | ||||||||||||||||||||

| Loan insurance expense |

636 | 589 | 676 | 744 | 706 | 8 | % | (10 | )% | |||||||||||||||||||

| Federal services fees |

328 | 321 | 342 | 338 | 291 | 2 | % | 13 | % | |||||||||||||||||||

| Other (f) (g) |

13,927 | 5,703 | 12,768 | 3,706 | 16,904 | NM | (18 | )% | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total |

$ | 54,118 | $ | 24,466 | $ | 35,709 | $ | 23,922 | $ | 74,739 | NM | (28 | )% | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

NM - Not meaningful

* Amount is less than one percent.

| (a) | 4Q11 includes $2.0 million related to Visa volume incentives. |

| (b) | Fees primarily impacted by the Durbin Amendment which became effective in 4Q11 resulting in lower interchange income. |

| (c) | Amounts driven by market conditions and are mirrored by changes in deferred compensation expense which is included in employee compensation expense. |

| (d) | 1Q12 includes $2.3 million associated with resolution of a legal matter. 4Q11 includes $4.0 million of interest related to a tax refund. |

| (e) | 2Q12 includes $22.0 million loss accrual related to pending legal matters; 2Q11 includes $36.7 million associated with a litigation settlement. |

| (f) | 4Q11 includes an $8.3 million increase in derivative liabilities associated with prior sales of Visa shares related to the decline in the conversion ratio for Visa Class B shares. |

| (g) | 2Q12 includes $3.4 million in ancillary expenses associated with legacy mortgage wind-down activities and $2.8 million related to the write-off of unrecoverable servicing advances. |

9

CONSOLIDATED PERIOD-END BALANCE SHEET

Quarterly, Unaudited

| 2Q12 Changes vs. | ||||||||||||||||||||||||||||

| (Thousands) | 2Q12 | 1Q12 | 4Q11 | 3Q11 | 2Q11 | 1Q12 | 2Q11 | |||||||||||||||||||||

| Assets |

||||||||||||||||||||||||||||

| Investment securities |

$ | 3,264,866 | $ | 3,296,603 | $ | 3,066,272 | $ | 3,327,846 | $ | 3,230,477 | (1 | )% | 1 | % | ||||||||||||||

| Loans held-for-sale |

424,051 | 431,905 | 413,897 | 386,147 | 397,931 | (2 | )% | 7 | % | |||||||||||||||||||

| Loans, net of unearned income (Restricted—$.1 billion) (a) |

16,185,763 | 15,971,330 | 16,397,127 | 16,241,402 | 16,061,646 | 1 | % | 1 | % | |||||||||||||||||||

| Federal funds sold and securities purchased under agreements to resell |

525,504 | 614,705 | 443,588 | 719,400 | 598,000 | (15 | )% | (12 | )% | |||||||||||||||||||

| Interest-bearing cash (b) |

484,430 | 761,098 | 452,856 | 358,537 | 263,441 | (36 | )% | 84 | % | |||||||||||||||||||

| Trading securities |

1,361,717 | 1,238,041 | 988,217 | 1,227,197 | 1,196,380 | 10 | % | 14 | % | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total earning assets |

22,246,331 | 22,313,682 | 21,761,957 | 22,260,529 | 21,747,875 | * | 2 | % | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Cash and due from banks |

330,931 | 349,604 | 384,667 | 339,895 | 313,416 | (5 | )% | 6 | % | |||||||||||||||||||

| Capital markets receivables |

377,496 | 522,001 | 164,987 | 521,198 | 625,243 | (28 | )% | (40 | )% | |||||||||||||||||||

| Mortgage servicing rights, net |

129,291 | 142,956 | 144,069 | 150,803 | 186,958 | (10 | )% | (31 | )% | |||||||||||||||||||

| Goodwill |

134,242 | 134,242 | 133,659 | 133,659 | 135,683 | * | (1 | )% | ||||||||||||||||||||

| Other intangible assets, net |

24,659 | 25,638 | 26,243 | 27,243 | 28,384 | (4 | )% | (13 | )% | |||||||||||||||||||

| Premises and equipment, net |

311,753 | 314,903 | 321,253 | 326,667 | 330,392 | (1 | )% | (6 | )% | |||||||||||||||||||

| Real estate acquired by foreclosure (c) |

69,603 | 78,947 | 85,244 | 91,492 | 92,662 | (12 | )% | (25 | )% | |||||||||||||||||||

| Allowance for loan losses (Restricted—$6.0 million) (a) |

(321,051 | ) | (346,016 | ) | (384,351 | ) | (449,645 | ) | (524,091 | ) | (7 | )% | (39 | )% | ||||||||||||||

| Other assets (Restricted—$2.6 million) (a) |

2,189,700 | 2,143,012 | 2,151,656 | 2,169,628 | 2,117,544 | 2 | % | 3 | % | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total assets (Restricted—$.1 billion) (a) |

