Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - TAURIGA SCIENCES, INC. | Financial_Report.xls |

| EX-32.1 - CERTIFICATION - TAURIGA SCIENCES, INC. | nvnc_ex321.htm |

| EX-31.1 - CERTIFICATION - TAURIGA SCIENCES, INC. | nvnc_ex311.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

þ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended March 31, 2012

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______ to ______.

Commission File Number:000-53723

IMMUNOVATIVE, INC.

(f/k/a Novo Energies Corporation)

(Exact name of registrant as specified in its charter)

|

Florida

|

65-1102237

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(IRS Employer Identification No.)

|

|

|

417, Rue St-Pierre, Suite 804

Montreal, QC

|

H2Y 2M3

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code: (514) 840-3697

Securities registered under Section 12(b) of the Exchange Act:

None

Securities registered under Section 12(g) of the Exchange Act:

Common Stock, $.00001 Par Value

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o Yes þ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.o Yes þ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the issuer was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. þ Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).x Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company filer. See definition of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).o Yes þ No

On September 30, 2011, the last business day of the registrant’s most recently completed second quarter, the aggregate market value of the Common Stock held by non-affiliates of the registrant was $11,781,807, based upon the closing price on that date of the Common Stock of the registrant on the OTC Bulletin Board system of $0.175. For purposes of this response, the registrant has assumed that its directors, executive officers and beneficial owners of 5% or more of its Common Stock are deemed affiliates of the registrant.

As of as of July 9, 2012 the registrant had 134,546,457 shares of its Common Stock, $0.00001 par value, outstanding.

TABLE OF CONTENTS

|

Page

|

|||||

|

PART I.

|

|||||

|

Item 1.

|

Business

|

4 | |||

|

Item 1.A.

|

Risk Factors

|

17 | |||

|

Item 1.B.

|

Unresolved Staff Comments

|

25 | |||

|

Item 2.

|

Properties

|

25 | |||

|

Item 3.

|

Legal Proceedings

|

25 | |||

|

Item 4.

|

Mine Safety Disclosures

|

25 | |||

|

PART II.

|

|||||

|

Item 5.

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

26 | |||

|

Item 6.

|

Selected Financial Data

|

28 | |||

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operation

|

28 | |||

|

Item 7A.

|

Quantitative and Qualitative Disclosures About Market Risk

|

32 | |||

|

Item 8.

|

Financial Statements and Supplementary Data

|

33 | |||

|

Item 9.

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure

|

33 | |||

|

Item 9A.

|

Controls and Procedures

|

34 | |||

|

Item 9B.

|

Other Information

|

34 | |||

|

PART III.

|

|||||

|

Item 10.

|

Directors, Executive Officers and Corporate Governance

|

36 | |||

|

Item 11.

|

Executive Compensation

|

37 | |||

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

39 | |||

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence

|

40 | |||

|

Item 14.

|

Principal Accounting Fees and Services

|

40 | |||

|

PART IV.

|

|||||

|

Item 15.

|

Exhibits, Financial Statement Schedules

|

41 | |||

| Signatures | 42 | ||||

| Exhibits | |||||

2

FORWARD LOOKING STATEMENTS

This report on Form 10-K contains forward-looking statements within the meaning of Rule 175 of the Securities Act of 1933, as amended, and Rule 3b-6 of the Securities Act of 1934, as amended, that involve substantial risks and uncertainties. These forward-looking statements are not historical facts, but rather are based on current expectations, estimates and projections about our industry, our beliefs and our assumptions. Words such as “anticipate,” “expects,” “intends,” “plans,” “believes,” “seeks” and “estimates” and variations of these words and similar expressions are intended to identify forward-looking statements. These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond our control and difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements. You should not place undue reliance on these forward-looking statements, which apply only as of the date of this Form 10-K. Investors should carefully consider all of such risks before making an investment decision with respect to the Company’s stock. The following discussion and analysis should be read in conjunction with our consolidated financial statements for Immunovative, Inc. Such discussion represents only the best present assessment from our Management.

3

PART I

Background

We are a Florida corporation formed on April 8, 2001. We were originally organized to be a blank check company.

On June 8, 2009, the Board of Directors approved the change of name to “Novo Energies Corporation”. As described in a report filed with the U.S. Securities and Exchange Commission on June 26, 2009, a majority of shareholders executed a written consent in lieu of an Annual Meeting (the “Written Consent”) effecting the change of the name of our business from “Atlantic Wine Agencies, Inc.” to “Novo Energies Corporation” on June 8, 2009 to better reflect what we then intended to be our future operations. We filed an amendment to our Articles of Incorporation on June 8, 2009 with the Florida Secretary of State to affect this name change after receiving the requisite corporate approval.

On June 23, 2009, the Board of Directors approved a 3-for-1 forward stock split. Accordingly, all share and per share amounts have been retroactively adjusted in the accompanying financial statements.

On July 30, 2009, Novo Energies Corporation(“Novo”) formed a wholly-owned subsidiary - WTL Renewable Energy, Inc. (“WTL”). WTL was established as a Canadian Federal Corporation whose business is to initially research available technologies capable of transforming plastic and tires into useful energy commodities. Simultaneously, WTL also intended to plan, build, own, and operate renewable energy plants throughout Canada utilizing a third party technology and using plastic and tire waste as feedstock. On May 8, 2012, the name was changed to Immunovative Canada, Inc.

On May 17, 2011, Novo entered into an exclusive memorandum of understanding with Immunovative Clinical Research, Inc. (“ICRI”), a Nevada corporation and wholly-owned subsidiary of Immunovative Therapies, Ltd. (“ITL”), an Israeli corporation pursuant to which the Company and ICRI intended to pursue a merger resulting in Novo owning ICRI.

Present

License Agreement:

The planned merger with ICRI was dropped in favor of a licensing agreement with ITL. On December 12, 2012, the Company entered into a License Agreement (the “License Agreement”) with ITL, pursuant to which Novo received an immediate exclusive and worldwide license to commercialize all the Licensed Products based on ITL’s current and future patents and a patent in-licensed from the University of Arizona. The license granted covers two experimental products for the treatment of cancer in clinical development called AlloStim™ and Allo Vax™ (“Licensed Products”). Accordingly, Novo abandoned its endeavors into the clean energy business and changed its name to Immunovative, Inc. (“Immunovative,” or the “Company”) on May 8, 2012 to develop the next generation of immunotherapies to treat cancer

4

In exchange for the license, the Company has undertaken an obligation to provide the financial support for ITL to conduct a Phase II/III clinical trial designed to provide evidence in support of the efficacy of ITL’s lead Licensed Product called “AlloStimTM” (“The Pivotal Trial”). The Company committed to provide $10 million in support of the Pivotal Trial to be paid over a period from the date of the License Agreement until the date that is two years after receiving notice from a regulatory agency in the US, Canada, EU or Thailand of approval to commence the Pivotal Trial.

Upon successful completion of the Pivotal Trial, the Company and ITL have agreed to consummate a merger transaction (either directly or through a subsidiary of the Company) with ITL’s shareholders immediately prior to the merger owning 75% of the post-merger shares and the shareholders of the Company immediately prior to the merger owning 25% of the post-merger shares on a fully diluted basis. The successful completion of the Pivotal Trial shall be defined as the date that the treatment protocol for the number of evaluable subjects necessary to conduct a statistical analysis comparing a placebo control group with a Licensed Product is completed, whereby there is sufficient power to detect a statistically significant (p<0.10) increase in overall survival of 50% or greater of the Licensed Product as compared to the placebo.

