Attached files

| file | filename |

|---|---|

| 8-K - XL GROUP LTD | c69992_8-k.htm |

Exhibit 99.1

XL GROUP PLC

MORGAN STANLEY US FINANCIALS CONFERENCE

Peter Porrino

Chief Financial Officer

June 13, 2012

1

Cautionary Note Regarding Forward-Looking

Statements

This presentation contains forward-looking statements. Statements that are not historical facts, including statements about XL’s beliefs, plans or expectations, are forward-looking statements. These statements are based on current plans, estimates and expectations, all of which involve risk and uncertainty. Statements that include the words “expect,” “intend,” “plan,” “believe,” “project,” “anticipate,” “will,” “may” or similar statements of a future or forward-looking nature identify forward-looking statements. Actual results may differ materially from those included in such forward-looking statements and therefore you should not place undue reliance on them. A non-exclusive list of the important factors that could cause actual results to differ materially from those in such forward-looking statements includes (a) changes in the size of XL’s claims relating to natural or man-made catastrophe losses due to the preliminary nature of some reports and estimates of loss and damage to date; (b) trends in rates for property and casualty insurance and reinsurance; (c) the timely and full recoverability of reinsurance placed by XL with third parties, or other amounts due to XL; (d) changes in ratings, rating agency policies or practices; (e) changes in the projected amount of ceded reinsurance recoverables; (f) XL’s ability to successfully implement its business strategy especially during a “soft” market cycle; (g) greater frequency or severity of claims and loss activity than XL’s underwriting, reserving or investment practices anticipate based on historical experience or industry data; (h) changes in general economic conditions, including the effects of inflation and changes in interest rates, credit spreads, foreign currency exchange rates and future volatility in the world’s credit, financial and capital markets that adversely affect the performance and valuation of XL’s investments or access to such markets; (i) developments, including uncertainties related to the ability of Euro-zone countries to service existing debt obligations and the strength of the Euro as a currency and to the financial condition of counterparties, reinsurers and other companies that are at risk of bankruptcy; (j) the impact of downgrades of U.S. securities by credit rating agencies or the European sovereign debt crisis, and the resulting effect on the value of securities (x) in our investment portfolio and (y) posted as collateral by and to us; (k) the potential for changes to methodologies, estimations and assumptions that underlie the valuation of XL’s financial instruments that could result in changes to investment valuations; (l) changes to XL’s assessment as to whether it is more likely than not that it will be required to sell, or has the intent to sell, available-for-sale debt securities before their anticipated recovery; (m) the ability of XL’s subsidiaries to pay dividends to XL Group plc and XLIT Ltd.; (n) the potential effect of regulatory developments in the jurisdictions in which XL operates, including those that could impact the financial markets or increase XL’s business costs and required capital levels; (o) changes in applicable tax laws, tax treaties or tax regulations or the interpretation or enforcement thereof; and (p) the other factors set forth in XL’s reports on Form 10-K, Form 10-Q and other documents on file with the Securities and Exchange Commission. XL undertakes no obligation to update publicly or revise any forward-looking statement, whether as a result of new information, future developments or otherwise.

2

Financial highlights

Commitment to margin expansion

Global Loss Triangles and prudent reserving

Mitigation of European uncertainty

Q&A

Today’s Topics

3

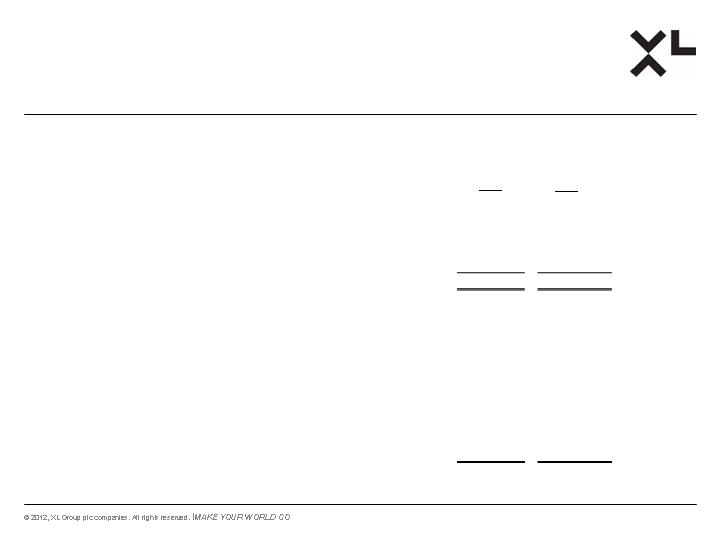

Financial Highlights

For the three months

ended March 31, 2012

$MM, except per share data

Unaudited

Basic book value per share(7) increased by 4% in Q1 2012

Bought back 4.7 million ordinary shares for $100MM during Q1 2012

See slide 13 for applicable footnotes

4

Q1 2012

Q1 2011

(5)