$ | 25,492,955 | $ | 25,678,969 | $ | 24,789,384 | $ | 25,571,469 | $ | 25,054,066 | (1 | )% | 2 | % | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Liabilities and Equity |

||||||||||||||||||||||||||||

| Deposits |

||||||||||||||||||||||||||||

| Savings |

$ | 5,979,874 | $ | 6,615,289 | $ | 6,624,405 | $ | 6,467,377 | $ | 6,382,963 | (10 | )% | (6 | )% | ||||||||||||||

| Other interest-bearing deposits |

3,565,873 | 3,500,445 | 3,193,697 | 3,096,621 | 2,784,787 | 2 | % | 28 | % | |||||||||||||||||||

| Time deposits |

1,109,163 | 1,142,249 | 1,173,375 | 1,210,661 | 1,277,905 | (3 | )% | (13 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total interest-bearing core deposits |

10,654,910 | 11,257,983 | 10,991,477 | 10,774,659 | 10,445,655 | (5 | )% | 2 | % | |||||||||||||||||||

| Noninterest-bearing deposits |

4,833,994 | 4,969,597 | 4,613,014 | 4,412,375 | 4,937,103 | (3 | )% | (2 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total core deposits (d) |

15,488,904 | 16,227,580 | 15,604,491 | 15,187,034 | 15,382,758 | (5 | )% | 1 | % | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Certificates of deposit $100,000 and more |

628,539 | 707,590 | 608,518 | 511,221 | 513,269 | (11 | )% | 22 | % | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total deposits |

16,117,443 | 16,935,170 | 16,213,009 | 15,698,255 | 15,896,027 | (5 | )% | 1 | % | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Federal funds purchased and securities sold under agreements to repurchase |

1,780,990 | 1,801,234 | 1,887,052 | 2,101,953 | 2,005,999 | (1 | )% | (11 | )% | |||||||||||||||||||

| Trading liabilities |

470,631 | 567,571 | 347,285 | 471,120 | 498,915 | (17 | )% | (6 | )% | |||||||||||||||||||

| Other short-term borrowings (e) |

1,094,179 | 181,570 | 172,550 | 621,998 | 187,902 | NM | NM | |||||||||||||||||||||

| Term borrowings (Restricted—$ .1 billion) (a) |

2,294,224 | 2,340,706 | 2,481,660 | 2,509,804 | 2,502,517 | (2 | )% | (8 | )% | |||||||||||||||||||

| Capital markets payables |

203,548 | 361,018 | 164,708 | 509,164 | 464,993 | (44 | )% | (56 | )% | |||||||||||||||||||

| Other liabilities |

1,017,534 | 817,527 | 838,483 | 915,945 | 816,331 | 24 | % | 25 | % | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total liabilities (Restricted—$ .1 billion) (a) |

22,978,549 | 23,004,796 | 22,104,747 | 22,828,239 | 22,372,684 | * | 3 | % | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Equity |

||||||||||||||||||||||||||||

| Common stock(f) |

155,506 | 157,917 | 160,918 | 164,762 | 164,812 | (2 | )% | (6 | )% | |||||||||||||||||||

| Capital surplus(f) |

1,528,161 | 1,560,343 | 1,601,346 | 1,641,878 | 1,638,423 | (2 | )% | (7 | )% | |||||||||||||||||||

| Undivided profits |

658,157 | 785,361 | 757,364 | 724,977 | 691,490 | (16 | )% | (5 | )% | |||||||||||||||||||

| Accumulated other comprehensive loss, net |

(122,583 | ) | (124,613 | ) | (130,156 | ) | (83,552 | ) | (108,508 | ) | (2 | )% | 13 | % | ||||||||||||||

| Noncontrolling interest(g) |

295,165 | 295,165 | 295,165 | 295,165 | 295,165 | * | * | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total equity |

2,514,406 | 2,674,173 | 2,684,637 | 2,743,230 | 2,681,382 | (6 | )% | (6 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total liabilities and equity |