The License Agreement provides that the percentage of the post-merger shares that the shareholders of the Company immediately prior to the merger may increase in certain circumstances, including if the Company provides ITL more than the $10 million set out in the License Agreement and if ITL has outstanding debt (excluding any liabilities owed to patent attorneys or for patent maintenance fees) at the time of the merger. Likewise the License Agreement provides that the percentage of the post-merger shares that the shareholders of the Company immediately prior to the merger may decrease in certain circumstances, including if ITL raises funds on its own or if the Company has outstanding debts at the time of the merger.

If there is a successful completion of a Pivotal Trial but the Company has not paid the full $10 million, the parties may agree to merge or the Company may receive shares of ITL based on the amount of funds the Company has provided ITL and the license will terminate. If there is not a successful completion of a Pivotal Trial and the Company decides to continue to fund the clinical trials, the Company will receive shares in ITL for any additional payments more than $10 million. In each of these instances, the shares that the Company will receive will be based on a valuation (prior to the funds provided by the Company) of ITL of $30 million, which can be decreased for any outstanding debts (with the exception of patent related debts and trade liabilities) of ITL or increased for any funds raised by ITL on its own.

If the Company pays all amounts due under the License Agreement, but there is no successful completion of a Pivotal Trial, The Company and ITL may nevertheless agree to merge. If they do not merge, the Company shall maintain the license granted under the License Agreement.

General Overview

The mission of the Company is to develop innovative biological drug products and treatment protocols which harness the power of the human immune system to provide patients with improved quality of life and curative or life-extending treatment options.

The Company serves as the commercial arm of ITL, a private Israeli biopharmaceutical company headquartered in Jerusalem, Israel. However, the Company’s current objective is to fund ITL sufficient funds to complete the Pivotal Trial and then consummate a merger. The intent is that the merged company would pursue the licensing and commercialization of the Licensed Products.

ITL was founded by Dr. Michael Har-Noy, ITL and has developed a novel approach for the treatment of cancer. The Licensed products are designed to mimic an immune mechanism already proven to be clinically effective in humans called the “graft vs. tumor” effect which occurs after allogeneic bone marrow transplant procedures while eliminating the need for a matched donor, chemotherapy conditioning and without any of the type of toxicity associated with transplant procedures. From this novel approach, two products called AlloStimTM (entering phase II/III) and AlloVaxTM (entering phase I/II) have been developed by ITL.

“Immunotherapy” is the science of harnessing the power of the human immune system to target and eliminate tumors wherever they reside in the body and then to protect against the return of the disease without further need for treatment.

5

Immunotherapy is an emerging type of cancer treatment that holds great promise and we believe is the only treatment method known that has the ability to hunt down and kill the very last microscopic tumor cell in the body. Surgery, chemotherapy, radiation and targeted therapies do not have this fine specificity at the single cell level. For this reason, immunotherapy is often referred to as the only known anti-cancer treatment that has a curative potential. In addition, cancer vaccine immunotherapy have been shown to have very mild side-effects, making cancer vaccines a welcome modality to patients that suffer from the side-effects of chemotherapy, radiation and surgery.

The Company has the worldwide, exclusive rights to commercialize AlloStimTM and AlloVaxTM, including any future improvements. AlloStimTM is a patented living cell product derived from normal blood donors. AlloVaxTM is an individualized anti-cancer vaccine derived from a sample of a patient’s own tumor.

AlloStimTM is the lead immunotherapy drug developed by ITL and licensed to the Company. Management believes that the available clinical data on the use of this drug supports that it may be the first immunotherapy drug with evidence that it can debulk chemotherapy-resistant metastatic cancer.

About Dr. Michal Har-Noy, ITL’s Founder

Dr. Michael Har-Noy has over 25 years of experience in immunotherapy drug development, GMP manufacturing and management of early stage biopharmaceutical operations. He is the author of numerous scientific publications and holder of numerous patents in the field of immunotherapy. He is the founder of ITL, an Israeli biopharmaceutical company focused on the development of minimally toxic cancer therapies where the active ingredient is living immune cells.

ITL was founded in May 2004 as a joint venture between the Israel Office of the Chief Scientist, Hadassah‐Hebrew University Medical Center Department of Bone Marrow Transplantation and Dr. Har-Noy. Dr. Har-Noy has lead ITL through pre-clinical toxicology/pharmacology studies, animal efficacy studies and human Phase I/II clinical trials on two immunotherapy drug candidates called AlloStim™ and AlloVax™. ITL operates a wholly-owned subsidiary, Immunovative Clinical Research, Inc., a Nevada Corporation, headquartered in Carlsbad, CA responsible for coordinating all worldwide clinical trial data analysis and GCP regulatory compliance. Prior to founding ITL, Dr. Har-Noy served as the President and CEO of MedCell Biologics from 1995‐2003 where he developed an immunotherapy for HIV/AIDS and Renal Cell Carcinoma that completed Phase I clinical trials.

Dr. Har-Noy attended an MD‐PhD program at Rush University Medical School in Chicago and conducted graduate and post-graduate studies at University of Minnesota, Harvard University Medical School‐Beth Israel hospital and the National Cancer Institute in the development of manufacturing technology for immune cells, such as LAK cells, TIL cells and other autologous cellular immunotherapies, development of immunomonitoring technology. Currently at Hadassah Medical Center, his research focus has been on investigating the mechanism of action of immune‐mediated graft vs. tumor and graft vs. host effects.

The Company announced on June 5, 2012, the publication of abstract reporting the results of the Company’s licensor, ITL’s Food and Drug Administration (“FDA”)-approved phase I/II clinical trial of 42 refractory metastatic solid tumor patients with a variety of indications. Although no objective tumor response was observed, there was evidence of enhanced survival and immune-mediated tumor debulking without graft-versus-host disease. Responsive Evaluation Criteria in Solid Tumors (RESIST) criteria which is usually used to determine response of chemotherapy drugs to cancer by measuring the change in size of tumors after treatment was reported to overestimate tumor burden after treatment with AlloStimTM, as responding tumors swelled and appeared larger on CT. This explained the reason why patients seemed to improve in health status and live longer after AlloStimTM treatment but were not scored as having objective tumor responses. While traditional RECIST criteria did not seem to accurately predict treatment response, multi-parameter analysis identified serum IL-12 as a biomarker predictor of enhanced survival. In the Phase I/II trial 50% were IL-12+ and survived a median of 211 days vs. 131 days for IL-12 negative patients (p < .009). Subset analysis determined that the patients with Her2+ metastatic breast cancer had the highest IL-12 response rate. The Abstract (Number e13013) titled: "Response of HER2+ Breast Cancer Patients to Allogenic Cell Immunotherapy" is now available on on-line at the American Society of Clinical Oncology Meeting ("ASCO 2012") website at: http://abstract.asco.org/AbstView_114_92017.html .

Immunovative, Inc. (“IMUN”) is a public Florida Corporation headquartered in Montreal, Canada and with sales offices located in Paris, Monaco and New York.

IMUN is responsible to fund the ITL’s pivotal Phase II/III clinical trial (estimated to require US$10 million) in late stage metastatic breast cancer to be conducted primarily at the National Cancer Institute of Thailand.

6

The Value Proposition

Management believes that the novel approach to treat cancer developed by ITL clearly represents a unique opportunity to fulfill an unmet medical need. Currently approved therapies to treat cancer provide minimal efficacy at the expense of high toxicity. The probabilities of success for a therapy providing significant survival benefits and little or no toxicity are extremely high in this sector where the efficacy hurdles for market approval are relatively very low.

