Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Avid Bioservices, Inc. | Financial_Report.xls |

| EX-21 - SUBSIDIARIES - Avid Bioservices, Inc. | pphm_10k-ex21.htm |

| EX-31.1 - CERTIFICATION - Avid Bioservices, Inc. | pphm_10k-ex3101.htm |

| EX-31.2 - CERTIFICATION - Avid Bioservices, Inc. | pphm_10k-ex3102.htm |

| EX-32 - CERTIFICATION - Avid Bioservices, Inc. | pphm_10k-ex3200.htm |

| EX-23.1 - CONSENT - Avid Bioservices, Inc. | pphm_10k-ex2301.htm |

| EX-10.2 - LOAN AND SECURITY AGREEMENT - Avid Bioservices, Inc. | peregrine_10k-ex1002.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended April 30, 2012

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number: _____

PEREGRINE PHARMACEUTICALS, INC.

(Exact name of Registrant as specified in its charter)

| Delaware | 95-3698422 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 14282 Franklin Avenue, Tustin, California | 92780 |

| (Address of principal executive offices) | (Zip Code) |

(714) 508-6000

(Registrant's telephone number, including area code)

| Securities registered pursuant to Section 12(b) of the Act: | |

| Title of Each Class | Name of Each Exchange on Which Registered |

|

Common Stock ($0.001 par value)

Preferred Stock Purchase Rights |

The Nasdaq Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (check one):

| Large accelerated filer o | Accelerated filer x | Non-accelerated filer o | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

The aggregate market value of Common Stock held by non-affiliates as of October 31, 2011 was $85,913,295.

Number of shares of Common Stock outstanding as of July 13, 2012: 104,174,056

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this report incorporates certain information by reference from the registrant’s proxy statement for the annual meeting of stockholders, which proxy statement will be filed no later than 120 days after the close of the registrant’s fiscal year ended April 30, 2012.

PEREGRINE PHARMACEUTICALS, INC.

Fiscal Year 2012

Annual Report on Form 10-K

Table of Contents

| PART I | ||

| Item 1. | Business | 2 |

| Item 1A. | Risk Factors | 23 |

| Item 1B. | Unresolved Staff Comments | 38 |

| Item 2. | Properties | 38 |

| Item 3. | Legal Proceedings | 39 |

| Item 4. | Mine Safety Disclosures | 39 |

| PART II | ||

| Item 5. | Market For Registrant’s Common Equity, Related Stockholder Matters And Issuer Purchases of Equity Securities | 39 |

| Item 6. | Selected Financial Data | 40 |

| Item 7. | Management’s Discussion And Analysis Of Financial Condition And Results of Operations | 41 |

| Item 7A. | Quantitative And Qualitative Disclosures About Market Risk | 56 |

| Item 8. | Financial Statements And Supplementary Data | 57 |

| Item 9. | Changes In And Disagreements With Accountants On Accounting And Financial Disclosures | 57 |

| Item 9A. | Controls And Procedures | 57 |

| Item 9B. | Other Information | 57 |

| PART III | ||

| Item 10. | Directors, Executive Officers And Corporate Governance | 60 |

| Item 11. | Executive Compensation | 60 |

| Item 12. | Security Ownership Of Certain Beneficial Owners And Management And Related Stockholder Matters | 60 |

| Item 13. | Certain Relationships And Related Transactions, And Director Independence | 60 |

| Item 14. | Principal Accounting Fees and Services | 60 |

| PART IV | ||

| Item 15. | Exhibits And Financial Statement Schedules | 61 |

| SIGNATURES | 67 | |

| 1 |

PART I

In this Annual Report, the terms “we”, “us”, “our”, “Company” and “Peregrine” refer to Peregrine Pharmaceuticals, Inc., and our wholly owned subsidiary, Avid Bioservices, Inc. This Annual Report contains forward-looking statements that involve risks and uncertainties. The inclusion of forward-looking statements should not be regarded as a representation by us or any other person that the objectives or plans will be achieved because our actual results may differ materially from any forward-looking statement. The words “may,” “should,” “plans,” “believe,” “anticipate,” “estimate,” “expect,” their opposites and similar expressions are intended to identify forward-looking statements, but the absence of these words does not necessarily mean that a statement is not forward-looking. We caution readers that such statements are not guarantees of future performance or events and are subject to a number of factors that may tend to influence the accuracy of the statements, including but not limited to, those risk factors outlined in the section titled “Risk Factors” as well as those discussed elsewhere in this Annual Report. You should not unduly rely on these forward-looking statements, which speak only as of the date of this Annual Report. We undertake no obligation to publicly revise any forward-looking statement to reflect circumstances or events after the date of this Annual Report or to reflect the occurrence of unanticipated events. You should, however, review the factors and risks we describe in the reports that we file from time to time with the Securities and Exchange Commission (“SEC”) after the date of this Annual Report.

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and all amendments to those reports filed with or furnished to the SEC are available, free of charge, through our website at www.peregrineinc.com as soon as reasonably practicable after such reports are electronically filed with or furnished to the SEC. The information on, or that can be accessed through, our website is not part of this Annual Report.

Certain technical terms used in the following description of our business are defined in the “Glossary of Terms”.

In addition, we own or have rights to the registered trademark Cotara® and Avid Bioservices®. All other company names, registered trademarks, trademarks and service marks included in this Annual Report are trademarks, registered trademarks, service marks or trade names of their respective owners.

| ITEM 1. | BUSINESS |

Overview

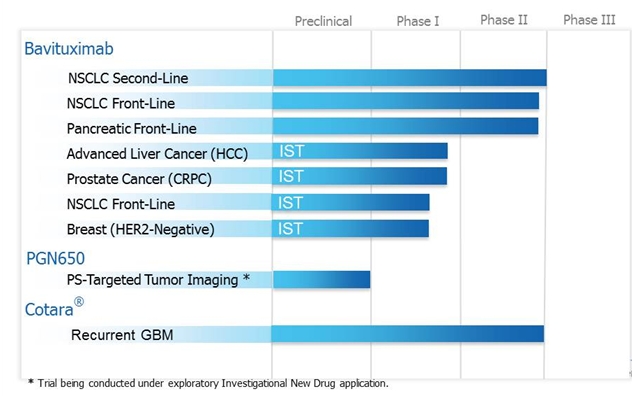

We are a biopharmaceutical company developing first-in-class monoclonal antibodies for the treatment and diagnosis of cancer. We are advancing toward our goal of bringing new therapeutic options to patients and we plan to execute the following strategies:

| — | Advance bavituximab toward Phase III clinical development in second-line non-small cell lung cancer (“NSCLC”) based on data from our Phase IIb randomized, double-blinded, placebo-controlled study in the same patient population; |

| — | Complete discussions with the U.S. Food and Drug Administration (“FDA”) regarding the optimal registration pathway for Cotara; |

| — | Explore additional oncology indications and therapeutic combinations for bavituximab in clinical trials, including front-line NSCLC, pancreatic cancer, liver cancer, HER2-negative metastatic breast cancer, and prostate cancer through company-sponsored trials and cost-effective investigator-sponsored trials (“IST”) program; |

| — | Advance the clinical development of our lead PS-targeting imaging agent, 124I-PGN650 (“PGN650”), across multiple solid tumor types; |

| 2 |

| — | Continue to leverage the broad potential of our phosphatidylserine (“PS”)-targeting platform to treat a broad range of cancer and infectious diseases and examine the platform for the potential imaging of multiple solid tumor types and other disease conditions that present our PS target; and |

| — | Continue to grow our commercial manufacturing business, Avid Bioservices, which provides important biomanufacturing services to third-party clients while also meeting the needs of our internal clinical programs. |

One of the key components of our strategy is to advance our clinical programs for our lead antibodies bavituximab, PGN650, and Cotara. Our pipeline of novel investigational monoclonal antibodies is based on two first-in-class technology platforms, including PS-targeting antibodies and DNA/histone-targeting antibodies.