$ | 25,492,955 | $ | 25,678,969 | $ | 24,789,384 | $ | 25,571,469 | $ | 25,054,066 | (1 | )% | 2 | % | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

NM - Not meaningful

* Amount is less than one percent.

| (a) | Restricted balances parenthetically presented are as of June 30, 2012. |

| (b) | Includes excess balances held at Fed. |

| (c) | 2Q12 includes $20.7 million of foreclosed assets related to government insured mortgages. |

| (d) | 2Q12 average core deposits were $15.6 billion. |

| (e) | 2Q12 includes increased FHLB borrowings as a result of deposit fluctuations and an increase in loans to mortgage companies near the end of the quarter. |

| (f) | Decreases in 2Q12, 1Q12 and 4Q11 relate to shares purchased under the share repurchase program. |

| (g) | Consists of preferred stock of subsidiary. |

10

CONSOLIDATED AVERAGE BALANCE SHEET

Quarterly, Unaudited

| 2Q12 Change vs. | ||||||||||||||||||||||||||||

| (Thousands) | 2Q12 | 1Q12 | 4Q11 | 3Q11 | 2Q11 | 1Q12 | 2Q11 | |||||||||||||||||||||

| Assets: |

||||||||||||||||||||||||||||

| Earning assets: |

||||||||||||||||||||||||||||

| Loans, net of unearned income: |

||||||||||||||||||||||||||||

| Commercial, financial, and industrial (C&I) |

$ | 7,712,551 | $ | 7,709,856 | $ | 7,740,802 | $ | 7,181,058 | $ | 6,867,893 | * | 12 | % | |||||||||||||||

| Income CRE |

1,236,016 | 1,255,713 | 1,295,079 | 1,308,059 | 1,362,459 | (2 | )% | (9 | )% | |||||||||||||||||||

| Residential CRE |

94,531 | 111,823 | 132,669 | 169,049 | 203,721 | (15 | )% | (54 | )% | |||||||||||||||||||

| Consumer real estate |

5,406,435 | 5,290,632 | 5,295,881 | 5,346,893 | 5,436,358 | 2 | % | (1 | )% | |||||||||||||||||||

| Permanent mortgage |

755,391 | 771,187 | 814,335 | 985,359 | 1,009,804 | (2 | )% | (25 | )% | |||||||||||||||||||

| Credit card and other |

276,017 | 279,150 | 289,189 | 292,800 | 299,904 | (1 | )% | (8 | )% | |||||||||||||||||||

| Restricted and secured real estate loans |

479,327 | 622,931 | 654,142 | 681,469 | 708,966 | (23 | )% | (32 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total loans, net of unearned income (Restricted - $ .1 billion) (a) (b) |

15,960,268 | 16,041,292 | 16,222,097 | 15,964,687 | 15,889,105 | (1 | )% | * | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Loans held-for-sale |

425,176 | 424,086 | 399,271 | 384,108 | 366,557 | * | 16 | % | ||||||||||||||||||||

| Investment securities: |

||||||||||||||||||||||||||||

| U.S. treasuries |

42,424 | 40,088 | 42,935 | 43,812 | 62,970 | 6 | % | (33 | )% | |||||||||||||||||||

| U.S. government agencies |

2,981,090 | 2,802,651 | 2,919,690 | 2,990,375 | 2,938,623 | 6 | % | 1 | % | |||||||||||||||||||

| States and municipalities |

18,005 | 18,070 | 17,681 | 19,365 | 23,869 | * | (25 | )% | ||||||||||||||||||||

| Other |

223,924 | 224,000 | 224,530 | 221,664 | 220,440 | * | 2 | % | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total investment securities |

3,265,443 | 3,084,809 | 3,204,836 | 3,275,216 | 3,245,902 | 6 | % | 1 | % | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Capital markets securities inventory |

1,327,596 | 1,277,372 | 1,263,427 | 1,250,249 | 1,235,642 | 4 | % | 7 | % | |||||||||||||||||||

| Mortgage banking trading securities |

22,841 | 25,797 | 26,927 | 30,320 | 32,263 | (11 | )% | (29 | )% | |||||||||||||||||||

| Other earning assets: |

||||||||||||||||||||||||||||

| Federal funds sold and securities purchased under agreements to resell |

632,019 | 632,972 | 641,464 | 660,048 | 653,984 | * | (3 | )% | ||||||||||||||||||||

| Interest-bearing cash (c) |

518,124 | 821,113 | 479,621 | 403,482 | 381,586 | (37 | )% | 36 | % | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total other earning assets |

