Attached files

| file | filename |

|---|---|

| 8-K - WESTERN ALLIANCE BANCORPORATION 8-K - WESTERN ALLIANCE BANCORPORATION | a50344852.htm |

| EX-99.1 - EXHIBIT 99.1 - WESTERN ALLIANCE BANCORPORATION | a50344852_ex991.htm |

Exhibit 99.2

Western Alliance Bancorporation (NYSE: WAL) July 20, 2012 2nd Quarter 2012 Earnings Call

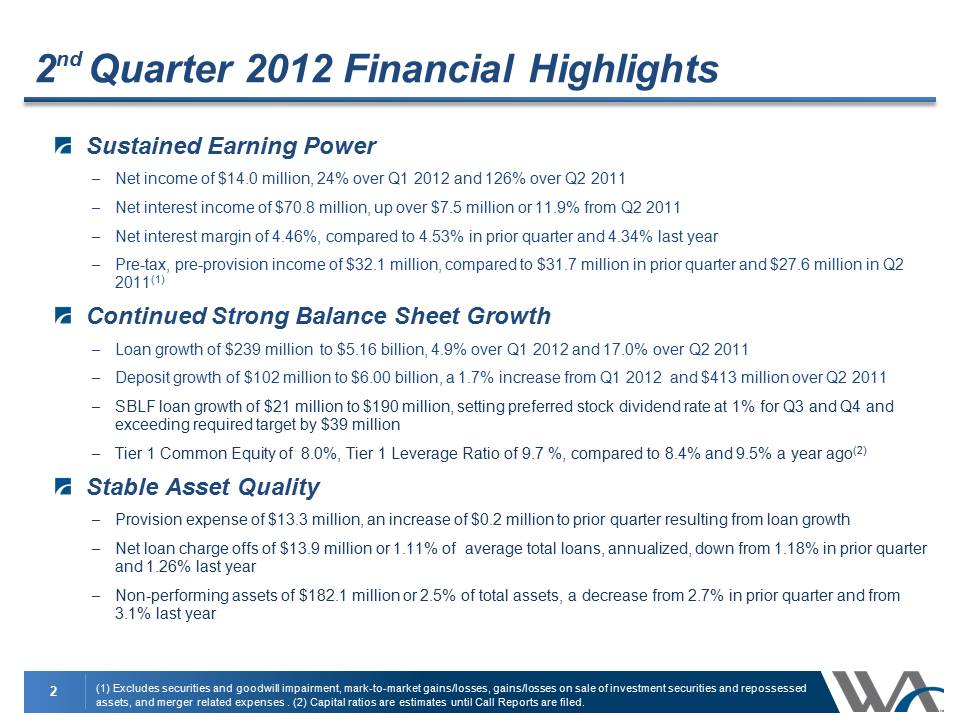

2nd Quarter 2012 Financial Highlights Sustained Earning Power– Net income of $14.0 million, 24% over Q1 2012 and 126% over Q2 2011– Net interest income of $70.8 million, up over $7.5 million or 11.9% from Q2 2011– Net interest margin of 4.46%, compared to 4.53% in prior quarter and 4.34% last year– Pre-tax, pre-provision income of $32.1 million, compared to $31.7 million in prior quarter and $27.6 million in Q22011(1)Continued Strong Balance Sheet Growth– Loan growth of $239 million to $5.16 billion, 4.9% over Q1 2012 and 17.0% over Q2 2012– Deposit growth of $102 million to $6.00 billion, a 1.7% increase from Q1 2012 and $413 million over Q2 2011– SBLF loan growth of $21 million to $190 million, setting preferred stock dividend rate at 1% for Q3 and Q4 and exceeding required target by $39 million– Tier 1 Common Equity of 8.0%, Tier 1 Leverage Ratio of 9.7 %, compared to 8.4% and 9.5% a year ago(2) Stable Asset Quality– Provision expense of $13.3 million, an increase of $0.2 million to prior quarter resulting from loan growth– Net loan charge offs of $13.9 million or 1.11% of average total loans, annualized, down from 1.18% in prior quarter and 1.26% last year– Non-performing assets of $182.1 million or 2.5% of total assets, a decrease from 2.7% in prior quarter and from 3.1% last year2

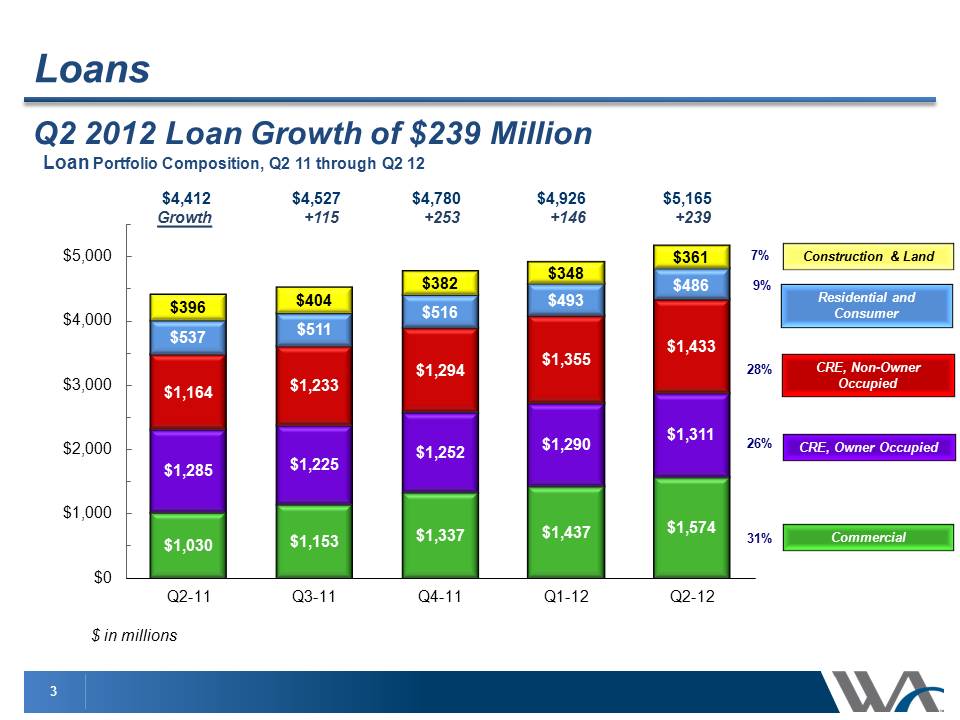

3 Loans Q2 2012 Loan Growth of $239 Million Loan Portfolio Composition, Q2 11 through Q2 12 $1,030 $1,153 $1,337 $1,437 $1,574 $1,285 $1,225 $1,252 $1,290 $1,311 $1,164 $1,233 $1,294 $1,355 $1,433 $537 $511 $516 $493 $486 $396 $404 $382 $348 $361 $0 $1,000 $2,000 $3,000 $4,000 $5,000 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Commercial CRE, Owner Occupied CRE, Non-Owner Occupied Construction & Land Residential and Consumer 31% 9% 28% 26% 7% $ in millions $4,412 $4,527 $4,780 $4,926 $5,165 Growth +115 +253 +146 +239

