Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Xcerra Corp | Financial_Report.xls |

| EX-31.2 - SECTION 302 CFO CERTIFICATION - Xcerra Corp | d316800dex312.htm |

| EX-31.1 - SECTION 302 CEO CERTIFICATION - Xcerra Corp | d316800dex311.htm |

| EX-32 - SECTION 906 CEO AND CFO CERTIFICATION - Xcerra Corp | d316800dex32.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended April 30, 2012

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 000-10761

LTX-CREDENCE CORPORATION

(Exact name of registrant as specified in its charter)

| Massachusetts | 04-2594045 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 825 University Ave, Norwood, Massachusetts |

02062 | |

| (Address of principal executive offices) | (Zip Code) | |

(781) 461-1000

(Registrant’s telephone number, including area code)

[None]

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

| Class |

Outstanding at June 5, 2012 | |

| Common Stock, $0.05 par value per share | 48,976,634 shares |

Table of Contents

LTX-CREDENCE CORPORATION

| Page Number |

||||||

| Part I. |

FINANCIAL INFORMATION |

|||||

| Item 1. |

Financial Statements |

|||||

| Consolidated Balance Sheets as of April 30, 2012 and July 31, 2011 |

3 | |||||

| 4 | ||||||

| Consolidated Statements of Cash Flows for the Nine Months Ended April 30, 2012 and April 30, 2011 |

5 | |||||

| 6 | ||||||

| Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

16 | ||||

| Item 3. |

25 | |||||

| Item 4. |

25 | |||||

| Part II. |

||||||

| Item 1. |

25 | |||||

| Item 1A. |

26 | |||||

| Item 2. |

26 | |||||

| Item 6. |

26 | |||||

| 27 | ||||||

| 28 | ||||||

2

Table of Contents

CONSOLIDATED BALANCE SHEETS

(In thousands)

| April 30, 2012 |

July 31, 2011 |

|||||||

| (Unaudited) | ||||||||

| ASSETS |

||||||||

| Current assets: |

||||||||

| Cash and cash equivalents |

$ | 35,339 | $ | 123,198 | ||||

| Marketable securities |

101,520 | 39,417 | ||||||

| Accounts receivable—trade, net of allowances of $39 and $40 |

28,658 | 42,646 | ||||||

| Accounts receivable—other |

268 | 408 | ||||||

| Inventories |

28,591 | 21,145 | ||||||

| Prepaid expenses and other current assets |

3,809 | 4,368 | ||||||

|

|

|

|

|

|||||

| Total current assets |

198,185 | 231,182 | ||||||

| Property and equipment, net |

18,742 | 20,827 | ||||||

| Intangible assets, net |

3,944 | 6,317 | ||||||

| Goodwill |

43,030 | 43,030 | ||||||

| Other assets |

1,229 | 759 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 265,130 | $ | 302,115 | ||||

|

|

|

|

|

|||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY |

||||||||

| Current liabilities: |

||||||||

| Accounts payable |

$ | 10,656 | $ | 15,232 | ||||

| Accrued expenses |

18,197 | 24,677 | ||||||

| Deferred revenue |

5,559 | 5,589 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

34,412 | 45,498 | ||||||

| Other long-term liabilities |

14,500 | 15,897 | ||||||

| Commitments and contingencies (Note 5) |

||||||||

| Stockholders’ equity: |

||||||||

| Common stock |

2,453 | 2,480 | ||||||

| Additional paid-in capital |

752,715 | 756,046 | ||||||

| Accumulated other comprehensive income |

121 | 41 | ||||||

| Accumulated deficit |

(539,071 | ) | (517,847 | ) | ||||

|

|

|

|

|

|||||

| Total stockholders’ equity |

216,218 | 240,720 | ||||||

|

|

|

|

|

|||||

| Total liabilities and stockholders’ equity |

$ | 265,130 | $ | 302,115 | ||||

|

|

|

|

|

|||||

See accompanying Notes to Consolidated Financial Statements.

3

Table of Contents

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(Unaudited)

(In thousands, except per share data)

| Three Months Ended April 30, |

Nine Months Ended April 30, |

|||||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| Net product sales |

$ | 21,753 | $ | 48,435 | $ | 60,761 | $ | 155,340 | ||||||||

| Net service sales |

9,084 | 10,230 | 27,910 | 31,520 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net sales |

30,837 | 58,665 | 88,671 | 186,860 | ||||||||||||

| Cost of sales |

15,024 | 22,203 | 43,941 | 71,730 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Gross profit |