Bavituximab is our lead therapeutic PS-targeting antibody, which has demonstrated broad therapeutic potential and represents a new approach to treating cancer. PGN650 is our lead PS-targeting imaging agent that represents a potential new approach to imaging cancer. PS is a highly immunosuppressive molecule usually located inside the membrane surface of healthy cells, but “flips” and becomes exposed on the outside of cells that line tumor blood vessels, creating a specific target for anti-cancer treatments and for the imaging of multiple solid tumor types. PS-targeting antibodies target and bind to PS and block this immunosuppressive signal, thereby enabling the immune system to recognize and fight the tumor. We are conducting three randomized Phase II trials for bavituximab in combination with standard chemotherapy for front and second-line non-small cell lung cancer (“NSCLC”) and front-line pancreatic cancer. In addition to these company-sponsored trials for bavituximab, we have four investigator-sponsored trials (“IST”) looking at different treatment combinations and additional oncology indications.

PGN650 is our lead PS-targeting imaging agent that represents a potential new approach to imaging cancer. Under our imaging program, in April 2012, we filed an exploratory Investigational New Drug (“IND”) application with the FDA to advance our lead imaging agent PGN650 into clinical development for the imaging of multiple solid tumor types.

Cotara is our lead DNA/histone-targeting antibody based on our Tumor Necrosis Therapy (“TNT”) technology platform. A novel approach to treating brain cancer, Cotara is a targeted monoclonal antibody linked to a radioisotope that is administered as a single-infusion, one-time therapy directly into the tumor, destroying the tumor from the inside out with minimal exposure to healthy tissue. Cotara has been granted orphan drug status and fast track designation for the treatment of glioblastoma multiforme (“GBM”) and anaplastic astrocytoma by the FDA. In addition, we are currently in discussions with the FDA to define the optimal registration pathway for Cotara based on data from patients treated with Cotara in our Phase II recurrent GBM trial and earlier Phase I trials.

We also have a wholly-owned biomanufacturing subsidiary Avid Bioservices, Inc. (www.avidbio.com), which provides integrated cGMP commercial and clinical manufacturing services for Peregrine and third-party clients. Avid was established in 2002 and began commercial production in 2005. Avid’s total revenue generated from third-party clients for fiscal years 2012, 2011, and 2010, amounted to $14,783,000, $8,502,000, and $13,204,000, respectively.

We were originally incorporated in California in June 1981 and reincorporated in the State of Delaware on September 25, 1996. Our principal executive offices are located at 14282 Franklin Avenue, Tustin, California, 92780 and our telephone number is (714) 508-6000. Our internet website addresses are www.peregrineinc.com, www.avidbio.com, and www.peregrinetrials.com. Information contained on, or accessed through, our websites do not constitute any part of this Annual Report.

| 3 |

Products in Clinical-Stage Development

Products we are advancing in clinical trials are focused on the treatment and imaging of cancer. The following product pipeline reflects our current ongoing clinical trials focused on oncology, as further discussed below:

Bavituximab for the Treatment of Solid Tumors

We believe bavituximab may have broad potential for the treatment of multiple types of cancer. Bavituximab is a novel monoclonal antibody with a unique mechanism of action that specifically targets PS exposed on tumor vasculature. In three previously completed Phase II signal-seeking clinical trials in NSCLC and breast cancer, bavituximab in combination with standard chemotherapy regimens demonstrated promising overall response rates (“ORR”), encouraging progression-free survival (“PFS”), and median overall survival (“OS”) with an acceptable safety profile.

Based on these data, we are currently running seven bavituximab oncology trials including a rigorous Phase II study in second-line non-small cell lung cancer (“NSCLC”). The following represents an overview of the ongoing trials and its current status:

Phase IIb Trial - Bavituximab Plus Docetaxel in Second-Line NSCLC

Our current lead indication clinical study is a randomized, double-blinded, placebo-controlled Phase IIb second-line NSCLC study evaluating two dose levels of bavituximab plus docetaxel (“bavituximab-containing arms”) versus docetaxel plus placebo (“control arm”) as second-line treatment in 121 patients with Stage IIIb or Stage IV NSCLC. Patients were randomized to one of three treatment arms in over 50 sites in the U.S. and internationally and enrollment was completed in October 2011. All patients received up to six 21-day cycles of docetaxel (75 mg/m2). In addition, one bavituximab-containing arm received bavituximab (3 mg/kg) weekly, a second bavituximab-containing arm received bavituximab (1 mg/kg) weekly, and the control arm received placebo weekly until progression or toxicity. The primary endpoint of this trial is ORR and secondary endpoints include median PFS, median overall survival (“OS”), duration of response, and safety. Patients were evaluated regularly for tumor response according to Response Evaluation Criteria In Solid Tumors (“RECIST”) criteria.

| 4 |

In May 2012, we announced positive top-line data from this trial from 117 evaluable patients, based on independent radiology reviews and current status of patients as of that date, as shown in the following table:

|

Treatment Arm |

Placebo plus docetaxel |

Bavituximab (1 mg/kg) plus docetaxel |

Bavituximab (3 mg/kg) plus docetaxel |

| Overall Response Rate | 7.9% | 15.0% | 17.9% |

| Median Progression-Free Survival | 3.0 months | 4.2 months | 4.5 months |

Both dose levels of bavituximab and docetaxel combination treatment were generally safe and well tolerated with adverse events being similar to the patients receiving docetaxel with placebo. Another secondary endpoint, median OS, in the control arm has already been determined at less than 6 months, while the median has not been reached in either bavituximab-containing arm. We anticipate announcing median OS from this trial in the second half of calendar year 2012, but this is a time-to-event endpoint and could take longer to reach.

Based on these encouraging data and our discussions with medical advisors, our strategy is to pursue Phase III development with bavituximab in second-line NSCLC.

Once a front-line NSCLC patient progresses following a first course of therapy, they are typically treated with a second course of therapy. There are approximately 135,000 patients with NSCLC receiving second-line treatment annually in the U.S., Europe, and Japan. The market for second-line NSCLC therapeutics is expected to exceed $1.0 billion annually by 2019 according to independent market research estimates.

Only three drugs are approved in the U.S. as second-line treatment for NSCLC. Administered as monotherapies, these include pemetrexed (Alimta®), docetaxel (Taxotere®), or erlotinib (Tarceva®). Package insert information for these three products shows ORRs of between 5 and 9% for second-line NSCLC. Given these low response rates with current approved therapies, there is an urgent need for new therapeutic options for second-line NSCLC.

Phase IIb Trial - Bavituximab Plus Paclitaxel/Carboplatin in Front-Line NSCLC

Our ongoing Phase IIb trial is designed to assess bavituximab in combination with paclitaxel and carboplatin in front-line NSCLC. This randomized trial enrolled 86 patients (enrollment completed in September 2011) in approximately 40 sites in the U.S. and internationally. Patients were randomized to one of two treatment arms. All patients received up to six 21-day cycles of paclitaxel (200 mg/m2) and carboplatin (AUC 6). In addition, the bavituximab-containing arm received bavituximab (3 mg/kg) weekly until progression or toxicity. The primary endpoint of this trial is ORR and secondary endpoints included median PFS, median OS, duration of response, and safety. Patients were evaluated regularly for tumor response according to RECIST criteria.