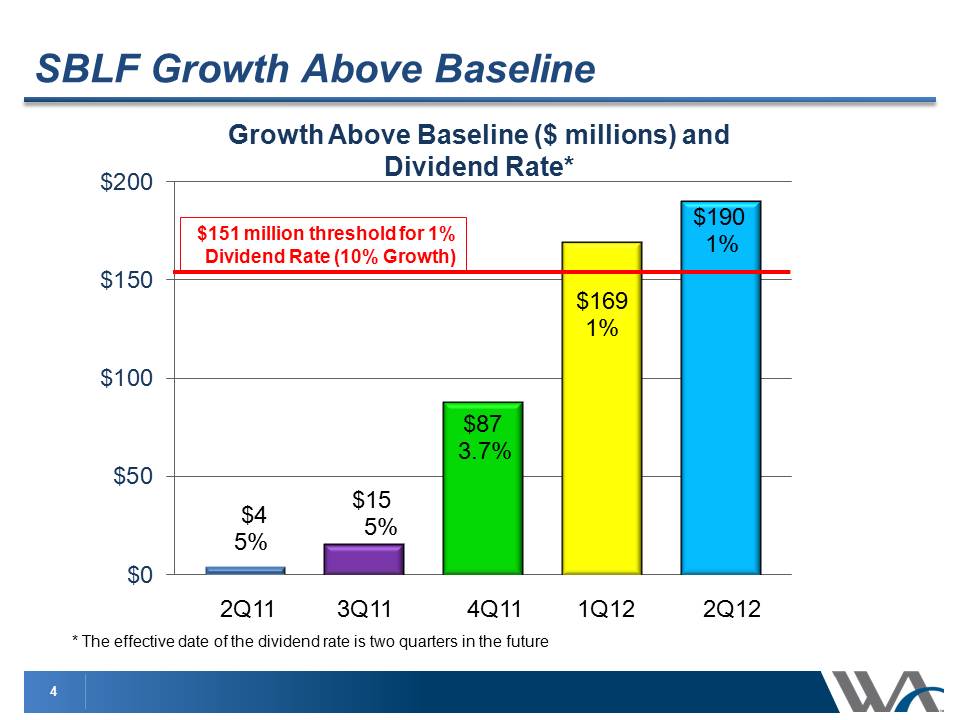

4 SBLF Growth Above Baseline $4 5% $15 5% $87 3.7% $169 1% $190 1% $0 $50 $100 $150 $200 $151 million threshold for 1% Dividend Rate (10% Growth) Growth Above Baseline ($ millions) and Dividend Rate* 2Q11 3Q11 4Q11 1Q12 2Q12 * The effective date of the dividend rate is two quarters in the future

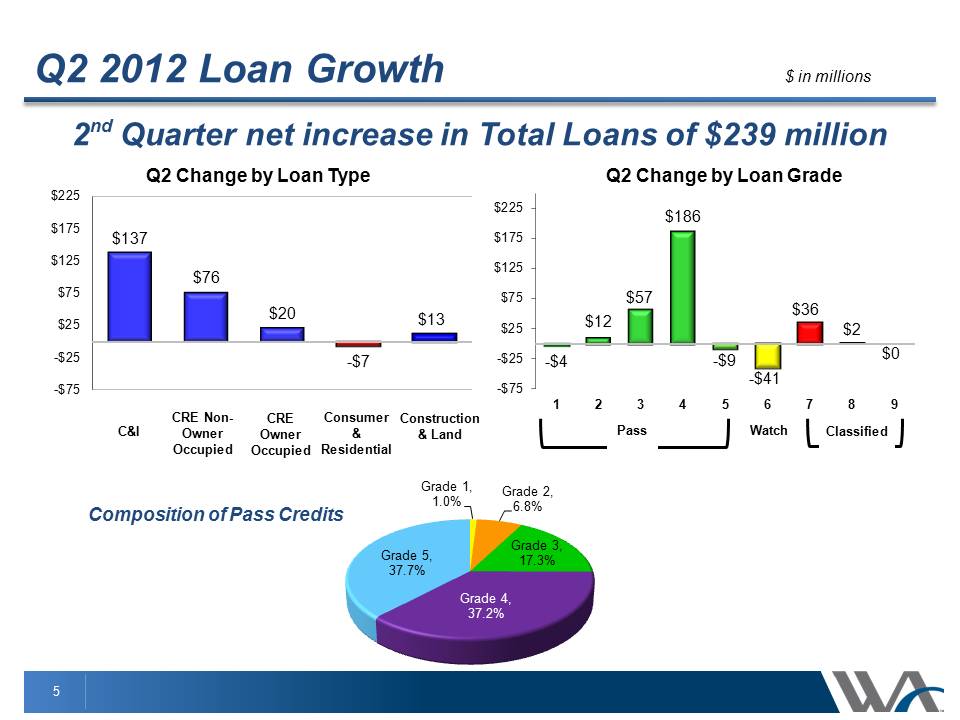

Q2 2012 Loan Growth 2nd Quarter net increase in Total Loans of $239 million $137 $76 $20-$7 $13-$75-$25 $25 $75 $125 $175 $225 Q2 Change by Loan Type-$4 $12 $57 $186-$9-$41 $36 $2 $0-$75-$25 $25 $75 $125 $175 $225 1 2 3 4 5 6 7 8 9 Q2 Change by Loan Grade Pass Watch Classified C&I CRE Non-Owner Occupied CRE Owner Occupied Consumer & Residential Construction & Land Composition of Pass Credits Grade 1, 1.0% Grade 2, 6.8% Grade 3, 17.3% Grade 4, 37.2% Grade 5, 37.7% $ in millions