1,150,143 | 1,454,085 | 1,121,085 | 1,063,530 | 1,035,570 | (21 | )% | 11 | % | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total earning assets (Restricted—$ .1 billion) (a) |

22,151,467 | 22,307,441 | 22,237,643 | 21,968,110 | 21,805,039 | (1 | )% | 2 | % | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Allowance for loan losses (Restricted—$ 8.2 million) (a) |

(336,642 | ) | (372,264 | ) | (424,774 | ) | (507,478 | ) | (567,923 | ) | (10 | )% | (41 | )% | ||||||||||||||

| Cash and due from banks (Restricted—$ 1.5 million) (a) |

337,366 | 351,760 | 337,755 | 346,100 | 343,162 | (4 | )% | (2 | )% | |||||||||||||||||||

| Capital markets receivables |

100,408 | 91,430 | 108,815 | 124,192 | 112,289 | 10 | % | (11 | )% | |||||||||||||||||||

| Premises and equipment, net |

312,313 | 317,621 | 323,569 | 328,172 | 324,584 | (2 | )% | (4 | )% | |||||||||||||||||||

| Other assets (Restricted—$ 3.5 million) (a) |

2,449,723 | 2,504,385 | 2,479,298 | 2,519,020 | 2,500,864 | (2 | )% | (2 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total assets (Restricted—$ .1 billion) (a) |

$ | 25,014,635 | $ | 25,200,373 | $ | 25,062,306 | $ | 24,778,116 | $ | 24,518,015 | (1 | )% | 2 | % | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Liabilities and equity: |

||||||||||||||||||||||||||||

| Interest-bearing liabilities: |

||||||||||||||||||||||||||||

| Interest-bearing deposits: |

||||||||||||||||||||||||||||

| Other interest-bearing deposits |

$ | 3,512,390 | $ | 3,246,658 | $ | 2,991,676 | $ | 2,900,808 | $ | 2,673,090 | 8 | % | 31 | % | ||||||||||||||

| Savings |

6,290,143 | 6,690,470 | 6,559,779 | 6,479,880 | 6,320,779 | (6 | )% | * | ||||||||||||||||||||

| Time deposits |

1,125,738 | 1,155,716 | 1,190,464 | 1,244,602 | 1,315,764 | (3 | )% | (14 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total interest-bearing core deposits |

10,928,271 | 11,092,844 | 10,741,919 | 10,625,290 | 10,309,633 | (1 | )% | 6 | % | |||||||||||||||||||

| Certificates of deposit $100,000 and more |

675,688 | 660,256 | 544,394 | 507,086 | 547,262 | 2 | % | 23 | % | |||||||||||||||||||

| Federal funds purchased and securities sold under agreements to repurchase |

1,879,252 | 2,003,566 | 2,170,222 | 2,081,379 | 2,130,832 | (6 | )% | (12 | )% | |||||||||||||||||||

| Capital markets trading liabilities |

602,344 | 614,084 | 629,019 | 626,982 | 620,726 | (2 | )% | (3 | )% | |||||||||||||||||||

| Other short-term borrowings |

377,075 | 182,083 | 362,579 | 284,163 | 340,015 | NM | 11 | % | ||||||||||||||||||||

| Term borrowings (Restricted—$ .1 billion) (a) |

2,317,247 | 2,457,291 | 2,506,088 | 2,491,227 | 2,499,794 | (6 | )% | (7 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total interest-bearing liabilities |

16,779,877 | 17,010,124 | 16,954,221 | 16,616,127 | 16,448,262 | (1 | )% | 2 | % | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Noninterest-bearing deposits |

4,696,844 | 4,623,457 | 4,519,590 | 4,546,876 | 4,574,342 | 2 | % | 3 | % | |||||||||||||||||||

| Capital markets payables |

73,312 | 71,180 | 68,662 | 102,831 | 79,463 | 3 | % | (8 | )% | |||||||||||||||||||

| Other liabilities |

786,886 | 814,417 | 785,356 | 789,190 | 735,786 | (3 | )% | 7 | % | |||||||||||||||||||

| Equity |

2,677,716 | 2,681,195 | 2,734,477 | 2,723,092 | 2,680,162 | * | * | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total liabilities and equity (Restricted—$ .1 billion) (a) |