15,813 | 36,462 | 44,730 | 115,130 | ||||||||||||

| Engineering and product development expenses |

12,223 | 13,314 | 37,503 | 39,188 | ||||||||||||

| Selling, general and administrative expenses |

8,829 | 11,755 | 26,496 | 37,611 | ||||||||||||

| Amortization of purchased intangible assets |

791 | 1,490 | 2,372 | 4,471 | ||||||||||||

| Restructuring |

739 | 248 | 926 | 363 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income (loss) from operations |

(6,769 | ) | 9,655 | (22,567 | ) | 33,497 | ||||||||||

| Other income (expense): |

||||||||||||||||

| Interest expense |

(47 | ) | (112 | ) | (129 | ) | (257 | ) | ||||||||

| Investment income |

266 | 96 | 650 | 255 | ||||||||||||

| Other income, net |

15 | 13,687 | 366 | 14,076 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income (loss) before provision for (benefit from) income taxes |

(6,535 | ) | 23,326 | (21,680 | ) | 47,571 | ||||||||||

| Provision for (benefit from) income taxes |

93 | (295 | ) | (456 | ) | (430 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) |

$ | (6,628 | ) | $ | 23,621 | $ | (21,224 | ) | $ | 48,001 | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) per share: |

||||||||||||||||

| Basic |

$ | (0.14 | ) | $ | 0.48 | $ | (0.43 | ) | $ | 0.97 | ||||||

| Diluted |

$ | (0.14 | ) | $ | 0.47 | $ | (0.43 | ) | $ | 0.96 | ||||||

| Weighted-average common and common equivalents shares used in computing net income (loss) per share: |

||||||||||||||||

| Basic |

49,017 | 49,491 | 49,156 | 49,348 | ||||||||||||

| Diluted |

49,017 | 50,368 | 49,156 | 50,240 | ||||||||||||

| Comprehensive income (loss): |

||||||||||||||||

| Net income (loss) |

$ | (6,628 | ) | $ | 23,621 | $ | (21,224 | ) | $ | 48,001 | ||||||

| Unrealized gain (loss) on marketable securities |

(13 | ) | (1 | ) | 80 | (3 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Comprehensive income (loss) |

$ | (6,641 | ) | $ | 23,620 | $ | (21,144 | ) | $ | 47,998 | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

See accompanying Notes to Consolidated Financial Statements.

4

Table of Contents

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

(In thousands, except per share data)

| Nine Months Ended April 30, |

||||||||

| 2012 | 2011 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: |

||||||||

| Net income (loss) |

$ | (21,224 | ) | $ | 48,001 | |||

| Add (deduct) non-cash items: |

||||||||

| Stock-based compensation |

3,435 | 2,851 | ||||||

| Depreciation and amortization |

8,352 | 13,434 | ||||||

| Restructuring |

926 | 363 | ||||||

| Other |

1,535 | 406 | ||||||

| Changes in operating assets and liabilities: |

||||||||

| Accounts receivable |

13,570 | 3,584 | ||||||

| Inventories |

(8,937 | ) | (752 | ) | ||||

| Prepaid expenses |

595 | (1,030 | ) | |||||

| Other assets |

— | (509 | ) | |||||

| Accounts payable |

(4,576 | ) | (835 | ) | ||||

| Accrued expenses |

(8,108 | ) | (4,215 | ) | ||||

| Deferred revenue |

(31 | ) | (3,123 | ) | ||||

|

|

|

|

|

|||||

| Net cash (used in) provided by operating activities |

(14,463 | ) | 58,175 | |||||

| CASH FLOWS FROM INVESTING ACTIVITIES: |

||||||||

| Proceeds from sales and maturities of available-for-sale securities |

53,536 | 18,836 | ||||||

| Proceeds from sales and maturities of held-to-maturity securities |

5,750 | 3,200 | ||||||

| Purchases of available-for-sale securities |

(112,229 | ) | (20,336 | ) | ||||

| Purchases of held-to-maturity securities |

(10,678 | ) | (15,187 | ) | ||||

| Purchases of property and equipment |

(2,485 | ) | (3,716 | ) | ||||

|

|

|

|

|

|||||

| Net cash used in investing activities |

(66,106 | ) | (17,203 | ) | ||||

| CASH FLOWS FROM FINANCING ACTIVITIES: |

||||||||

| Repurchases of common stock |

(6,077 | ) | — | |||||

| Payments of tax withholdings for vested RSUs, net of proceeds from stock option exercises |

(1,128 | ) | (658 | ) | ||||

| Proceeds from shares issued from employees’ stock purchase plan |

397 | 320 | ||||||

|

|

|

|

|

|||||

| Net cash used in financing activities |

(6,808 | ) | (338 | ) | ||||

| Effect of exchange rate changes on cash and cash equivalents |

(482 | ) | 666 | |||||

|

|

|

|

|

|||||

| Net (decrease) increase in cash and cash equivalents |

(87,859 | ) | 41,300 | |||||

| Cash and cash equivalents at beginning of period |

123,198 | 74,978 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents at end of period |

$ | 35,339 | $ | 116,278 | ||||

|

|

|

|

|

|||||

See accompanying Notes to Consolidated Financial Statements.

