Attached files

| file | filename |

|---|---|

| EX-31.2 - CERTIFICATION PURSUANT TO SECTION 302 - CHC Helicopter S.A. | d375764dex312.htm |

| EX-12.1 - COMPUTATION OF RATIO OF EARNINGS TO FIXED CHARGES - CHC Helicopter S.A. | d375764dex121.htm |

| EX-18.1 - LETTER OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - CHC Helicopter S.A. | d375764dex181.htm |

| EX-32.1 - CERTIFICATION PURSUANT TO 18 U.S.C. SECTION 1350 - CHC Helicopter S.A. | d375764dex321.htm |

| EX-31.1 - CERTIFICATION PURSUANT TO SECTION 302 - CHC Helicopter S.A. | d375764dex311.htm |

| EX-32.2 - CERTIFICATION PURSUANT TO 18 U.S.C. SECTION 1350 - CHC Helicopter S.A. | d375764dex322.htm |

| EX-21.1 - SCHEDULE OF SUBSIDIARIES - CHC Helicopter S.A. | d375764dex211.htm |

| EX-10.36 - EMPLOYMENT AGREEMENT - CHC Helicopter S.A. | d375764dex1036.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED APRIL 30, 2012

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 333-179072

CHC Helicopter S.A.

(Exact Name of Registrant as Specified in Its Charter)

| Luxembourg | N/A | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

4740 Agar Drive

Richmond, BC V7B 1A3, Canada

(Address of Principal Executive Offices, Zip code)

(604) 276-7500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None.

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ¨ No x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2). Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates as of the last business day of the registrant’s most recently completed second fiscal quarter was $0, as there was no public market for the registrant’s common stock as of October 31, 2011. As of June 30, 2012, there were 1,870,561,417 Class A Shares, 8,512,986 Class B Shares, 318,000 Special Shares and one Class C Share of stock outstanding.

DOCUMENT INCORPORATED BY REFERENCE.

None.

Table of Contents

ANNUAL REPORT ON FORM 10-K

FOR THE FISCAL YEAR ENDED

April 30, 2012

TABLE OF CONTENTS

| Page Number | ||||||

| PART I | ||||||

| Cautionary Note Regarding Forward-Looking Statements and Other Industry and Market Data |

ii | |||||

| Item 1. | 1 | |||||

| Item 1A. | 10 | |||||

| Item 1B. | 19 | |||||

| Item 2. | 19 | |||||

| Item 3. | 19 | |||||

| Item 4. | 20 | |||||

| PART II | ||||||

| Item 5. | 20 | |||||

| Item 6. | 21 | |||||

| Item 7. | Management’s discussion and analysis of financial condition and results of operations |

24 | ||||

| Item 7A. | 46 | |||||

| Item 8. | 47 | |||||

| Item 9. | Changes in and disagreements with accountants on accounting and financial disclosure |

48 | ||||

| Item 9A. | 48 | |||||

| Item 9B. | 48 | |||||

| PART III | ||||||

| Item 10. | 48 | |||||

| Item 11. | 52 | |||||

| Item 12. | Security ownership of certain beneficial owners and management and related stockholder matters |

73 | ||||

| Item 13. | Certain relationships and related transactions, and director independence |

75 | ||||

| Item 14. | 76 | |||||

| PART IV | ||||||

| Item 15. | 77 | |||||

| SIGNATURES | ||||||

| 78 | ||||||

i

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS AND OTHER INDUSTRY AND

MARKET DATA

This Annual Report on Form 10-K and the documents incorporated herein by reference contain forward-looking statements, within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and Section 27A of the Securities Act of 1933, as amended, about our future expectations, plans or prospects and our business. All statements contained in this Annual Report on Form 10-K, other than statements of historical fact, regarding our strategy, future operations, financial position, estimated revenues and losses, projected costs, prospects, plans and objectives of management, are forward-looking statements. When used in this Annual Report on Form 10-K, the words “could,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. Although these forward-looking statements are based on our current expectations and assumptions about future events and are based on currently available information as to the outcome and timing of future events, actual results may differ materially from those stated in or implied by these forward-looking statements. Such factors include, but are not limited to, the following:

| • | Competition in the markets we serve; |

| • | loss of any of our large, long-term support contracts; |

| • | failure to maintain standards of acceptable safety performance; |

| • | political, economic and regulatory uncertainty; |

| • | problems with our non-wholly owned entities; |

| • | exposure to credit risks; |

| • | assimilation of acquisitions and the impact of any future material acquisitions; |

| • | inability to fund our working capital requirements; |

| • | unanticipated costs or cost increases; |

| • | risks inherent in the operation of helicopters; |

| • | reduced activity in the oil and gas industry; |

| • | inability to obtain or maintain necessary aircraft, aircraft parts, insurance or lease financing; |

| • | exchange rate fluctuations; |

| • | loss of key personnel; |

| • | labor problems; |

| • | global financial market instability; |

| • | insufficient assets in our defined benefit pension plan; |

| • | allocation of risk between our customers and us; |

| • | inability to dispose of our older aircraft and parts; |

| • | inability to service our debt obligations or comply with our obligations under our operating leases; |

| • | compliance risks associated with international activities; |

| • | application of tax laws in various jurisdictions; |

| • | inability to upgrade our technology; |

| • | reduction or cancellation of services for government agencies; |

| • | our sponsor may have interests that conflict with ours; |

| • | risk related to our operations under local law; and |

| • | inability to maintain government issued licenses. |

Actual results may differ materially from those discussed in these forward-looking statements due to a number of factors, including the risks set forth in the section entitled “Risk Factors” in Part I, Item 1A of this Annual Report on Form 10-K and elsewhere in this filing. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Moreover, neither we nor any other person assumes responsibility for the accuracy and completeness of these forward-looking statements. We are under no duty to update any of the forward-looking statements after the date of this Annual Report on Form 10-K to conform our prior statements to actual results.

The market data and other statistical information (such as the size of certain markets and our position and the position of our competitors within these markets, oil and gas production and market information) used throughout this Annual Report on Form 10-K are based on independent industry publications, government publications, reports by market research firms or

ii

Table of Contents

other published independent sources. Some market data and statistical information are also based on our good faith estimates, which are derived from our review of internal surveys, as well as the independent sources listed above. This information may prove to be inaccurate because of the method by which we obtain some of the data for our estimates or because this information cannot always be verified with complete certainty due to the limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties. As a result, although we believe these sources are reliable, we have not independently verified the information and cannot guarantee its accuracy and completeness. The industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the section entitled “Risk Factors” in Part I, Item 1A of this Annual Report on Form 10-K.

BASIS OF PRESENTATION

The audited consolidated financial statements of the top-most parent guarantor, 6922767 Holding S.à r.l. (the “Successor”, the “Company”, “we”, “us” or “our”), consist of the Successor’s consolidated balance sheets as of April 30, 2012 and 2011 and the Successor’s consolidated statements of operations, changes in shareholder’s equity and cash flows for the years ended April 30, 2012, 2011, and 2010.