Change

(6)

P&C Operations:

Gross Premiums Written

$2,317

$2,099

10.4%

Net Premiums Written

$1,963

$1,714

14.5%

Net Premiums Earned

$1,358

$1,272

6.8%

Loss Ratio

62.9%

95.1%

(32.2) pts

Combined Ratio

95.3%

125.8%

(30.5) pts

Underwriting Profit (Loss)

$63

($328)

N/M

Net Investment Income (P&C)

$190

$203

(6.4%)

Operating Net Income (loss)

(1)

$165

($163)

N/M

Net Income (loss) to Ordinary Shareholders

$177

($227)

N/M

Operating EPS

- Fully Diluted

(2)

$0.52

($0.52)

N/M

EPS - Fully Diluted

(2)

$0.56

($0.73)

N/M

Annualized Operating ROE

(3) (4)

6.9%

(6.9%)

13.8 pts

Annualized ROE

(4)

7.4%

(9.6%)

17.0 pts

Margin Expansion

5

Loss ratio = left scale

Net premiums Earned (US$ MM) = right scale

Insurance loss ratio

trend (ex CAT and

PYD) has shown

improvement over

past 5 quarters

810

830

850

870

890

910

930

950

67%

68%

69%

70%

71%

72%

73%

74%

75%

76%

77%

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

Loss ratio

NPE

Prudent Reserving Policy Remains an XL Cornerstone

Redundancy estimates by industry analysts

Bubble size = midpoint of analysts’

estimated US$ redundancy

Arrow = year over year trend in redundancy

Green = GLT published for 2011 data

Red = GLT published for 2010 data

Redundancy as % of net premiums earned

Source: Industry analyst reports

Analyst comparison versus

peers that have published

global loss triangles for

2010 or 2011

Positive year-over-year

trend for XL

Flat or up slightly for most

others

Down for one

6

0%

5%

10%

15%

20%

25%

30%

0%

5%

10%

15%

Mitigating Eurozone Exposures

A review of the likely currency of settlement in the event of a full Euro break-up shows that XL is overweight a number of core countries (i.e. Netherlands and Germany), underweight a number of peripheral countries (i.e. Ireland, Spain and Italy) and broadly flat the others

XL’s policy is to match assets and liabilities by currency so that if Euro assets lose value in US$ terms, we would see an offsetting reduction in liability values

In addition, we hedge out the majority of the FX risk arising from holding capital in Euro

As of March 31, 2012 we were long $17 million equivalent of Euro on a net basis

The main underweight position is in Ireland, which is driven by the Life reinsurance book

We have liabilities to Irish cedents where the assets have been invested in non-Irish assets

Other underweight positions (i.e. Spain and Italy) are driven by local P&C insurance reserves that are backed by assets issued by Eurozone core countries

7

Notes:

(1)

Country of Risk is defined as the country of the issuer’s main operations

(2)

Eurozone Core includes Austria, Belgium, Finland, France, Germany, Luxembourg, and Netherlands

(3)

Non-Eurozone Europe includes Supranational, Swiss and other Europe issuers

(4)

GIIPS includes Greece, Ireland, Italy, Portugal and Spain

(5)

Structured Credit includes Covered bonds and Pfandbriefe holdings

(6)

Note that $2,784MM of the $5,373MM total exposure is Euro currency denominated

Exposure by Continental European Country of Risk

(US Dollar equivalent, $MM)

(As of May 31, 2012)

8

Country

Net Unrealized

Net Unrealized

Net Unrealized

Net Unrealized

Net Unrealized

of Risk

(1)

Gain/(Loss)

Gain/(Loss)

Gain/(Loss)

Gain/(Loss)

Gain/(Loss)

Eurozone Core

(2)

$ 2,029

$36

$ 1,160

$15

$ 348

($2)

$ 213

$7

$ 3,750

$56

Non-Eurozone Europe (3)

731

16

268

11

302

(6)

86

1

1,387

22

GIIPS

(4)

18

(1)

202

(4)

4

(2)

12

-

236

(7)

Total

$ 2,778

$51

$ 1,630

$22

$ 654

($10)

