Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Nuwellis, Inc. | Financial_Report.xls |

| EX-23.1 - EX-23.1 - Nuwellis, Inc. | a2210234zex-23_1.htm |

| EX-10.4 - EX-10.4 - Nuwellis, Inc. | a2210234zex-10_4.htm |

As filed with the Securities and Exchange Commission on July 17, 2012

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

SUNSHINE HEART, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 3841 | 68-0533453 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

12988 Valley View Road

Eden Prairie, MN 55344

(952) 345-4200

(Address, including zip code, and telephone number, including

area code, of registrant's principal executive offices)

David A. Rosa

Chief Executive Officer

Sunshine Heart, Inc.

12988 Valley View Road

Eden Prairie, MN 55344

(952) 345-4200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||

Jonathan R. Zimmerman Matthew R. Kuhn Faegre Baker Daniels LLP 2200 Wells Fargo Center 90 South Seventh Street Minneapolis, MN 55402-3901 (612) 766-7000 |

Timothy R. Curry Jacob C. Tiedt Jones Day 1755 Embarcadero Road Palo Alto, CA 94303 (650) 739-3939 |

|

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. o

If this Form is a post effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company ý |

CALCULATION OF REGISTRATION FEE

| |

||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

Title of Each Class of Securities to be Registered |

|

Proposed Maximum Aggregate Offering Price(1) |

|

Amount of Registration Fee |

|

||||||

|

Common stock, par value $0.0001 per share |

$28,750,000 | $3,295 | |||||||||

- (1)

- Estimated solely for the purpose of computing the registration fee pursuant to Rule 457(o) of the Securities Act of 1933.

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 17, 2012

Shares

Common Stock

$ per share

We are selling shares of our common stock. We have granted the underwriters a 30-day option to purchase up to an additional shares from us to cover over-allotments, if any.

This is a public offering of our common stock. Our common stock is listed on the Nasdaq Capital Market under the symbol "SSH." The closing price of our common stock on the Nasdaq Capital Market on July 16, 2012 was $11.03 per share.

WE ARE AN "EMERGING GROWTH COMPANY" UNDER THE U.S. FEDERAL SECURITIES LAWS AND WILL BE SUBJECT TO REDUCED PUBLIC COMPANY REPORTING REQUIREMENTS. INVESTING IN OUR COMMON STOCK INVOLVES RISKS. SEE "RISK FACTORS" BEGINNING ON PAGE 8.

| |

Per Share | Total | |||||

|---|---|---|---|---|---|---|---|

Public offering price |

$ | $ | |||||

Underwriting discount |

$ | $ | |||||

Proceeds, before expenses, to us |

$ | $ | |||||

The underwriters are offering the common stock as set forth in the "Underwriting" section.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Sole Book-Running Manager

Canaccord Genuity

Co-Managers

| Lazard Capital Markets |

| Cowen and Company |

| Craig-Hallum Capital Group |

| Northland Capital Markets |

The date of this prospectus is , 2012.

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus and any free-writing prospectus that we authorize to be distributed to you. We have not, and the underwriters have not, authorized any other person to provide you with information different from that contained in this prospectus or any related free-writing prospectus that we authorize to be distributed to you. This prospectus is not an offer to sell, nor is it seeking an offer to buy, these securities in any state where the offer or sale is not permitted. The information in this prospectus speaks only as of the date of this prospectus unless the information specifically indicates that another date applies, regardless of the time of delivery of this prospectus or of any sale of our common stock.

C-Pulse®, Sunshine®, Sunshine HeartTM, C-PatchTM and other trademarks or service marks of Sunshine Heart appearing in this prospectus are the property of Sunshine Heart, Inc. Trade names, trademarks and service marks of other companies appearing in this registration statement are the property of the respective owners.

We obtained industry and market data used throughout this prospectus through our research, surveys and studies conducted by third parties and industry and general publications. We have not independently verified market and industry data from third-party sources.

In this prospectus, "company," "we," "our," and "us" refer to Sunshine Heart, Inc. and its subsidiary, except where the context otherwise requires.

All references in this prospectus to "$" are to U.S. Dollars and all references to "A$" are to Australian Dollars.

Investing in our common stock involves a high degree of risk. We believe the risks described under the caption "Risk Factors" below and elsewhere in this prospectus are the material risks we face. However, these risks may not be the only risks we face. Additional unknown risks or risks that we currently consider immaterial may also impair our business operations. If any of the events or circumstances described actually occurs, our business, financial condition or results of operations could suffer, and the trading price of our common stock could decline significantly. Investors should consider the specific risk factors discussed under the caption "Risk Factors" below and elsewhere in this prospectus, together with the "Special Note Regarding Forward-Looking Statements" and the other information contained in this prospectus, including our financial statements and the related notes, before investing in our common stock.

Overview

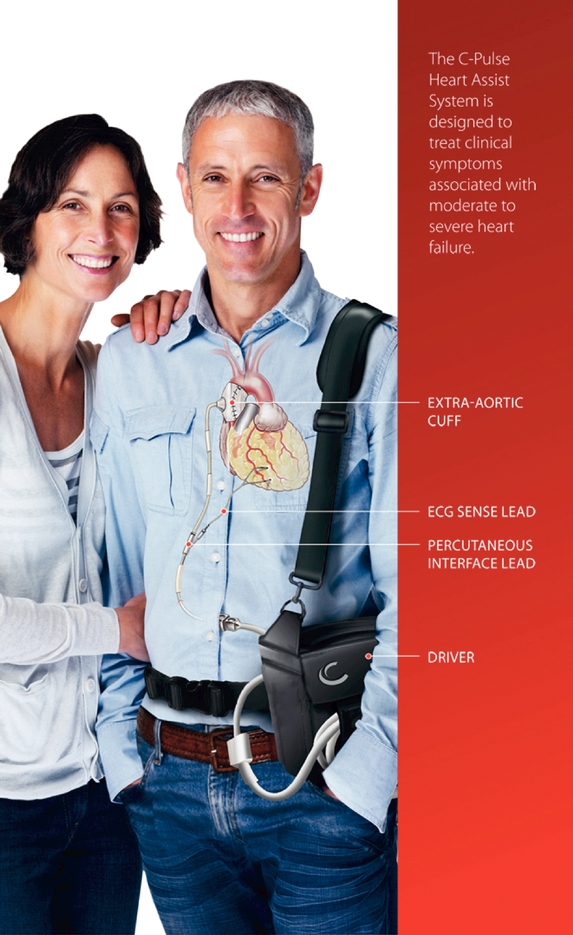

We are an early-stage medical device company focused on developing, manufacturing and commercializing our C-Pulse Heart Assist System, or C-Pulse System, for treatment of Class III and ambulatory Class IV heart failure. The C-Pulse System utilizes the scientific principles of intra-aortic balloon counter-pulsation applied in an extra-aortic approach to assist the left ventricle by reducing the workload required to pump blood throughout the body, while increasing blood flow to the coronary arteries.