IMUN has a locked value of $30 million to acquire its parent, ITL, in exchange of $10 million in financing.

The Business Model

ITL has GMP production facilities in Jerusalem. AlloStimTM is produced in batches from the blood of normal blood donors and aliquoted into single dose vials and stored frozen in liquid nitrogen as an intermediate product called T-StimTM. At current scale, one blood donor currently produces about 100 doses of T-StimTM. T-StimTM is believed to be stable for at least two years in liquid nitrogen. Prior to use in the clinic, T-StimTM is thawed and activated in a 4h process and then formulated into syringes and shipped by courier service to the point-of-care. There is no need to match a donor with a patient.

INVESTIGATOR-INITIATED CLINICAL TRIALS AND SUB-LICENSING

Under the Licensing Agreement, IMUN has the right to sub-license marketing rights to the Licensed Products. These products are believed to have broad applicability to a variety of cancer and infectious disease indications. In order to develop initial feasibility data on other indications, IMUN intends to establish collaborations with academic medical centers to conduct Phase I/II clinical studies. It is expected that the funding for a majority of the costs for these studies will come from grants or private donations to the academic medical centers. IMUN intends to use any positive data from these studies to support a sub-licensing program where the marketing rights to the indication will be sub-licensed to a marketing partner. These sub-licenses are intended to be negotiated by indication and by territory.

It is expected that the sub-licensee would fund continued clinical development in the indication an territory with the aim to obtain regulatory approval in the licensed territory. It is possible that such sub-licensing agreements could provide for upfront licensing fees, milestone payments or other strategic assets. It is also expected that such sub-licensing would include an agreement on royalties an/or transfer pricing which would provide revenues to IMUN upon successful commercialization.

Development Plans and Capital Requirements

IMUN plans to primarily be engaged in fund raising to support the $10 million requirement to conduct the Pivotal Trial over the next two years and subsequently to execute collaborative agreements with academic medical centers and then pursue a sub-licensing strategy. The main mode of fund raising is expected to be through sale of our common stock at a discount to our public price through sales to private and institutional investors. ITL will use the funding to support the completion of a pivotal, randomized, controlled, Phase II/III clinical trial of AlloStimTM in advanced metastatic breast cancer.

The pivotal breast cancer clinical trial will be conducted at the National Cancer Institute of Thailand (NCIT) located in Bangkok, Thailand. A complete Investigational New Drug Application (“IND”) application has been submitted to the Thai FDA and the NCI Institutional Review Board detailing the plans for this Phase II/III pivotal study. The trial is anticipated to be approved in the fourth quarter of 2012, with. first patient accruals in the first quarter of 2013. The Pivotal Trial is estimated to complete accrual in 24 months and the data is estimated to be mature for analysis after 32 months. There are many factors that can negatively influence these timing projections and many are not within our control (see “Risk Factors”).

7

After completion of the $10 million financing for the Pivotal Trial, additional funds will be required for scale-up of manufacturing and building of commercialization infrastructure. It is estimated that approximately $30 million will be required for this purpose. The Company intends to begin plans for raising this additional $30 million shortly after completion of the $10 million fund raising obligation for financing the Pivotal Trial. IMUN plans to merge with ITL upon successful completion of the Pivotal Trial. Management believes that if the survival data indicates statistically significant extension of survival of AlloStimTM vs. Placebo, that it may be possible to conduct an IPO at the time of, or shortly after, the completion of the merger. After the merger, IMUN will own 25% of the merged entity and 75% will be owned by ITL (subject to adjustment).

Management intends to list this newly merged entity on the NASDAQ market system concurrent with the announcement of successful pivotal trials. IPO will be sized to provide sufficient capital to finance the launch of the AlloStimTM product into the market. It is estimated that at least $100 million may be required for this purpose.

Once the overall survival end-point of the Pivotal Study is reached and a pilot manufacturing facility has been built and validated, a Biological License Application (BLA) is intended to be submitted in the third and/or fourth quarter of 2016 seeking US FDA marketing approval for AlloStimTM. Under expected fast track approval status, the BLA could be approved by as early as the first or second quarter of 2017.

OVERVIEW IMMUNOTHERAPY

Immunotherapy is a new modality for cancer treatment that potentially holds great promise for becoming a curative therapy with minimal toxicity. The human immune system is capable of seeking out and destroying cancers cells wherever they reside in the body. Harnessing the power of the immune system may hold one of the greatest potentials for winning the battle against cancer.

The immune system, if properly stimulated and educated, is capable of eliminating every last tumor cell. The concept of vaccine immunotherapy against cancer is based on the body's natural defense system, which protects against a variety of diseases. Vaccine immunotherapy has proven to be one of the most effective treatment strategies for prevention of certain infectious diseases. Vaccines using killed or attenuated pathogens have revolutionized public health by preventing the development of many important infectious diseases, including poliomyelitis, small pox, diphtheria, rabies, typhoid, cholera, plague, measles, mumps, hepatitis B, diphtheria toxin and tetanus. Application of these vaccination concepts to cancer could similarly potentially revolutionize cancer treatment.

However, attempts to develop cancer vaccines for treatment of existing tumors have proven to be much more difficult than developing vaccines for prevention of infectious diseases. Attempts to develop immunotherapies such as cancer vaccines, despite many decades of experimental work, have yet to consistently reach their curative potential in human clinical trials.

8

Immunotherapy Failure

There are two main reasons we believe why prior immunotherapies have failed in clinical trials in the past: the stimulation of the wrong immune response and the Inability to overcome tumor immunoavoidance mechanisms.

Stimulation of wrong immune response

Cancer patients by definition are immunocompromised, therefore many immunotherapy strategies have focused on methods to stimulate or strengthen the immune system in order to eradicate cancer. We believe this is a failed strategy because the immune system in fact does respond to cancer. Most tumors are infiltrated with large numbers of immune cells. Stimulating an immune response that has already failed to eradicate the tumor only enhances this wrong immune response.

Inability to overcome tumor immunoavoidance mechanisms

Attempts to educate the immune system to generate the correct immune response through cancer vaccination failed because they may not able to overcome the tumor’s ability to avoid the specific immune response created. Some tumors have evolved very sophisticated methods to avoid the correct immune response. Many tumors can avoid the immune system in the same manner as a fetus is protected from the mother’s immune system in the womb.

Despite all the previous failures of immunotherapies in clinical trials, there has been one major exception.

BONE MARROW TRANSPLANT

The one exception to the failure of immunotherapy protocols to produce significant anti-tumor effects in patients is the immune response that occurs in patients that undergo allergenic bone marrow/stem cell transplant procedures (BMT). BMT is a proven curative therapy for hematological malignancy and also has shown application for the treatment of solid tumors. The curative effect of BMT is mediated by transplanted immune cells derived from a normal (tissue matched) donor. The immune mediated anti-tumor effect of these transplanted immune cells is known as the graft vs. tumor (GVT) effect.

The powerful GVT immune response observed in BMT procedures is capable of overcoming tumor immunoavoidance mechanisms, resulting in complete systemic eradication of cancer in many instances. This GVT effect has been shown to be capable of curing patients with large tumor burdens, including patients with tumors unresponsive to chemotherapy, radiation and other forms of immunotherapy.

The GVT effect is believed to be the most powerful and most effective anti-tumor mechanism ever observed in the treatment of human malignancy. However, the same immune cells (primarily T-cells) which mediate GVT also mediate a serious and often lethal side effect known as graft vs. host disease (GVHD). This is due to the fact that the transplanted immune T-cells recognize both normal and tumor cells as foreign and mount attacks against both indiscriminately. Despite the curative effect of BMT, the severe treatment related toxicity has prevented the wide spread application of BMT for cancer treatment.