$ | 25,014,635 | $ | 25,200,373 | $ | 25,062,306 | $ | 24,778,116 | $ | 24,518,015 | (1 | )% | 2 | % | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

NM - Not meaningful

* Amount is less than one percent.

| (a) | Restricted balances parenthetically presented are quarterly averages as of June 30, 2012. |

| (b) | Includes loans on nonaccrual status. |

| (c) | Includes excess balances held at Fed. |

11

CONSOLIDATED NET INTEREST INCOME (a)

Quarterly, Unaudited

| 2Q12 Changes vs. | ||||||||||||||||||||||||||||

| (Thousands) | 2Q12 | 1Q12 | 4Q11 | 3Q11 | 2Q11 | 1Q12 | 2Q11 | |||||||||||||||||||||

| Interest Income: |

||||||||||||||||||||||||||||

| Loans, net of unearned income (b) |

$ | 162,698 | $ | 163,070 | $ | 169,169 | $ | 163,774 | $ | 162,281 | * | * | ||||||||||||||||

| Loans held-for-sale |

3,628 | 3,738 | 3,859 | 5,126 | 3,267 | (3 | )% | 11 | % | |||||||||||||||||||

| Investment securities: |

||||||||||||||||||||||||||||

| U.S. treasuries |

39 | 66 | 67 | 66 | 88 | (41 | )% | (56 | )% | |||||||||||||||||||

| U.S. government agencies |

23,562 | 23,768 | 25,262 | 27,615 | 28,643 | (1 | )% | (18 | )% | |||||||||||||||||||

| States and municipalities |

63 | 76 | 99 | 116 | 197 | (17 | )% | (68 | )% | |||||||||||||||||||

| Other |

2,324 | 2,422 | 2,264 | 2,249 | 2,390 | (4 | )% | (3 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total investment securities |

25,988 | 26,332 | 27,692 | 30,046 | 31,318 | (1 | )% | (17 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Capital markets securities inventory |

9,204 | 8,934 | 9,789 | 10,141 | 10,479 | 3 | % | (12 | )% | |||||||||||||||||||

| Mortgage banking trading securities |

578 | 642 | 675 | 706 | 821 | (10 | )% | (30 | )% | |||||||||||||||||||

| Other earning assets: |

||||||||||||||||||||||||||||

| Federal funds sold and securities purchased under agreements to resell (c) |

115 | — | (32 | ) | (58 | ) | (93 | ) | NM | NM | ||||||||||||||||||

| Interest-bearing cash |

280 | 446 | 213 | 180 | 181 | (37 | )% | 55 | % | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total other earning assets |

395 | 446 | 181 | 122 | 88 | (11 | )% | NM | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Interest income |

$ | 202,491 | $ | 203,162 | $ | 211,365 | $ | 209,915 | $ | 208,254 | * | (3 | )% | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Interest Expense: |

||||||||||||||||||||||||||||

| Interest-bearing deposits: |

||||||||||||||||||||||||||||

| Other interest-bearing deposits |

$ | 1,655 | $ | 1,518 | $ | 1,407 | $ | 1,650 | $ | 1,638 | 9 | % | 1 | % | ||||||||||||||

| Savings |

4,744 | 5,619 | 5,921 | 6,773 | 7,018 | (16 | )% | (32 | )% | |||||||||||||||||||

| Time deposits |

5,541 | 5,916 | 6,363 | 7,096 | 7,783 | (6 | )% | (29 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total interest-bearing core deposits |

11,940 | 13,053 | 13,691 | 15,519 | 16,439 | (9 | )% | (27 | )% | |||||||||||||||||||

| Certificates of deposit $100,000 and more |

2,305 | 2,306 | 2,166 | 2,328 | 2,612 | * | (12 | )% | ||||||||||||||||||||

| Federal funds purchased and securities sold under agreements to repurchase |

1,114 | 1,223 | 1,269 | 1,159 | 1,237 | (9 | )% | (10 | )% | |||||||||||||||||||

| Capital markets trading liabilities |

2,843 | 2,515 | 3,363 | 3,703 | 4,102 | 13 | % | (31 | )% | |||||||||||||||||||

| Other short-term borrowings |

36 | 142 | 171 | 230 | 233 | (75 | )% | (85 | )% | |||||||||||||||||||

| Term borrowings |

9,822 | 10,335 | 10,178 | 9,081 | 9,274 | (5 | )% | 6 | % | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Interest expense |