In March 2012, we announced top-line data from this Phase IIb trial in which the primary ORR endpoint was determined by both an independent central review and a local investigator review. Based on an independent central imaging review of eligible patients using RECIST criteria, data showed that patients treated with bavituximab plus carboplatin and paclitaxel demonstrated an ORR of 25%, versus 23% in patients treated with carboplatin and paclitaxel alone. Investigator-determined response rates were 32% for bavituximab plus carboplatin and paclitaxel versus 31% for carboplatin and paclitaxel alone.

| 5 |

Based on local investigator assessments, patients treated with bavituximab plus carboplatin and paclitaxel demonstrated a current median PFS estimate of 5.8 months versus 4.6 months in patients treated with carboplatin and paclitaxel alone, a 26% improvement. These results are consistent with our prior phase II single-arm study testing the same bavituximab combination in front-line NSCLC which showed a 6.1 month median PFS and consistent with several prior published studies with carboplatin and paclitaxel in front-line patients that showed approximately a 4.5 month median PFS. Based on independent central imaging reads, patients demonstrated a current median PFS estimate of 6.7 months for the bavituximab-containing arm and 6.4 months for the chemotherapy-only arm. Dose levels of bavituximab, carboplatin and paclitaxel combination treatment were generally safe and well tolerated with adverse events being similar to the patients receiving carboplatin and paclitaxel. Based on these inconclusive data, we believe median OS will be an important data point from this study and instrumental in determining our next steps in advancing bavituximab in front-line NSCLC. We anticipate announcing median OS from this trial in the second half of calendar year 2012, but this is a time-to-event endpoint and could take longer to reach.

Lung cancer is the leading cause of cancer death, and according to the American Cancer Society, lung cancer is the second most commonly diagnosed cancer in the U.S., with approximately 226,160 new cases and 160,340 deaths each year, representing approximately 28% of all cancer deaths. NSCLC is the most common type of lung cancer, accounting for approximately 85-90% of lung cancer cases.

With new cases being diagnosed and given the limitations of current therapies, there is an urgent need for new therapeutic options for front-line NSCLC.

Current treatment options for front-line NSCLC include chemotherapy drugs gemcitabine (Gemzar®), paclitaxel (Taxol®), or docetaxel (Taxotere®) combined with cisplatin or carboplatin. In addition, pemetrexed has been approved for use in combination with cisplatin for front-line NSCLC and bevacizumab (Avastin®) is often added to the standard chemotherapy for front-line NSCLC.

Phase II Trial - Bavituximab Plus Gemcitabine in Pancreatic Cancer

Our ongoing Phase II trial is designed to assess bavituximab in combination with gemcitabine in previously untreated stage IV pancreatic cancer patients. This randomized trial enrolled 70 patients (enrollment completed in June 2012) in approximately 29 sites in the U.S. and internationally. Patients were randomized to one of two treatment arms. All patients received gemcitabine (1000 mg/m2) on days 1, 8 and 15 of each 28 day cycle (4 weeks) until disease progression or unacceptable toxicities. In addition, patients in the bavituximab-containing arm received bavituximab (3 mg/kg) weekly. The primary endpoint of this trial is median OS and secondary endpoints include median PFS, ORR, duration of response, and safety. Patients will be evaluated regularly for tumor response according to RECIST criteria.

We initiated this trial based on prior early clinical and preclinical data. In a Phase Ib trial evaluating bavituximab in combination with different chemotherapies, bavituximab with gemcitabine demonstrated a positive safety profile in advanced cancer patients. Preclinical pancreatic cancer animal model studies show gemcitabine increases the exposure of bavituximab’s PS target on tumor vasculature. In addition, this combination treatment enhanced anti-tumor activity and inhibited metastases without added toxicity in preclinical models. We anticipate reporting interim OS data from this trial in the second half of calendar year 2012 , but this is a time-to-event endpoint and could take longer to reach.

Pancreatic cancer is the fourth leading cause of cancer death. There are approximately 105,000 pancreatic cancer patients treated annually in the U.S., Europe, and Japan. The current market for pancreatic cancer therapeutics is approximately $694 million annually and is expected to approach $830 million annually by 2019 according to independent market research estimates. Current treatment for pancreatic cancer patients includes gemcitabine (Gemzar®) with or without erlotinib (Tarceva®). Patients treated with gemcitabine typically have a time-to-progression of 2-3 months and median OS of approximately 6 months.

| 6 |

Investigator-Sponsored Trials (“IST”) Program

In addition to our Company-sponsored trials, we initiated an IST program for bavituximab as a cost-effective way of generating additional clinical data on bavituximab’s broad therapeutic potential. The investigator plans, designs, and conducts the study under their own Investigational New Drug (“IND”) application. Our goal is to have investigators’ trials supported from a variety of public and private sources, such as governments and foundations, and we will supply the clinical materials of our products produced by our subsidiary Avid Bioservices with modest financial support, if necessary. These multiple small studies can provide additional insight into bavituximab’s mechanism of action, augment our safety database, and evaluate new combination therapy approaches to treating cancer patients. We currently have four ISTs that are enrolling and dosing patients. In March 2012, at the American Academy of Cancer Research (“AACR”) Annual Meeting, preliminary data was presented on three of these four ongoing trials, as further described below.

| — | Advanced Liver Cancer IST. A Phase I/II trial evaluating bavituximab combined with sorafenib (Nexavar®) in up to 50 patients with advanced liver cancer (hepatocellular carcinoma, or HCC) showed that of the nine patients enrolled in the Phase I portion of the study, no dose-limiting toxicities or serious adverse events were observed and the trial is now enrolling in the Phase II part of the study. This trial continues to enroll and dose patients. |

| — | Front-line NSCLC IST. A Phase Ib trial evaluating bavituximab with pemetrexed and carboplatin in up to 25 patients with locally advanced or metastatic NSCLC showed that five patients enrolled with locally advanced or metastatic NSCLC showed a promising safety profile comparable to that expected for the chemotherapy combination alone, with three of the five patients achieving a partial tumor response and no signs of unexpected safety events. This trial continues to enroll and dose patients. |

| — | HER2-negative Metastatic Breast Cancer IST. A Phase I trial evaluating bavituximab combined with paclitaxel in up to 14 patients with HER2-negative metastatic breast cancer showed that five evaluable patients with HER-2 negative metastatic breast cancer showed a promising safety profile comparable to that expected for the chemotherapy combination alone, two patients achieved a complete tumor response, one achieved a partial response, and two had progressive disease according to RECIST measurement criteria. This trial continues to enroll and dose patients. |

| — | Second-line Castration Resistant Prostate Cancer IST. A Phase I/II trial evaluating bavituximab combined with cabazitaxel in up to 31 patients with second-line castration resistant prostate cancer (CRPC) continues to enroll and dose patients. |

PS-Targeting Imaging Program

In addition to our PS-targeting antibodies potential to treat cancer, we believe these antibodies may have broad potential for the imaging and diagnosis of multiple diseases, including cancer. PS-targeting antibodies are able to target diseases that present PS on the surface of distressed cells, which we believe is present in multiple disease settings. In oncology, PS is a molecule usually located inside the membrane of healthy cells, but "flips" and becomes exposed on the outside of cells that line tumor blood vessels, creating a specific target for the imaging of multiple solid tumor types.

Our initial clinical candidate is 124I -PGN650 (“PGN650”), a first-in-class PS-targeting F(ab’)2 fully human monoclonal antibody fragment joined to the positron emission tomography (“PET”) imaging radio-isotope iodine-124 (124I) that represents a potential new approach to imaging cancer. In preclinical studies, PGN650 accumulates in tumor vasculature and provides exceedingly clear in vivo tumor images.

In April 2012, we filed an Investigational New Drug Application with the FDA to advance our lead imaging agent PGN650 into clinical development for the imaging of multiple solid tumor types. Our initial goal for the PGN650 program is to further validate the broad nature of the PS-targeting platform. Results from this study may open the door for multiple applications including development of antibody drug conjugates (“ADC”), the ability of PGN650 to monitor the effectiveness of current standard cancer treatments, and the ability to potentially select patients that may benefit from bavituximab-based treatment. The trial will enroll up to 12 patients. Patients will receive an imaging dose followed by three (3) PET images: two images on day one and one image on either day 2 or 3. Successful results from this trial could support several promising new areas of research in the imaging and diagnostic fields.

| 7 |

Cotara for the Treatment of Brain Cancer

Our novel single-treatment brain cancer therapy Cotara is our first agent based on our Tumor Necrosis Therapy (“TNT”) technology platform. Cotara is a targeted monoclonal antibody conjugated to Iodine 131, a therapeutic radioisotope that is administered as a single-infusion therapy directly into the tumor destroying the tumor from the inside out, with minimal exposure to healthy tissue. In four prior clinical studies, Cotara has demonstrated encouraging survival, localization to the tumor, and an acceptable safety profile in patients with brain cancer.