ITL’s products are based upon “Mirror Effect™” technology which is designed to provide the same anti-tumor effect that has been proven to be curative in allergenic bone marrow transplant (BMT) procedures without the lethal toxicity.

Technology Overview

The “Mirror Effect™” technology developed by ITL is based on products and methods using T-cells of the immune system.

9

T-CELLS OF THE IMMUNE SYSTEM

T-cells are part of the adaptive immune system of humans. T cells or T lymphocytes belong to a group of white blood cells known as lymphocytes, and play a central role in cell-mediated immunity. They can be distinguished from other lymphocyte types, such as B cells and natural killer cells (NK cells) by the presence of a special receptor on their cell surface called T cell receptors (TCR). Several different subsets of T cells are known, each with a distinct function.

T helper cells (Th cells) are a subset of T-cells that assist other white blood cells in immunologic processes, including maturation of B cells into plasma cells and memory B cells, and activation of cytotoxic T cells and macrophages, among other functions. These T helper cells are also known as CD4+ T cells because they express the CD4 protein on their surface. Helper T cells become activated when they are presented with peptide antigens by MHC class II molecules that are expressed on the surface of Antigen Presenting Cells (APCs). Once activated, they divide rapidly and secrete small proteins called cytokines that regulate or assist in the active immune response.

Memory T cells are another subset of antigen-specific T cells that persist long-term after an infection has resolved. They quickly expand to large numbers of effector T cells upon re-exposure to their cognate antigen, thus providing the immune system with "memory" against past infections. Memory cells may be either CD4+ or CD8+.

THE “MIRROR EFFECTTM” TECHNOLOGY

At ITL, technology has been developed to separate the beneficial GVT effect from the detrimental GVH effect of BMT procedures. ITL products and methods use T-cell infusions to elicit mechanisms that mirror the mechanisms mediated by an allogeneic BMT. This concept is called the Mirror Effect™. In the Mirror Effect™, T-cells from a normal donor are infused into a patient and instead of these foreign cells mediating the GVT effect, these cells instead stimulate the patient's own immune system to attack the tumor. This effect is known as the host-vs-tumor (HVT) effect and it is the mirror image of the GVT effect. The patient's immune system is alerted by the infusion of foreign cells and raises up to reject the foreign cells, an effect known as host-vs-graft (HVG). The HVG effect is the mirror image of the GVH effect. However, unlike the GVH effect the HVG effect is not toxic to a patient.

The reason that the GVT effect maybe such a powerful immune mechanism for curing cancers is that the interaction between the host and donor creates the release of an array of inflammatory cytokines that signal the body of an imminent danger. These danger signals shut down the ability of the tumor to avoid an immune attack and enable immune-mediated killing of tumors disseminated throughout the body. The Mirror Effect™ creates these same danger signals in the context of a rejection response to a foreign cell infusion (HVG) rather than as an attack against normal tissues (GVH). Thus the Mirror Effect™ has the potential to cause a proven curative anti-tumor effect of BMT without the extremely toxic side-effects. This may represent a new concept in the treatment of cancer.

10

The products developed at ITLgenerate the Mirror Effect™ in patients by utilizing immune cells from healthy donors. T-cells from healthy donors are activated and administered to a patient who has not been immunosuppressed.All of the therapies developed at ITLare dependent on the patient having a robust immune system because the desired Mirror Effect™ is based on the rejection response elicited by the patient’s immune system against the administered donor T-cells. The donor T-cells are not HLA-matched to the patient and it is preferable that the HLA-mismatch is maximized between donor T-cells and the patient.

Activation of T-cells occurs by engagement of cell surface proteins, i.e. CD3 and CD28, on the T-cells. Binding of the CD3 protein and costimulation of the CD28 protein on the CD4+ T-cells is required for initiating an effective T-cell mediated immune response. Although activation of T-cells is well known in the art, the methods of activating T-cells at Immunovative are unique and have been patented and result in T-cell compositions with unique characteristics that have also been patented.

The procedures used at ITLresults in enhanced activation of the T-cells. “Activated” T-cells at ITL have one or more agents, i.e. anti-CD3 and anti-CD28 antibodies, bound to the T-cell surface proteins and these bound agents are in turn, cross-linked by the use of a cross-linking agent. The cross-linking agent can be attached to a support.

Product Details:

The main products in the product portfolio of ITLare AlloStim™ and AlloVax™. The process of developing these products involves a separate intermediate product called T-Stim™. T-Stim™ and AlloStim™ are products of two sequential production processes. AlloVax™ is a customized vaccine product in which the disease antigens of a patient are administered along with AlloStim™.

ALLOSTIM™

AlloStim™ is the product of two sequential production processes:

1.T-Stim™

T-Stim™ cells are produced ex-vivo in a 9 day proprietary culture process (patents pending) in a bioreactor. T-Stim™ cells are produced from CD4+ CD45RA+ naïve T-cell precursors that are purified from the blood of normal donors.

After the 9 days in culture approximately 10 billion T-Stim™ cells are produced. There is no need to match the donor to the recipient as is required in BMT procedures. The AlloStim™ product is an intentional mismatch to the recipient.

The T-Stim™ production process involves:

|

I.

|

Purifying precursor immune cells from the blood (from leukapheresis source material) of normal screened donors;

|

|

II.

|

Culturing the precursors in the presence of custom monoclonal antibodies (mAbs) conjugated to a biodegradable tissue-like matrix simulating a lymph node;

|

|

III.

|

Aliquoting the resulting cultured T-Stim™ cells into single dosage forms;

|

|

IV.

|

Freezing the aliquoted T-Stim™ cells in liquid nitrogen for long-term inventory storage.

|

In culture, the mAbs (anti-CD3 and anti-CD28) together with the cell-to cell contact due to the high density of the cells in culture, causes the activation, expansion and maturation of the naïve CD4 cells. The cells expand approximately 100-fold over the culture period resulting in one donor producing enough T-Stim™ cells for approximately 100 doses.

11

Under these controlled conditions, T-Stim™ cells mature into memory CD4 cells that produce extraordinary high amounts of IL-2, IFN-gamma and TNF-alpha upon activation. Additionally, T-Stim™ cells express high density CD40L and FasL on the cell surface. CD40L interacts with CD40 expressed on innate immune cells and activates these cells to produce Th1 cytokines and kill tumors. FasL enables these cells to directly kill tumors.

The frozen product can be distributed through hospital pharmacies and remains stable for over 24 months.

|

I.

|

Activation

|

In order to produce the Mirror Effect™ in a patient, the T-Stim™ cells require activation prior to infusion into the patient. The second production process involves converting T-Stim™ to AlloStim™. T-Stim™ cells are activated with monoclonal antibody-coated particles that remain attached during infusion. When T-Stim™ cells are activated and formulated for infusion the product is called AlloStim™.

ALLOVAX™

AlloVax™ is a new product under development that combines AlloStim™ with a vaccine formulation containing chaperone proteins (also known as heat shock proteins) isolated from a sample of a patient’s cancer. This product is applicable to patients with both solid tumors and hematological (blood) cancers that have been recommended for first line chemotherapy/radiation treatment to induce remission. A high percentage of patients can be induced into remission with first line chemotherapy/radiation, but almost all patients eventually have a recurrence of the cancer. There is no curative therapy for patients that have a recurrence of a blood cancer except for allogeneic bone marrow/stem cell transplant (BMT) procedures. However, the high toxicity associated with the procedure, requirements for a matched tissue donor and the often lethal side effects limit the clinical application.