28,060 | 29,574 | 30,838 | 32,020 | 33,897 | (5 | )% | (17 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net interest income—tax equivalent basis |

174,431 | 173,588 | 180,527 | 177,895 | 174,357 | * | * | |||||||||||||||||||||

| Fully taxable equivalent adjustment |

(1,756 | ) | (1,659 | ) | (1,650 | ) | (1,555 | ) | (1,497 | ) | 6 | % | 17 | % | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net interest income |

$ | 172,675 | $ | 171,929 | $ | 178,877 | $ | 176,340 | $ | 172,860 | * | * | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

NM - Not meaningful

* Amount is less than one percent.

Certain previously reported amounts have been reclassified to agree with current presentation.

| (a) | Net interest income adjusted to a fully taxable equivalent (“FTE”) basis. |

| (b) | Includes loans on nonaccrual status. |

| (c) | 4Q11, 3Q11 and 2Q11 driven by negative market rates on reverse repurchase agreements. |

12

CONSOLIDATED AVERAGE BALANCE SHEET: YIELDS AND RATES

Quarterly, Unaudited

| (Thousands) | 2Q12 | 1Q12 | 4Q11 | 3Q11 | 2Q11 | |||||||||||||||

| Assets: |

||||||||||||||||||||

| Earning assets (a): |

||||||||||||||||||||

| Loans, net of unearned income: |

||||||||||||||||||||

| Commercial loans |

3.92 | % | 3.90 | % | 3.95 | % | 3.84 | % | 3.90 | % | ||||||||||

| Retail loans |

4.33 | 4.32 | 4.42 | 4.37 | 4.31 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total loans, net of unearned income (b) |

4.09 | 4.08 | 4.15 | 4.08 | 4.09 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Loans held-for-sale |

3.41 | 3.53 | 3.87 | 5.34 | 3.57 | |||||||||||||||

| Investment securities: |

||||||||||||||||||||

| U.S. treasuries |

0.37 | 0.66 | 0.62 | 0.60 | 0.56 | |||||||||||||||

| U.S. government agencies |

3.16 | 3.39 | 3.46 | 3.69 | 3.90 | |||||||||||||||

| States and municipalities |

1.39 | 1.68 | 2.23 | 2.39 | 3.29 | |||||||||||||||

| Other |

4.15 | 4.33 | 4.03 | 4.06 | 4.34 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total investment securities |

3.18 | 3.41 | 3.46 | 3.67 | 3.86 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Capital markets securities inventory |

2.77 | 2.80 | 3.10 | 3.24 | 3.39 | |||||||||||||||

| Mortgage banking trading securities |

10.12 | 9.96 | 10.03 | 9.31 | 10.17 | |||||||||||||||

| Other earning assets: |

||||||||||||||||||||

| Federal funds sold and securities purchased under agreements to resell (c) |

.07 | — | (0.02 | ) | (0.03 | ) | (0.06 | ) | ||||||||||||

| Interest-bearing cash |

0.22 | 0.22 | 0.18 | 0.18 | 0.19 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total other earning assets |

0.14 | 0.12 | 0.06 | 0.05 | 0.03 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Interest income/total earning assets |

3.67 | % | 3.65 | % | 3.78 | % | 3.80 | % | 3.83 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Liabilities: |

||||||||||||||||||||

| Interest-bearing liabilities: |

||||||||||||||||||||

| Interest-bearing deposits: |

||||||||||||||||||||

| Other interest-bearing deposits |

0.19 | % | 0.19 | % | 0.19 | % | 0.23 | % | 0.25 | % | ||||||||||

| Savings |

0.30 | 0.34 | 0.36 | 0.41 | 0.45 | |||||||||||||||

| Time deposits |

1.98 | 2.06 | 2.12 | 2.26 | 2.37 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total interest-bearing core deposits |

0.44 | 0.47 | 0.51 | 0.58 | 0.64 | |||||||||||||||

| Certificates of deposit $100,000 and more |

1.37 | 1.40 | 1.58 | 1.82 | 1.91 | |||||||||||||||

| Federal funds purchased and securities sold under agreements to repurchase |

0.24 | 0.25 | 0.23 | 0.22 | 0.23 | |||||||||||||||

| Capital markets trading liabilities |

1.90 | 1.65 | 2.12 | 2.34 | 2.65 | |||||||||||||||

| Other short-term borrowings |

0.04 | 0.31 | 0.19 | 0.32 | 0.27 | |||||||||||||||

| Term borrowings (d) |

1.70 | 1.68 | 1.63 | 1.46 | 1.49 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Interest expense / total interest-bearing liabilities |