6922767 Holding S.à r.l. was incorporated on February 20, 2008 under the laws of Luxembourg and is a private limited liability company (Société à responsabilité limitée) (S.à r.l.) whose sole purpose was to acquire CHC Helicopter Corporation (the “Predecessor”). The Company completed its acquisition of the Predecessor on September 16, 2008 and has included the results of operations and cash flows of the entity formerly known as CHC Helicopter Corporation from September 16, 2008 to April 30, 2009 in its audited consolidated financial statements for the fiscal year ended April 30, 2009, which are not included in this Annual Report on Form 10-K. The Company’s results of operations also include organizational expenses and losses related to the acquisition as it was not previously operating in the helicopter transportation services industry from May 1, 2008 up to the date of the acquisition. The acquisition of CHC Helicopter Corporation was accounted for using the purchase method of accounting. The application of the purchase method of accounting requires the allocation of the acquisition purchase price to the tangible and intangible assets acquired and liabilities assumed based on their respective fair values as of the date of the acquisition. As a result, the assets and liabilities acquired from the Predecessor on the date of acquisition are recorded at fair values and these became the Successor’s cost basis. Accordingly, the Predecessor period from May 1, 2008 to September 15, 2008 and the Successor period from May 1, 2008 to April 30, 2009 have a different basis of accounting.

The Predecessor adopted the U.S. dollar as its reporting currency on May 1, 2008. As such, historical figures previously reported in Canadian dollars have been translated into U.S. dollars using the current rate method. Under this method, the statement of operations and cash flow statement items have been translated into U.S. dollars using the rates in effect at the date of the transactions. Assets and liabilities have been translated using the exchange rate in effect at the balance sheet date. The Predecessor applied this method retrospectively to all activity that commenced May 1, 2004. Equity balances which arose prior to May 1, 2004 have been translated to the reporting currency at the exchange rate in effect on May 1, 2004.

TRADEMARKS

CHC Helicopter and the CHC Helicopter logo are trademarks of CHC Helicopter S.A. All other trademarks and service marks appearing in this Annual Report on Form 10-K are the property of their respective holders. All rights reserved. The absence of a trademark or service mark or logo from this Annual Report on Form 10-K does not constitute a waiver of trademark or other intellectual property rights of CHC Helicopter S.A, its affiliates and/or licensors.

GLOSSARY

| Embedded equity | Embedded equity represents the amount by which the estimated market value of a leased aircraft exceeds the leased aircraft purchase option price at September 16, 2008, the acquisition date. Embedded equity is assessed on an ongoing basis for impairment. Impairment, if any, is recognized in the consolidated statements of operations. | |

| EMS | Emergency medical services. | |

| Fixed wing | An airplane. | |

iii

Table of Contents

| Heavy helicopter | A category of twin-engine helicopters that requires two pilots, can accommodate 19 to 26 passengers and can operate under instrument flight rules, which allow daytime and nighttime flying in a variety of weather conditions. The greater passenger capacity, larger cabin, longer range, and ability to operate in adverse weather conditions make heavy aircraft more suitable than single engine aircraft for offshore support. Heavy helicopters are generally utilized to support the oil and gas sector, construction and forestry industries and SAR and EMS customer requirements. | |

| IFR | Instrument flight rules, which allow for daytime and nighttime flying in a variety of weather conditions. | |

| Long-term contracts | Contracts of three years or longer in duration. | |

| Medium helicopter | A category of twin-engine helicopters that generally requires two pilots, can accommodate nine to 15 passengers and can operate under instrument flight rules, which allow daytime and nighttime flying in a variety of weather conditions. The greater passenger capacity, longer range, and ability to operate in adverse weather conditions make medium aircraft more suitable than single engine aircraft for offshore support. Medium helicopters are generally utilized to support the oil and gas sector, construction and forestry industries and SAR and EMS customer bases in certain jurisdictions. Medium helicopters can also be used to support the utility and mining sectors, where transporting a smaller number of passengers or carrying light loads over shorter distances is required. | |

| Medium term contracts | Contracts of greater than one year and less than three years in duration. | |

| MRO | Maintenance, repair and overhaul. | |

| New technology | When used herein to classify our aircraft, a category of higher value, recently produced, more sophisticated and more comfortable aircraft, including Eurocopter’s EC225, EC135, EC145 and EC155; Agusta’s AW139; and Sikorsky’ S76C+, S76C++ and S92A. | |

| Old technology | When used herein to classify our aircraft, all aircraft other than new technology aircraft, including Eurocopter’s AS365 and Super Puma; Sikorsky’s 76A, 76B, 76C and S61N; and Bell’s 412, 212 and 214. | |

| OEM | Original equipment manufacturer. | |

| PBH | Power-by-the-hour. A program where an aircraft operator pays a fee per flight hour to an MRO provider as compensation for repair and overhaul components required in order for the aircraft to maintain an airworthy condition. | |

| SAR | Search and rescue. | |

| VFR | Visual flight rules, which require daylight and good weather conditions. | |

iv

Table of Contents

| Item 1. | Business |

Overview

Our Company

We are a world-leading commercial operator of medium and heavy helicopters, providing mission-critical services to the offshore oil and gas industry, as well as SAR and EMS to government agencies and commercial operators through our Helicopter Services segment. We believe the helicopter services we provide to our oil and gas customers are critical for the continued production of hydrocarbons from existing offshore oil and gas platforms and the exploration and development of new oil fields, while our SAR and EMS services help save lives. In addition, our MRO segment, Heli-One is a world leading independent commercial provider of helicopter support services with offerings that include MRO services, integrated logistics support, helicopter parts sales and distribution, and complete outsourcing of maintenance for helicopter operators. Heli-One services our own flight operations and third-party customers around the world.

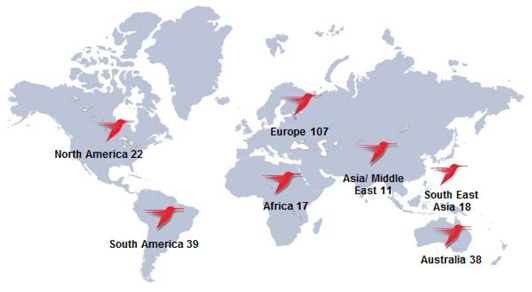

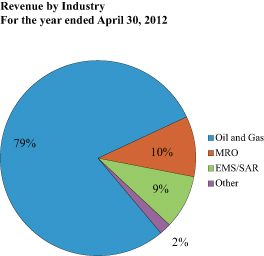

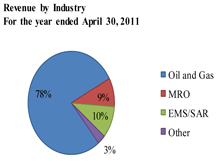

We have been providing helicopter services through our subsidiaries and predecessor companies, for more than 60 years and currently operate in approximately 30 countries, covering every major offshore oil and gas producing region of the world except the Gulf of Mexico. Our major operations are in Norway, the United Kingdom, Ireland, the Netherlands, Australia, Brazil, Canada, Europe and Africa. As of April 30, 2012, we operated 252 aircraft, comprising 113 heavy helicopters, 137 medium helicopters, and two fixed-wing aircraft. For the fiscal years ended April 30, 2012 and April 30, 2011, helicopter transportation services for the oil and gas industry accounted for approximately 79% and 78% of our total revenue, respectively, SAR and EMS activities accounted for approximately 9% and 10% of our total revenue, respectively, while MRO and other helicopter support services represented approximately 12% and 12% of our total revenue, respectively. For the fiscal years ended April 30, 2012, April 30, 2011 and April 30, 2010, the Company earned revenues of $1,692.5 million, $1,445.5 million and $1,313.6 million and incurred net losses of $95.0 million, $65.3 million and $76.5 million, respectively.

The following map shows our aircraft distribution as of April 30, 2012:

| Note 1: | Aircraft in Europe and North America include aircraft in post-delivery modification, those used for base maintenance and aircraft held for sale. |

Helicopter Services

Our Helicopter Services segment consists of flying operations in the Eastern North Sea, the Western North Sea, the Americas, the Australasia region and the Africa-Euro Asia region serving customers primarily in the offshore oil and gas industry and SAR and EMS. The Eastern North Sea is comprised mainly of Norway while the Western North Sea includes the United Kingdom, Ireland, the Netherlands and Denmark. The Americas is comprised of Brazil and North and South American countries. The Australasia region includes Australia and Southeast Asian countries and the Africa-Euro Asia region includes Nigeria, Kazakhstan, Turkey, Mozambique, Tanzania and other African and European countries.