AlloVax™ is individualized anti-cancer vaccine that is designed to educate the immune system during the period of cancer remission to prevent the tumor from recurring. Chaperone proteins isolated from cancer cells have been shown to carry hidden tumor antigens that can be used to educate the immune system to identify and kill the cancer cells from which they were derived. ITL has purchased the exclusive rights to a patented process developed by Dr. EmmanualKatsanis and scientists at the University of Arizona to purify these chaperone proteins from a small sample of tumor tissue. (See U.S. patent no. 6,875,849).

The AlloVax™ treatment protocol involves first removing a sample of the cancer cells from the patient prior to chemotherapy/radiation therapy. After the patient is in remission, the patient receives intradermal injections of AlloStim™ which are rejected by the patient immune system making the patient immune to the AlloStim™ cells. The cancer sample obtained prior to chemotherapy/radiation treatment is then processed in the laboratory to isolate the chaperone proteins containing the unique tumor antigens. The chaperone protein sample is then combined with AlloStim™ and injected intradermally. In this setting, AlloStim™ acts as an adjuvant for the chaperone protein vaccine formulation. This causes an immune response to reject the AlloStim™ and an immune response against the unique tumor antigens carried by the chaperone proteins. The combination of these immune responses serves to educate the immune system that the tumor antigens are a danger to the body. In this manner, if the tumor recurs the immune system is primed to destroy the tumor without any further treatment in order to keep the patient in remission.

Patent Portfolio Protection Summary:

The patent portfolio of ITL includes a number of claims in different patents and patent applications that protect T-Stim™ and AlloStim™. These claims cover a number of embodiments including compositions of activated T-cells, methods of making these compositions and methods of using these compositions to elicit the Mirror Effect™ in a patient. Some of the broader embodiments of the claims encompass engendering the Mirror Effect™ or aspects of the Mirror Effect™ by using allogeneic cells. Claims have been pursued that are tiered as well as overlapping in order to maximize the protection of Immunovative products. Claims are still being prosecuted that encompass different aspects of these unique cell products.

12

Clinical Trials:

PRIOR HUMAN DATA

Protocol planned for use in taxane-anthracycline metastatic breast cancer (MBC) has successfully completed a Phase I/II clinical trial in 42 advanced metastatic cancer patients, including 16 MBC patients, under a US FDA cleared IND application. The results from this clinical trial provided radiological, pathological and immunological evidence of immune-mediated anti-tumor killing (debulking) activity correlating with survival. 11 of these 42 patients (26%) survived over 1 year, with 9 of the 42 (21%) alive at 18 months. Of the 16 MBC patients accrued in the trial, 5 of the 16 (31%) were still stable and surviving after 1 year. The patient population in this trial were heavily pre-treated, high disease burdened, low performance status metastatic cancer patients that had exhausted all standard treatment options and have a life expectancy of less than 60 days. The average ECOG score (0-4) at baseline was 2.143 ± 0.1208 (N=42). At 60 days, the average ECOG score improved significantly (p< 0.0001) to 1.250 ± 0.1421 (N=40). The Kaplan-Meyer curve for all accrued and evaluable patients in the Phase I/II clinical trial is shown below. Patients were accrued between September 2009 and May 2010 and followed for survival until May 2011.

PATIENTS CHARACTERISTICS

The average age was 60.5 years (range 44-89 years) with 18 male and 24 female. Patients were heavily pre-treated with an average of 2.7 lines of prior chemotherapy with an average of 7 prior courses, 52% had prior radiotherapy and 90% had prior surgical excision of either the primary tumor or metastatic disease lesions. The most common indication was breast cancer (38%), followed by colorectal cancer (16.6%) and also including metastatic ovarian, sarcoma, squamous cell carcinoma, lung, bladder/ureter, pancreas, melanoma and esophageal cancers. The patients had high tumor burdens with an average of 21.2 metastatic lesions per patient (patients with innumerable lesions in an organ were scored as 10 lesions). The most common metastatic tumor sites were lung/pleural (63% of accrued patients), liver (63%), lymph node (53%) and bone (50%). In addition, 60% of patients presented with pleural effusion and/or atelectasis and 13% with malignant ascites.

The following table presents details about the clinical trial design as well as the patients characteristics prior to initiating the therapy.

13

Clinical Trial Design:

Next Milestones:

ALLOSTIMTM

PHASE II/III:Metastatic Breast Cancer

A pivotal metastatic breast cancer clinical trial will be conducted at the National Cancer Institute of Thailand (NCIT) located in Bangkok. A complete IND application has been submitted to the Thai FDA and the NCI Institutional Review Board detailing the plans for this Phase II/III pivotal study.

The trial is anticipated to be cleared in the fourth quarter of 2012, with the accrual beginning first in the fourth quarter of 2013 and completed by the fourth quarter of 2014.The survival data is expected to mature and possibly hit statistical significance by the fourth quarter of 2015.

Trial Specifications:

|

·

|

Randomized, controlled clinical trial anthracycline/taxane resistant metastatic breast cancer

|

|

·

|

InSituVaxTM protocol : AlloStimTM(cells + beads) vs. beads alone combined with ablation

|

|

·

|

208 patients randomized 1:1 treatment vs control

|

|

·

|

Powered to detect 80% overall survival advantage (control=8 months)

|

ALLOVAXTM

PHASE I/II: Advanced Head & Neck Cancer

AlloVaxTM is expected to be submitted at the Thai and US FDA during the the fourth quarter of 2012. The trial design proposed is for a phase I/II randomized, placebo-controlled clinical trial of advanced head and neck cancer. The study is expected to last 1 year and will accrue 52 patients randomized 3:1 treatment to placebo. It will be conducted at the National Cancer Institute of Thailand.

Funding for this trial is anticipated to be covered under the same $10 million IMUN will pay for the Pivotal Trial.

14

Overall Cancer Situation/ Recent Trends

Over recent decades, the incidence of cancer has escalated to epidemic proportions, now striking nearly one in two men (44%) and more than one in three women (39%). This increase translates into approximately 56% more cancer in men and 22% more cancer in women over the course of a single generation. The National Cancer Institute estimates that the number of cancer cases will increase still further because of the growth and aging of the population, dramatically doubling by 2050.

Despite decades of research and new treatment approaches, reversal in overall mortality rates has been minimal and due largely to a reduction in lung cancer deaths from reduced smoking in men, rather than to advances in treatment. Overall five-year survival rates for all cancers have remained virtually static since 1970, from 49 to 54 percent for all races combined.

Current therapies for cancer have significant emotional and physical side effects. Many patients view the treatments to be worse than the disease. The monetary costs for treating cancer are also staggering. The annual direct costs of cancer treatment has more than quadrupled over the past 20 years from $18 billion in 1985 to $41 billion in 1995 to over $120 billion in 2010. Additionally, indirect costs from loss of wages, taxes, earnings and productivity were estimated at $100 billion in 1999.Cancer costs are projected to reach $158 billion, in 2010 dollars, by the year 2020, because of a growing population of older people who are more likely to develop cancer.

Each year, 226,000 women develop breast cancer in the United States and 30% of women with early stage breast cancer may eventually develop metastatic breast cancer. The 5-year survival rate is 21% for women with metastatic cancer and 96% without metastatic cancer. Traditional first/second line treatments still result in recurrences in 50% of women with metastatic breast cancer. These individuals are the targets of the first Clinical Trial.

