Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - MOSAIC CO | d382003d8k.htm |

| EX-99.1 - TRANSCRIPT OF CONFERENCE CALL - MOSAIC CO | d382003dex991.htm |

The Mosaic Company

Earnings

Conference

Call

–

4th

Quarter

Fiscal

2012

July 17th, 2012

Jim Prokopanko, President and Chief Executive Officer

Larry

Stranghoener,

Executive

Vice

President

and

Chief

Financial

Officer

Laura Gagnon, Vice President Investor Relations

Exhibit 99.2 |

This presentation contains forward-looking statements within the meaning of

the Private Securities Litigation Reform Act of 1995. Such statements

include, but are not limited to, statements about future financial and operating results. Such statements are based upon the

current beliefs and expectations of The Mosaic Company’s management and are

subject to significant risks and uncertainties. These risks and

uncertainties include but are not limited to the predictability and volatility of, and customer expectations about, agriculture,

fertilizer,

raw

material,

energy

and

transportation

markets

that

are

subject

to

competitive

and

other

pressures

and

economic

and

credit

market conditions; the level of inventories in the distribution channels for crop

nutrients; changes in foreign currency and exchange rates; international

trade risks; changes in government policy; changes in environmental and other governmental regulation, including

greenhouse gas regulation, implementation of the U.S. Environmental Protection

Agency’s numeric water quality standards for the discharge of

nutrients into Florida lakes and streams or possible efforts to reduce the flow of excess nutrients into the Gulf of Mexico;

further developments in judicial or administrative proceedings; difficulties or

delays in receiving, increased costs of or challenges to necessary

governmental permits or approvals; or increased financial assurance requirements; the effectiveness of the Company’s

processes

for

managing

its

strategic

priorities;

adverse

weather

conditions

affecting

operations

in

Central

Florida

or

the

Gulf

Coast

of

the United States, including potential hurricanes or excess rainfall; actual costs

of various items differing from management’s current estimates,

including, among others, asset retirement, environmental remediation, reclamation or other environmental regulation, or

Canadian resources taxes and royalties; accidents and other disruptions involving

Mosaic’s operations, including brine inflows at its Esterhazy,

Saskatchewan potash mine and other potential mine fires, floods, explosions, seismic events or releases of hazardous or

volatile chemicals, as well as other risks and uncertainties reported from time to

time in The Mosaic Company’s reports filed with the Securities and

Exchange Commission. Actual results may differ from those set forth in the forward-looking statements.

Safe Harbor Statement

Slide 2 |

Mosaic had an excellent year, despite macro challenges

Records set in FY 12

Highest Revenue

Highest Operating Cash Flow

ROIC

(1)

of 15%

>65% shareholder payout ratio

*FY11 includes $569 million gain from sale of Fosfertil

MACRO CHALLENGES

MOSAIC RESULTS

European uncertainty

Distributor de-stocking

Indian government subsidy

change

1. Non-GAAP, reconciliation on slide 24

Slide 3

DIVIDEND INCREASE

400% increase in targeted

dividend since February

$1.00 per share

$6.8

$9.9

$11.1

$1.3

$2.7

$2.6

2010

2011

2012

Net Sales and Operating Earnings

$ in billions

$0.8

$2.5

$1.9

2010

2011

2012

Net Income and Operating Cash Flow

$ in billions |

A

Year of Progress All-time best safety performance

Operational efficiencies

Expansion on plan

Premium products

Operational processes

South Fort Meade resolution

Potash Tolling agreement resolution

Formation offering completed

Debt restructure

Share repurchase

Dividend increase

Slide 4

Operational Excellence

Innovation

Issue Resolution

Capital Strength |

Financial Results Review |

Performance Reflects Grower Demand

Slide 6

Consolidated

Q4 FY12

Q4 FY12

vs.

Q4 FY11

Q4 FY12

vs.