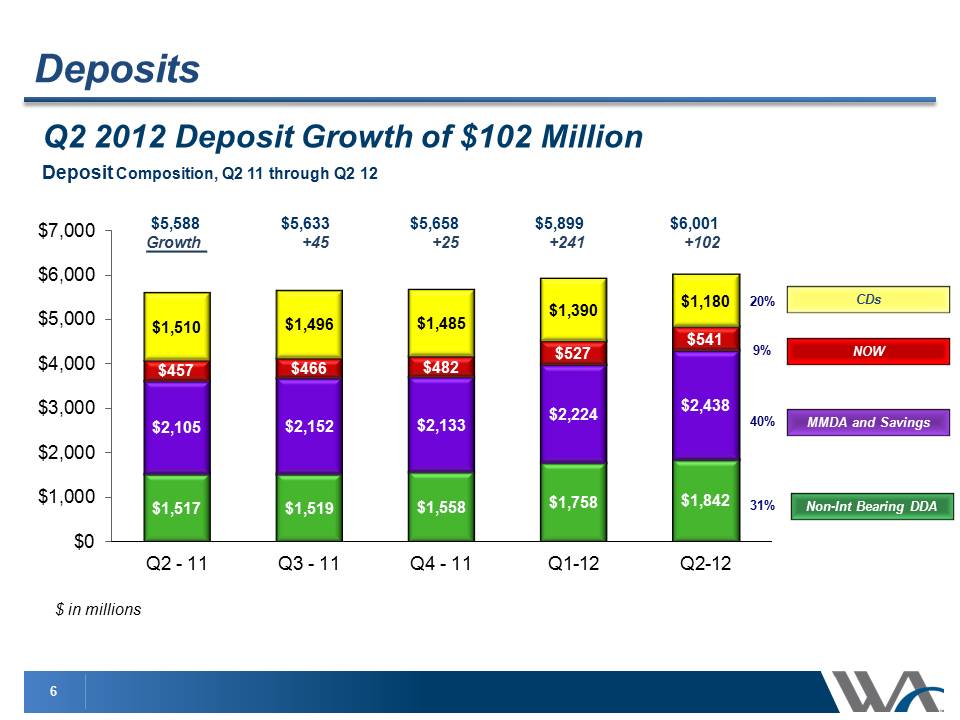

6 Deposits Q2 2012 Deposit Growth of $102 Million $1,517 $1,519 $1,558 $1,758 $1,842 $2,105 $2,152 $2,133 $2,224 $2,438 $457 $466 $482 $527 $541 $1,510 $1,496 $1,485 $1,390 $1,180 $0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000 Q2 - 11 Q3 - 11 Q4 - 11 Q1-12 Q2-12 Deposit Composition, Q2 11 through Q2 12 $5,588 $5,633 $5,658 $5,899 $6,001 Growth +45 +25 +241 +102 MMDA and Savings NOW CDs Non-Int Bearing DDA 9% 40% 31% 20% $ in millions

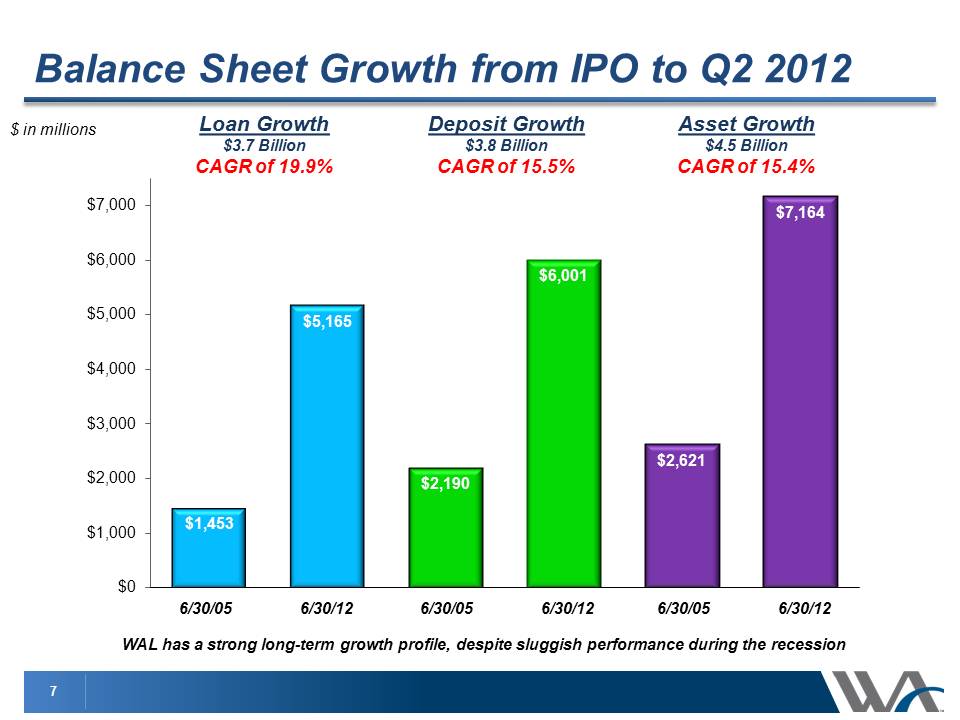

7 Balance Sheet Growth from IPO to Q2 2012 $1,453 $5,165 $2,190 $6,001 $2,621 $7,164 $0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000 $ in millions WAL has a strong long-term growth profile, despite sluggish performance during the recession Loan Growth $3.7 Billion CAGR of 19.9% Deposit Growth $3.8 Billion CAGR of 15.5% Asset Growth $4.5 Billion CAGR of 15.4% 6/30/05 6/30/12 6/30/05 6/30/12 6/30/05 6/30/12