PROBLEMS WITH CURRENT THERAPIES

Despite dramatic advances in our understanding of cancer cell biology, conventional cancer therapy has remained fundamentally unchanged for decades. The three major forms of cancer therapy remain to be surgery, radiation and chemotherapy. Surgery and radiation therapies have reached their logical limits, and chemotherapy remains the current mainstay of cancer management.

Most chemotherapy drugs are broad-spectrum cytotoxic agents. These drugs are designed to inflict greater damage on cancer cells than on normal cells. Nonetheless, all chemotherapy drugs affect normal cells and cause severe side effects. Chemotherapy is an attempt to kill the tumor before the drug kills the patient.

The major limitation of all current cancer therapies is the inability to eliminate the last tumor cell. This means that current cancer therapies, for the most part, can only extend survival but rarely can actually cure the disease. While current therapies can often initially eradicate measurable evidence of disease, they generally fail to eliminate all the tumor cells. Therefore, any remaining cells may proliferate and cause a relapse of cancer. In this common scenario, the first set of remaining cells has resisted chemotherapy/radiation. The offspring of these tumor cells that were not destroyed by the chemotherapy/radiation have a selective advantage, leaving the person with a recurrence of cancer that is often widespread and resistant to chemotherapy/radiation and other techniques.

Breast Cancer

Breast cancer is the most prevalent cancer in women worldwide and is also the principle cause of cancer death among women. In 2010, nearly 1.5 million women were newly diagnosed with breast cancer (Worldwide Breast Cancer, 2011). Breast cancer accounts for about 10% of worldwide cancer.

15

According to the National Cancer Institute, in 2012 for the United States only, the number of new breast cancer cases for females is expected to reach 226,870 (2,190 males) with expected related deaths of 39,510 (410 males) (NCI, 2012). From a daily perspective, this represent 621 new female breast cancer cases and 108 related deaths every day.

North America, Eastern and Northern Europe, together with Australia and New Zealand have the highest breast cancer incidence rates worldwide, making these countries an attractive opportunity for a novel treatment approach such as AlloStimTM. The world map below presents the number of new breast cancer cases occurring worldwide per 100,000 of population.

Map: number of new breast cancer cases occurring worldwide per 100,000 of population.

Despite innovative therapeutic advances such as the introduction of molecularly targeted therapies Avastin, Herceptin, and Tyverb/Tykerb, there is still a clear unmet need across all lines of therapy in the metastatic setting. This, combined with the potential size of the patient population, strong advocacy framework, and treatment across multiple lines of therapy, makes breast cancer a very attractive commercial opportunity.

Metastatic Breast Cancer

Breast cancer can be divided in different sub-types of breast cancers, with a great variability in the disease characteristics, development rate and survival rate for each of them. Even if there is not a single type of cancer someone would wish for, metastatic breast cancer is certainly one of the most devastating and feared types of cancer.

Nearly 30% of women with early stage breast cancer will eventually develop metastatic breast cancer (O’Shaughnessy, 2005). According to theAmerican Cancer Society statistics (2000-2011), despite all the medical advances and decrease in cancer overall mortality rates over the past 20 years, deaths caused by metastatic breast cancer have remained stable with around 40,000 victims each year. The median survival rate after metastatic breast cancer diagnosis is 3 years and there has been no statistically significant improvement since the 1990’s (American Society of Clinical Oncology [ASCO] Report - 2008).

16

Inefficient Therapies

ITL will target anthracycline-taxane resistant metastatic breast cancer in the pivotal Phase II/III clinical trial for AlloStimTM. Anthracyclines and taxanes are the most active and widely used chemotherapeutic agents for treating breast cancer in hormone receptor-negative patients and those whose disease progresses while they are taking hormone therapy. These agents are commonly used in the adjuvant setting (after surgical removal of a lump or the breast), either in combination or sequentially. Incorporating taxanes into anthracycline-based regimens significantly improves disease-free survival and overall survival (OS) rates.

This benefit is evident regardless of hormone receptor status, degree of nodal involvement, age, menopausal status, and type of taxane or administration schedule. Anthracyclines and taxanes, either alone or in combination, are also the preferred option for hormone receptor-negative patients with metastatic breast cancer (MBC). Response rates of 25% to 69% have been reported when taxanes (paclitaxel or docetaxel) are used as first-line treatment of MBC.

Accordingly, anthracycline- and taxane-containing regimens have been established as the most effective chemotherapeutic agents for first- and second-line therapies in MBC. Because of this, more women are receiving anthracyclines and taxanes early in the treatment of the disease. Even despite this recent trend toward aggressive treatment of early stage breast cancer with anthracyclines and taxanes, nearly half of these women will have metastatic recurrence. The prior exposure to anthracycline and taxane drugs leaves these women facing first-line therapy for metastatic disease resistant to anthracycline and taxane drugs and, thus, with limited treatment options. Anthracycline-taxane resistant metastatic breast cancer is an unmet medical need. There are no effective treatment options available for these women. This is the target of ITL’s pivotal trial.

Competitive Landscape

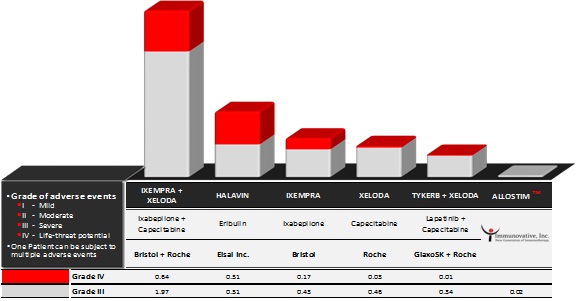

MARKET SIZE & PARTICIPANTS

The market for currently commercialized third-line treatments for anthracycline/taxane resistant metastatic breast cancer represents close to $2.2 Billion in annual sales and is led by 4 fours companies (products): Roche (Xeloda), GlaxoSmithKline (Tykerb), Bristol Myers Squibb (Ixempra), Eisai Inc. (Halavin)

ITEM 1A. RISK FACTORS

The following important factors among others, could cause our actual operating results to differ materially from those indicated or suggested by forward-looking statements made in this Form 10-K or presented elsewhere by management from time to time.

There are numerous and varied risks, known and unknown, that may prevent us from achieving our goals. If any of these risks actually occur, our business, financial condition or results of operation may be materially adversely affected. In such case, the trading price of our common stock could decline and investors could lose all or part of their investment.

17

Risks Related to Our Business

Early Stage Biopharmaceutical Research Company

The success of the Company’s business plan depends not only on its own success, but also on the success of ITL. ITL is in the early stages of development, faced with all the initial and inherent risks associated with the commencement of a new business. To date, ITL has not generated any material revenues. ITL will continue to conduct research activities, including human clinical trials, for an additional at least three years before having the possibility of realizing any material revenues from operations. ITL's technology and research activities may never lead to a successful therapy for human disease, and there may never be any revenues generated from those activities. To date, ITL's resources have been dedicated to the research and development of the AlloStimTM and AlloVaxTM products.

The commercialization of AlloStimTM and AlloVaxTM will require significant additional investment, research and development, clinical testing, and regulatory approvals. ITL and the Company may not be able to develop, produce at a reasonable cost, or market AlloStimTM or AlloVaxTM successfully. Further, AlloStimTM or AlloVaxTM may prove to have undesirable or unintended side effects that may prevent or limit the commercial use and stability. AlloStimTM and AlloVaxTM will require regulatory approval before they can be commercialized and will be subject to regulatory oversight upon commencement of commercial use. If any products are ultimately developed, they may not generate substantial revenues and the Company may never be profitable.