Cotara has been granted FDA and European Medicines Agency (“EMA”) orphan drug status for glioblastoma multiforme (“GBM”) and anaplastic astrocytoma and fast track designation in the U.S. for the treatment of recurrent GBM.

In our Phase II open-label, multicenter trial, 41 GBM patients at first relapse received a single-treatment with Cotara. The primary endpoint was safety and tolerability of the maximum tolerated dose, a single 25-hour interstitial infusion of 2.5 mCi/cc of Cotara. Secondary endpoints include median OS, median PFS, and proportion of patients alive at six months after treatments. Median OS for patients treated with Cotara was 9.3 months, consistent with a prior Phase II trial. The 6-month, 12-month and 24-month survival estimates are 73%, 38% and 22%, respectively, and two patients survived three years after a single treatment with Cotara.

Cotara was generally safe and well tolerated in this trial. The most common drug-related adverse events (AEs) were neurologic in nature and most were managed with corticosteroids. Based on these data, we continue to have discussions with the FDA to define the optimal registration pathway for Cotara.

According to the American Cancer Society, in 2012 there are expected to be an estimated 22,900 malignant tumors diagnosed and approximately 13,700 deaths attributed to brain or spinal cord cancer in the United States. GBM accounts for about 15% of all brain tumors and primarily occurs in adults between ages of 45 and 70. Overall, the 5-year survival rate is only 5%.

Other Research and Development Programs

Preclinical research conducted by our researchers and collaborators demonstrate that PS becomes exposed on the surface of a broad class of viruses known as enveloped viruses, as well as on the cells they infect. Scientists studying bavituximab believe the drug’s mechanism of action may help reactivate the body's natural immune defenses to destroy both the virus particles and the cells they infect. Since the target for bavituximab is only exposed on diseased cells, healthy cells should not be affected by bavituximab.

We have conducted a randomized Phase II trial for previously untreated genotype 1 chronic HCV patients with bavituximab. In this trial, 66 patients were randomly assigned to one of three treatment arms. Patients received daily oral ribavirin (1000 mg) with either weekly bavituximab (0.3 mg/kg or 3 mg/kg) or pegylated interferon alpha-2a (180 µg) for up to 12 weeks and were tested for safety parameters and antiviral activity.

The primary endpoint of the study is the proportion of patients achieving early virologic response (“EVR”), an early predictor of which patients are likely to clear virus with continued treatment. EVR is defined as a greater than or equal to 2 log reduction in HCV RNA after 12 weeks of treatment. Secondary endpoints include safety, tolerability and HCV viral kinetics.

| 8 |

In December 2011, we announced preliminary data from this trial indicating that both dose levels of bavituximab with ribavirin demonstrated antiviral activity, with patients receiving the 0.3 mg/kg dosing level having a more pronounced antiviral effect. In addition, a comparison of the viral data indicated that the kinetics of antiviral activity were different between the interferon and bavituximab treatment groups with a high percentage of those patients achieving EVR in the interferon arm of the study doing so between week 4 and week 8 and the majority of patients achieving EVR in the bavituximab groups doing so at the week 12 end of study time point. Data also showed that more patients had achieved EVR in the interferon-containing group by the end of the study, however based on the nature of late EVR development in the bavituximab containing arms at the very end of the 12 week trial, a longer-term evaluation would be warranted to adequately compare the effectiveness of bavituximab and interferon. Lastly, data showed that the combination of bavituximab and ribavirin appeared safe and well tolerated with patients reporting fewer side effects than in the interferon-containing arm. We believe that future studies evaluating longer bavituximab treatment durations at or around the lower dose level in combination with ribavirin and potentially direct acting antivirals in certain patient populations may hold promise as interferon-free HCV therapeutic regimens. Our goal is to secure a partner who will lead the future development of this program.

Mechanism of Action of Our Technology Platforms

Our three products in clinical development fall under two technology platforms: PS-targeting technology and Tumor Necrosis Therapy (“TNT”) technology.

PS-Targeting Technology Platform

Peregrine’s new class of PS-targeting therapeutics are monoclonal antibodies that target and bind to components of cells normally found only on the inner surface of the cell membrane. This target is a specific phospholipid known as phosphatidylserine (“PS”). Under stress or apoptosis, PS becomes exposed on the surface of tumor blood vessels and on virus infected cells, exposing a specific target for imaging and therapy of multiple diseases.

PS is a highly immunosuppressive molecule that inactivates the body’s immune system from recognizing the disease. Bavituximab targets and binds to exposed PS on tumor blood vessels and virally infected cells, and has been shown to reactivate the body’s immune system, restoring its ability to recognize and respond to tumors and viruses by blocking PS-mediated immunosuppression.

Tumor Necrosis Therapy (“TNT”) Technology Platform

Peregrine’s targeted TNT technology uses monoclonal antibodies designed to bind to DNA/histone H1 complex which is exposed primarily in the dead and dying cells that are present in abundance at the center of tumors. TNT antibodies are capable of carrying a variety of therapeutic agents, including radioisotopes, into the interior of solid tumors where they kill the tumor from the inside out. Peregrine’s lead TNT-based brain cancer therapy is Cotara, an antibody conjugated to a therapeutic radioisotope that binds to the core of the tumor mass and kills adjacent cells.

In-Licensing Collaborations

The following discussions cover our collaborations and in-licensing obligations related to our products in clinical trials:

PS-Targeting Program

During fiscal year 2011, we expensed $114,000 associated with milestone obligations under in-licensing agreements covering our PS-targeting program, which is included in research and development expense in the accompanying consolidated statements of operations. We did not incur any milestone related expenses during fiscal years 2012 and 2010. In addition, no product revenues have been generated from the PS-targeting program to date. The following represents a summary of our current potential milestone obligations under our various agreements covering our bavituximab and PGN650 programs:

| 9 |

Bavituximab

In August 2001 and August 2005, we exclusively in-licensed the worldwide rights to the PS-targeting technology platform from the UT Southwestern Medical Center at Dallas (“UTSWMC”), including bavituximab. During November 2003, we entered into a non-exclusive license agreement with Genentech, Inc., to license certain intellectual property rights covering methods and processes for producing antibodies used in connection with the development of our PS-targeting program. During December 2003, we entered into an exclusive commercial license agreement with Avanir Pharmaceuticals, Inc., (“Avanir”) covering the generation of a chimeric monoclonal antibody. In March 2005, we entered into a worldwide non-exclusive license agreement with Lonza Biologics (“Lonza”) for intellectual property and materials relating to the expression of recombinant monoclonal antibodies for use in the manufacture of bavituximab.