0.67 | 0.70 | 0.72 | 0.77 | 0.83 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest spread |

3.00 | % | 2.95 | % | 3.06 | % | 3.03 | % | 3.00 | % | ||||||||||

| Effect of interest-free sources used to fund earning assets |

0.16 | 0.17 | 0.17 | 0.20 | 0.20 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest margin |

3.16 | % | 3.12 | % | 3.23 | % | 3.23 | % | 3.20 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Yields are adjusted to a fully taxable equivalent (“FTE”) basis. Refer to the Non-GAAP to GAAP Reconciliation on page 27 for reconciliation of net interest income (GAAP) to net interest income adjusted for impact of FTE—(non-GAAP).

| (a) | Earning assets yields are expressed net of unearned income. |

| (b) | Includes loans on nonaccrual status. |

| (c) | 4Q11, 3Q11 and 2Q11 driven by negative market rates on reverse repurchase agreements. |

| (d) | Rates are expressed net of unamortized debenture cost for term borrowings. |

13

MORTGAGE SERVICING RIGHTS

Quarterly, Unaudited

| 2Q12 Changes vs. | ||||||||||||||||||||||||||||

| (Thousands) | 2Q12 | 1Q12 | 4Q11 | 3Q11 | 2Q11 | 1Q12 | 2Q11 | |||||||||||||||||||||

| First Liens |

||||||||||||||||||||||||||||

| Fair value beginning balance |

$ | 139,676 | $ | 140,724 | $ | 147,431 | $ | 183,530 | $ | 204,257 | ||||||||||||||||||

| Reductions due to loan payments |

(6,665 | ) | (5,499 | ) | (3,567 | ) | (5,286 | ) | (5,522 | ) | ||||||||||||||||||

| Reductions due to exercise of cleanup calls |

— | — | — | — | (195 | ) | ||||||||||||||||||||||

| Changes in fair value due to: |

||||||||||||||||||||||||||||

| Changes in valuation model inputs or assumptions (a) |

(6,855 | ) | 4,459 | (3,140 | ) | (30,813 | ) | (15,010 | ) | |||||||||||||||||||

| Other changes in fair value |

(71 | ) | (8 | ) | — | — | — | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Fair value ending balance |

$ | 126,085 | $ | 139,676 | $ | 140,724 | $ | 147,431 | $ | 183,530 | (10 | )% | (31 | )% | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Second Liens |

||||||||||||||||||||||||||||

| Fair value beginning balance |

$ | 222 | $ | 231 | $ | 241 | $ | 251 | $ | 259 | ||||||||||||||||||

| Reductions due to loan payments |

(7 | ) | (9 | ) | (10 | ) | (10 | ) | (8 | ) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Fair value ending balance |

$ | 215 | $ | 222 | $ | 231 | $ | 241 | $ | 251 | (3 | )% | (14 | )% | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| HELOC |

||||||||||||||||||||||||||||

| Fair value beginning balance |

$ | 3,058 | $ | 3,114 | $ | 3,131 | $ | 3,177 | $ | 3,232 | ||||||||||||||||||

| Reductions due to loan payments |

(79 | ) | (76 | ) | (54 | ) | (59 | ) | (59 | ) | ||||||||||||||||||

| Changes in fair value due to: |

||||||||||||||||||||||||||||

| Other changes in fair value |

12 | 20 | 37 | 13 | 4 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Fair value ending balance |

$ | 2,991 | $ | 3,058 | $ | 3,114 | $ | 3,131 | $ | 3,177 | (2 | )% | (6 | )% | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total Consolidated |

||||||||||||||||||||||||||||

| Fair value beginning balance |

$ | 142,956 | $ | 144,069 | $ | 150,803 | $ | 186,958 | $ | 207,748 | ||||||||||||||||||

| Reductions due to loan payments |

(6,751 | ) | (5,584 | ) | (3,631 | ) | (5,355 | ) | (5,589 | ) | ||||||||||||||||||

| Reductions due to exercise of cleanup calls |

— | — | — | — | (195 | ) | ||||||||||||||||||||||

| Changes in fair value due to: |

||||||||||||||||||||||||||||

| Changes in valuation model inputs or assumptions (a) |

(6,855 | ) | 4,459 | (3,140 | ) | (30,813 | ) | (15,010 | ) | |||||||||||||||||||

| Other changes in fair value |

(59 | ) | 12 | 37 | 13 | 4 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Fair value ending balance |