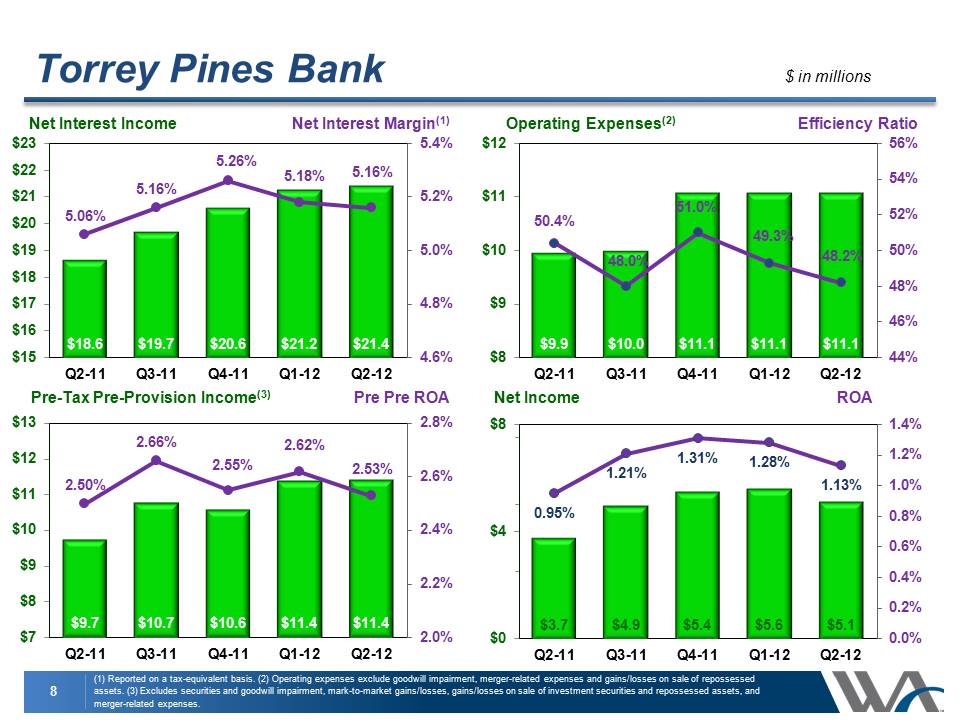

8 Torrey Pines Bank (1) Reported on a tax-equivalent basis. (2) Operating expenses exclude goodwill impairment, merger-related expenses and gains/losses on sale of repossessed assets. (3) Excludes securities and goodwill impairment, mark-to-market gains/losses, gains/losses on sale of investment securities and repossessed assets, and merger-related expenses. Net Interest Income Operating Expenses(2) Pre-Tax Pre-Provision Income(3) $ in millions Net Interest Margin(1) Efficiency Ratio Pre Pre ROA $9.7 $10.7 $10.6 $11.4 $11.4 2.50% 2.66% 2.55% 2.62% 2.53% 2.0% 2.2% 2.4% 2.6% 2.8% $7 $8 $9 $10 $11 $12 $13 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Net Income ROA $3.7 $4.9 $5.4 $5.6 $5.1 0.95% 1.21% 1.31% 1.28% 1.13% 0.0% 0.2% 0.4% 0.6% 0.8% 1.0% 1.2% 1.4% $0 $4 $8 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 $23 $22 $21 $20 $19 $18 $17 $16 $15 $12 $11 $10 $9 $8 $18.6 $19.7 $20.6 $21.2 $21.4 $9.9 $10.0 $11.1 5.06% 5.16% 5.26% 5.18% 5.16% 5.4% 5.2% 5.0% 4.8% 4.6% 50.4% 48.0% 51.0% 49.3% 48.2% 5.4% 5.2% 5.0% 4.8% 4.6% 56% 54% 52% 50% 48% 46% 44%

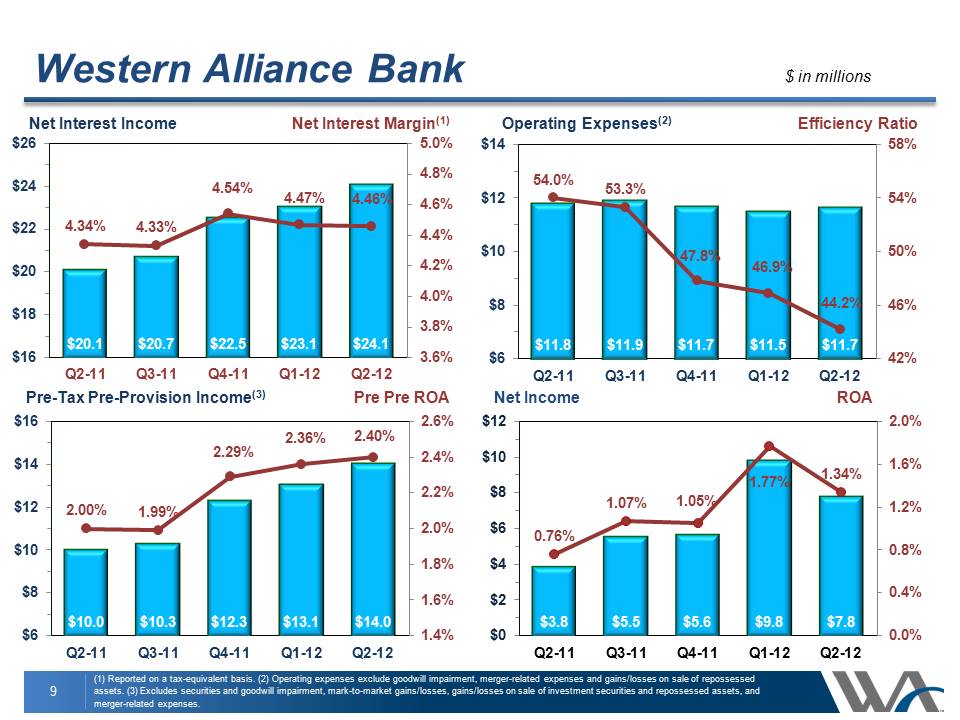

4.34% 4.33% 4.54% 4.47% 4.46% 3.6% 3.8% 4.0% 4.2% 4.4% 4.6% 4.8% 5.0% $16 $18 $20 $22 $24 $26Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 $11.8 $11.9 $11.7 $11.5 $11.7 54.0% 53.3% 47.8% 46.9% 44.2% 42% 46% 50% 54% 58% $6 $8 $10 $12 $14 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Western Alliance Bank (1) Reported on a tax-equivalent basis. (2) Operating expenses exclude goodwill impairment, merger-related expenses and gains/losses on sale of repossessed assets. (3) Excludes securities and goodwill impairment, mark-to-market gains/losses, gains/losses on sale of investment securities and repossessed assets, and merger-related expenses. Net Interest Income Operating Expenses(2) Pre-Tax Pre-Provision Income(3)$ in millions Net Interest Margin(1) Efficiency Ratio Pre Pre ROA $10.0 $10.3 $12.3 $13.1 $14.02.00% 1.99% 2.29%2.36% 2.40% 1.4% 1.6% 1.8% 2.0% 2.2% 2.4% 2.6% $6 $8 $10 $12 $14 $16Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Net Income ROA $3.8 $5.5 $5.6 $9.8 $7.8 0.76% 1.07% 1.05% 1.77% 1.34% 0.0% 0.4% 0.8% 1.2% 1.6% 2.0% $0 $2 $4 $6 $8 $10 $12 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12