We are in the process of pursuing regulatory approvals necessary to sell our system in the United States and Europe. We completed enrollment of our North American feasibility clinical trial in the first half of 2011. In November 2011, we announced the preliminary results of the six-month follow-up period for the feasibility study and we submitted the clinical data to the United States Food and Drug Administration, or FDA. In March 2012, the FDA notified us that it completed its review of the C-Pulse System feasibility trial data, concluded we met the applicable agency requirements, and indicated that we can move forward with an investigational device exemption, or IDE, application. We expect to submit an IDE application to the FDA in the second half of 2012 for approval to initiate our pivotal trial. We expect to complete enrollment of our pivotal trial by the end of 2015 and do not anticipate marketing our system in the United States before 2017.

We are seeking CE Mark for the C-Pulse System in Europe and anticipate that we will obtain approval in the second half of 2012. We have taken initial steps to evaluate the market potential for our system in targeted countries that accept the CE Mark in anticipation of commencing commercial sales of the C-Pulse System in Europe following CE Mark approval. In order to gain additional clinical data and support reimbursement in Europe, we also expect to initiate a post-market trial in Europe that will evaluate endpoints similar to those for our U.S. pivotal trial.

We incurred net losses of $16.2 million and $7.6 million in the years ended December 31, 2011 and 2010, respectively, and $4.1 million in the quarter ended March 31, 2012. Historically, we have generated our revenue solely from sales of the C-Pulse System to hospitals and clinics pursuant to research arrangements and with appropriate regulatory approvals for sales in conjunction with our feasibility clinical trial. We expect to continue to incur significant net losses as we continue to conduct clinical trials, pursue commercialization and as we ramp up sales of our system.

Our Market Opportunity

Heart failure is one of the leading causes of death in the United States and other developed countries. The American Heart Association estimates that 5.7 million people in the United States age 20 and over are

1

affected by heart failure, with an estimated 670,000 new cases diagnosed each year. Nearly 30% of heart failure patients are below the age of 60, and congestive heart failure is the highest U.S. chronic health care expense category.

Heart failure is a progressive disease caused by impairment of the heart's ability to pump blood to the various organs of the body. Patients with heart failure commonly experience shortness of breath, fatigue, difficulty exercising and swelling of the legs. The heart becomes weak or stiff and enlarges over time, making it harder to pump the blood needed for the body to function properly. The severity of heart failure depends on how well a person's heart is able to pump blood throughout the body. A common measure of heart failure severity is the New York Heart Association, or NYHA, Class guideline. Patients are classified in Class I through Class IV based on their symptoms and functional limitations. Classes I and II include mild heart failure patients, Class III includes moderate heart failure patients, and Class IV includes severe heart failure patients.

Our C-Pulse System targets Class III and ambulatory Class IV patients as defined by the NYHA. It is estimated that approximately 1.5 million heart failure patients in the United States fall into this classification range, and we believe approximately 3.7 million patients in Europe are similarly affected.

Treatment alternatives currently available for Class III heart failure patients in the United States consist primarily of pharmacological therapies and pacing devices that are designed to address heart rhythm issues. Although these treatments may provide symptomatic relief and prolong the life of patients, they do not often halt the progression of congestive heart failure. Circulatory assist devices, specifically left ventricular assist devices, or LVADs, have been used to treat Class IV patients in the United States, and one product received FDA approval in the United States for Class IIIb patients although the device is not reimbursed by the Centers for Medicare and Medicaid Services, or CMS, for Class IIIb patients. These devices are designed to take over some or all of the pumping function of the heart by mechanically pumping blood into the aorta. Although such products are effective in increasing blood flow, these devices are implanted in the patient's body and by design are in contact with the patient's bloodstream, increasing the risk of adverse events, including thrombosis, bleeding and neurologic events. The FDA recently rejected a proposed clinical trial that would evaluate the safety and performance of an LVAD technology for Class III heart failure patients because they did not believe the technology risks outweighed the potential rewards for these patients.

Our Strategy

Our goal is to become a market leader in the treatment of heart failure patients through the commercialization of our C-Pulse System, and to continue the development of the system to make it safer and more convenient for patients and physicians. We believe that our technology will provide us with a competitive advantage in the market for treating specific segments of heart failure patients. To achieve our objectives, we intend to:

- •

- obtain regulatory approval to market and sell the C-Pulse System in Europe;

- •

- plan for the commercial launch of the C-Pulse System in Europe;

- •

- obtain IDE approval for our pivotal trial in the United States;

- •

- conduct a pivotal trial in the United States;

- •

- conduct trials in Europe to support reimbursement of the C-Pulse System; and

- •

- continue to enhance the C-Pulse System.

2

Our System

The C-Pulse System utilizes the scientific principles of intra-aortic balloon counter-pulsation applied in an extra-aortic approach to assist the left ventricle by reducing the workload required to pump blood throughout the body, while increasing blood flow to the coronary arteries. Combined, these potential benefits may help sustain the patient's current condition or, in some cases, reverse the heart failure process, thereby potentially preventing the need for later-stage heart failure devices, such as LVADs, artificial hearts or transplants. It may also provide relief from the symptoms of Class III and ambulatory Class IV heart failure and improve quality of life and cardiac function. Based on the patient results from our feasibility trial, we also believe that some patients treated with our C-Pulse System will be able to stop using the device due to sustained improvement in their conditions as a result of the therapy.

Once implanted, the C-Pulse cuff is positioned on the outside of the patient's ascending aorta above the aortic valve. An electrocardiogram sensing lead is then attached to the heart to determine timing for cuff inflation and deflation in synchronization with the heartbeat. As the heart fills with blood, the C-Pulse cuff inflates to push blood from the aorta to the rest of the body and to the heart muscle via the coronary arteries. Just before the heart pumps, the C-Pulse cuff deflates to reduce the heart's workload through pressure changes, allowing the heart to pump with less effort. The C-Pulse cuff and electrical leads are connected to a single line that is run through the abdominal wall to connect to a power driver outside the body. The system's driver and battery source are contained inside a carrying bag.

Surgeons in the feasibility phase of our clinical trial initially implanted the C-Pulse System in patients via a full sternotomy. We have developed a procedure to allow the C-Pulse System to be implanted via a small pacemaker-like incision between the patient's ribs and sternum, rather than through a full sternotomy, and the first implant using this less invasive procedure was completed in 2010. Patients implanted via our minimally invasive procedure typically require a hospital stay of four to seven days in connection with implantation of the C-Pulse System, after which they return home. This compares to an average hospital stay of 14 days for patients implanted with the C-Pulse System via a full sternotomy. Further, final clinical data from two LVAD studies indicate median hospital stays of 19 and 25 days for patients implanted via a full sternotomy. Therefore, we believe this less invasive approach can reduce procedural time, hospital stays, overall cost and patient risk as compared to treatment options that require a full sternotomy.

The C-Pulse System distinguishes itself from other mechanical heart failure therapies in two important respects, which we believe differentiate our system from other products addressing moderate to severe heart failure patients:

- •

- The C-Pulse System is Placed Outside a Patient's Vascular

System. The C-Pulse cuff is placed outside a patient's ascending aorta and assists the heart's normal pumping function,

rather than being inserted into the vascular system and replacing heart function in a manner similar to other devices such as LVADs. Because the C-Pulse System remains outside the vascular

system, there is potentially less risk of complications such as blood clots, stroke and thrombosis in comparison to other mechanical devices that reside or function inside the vascular system. Because

it rests outside the vasculature, it also does not require blood thinning agents that are necessary for patients with devices that are in contact with the bloodstream.