1

Table of Contents

We are one of two global helicopter service providers to the offshore oil and gas industry. We provide transportation services to and from production platforms, drilling rigs and other offshore installations and facilities.

| • | Our helicopter services business in the oil and gas industry is largely characterized by medium to long-term contracts (i.e., two to eight years in duration, with an average of four years). |

| • | The majority of our customers are large national and multinational companies. |

| • | We believe our services are critical to customers as helicopter transportation is a cost-effective, viable means to transport crews from land to offshore oil and gas platforms. Our fuel costs are passed through to our customers. |

| • | Maintaining a strong safety record is a primary concern for our customers, and as of April 30, 2012, our five year rolling average was 0.23 accidents per 100,000 flight hours. The accident rate is calculated using the number of accidents, as defined by the International Civil Aviation Organization, divided by the number of hours flown in the same period and then multiplied by 100,000. |

We particularly target opportunities for long-term contracts that require sophisticated, medium and heavy helicopters, operated by highly trained personnel with state-of-the-art safety management systems and a world-class operating track record. We are a market leader in most of the regions we serve, with a well-established reputation for safety, customer service and aircraft reliability. We are a major operator in the North Sea, one of the world’s largest oil producing regions. We operate the largest fleet of heavy helicopters in Brazil to service our customers in the oil and gas sector, a market that is shifting to heavy helicopter technology as pre-salt fields in ultra deepwater environments have been further developed, and we service the industry in Africa, Europe, Australia and Southeast Asia. For the fiscal years ended April 30, 2012 and April 30, 2011, revenues generated by helicopter transportation services for the oil and gas industry accounted for approximately 79% and 78% of our total revenues, respectively.

Our oil and gas production customers generally provide our helicopter services business with a less cyclical revenue stream, while oil and gas exploration and development activities are more cyclical in nature. Offshore production platforms generally run at full capacity, irrespective of commodity prices, until the economic end-life of the respective field. These production platforms generally have expected lives of twenty years or more, depending on the size and characteristics of the field.

We are one of the world’s leading commercial providers of SAR and EMS services through our Helicopter Services segment. We have long-term contracts with government agencies and commercial operators in the United Kingdom, Ireland, Norway and Australia. Our SAR and EMS contracts average eight years in duration. Contracts are generally entered into directly with state and federal governments.

| • | Our SAR business utilizes state-of-the-art aircraft specifically configured and equipped with emergency medical and rescue equipment. Our crews are multi-disciplinary professionals with extensive training for the high level of expertise required for maritime search and rescue, thus ensuring maximum safety during the operations conducted. |

| • | Our EMS business provides for the transport of medical personnel and equipment directly to the scene of an accident, and the rapid transport of victims to and between hospitals. |

| • | We expect increased demand for SAR and EMS helicopter services as governments increasingly outsource these services. |

| • | Revenue streams from SAR and EMS services are not driven by general economic conditions or short-term hydrocarbon prices. For the fiscal years ended April 30, 2012 and April 30, 2011, revenues generated by SAR and EMS services accounted for approximately 9% and 10% of our total revenues, respectively. |

Maintenance, Repair and Overhaul

Our MRO segment, Heli-One, is a world-leading independent commercial provider of helicopter support and MRO services. Our comprehensive range of capabilities and broad geographic footprint allow us to offer a full suite of aftermarket services, including engine, airframe and component MRO, logistics support, parts sales and distribution, and high-value engineering and design. We provide these services individually or as part of multi-year complete maintenance outsourcing. We operate independent licensed commercial engine and major component MRO facilities for the Eurocopter SuperPuma and Eurocopter EC225 helicopters. Additionally, we service a wide variety of other helicopter types, including the Eurocopter Dauphin, Sikorsky S61N, Sikorsky S76 series, Sikorsky S92A, Agusta AW139, Bell 212 and Bell 412. We provide sophisticated avionics integration services to the armed forces of European nations, and we partner with helicopter manufacturers around the world to provide MRO services to their direct customers.

2

Table of Contents

We believe that Heli-One enhances our business model in several respects:

| • | Third party demand for MRO services by each of the government, military and civil sectors provides us with a diverse stream of revenue. |

| • | Air worthiness regulations, which are established by civil aviation authorities and manufacturers, require that every dynamic component of a helicopter be replaced or overhauled on a regularly scheduled basis, resulting in steady demand for our MRO services. |

| • | Our in-house repair and overhaul capabilities provide operational control and flexibility over the maintenance of our fleet, lowering operating cost and providing a competitive advantage. |

Our Customers

Our customer base includes a broad range of blue-chip oil and gas companies, government agencies and commercial operators. Key customers include Statoil (year ended April 30, 2012 – 16% of revenues) and Petrobras (year ended April 30, 2012 – 11% of revenues).

Our Industry

Regulated Industry With a Focus on Safety. We operate within extensive and complex regulatory requirements. A strong record for safety, respected brand name and ongoing investment are instrumental in attracting pilots, maintenance engineers and personnel with the requisite levels of training, technical qualifications, and certifications. Helicopter operators are required to undergo licensing processes in every country in which they do business. In many countries, operators also need local partners or representatives to meet national aviation requirements.

Limited Aircraft Supply. Helicopters are generally classified as light (four to eight passengers), medium (nine to 15 passengers) and heavy (19 to 26 passengers). Medium and heavy helicopters are primarily used for crew change transportation services on oil and gas production and exploration rigs in the regions of the world where we operate because they can fly in a wide variety of operating conditions, over longer distances at faster speeds, and with larger payloads than light helicopters. Lead times for delivery of new heavy helicopters are long, currently about one year and have historically been as long as two years. We believe long lead times for heavy helicopter delivery and trends toward increasing deepwater oil and gas activity should create attractive market conditions for us since we operate the largest fleet of heavy helicopters in the world. These circumstances were enhanced by our commitments to purchase and incorporate an additional 22 Eurocopter EC225 and 10 Agusta Westland AW139 heavy helicopters into our operations over the next several years, with options to acquire additional aircraft.

Helicopter Values and Resale Market. The secondary market for helicopters has historically been larger than the annual new production market. Secondary market values are widely published with several independent firms providing valuations and performing annual appraisals. Unlike fixed wing aircraft, heavy and medium helicopters typically maintain

3

Table of Contents

their value, or depreciate modestly over the long-term. This is because the regulatory requirements to periodically replace, overhaul and upgrade major components, such as engines, gear boxes, transmissions and other rotable parts, preserve the aircraft in near-new condition throughout the repair and overhaul cycle. Resale values for certain types of aircraft with older technology have declined recently as a result of general economic conditions; however, we expect valuations to improve once the economy stabilizes. The resale market includes customers in many non-hydrocarbon industries, including SAR, EMS, construction, forestry, mining, police, military and recreation.

Technological Advancements. Technology improvements have allowed oil and gas companies to expand exploration and production into deeper waters. This translates into longer trips, more flying hours and the need for larger helicopters with the newest technology for improved range and passenger capacity. A large number of these deepwater installations are planned over the next five years and we expect the demand for new offshore helicopters to increase.