Under our in-licensing agreements relating to bavituximab, we typically pay an up-front license fee, annual maintenance fees, and are obligated to pay future milestone payments based on potential clinical development and regulatory milestones, plus a royalty on net sales and/or a percentage of sublicense income. The applicable royalty rate under each of the foregoing in-licensing agreements is in the low single digits. The following table provides certain information with respect to each of our in-licensing agreements relating to our bavituximab program.

| Licensor | Agreement Date | Expiration Date | Total Milestones Incurred To Date | Potential Future Milestone Obligations (1) | ||||||||||||

| UTSWMC | August 2001 | (2) | $ | 98,000 | $ | 375,000 | ||||||||||

| UTSWMC | August 2005 | (3) | $ | 85,000 | $ | 375,000 | ||||||||||

| Lonza | March 2005 | (4) | $ | 64,000 | (5 | ) | ||||||||||

| Avanir | December 2003 | (6) | $ | 50,000 | $ | 1,050,000 | ||||||||||

| Genentech, Inc. | November 2003 | December 2018 | $ | 500,000 | $ | 5,000,000 | ||||||||||

| Total | $ | 797,000 | $ | 6,800,000 | ||||||||||||

| (1) | Potential future milestone obligations are generally tied to regulatory progress to gain product approval, which approval significantly depends on positive clinical trials results. In addition, potential future milestone obligations vary by license agreement (as defined in each license agreement) and depend on valid claims under each of these underlying agreements at the time the potential milestone is achieved, however, the following clinical development and regulatory milestones are typical of such potential future milestone events: upon dosing of first patient in a Phase I, Phase II, and/or Phase III clinical trial; completion of patient enrollment in a phase II trial; submission of a biologics license application in the U.S.; and upon FDA approval. |

| (2) | Expiration date of the license agreement occurs upon expiry of underlying patents. These patents, and certain related patent applications that may issue as patents, are currently set to expire between 2019 and 2021. |

| (3) | Expiration date of the license agreement occurs upon expiry of underlying patents. These patents, and certain related patent applications that may issue as patents, are currently set to expire between 2023 and 2025. |

| (4) | Expiration date of the license agreement is 15 years from first commercial sale or upon expiry of underlying patents, whichever occurs last. The last patent covered under this license agreement expires in November 2016. |

| (5) | In fiscal year 2011, we incurred a milestone fee of 37,500 pounds sterling ($64,000 U.S.) upon commencement of patient enrollment in our first randomized phase II clinical trial using bavituximab, which amount would continue as an annual license fee thereafter until completion of patient enrollment, at which time the annual license fee would increase to 75,000 pounds sterling per annum. During fiscal year 2012, we completed patient enrollment of the aforementioned phase II clinical trial, which triggered the annual license fee to increase to 75,000 pounds sterling per annum (or approximately $122,000 U.S. based on the exchange rate at April 30, 2012). In addition, in the event we utilize an outside contract manufacturer other than Lonza to manufacture bavituximab for commercial purposes, we would owe Lonza 300,000 pounds sterling per year (or approximately $488,000 U.S. based on the exchange rate at April 30, 2012). |

| (6) | Expiration date of license agreement is 10 years from first commercial sale in each respective country. |

| 10 |

Of the total potential future milestone obligation of $6,800,000, we anticipate milestone obligations not to exceed $200,000 during fiscal year 2013. In addition, of the total potential future milestone obligations of $6,800,000, up to $6,400,000 would be due upon the first commercial approval of a drug candidate developed under our PS-targeting program, including bavituximab, with the technologies licensed pursuant to such license agreements. However, given the uncertainty of the drug development and the regulatory approval process, we are unable to predict with any certainty when any of these milestones will occur, if at all.

PGN650

In October 1998, we exclusively in-licensed worldwide rights from UTSWMC, to certain patent families, which was amended in January 2000 to license patents related to aminophospholipid targeting conjugates, such as PGN650. Under the October 1998 license agreement, as amended, we are obligated to pay UTSWMC future milestone payments of up to $300,000 for PGN650 based on the achievement of certain potential clinical development and commercial milestones, plus a low single digit royalty on net sales. Under this agreement, we do not anticipate any milestone obligations during fiscal year 2013.

In addition, during fiscal year 2007, we entered into a research collaboration agreement and a development and commercialization agreement with Affitech A/S regarding the generation and commercialization of a certain number of fully human monoclonal antibodies under our platform technologies to be used as possible future clinical candidates, including our imaging agent PGN650. Under the terms of the development and commercialization agreement, we have elected to enter into a license agreement for the PS-targeting antibody used to create PGN650, and therefore, are obligated to pay future milestones payments of up to $1,971,000 based on the achievement of certain potential clinical development and regulatory milestones, plus a low single digit royalty on net sales. We anticipate milestone obligations for PGN650 under this agreement to not exceed $101,000 during fiscal year 2013.

Tumor Necrosis Therapy (Cotara)

We acquired the patent rights to the Tumor Necrosis Therapy (“TNT”) technology, including Cotara, in July 1994 after the merger between Peregrine and Cancer Biologics, Inc. was approved by our stockholders. To date, no product revenues have been generated from Cotara.

In October 2004, we entered into a worldwide non-exclusive license agreement with Lonza for intellectual property and materials relating to the expression of recombinant monoclonal antibodies for use in the manufacture of Cotara. Under the terms of the agreement, we will pay a royalty (in the low single digits) on net sales of any products we market that utilize the underlying technology. In the event a product is approved and we or Lonza do not manufacture Cotara, we would owe Lonza 300,000 pounds sterling per year (or approximately $488,000 U.S. based on the exchange rate at April 30, 2012) in addition to an increased royalty (in the low single digits) on net sales. In addition, upon completion of patient enrollment in our Cotara Phase II clinical trial during fiscal year 2011, we incurred a milestone payment of 75,000 pounds sterling (or $125,000 U.S.), which amount will continue as an annual license fee thereafter. Unless sooner terminated due to a party’s breach of the license agreement, the license agreement with Lonza will terminate upon the last to occur of the expiration of a period of fifteen (15) years following our first commercial sale of a product or the expiration of the last valid claim within the patents that are the subject of the license agreement; provided that if after the expiration of the last claim but prior to the expiration of the fifteen (15) year period, Lonza has publicly made available certain materials and know how, then the agreement will terminate at such time as the materials and know how are made public.

Out-Licensing Collaborations

The following represents a summary of our key out-licensing collaborations:

In October 2000, we entered into a licensing agreement with Merck KGaA to out-license a segment of our TNT technology for use in the application of cytokine fusion proteins. During January 2003, we entered into an amendment to the license agreement, whereby we received an extension to the royalty period from six years to ten years from the date of the first commercial sale. Under the terms of the agreement, we would receive a royalty on net sales if a product is approved under the agreement. Merck KGaA has not publicly disclosed the current development status of its program.

| 11 |

In July 2009, we entered into a patent assignment and sublicense agreement (collectively, the “Affitech Agreements”) with Affitech A/S (“Affitech”), whereby we licensed exclusive worldwide rights to develop and commercialize certain products under our anti-VEGF intellectual property portfolio, including the fully human antibody AT001/r84. We recognized revenue of $350,000 during fiscal years 2012 and 2011 and $243,000 during fiscal year 2010 under the Affitech Agreements, which amounts are included in license revenue in the accompanying consolidated financial statements. During September 2010, Peregrine and Affitech amended certain terms of the Affitech Agreements for sublicenses entered into by Affitech with non-affiliates for the territories of Brazil, Russia and other countries of the Commonwealth of Independent States (CIS) (“September 2010 Amendment”). Under the amended terms, Peregrine and Affitech will reinvest their respective portions of any future milestone payments to be received under the agreements for the countries of Brazil, Russia and the CIS toward the further development of AT001/r84. In the event Affitech enters into a licensing deal for AT001/r84 with a non-affiliate in a major pharmaceutical market (defined as U.S., European Union, Switzerland, United Kingdom and/or Japan), Affitech has agreed to reimburse us for our milestone payments that were applied to the AT001/r84 program while Affitech will be eligible to be reimbursed for up to 50% of their development costs in Brazil, Russia and CIS territories. The remaining terms of the Affitech Agreements remain unchanged, including milestone and royalty payments. As of April 30, 2012, we have not received any payments from Affitech under the September 2010 Amendment.

In May 2010, we entered into an assignment agreement and a license agreement (collectively, the “Agreements”) with an unrelated entity to develop our TNT technologies in certain Asia-Pacific Economic Cooperation (APEC) countries. Under the terms of the Agreements, we licensed certain non-exclusive and exclusive rights and assigned certain exclusive development and commercialization rights under our TNT program in certain APEC countries. We have retained exclusive rights to our TNT program in the United States, European Union countries, and other select countries internationally. Under the terms of the Agreements, we could receive low double digit royalties on net sales, as defined in the Agreements. During fiscal year 2012, we recognized revenue of $100,000 under the Agreements, which amount is included in license revenue in the accompanying consolidated financial statements. No revenue was recognized under the Agreements during fiscal year 2011.