- •

- The C-Pulse System Can be Safely Turned On or Off at Any Time. The C-Pulse System does not need to be in constant operation for patients once implanted, and the device can be safely turned on or off at any time. This feature allows patients intervals of freedom to perform certain activities such as showering. Patients are not required to visit a medical facility when turning our device on or off or using the device. However, patients are advised to turn off the C-Pulse System

3

only for short periods of time and for specified activities to maximize the benefit from the system. If the C-Pulse System is not used as directed, patients might experience a return of their heart failure symptoms, a loss of any improvement in their condition resulting from use of our system or an overall worsening of their heart failure symptoms compared to when they began using our system.

Clinical Development

We completed enrollment and implantation of 20 patients in our North American feasibility trial in the first half of 2011. The feasibility phase of our clinical trial was primarily designed to assess safety and provide indications of performance of the C-Pulse System in moderate to severe heart failure patients who suffer from symptoms such as shortness of breath and reduced mobility.

In November 2011, we announced the preliminary results of the six-month follow-up period for the feasibility study and we submitted the clinical data to the FDA. The table below summarizes results from the six-month follow-up data as well as the twelve-month data, which became available in June 2012.

| |

||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

All Patients Mean ± Standard Deviation(1) |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

||||||||||

|

|

Parameter |

|

Change (6-Month—Baseline(2)) N=15(3) |

|

Change (12-Month—Baseline(2)) N=12(4) |

|

Significance |

|

||||||||

| Quality of Life (MLWHF)(5) |

-23.4 ± 19.0 | -24.6 ± 16.5 | A reduction of seven points (-7) demonstrates material improvement in patient quality of life | |||||||||||||

| NYHA Class | -1.1 ± 0.7 | -1.2 ± 0.8 | Material reduction to NYHA Class for most patients as indicated in footnote 6 below | |||||||||||||

| Six Minute Hall Walk (meters) |

24.1 ± 62.6 | 46.8 ± 64.9 | Improvement doubled from 6-12 months | |||||||||||||

- (1)

- All

event types and relationship to device have been adjudicated by the Clinical Events Committee (CEC).

- (2)

- Baseline

reflects a patient's result for the particular parameter prior to C-Pulse System implant.

- (3)

- Patients

at 6 months exclude 1 patient that received a heart transplant, 1 patient implanted with an LVAD, 1 patient death during

surgery to treat a sternal infection, 1 patient death resulting from a non-device related drug allergic reaction, and 1 patient death for which the autopsy report notes "no definite

anatomic cause of death" and for which the investigator stated the death was due to a respiratory, non-device related issue.

- (4)

- Patient

population at 12 months includes patients from 6-month follow-up, excluding 1 patient that received a

heart transplant at day 212, 1 patient removed from the study at day 232 due to issues with the PIL that led physician to implant an LVAD, and 1 patient that was explanted due to a fall that resulted

in damage to the PIL.

- (5)

- Minnesota Living with Heart Failure Quality of Life (MLWHF) scores are derived from a questionnaire that asks each patient to indicate, using a six-point scale (zero to five), how much each of 21 facets prevents the patient from living as desired.

4

- (6)

- The table below summarizes the data from follow-up periods indicated for NYHA Class:

| |

||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

Follow-up Period |

|

No Change |

|

1 Class Reduction |

|

2 Class Reduction |

|

3 Class Reduction |

|

||||||||||||||

|

6 months |

3 | 7 | 5 | 0 | |||||||||||||||||||

|

12 months |

2 | 7 | 2 | 1 | |||||||||||||||||||

Summary of Safety Device Events at 6 and 12 Months(1)

| |

||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

|

|

All Subjects (N=20) |

|

||||||||||||

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

6 months |

|

12 months |

|

||||||||||

|

Aortic Disruption(2) | 1 | 1 | |||||||||||||||

|

Neurological Dysfunction | 0 | 0 | |||||||||||||||

|

Myocardial Infarction | 0 | 0 | |||||||||||||||

|

Major Infection | |||||||||||||||||

|

• | Localized Non-Device Infection—PICC Line |

1 | 1 | ||||||||||||||

|

• | Exit Site Infection |

8 | 8 | ||||||||||||||

|

• | Pocket Infection |

0 | 0 | ||||||||||||||

|

• | Internal Pump Component, Inflow or Outflow Tract Infection Percutaneous Interface Lead (PIL) (Replaceable Portion of Drive-line) |

1 | 1 | ||||||||||||||

|

• | Sepsis |

0 | 0 | ||||||||||||||

|

Any Other Device-related AE Acute Renal Dysfunction(3) | 1 | 1 | |||||||||||||||

|

Patients re-hospitalized due to worsening heart failure | 1 | 3 | (4) | ||||||||||||||

- (1)

- All

event types and relationship to device have been adjudicated by the Clinical Events Committee (CEC).

- (2)

- Device-related

adverse event of aortic disruption at time of re-do surgery for mediastinitis.

- (3)

- Computed

tomography (CT) with contrast for the assessment of possible device infection resulted in acute renal dysfunction.

- (4)

- The 2 patient increase from 6 months to 12 months were noncompliant due to approximately 20% driver usage. Patients participating in our feasibility trial were advised to keep the C-Pulse System on for at least 80% of each day. Our 12 month rehospitalization rate of 15% compares to a recent study control group rehospitalization rate of over 40% at 6 months (n=280), which included NYHA Class III patients who had been previously hospitalized for heart failure. We believe that this population is similar to the majority of patients profiled in our feasibility study and our planned IDE study with the exception of NYHA Class IV ambulatory.

We believe the results of the six-month and 12-month follow-up demonstrate the feasibility of the C-Pulse System implantation procedure and provide indications of safety and efficacy of the C-Pulse System in patients with moderate to severe heart failure necessary to proceed with a pivotal trial. In March 2012, the FDA notified us that it completed its review of the C-Pulse System feasibility trial data, concluded we met the applicable agency requirements, and indicated that we can move forward with an IDE application. We currently anticipate that we will have pivotal trial IDE approval in 2012, begin enrollment promptly thereafter, and complete our pivotal trial enrollment by the end of 2015. We are seeking CE Mark for the C-Pulse System in Europe, which we currently anticipate we will obtain in the second half of 2012.

5

Corporate Information

Sunshine Heart, Inc. was incorporated in Delaware on August 22, 2002. We began operating our business in November 1999 through Sunshine Heart Company Pty Ltd., which currently is a wholly owned Australian subsidiary of Sunshine Heart, Inc. Since September 2004, Chess Depositary Instruments, or CDIs, representing beneficial ownership of our common stock have been have traded on the Australian Securities Exchange, or ASX, under the symbol "SHC". Historically, each CDI represented one share of our common stock. In connection with the 200 for 1 reverse stock split we affected on January 27, 2012, we changed this ratio so that each CDI represents 1/200th of a share of our common stock.

On September 30, 2011, we filed a Form 10 registration statement with the SEC, which was declared effective on February 14, 2012. The Form 10 registered our common stock under the Securities Exchange Act of 1934, as amended, or the Exchange Act. Our common stock began trading on the Nasdaq Capital Market on February 16, 2012.

Our principal executive offices are located at 12988 Valley View Road, Eden Prairie, Minnesota 55344, and our telephone number is (952) 345-4200. Our website address is www.sunshineheart.com. The information on, or that may be accessed through, our website is not incorporated by reference into and should not be considered a part of this prospectus or the registration statement of which it is a part.