Q3 FY12

Revenue

$2.8 billion

(1)%

29%

Gross Profit

$834 million

(16)%

60%

Operating Cash

Flow

$1.2 billion

28%

208% |

Earnings

Slide 7

Reported Earnings

($ in million except per share)

Q4 FY12

Earnings Before Taxes

$689

Net Earnings

$507

Earnings per share (diluted)

$1.19

Impact of Notable Items

$(0.06) |

Potash Segment Highlights

Slide 8

In millions, except MOP price

Q4 FY12

Q3 FY12

Q4 FY11

Net sales

$1,037

$553

$982

Gross Margin

$514

$270

$516

Percent of net sales

50%

49%

53%

Operating earnings

$464

$234

$469

Sales volumes

2.0

1.1

2.2

Production volume

1.9

1.8

2.2

Production operating rate

85%

79%

95%

Avg MOP selling price

$455

$453

$404

Fourth quarter highlights:

Volumes and prices reflect long North American spring season offset by limited

dealer restocking o

Sales

volumes

negatively

impacted

by

Canadian

rail

strike

–

approximately

100,000

tonnes

(timing

issue)

Operating rates increased later in the quarter to prepare for normal summer

maintenance o

Mosaic inventory levels are primarily standard grades, while blend grades remains

limited •

Gross margins were impacted by increased brine

management expenses, mark-to-market on

derivatives and higher depreciation |

Phosphates Segment Highlights

Slide 9

In millions, except DAP price

Q4 FY12

Q3 FY12

Q4 FY11

Net sales

$1,789

$1,652

$1,882

Gross Margin

$322

$259

$479

Percent of net sales

18%

16%

25%

Operating earnings

$224

$190

$370

Sales volumes

2.9

2.6

2.8

NA production volume

(a)

2.1

2.0

2.1

Finished product operating rate

86%

81%

86%

Avg DAP selling price

$494

$536

$574

(a)

Includes crop nutrient dry concentrates and animal feed ingredients

Fourth quarter highlights:

Average realized price declined, with upward trends during the quarter

Very

strong

volumes,

with

shipments

to

South

and

Central

America

replacing

Indian

sales

North

America

sales

included

summer

fill

volumes

Margins exceeded guidance due to intra-quarter demand-driven price

increases Operating earnings includes an asset retirement obligation

adjustment of $21 million |

Category

Guidance

–

Fiscal

2013

Potash

Q1 Sales volume 1.8 –

2.2 million tonnes

Q1 MOP selling price $415 –

$440 per tonne

Q1 Operating rate above 70 percent

Phosphates

Q1 Sales volume 2.5 –

2.8 million tonnes

Q1 DAP selling price $510 -

$535 per tonne

Q1 Operating rate above 75 percent

Capital Expenditures

$1.5 -

$1.8 billion

Canadian Resource Taxes and Royalties

$320 –

$380 million

SG&A

$420 –

$445 million

Effective Tax Rate

Upper 20 percent range

Financial Guidance Summary

Slide 10 |

Disciplined Capital Allocation

1.

Expansion Capital

2.

Potential Investments

3.

Return to shareholders

CAPITAL MANAGEMENT

Maximize shareholder value

through our capital policy

We are confident in our ability to generate significant cash

for investment in our business and shareholder distributions.