Competitive Strengths

| • | Global Footprint. We currently operate helicopter transportation services in approximately 30 countries. In addition, we have our own internal MRO operations, Heli-One, which services aircraft in most of the countries in which we maintain flying operations. Our broad geographic coverage enables us to respond quickly to customer needs and new business opportunities, while adhering to international safety standards, local market regulations and customs. Additionally, as multinational oil and gas companies seek helicopter operators that can provide one standard of service in many locations around the world, our geographic coverage allows us to effectively compete for many of these contracts. We have a record of obtaining the required licenses and permits to operate in new jurisdictions, including, where necessary, through local alliances. |

| • | Safety Record. In more than 60 years of operation, we believe we have developed sophisticated safety and training programs and practices and are proud of our safety record. We have implemented a single safety management system worldwide and continue to meet or exceed the stringent safety and performance audits conducted by our customers. We also host a highly regarded annual international safety summit, which is a manifestation of our single-minded commitment to safe operations. The summit is attended by our customers, manufacturers, competitors and regulators. |

| • | Strong Long-Term Relationships with Leading Companies and Organizations. We have multi-year relationships with major oil and gas companies and with SAR and EMS customers around the world, especially in Norway, Ireland, the United Kingdom and Australia, where many have been our customers continuously for more than two decades. We believe these long-term customer relationships are enabled, in large part, because of our focus on and accomplishments in safety and flight training, our crews’ experience, and service quality that consistently meets or exceeds customer standards. In addition to helicopter transportation, certain customers rely on us for ancillary services, including our computerized logistics systems that enhance crew scheduling and passenger handling services, which further strengthen relationships and often generate additional revenue. |

| • | Large, Modern and Diversified Fleet of Helicopters. We are a world-leading commercial operator of medium and heavy helicopters. Our large fleet allows us to meet the diverse operational requirements of our customers and minimize disruptions in service. To meet customer-specific requirements and ensure that we and our customers are not overly reliant on any one aircraft type or manufacturer, we most commonly operate Sikorsky S92A and Eurocopter EC225 heavy aircraft and Sikorsky S76 series and Agusta AW139 medium aircraft. Our fleet includes some of the most advanced civilian aircraft in the world. We have modernized our fleet significantly over the last five years and continue to invest in modernizing our fleet as evidenced through our continued commitment to purchase EC225s and AW139s. The total committed capital requirement as of April 30, 2012 is approximately $558.0 million for aircraft with delivery dates between fiscal 2013 and 2017. |

| • | Retention of Asset Value in Our Owned Fleet. A significant portion of a helicopter’s value resides in its major components, including engines, gearboxes, transmissions and rotable parts. Because these components are replaced or upgraded on a regular basis, older models of helicopters remain capable of meeting many of the same performance standards as newer aircraft. |

| • | In-House Repair and Overhaul Business. Our MRO segment, Heli-One diversifies our revenue streams, reduces our costs and positions us as a full-service, high-quality helicopter operator. We are a market leader in MRO and operate independent licensed commercial-engine and major-component MRO facilities for the Eurocopter Super Puma and Eurocopter EC225 helicopters. We also have the capability to support several other helicopter types including the Eurocopter Dauphin, Sikorsky S61N, Sikorsky S76 series, Sikorsky S92A, Agusta AW139, Bell 212 and Bell 412. This allows us to control the quality and cost of our helicopter maintenance, repair and refurbishment. |

Our Business Strategy

Our goal is to enhance our leadership position in and create superior value by consistently and efficiently providing safe, reliable value-added services to our customers while maximizing return on assets, earnings and cash flow. In our pursuit of this goal, we intend to focus on the following key initiatives:

| • | Strengthening Our Competitive Position in Existing Markets. We intend to improve our ability to win new contracts, renew existing contracts, strengthen our existing customer relationships and enhance our competitive position by increasing our focus on customer needs and reducing costs, while maintaining high standards for safety and reliability. We believe our global footprint, safety record and diversified fleet of large and medium helicopters ideally position us to serve increased demand from existing customers and new customers. |

4

Table of Contents

| • | Expanding Our Helicopter Transportation Operations. We intend to capitalize on our broad geographic coverage, long-term customer relationships and our fleet capabilities to fulfill new opportunities in developing oil and gas regions. Some of these geographic regions, including Brazil, Australia, Europe and Southeast Asia, where we currently have infrastructure and operations, are expected to be the fastest growing markets for offshore helicopter transportation services. We are exploring expansion into military transportation services. |

| • | Growing the MRO Business. We plan to expand our Heli-One revenue by further penetrating markets for overhaul of major components and engines and by pursuing new opportunities in heavy- and medium-aircraft maintenance, as well as military helicopter support. |

| • | Growth Through Acquisition. We may evaluate acquisition opportunities for both our flying and MRO businesses to further strengthen our position in existing markets and establish ourselves in new ones. |

| • | Focusing on Long-Term Contracts. We are prioritizing long-term contracts with our major customers to maximize the stability of our revenue. |

Revenue by End Market

| (in thousands of U.S. dollars) | For the year ended April 30, | |||||||||||||||||||||||

| 2012 | 2011 | 2010 | ||||||||||||||||||||||

| Industry Sector |

||||||||||||||||||||||||

| Oil and Gas |

$ | 1,330,163 | 79 | % | $ | 1,129,749 | 78 | % | $ | 1,042,980 | 79 | % | ||||||||||||

| Repair and Overhaul |

166,479 | 10 | % | 129,222 | 9 | % | 112,470 | 9 | % | |||||||||||||||

| EMS/SAR |

158,505 | 9 | % | 151,101 | 10 | % | 138,012 | 11 | % | |||||||||||||||

| Other |

37,392 | 2 | % | 35,388 | 3 | % | 20,104 | 1 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total |

$ | 1,692,539 | 100 | % | $ | 1,445,460 | 100 | % | $ | 1,313,566 | 100 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Revenue by Geography

| (in thousands of U.S. dollars) |

For the year ended April 30, | |||||||||||||||||||||||

| 2012 | 2011 | 2010 | ||||||||||||||||||||||

| Canada |

$ | 13,914 | 1 | % | $ | 12,671 | 1 | % | $ | 16,386 | 1 | % | ||||||||||||

| United Kingdom |

262,592 | 16 | % | 243,921 | 17 | % | 251,627 | 19 | % | |||||||||||||||

| Norway |

531,452 | 31 | % | 452,578 | 31 | % | 405,258 | 31 | % | |||||||||||||||

| Africa |

60,503 | 4 | % | 56,361 | 4 | % | 54,776 | 4 | % | |||||||||||||||

| Australia |

213,970 | 13 | % | 137,639 | 10 | % | 126,992 | 10 | % | |||||||||||||||

| Denmark |

29,538 | 2 | % | 29,108 | 2 | % | 29,535 | 2 | % | |||||||||||||||

| The Netherlands |

94,663 | 6 | % | 95,835 | 7 | % | 119,234 | 9 | % | |||||||||||||||

| Brazil |

210,347 | 12 | % | 163,928 | 11 | % | 105,856 | 8 | % | |||||||||||||||

| Asia |

93,782 | 6 | % | 107,305 | 7 | % | 93,671 | 7 | % | |||||||||||||||

| Other European Countries |

139,955 | 8 | % | 112,188 | 8 | % | 49,539 | 4 | % | |||||||||||||||

| Other Countries |

41,823 | 1 | % | 33,926 | 2 | % | 60,692 | 5 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Consolidated total |

$ | 1,692,539 | 100 | % | $ | 1,445,460 | 100 | % | $ | 1,313,566 | 100 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

5

Table of Contents

THE BUSINESS

Helicopter Flying Operations

Medium and heavy helicopters are generally used to support the oil and gas sector, as well as SAR and EMS. Where appropriate, specialized equipment is installed to support SAR and EMS services.