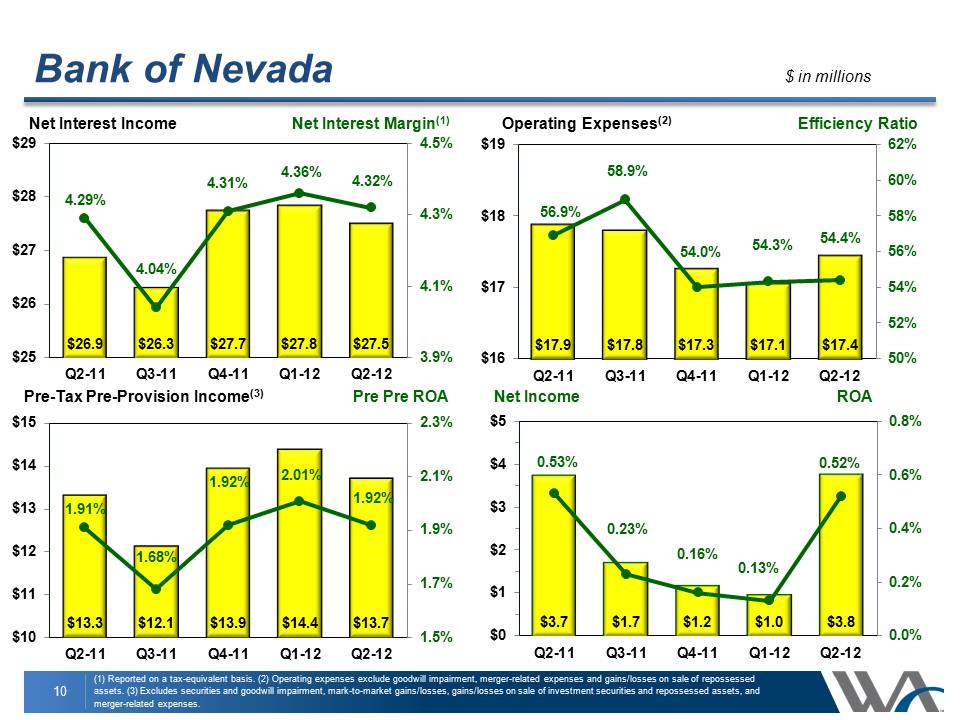

$26.9 $26.3 $27.7 $27.8 $27.5 4.29% 4.04% 4.31% 4.36% 4.32% 3.9%4.1%4.3%4.5%$25$26$27$28$29Q2-11Q3-11Q4-11Q1-12Q2-12$17.9 $17.8 $17.3 $17.1 $17.4 56.9% 58.9% 54.0% 54.3% 54.4% 50%52%54%56%58%60%62%$16$17$18$19Q2-11Q3-11Q4-11Q1-12Q2-12 Bank of Nevada (1) Reported on a tax-equivalent basis. (2) Operating expenses exclude goodwill impairment, merger-related expenses and gains/losses on sale of repossessed assets. (3) Excludes securities and goodwill impairment, mark-to-market gains/losses, gains/losses on sale of investment securities and repossessed assets, and merger-related expenses. Net Interest Income Operating Expenses(2) Pre-Tax Pre-Provision Income(3) $ in millions Net Interest Margin(1) Efficiency Ratio Pre Pre ROA $13.3 $12.1 $13.9 $14.4 $13.7 1.91% 1.68% 1.92% 2.01% 1.92% 1.5%1.7%1.9%2.1%2.3%$10$11$12$13$14$15Q2-11Q3-11Q4-11Q1-12Q2-12Net Income ROA $3.7 $1.7 $1.2 $1.0 $3.8 0.53% 0.23% 0.16% 0.13% 0.52% 0.0%0.2%0.4%0.6%0.8%$0$1$2$3$4$5Q2-11Q3-11Q4-11Q1-12Q2-1210