Slide 11

Share repurchases allowed by end

of FY13

0.3

0.4

0.8

0.9

1.3

1.6

0.7

2.5

1.2

1.4

2.4

2.7

07

08

09

10

11

12

OPERATING CASH FLOW AND CAPEX

$ IN BILLIONS |

Fiscal FY13 Outlook |

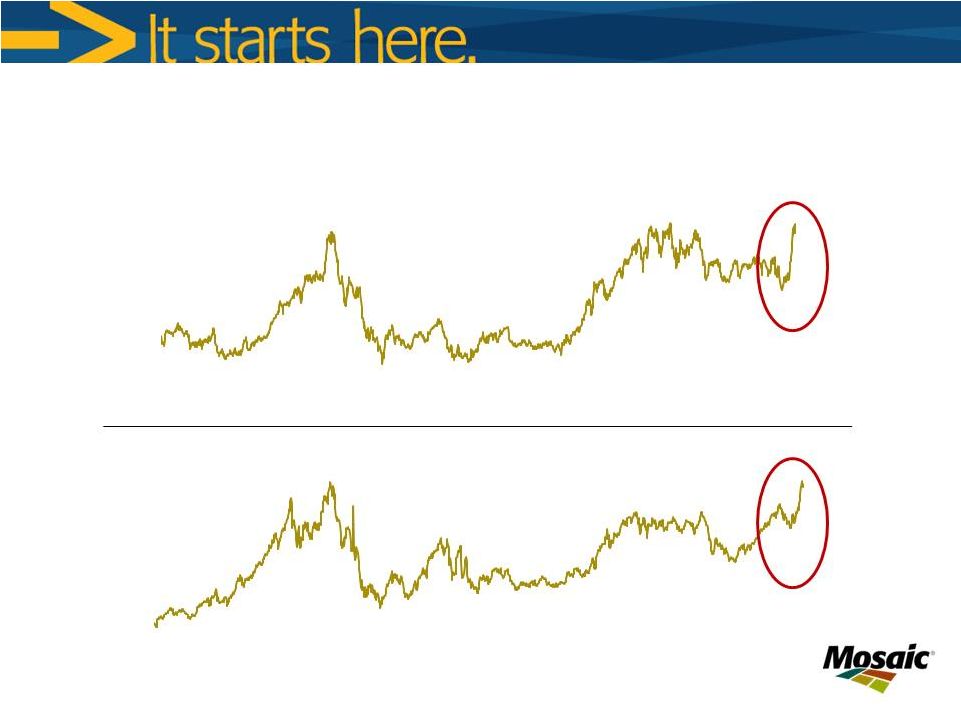

Recent commodity price jumps highlight delicate nature of global

food security

Slide 13

2.5

3.5

4.5

5.5

6.5

7.5

07

08

09

10

11

12

$ BU

Corn Price

Daily Close of Front Month Futures Contract

Source: CME

6.0

8.0

10.0

12.0

14.0

16.0

07

08

09

10

11

12

$ BU

Soybean Price

Daily Close of Front Month Futures Contract

Source: CME |

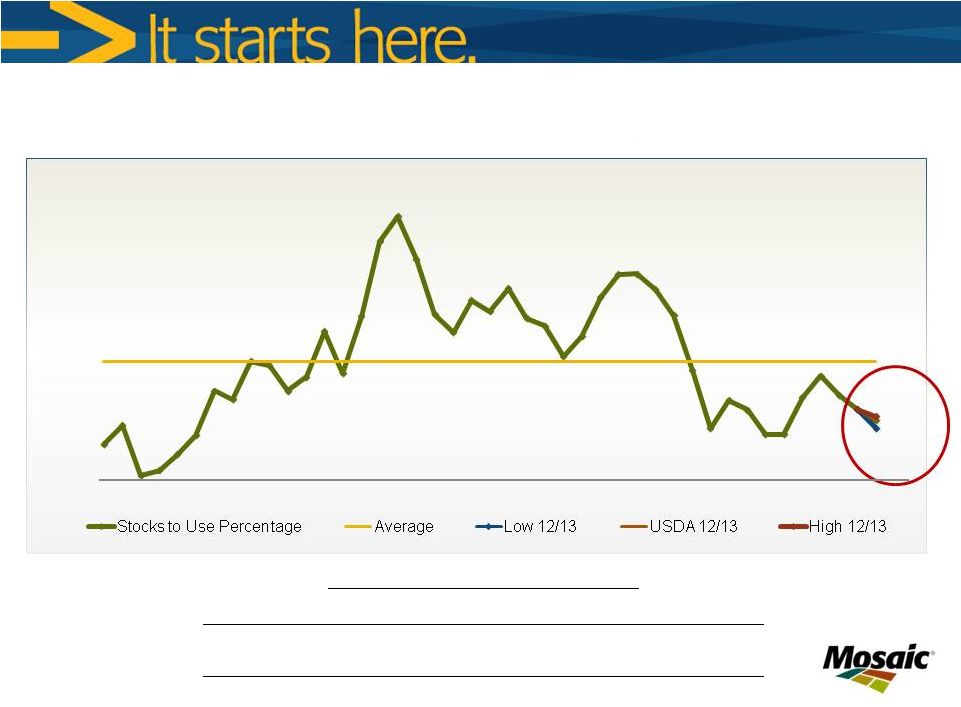

Global stock to use below historical average

Source: USDA and Mosaic

Slide 14

2012/13 Grain and Oilseed Scenario Assumptions

Low

USDA

High

Harvested Area Change

1.35%

1.35%

1.35%

Yield Deviation from Trend *

-0.08

-0.06

-0.04

Demand Growth

1.43%

1.63%

1.83%

* Largest deviation from the 12-year trend 2000-2011 in MT HA

18.4%

18.7%

17.9%

14%

19%

24%

29%

34%

70

72

74

76

78

80

82

84

86

88

90

92

94

96

98

00

02

04

06

08

10

12

WORLD GRAIN AND OILSEED STOCKS TO USE RATIO |

Supply uncertainty

Low inventories

Phosphates: A tight market

INDUSTRY DYNAMICS