5

Table of Contents

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. THE COMPANY

LTX-Credence Corporation (“LTX-Credence” or the “Company”) provides market-focused, cost-optimized automated test equipment (ATE) solutions. The Company designs, manufactures, markets and services ATE solutions that address the broad, divergent test requirements of the wireless, computing, automotive and digital consumer market segments. Semiconductor designers and manufacturers worldwide use its equipment to test their devices during the manufacturing process. After testing, these devices are then incorporated in a wide range of products, including computers, mobile internet equipment such as wireless access points and interfaces, broadband access products such as cable modems and set top boxes, personal communication products such as mobile phones and personal digital music players, consumer products such as televisions, videogame systems, digital cameras and automobile electronics, and power management in portable and automotive electronics. The Company also sells hardware and software support and maintenance services for its test systems. The Company is headquartered and has a development facility in Norwood, Massachusetts, development facilities in Milpitas, California and Beaverton, Oregon, and sales and service facilities located across the world to support its customer base.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The accompanying unaudited consolidated financial statements have been prepared pursuant to the Rules of the Securities and Exchange Commission for quarterly reports on Form 10-Q and, accordingly, these footnotes condense or omit information and disclosures which substantially duplicate information provided in our latest audited financial statements. These unaudited consolidated financial statements should be read in conjunction with the financial statements and notes included in our Annual Report on Form 10-K for the year ended July 31, 2011. In the opinion of management, these unaudited consolidated financial statements reflect all adjustments, including normal recurring accruals, necessary for a fair presentation of the results for the interim periods presented. The operating results for the three or nine months ended April 30, 2012 are not necessarily indicative of future trends or the Company’s results of operations for the entire fiscal year ending July 31, 2012.

These unaudited consolidated financial statements include the accounts of the Company and its wholly owned subsidiaries. All significant inter-company transactions and balances have been eliminated in consolidation.

Foreign Currency Remeasurement

The financial statements of the Company’s foreign subsidiaries are remeasured in accordance with Financial Accounting Standards Board Accounting Standards Codification (“FASB ASC”) Topic 830, Foreign Currency Matters. The subsidiaries’ functional currency is the U.S. dollar. Accordingly, the Company’s foreign subsidiaries remeasure monetary assets and liabilities at month-end exchange rates while long-term non-monetary items are remeasured at historical rates. Income and expense accounts are remeasured at the average rates in effect during the month. Net gains or losses resulting from foreign currency remeasurement and transaction gains or losses are included in the consolidated results of operations as a component of Other income, net, and were not significant for the three or nine months ended April 30, 2012 or 2011.

Derivatives

The Company conducts business in a number of foreign countries, with certain transactions denominated in local currencies. The purpose of the Company’s foreign currency management is to minimize the effect of exchange rate fluctuations on certain foreign denominated net monetary assets. The Company does not use derivative financial instruments for trading or speculative purposes.

During the fiscal year ended July 31, 2011, the Company entered into a derivative in the form of a foreign currency forward contract to minimize the effect of exchange rate fluctuations associated with the remeasurement of net monetary assets denominated in foreign currencies. This transaction did not qualify for hedge accounting under FASB ASC Topic 815, Derivatives and Hedging. The change in fair value of this derivative is recorded directly in the Company’s statement of operations and offsets the change in fair value of the net monetary assets denominated in foreign currencies.

6

Table of Contents

The notional amount and market amount of the foreign currency forward contract was $4.6 million and $4.8 million, respectively, at July 31, 2011. During the nine months ended April 30, 2012, the Company’s foreign currency forward contract expired. The following table summarizes the fair value of the derivative instrument as of July 31, 2011 and reflects the expiration of the derivative instrument as of April 30, 2012:

| Derivatives not designated as hedging instruments: |

Balance Sheet Location | April 30, 2012 |

July 31, 2011 |

|||||||||

| (in thousands) | ||||||||||||

| Foreign exchange contract |

Other accrued expenses | $ | — | $ | 187 | |||||||

|

|

|

|

|

|||||||||

Revenue Recognition

The Company recognizes revenue based on guidance provided in FASB ASC Topic 605, Revenue Recognition (“ASC 605”). The Company recognizes revenue when persuasive evidence of an arrangement exists, delivery has occurred or services have been rendered, the seller’s price is fixed or determinable and collectability is reasonably assured.