Avid Bioservices, Inc., Integrated Biomanufacturing Subsidiary

Our wholly-owned subsidiary, Avid Bioservices, Inc. (“Avid”) is a Contract Manufacturing Organization (“CMO”) that provides fully-integrated services from cell line development to commercial current Good Manufacturing Practices (“cGMP”) biomanufacturing for Peregrine and Avid’s third-party clients. Avid’s total revenue generated from third-party customers for fiscal years 2012, 2011, and 2010 amounted to $14,783,000, $8,502,000, and $13,204,000, respectively.

Avid manufactures cGMP commercial and clinical products and has over 10 years of experience developing and producing monoclonal antibodies, recombinant proteins and enzymes in batch, fed-batch and perfusion modes. Avid provides an array of contract biomanufacturing services, including contract manufacturing of antibodies, recombinant proteins and enzymes; cell culture development; process development; and testing of biologics for biopharmaceutical and biotechnology companies under cGMP. In its cGMP manufacturing suite, Avid maintains four bioreactors: two 1,000 liter, a 300 liter, and a 100 liter.

Operating a cGMP facility requires highly specialized personnel and equipment that must be maintained on a continual basis. Prior to the formation of Avid, we manufactured our own antibodies for more than 10 years and developed the manufacturing expertise and quality systems to provide the same service to other biopharmaceutical and biotechnology companies.

The manufacturing of monoclonal antibodies and recombinant proteins under cGMP is a complex process that includes several phases before the finished drug product is released for clinical or commercial use. The first phase of the manufacturing process, called technology transfer phase, is to receive the production cell line (the cells that produce the desired protein) and any available process information from the client. The cell line must be adequately tested according to FDA guidelines and/or other regulatory guidelines to certify that it is suitable for cGMP manufacturing.

| 12 |

The second phase of the process is in the manufacturing facility. Once the process is developed, pilot runs are generally performed using smaller scale bioreactors, such as the 36 or 100 liter bioreactors, in order to verify the process. Once the process is set, the process will be transferred to GMP manufacturing and a pilot run(s) or full scale engineering run(s) will be performed to finalize manufacturing batch records. After completing the pilot batch run(s), full-scale cGMP manufacturing is typically initiated. Once the cGMP run(s) is completed, batch samples are taken for various required tests, including sterility and viral testing. Once the test results verify that the material meets specifications, the material and/or product is released for its intended use.

Each batch manufactured is tailored to meet the specific needs of Peregrine or the client. Full process development from start to finish can take ten months or longer. All stages of manufacturing can generally take from one to several weeks depending on the manufacturing method and process. Material or product testing and release can take up to an additional three months to complete once the manufacturing process is complete.

Given its inherent complexity, necessity for detail, and magnitude (contracts may be into the millions of dollars), contract negotiations and sales cycle for cGMP manufacturing services can take a significant amount of time. Our anticipated sales cycle from client introduction to signing an agreement will take anywhere from between six months to more than one year.

To date, Avid has been audited and qualified by large and small, domestic and foreign, biotechnology companies interested in the production of biologic material for clinical and commercial use. Additionally, Avid has been audited by the European Regulatory authorities, the FDA and the California Department of Health.

Government Regulation

Regulation by governmental authorities in the U.S. and other countries is a significant factor in our ongoing research and development activities and in the production of our products under development. Our products and our research and development activities are subject to extensive governmental regulation in the U.S., including the Federal Food, Drug, and Cosmetic Act, as amended, the Public Health Service Act, also as amended, as well as to other federal, state, and local statutes and regulations. These laws, and similar laws outside the U.S., govern the clinical and non-clinical testing, manufacture, safety, effectiveness, approval, labeling, distribution, sale, import, export, storage, record keeping, reporting, advertising and promotion of our products, if approved. Violations of regulatory requirements at any stage may result in various adverse consequences, including regulatory delay in approving or refusal to approve a product, enforcement actions, including withdrawal of approval, labeling restrictions, seizure of products, fines, injunctions and/or civil or criminal penalties. Any product that we develop must receive all relevant regulatory approvals or clearances before it may be marketed in a particular country.

The regulatory process, which includes extensive preclinical testing and clinical trials of each product candidate to study its safety and efficacy, is uncertain, takes many years and requires the expenditure of substantial resources. We cannot assure you that the clinical trials of our product candidates under development will demonstrate the safety and efficacy of those product candidates to the extent necessary to obtain regulatory approval.

The activities required before a product may be marketed in the U.S., such as Cotara or bavituximab, are generally performed in the following sequential steps:

| 1. | Preclinical testing. This generally includes evaluation of our products in the laboratory or in animals to characterize the product and determine safety and efficacy. Some preclinical studies must be conducted by laboratories that comply with FDA regulations regarding good laboratory practice. | |

| 2. | Submission to the FDA of an Investigational New Drug application (“IND”). The results of preclinical studies, together with manufacturing information, analytical data and proposed clinical trial protocols, are submitted to the FDA as part of an IND, which must become effective before the clinical trials can begin. Once a new IND is filed, the FDA has 30 days to review the IND. The IND will automatically become effective 30 days after the FDA received the application, unless the FDA indicates prior to the end of the 30-day period that the application raises concerns that must be resolved to the FDA’s satisfaction before clinical trials may proceed. If the FDA raises concerns at any time, we may be unable to resolve the issues in a timely fashion, if at all. |

| 13 |

| 3. | Completion of clinical trials. Human clinical trials are necessary to seek approval for a new drug or biologic and typically involve a three-phase process. In Phase I, small clinical trials are generally conducted to determine the safety of the product. In Phase II, clinical trials are generally conducted to assess safety, acceptable dose, and gain preliminary evidence of the efficacy of the product. In Phase III, clinical trials are generally conducted to provide sufficient data for the statistically valid proof of safety and efficacy. A clinical trial must be conducted according to good clinical practices under protocols that detail the trial’s objectives, inclusion and exclusion criteria, the parameters to be used to monitor safety and the efficacy criteria to be evaluated, and informed consent must be obtained from all study subjects. Each protocol involving U.S. trial sites must be submitted to the FDA as part of the IND. The FDA may impose a clinical hold on an ongoing clinical trial if, for example, safety concerns arise, in which case the study cannot recommence without FDA authorization under terms sanctioned by the Agency. Similarly, trials conducted outside the U.S. require notification and/or approval by the governing Health Authority (“HA”). In addition, before a clinical trial can be initiated, each clinical site or hospital administering the product must have the protocol reviewed and approved by an institutional review board (“IRB”) or independent ethics committee (“IEC”). The IRB/IEC will consider, among other things, ethical factors and the safety of human subjects. The IRB/IEC may require changes in a protocol, which may delay initiation or completion of a study. Phase I, Phase II or Phase III clinical trials may not be completed successfully within any specific period of time, if at all, with respect to any of our potential products. Furthermore, we, the HA (including the FDA) or an IRB/IEC may suspend a clinical trial at any time for various reasons, including a finding that the healthy individuals or patients are being exposed to an unacceptable health risk. | |

| 4. | Submission to the FDA of a Biologics License Application (“BLA”) or New Drug Application (“NDA”). After completion of clinical studies for an investigational product, a BLA or NDA is submitted to the FDA for product marketing approval. No action can be taken to market any new drug or biologic product in the U.S. until the FDA has approved an appropriate marketing application. | |

| 5. | FDA review and approval of the BLA or NDA before the product is commercially sold or shipped. The results of preclinical studies, clinical trials, and manufacturing information are submitted to the FDA in the form of a BLA or NDA for approval of the manufacture, marketing and commercial shipment of the product. The FDA may take a number of actions after the BLA or NDA is filed, including but not limited to, denying the BLA or NDA if applicable regulatory criteria are not satisfied, requiring additional clinical testing or information; or requiring post-market testing and surveillance to monitor the safety or efficacy of the product. Adverse events that are reported after marketing approval can result in additional limitations being placed on the product’s use and, potentially, withdrawal of the product from the market. Any adverse event, either before or after marketing approval, can result in product liability claims against us. | |