MOSAIC

STRENGTHS

Mine productivity

Ammonia manufacturing

Premium products

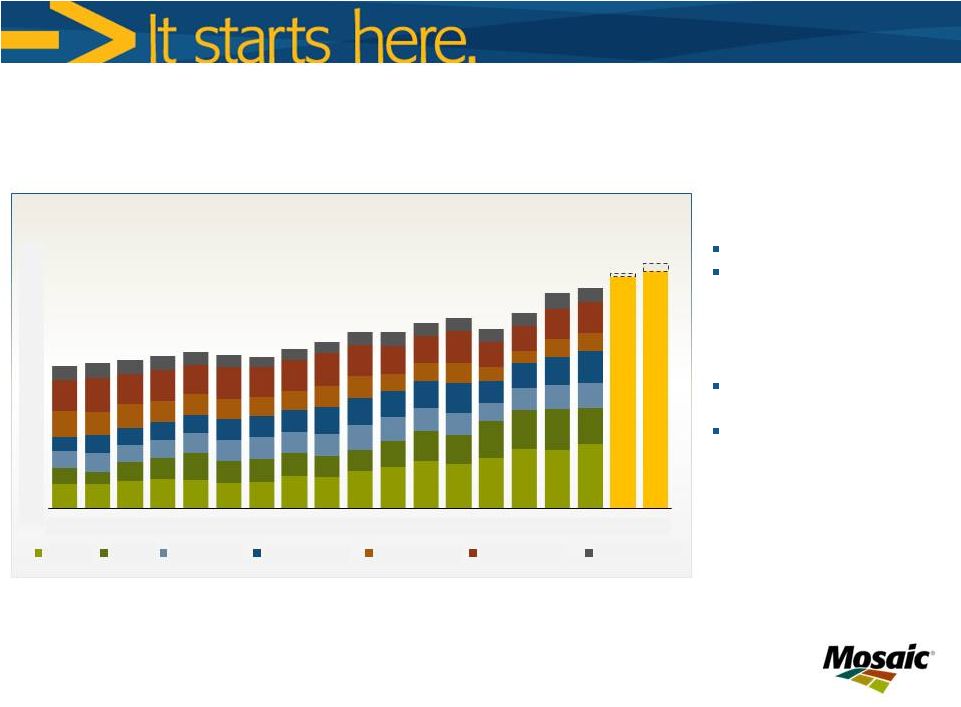

Slide 15

Calendar years

0

10

20

30

40

50

60

70

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11E

12F

13F

Mil Tonnes

DAP/MAP/TSP

WORLD PROCESSED PHOSPHATE SHIPMENTS

China

India

Other Asia

Latin America

Europe/FSU

North America

Rest of World

Sources: Fertecon

and Mosaic |

Uncertain Indian demand

Growing emerging

markets

Muted dealer sentiment

Low natural gas prices

Potash: Stable

Tolling

agreement

benefit

New capacity online

Solution mining

INDUSTRY DYNAMICS

MOSAIC STRENGTHS

Slide 16

Calendar years

0

10

20

30

40

50

60

70

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11E

12F

13F

Mil Tonnes

KCl

WORLD MURIATE OF POTASH SHIPMENTS

China

India

Other Asia

Latin America

Europe/FSU

North America

Rest of World

Sources: Fertecon

and Mosaic |

The Mosaic Company

Thank you |

Earnings

Sensitivity

to

Key

Drivers

(a)

Slide 18

FY12

Actual

Change

FY12

Margin %

Actual

% Impact on

Segment

Margin

Pre-Tax

Impact

EPS

Impact

Marketing

MOP Price ($/tonne) (b)

$448

$50

49.1%

9.0%

$299

$0.50

Potash Volume (million

metric tonnes)