The Company’s business could suffer if the FDA does not lift the hold it has placed on AlloStimTM

On September 26, 2011, ITL received a letter from the U.S. Department of Health & Human Services, FDA in which the FDA proposed to terminate the IND related to AlloStimTM. If that IND is terminated or the clinical hold is continued, ITL will not be able to proceed with clinical trials in the United States. ITL provided responses to the FDA in January 2012 and in June 2012 and does not believe that the IND will be terminated. However, the clinical hold placed by the U.S. FDA still remains in place.

ITL plans to continue with clinical phase II/III trials for AlloStimTM in other jurisdictions outside the US and, plans to conduct these foreign trials under a U.S. IND. However, a U.S. IND is not required to initiate the foreign trials and ITL believes that as long as the clinical trials are conducted under international standards for Good Clinical Practices (“GCP”), and meet FDA regulations for acceptance of foreign clinical data (21 CFR 312.120) that the results could be used at a later date in support of a marketing application to the U.S. FDA even if the clinical hold remains on the current IND.

However, there may be negative perceptions from investors and potential licensing partners with respect to the regulatory status of ITL's products with the U.S. FDA. These negative perceptions could have serious negative impact on the ability of ITL to advance its clinical development and for the Company to raise funds for this advancement. There are no provisions in the License Agreement for a reduction in terms if the FDA terminates the IND or continues the clinical hold.

We require additional financing to meet our obligations under the License Agreement, to fund our operations and to commercialize the product.

The Company needs significant additional financing to meet the terms of the License Agreement and to reach the stage of commercialization of at least one product candidate. In addition to funds necessary to support ITL’s clinical trials, we will also have to raise funds to continue the Company’s operations. We may not be able to raise such funds on favorable terms, if at all.

If clinical tests establish both the safety and efficacy of AlloStimTM in phase II/III clinical trials, significantly more capital will be required to manufacture and market the product. Significant capital requirements will be required for each indication that the Company may seek regulatory approval. If adequate funds are not available, the Company may lose the exclusive license or be required to delay, scale back or eliminate one or more of product development programs, or obtain funds through arrangements with collaborative partners or others that may require the Company to relinquish rights to certain of its products, product candidates or technologies that the Company might not otherwise relinquish.

Other unfavorable factors may also require the Company to seek additional financing, such as unexpected extended pre-clinical or clinical data required by the FDA, difficulty in obtaining regulatory approvals, competition, unforeseen market developments, unforeseen or unexpected difficulties scaling-up and manufacturing AlloStimTM or AlloVaxTM, or unexpected expenditures relating to its operations. Any of these could result in the Company needing more funds than anticipated, which could add significant unexpected dilution to existing shareholders. The Company cannot assure investors that it will be able to raise any required additional funds, or that even if the Company will be able to raise those funds that they can be raised in a timely manner, or on terms which are favorable to the Company.

18

Dilution.

Investors may experience dilution due to future equity issuances and will experience dilution if the Company completes a merger with ITL.

There is a need for significant additional financing to meet the terms of the License Agreement. We must raise significant funds to meet our outstanding obligations under the License Agreement, and intend to do so through the use of sales of our equity. Additionally, we will have to raise funds to continue the Company’s operations and to eventually commercialize ITL's technology. We do not know the terms of any future placements of equity, but any future placements at a purchase price below current market value on a per share basis will dilute the value of current shareholders investments.

Under the terms of the License Agreement, the Company and ITL will merge upon the successful completion of clinical trials. In such an instance, the shareholders of the Company at the time of the Merger will own 25% of the post-merger company, subject to certain adjustments. The investors in this placement will experience a dilution in their share ownership of the Company and, depending on the net tangible book value of ITL at the time of the merger, may experience a dilution in their net tangible book value per share. If there has been a successful completion of clinical trials and the merger does not occur, we will need to raise additional funds to commercialize the products and such raises will likely further dilute the equity ownership of existing stockholders.

Technologies Ultimately May Not Prove Successful

ITL will focus its research and development activities on areas that are highly technical and extremely advanced. As a result, the outcome of any research and development and clinical testing programs are highly uncertain. Historically, only a very small fraction of such programs sponsored by pharmaceutical or biotechnology companies ultimately result in commercial products. Product candidates that initially appear promising, often fail to yield successful products after human clinical testing. In many cases, clinical studies will show that a product candidate does not work, or that it raises safety concerns, or has other side effects that outweigh the intended benefit. Success in pre-clinical or early clinical trials that generally focus on safety issues may not translate into success in large-scale clinical trials designed to demonstrate statistically significant efficacy for reasons that often are not fully understood. Even after a product is approved and launched, general usage or post-marketing studies may identify safety or other previously unknown problems with the product that may result in regulatory approvals being suspended, limited to more narrow indications, or revoked.

The Company’s success relies upon IT.L

The Company’s success relies on the successful execution of clinical trials by ITL. How ITL conducts its clinical trials, appoints, retains and replaces management, handles its expenses and operates other matters related to its day-to-day business are outside of the Company’s control. If ITL mishandles any of these matters, the Company does not have the authority or capability to correct such mistakes.

Key Employee.

The Company is materially dependent upon the continued service, technical knowledge, expertise and abilities of Dr. Michael Har-Noy, as founder and Chief Executive Officer for ITL. If the services of Dr. Har-Noy should become unavailable for any reason, business would be seriously and adversely affected. Dr. Har-Noy currently does not have an employment contract with the ITL nor any key man life insurance.

Biomanufacturing.

The FDA has determined that the current product candidates will be classified as biological drugs. Manufacturing of biological drugs is complex. Unlike traditional chemical pharmaceutical products, a biological drug cannot be characterized in terms of its physical and chemical properties to a degree that would enable an assay of the finished product alone to ensure that the product will perform in the intended manner. Accordingly, it is essential for the manufacturing of a biological drug to be able to both validate and control the manufacturing process in order to demonstrate that the finished product is made strictly and consistently in compliance with pre-established product release criteria. Slight deviations in the manufacturing process may result in unacceptable changes in the final products resulting in rejection of the finished product. For these reasons, manufacturing of biological products is subject to extensive government regulations.

Manufacturing processes which are used to produce smaller quantities of biological products for research and development purposes or initial small clinical trials can not always be successfully scaled-up to allow production of commercial quantities of the product at a reasonable cost, or at all. All of these difficulties are compounded when dealing with novel biological products that require novel-manufacturing processes such as ITL intends to employ. Even minor changes in the manufacturing process may require regulatory approval, which in turn may require additional clinical testing.

ITL could encounter technical problems during the design, scale-up and validation of its planned cell processing system. ITL has attempted to anticipate potential problems in the scale-up of its cell processing system design. However, it is possible that unanticipated problems with the manufacturing system could delay the planned start of clinical trials and could cause ITL to run out of cash before completing the validation of its cell processing system and the clinical trials

Even if ITL is successful in validating a cell processing system, it cannot be assured that the system will be able to produce product from every donor’s blood, or even a majority of donor’s blood. It is possible that some patients may require multiple infusions of cells, increasing its manufacturing costs. It is also possible that ITL could expend considerable funds in attempts to produce product from some donor’s blood and not be successful in producing a product.

19

Dependence Upon Suppliers

Some of the reagents and components ITL intends to use in its proposed cell processing system are purchased from a single source. It is possible, due to the time and expense it might take to change a component or reagent and re-validate the manufacturing process, and receive regulatory approval for the change, that vendors could take advantage of their single source status and raise the price of their products or delay delivery of their products, forcing ITL to accept inflated vendors’ terms. To mitigate this risk, ITL plans to attempt to validate second sources of critical reagents. However, ITL cannot assure that it will be able to second source all the reagents and components used in its manufacturing process.