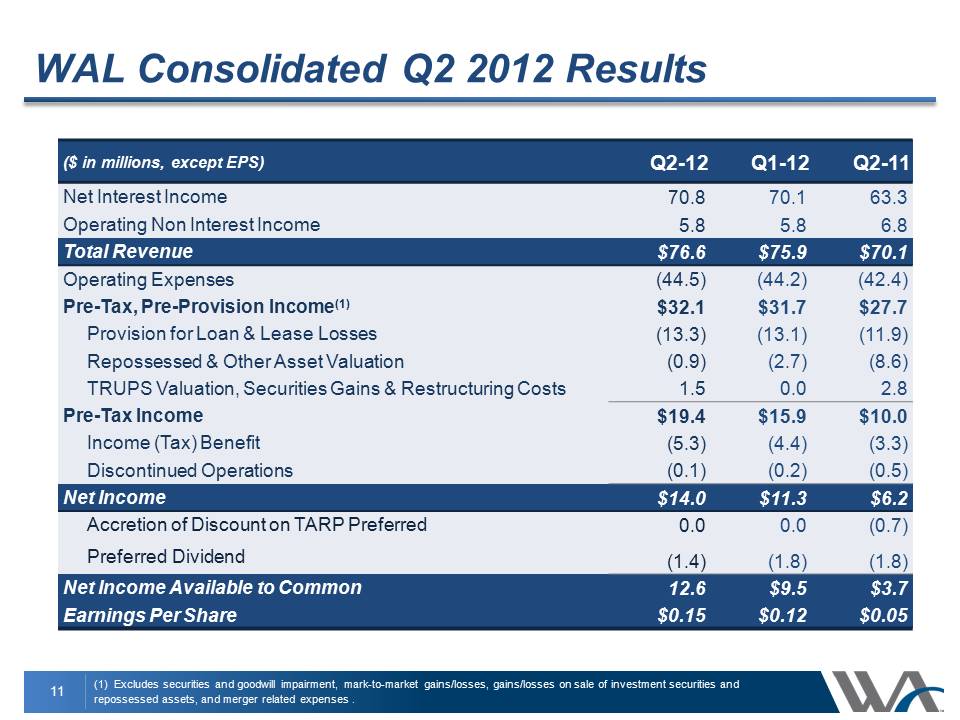

WAL Consolidated Q2 2012 Results (1) Excludes securities and goodwill impairment, mark-to-market gains/losses, gains/losses on sale of investment securities and repossessed assets, and merger related expenses . ($ in millions, except EPS) Q2-12 Q1-12 Q2-11 Net Interest Income 70.8 70.1 63.3 Operating Non Interest Income 5.8 5.8 6.8 Total Revenue $76.6 $75.9 $70.1 Operating Expenses (44.5) (44.2) (42.4)Pre-Tax, Pre-Provision Income(1) $32.1 $31.7 $27.7 Provision for Loan & Lease Losses (13.3) (13.1) (11.9) Repossessed & Other Asset Valuation (0.9) (2.7) (8.6) TRUPS Valuation, Securities Gains & Restructuring Costs 1.5 0.0 2.8 Pre-Tax Income $19.4 $15.9 $10.0 Income (Tax) Benefit (5.3) (4.4) (3.3)Discontinued Operations (0.1) (0.2) (0.5) Net Income $14.0 $11.3 $6.2 Accretion of Discount on TARP Preferred 0.0 0.0 (0.7) Preferred Dividend (1.4) (1.8) (1.8)

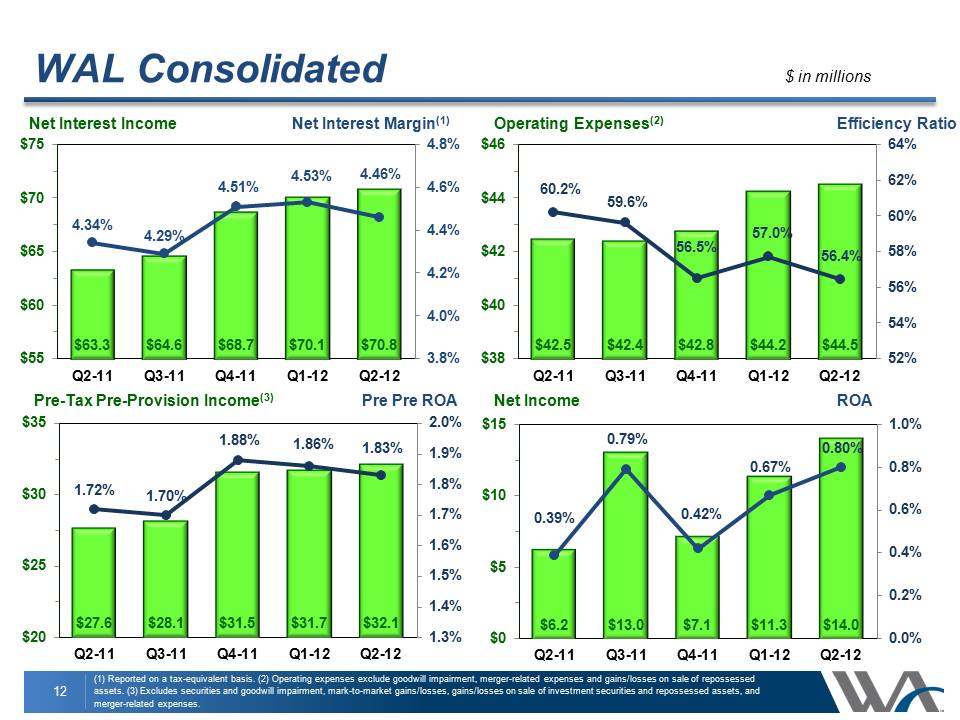

$63.3 $64.6 $68.7 $70.1 $70.8 4.34% 4.29% 4.51% 4.53% 4.46% 3.8%4.0%4.2%4.4%4.6%4.8%$55$60$65$70$75Q2-11Q3-11Q4-11Q1-12Q2-12$42.5 $42.4 $42.8 $44.2 $44.5 60.2% 59.6% 56.5% 57.0% 56.4% 52%54%56%58%60%62%64%$38$40$42$44$46Q2-11Q3-11Q4-11Q1-12Q2-12WAL Consolidated (1) Reported on a tax-equivalent basis. (2) Operating expenses exclude goodwill impairment, merger-related expenses and gains/losses on sale of repossessed assets. (3) Excludes securities and goodwill impairment, mark-to-market gains/losses, gains/losses on sale of investment securities and repossessed assets, and merger-related expenses. Net Interest Income Operating Expenses(2) Pre-Tax Pre-Provision Income(3) $ in millions Net Interest Margin(1) Efficiency Ratio Pre Pre ROA $27.6 $28.1 $31.5 $31.7 $32.1 1.72% 1.70% 1.88% 1.86% 1.83% 1.3%1.4%1.5%1.6%1.7%1.8%1.9%2.0%$20$25$30$35Q2-11Q3-11Q4-11Q1-12Q2-12Net Income ROA $6.2 $13.0 $7.1 $11.3 $14.0 0.39% 0.79% 0.42% 0.67% 0.80% 0.0%0.2%0.4%0.6%0.8%1.0%$0$5$10$15Q2-11Q3-11Q4-11Q1-12Q2-1212