We qualify as an "emerging growth company" as defined in the Jumpstart our Business Startups Act of 2012, or the JOBS Act. An emerging growth company may take advantage of specified reduced reporting and other burdens that are otherwise applicable generally to U.S. public companies. These provisions include:

- •

- a requirement to have only two years of audited financial statements and only two years of related Management's Discussion

and Analysis of Financial Condition and Results of Operations disclosure; and

- •

- an exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting pursuant to the Sarbanes-Oxley Act of 2002.

We may take advantage of these provisions for up to five years or such earlier time that we are no longer an emerging growth company. We would cease to be an emerging growth company if we have more than $1.0 billion in annual revenue, have more than $700 million in market value of our shares of common stock held by non-affiliates, or issue more than $1.0 billion of non-convertible debt over a three-year period. We may choose to take advantage of some but not all of these reduced burdens. The JOBS Act permits emerging growth companies to take advantage of an extended transition period to comply with new or revised accounting standards applicable to U.S. public companies.

6

| Common stock offered by us | shares of our common stock, par value $0.0001 per share. | |

Common stock to be outstanding immediately after this offering |

shares |

|

Over-allotment option |

We have granted the underwriters an option to purchase up to an additional shares of common stock within 30 days of the date of this prospectus in order to cover over-allotments, if any. |

|

Use of proceeds |

We estimate that the net proceeds to us from this offering, after deducting estimated underwriting discounts and offering expenses, will be approximately $ million. |

|

We intend to use approximately $300,000 of the net proceeds from this offering to repay outstanding indebtedness owed to our outside legal counsel (see "Legal Matters") and the remainder of the net proceeds to fund our pivotal clinical trial and for general corporate purposes. General corporate purposes may include providing working capital and funding capital expenditures and research and development. See "Use of Proceeds." |

||

Nasdaq Capital Market symbol |

SSH |

The number of shares of our common stock outstanding after this offering is based on 6,277,538 shares outstanding as of July 13, 2012. The number of shares of our common stock outstanding as of that date excludes (a) 892,642 shares of common stock issuable upon the exercise of outstanding options to purchase our common stock at a weighted average exercise price of $9.14 per share, (b) 1,580,649 shares of common stock issuable upon the exercise of outstanding warrants at a weighted average exercise price of A$7.92 per share (approximately $8.10 per share based on a conversion rate of A$1 to $1.0231) and (c) 123,820 shares of common stock reserved for future grants under our Amended and Restated 2011 Equity Incentive Plan, or 2011 Equity Incentive Plan.

Except as otherwise indicated, information in this prospectus:

- •

- reflects a 1-for-200 reverse split of our outstanding common stock that was effected on

January 27, 2012;

- •

- assumes a public offering price of $ per share (the closing price of our common stock on the Nasdaq

Capital Market on , 2012); and

- •

- assumes no exercise of the underwriters' over-allotment option to purchase up to additional shares of our common stock from us.

7

Our business faces many risks. We believe the risks described below are the material risks we face. However, the risks described below may not be the only risks we face. Additional unknown risks or risks that we currently consider immaterial may also impair our business operations. If any of the events or circumstances described below actually occurs, our business, financial condition or results of operations could suffer, and the trading price of our shares of common stock could decline significantly. Investors should consider the specific risk factors discussed below, together with the "Special Note Regarding Forward-Looking Statements" and the other information contained this prospectus.

Risks Relating to Our Business

We have incurred operating losses since our inception and anticipate that we will continue to incur operating losses for the foreseeable future.

We are an early-stage company with a history of incurring net losses. We have incurred net losses since our inception, including net losses of $16.2 million and $7.6 million for the years ended December 31, 2011 and 2010, respectively, and $4.1 million for the quarter ended March 31, 2012. As of March 31, 2012, our accumulated deficit was $69.3 million. We do not have any products that have been approved for marketing, and we continue to incur research and development and general and administrative expenses related to our operations. We expect to continue to incur significant and increasing operating losses for the foreseeable future as we incur costs associated with the conduct of clinical trials, continue our research and development programs, seek regulatory approvals, expand our sales and marketing capabilities, increase manufacturing of our system and comply with the requirements related to being a U.S. public company listed on the ASX and the Nasdaq Capital Market. To become and remain profitable, we must succeed in developing and commercializing products with significant market potential. This will require us to succeed in a range of challenging activities, including conducting clinical trials, obtaining regulatory approvals, manufacturing products and marketing and selling commercial products. There can be no assurance that we will succeed in these activities, and we may never generate revenues sufficient to achieve profitability. If we do achieve profitability, we may not be able to sustain it.

We will need additional funding to continue operations, which may not be available to us on favorable terms or at all.

We have no products currently available for commercial sale, and to date we have generated only limited revenue from our feasibility study. In addition, the report of our independent registered public accounting firm includes an explanatory paragraph with regard to our ability to continue as a going concern in connection with its audit of our financial statements for the fiscal year ended December 31, 2011. After completion of this offering, we expect to continue to incur significant and increasing operating losses for the foreseeable future as we incur costs associated with the conduct of clinical trials, continue our research and development programs, seek regulatory approvals, expand our sales and marketing capabilities, increase manufacturing of our system and comply with the requirements related to being a U.S. public company listed on the ASX and the Nasdaq Capital Market. Additional funding will likely be needed after completion of this offering may not be available on terms favorable to us, or at all. If we raise additional funding through the issuance of equity securities, our stockholders may suffer dilution and our ability to use our net operating losses to offset future income may be limited. If we raise additional funding through debt financing, we may be required to accept terms that restrict our ability to incur additional indebtedness, require us to use our cash to make payments under such indebtedness, force us to maintain specified liquidity or other ratios or restrict our ability to pay dividends or make acquisitions. If we are unable to secure additional funding, our development programs and our commercialization efforts would be delayed, reduced or eliminated, our relationships with our suppliers and manufacturers may be harmed, and we may not be able to continue our operations.

8

Our near-term prospects are highly dependent on the development of a single product, our C-Pulse System. If we fail to obtain the regulatory approvals necessary to sell the C-Pulse System or fail to successfully commercialize this system, our business and prospects would be harmed significantly.

Our near-term prospects are highly dependent on the development of a single product, our C-Pulse System, and we have no other product candidates in active development at this time. We are in the process of pursuing regulatory approvals necessary to sell our system in the United States and Europe. We completed enrollment of our North American feasibility clinical trial in the first half of 2011. In November 2011, we announced the preliminary results of the six-month follow-up period for the feasibility study and we submitted the clinical data to the FDA. In March 2012, the FDA notified us that it completed its review of the C-Pulse System feasibility trial data, concluded we met the applicable agency requirements, and indicated that we can move forward with an IDE application. We expect to submit an IDE application to the FDA in the second half of 2012 for approval to initiate our pivotal trial. We expect to complete enrollment of our pivotal trial by the end of 2015 and do not anticipate marketing our system in the United States before 2017. In addition, we are seeking CE Mark for the C-Pulse System in Europe and anticipate that we will obtain approval in the second half of 2012.