Need for Technical and Management Personnel

The Company and ITL will need to hire technical and management personnel with relevant biopharmaceutical experience to assist the Company in its efforts to develop and commercialize its products. People with the requisite technical and management background are in high demand and may be difficult to find, hire and retain. The Company’s inability to recruit such personnel could have a materially adverse effect on its ability to develop, manufacture and test its proposed products or obtain the necessary regulatory approvals or raise additional financing.

Government Regulation

The Company’s proposed production of biological products for use in the treatment of human diseases and disorders is subject to extensive regulation by the FDA, as well as comparable agencies in foreign countries. The process of obtaining regulatory approvals, which may eventually allow the Company to produce and market its proposed products, will be time consuming and expensive. The Company cannot assure that such approvals will be granted. In addition, even if approval is granted, it could be limited, or it could be withdrawn for any number of reasons, including its failure to comply with certain regulatory standards. Currently, the testing of ITL's products in the United States is on clinical hold. There is no assurance that the clinical hold will be lifted in a timely manner or ever.

Assuming the Company eventually engages in the commercial production of AlloStimTM or AlloVaxTM, the FDA and various State and foreign regulatory agencies will inspect the Company and its facilities from time to time to determine whether the Company is in compliance with regulations relating to manufacturing practices of biological products, including validation, testing and quality control data and documentation. A determination that the Company is in violation of any such regulations could lead to the imposition of civil penalties, including fines, product recalls or product seizures and, in extreme cases, criminal sanctions.

Patents and Licenses

The pharmaceutical industry places considerable importance on obtaining patent and trade secret protection for new technologies, products and processes. Its success will depend in large part on its ability to file for and obtain patent protection for many of its principal products and procedures, to defend existing or future patents, to maintain trade secrets, and to operate without infringing upon the proprietary rights of others. ITL has applied for several patents involving compositions, methods and uses relating to AlloStimTM and AlloVaxTM in the United States and in certain foreign countries. The Company cannot assure that a patent will be issued in response to all these applications.

Patent protection is highly uncertain and involves complex legal and factual questions and issues. The patent application and issuance process can be expected to take several years and will entail considerable expense. ITL cannot assure that patents will issue as a result of any applications or that the existing patents, or any patents resulting from such applications, will be sufficiently broad to afford protection against competitors with similar or competing technology. Patents ITL obtains may be challenged, invalidated or circumvented, or the rights granted under such patents may not provide the Company with any competitive advantages.

A United States patent application is maintained under conditions of confidentiality while the application is pending, so the Company cannot determine the inventions being claimed in pending patent applications filed by third parties, if any. Litigation may be necessary to defend or enforce its patent rights or to determine the scope and validity of the proprietary rights of others. Defense and enforcement of patent claims can be expensive and time consuming, even in those instances in which the outcome is favorable, and could result in the diversion of substantial resources and management time and attention from its other activities. An adverse outcome could subject Immunovative to significant liability to third parties, which shall require the Company to obtain additional licenses from third parties, require the Company to alter its products or processes, or require that the Company cease altogether any related research and development activities or product sales.

Competition

Pharmaceutical and biotechnology companies which have far greater technical and financial resources than the Company are known to be conducting research into cures and therapies for diseases targeted by the Company. Many of these competing entities are developing alternative immunotherapy. Even if the Company is successful in developing AlloStimTM for disease, any one of the competing pharmaceutical or biotechnology companies could at any time develop a cure or therapy which is superior to, or comparable and less costly than, any therapy developed by the Company.

Lack of Public Market; Limited Liquidity and Transferability; Offering Price

There is currently limited market for any of the Company’s shares, and no assurances are given that a market will develop or, if such a market develops, that it will be sustained with sufficient liquidity to permit investors to sell their Shares at any time. Accordingly, investors may have difficulty in selling their Shares in the future, and the Company can give no assurance that the Shares can ever be resold at or near the offering price, or at all, even in an emergency. Investors must be prepared to hold the Shares for an unlimited period of time.

Authorization of Share Rights

The Company’s Articles of Association authorize the issuance of shares with such rights and the board of directors may determine preferences as from time to time. Accordingly, the board of directors may, without shareholder approval, issue capital stock with dividend, liquidation, conversion, voting or other rights that could adversely affect the voting power or other rights of the holders of the Company’s ordinary stock. In addition, the issuance of such capital stock may have the effect of rendering more difficult or discouraging an acquisition of the Company or changes in control of the Company. Although the Company does not currently intend to issue any special rights shares, there can be no assurance that the Company will not do so in the future.

Product Liability

The Company may, during clinical development and in the future, be subject to claims for product liability. The Company anticipates that the Company will be named on ITL’s clinical trial and product liability insurance at such time as its operations warrant such coverage. A successful claim against the Company in excess of any such coverage could have a material adverse effect on the Company. Additionally, such insurance is expensive and may not be available to the Company in the future on reasonable terms, if at all.

The Company has not paid dividends to date and does not intend to pay any dividends in the near future.

The Company has never paid dividends on its common stock and presently intends to retain future earnings, if any, to finance the operations of our business. You may never receive any dividends on the shares.

20

We have sustained recurring losses since inception and expect to incur additional losses in the foreseeable future.

We were formed on April 8, 2001 and have reported annual net losses since inception. For our year ended March 31, 2012 and 2011, we experienced net losses of $6,245,879 and $2,811,538, respectively. We used cash in operating activities of $2,222,296 and $736,909 in 2012 and 2011, respectively. As of March 31, 2012, we had a combined accumulated deficit of $16,244,237 from prior operations and $4,595,168 from the period December 11, 2011 (inception of development) to March 31, 2012. In addition, we expect to incur additional losses in the foreseeable future, and there can be no assurance that we will ever achieve profitability. Our future viability, profitability and growth depend upon our ability to successfully operate, expand our operations and obtain additional capital. There can be no assurance that any of our efforts will prove successful or that we will not continue to incur operating losses in the future.

We do not have substantial cash resources and if we cannot raise additional funds or generate more revenues, we will not be able to pay our vendors and will probably not be able to continue as a going concern.

As of March 31, 2012, our available cash balance was $619,624. We will need to raise additional funds to pay outstanding vendor invoices and execute our business plan. Our future cash flows depend on our ability to market and sell our common stock and into sublicensing. There can be no assurance that additional funds will be available when needed from any source or, if available, will be available on terms that are acceptable to us.

We may be required to pursue sources of additional capital through various means, including joint-venture projects and debt or equity financings. Future financings through equity investments will be dilutive to existing stockholders. Also, the terms of securities we may issue in future capital transactions may be more favorable for our new investors. Newlyissued securities may include preferences, superior voting rights, the issuance of warrants or other convertible securities, which will have additional dilutive effects. Further, we may incur substantial costs in pursuing future capital and/or financing, including investment banking fees, legal fees, accounting fees, printing and distribution expenses and other costs. We may also be required to recognize non-cash expenses in connection with certain securities we may issue, such as convertible notes and warrants, which will adversely impact our financial condition and results of operations.

Our ability to obtain needed financing may be impaired by such factors as the weakness of capital markets and the fact that we have not been profitable, which could impact the availability or cost of future financings. If the amount of capital we are able to raise from financing activities, together with our revenues from operations, is not sufficient to satisfy our capital needs, even to the extent that we reduce our operations accordingly, we may be required to cease operations.

We have a limited operating history, and it may be difficult for potential investors to evaluate our business.