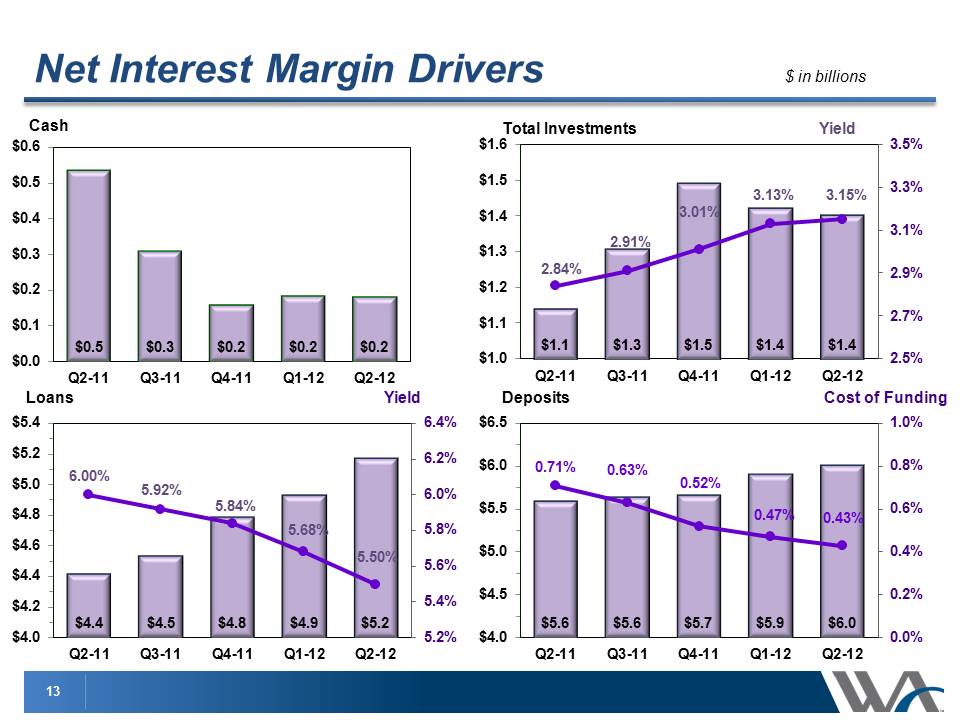

13 $0.5 $0.3 $0.2 $0.2 $0.2 $0.0 $0.1 $0.2 $0.3 $0.4 $0.5 $0.6 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 $1.1 $1.3 $1.5 $1.4 $1.4 2.84% 2.91% 3.01% 3.13% 3.15% 2.5% 2.7% 2.9% 3.1% 3.3% 3.5% $1.0 $1.1 $1.2 $1.3 $1.4 $1.5 $1.6 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Net Interest Margin Drivers Cash Loans $ in billions Yield $4.4 $4.5 $4.8 $4.9 $5.2 6.00% 5.92% 5.84% 5.68% 5.50% 5.2% 5.4% 5.6% 5.8% 6.0% 6.2% 6.4% $4.0 $4.2 $4.4 $4.6 $4.8 $5.0 $5.2 $5.4 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Deposits Cost of Funding $5.6 $5.6 $5.7 $5.9 $6.0 0.71% 0.63% 0.52% 0.47% 0.43% 0.0% 0.2% 0.4% 0.6% 0.8% 1.0% $4.0 $4.5 $5.0 $5.5 $6.0 $6.5 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Total Investments Yield

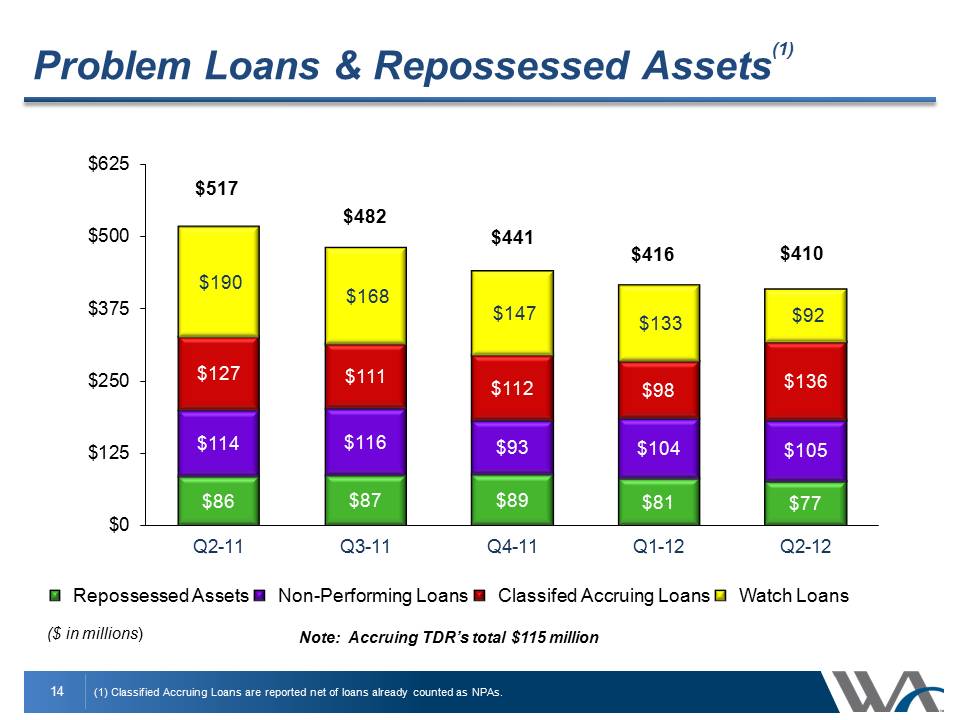

$190 $168 $147 $133 $92 $0 $125 $250 $375 $500 $625 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Repossessed Assets Non-Performing Loans Classifed Accruing Loans Watch Loans $482 $441 $416 $410 Problem Loans & Repossessed Assets(1) (1) Classified Accruing Loans are reported net of loans already counted as NPAs. ($ in millions) $517 Note: Accruing TDR’s total $115 million