There can be no assurance that we will be able to obtain the regulatory approvals necessary to sell our system. In addition, even if we obtain such regulatory approvals, there can be no assurance that we will be able to successfully commercialize our system. If we fail to obtain the regulatory approvals necessary to sell our system or fail to successfully commercialize our system, our business and prospects would be harmed significantly.

We currently have no sales, marketing or distribution operations and will need to expand our expertise in these areas.

We currently have no sales, marketing or distribution operations and, in connection with the expected commercialization of our system, will need to expand our expertise in these areas. To increase internal sales, distribution and marketing expertise and be able to conduct these operations, we would have to invest significant amounts of financial and management resources. In developing these functions ourselves, we could face a number of risks, including:

- •

- we may not be able to attract and build an effective marketing or sales force;

- •

- the cost of establishing, training and providing regulatory oversight for a marketing or sales force may be substantial;

and

- •

- there are significant legal and regulatory risks in medical device marketing and sales that we have never faced, and any failure to comply with applicable legal and regulatory requirements for sales, marketing and distribution could result in an enforcement action by the FDA, European regulators or other authorities that could jeopardize our ability to market the system or could subject us to substantial liability.

We plan to commercialize our system outside of the United States, which will expose us to risks associated with international operations.

We plan to commercialize our system outside of the United States and expect to commence clinical trials in certain European countries in addition to the United States. Conducting international operations subjects us to risks, including:

- •

- costs of complying with varying regulatory requirements and potential, unexpected changes to those requirements;

- •

- fluctuations in and management of currency exchange rates;

9

- •

- potentially adverse tax consequences, including the complexities of foreign value added tax systems and restrictions on

the repatriation of earnings;

- •

- government-imposed pricing controls on sales of our system;

- •

- longer payment cycles and difficulties in collecting accounts receivable;

- •

- difficulties in managing and staffing international operations;

- •

- the burdens of complying with a wide variety of non-U.S. laws and legal standards;

- •

- increased financial accounting and reporting burdens and complexities; and

- •

- reduced or varied protection for intellectual property rights in some countries.

The occurrence of any one of these risks could negatively affect our international operations. Additionally, operating in international markets also requires significant management attention and financial resources. We cannot be certain that our operations in other countries will produce desired levels of revenues or profitability.

We depend on a limited number of manufacturers and suppliers of various critical components for our C-Pulse System. The loss of any of these manufacturer or supplier relationships could delay future clinical trials or prevent or delay commercialization of our C-Pulse System.

We rely entirely on third parties to manufacture our C-Pulse System and to supply us with all of the critical components of our C-Pulse System, including the balloon, driver, cuff and interface lead. We primarily purchase our components and products on a purchase order basis and do not "second source" any components of our system. If one or more of the suppliers of the components used in our system were unable or unwilling to meet our demand for such components or faced financial or business difficulties in general, or if the components or finished products provided by any of our suppliers do not meet quality and other specifications, clinical trials or commercialization of our system could be delayed and our expenses could increase. Moreover, if any of the suppliers were unable or unwilling to perform, we would be required to find alternative sources for the components provided by such supplier, and there can be no assurance that we would be able to find a replacement supplier on a timely basis, or at all. In particular, the balloon used in our system is highly specialized and is currently solely available from a single supplier. If the manufacturer of the balloon were unable or unwilling to supply this component for any reason, we would have to locate and qualify another supplier and such supplier and its balloon product would have to be qualified with the FDA. Since there is currently no other supplier in the industry, locating and qualifying another supplier could cause significant production delays, causing us to lose revenues and market share and to potentially suffer increased costs and damage to our reputation. Additionally, even if we are able to find a replacement supplier of any of the components used in our system, we may face additional regulatory delays, and the manufacture and delivery of our C-Pulse System could be interrupted for an extended period of time and become significantly more expensive. This could delay completion of future clinical trials or commercialization of our C-Pulse System and adversely affect our results of operations. In addition, we may be required to use different suppliers or components to obtain regulatory approval from the FDA.

If our manufacturers or our suppliers are unable to provide an adequate supply of our system following the start of commercialization, our growth could be limited and our business could be harmed.

In order to produce our C-Pulse System in the quantities that we anticipate will be required to meet market demand, we will need our manufacturers to increase, or scale-up, the production process by a significant factor over the current level of production. There are technical challenges to scaling-up manufacturing capacity and developing commercial-scale manufacturing facilities that may require the investment of substantial additional funds by our manufacturers and hiring and retaining additional

10

management and technical personnel who have the necessary manufacturing experience. If our manufacturers are unable to do so, we may not be able to meet the requirements for the launch of the system or to meet future demand, if at all. We also may represent only a small portion of our supplier's or manufacturer's business, and if they become capacity constrained they may choose to allocate their available resources to other customers that represent a larger portion of their business. We currently anticipate that we will continue to rely on third-party manufacturers and suppliers for the production of our C-Pulse System following commercialization. If we develop and obtain regulatory approval for our system and are unable to obtain a sufficient supply of our system, our revenue, business and financial prospects would be adversely affected.

If we are unable to manage our expected growth, we may not be able to commercialize our system.

We have expanded, and expect to continue to expand, our operations and grow our research and development, product development, regulatory, manufacturing, sales, marketing and administrative operations. This expansion has placed, and is expected to continue to place, a significant strain on our management and operational and financial resources. To manage any further growth and to commercialize our system, we will be required to improve existing and implement new operational and financial systems, procedures and controls and expand, train and manage our growing employee base. In addition, we will need to manage relationships with various manufacturers, suppliers and other organizations. Our ability to manage our operations and growth will require us to improve our operational, financial and management controls, as well as our internal reporting systems and controls. We may not be able to implement such improvements to our management information and internal control systems in an efficient and timely manner and may discover deficiencies in existing systems and controls. Our failure to accomplish any of these tasks could materially harm our business.

We may not be able to correctly estimate or control our future operating expenses, which could lead to cash shortfalls.

Our operating expenses may fluctuate significantly in the future as a result of a variety of factors, many of which are outside of our control. These factors include:

- •

- the time and resources required to develop, conduct clinical studies and obtain regulatory approvals for the products we

develop;

- •

- the expenses we incur for the research and development required to maintain and improve our system;

- •

- the costs of preparing, filing, prosecuting, defending and enforcing patent claims and other patent related costs,

including litigation costs and the results of such litigation;

- •

- the expenses we incur in connection with commercialization activities, including marketing, sales and distribution;

- •

- our sales strategy and whether the revenues from sales of our system will be sufficient to offset our expenses;

- •

- the costs to attract and retain personnel with the skills required for effective operations; and

- •

- the costs associated with being a public company.

Our budgeted expense levels are based in part on our expectations concerning future revenues from sales of our C-Pulse System. We may be unable to reduce our expenditures in a timely manner to compensate for any unexpected shortfall in revenue. Accordingly, a significant shortfall in demand for our system could have an immediate and material impact on our business and financial condition.

11

We compete against many companies, some of which have longer operating histories, more established products and greater resources than we do, which may prevent us from achieving further market penetration or improving operating results.