$ | 129,291 | $ | 142,956 | $ | 144,069 | $ | 150,803 | $ | 186,958 | (10 | )% | (31 | )% | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| (a) | Principally reflects changes in discount rates and prepayment speed assumptions, mostly due to changes in interest rates. |

14

BUSINESS SEGMENT HIGHLIGHTS

Quarterly, Unaudited

| 2Q12 change vs. | ||||||||||||||||||||||||||||

| (Thousands) | 2Q12 | 1Q12 | 4Q11 | 3Q11 | 2Q11 | 1Q12 | 2Q11 | |||||||||||||||||||||

| Regional Banking |

||||||||||||||||||||||||||||

| Net interest income |

$ | 147,204 | $ | 146,073 | $ | 149,597 | $ | 140,072 | $ | 135,583 | 1 | % | 9 | % | ||||||||||||||

| Noninterest income |

64,838 | 59,901 | 64,559 | 68,096 | 67,853 | 8 | % | (4 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total revenues |

212,042 | 205,974 | 214,156 | 208,168 | 203,436 | 3 | % | 4 | % | |||||||||||||||||||

| Provision/(provision credit) for loan losses |

4,828 | (7,426 | ) | (12,654 | ) | (22,698 | ) | (13,748 | ) | NM | NM | |||||||||||||||||

| Noninterest expense |

142,428 | 139,359 | 136,428 | 137,294 | 143,346 | 2 | % | (1 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Income before income taxes |

64,786 | 74,041 | 90,382 | 93,572 | 73,838 | (12 | )% | (12 | )% | |||||||||||||||||||

| Provision for income taxes |

23,362 | 27,013 | 33,287 | 34,592 | 27,075 | (14 | )% | (14 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net income |

$ | 41,424 | $ | 47,028 | $ | 57,095 | $ | 58,980 | $ | 46,763 | (12 | )% | (11 | )% | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Capital Markets |

||||||||||||||||||||||||||||

| Net interest income |

$ | 5,613 | $ | 5,684 | $ | 5,527 | $ | 5,552 | $ | 5,509 | (1 | )% | 2 | % | ||||||||||||||

| Noninterest income |

74,964 | 106,775 | 88,230 | 99,505 | 77,925 | (30 | )% | (4 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total revenues |

80,577 | 112,459 | 93,757 | 105,057 | 83,434 | (28 | )% | (3 | )% | |||||||||||||||||||

| Noninterest expense (a) |

60,886 | 80,302 | 66,721 | 77,168 | 103,383 | (24 | )% | (41 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Income/(loss) before income taxes |

19,691 | 32,157 | 27,036 | 27,889 | (19,949 | ) | (39 | )% | NM | |||||||||||||||||||

| Provision/(benefit) for income taxes |

7,421 | 12,240 | 10,302 | 10,656 | (7,756 | ) | (39 | )% | NM | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net income/(loss) |

$ | 12,270 | $ | 19,917 | $ | 16,734 | $ | 17,233 | $ | (12,193 | ) | (38 | )% | NM | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Corporate |

||||||||||||||||||||||||||||

| Net interest income/(expense) |

$ | (4,110 | ) | $ | (4,727 | ) | $ | (3,764 | ) | $ | (494 | ) | $ | 412 | 13 | % | NM | |||||||||||

| Noninterest income |

3,838 | 9,266 | 9,865 | 37,914 | 8,850 | (59 | )% | (57 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total revenues |

(272 | ) | 4,539 | 6,101 | 37,420 | 9,262 | NM | NM | ||||||||||||||||||||

| Noninterest expense |

19,374 | 22,521 | 29,244 | 19,013 | 36,287 | (14 | )% | (47 | )% | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Income/(loss) before income taxes |

(19,646 | ) | (17,982 | ) | (23,143 | ) | 18,407 | (27,025 | ) | (9 | )% | 27 | % | |||||||||||||||

| Provision/(benefit) for income taxes |

(12,922 | ) | (11,805 | ) | (22,464 | ) | 599 | (18,917 | ) | (9 | )% | 32 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||