In addition, we are subject to regulation under state, federal, and international laws and regulations regarding occupational safety, laboratory practices, the use and handling of radioactive isotopes, environmental protection and hazardous substance control, and other regulations. Our clinical trial and research and development activities involve the controlled use of hazardous materials, chemicals and radioactive compounds. Although we believe that our safety procedures for handling and disposing of such materials comply with the standards prescribed by state and federal regulations, the risk of accidental contamination or injury from these materials cannot be completely eliminated. In the event of such an accident, we could be held liable for any damages that result and any such liability could exceed our financial resources. In addition, disposal of radioactive materials used in our clinical trials and research efforts may only be made at approved facilities. We believe that we are in material compliance with all applicable laws and regulations including those relating to the handling and disposal of hazardous and toxic waste.

| 14 |

Our product candidates, if approved, may also be subject to import laws in other countries, the food and drug laws in various states in which the products are or may be sold and subject to the export laws of agencies of the U.S. government.

In addition, we must also adhere to current Good Manufacturing Practice (“cGMP”) and product-specific regulations enforced by the FDA through its facilities inspection program. Failure to comply with manufacturing regulations can result in, among other things, warning letters, fines, injunctions, civil penalties, recall or seizure of products, total or partial suspension of production, refusal of the government to renew marketing applications and criminal prosecution.

During fiscal year 1999, the Office of Orphan Products Development of the FDA determined that Cotara qualified for orphan designation for the treatment of glioblastoma multiforme and anaplastic astrocytoma (both brain cancers). The 1983 Orphan Drug Act (with amendments passed by Congress in 1984, 1985, and 1988) includes various incentives that have stimulated interest in the development of orphan drug and biologic products. These incentives include a seven-year period of marketing exclusivity for approved orphan products, tax credits for clinical research, protocol assistance, and research grants. Additionally, legislation re-authorizing FDA user fees also created an exemption for orphan products from fees imposed when an application to approve the product for marketing is submitted. A grant of an orphan designation is not a guarantee that a product will be approved. If a sponsor receives orphan drug exclusivity upon approval, there can be no assurance that the exclusivity will prevent another entity from receiving approval for the same or a similar drug for the same or other uses.

Cotara was granted Fast Track designation by the FDA for the treatment of recurrent glioblastoma multiforme. This designation facilitates the development and expedites the review of new drugs that are intended to treat serious or life-threatening conditions and that demonstrate the potential to address unmet medical needs. The Fast Track mechanism is described in the Food and Drug Administration Modernization Act of 1997 (“FDAMA”). The benefits of Fast Track include scheduled meetings to seek FDA input into development plans, the option of submitting an NDA in sections rather than all components simultaneously, and the option of requesting evaluation of studies using surrogate endpoints.

Manufacturing and Raw Materials

Manufacturing. We manufacture pharmaceutical-grade products to supply our clinical trials through our wholly owned subsidiary, Avid Bioservices, Inc. We have assembled a team of experienced scientific, production and regulatory personnel to facilitate the manufacturing of our antibodies, including bavituximab and Cotara.

Our bavituximab product is shipped directly from our facility to the clinical trial sites or to third party depots that distribute the clinical trial materials to clinical sites. Our TNT antibodies are shipped to a third party facility for radiolabeling (the process of attaching the radioactive agent, Iodine 131, to the antibody). From the radiolabeling facility, Cotara (the radiolabeled-TNT antibodies) is shipped directly to the clinical sites for use in clinical trials.

Any commercial radiolabeling supply arrangement will require a significant investment of funds by us in order for a radiolabeling vendor to develop the expanded facilities necessary to support our product. There can be no assurance that material produced by our current radiolabeling supplier will be suitable for commercial quantities to meet the possible demand of Cotara, if approved. We will continue with our research in radiolabeling scale-up, but we believe this research will be eventually supported by a potential licensing or marketing partner for Cotara.

Raw Materials. Various common raw materials are used in the manufacture of our products and in the development of our technologies. These raw materials are generally available from several alternate distributors of laboratory chemicals and supplies. We have not experienced any significant difficulty in obtaining these raw materials and we do not consider raw material availability to be a significant factor in our business.

| 15 |

Patents and Trade Secrets

Peregrine continues to seek patents on inventions originating from ongoing research and development activities within the Company and in collaboration with other companies and university researchers. In addition to seeking patent protection in the U.S., we typically file patent applications in Europe, Canada, Japan and additional countries on a selective basis. Patents, issued or applied for, cover inventions relating in general to cancer therapy and anti-viral therapy and in particular to different proteins, peptides, antibodies and conjugates, methods and devices for labeling antibodies, and therapeutic and diagnostic uses of the peptides, antibodies and conjugates. We intend to pursue opportunities to license these technologies and any advancements or enhancements, as well as to pursue the incorporation of our technologies in the development of our own products.

Our issued patents extend for varying periods according to the date of patent application filing and/or grant and the legal term of patents in the various countries where patent protection is obtained. In the U.S., patents issued on applications filed prior to June 8, 1995 have a term of 17 years from the issue date or 20 years from the earliest effective filing date, whichever is longer. U.S. patents issued on applications filed on or after June 8, 1995, have a term first calculated as 20 years from the earliest effective filing date, not counting any provisional application filing date. Certain U.S. patents issued on applications filed on or after June 8, 1995, and particularly on applications filed on or after May 29, 2000, are eligible for Patent Term Adjustment (“PTA”), which extends the term of the patent to compensate for delays in examination at the U.S. Patent and Trademark Office. The term of foreign patents varies in accordance with provisions of applicable local law, but is typically 20 years from the effective filing date, which is often the filing date of an application under the provisions of the Patent Cooperation Treaty (“PCT”).

In addition, in certain cases, the term of U.S. and foreign patents can be extended to recapture a portion of the term effectively lost as a result of health authority regulatory review. As such, certain U.S. patents may be eligible for Patent Term Extension under 35 U.S.C. § 156 (known as “the Hatch-Waxman Act”) to restore the portion of the patent term that has been lost as a result of review at the U.S. FDA. Such extensions, which may be up to a maximum of five years (but cannot extend the remaining term of a patent beyond a total of 14 years), are potentially available to one U.S. patent that claims an approved human drug product (including a human biological product), a method of using a drug product, a method of manufacturing a drug product, or a medical device.

We consider that in the aggregate our patents, patent applications and licenses under patents owned by third parties are of material importance to our operations. Of the patent portfolios that are owned, controlled by or exclusively licensed to Peregrine, those concerning our PS-Targeting Technology Platform and our TNT Technology Platform are of particular importance to our operations.

Our patent portfolios relating to the PS-Targeting Technology Platform in oncology include U.S. and foreign patents and patent applications with claims directed to methods, compositions and combinations for targeting tumor vasculature and imaging and treating cancer using antibodies and conjugates that localize to the aminophospholipids, PS (Phosphatidylserine) and PE (Phosphatidylethanolamine), exposed on tumor vascular endothelial cells. These patents, and any related patent applications that may issue as patents, are currently set to expire between 2019 and 2021.

Our patent portfolios relating to the PS-Targeting Technology Platform in the viral field include U.S. and foreign patents and patent applications with claims directed to methods, compositions and combinations for inhibiting viral replication or spread and for treating viral infections and diseases using antibodies and conjugates that localize to the aminophospholipids, PS and PE, exposed on viruses and virally-infected cells. These patents, and certain related patent applications that may issue as patents, are currently set to expire in 2023.