Competition from medical device companies and medical device divisions of health care companies, as well as pharmaceutical companies and gene- and cell-based therapies is intense and is expected to increase. Our system will compete against therapies, including pharmacological therapies, as well as other medical device competitors that treat or may treat in the future Class III or ambulatory Class IV heart failure patients, including AbioMed, Inc., Berlin Heart GmbH, CardioKinetix, Inc., CircuLite, Inc., HeartWare International Inc., Jarvik Heart, Inc., MicroMed Technology, Inc., SynCardia Systems, Inc., Terumo Heart, Inc. and Thoratec Corporation, as well as a range of other specialized medical device companies with devices at varying stages of development. Some of these competitors have significantly greater financial and human resources than we do and have established reputations, as well as worldwide distribution channels and sales and marketing capabilities that are larger and more established than ours. Additional competitors may enter the market, and we are likely to compete with new companies in the future. We also face competition from other medical therapies which may focus on our target market as well as competition from manufacturers of pharmaceutical and other devices that have not yet been developed. Competition from these companies could harm our business.

Our ability to compete effectively depends upon our ability to distinguish our company and our system from our competitors and their products. Factors affecting our competitive position include:

- •

- financial resources;

- •

- product performance and design;

- •

- product safety;

- •

- acceptance of our system in the marketplace;

- •

- sales, marketing and distribution capabilities;

- •

- manufacturing and assembly costs;

- •

- pricing of our system and of our competitors' products;

- •

- the availability of reimbursement from government and private health insurers;

- •

- success and timing of new product development and introductions;

- •

- regulatory approvals in the United States and Europe; and

- •

- intellectual property protection.

The competition for qualified personnel is particularly intense in our industry. If we are unable to retain or hire key personnel, we may not be able to sustain or grow our business.

Our ability to operate successfully and manage our potential future growth depends significantly upon our ability to attract, retain and motivate highly skilled and qualified research, technical, clinical, regulatory, sales, marketing, managerial and financial personnel. We face intense competition for such personnel, and we may not be able to attract, retain and motivate these individuals. We compete for talent with numerous companies, as well as universities and nonprofit research organizations. Our future success also depends on the personal efforts and abilities of the principal members of our senior management and scientific staff to provide strategic direction, manage our operations and maintain a cohesive and stable environment. We do not maintain key man life insurance on the lives of any of the members of our senior management. The loss of key personnel for any reason or our inability to hire, retain and motivate additional qualified personnel in the future could prevent us from sustaining or growing our business.

12

Product defects could harm our results of operations.

The design, manufacture and marketing of medical devices involve certain inherent risks. Manufacturing or design defects, unanticipated use of a product or inadequate disclosure of risks relating to the use of the product can lead to injury or other adverse events. These events could lead to recalls or safety alerts relating to a product (either voluntary or required by the FDA or similar governmental authorities in other countries), and could result, in certain cases, in the removal of a product from the market. Any recall of our system could result in significant costs, as well as negative publicity and damage to our reputation that could reduce demand for our system. Personal injuries relating to the use of our system could also result in product liability claims being brought against us. In some circumstances, such adverse events could also cause delays in new product approvals. Any one of these factors could substantially harm our business and results of operations.

We may be sued for product liability, which could adversely affect our business.

The design, manufacture and marketing of medical devices carries a significant risk of product liability claims. Our system treats Class III and ambulatory Class IV heart failure for patients who typically have serious medical issues. As a result, our exposure to product liability claims may be heightened because the people who use our system have a high risk of suffering adverse outcomes, regardless of the safety or efficacy of our system.

We may be held liable if any product we develop and commercialize causes injury or is found otherwise unsuitable during product testing, manufacturing, marketing, sale or consumer use. The safety studies we must perform and the regulatory approvals required to commercialize our system will not protect us from any such liability. We carry product liability insurance with a $10 million aggregate limit. However, if there are product liability claims against us, our insurance may be insufficient to cover the expense of defending against such claims, or may be insufficient to pay or settle such claims. Furthermore, we may be unable to obtain adequate product liability insurance coverage for commercial sales of any of our approved products. If such insurance is insufficient to protect us, our results of operations will be harmed. If any product liability claim is made against us, our reputation and future sales will be damaged, even if we have adequate insurance coverage. Even if a product liability claim against us is without merit or if we are not found liable for any damages, a product liability claim could result in decreased demand for our system, injury to our reputation, diversion of management's attention from operating our business, withdrawal of clinical trial participants, significant costs of related litigation, loss of revenue or the inability to commercialize the C-Pulse System.

Risks Relating to Regulation

We have no products approved for commercial sale, and our success will depend heavily on the success of our pivotal trial for our C-Pulse System. Any failure or significant delay in successfully completing our pivotal trial or obtaining regulatory approvals could harm our financial results and our prospects and require us to seek additional funding.

Upon completion of the six-month follow-up period for our feasibility trial, we submitted the trial's clinical data to the FDA in November 2011. We expect to submit an IDE application to the FDA in the second half of 2012 for approval to initiate our pivotal trial. Completion of the pivotal trial could be delayed, and adverse events during the trial could cause us to modify the existing design, repeat or terminate the trial. If the trial is delayed, if it must be repeated or if it is terminated, our costs associated with the trial will increase, and it will take us longer to obtain regulatory approvals and commercialize the C-Pulse System, if we are able to do so at all. Our pivotal trial also may be suspended or terminated at any time by

13

regulatory authorities or by us. FDA scrutiny of IDE applications has intensified in recent years, increasing the risk of delay or failure.

If we commence and complete our pivotal clinical trial, we must demonstrate the safety and efficacy of the C-Pulse System by meeting the trial's endpoints before we can commercialize the C-Pulse System in the United States. Our inability to achieve the safety or efficacy endpoints in the pivotal trial could delay our timeline for obtaining regulatory approval to commercialize our system or prevent us from obtaining such regulatory approval altogether.

In addition to successfully completing our pivotal trial, we will need to receive approval from regulatory agencies in each country in which we seek to sell our system. Approval procedures vary among countries and can involve additional product testing and additional administrative review periods. The time required to obtain approval varies from country to country and approval in one country does not ensure regulatory approval in another. In addition, a failure or delay in obtaining regulatory approval in one country may negatively impact the regulatory process in others. We cannot assure you when, or if, we will be able to commence sales in any jurisdiction within or outside the United States.

If we are unable to complete our pivotal trial, or experience significant delays in the trial, or if the results of the trial do not meet its safety and efficacy endpoints, our ability to obtain regulatory approval to commercialize our system and to generate revenues will be harmed.

Even if we obtain foreign regulatory approvals, we will need to obtain FDA approval to commercialize our system in the United States.

Even if we obtain foreign regulatory approvals, we will need to obtain FDA approval to commercialize our system in the United States, which will require us to receive FDA approval to conduct clinical trials in the United States and to complete those trials successfully. If we fail to obtain approval from the FDA, we will not be able to market and sell our system in the United States. We do not currently have the necessary regulatory approvals to commercialize our C-Pulse System in the United States, which we believe is the largest potential market for our C-Pulse System. We can offer no assurance that our IDE application will be approved, that our clinical trials will be successful or that we will ever obtain FDA approval of the C-Pulse System or any future products.

In order to obtain FDA approval for our C-Pulse System, we will be required to receive a Premarket Approval, or PMA, from the FDA. A PMA must be supported by pre-clinical and clinical trials to demonstrate safety and efficacy. A clinical trial will be required to support an application for a PMA, and we will be seeking FDA approval of our IDE application that will allow us to commence a clinical trial in the United States. We intend to commence our U.S. pivotal trial in 2012, but there can be no assurance that our U.S. pivotal trial will begin or be completed on schedule or at all. Even if completed, we do not know if this trial will meet its objectives or end-points to show the safety and efficacy of our system so as to support an application for a PMA.