Contracts with oil and gas customers are typically two to eight years in duration, with an average of four years. Such contracts are ordinarily awarded following competitive bidding processes among pre-qualified operators.

A substantial number of our long-term contracts, defined as three years or longer, contain provisions permitting early termination by the customer without penalty. At the expiration of a contract, customers typically solicit new bids for the next contract period. Contracts are usually awarded based on a number of factors, including price, long-term relationships, safety record of the helicopter service provider and quality of customer service. An incumbent operator commonly has a competitive advantage because of its relationship with the customer, knowledge of site characteristics, investment in infrastructure and demonstrated ability to meet service-level requirements and provide the necessary aircraft and services. Also, customers often want to avoid start-up costs associated with switching to another operator.

Our contracts generally require that fuel be provided by the customer or be charged directly to the customer based on actual fuel costs. As a result, we have no significant exposure to changes in fuel prices. For the year ended April 30, 2012, substantially all of our fuel costs were passed through to our clients.

Flying Operations Competition

CHC is one of two global helicopter service providers to the offshore oil and gas industry; other competitors are smaller, regional operators. The Company has a significant market position in all global offshore oil and gas markets, with the exception of the Gulf of Mexico. Oil and gas companies operating in the Gulf of Mexico utilize primarily light and medium helicopters under short term contracts and, as a result, the economics of providing services in the Gulf of Mexico would be less profitable for CHC than those in other regions of the world.

The Company is well positioned to capitalize on future growth opportunities. As oil and gas wells are depleted, oil companies are developing deep water reserves further offshore. The Company’s global presence, long-term customer relationships and modern fleet of aircraft position it to participate in new oil and gas developments in most offshore oil and gas regions.

Repair and Overhaul

All aircraft airframes, engines and components are required by manufacturer and government regulations to be serviced and overhauled based on flight hours, cycles or the actual condition of parts. The repair and overhaul process includes disassembling, cleaning, inspecting, repairing and reassembling engines, components and accessories, and testing complete engines and components. Operators typically consider the complexity and cost of tasks when choosing whether to perform them in-house or outsource the work to a third-party. MRO companies such as Heli-One are required to obtain licenses from government regulatory bodies and, in many cases, from aircraft manufacturers. Companies active in this industry include manufacturers of helicopters, components and accessories; manufacturer-authorized repair and overhaul operators; and small workshops typically not authorized by the manufacturers. The low cost of transporting components relative to the total cost of repair and overhaul services has resulted in development of a worldwide MRO market.

Our MRO segment, Heli-One, specializes in heavy structural repair, maintenance, overhaul and testing of helicopters and helicopter components in North America and Norway. Our comprehensive capabilities span aircraft including Sikorsky S61N, S76 series and S92A; Bell 212 and 412; Agusta AW139, 119 and 109; Eurocopter Super Puma, AS332, EC225, AS350, AS355, AS365 and BK117. Our engine expertise spans models including Pratt & Whitney PT6; Turbomeca Arriel 1 and 2; Makila; Artouste; Turmo; and GE CT58 and T58.

6

Table of Contents

Heli-One’s main MRO competitors are helicopter manufacturers, which are also our main parts suppliers. Factors that affect competition within the repair and overhaul market include price, quality, safety record and customer service. To minimize issues related to availability and pricing of the parts we need to perform MRO work, Heli-One generally has long-term supply arrangements with the helicopter manufactures and works closely with them on items such as modifications and approvals of parts and components. In addition, we have certain negotiation leverage with the manufacturers on parts, since we are one of the major customers of these manufacturers for new aircraft.

We also provide customers with integrated logistics support, including 24-hour service for all scheduled and unscheduled MRO for engines, dynamic components, repairable components and consumable parts. We also support special mission equipment. Heli-One offers next-day delivery in most locations on a wide range of helicopter parts from all major manufacturers through a global distribution network that includes a global warehouse in the Netherlands. We believe our global buying power gives us competitive pricing on all major components. We believe we provide quality, competitively priced support services to civilian and military helicopter operators worldwide. In addition, we have extensive expertise in all areas of engineering and design for conversion upgrades and refurbishments, including avionics.

Seasonality

Our operations are not subject to seasonality.

PROPERTY AND EQUIPMENT

As of April 30, 2012, the Company’s fleet was comprised of the following aircraft:

| Aircraft Type |

Total | Owned | Leased | |||||||||

| Medium |

||||||||||||

| Sikorsky S76C+ |

22 | 11 | 11 | |||||||||

| Sikorsky S76C++ |

23 | 3 | 20 | |||||||||

| Sikorsky S76A/B/C |

29 | 26 | 3 | |||||||||

| Eurocopter EC135/145/155 |

6 | 1 | 5 | |||||||||

| Eurocopter AS365 Series |

14 | 6 | 8 | |||||||||

| Bell 412 |

13 | 7 | 6 | |||||||||

| Bell 212/214 |

1 | 1 | — | |||||||||

| Agusta AW139 |

29 | 3 | 26 | |||||||||

|

|

|

|

|

|

|

|||||||

| 137 | 58 | 79 | ||||||||||

| Heavy |

||||||||||||

| Eurocopter Super Puma series (i) |

45 | 18 | 27 | |||||||||

| Eurocopter EC225 |

29 | 2 | 27 | |||||||||

| Sikorsky S92A (i) |

33 | 2 | 31 | |||||||||

| Sikorsky S61N |

6 | 6 | — | |||||||||

|

|

|

|

|

|

|

|||||||

| 113 | 28 | 85 | ||||||||||

| Total Helicopters |

250 | 86 | 164 | |||||||||

| Fixed Wing |

2 | 2 | — | |||||||||

|

|

|

|

|

|

|

|||||||

| Total Aircraft |

252 | 88 | 164 | |||||||||

|

|

|

|

|

|

|

|||||||

| (i) | Below is a summary of aircraft under capital lease, which are classified above as owned aircraft: |

| Eurocopter Super Puma Series |

1 | |||

| Sikorsky S92A |

1 |

7

Table of Contents

Lease Obligations

We had entered into aircraft operating leases for 164 aircraft included in our fleet as of April 30, 2012. At April 30, 2012, the total minimum lease payments under aircraft operating leases with expiry dates ranging from fiscal 2013 to fiscal 2022 totaled $1,186.5 million. At our option, we have the right to purchase the majority of aircraft at agreed amounts that are not considered bargain purchase options. Substantially all of the costs to perform inspections, major repairs and overhauls of major components on such leased aircraft are at our expense. We may perform this work through Heli-One or have the work performed by an external MRO service provider. We have also provided guarantees to certain lessors in connection with these aircraft leases. See “Future Cash Requirements—Contractual Obligations and Off-Balance Sheet Arrangements.”

In addition to payment under aircraft operating leases, we had operating lease commitments as of April 30, 2012 for buildings, land and other equipment with minimum lease payments of $90.9 million and expiry dates ranging from fiscal 2013 to fiscal 2099.

For additional details see “Future Cash Requirements—Contractual Obligations and Off-Balance Sheet Arrangements” and see Notes 25, 26 and 28 to the audited annual consolidated financial statements for the year ended April 30, 2012 included elsewhere in this Annual Report on Form 10-K.

Commitments to Acquire New Aircraft

As of April 30, 2012, we had ordered and advanced deposits to purchase 23 aircraft, with expected delivery dates from fiscal 2013 to fiscal 2017. We have committed total capital of approximately $558.0 million for these new aircraft, which will be purchased outright or financed through additional leases on the delivery date. We expect that most of these aircraft will be used internally to support continued growth.