Additionally, we have U.S. and foreign patents and patent applications relating more specifically to our product, bavituximab, including compositions, combinations and methods of use in treating angiogenesis and cancer and in treating viral infections and diseases. These patents, and certain related patent applications that may issue as patents, are currently set to expire between 2023 and 2025.

| 16 |

Our patent portfolios relating to the TNT Technology Platform, which includes our Cotara product, include U.S. and foreign patents with claims directed to compositions of matter and claims directed to diagnostic methods, which patents are currently set to expire in 2017 and 2016, respectively. Our TNT Technology Platform and Cotara product are also protected by patents and patent applications that include claims directed to methods and apparatus for radiolabeling and to the resultant radiolabeled products. The radiolabeling patents in the U.S. and overseas, and any related patent applications that may issue as patents, are currently set to expire between 2024 and 2028.

The information given above is based on our current understanding of the patents and patent applications that we own, control, or have exclusively licensed. The information is subject to revision, for example, in the event of changes in the law or legal rulings affecting our patents or if we become aware of new information. In particular, the expiry information given above does not account for possible extension of any U.S. or foreign patent to recapture patent term effectively lost as a result of FDA or other health authority regulatory review. We intend to seek such extensions, as appropriate to approved product(s), which may be up to a maximum of five years (but not extending the term of a patent beyond 14 years).

The actual protection afforded by a patent, which can vary from country to country, depends upon the type of patent, the scope of its coverage and the availability of legal remedies in the country. We have either been issued patents or have patent applications pending that relate to a number of current and potential products including products licensed to others. In general, we have obtained licenses from various parties that we deem to be necessary or desirable for the manufacture, use or sale of our products. These licenses (both exclusive and non-exclusive) generally require us to pay royalties to the parties. The terms of the licenses, obtained and that we expect to be obtained, are not expected to significantly impact the cost structure or marketability of the Company’s products.

In general, the patent position of a biotechnology firm is highly uncertain and no consistent policy regarding the breadth of issued claims has emerged from the actions of the U.S. Patent Office and courts with respect to biotechnology patents. Similar uncertainties also exist for biotechnology patents in important overseas markets. Accordingly, there can be no assurance that our patents, including those issued and those pending, will provide protection against competitors with similar technology, nor can there be any assurance that such patents will not be legally challenged, invalidated, infringed upon and/or designed around by others.

International patents relating to biologics are numerous and there can be no assurance that current and potential competitors have not filed or in the future will not file patent applications or receive patents relating to products or processes utilized or proposed to be used by the Company. In addition, there is certain subject matter which is patentable in the U.S. but which may not generally be patentable outside of the U.S. Statutory differences in patentable subject matter may limit the protection the Company can obtain on some of its products outside of the U.S. These and other issues may prevent the Company from obtaining patent protection outside of the U.S. Failure to obtain patent protection outside the U.S. may have a material adverse effect on the Company’s business, financial condition and results of operations.

No one has sued us for infringement and no third party has asserted their patents against us that we believe are of any merit. However, there can be no assurances that such lawsuits have not been or will not be filed and, if so filed, that we will prevail or be able to reach a mutually beneficial settlement.

| 17 |

We also intend to continue to rely upon trade secrets and improvements, unpatented proprietary know-how, and continuing technological innovation to develop and maintain our competitive position in research and development of therapeutic and diagnostic products. We typically place restrictions in our agreements with third parties, which contractually restrict their right to use and disclose any of the Company’s proprietary technology with which they may be involved. In addition, we have internal non-disclosure safeguards, including confidentiality agreements, with our employees. There can be no assurance, however, that others may not independently develop similar technology or that the Company’s secrecy will not be breached.

Customer Concentration and Geographic Area Financial Information

We are currently in the research and development phase for all of our products and we have not generated any product sales from any of our technologies under development. For financial information concerning Avid’s customer concentration and geographic areas of its customers, see Note 12, “Segment Reporting” to the accompanying consolidated financial statements.

Marketing Our Potential Products

We intend to sell our products, if approved, in the U.S. and internationally in collaboration with marketing partners or through a direct sales force. If the FDA approves bavituximab or Cotara or our other product candidates under development, the marketing of these product candidates will be contingent upon us entering into an agreement with a company to market our products or upon us recruiting, training and deploying our own sales force, either internally or through a contract sales organization. We do not presently possess the resources or experience necessary to market bavituximab, Cotara, or any of our other product candidates and we currently have no arrangements for the distribution of our product candidates, if approved. Development of an effective sales force requires significant financial resources, time, and expertise. There can be no assurance that we will be able to obtain the financing necessary to establish such a sales force in a timely or cost effective manner or that such a sales force will be capable of generating demand for our product candidates.

Competition

The pharmaceutical and biotechnology industry is intensely competitive and subject to rapid and significant technological change. Many of the drugs that we are attempting to discover or develop will be competing with existing therapies. In addition, we are aware of several pharmaceutical and biotechnology companies actively engaged in research and development of antibody-based products that have commenced clinical trials with, or have successfully commercialized, antibody products. Some or all of these companies may have greater financial resources, larger technical staffs, and larger research budgets than we have, as well as greater experience in developing products and running clinical trials. We expect to continue to experience significant and increasing levels of competition in the future. In addition, there may be other companies which are currently developing competitive technologies and products or which may in the future develop technologies and products that are comparable or superior to our technologies and products.

Bavituximab is currently in clinical trials for the treatment of advanced solid tumors, including NSCLC and pancreatic cancer. Although we are not aware of any other products in clinical development targeting PS as a potential therapy for advanced solid tumors, there are a number of possible competitors with approved or developmental targeted agents used alone or in combination with standard chemotherapy for the treatment of cancer, including but not limited to, Avastin® (bevacizumab) by Roche/Genentech, Gleevec® (imatinib) by Novartis, Tarceva® (erlotinib) by OSI Pharmaceuticals, Inc. and Roche/Genentech, Erbitux® (Cetuximab) by ImClone Systems Incorporated and Bristol-Myers Squibb Company, Rituxan® (rituximab) and Herceptin® (trastuzumab) by Roche/Genentech, Vectibix® (panitumumab) by Amgen, afatinib by Boehringer Ingelheim, XALKORI® (crizotinib) by Pfizer, iniparib by Sanofi-Aventis, ganetespib by Synta Pharmaceuticals, ARQ-197 by ArQule and Daiichi Sankyo, and Yervoy® (ipilimumab) by Bristol-Myers Squibb Company. Additional possible competitors also exist with approved or developmental immunotherapies including but not limited to Provenge® (sipuleucel-T) and other Active Cellular Immunotherapy candidates by Dendreon, Emepepimut-S by Biomira and EMD Serono, and Astuprotimut-r by GlaxoSmithKline. There are a significant number of companies developing cancer therapeutics using a variety of targeted and non-targeted approaches. A direct comparison of these potential competitors will not be possible until bavituximab advances to later-stage clinical trials.

| 18 |

In addition, we are evaluating bavituximab in combination with ribavirin as a potential replacement for the pegylated interferon alpha component for the current standard of care for HCV. We are aware of no other products in clinical development targeting PS as a potential therapy for HCV. There are a number of companies that have products approved and on the market for the treatment of HCV, including but not limited to: Peg-Intron® (pegylated interferon-alpha-2b), Rebetol® (ribavirin), which are marketed by Merck, and Pegasys® (pegylated interferon-alpha-2a) and Copegus® (ribavirin USP), which are marketed by Roche, INCIVEKTM (telaprevir) by Vertex, Victrelis® (boceprevir) by Merck, and Infergen® (interferon alfacon-1) marketed by Three Rivers Pharmaceuticals, LLC. The cornerstone of HCV therapy remains pegylated interferon alpha with ribavirin and recently approved telaprevir or boceprevir are being added to this regimen. Pegylated interferon alpha is generally associated with considerable toxicity including flu-like symptoms, hematologic changes and central nervous system side effects including depression and it is not uncommon for patients to discontinue therapy because they are unable to tolerate the side effects.