The process of obtaining a PMA from the FDA for our C-Pulse System, or any future products or enhancements or modifications to any products, could:

- •

- take a significant period of time;

- •

- require the expenditure of substantial resources;

- •

- involve rigorous pre-clinical and clinical testing;

- •

- require changes to the product; and

14

- •

- result in failure to support approval of the product or limitations on the indicated uses of the product.

Increased attention to safety and oversight issues in light of recent, widely publicized events concerning the safety of certain food, drug and medical device products could cause the FDA to take a more cautious approach in connection with approvals for devices such as ours, which could delay or prevent FDA approval of our C-Pulse System.

There can be no assurance that we will receive the required approvals from the FDA or, if we do receive the required approvals, that we will receive them on a timely basis. The failure to receive product approval by the FDA would significantly harm our business, financial condition or results of operations.

We may be unable to enroll and complete our planned U.S. pivotal trial for the C-Pulse System or other clinical trials, which could prevent or delay regulatory approval of the C-Pulse System and impair our financial position.

We intend to commence our U.S. pivotal trial in 2012. The trial is designed to be a randomized trial that includes approximately 380 patients and is expected to involve approximately 40 sites. Conducting a clinical trial of this size is a complex and uncertain process.

The commencement of our trial could be delayed for a variety of reasons, including:

- •

- reaching agreement on acceptable terms with prospective clinical trial sites;

- •

- manufacturing sufficient quantities of our C-Pulse System;

- •

- obtaining institutional review board approval to conduct the trial at a prospective site; and

- •

- obtaining sufficient patient enrollment, which is a function of many factors, including the size of the patient population, the nature of the protocol, the proximity of patients to clinical sites and the eligibility criteria for the trial.

Once the trial has begun, the completion of the trial, and our other ongoing clinical trials, could be delayed, suspended or terminated for several reasons, including:

- •

- ongoing discussions with regulatory authorities regarding the scope or design of our preclinical results or clinical trial

or requests for supplemental information with respect to our preclinical results or clinical trial results;

- •

- our failure or inability to conduct the clinical trials in accordance with regulatory requirements;

- •

- sites currently participating in the trial may drop out of the trial, which may require us to engage new sites or petition

the FDA for an expansion of the number of sites that are permitted to be involved in the trial;

- •

- patients may not achieve the required clinical end-points of the trial;

- •

- patients may not remain in or complete clinical trials at the rates we expect;

- •

- patients may experience serious adverse events or side effects during the trial, which, whether or not related to our

system, could cause the FDA or other regulatory authorities to place the clinical trial on hold; and

- •

- clinical investigators may not perform clinical trials on our anticipated schedule or consistent with the clinical trial protocol and good clinical practice requirements.

If our pivotal trial is delayed, it will take us longer to ultimately commercialize a product or the delay could result in our being unable to do so. Our development costs will also increase if we have material

15

delays in our pivotal trial or if we need to perform more or larger clinical trials than planned. Moreover, there can be no assurance that we will be able to successfully complete, or achieve the desired clinical end-points from, our pivotal trial at all, which could prevent us from receiving regulatory approval for the C-Pulse System altogether. Any of the foregoing could harm our financial results and our prospects and cause us to seek additional funding.

We depend on clinical investigators and clinical sites to enroll patients in our clinical trials, and on other third parties to manage the trials and to perform related data collection and analysis, and, as a result, we may face costs and delays that are outside of our control.

We have and plan to continue to rely on clinical investigators and clinical sites to enroll patients in our clinical trials, including our planned U.S. pivotal trial, and other third parties to manage the trials and to perform related data collection and analysis. However, we have limited oversight over these entities and cannot control the amount and timing of resources that clinical sites may devote to our clinical trials. If these clinical investigators and clinical sites fail to enroll a sufficient number of patients in our clinical trials, to ensure compliance by patients with clinical protocols or comply with regulatory requirements, we will be unable to complete these trials, which could prevent us from obtaining regulatory approvals for our system. Our agreements with clinical investigators and clinical trial sites for clinical testing place substantial responsibilities on these parties and, if these parties fail to perform as expected, our trials could be delayed or terminated. If these clinical investigators, clinical sites or other third parties do not carry out their contractual duties or obligations or fail to meet expected deadlines, or if the quality or accuracy of the clinical data they obtain is compromised due to their failure to adhere to our clinical protocols, regulatory requirements or for other reasons, our clinical trials may be extended, delayed or terminated, or the clinical data may be rejected by the FDA, and we may be unable to obtain regulatory approval for, or successfully commercialize, our system.

Our manufacturers and suppliers might not meet regulatory quality standards applicable to manufacturing and quality processes, which could harm our financial results and prospects.

Even if our system receives marketing approval, product approvals by the FDA can be withdrawn due to failure to comply with regulatory standards. We rely entirely on third parties to manufacture our C-Pulse System and those manufacturers are required to demonstrate and maintain compliance with the FDA's Quality System Regulation, or QSR. The QSR is a complex regulatory scheme that covers the methods and documentation of the design, testing, control, manufacturing, labeling, quality assurance, packaging, storage and shipping of our system. The FDA enforces the QSR through periodic unannounced inspections. Compliance with applicable regulatory requirements is subject to continual review and is rigorously monitored through periodic inspections by the FDA. A failure by our manufacturers to comply with the QSR or to take satisfactory corrective action in response to an adverse QSR inspection could cause a significant delay in our ability to have our system manufactured and to complete our clinical trials and could significantly increase our costs, which would harm our financial results and our prospects. In addition, suppliers of components of, and products used to manufacture, our system must also comply with FDA and foreign regulatory requirements, which often require significant time, money and record-keeping and quality assurance efforts and subject us and our suppliers to potential regulatory inspections and stoppages.

We plan to operate in multiple regulatory environments that require costly and time consuming approvals.

Even if we obtain regulatory approvals to commercialize the C-Pulse System or any other product that we may develop, sales of our system in other jurisdictions will be subject to regulatory requirements that vary from country to country. The time and cost required to obtain approvals from these countries may be longer or shorter than that required for FDA approval, and requirements for licensing may differ from those of the FDA. Laws and regulations regarding the manufacture and sale of our system are subject to future

16

changes, as are administrative interpretations and policies of regulatory agencies. If we fail to comply with applicable foreign, federal, state or local market laws or regulations or administrative interpretations and policies of regulatory agencies, we could be precluded from commercializing our system in those countries and could become subject to enforcement actions. Enforcement actions could include product seizures, recalls, withdrawal of clearances or approvals and civil and criminal penalties, which in each case would harm our business.

The C-Pulse System may never achieve market acceptance even if we obtain regulatory approvals.

Even if we obtain regulatory approvals to commercialize the C-Pulse System or any other product that we may develop, our products may not gain market acceptance among physicians, patients, third-party health care payors or the medical community. The degree of market acceptance of any of the devices that we may develop will depend on a number of factors, including:

- •

- the perceived effectiveness and price of the product;

- •

- the prevalence and severity of any side effects;

- •

- potential advantages over alternative treatments;

- •

- the strength of marketing and distribution support; and

- •

- sufficient third-party coverage or reimbursement.