$ 311

$8

$ 5,373

$71

Governments

Corp Non-Financials

Corp Financials

Aggregate Europe

(6)

Structured Credit

(5)

XL Policies to Manage Investment Risk in Continental

Europe

Investment portfolio positioned defensively vis-à-vis Continental Europe

Underweight corporate exposure, particularly banks

Most bank exposure is to national champions in northern Europe

Exposure to peripheral corporates is modest

$4MM financial and $202MM non-financial at May 31, 2012

Majority of non-financial exposure is essential services or issuers with significant geographic business

diversification

Nearly 80% of exposure is from Germany, France, Switzerland and the Netherlands

We have taken further action since May 31, 2012 to reduce tail risk exposure in

the event

conditions worsen in the financial markets in Europe

Reduced Continental European financials by approximately $100MM, or 8%

9

Continue margin expansion

Grow premium in disciplined manner

Continue prudent reserving policies

Maintain matched European asset and liability profiles

Conclusions

10

Q&A

11

Reconciliation

For the three Months ended March 31, 2012

$MM, except per share data

Unaudited

The following is a reconciliation of the Company’s net income (loss) attributable to ordinary shareholders to operating net income (loss) (Note 1) and also includes the calculation of annualized return on ordinary shareholders’ equity based on operating net income (loss) for the three months ended March 31, 2012 and 2011:

Please see slide 13 for applicable footnotes

12

2012

2011

(5) (6)

Net income (loss) attributable to ordinary shareholders

176,628

$

(227,284)

$

Net realized (gains) losses on investments, net of tax

(20,462)

63,315

Net realized and unrealized (gains) losses on derivatives, net of tax

(697)

(5,209)

Net realized and unrealized (gains) losses on investments and derivatives related to the

Company's insurance company affiliates

(40)

(874)

Foreign exchange (gains) losses, net of tax

9,802

7,197

Gain on repurchase of non-controlling interest preference ordinary shares

-

(134)

Operating net income (loss)

(1)

165,231

$

(162,989)

$

Per ordinary share results:

(2)

Net income (loss) attributable to ordinary shareholders

0.56

$

(0.73)

$

Operating net income (loss)

(1)

0.52

$

(0.52)

$

Weighted average ordinary shares outstanding:

Basic

315,120,210

311,478,402

Diluted - Net income

317,639,325

311,478,402

Diluted - Operating net income

317,639,325

311,478,402

Return on ordinary shareholders' equity

:

Closing ordinary shareholders' equity

(4) (8)

9,710,022

$

9,253,918

$

Average ordinary shareholders' equity

(4) (8)

9,560,840

$

9,425,695

$

Operating net income (loss)

(1)

165,231

$

(162,989)

$

Annualized operating net income (loss)

(1) (3)

660,924

N/M

Annualized return on ordinary shareholders' equity

(3) (4) (8)

- operating net income (loss)

(1)

6.9%

(6.9%)

Three months ended

March 31

Footnotes

1

Defined as net income (loss) attributable to ordinary shareholders excluding (1) net realized gains and losses on investments, net of tax for XL, (2) net realized and unrealized gains and losses on derivatives, net of tax, for XL, (3) its share of items (1) and (2) for the Company’s insurance company affiliates for the periods presented, (4) goodwill impairment charges, net of tax, (5) the gains recognized on the repurchase of XLIT Ltd.’s preference ordinary shares and (6) foreign exchange gains or losses, net of tax. “Operating net income” and “return on ordinary shareholders’ equity” based on operating net income are “non-GAAP financial measures.” See the schedule entitled “Reconciliation” on slide 12 for a reconciliation of “operating net income” to net income (loss) attributable to ordinary shareholders and the calculation of “return on ordinary shareholders’ equity” based on operating net income to average ordinary shareholders’ equity.

2

Diluted weighted average number of ordinary shares outstanding is used to calculate per share data except where it is anti-dilutive to earnings per share or where there is a net loss. When it is anti-dilutive or when a net loss occurs, basic weighted average ordinary shares outstanding is utilized in the calculation of fully diluted net loss per share and fully diluted net operating loss per share.

3 Calculated based on operating net income. See Note 1 above.

4

On January 1, 2012, for all fiscal years and interim periods presented, the Company adopted a FASB accounting standards update to address disparities in practice regarding the interpretation of which costs relating to the acquisition of new and renewal insurance contracts qualify for deferral. This guidance was adopted on a retrospective basis. The impact of adoption of this guidance was a reduction in deferred acquisition costs of approximately $21 million, a reduction in deferred tax liabilities of approximately $7 million, and a corresponding reduction in opening retained earnings of approximately $14 million from the amounts presented in the Company’s December 31, 2011 balance sheet. The adoption of this guidance did not have an impact on the Company’s consolidated statements of income or comprehensive income.