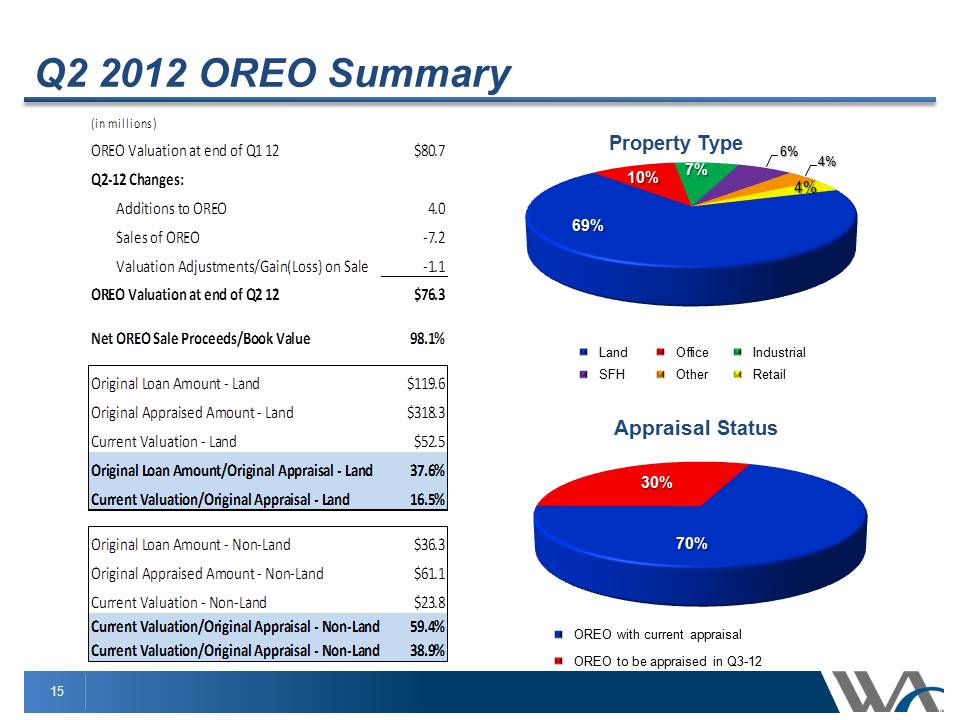

Q2 2012 OREO Summary 69% 10% 7% 6% 4% 4% Property Type Land Office Industrial SFH Other Retail 70% 30% Appraisal Status OREO with current appraisal OREO to be appraised in Q3-12 (in millions)OREO Valuation at end of Q1 12 $80.7 Q2‐12 Changes: Additions to OREO 4.0 Sales of OREO ‐7.2 Valuation Adjustments/Gain(Loss) on Sale ‐1.1 OREO Valuation at end of Q2 12 $76.3 Net OREO Sale Proceeds/Book Value 98.1% Original Loan Amount ‐ Land $119.6 Original Appraised Amount ‐ Land $318.3 Current Valuation ‐ Land $52.5 Original Loan Amount/Original Appraisal ‐ Land 37.6%Current Valuation/Original Appraisal ‐ Land 16.5% Original Loan Amount ‐ Non‐Land $36.3 Original Appraised Amount ‐ Non‐Land $61.1 Current Valuation ‐ Non‐Land $23.8 Current Valuation/Original Appraisal ‐ Non‐Land 59.4% Current Valuation/Original Appraisal ‐ Non‐Land 38.9%

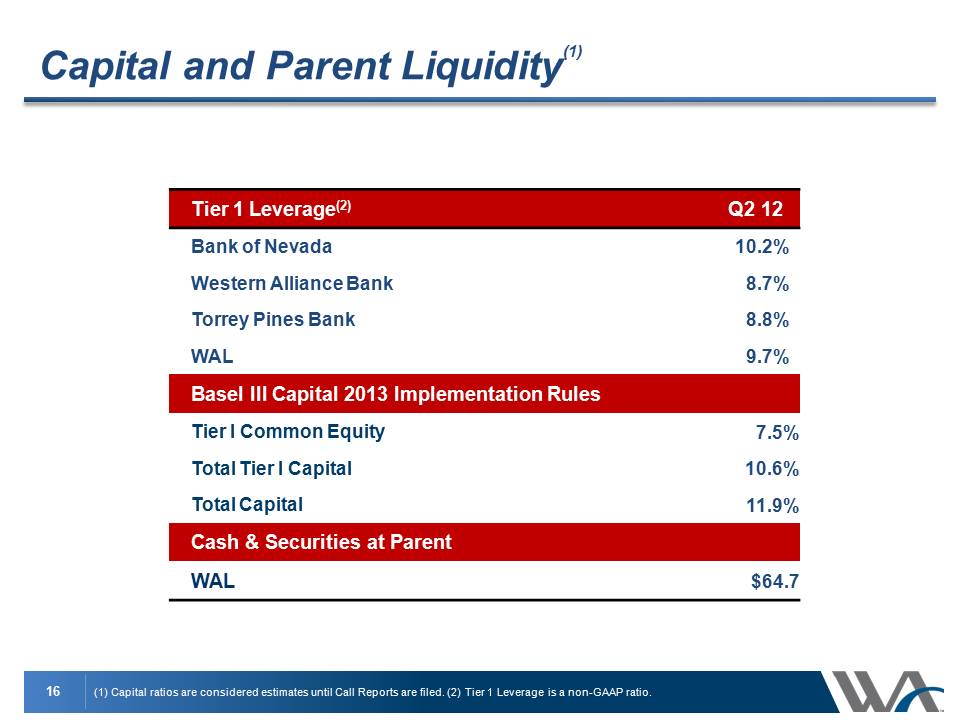

16 Capital and Parent Liquidity(1) (1) Capital ratios are considered estimates until Call Reports are filed. (2) Tier 1 Leverage is a non-GAAP ratio. Tier 1 Leverage(2) Q2 12 Bank of Nevada 10.2% Western Alliance Bank 8.7% Torrey Pines Bank 8.8% WAL 9.7% Basel III Capital 2013 Implementation Rules Tier I Common Equity 7.5% Total Tier I Capital 10.6% Total Capital 11.9% Cash & Securities at Parent WAL $64.7

17 Loan and deposit growth Net interest margin Efficiency ratio Asset quality Branch strategy Outlook 2nd Half 2012

18 Western Alliance Bancorporation Question & Answer

19 This presentation contains forward-looking statements that relate to expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. The forward-looking statements contained herein reflect our current views about future events and financial performance and are subject to risks, uncertainties, assumptions and changes in circumstances that may cause our actual results to differ significantly from historical results and those expressed in any forward-looking statement. Some factors that could cause actual results to differ materially from historical or expected results include: factors listed in the Company’s annual report on Form 10-K as filed with the Securities and Exchange Commission; changes in general economic conditions, either nationally or locally in the areas in which we conduct or will conduct our business; inflation, interest rate, market and monetary fluctuations; increases in competitive pressures among financial institutions and businesses offering similar products and services; higher defaults on our loan portfolio than we expect; changes in management’s estimate of the adequacy of the allowance for loan losses; legislative or regulatory changes or changes in accounting principles, policies or guidelines; supervisory actions by regulatory agencies which may limit our ability to pursue certain growth opportunities; management’s estimates and projections of interest rates and interest rate policy; the execution of our business plan; and other factors affecting the financial services industry generally or the banking industry in particular. We do not intend and disclaim any duty or obligation to update or revise any industry information or forward-looking statements set forth in this presentation to reflect new information, future events or otherwise. Forward-Looking Information