Revenue related to equipment sales is recognized when: (a) the Company has a written sales agreement; (b) delivery has occurred; (c) the price is fixed or determinable; (d) collectability is reasonably assured; (e) the product delivered is standard product with historically demonstrated acceptance; and (f) there is no unique customer acceptance provision or payment tied to acceptance or an undelivered element significant to the functionality of the system. Generally, payment terms are time based after product shipment. When sales to a customer involve multiple elements, revenue is recognized on the delivered element provided that (1) the undelivered element is a proven technology, (2) there is a history of acceptance on the product with the customer, (3) the undelivered element is not essential to the customer’s application, (4) the delivered item(s) has value to the customer on a stand-alone basis, and (5) if the arrangement included a general right of return relative to the delivered item(s), delivery or performance of the undelivered item(s) is considered probable and substantially in the control of the Company. The arrangement consideration, or the amount of revenue to be recognized on each separate unit of accounting, is allocated at the inception of the arrangement to all deliverables on the basis of their relative selling price based on the provisions of Accounting Standards Update (“ASU”) 2009-13.

Revenue related to spare parts is recognized on shipment.

Revenue related to maintenance and service contracts is recognized ratably over the duration of the contracts.

Engineering and Product Development Costs

The Company expenses all engineering and product development costs as incurred. Expenses subject to capitalization in accordance with the FASB ASC Topic 985, Software, relating to certain software development costs, were insignificant for the three and nine months ended April 30, 2012 and 2011, respectively.

Shipping and Handling Costs

Shipping and handling costs are included in cost of sales in the consolidated statements of operations. These costs, when included in the sales price charged for products, are recognized in net sales. Shipping and handling costs were insignificant for the three and nine months ended April 30, 2012 and 2011, respectively.

Income Taxes

The provision for (benefit from) income taxes relates principally to operating results of foreign entities in jurisdictions primarily in Asia and Europe and the release of reserves due to statute of limitation expirations. The Company recorded an income tax provision/(benefit) of $0.1 million and ($0.5) million, respectively, for the three and nine months ended April 30, 2012 related to the release of reserves due to statute of limitations expirations. For the three and nine months ended April 30, 2011, the Company recorded an income tax benefit of ($0.3) million and ($0.4) million primarily due to the receipt of an income tax refund in the United States.

As of April 30, 2012 and July 31, 2011, the Company’s total liability for unrecognized income tax benefits was $8.6 million and $9.1 million, respectively, (of which $4.8 million and $5.3 million, respectively, if recognized, would impact the Company’s income tax rate and are recorded in other long-term liabilities on the Company’s consolidated balance sheet). The Company recognizes interest and penalties related to uncertain tax positions as a component of income tax expense. As of April 30, 2012 and July 31, 2011, the Company had accrued approximately $1.1 million and $1.3 million, respectively, for potential payment of accrued interest and penalties.

The Company conducts business globally and, as a result, the Company and its subsidiaries or branches file income tax returns in the U.S. federal jurisdiction and various U.S. state and foreign jurisdictions. In the normal course of business the Company is subject to examination by taxing authorities throughout the world, including such major jurisdictions as the United States, Singapore, France and Germany. With few exceptions, the Company is no longer subject to U.S. federal, state, local or non-U.S. income tax examinations for years before 2000.

7

Table of Contents

As a result of completion of the merger with Credence Systems Corporation (“Credence”) on August 29, 2008, a greater than 50% cumulative ownership change in both entities triggered a significant limitation in net operating loss carryforward utilization. The Company’s ability to use operating and acquired net operating loss and credit carryforwards is subject to annual limitation as defined in sections 382 and 383 of the Internal Revenue Code. The Company currently estimates that the annual limitation on its use of net operating losses generated through August 29, 2008 will be approximately $10.1 million which, based on currently enacted federal carryforward periods, limits the amount of net operating losses able to be used to approximately $202.0 million. The Company will continue to assess the realizability of these carryforwards in subsequent periods.

Accounting for Stock-Based Compensation

The Company maintains and has made awards that remain outstanding under various stock-based compensation plans, including the Company’s 2010 Stock Plan, as amended on November 26, 2010 (“2010 Plan”), the Company’s 2004 Stock Plan, the Company’s 2001 Stock Plan, the Company’s 1999 Stock Plan, and the Company’s 1993 Stock Plan. In addition, the Company assumed and has made awards that remain outstanding under the StepTech, Inc. Stock Option Plan as part of its acquisition of StepTech, Inc. (“StepTech”) and the Credence 2005 Stock Incentive Plan in connection with its acquisition of Credence. The Company can only grant new awards under the 2010 Plan.