5 Certain amounts have been reclassified to conform with the current period presentation.

6 N/M = not meaningful.

7 Book value per ordinary share is a non-GAAP financial measure. See “Comment on Regulation G” on slide 14.

8 Ordinary shareholders’ equity is defined as total shareholders’ equity less non-controlling interest in equity of consolidated subsidiaries.

13

Comment on Regulation G

XL presents its operations in the way it believes will be most meaningful and useful to investors, analysts, rating agencies and others who use XL’s financial information

in evaluating XL’s performance. This

presentation contains the presentation of (i) operating net income (loss) (“Operating Net Income”), which is defined as net income (loss) attributable to ordinary shareholders excluding: (1)

net realized gains and

losses on investments net of tax, for XL, (2) net realized and unrealized gains and losses on derivatives, net of tax, for XL, (3) its share of items (1) and (2) for the Company’s insurance company affiliates for the

periods

presented, (4) goodwill impairment charges, net of tax, (5) the gains recognized on the repurchase of XLIT Ltd.’s preference ordinary shares and (6) foreign exchange gains or losses, net of tax, (ii) annualized

return on ordinary shareholders’

equity (“ROE”) based on operating net income (loss) (“Operating ROE”) and (iii) book value per ordinary share, (ordinary shareholders’ equity divided by the number of shares

outstanding at any period end).

These items are “non-GAAP financial measures” as defined in Regulation G. The reconciliation of such measures to the most directly comparable GAAP financial measures in

accordance with Regulation G is included herein.

Although the investment of premiums to generate income (or loss) and realized capital gains (or losses) is an integral part of XL’s operations, the determination to realize

capital gains (or losses) is independent of the

underwriting process. In addition, under applicable GAAP accounting requirements, losses can be created as the result of other than temporary declines in value and from goodwill impairment charges

without actual

realization. In this regard, certain users of XL’s financial information, including certain rating agencies, evaluate earnings before tax and capital gains to understand the profitability of the recurring sources of income

without the effects of these two variables. Furthermore, these users believe that, for many companies, the timing of the realization of capital gains and the recognition of goodwill impairment charges are largely a

function of economic and interest

rate conditions.

Net realized and unrealized (gains) losses on derivatives, net of tax include all derivatives entered into by XL other than certain credit derivatives. With respect to

credit derivatives, because XL and its insurance

company operating affiliates generally hold financial guaranty contracts written in credit default derivative form to maturity, the net effects of the changes in fair value of these credit derivatives are

excluded (similar

with other companies’ treatment of such contracts) as the changes in fair value each quarter are not indicative of underlying business performance.

The gains recognized on the repurchase of XLIT Ltd.’s preference ordinary shares are excluded as these transactions were capital in nature and outside the scope of the Company’s underlying business.

Foreign exchange gains and losses in the income statement are only one element of the overall impact of foreign exchange fluctuations on the Company’s financial position

and are not representative of any economic

gain or loss made by the Company. Accordingly, it is not a relevant indicator of financial performance and it is excluded.

In summary, XL evaluates the performance of and manages its business to produce an underwriting profit. In addition to presenting net income (loss), XL believes that showing

operating net income (loss) enables

investors and other users of XL’s financial information to analyze XL’s performance in a manner similar to how management of XL analyzes performance. In

this regard, XL believes that providing only a GAAP

presentation of net income (loss) makes it much more difficult for users of XL’s financial information to evaluate XL’s underlying business. Also, as stated above, XL believes that the equity

analysts and certain rating

agencies that follow XL (and the insurance industry as a whole) exclude these items from their analyses for the same reasons and they request that XL provide this non-GAAP financial information on a regular basis.

Operating ROE is a widely used measure of any company’s profitability that is calculated by dividing annualized Operating Net Income for any period by the average of the

opening and closing ordinary shareholders’

equity. The Company establishes target Operating ROEs for its total operations, segments and lines of business. If the Company’s Operating ROE targets are not met with respect to any line of business

over time,

the Company seeks to re-evaluate these lines.

The Company believes that book value per ordinary share is a financial measure important to investors and other interested parties who benefit from having a consistent basis

for comparison with other companies

within the industry. However, this measure may not be comparable to similarly titled measures used by companies either outside or inside of the insurance industry.

14