On June 12, 2012, we committed to acquire 10 AW139 helicopters from AgustaWestland to be delivered between October 2012 and September 2014, with options to acquire an additional 16 AW139 helicopters. On June 13, 2012, we exercised our option to acquire two additional EC225s from Eurocopter in addition to the twenty helicopters we committed to acquire in fiscal 2012.

Safety and Insurance

Operation of helicopters involves some degree of risk. Hazards, such as aircraft accidents, collisions and fire, are inherent in providing helicopter services. We maintain a flight safety organization that is responsible for ensuring compliance with safety standards within our organization and the requisite proficiency among flight crews. Our safety organization is responsible for training flight crews, conducting regular safety audits and seminars for all flight personnel, and generally ensuring safe operating techniques and standards consistent with government regulations and customer requirements. In addition, aviation regulatory bodies and customers conduct safety audits to ensure that our standards meet their requirements.

We maintain comprehensive aviation hull and liability insurance coverage in amounts and on terms that reflect prudent helicopter operations. This includes engine and spare-parts coverage. The hull policies insure against the physical loss of or damage to our helicopters. In addition we purchase hull war coverage for losses due to terrorism, hijacking, war, expropriation, confiscation and nationalization. We self retain the risk of the loss of use or loss of profit from our operations, which is mitigated by the possible use of other aircraft given our fleet size.

In addition, we procure property all risks insurance, automobile liability and general liability insurance and the customary corporate insurances.

Facilities

We currently operate in approximately 30 countries worldwide, using facilities that include hangars, supply and service centers, engineering support facilities and offices. In Norway, the United Kingdom, the Netherlands and Australia, we generally own the hangars we use in our helicopter operations, which are located primarily on leased airport land. We typically lease supply and service centers, engineering support facilities and offices from third parties.

The principal properties from which we now conduct our operations are:

| Location |

Operations |

Buildings (Sq. Feet) |

Owned or Leased | |||||||||||

| Land | Buildings | |||||||||||||

| Richmond, British Columbia, Canada |

Corporate Headquarters | 80,000 | Leased | Owned | ||||||||||

| Delta, British Columbia, Canada |

Headquarters for MRO Segment | 240,000 | Leased | Leased | ||||||||||

| Aberdeen, Scotland |

CHC Scotia Limited; Helicopter Services | 42,000 | Leased | Leased | ||||||||||

| CHC Scotia Limited; Terminal Building | 25,000 | Leased | Owned | |||||||||||

| Stavanger, Norway |

CHC Norway AS; Helicopter Services | 199,000 | Leased | Owned | ||||||||||

| Heli-One Norway AS Headquarters; MRO Segment | 179,000 | Leased | Owned | |||||||||||

| Fort Collins, Colorado |

Heli-One American Support, LLC | 80,000 | Leased | Leased | ||||||||||

| Hoofddorp, The Netherlands |

CHC Netherlands BV; Heli-One (Netherlands) BV | 39,000 | Leased | Leased | ||||||||||

| Bergen, Norway |

CHC Norway AS | 66,000 | Leased | Owned | ||||||||||

| Den Helder, The Netherlands |

CHC Helicopter Netherlands BV; Helicopter Services | 56,000 | Owned | Owned | ||||||||||

| Perth, Australia |

CHC Australia Headquarters | 7,400 | Leased | Leased | ||||||||||

| Fort Worth, Texas |

CHC Operations Centre | 26,926 | Leased | Leased | ||||||||||

8

Table of Contents

AVIATION REGULATIONS

Most of the countries in which we conduct flying operations have laws that require us to hold either or both of an operating license and an air operator certificate. Most of these countries also have materiality requirements for issuance of operating licenses and/or air operator certificates that require the holder of such license or certificate to be a qualified national of such country. Companies holding such licenses and certificates must typically be both majority owned and effectively controlled, or controlled in fact, by citizens of the issuing state.

The European Union and the European Economic Area

We operate in the EU and the EEA through our 49.9% ownership in EEA Helicopter Operations B.V. (“EHOB”). EHOB’s five wholly-owned operating subsidiaries operate in four member states of the EU (the UK, the Netherlands, Denmark and Ireland) and Norway, a member state of the EEA. Each of Norway and the member states of the EU must comply with EU Directive 1008/2008 and common rules for the operation of aircraft. Among other things, this directive restricts the issuance of operating licenses to carry passengers for remuneration to those companies that are majority owned and effectively controlled by nationals of a member state of the EU or the EEA. We believe that EHOB, and therefore each of EHOB’s wholly-owned subsidiaries, are both majority owned and effectively controlled by nationals of a member state of the EU.

Canada

Our helicopter operations in Canada are conducted through CHC Helicopters Canada Inc., a company wherein we hold a minority interest. That company’s flying operations are regulated by Transport Canada and are conducted under that company’s air operator’s certificate (AOC). Our ability to conduct our helicopter operating business in Canada is dependent on our ability to maintain our relationship with CHC Helicopters Canada Inc. Our helicopter operations in certain other countries are conducted pursuant to an AOC issued by the Minister of Transport (Canada) under the provisions of the Aeronautics Act (Canada) for which our wholly owned subsidiary holds an exemption until 2015. If we are unable to extend the ministerial exemption pursuant to which this certificate is issued, we will need to obtain licenses and certificates issued by the countries in which we conduct such operations or reach an agreement with CHC Helicopters Canada Inc. and/or customers in such countries to transfer the operations there to CHC Helicopters Canada Inc. We cannot guarantee that we will be able to either extend the ministerial exemption, obtain local licenses and certificates or transfer such operations to CHC Helicopters Canada Inc., either at all or on acceptable terms.

Australia

Civil aviation in Australia is governed by the Civil Aviation Act, 1988, and regulations made thereunder. To operate an aircraft in Australia, it must be registered with the Australian Civil Aviation Safety Authority and a Certificate of Airworthiness must be obtained, be valid and in effect. The operation of an aircraft for a commercial purpose into, out of, or within Australian territory can only be undertaken as authorized by an Air Operators’ Certificate. Our ability to offer our helicopter transportation services in Australia is dependent on maintaining this certificate. Australia does not have a requirement for ownership or control by Australian nationals.

Other Countries

Our operations in other foreign jurisdictions are regulated to various degrees by the governments of such jurisdictions and must be conducted in compliance with those regulations and, where applicable, in accordance with our air service licenses and air operator certificates. These regulations may require us to obtain a license to operate in that country, may favor local companies or require operating permits that can only be obtained by locally registered companies and may impose other nationality requirements. In such cases, we partner with local persons, but there is no assurance regarding which foreign governmental regulations may be applicable in the future to our helicopter operations and whether we would be able to comply with them.

9

Table of Contents

The revocation of any of the licenses discussed above or the termination of any of the relationships with local parties discussed above could have a material adverse effect on our business, financial condition and results of operations.

ENVIRONMENTAL MATTERS

We are subject to extensive laws, rules, regulations and ordinances in the various jurisdictions in which we operate relating to pollution and protection of the environment and to human health and safety, including those related to noise, emissions to the air, releases or discharges to soil or water, the use, storage and disposal of petroleum and other regulated materials, and the remediation of contaminated sites. Our operations, including aircraft maintenance and aircraft fueling, involve the use, handling, storage and disposal of materials that may be classified as hazardous to human health and safety and to the environment. Non-compliance with these regulations may result in significant fines or penalties or limitations on our operations. Many of the countries in which we operate have laws that may impose liability for the investigation and cleanup of releases of regulated materials and the remediation of related environmental damage without regard to negligence or fault. These laws may also expose us to liability for the conduct of, or conditions caused by, others, such as historic spills of regulated materials at our facilities, for acts that were in compliance with all applicable environmental laws at the time such acts were performed, and for contamination at third-party sites where substances were sent for off-site treatment or disposal. Additionally, any failure by us to comply with applicable environmental, health and safety or planning laws and regulations may result in governmental authorities or other third parties taking action against our business that could adversely impact our operations and financial condition. We believe we are in substantial compliance with applicable environmental laws and that ensuring compliance has not, to date, had a material adverse effect upon our financial position. We cannot, however, predict the likelihood of change to these laws or in their enforcement nor the impact that any such change, or any discovery of previously unknown conditions, may have on our costs and financial position. Please see Item 1A Risk Factors – “We are subject to extensive environmental, health and safety laws, rules and regulations, which may have an adverse impact on our business” below.