The Company recognizes stock-based compensation expense for its equity awards in accordance with the provisions of FASB ASC Topic 718, Compensation – Stock Compensation (“ASC 718”). Under ASC 718, the Company is required to recognize as expense the estimated fair value as of the grant date of all share-based payments to employees. In accordance with this standard, the Company has elected to recognize the compensation cost of each service based award on a straight-line basis over the vesting period of such award. The Company recorded stock-based compensation expense of approximately $0.9 million and $3.4 million for the three and nine months ended April 30, 2012, respectively, and $0.9 million and $2.9 million, respectively, for the three and nine months ended April 30, 2011, in connection with its share-based payments.

The Company granted 117,500 restricted stock unit awards during the three months ended April 30, 2012, all of which are service-based and vest over four years, 25% per year.

The Company granted 72,000 restricted stock unit awards during the three months ended January 31, 2012, all of which are service-based and vest in one year.

The Company granted 737,100 restricted stock unit awards during the three months ended October 31, 2011, all of which are service-based and have four year vesting terms.

Product Warranty Costs

The Company’s products are sold with warranty provisions that require it to remedy deficiencies in quality or performance of products over a specified period of time at no cost to its customers. The Company generally offers a warranty for all of its products, the standard terms and conditions of which are based on the product sold and the customer. For all tester products sold, the Company accrues a liability for the estimated cost of standard warranty at the time of tester shipment and defers the portion of product revenue attributed to the estimated selling price of non-standard warranty. Costs for non-standard warranties are expensed as incurred. Factors that impact the expected product warranty liability include the number of installed testers, historical and anticipated product failure rates, material usage and service labor costs. The Company periodically assesses the adequacy of its recorded product warranty liability and adjusts it as necessary.

The following table shows the change in the product warranty liability, as required by FASB ASC Topic 460, Guarantees, for the nine months ended April 30, 2012 and 2011:

| Nine Months Ended April 30, |

||||||||

| Product Warranty Activity |

2012 | 2011 | ||||||

| (in thousands) | ||||||||

| Balance at beginning of period |

$ | 2,281 | $ | 4,398 | ||||

| Warranty expenditures for current period |

(2,426 | ) | (6,441 | ) | ||||

| Changes in liability related to pre-existing warranties |

60 | (257 | ) | |||||

| Provision for warranty costs in the period |

1,658 | 5,145 | ||||||

|

|

|

|

|

|||||

| Balance at end of period |

$ | 1,573 | $ | 2,845 | ||||

|

|

|

|

|

|||||

Net income (loss) per share

8

Table of Contents

Net income (loss) per share

Basic net income (loss) per share is computed by dividing net income (loss) available to common stockholders by the weighted average number of common shares outstanding for the period. Diluted net income (loss) per share reflects the maximum dilution that would have resulted from the assumed exercise and share repurchase related to dilutive stock options and restricted stock units and is computed by dividing net income (loss) by the weighted average number of common shares and the dilutive effect of all securities outstanding. Reconciliation between basic and diluted earnings per share is as follows:

| Three Months Ended April 30, |

Nine Months Ended April 30, |

|||||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| (in thousands, except per share data) | ||||||||||||||||

| Net income (loss) |

$ | (6,628 | ) | $ | 23,621 | $ | (21,224 | ) | $ | 48,001 | ||||||

| Basic EPS: |

||||||||||||||||

| Weighted average shares outstanding |

49,017 | 49,491 | 49,156 | 49,348 | ||||||||||||

| Basic EPS |

$ | (0.14 | ) | $ | 0.48 | $ | (0.43 | ) | $ | 0.97 | ||||||

| Diluted EPS: |

||||||||||||||||

| Weighted average shares outstanding |

49,017 | 49,491 | 49,156 | 49,348 | ||||||||||||

| Plus: impact of stock options and unvested restricted stock units |

— | 877 | — | 892 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average common and common equivalents shares outstanding |

49,017 | 50,368 | 49,156 | 50,240 | ||||||||||||

| Diluted EPS |

$ | (0.14 | ) | $ | 0.47 | $ | (0.43 | ) | $ | 0.96 | ||||||

For the three and nine months ended April 30, 2012 and 2011 stock options to purchase approximately 1.3 million shares and 1.5 million shares, respectively, of common stock were not included in the calculation of diluted net income (loss) per share because their inclusion would have been anti-dilutive. These options could be dilutive in the future. The calculation of diluted net loss per share also excludes 1.9 million restricted stock units for the periods ended April 30, 2012 in accordance with the contingently issuable shares guidance of FASB ASC Topic 260, Earnings Per Share. The calculation of diluted net income per share for the three and nine months ended April 30, 2011 also excludes the impact of conversion features of the Company’s Convertible Subordinated Notes that matured in May 2011, as including them would have been anti-dilutive.