If our C-Pulse System, or any other product that we may develop, is approved but does not achieve an adequate level of acceptance by physicians, patients, third-party health care payors and the medical community, we may not generate product revenue and we may not become profitable or be able to sustain profitability.

If we fail to obtain an adequate level of reimbursement for our system by third-party payors, there may be no commercially viable markets for our system or the markets may be much smaller than expected.

The availability and levels of reimbursement by governmental and other third-party payors significantly affect the market for our system. Reimbursement by third-party payors in the United States typically is based on the device's perceived benefit and whether it is deemed medically reasonable and necessary. Reimbursement levels of third-party payors in the United States are also based on established payment formulas that take into account part or all of the cost associated with these devices and the related procedures performed. We cannot assure you the level of reimbursement we might obtain in the United States, if any, for our system. If we do not obtain adequate levels of reimbursement for our system by third-party payors in the United States, which we believe is largest potential market for our system, our financial condition, results of operations and prospects would be harmed.

Reimbursement and health care payment systems in international markets vary significantly by country, and include both government-sponsored health care and private insurance. To obtain reimbursement or pricing approval in some countries, we may be required to produce additional clinical data, which may involve one or more additional clinical trials, that compares the cost-effectiveness of our system to other available therapies. We may not obtain international reimbursement or pricing approvals in a timely manner, if at all. Our failure to receive international reimbursement or pricing approvals would negatively impact market acceptance of our system in the international markets in which those approvals are sought.

17

We believe that future reimbursement may be subject to increased restrictions both in the United States and in international markets. Future legislation, regulation or reimbursement policies of third-party payors may adversely affect the demand for the C-Pulse System and limit our ability to sell the C-Pulse System or any future products on a profitable basis. In addition, third-party payors continually attempt to contain or reduce the costs of health care by challenging the prices charged for health care products and services. If reimbursement for our system is unavailable in any market or limited in scope or amount, or if pricing is set at unsatisfactory levels, market acceptance of our system would be significantly impaired and our future revenues, if any, would be significantly harmed.

We may be subject, directly or indirectly, to U.S. federal and state health care fraud and abuse and false claims laws and regulations. Prosecutions under such laws have increased in recent years and we may become subject to such litigation. If we are unable to, or have not fully complied with such laws, we could face substantial penalties.

If we are successful in achieving regulatory approval to market our C-Pulse System, our operations will be directly, or indirectly through our customers and health care professionals, subject to various U.S. federal and state fraud and abuse laws, including, without limitation, the federal Anti-Kickback Statute, federal False Claims Act, and federal Foreign Corrupt Practices Act, or the FCPA. These laws may impact, among other things, our proposed sales, and marketing and education programs.

The federal Anti-Kickback Statute prohibits persons from knowingly and willfully soliciting, offering, receiving or providing remuneration, directly or indirectly, in exchange for or to induce either the referral of an individual, or the furnishing or arranging for a good or service, for which payment may be made under a federal health care program such as the Medicare and Medicaid programs. Several courts have interpreted the statute's intent requirement to mean that if any one purpose of an arrangement involving remuneration is to induce referrals of federal health care covered business, the statute has been violated. The Anti-Kickback Statute is broad and, despite a series of narrow safe harbors, prohibits many arrangements and practices that are lawful in businesses outside of the health care industry. Penalties for violations of the federal Anti-Kickback Statute include criminal penalties and civil and administrative sanctions such as fines, imprisonment and possible exclusion from Medicare, Medicaid and other federal health care programs. An alleged violation of the Anti-Kickback Statute may be used as a predicate offense to establish liability pursuant to other federal laws and regulations such as the federal False Claims Act. Many states have also adopted laws similar to the federal Anti-Kickback Statute, some of which apply to the referral of patients for health care items or services reimbursed by any source, not only the Medicare and Medicaid programs.

The federal False Claims Act prohibits persons from knowingly filing, or causing to be filed, a false claim to, or the knowing use of false statements to obtain payment from, the federal government. Suits filed under the False Claims Act, known as "qui tam" actions, can be brought by any individual on behalf of the government and such individuals, commonly known as "relators" or "whistleblowers," may share in any amounts paid by the entity to the government in fines or settlement. The frequency of filing qui tam actions has increased significantly in recent years, causing greater numbers of medical device, pharmaceutical and health care companies to have to defend a False Claim Act action. The federal Patient Protection and Affordable Care Act includes provisions expanding the ability of certain relators to bring actions that would have been previously dismissed under prior law. When an entity is determined to have violated the federal False Claims Act, it may be required to pay up to three times the actual damages sustained by the government, plus civil penalties for each separate false claim. The Deficit Reduction Act of 2005 encouraged states to enact or modify their state false claims act to be at least as effective as the federal False Claims Act by granting states a portion of any federal Medicaid funds recovered through Medicaid-related actions. Most states have enacted state false claims laws, and many of those states included laws including qui tam provisions. States have until March 31, 2013 to enact or amend their false claims laws

18

modeled after the federal False Claims Act for review and approval to receive a greater portion of any recovery.

The federal Patient Protection and Affordable Care Act includes provisions known as the Physician Payments Sunshine Act, which requires manufacturers of drugs, biologics, devices and medical supplies covered under Medicare and Medicaid starting in 2012 to record any transfers of value to physicians and teaching hospitals and to report this data beginning in 2013 to the Centers for Medicare and Medicaid Services for subsequent public disclosure. Manufacturers must also disclose investment interests held by physicians and their family members. Failure to submit the required information may result in civil monetary penalties of up to $1 million per year for knowing violations and may result in liability under other federal laws or regulations. Similar reporting requirements have also been enacted on the state level in the United States, and an increasing number of countries worldwide either have adopted or are considering similar laws requiring transparency of interactions with health care professionals. In addition, some states such as Massachusetts and Vermont impose an outright ban on certain gifts to physicians. If we receive FDA clearance to market our system in the United States, these laws could affect our promotional activities by limiting the kinds of interactions we could have with hospitals, physicians or other potential purchasers or users of our system. Both the disclosure laws and gift bans will impose administrative, cost and compliance burdens on us.

We are unable to predict whether we could be subject to actions under any of these laws, or the impact of such actions. If we are found to be in violation of any of the laws described above and other applicable state and federal fraud and abuse laws, we may be subject to penalties, including civil and criminal penalties, damages, fines, or an administrative action of suspension or exclusion from government health care reimbursement programs and the curtailment or restructuring of our operations.

In addition, to the extent we commence commercial operations overseas, we will be subject to the FCPA and other countries' anti-corruption/anti-bribery regimes, such as the U.K. Bribery Act. The FCPA prohibits improper payments or offers of payments to foreign governments and their officials for the purpose of obtaining or retaining business. Safeguards we implement to discourage improper payments or offers of payments by our employees, consultants, sales agents or distributors may be ineffective, and violations of the FCPA and similar laws may result in severe criminal or civil sanctions, or other liabilities or proceedings against us, any of which would likely harm our reputation, business, financial condition and result of operations.

Risks Relating to our Intellectual Property

We may not be able to protect our intellectual property rights effectively, which could have an adverse effect on our business, financial condition or results of operations.