EMPLOYEES

As of April 30, 2012, we had approximately 4,350 full-time employees. We hire independent contractors on an as needed basis. We believe that our employee relationships are satisfactory.

Certain of our employees in the UK, Ireland, the Netherlands, Norway, Brazil, Canada and Australia (collectively, approximately 65% of our employees) are represented under collective bargaining or union agreements. Any disputes over the terms of these agreements or our potential inability to negotiate acceptable contracts with the unions that represent our employees could result in strikes, work stoppages or other slowdowns by the affected workers. Periodically, certain groups of our employees who are not covered under a collective bargaining agreement consider entering into such an agreement.

If our unionized workers engage in a strike, work stoppage or other slowdown, other employees elect to become unionized, existing labor agreements are renegotiated, or future labor agreements contain terms that are unfavorable to us, we could experience a disruption of our operations or higher ongoing labor costs, which could adversely affect our business, financial condition and results of operations.

AVAILABLE INFORMATION

We are required to file annual, quarterly and current reports and other information with the SEC. You may read and copy any documents filed by us with the SEC at the SEC’s Public Reference Room at 100 F. Street, N.E., Washington, D.C. 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Our filings with the SEC are also available to the public from commercial document retrieval services and at the SEC’s website at http://www.sec.gov.

We also make available on our website at www.chc.ca all of the documents that we file with the SEC, free of charge, as soon as reasonably practicable after we electronically file such material with the SEC. Information contained on our website is not incorporated by reference into this Form 10-K.

| Item 1A. | Risk factors |

The risks described below could have a material adverse impact on our financial position, results of operations, liquidity and cash flows. Although it is not possible to predict or identify all such risks and uncertainties, they may include, but are not limited to, the factors discussed below. Our business operations could also be affected by additional factors that are not presently known to us or that we currently consider not to be material to our operations. You should not consider this list to be a complete statement of all risks and uncertainties.

10

Table of Contents

Our indebtedness and lease obligations could adversely affect our business and liquidity position.

We have a substantial amount of financial debt and lease obligations. If we fail to meet our payment or covenant obligations or otherwise default under the agreements governing indebtedness or lease obligations, the lenders under those agreements will have the right to accelerate the indebtedness or terminate the leases and exercise other rights and remedies against us. These rights and remedies include the rights to repossess and foreclose upon the assets that serve as collateral, initiate judicial foreclosure against us, petition a court to appoint a receiver for us, and initiate involuntary bankruptcy proceedings against us. If lenders or lessors exercise their rights and remedies, our assets may not be sufficient to repay outstanding indebtedness and lease obligations, and we may not have sufficient liquidity after payment of indebtedness and lease obligations to continue our business operations. In some instances, the Company may enter into discussions with the lessor for a covenant reset, amendment or waiver if we anticipate to fail or fail to meet our covenant obligations.

Subsequent to April 30, 2012, a lessor that had been engaged in discussions with the Company approved a financial covenant reset to October 31, 2013. As part of previous negotiations in 2011 with this lessor, the Company also made a commitment to further reduce its total lease portfolio by $64.4 million.

Failure to comply with covenants contained in certain of our lease agreements could limit our ability to maintain our leased helicopter fleet and adversely affect our business.

The terms of certain of our helicopter lease agreements contain covenants that impose operating and financial limitations on us. Such lease agreements limit, among other things, our ability to utilize aircraft in certain jurisdictions and/or sublease the aircraft, and may contain restrictions upon a change of control. A breach of lease covenants could result in an obligation to repay amounts outstanding under the lease. If such an event occurs, we may not be able to pay all amounts due under the leases or refinance such leases on terms satisfactory to us or at all, which could have a material adverse effect on our business, financial condition and results of operations.

Our business requires substantial capital expenditures, lease and working capital financing. Continued deterioration of economic conditions and the current global financial and credit crisis could adversely impact our business and financial condition and we may be unable to obtain needed capital or financing on satisfactory terms or at all. In addition, financial market instability could leave our creditors unable to meet their obligations to us.

Our business requires significant capital expenditure including significant ongoing investment to purchase or lease new aircraft, refinance existing leases and maintain our existing fleet. To the extent that we do not generate sufficient cash from our operations, we will need to raise additional funds through operating lease financing or other debt financing to execute our growth strategy and make the capital expenditures required to successfully operate our business.

Continued concerns about the systemic impact of a potential long-term and wide-spread recession, increased energy costs, the availability and cost of credit, diminished business and consumer confidence and increased unemployment have contributed to increased market volatility and diminished expectations for western and emerging economies, including the jurisdictions in which we operate. In particular, the cost of raising money in the credit markets has increased substantially as many lenders and institutional investors, concerned about the stability of the financial markets generally and about the solvency of counterparties, have increased interest rates, enacted tighter lending standards and reduced and, in some cases, ceased to provide funding, to borrowers.

Such factors may restrict our ability to access capital and bank markets or avail of lease or other financings at a time when we would like to, or need to, which could have an impact on our growth plans or on our flexibility to react to changing economic and business conditions. In addition, our credit facilities and helicopter leases have maintenance covenants which may need to be renegotiated from time to time, and the financial market instability could have an impact on the lenders or lessors willingness to renegotiate these covenants on reasonable terms or at all.

Many of the markets in which we operate are highly competitive, which may result in a loss of market share or a decrease in revenue or profit margins.

Many of the markets in which we operate are highly competitive, which may result in a loss of market share or a decrease in revenue or profit margins. Contracting for helicopter services is usually done through a competitive bidding process among those having the necessary equipment and resources. Factors that affect competition in our industry include price, reliability, safety, professional reputation, availability, equipment and quality of service. We compete against a number of helicopter operators, including the other major global commercial helicopter operator, and other local and regional operators. There can be no assurance that our competitors will not be successful in capturing a share of our present or potential customer base. In addition, many oil and gas companies and government agencies to which we provide services have the financial ability to perform their own helicopter flying operations in-house should they elect to do so.

11

Table of Contents

Our main competitors within the repair and overhaul business are the OEMs of helicopters and helicopter components. As such, our main competitors in this industry are also our main parts suppliers and MRO license providers. A conflict with the OEMs could result in our inability to obtain parts and licenses in a timely manner in required quantities and at competitive prices.

We rely on a limited number of large offshore helicopter support contracts for a limited number of customers. If any of these are terminated early or not renewed, our revenues could decline.

We rely on a limited number of large offshore helicopter support contracts. For the fiscal year ended April 30, 2012, revenue from Statoil ASA totaling $262.7 million and Petrobas totaling $187.8 million was greater than 10% of the Company’s total revenues. Many of our contracts contain clauses that allow for early termination by the customer for convenience, which could have a material adverse effect on our business, financial condition and results of operation.

Failure to maintain standards of acceptable safety performance may have an adverse impact on our ability to attract and retain customers and could adversely impact our reputation, operations and financial performance.