Cash and Cash Equivalents and Marketable Securities

The Company considers all highly liquid investments that are readily convertible to cash and that have original maturity dates of three months or less to be cash equivalents. Cash and cash equivalents consist primarily of operating cash. Marketable securities consist primarily of debt securities that are classified as available-for-sale and held-to-maturity, in accordance with FASB ASC Topic 320, Investments – Debt and Equity Securities. The Company also holds certain investments in commercial paper that it considers to be held to maturity, based on their maturity dates. Securities available for sale include corporate and governmental obligations with various contractual maturity dates some of which are greater than one year. The Company considers the securities to be liquid and convertible to cash within 30 days. The Company has the ability and intent to liquidate any security that the Company holds to fund operations over the next twelve months if necessary and as such has classified these securities as short-term. Governmental obligations include U.S. Government, State, Municipal and Federal Agency securities. The Company has an overnight sweep investment arrangement with its bank for certain accounts to allow the Company to enter into diversified overnight investments via a money market mutual fund which generally provides a higher investment yield than a regular operating account.

Gross unrealized gains and losses for the three and nine months ended April 30, 2012 and 2011 were not significant. Unrealized gains and losses are reflected as a separate component of comprehensive income (loss) and are included in Stockholders’ Equity. Realized gains, losses and interest are included in investment income in the Statements of Operations. The Company analyzes its securities portfolio for impairment on a quarterly basis or upon occurrence of a significant change in circumstances. There were no other-than-temporary impairment losses recorded in the three and nine months ended April 30, 2012 or 2011.

9

Table of Contents

Inventories

Inventories are stated at the lower of cost or market, determined on the first-in, first-out (“FIFO”) method, and include materials, labor and manufacturing overhead. The components of inventories are as follows:

| April 30, 2012 |

July 31, 2011 |

|||||||

| (in thousands) | ||||||||

| Purchased components and parts |

$ | 13,641 | $ | 11,313 | ||||

| Units-in-progress |

4,619 | 2,080 | ||||||

| Finished units |

10,331 | 7,752 | ||||||

|

|

|

|

|

|||||

| Total inventories |

$ | 28,591 | $ | 21,145 | ||||

|

|

|

|

|

|||||

The Company establishes inventory reserves when conditions exist that indicate inventory may be in excess of anticipated demand or is obsolete based upon assumptions about future demand for the Company’s products or market conditions. The Company regularly evaluates the ability to realize the value of inventory based on a combination of factors including the following: forecasted sales or usage, estimated product end of life dates, estimated current and future market value and new product introductions.

Purchasing and usage alternatives are also explored to mitigate inventory exposure. When recorded, reserves are intended to reduce the carrying value of inventory to its net realizable value. As of April 30, 2012 and July 31, 2011, inventory is stated net of inventory reserves of $41.8 million and $43.0 million, respectively. If actual demand for products deteriorates or market conditions are less favorable than projected, additional inventory reserves may be required. Such reserves are not reversed until the related inventory is sold or otherwise disposed of.

The Company had sales of $0.7 million and $5.9 million of previously reserved inventory for the three months and nine months ended April 30, 2012, respectively, which represents the gross cash received from the customer. The Company released reserves of $0.4 million and $1.5 million for the three months and nine months ended April 30, 2012, respectively, related to these sales.

The Company had sales of $8.3 million and $13.2 million of previously reserved inventory for the three months and nine months ended April 30, 2011, respectively, which represents the gross cash received from the customer. The Company released reserves of $2.0 million and $3.4 million for the three months and nine months ended April 30, 2011, respectively, related to these sales.

Property and Equipment

Property and equipment acquired is recorded at cost. The Company provides for depreciation and amortization on the straight-line method. Charges are made to operating expenses in amounts that are sufficient to amortize the cost of the assets over their estimated useful lives. Equipment spares used for service and internally manufactured test systems used for testing components and engineering projects are recorded at cost and depreciated over 3 to 7 years. Repair and maintenance costs that do not extend the lives of property and equipment are expensed as incurred. Property and equipment are summarized as follows:

| (in thousands) | (in years) | |||||||||

| April 30, 2012 |

July 31, 2011 |

Estimated Useful Lives | ||||||||

| Equipment spares |

$ | 55,270 | $ | 65,078 | 5 or 7 | |||||

| Machinery, equipment and internally manufactured systems |

44,323 | 41,476 | 3-7 | |||||||

| Office furniture and equipment |

4,028 | 4,892 | 3-7 | |||||||

| Purchased software |

2,861 | 2,805 | 3 | |||||||

| Land |

2,524 | 2,524 | — | |||||||

| Leasehold improvements |

6,197 | 6,134 | Term of lease or useful life, not to exceed 10 years | |||||||

|

|

|

|

|

|||||||

| Property and equipment, gross |

115,203 | 122,909 | ||||||||

| Less: accumulated depreciation and amortization |

(96,461 | ) | (102,082 | ) | ||||||

|

|

|

|

|

|||||||

| Property and equipment, net |

$ | 18,742 | $ | 20,827 | ||||||

|

|

|

|

|

|||||||

Impairment of Long-Lived Assets Other Than Goodwill

On an on-going basis, management reviews the value and period of amortization or depreciation of long-lived assets. In accordance with FASB ASC Topic 360, Property, Plant and Equipment, the Company reviews whether impairment losses exist on long-lived assets when indicators of impairment are present. During this review, the Company re-evaluates the significant assumptions used in determining the original cost of long-lived assets. Although the assumptions may vary, they generally include revenue growth, operating results, cash flows and other indicators of value. Management then determines whether there has been a permanent

10

Table of Contents

impairment of the value of long-lived assets based upon events or circumstances that have occurred since acquisition. The extent of the impairment amount recognized is based upon a determination of the impaired asset’s fair value. As of April 30, 2012 and July 31, 2011 there were no indicators that required the Company to conduct a recoverability test as of those dates.

Goodwill and Other Intangibles

In accordance with FASB ASC Topic 350, Intangibles – Goodwill and Other, (“ASC 350”), the Company is required to review goodwill by reporting unit for impairment at least annually or more often if there are indicators of impairment present. The Company has determined its entire business represents one reporting unit. Historically, the Company has performed its annual impairment analysis during the fourth quarter of each year. The provisions of ASC 350 require that a two-step impairment test be performed for goodwill. In the first step, the Company compares the implied fair value of each reporting unit to which goodwill has been allocated to its carrying value. If the implied fair value of the reporting unit exceeds the carrying value of the net assets assigned to that reporting unit, goodwill is considered not impaired and the Company is not required to perform further testing. If the carrying value of the net assets assigned to the reporting unit exceeds the implied fair value of the reporting unit, then the Company must perform the second step of the impairment test in order to determine the implied fair value of the reporting unit’s goodwill. If the carrying value of a reporting unit’s goodwill exceeds its implied fair value, then the Company would record an impairment loss equal to the difference. As of April 30, 2012 and July 31, 2011, the implied fair value of the goodwill of the Company’s reporting unit exceeded the Company’s carrying value of its net assets and therefore no impairment existed as of those dates.

The Company’s goodwill consists of the following:

| Goodwill |

April 30, 2012 |

July 31, 2011 |

||||||

| (in thousands) | ||||||||

| Merger with Credence Systems Corporation (August 29, 2008) |

$ | 28,662 | $ | 28,662 | ||||

| Acquisition with Step Tech Inc. (June 10, 2003) |

14,368 | 14,368 | ||||||

|

|

|

|

|

|||||

| Total goodwill |

$ | 43,030 | $ | 43,030 | ||||

|

|

|

|

|

|||||

There was no change in the goodwill balance for the three or nine months ended April 30, 2012 or 2011.

Intangible assets, all of which relate to the Credence merger, consist of the following:

| As of April 30, 2012 | ||||||||||||||||

| Description |

Estimated Useful Life |

Gross Carrying Amount |

Accumulated Amortization |

Net Amount | ||||||||||||

| (in years) | (in thousands) | (in thousands) | (in thousands) | |||||||||||||

| Trade names |

2.0 | $ | 300 | $ | 300 | $ | — | |||||||||

| Distributor relationships |

2.0 | 2,800 | 2,800 | — | ||||||||||||

| Key customer relationships |

3.0 | 8,500 | 8,500 | — | ||||||||||||

| Developed technology—ASL |

6.0 | 16,000 | 14,460 | 1,540 | ||||||||||||

| Developed technology—Diamond |

9.0 | 9,400 | 8,149 | 1,251 | ||||||||||||

| Maintenance agreements |

7.0 | 1,900 | 747 | 1,153 | ||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total intangible assets |