6.7

500

49.1%

4.8%

$158

$0.26

DAP Price ($/tonne)

$555

$50

18.7%

6.1%

$474

$0.79

Phosphate Volume (million

metric tonnes)

11.8

500

18.7%

1.2%

$91

$0.15

Raw Materials

Sulfur ($/lt)

$223

$50

18.7%

2.2%

$173

$0.29

Ammonia ($/tonne)

$528

$50

18.7%

1.3%

$104

$0.17

(a) These factors do not change in isolation; actual results could vary from the

above estimates (b) assumes no change to KMAG pricing

|

Phosphate Raw Material Costs

Slide 19

Realized costs of raw materials in COGS lag spot prices by approximately 3 months.

Realized ammonia costs, in most periods shown, include a benefit of our

manufacture of ammonia at Faustina. $417

$451 |

Phosphate Raw Material Costs

Slide 20

$200

$196

Realized costs of raw materials in COGS lag spot prices by approximately 3 months. Sulfur realized

prices include storage, conversion and transformation costs of $10 - $15 / ton. |

Phosphate Rock Sourcing

Slide 21

$

-

$25

$50

$75

$100

$125

$150

$175

$200

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Q4 FY11

Q1 FY12

Q2 FY12

Q3 FY12

Q4 FY 12

ROCK MIX USED IN U.S. OPERATIONS

US mined rock

Purchased Miski Mayo rock

Other purchased rock

- |

Canadian Resource Taxes and Royalties

Slide 22

FY12 ACTUAL

In millions

Sales

$3,302

Combined Royalty & Surcharge Rate

4.0%

Royalty & Surcharge

132

Potash Segment GM before CRT

1,950

Add back Depreciation

234

Subtract Capex

1,171

Estimated Taxable Profit

1,012

Estimate Profit Tax: 15% and 20% of taxable profit

@ 15%

152

@ 20%

202

Total CRT (Royalty & Surcharge + Profit Tax)

@ 15%

284

@ 20%

335

Compare to actual Resource Tax & Royalties

328 |

ROIC Reconciliation

Slide 23

($ in millions)

FY2011

FY2012

FY2012

FY2012

FY2012

Actual

Actual

Actual

Actual

Actual

Q4

Q1

Q2

Q3

Q4

Operating Profit

729.6

797.0

413.7

670.8

Taxes

205.1

230.7

87.0

188.6

Equity Earnings

1.8

0.9

4.2

6.4

NOPAT

526.3

567.2

330.9

488.6

NOPAT -

Trailing 4 Quarters

1,913.0

May-11

Aug-11

Nov-11

Feb-12

May-12

Invested

Capital:

Total assets

15,786.9

16,180.8

15,802.3

15,936.7

16,690.4

Accounts payable

(941.1)

(903.1)

(853.6)

(800.5)

(912.4)

Accrued liabilities

(843.6)

(723.0)

(635.1)

(657.9)

(899.9)

Deferred

income

taxes

-

current

(72.2)

(70.1)

(68.2)

(73.7)

(62.4)

Deferred

income

taxes

-

noncurrent

(580.1)

(579.7)

(589.4)

(611.2)

(787.9)

Other noncurrent liabilities

(855.1)

(841.1)

(785.1)

(869.8)

(975.4)

Total Invested Capital

12,494.8

13,063.8

12,870.9

12,923.6

13,052.4

Invested

Capital

-

5

Quarter

Average

11,290.9

11,885.2

12,381.2

12,649.9

12,881.1

ROIC (including goodwill)

14.9%

We have presented ROIC, which is a non-GAAP financial measure. Generally, non-GAAP financial

measures are supplemental numerical measures of a company's performance, financial

position or cash flows that either exclude or include amounts that are not normally excluded or included in the most

directly comparable measure calculated and presented in accordance with U.S. generally accepted

accounting principles ("GAAP"). ROIC is not a measure of financial

performance under GAAP. Because not all companies use identical calculations, our calculation of ROIC may not be comparable to

other similarly titled measures presented by other companies. In evaluating this measure, investors

should consider that our methodology in calculating such measures may differ from that

used by other companies. We consider ROIC to be a meaningful indicator of how effectively a company is investing its

capital and deploying its assets.”

1 |