Our customers consider safety and reliability as the two primary attributes when selecting a provider of helicopter transportation services. If we fail to maintain standards of safety and reliability that are satisfactory to our customers, our ability to retain current customers and attract new customers may be adversely affected. Moreover, helicopter crashes or similar disasters of another helicopter operator could impact customer confidence and lead to a reduction in customer contracts, particularly if such helicopter crash or disaster were due to a safety fault in a type of helicopter used in our fleet. In addition, the loss of aircraft as a result of accidents could cause significant adverse publicity and the interruption of air services to our customers, which could adversely impact our reputation, operations and financial results. Our aircraft have been involved in accidents in the past, some of which have included loss of life and property damage. We may experience similar accidents in the future.

Our operations are subject to extensive regulations which may increase our costs and adversely affect us.

The helicopter industry is regulated by various laws and regulations in the jurisdictions in which we operate. The scope of such regulation includes infrastructure and operational issues relating to helicopters, maintenance, spare parts and route flying rights as well as safety and security requirements. We cannot fully anticipate all future changes that might be made to laws and regulations to which we are subject and the possible impact of all such changes.

Our ability to conduct our business is dependent on our ability to maintain authorizations, licenses and certificates, which in many jurisdictions require us to subcontract with third parties to obtain required aircraft operating leases. We are routinely audited to ensure compliance with all flight operation and aircraft maintenance requirements. There can be no assurance that we will pass all audits. Our failure to pass such audits or any breach of regulations applicable to us could result in fines, adverse publicity or grounding of our aircraft, all of which could have a material adverse effect on our business, results of operations and financial condition, especially if a regulatory breach led to a helicopter crash or accident. Changes in laws or regulations could have a material adverse impact on our cost of operations or revenues from operations.

If we are unable to maintain required government-issued licenses for our operations, we will be unable to conduct helicopter operations in the applicable jurisdiction, as outlined below.

Europe

Approximately 25% of our revenue for the fiscal year ended April 30, 2012 originated from helicopter flying services provided by subsidiaries of EEA Helicopter Operations B.V. (“EHOB”), a Dutch Company 49.9% owned by us. These subsidiaries operate in the UK, Denmark, the Netherlands and Ireland (member states of the European Union (“EU”)), and Norway (member state of the European Economic Area (“EEA”)). To operate helicopters in the EU and EEA, an operator must be licensed by the applicable national Civil Aviation Authority. Under applicable European law, an operator must be “effectively controlled” and “majority owned” by nationals of member states of the EU or the EEA to maintain its license. We believe that the majority shareholder in EHOB is an EU national and therefore these subsidiaries are currently “majority owned” and “effectively controlled” within the meaning of European Union and European Economic Area licensing requirements. Any change in the national status of the majority shareholder could affect the licenses of these subsidiaries.

Canada

Our helicopter operations in Canada are conducted through CHC Helicopters Canada Inc., a company wherein we hold a minority interest. That company’s flying operations are regulated by Transport Canada and are conducted under that company’s air operator’s certificate (AOC). Our ability to conduct our helicopter operating business in Canada is dependent on our ability to maintain our relationship with CHC Helicopters Canada Inc. Our helicopter operations in certain other countries are conducted pursuant to an AOC issued by the Minister of Transport (Canada) under the provisions of the Aeronautics Act (Canada) for which our wholly owned subsidiary holds an exemption until 2015. If we are unable to extend the ministerial exemption pursuant to which this certificate is issued, we will need to obtain licenses and certificates issued by the countries in which we conduct such operations or reach an agreement with CHC Helicopters Canada Inc. and/or customers in such countries to transfer the operations there to CHC Helicopters Canada Inc. We cannot guarantee that we will be able to either extend the ministerial exemption, obtain local licenses and certificates or transfer such operations to CHC Helicopters Canada Inc., either at all or on acceptable terms.

12

Table of Contents

Australia

Civil aviation in Australia is governed by the Civil Aviation Act, 1988, and regulations made thereunder. To operate an aircraft in Australia, it must be registered with the Australian Civil Aviation Safety Authority and a Certificate of Airworthiness must be obtained, be valid and in effect. The operation of an aircraft for a commercial purpose into, out of, or within Australian territory can only be undertaken as authorized by an Air Operators’ Certificate. Our ability to offer our helicopter transportation services in Australia is dependent on maintaining this certificate.

Other Countries

Our operations in other foreign jurisdictions are regulated to various degrees by the governments of such jurisdictions and must be conducted in compliance with those regulations and, where applicable, in accordance with our air service licenses and air operator certificates. These regulations may require us to obtain a license to operate in that country, may favor local companies or require operating permits that can only be obtained by locally registered companies and may impose other nationality requirements. In such cases, we partner with local persons, but there is no assurance regarding which foreign governmental regulations may be applicable in the future to our helicopter operations and whether we would be able to comply with them.

The revocation of any of the licenses discussed above or the termination of any of the relationships with local parties discussed above could have a material adverse effect on our business, financial condition and results of operations.

Our operations may suffer due to political and economic uncertainty.

Risks associated with some of our operations include political, social and economic instability, war and civil disturbances or other events that may limit or disrupt markets, expropriation without fair compensation, requirements to award contracts, concessions or licenses to nationals, international exchange restrictions and currency fluctuations, changing political conditions and monetary policies of foreign governments. Any of these events could materially adversely affect our ability to provide services to our international customers. Certain of our helicopter leases and loan agreements impose limitations on our ability, including requiring the prior approval of the lessor or the lender, to locate particular helicopters in certain countries. We cannot provide assurance that these limitations will not affect our ability to allocate resources in the future.

We derive significant revenue from non-wholly owned entities, which, if we develop problems with our non-wholly entities, could adversely affect our financial condition and results of operations.

Aviation regulatory requirements often require us to operate through non-wholly owned entities with local shareholders. We depend to some extent upon good relations with our local shareholders to ensure profitable operations. In the event shareholder disputes arise, these could negatively impact our revenues and profit sharing from these entities.

We are exposed to credit risks.

We are exposed to credit risk on our financial investments due to the ability of our counterparties to fulfill their obligations to us. We manage credit risk by entering into arrangements with established counterparties and through the establishment of credit policies and limits, which are applied in the selection of counterparties.

Credit risk on financial instruments arises from the potential for counterparties to default on their contractual obligations and is limited to those contracts where we would incur a loss in replacing the instrument. We limit our credit risk by dealing only with counterparties that possess investment grade credit ratings and monitor our concentration risk with counterparties on an ongoing basis. The carrying amount of financial assets represents the maximum credit exposure for financial assets.

Credit risk arises on our trade receivables from the unexpected loss in cash and earnings when a customer cannot meet its obligation to us or the value of security provided declines. To mitigate trade credit risk, we have developed credit policies that include the review, approval and monitoring of new customers, annual credit evaluations and credit limits. We do not believe that we are subject to significant concentrations of credit risk as trade receivables consists primarily of amounts due from multinational companies operating in the oil and gas industry and are geographically diverse. There can be no assurances that our risk mitigation strategies will be effective and that credit risk will not adversely affect our results of operations and financial position.

Assimilating any future material acquisitions into our corporate structure may strain our resources and have an adverse impact on our business.

The assimilation of any future material acquisitions we may make will require substantial time, effort, attention and dedication of management resources and may distract management from ordinary operations. The transition process could create a number of potential challenges and adverse consequences, including the possible unexpected loss of key employees, customers or suppliers, a possible loss of revenues or an increase in operating or other costs. Inefficiencies and difficulties may arise because of unfamiliarity with new assets and the business associated with them, new geographic areas and new

13

Table of Contents