$ | 38,900 | $ | 34,956 | $ | 3,944 | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| As of July 31, 2011 | ||||||||||||||||

| Description |

Estimated Useful Life |

Gross Carrying Amount |

Accumulated Amortization |

Net Amount | ||||||||||||

| (in years) | (in thousands) | (in thousands) | (in thousands) | |||||||||||||

| Trade names |

2.0 | $ | 300 | $ | 300 | $ | — | |||||||||

| Distributor relationships |

2.0 | 2,800 | 2,800 | — | ||||||||||||

| Key customer relationships |

3.0 | 8,500 | 8,500 | — | ||||||||||||

| Developed technology—ASL |

6.0 | 16,000 | 12,945 | 3,055 | ||||||||||||

| Developed technology—Diamond |

9.0 | 9,400 | 7,495 | 1,905 | ||||||||||||

| Maintenance agreements |

7.0 | 1,900 | 543 | 1,357 | ||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total intangible assets |

$ | 38,900 | $ | 32,583 | $ | 6,317 | ||||||||||

|

|

|

|

|

|

|

|||||||||||

11

Table of Contents

Intangible assets are amortized based upon the pattern of estimated economic use over their estimated useful lives. The weighted average estimated remaining useful life over which these intangible assets will be amortized is 2.4 years.

The Company expects amortization for these intangible assets to be:

| For the fiscal year ending July 31, |

Amount | |||

| (in thousands) | ||||

| Remainder of 2012 |

$ | 791 | ||

| 2013 |

1,583 | |||

| 2014 |

769 | |||

| 2015 |

396 | |||

| Thereafter |

405 | |||

|

|

|

|||

| Total |

$ | 3,944 | ||

|

|

|

|||

3. SEGMENT REPORTING

In accordance with the provisions of FASB ASC Topic 280, Segment Reporting, the Company operates as one reporting segment, that is, the design, manufacture and marketing of automated test equipment for the semiconductor industry that is used to test system-on-a-chip, digital, analog and mixed signal integrated circuits.

The Company’s net sales by geographic area for the three and nine months ended April 30, 2012 and 2011, along with its long-lived assets at April 30, 2012 and July 31, 2011, are summarized as follows:

| Three Months Ended April 30, |

Nine Months Ended April 30, |

|||||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| (in thousands) | ||||||||||||||||

| Net sales: |

||||||||||||||||

| United States |

$ | 7,309 | $ | 7,439 | $ | 23,828 | $ | 27,913 | ||||||||

| Philippines |

6,149 | 11,309 | 14,805 | 50,708 | ||||||||||||

| Taiwan |

6,532 | 13,396 | 14,298 | 42,768 | ||||||||||||

| Malaysia |

4,108 | 2,485 | 6,914 | 8,720 | ||||||||||||

| China/Hong Kong |

1,829 | 6,018 | 6,139 | 10,863 | ||||||||||||

| Singapore |

786 | 8,389 | 4,335 | 18,321 | ||||||||||||

| All other countries (none greater than 10% of total) |

4,124 | 9,629 | 18,352 | 27,567 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total Net Sales |

$ | 30,837 | $ | 58,665 | $ | 88,671 | $ | 186,860 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Long-lived assets consist of property and equipment:

| April 30, 2012 |

July 31, 2011 |

|||||||

| (in thousands) | ||||||||

| Long-lived assets: |

||||||||

| United States |

$ | 17,202 | $ | 18,820 | ||||

| Singapore |

357 | 559 | ||||||

| Philippines |

193 | 371 | ||||||

| All other countries |

990 | 1,077 | ||||||

|

|

|

|

|

|||||

| Total long-lived assets |

$ | 18,742 | $ | 20,827 | ||||

|

|

|

|

|

|||||

Transfer prices on products sold to foreign subsidiaries are intended to produce profit margins that correspond to the subsidiary’s sales and support efforts.

12

Table of Contents

4. RESTRUCTURING

In the year ended July 31, 2009, the Company vacated certain facilities in an effort to consolidate operations and align the Company’s capacity after the merger with Credence. As of April 30, 2012 and 2011, the accrual for the previously restructured facility leases was $3.7 million and $5.1 million, respectively. This includes $2.7 million and $3.7 million, respectively, of long-term payments to be made for the remainder of the respective lease terms, the longest of which is through 2017. This liability is included in other long term liabilities on the Company’s consolidated balance sheets. The remainder of the accrual of $1.0 million and $1.4 million, respectively, is included in other accrued expenses on the Company’s consolidated balance sheets as of April 30, 2012 and July 31, 2011, respectively.

During the nine months ending April 30, 2012, the Company reduced headcount in its global field service and applications engineering groups. The Company also exercised an early termination clause in one of its North America facility leases and vacated the facility. Consequently the Company recorded a liability for severance costs and other post-employment benefits for headcount reductions, as well as for its remaining obligation under the lease, including a termination fee for triggering the early termination clause. The total restructuring expense recorded related to these actions was approximately $0.9 million.

The restructuring accrual as of April 30, 2012 for severance costs includes approximately $0.1 million of stock-based compensation associated with outstanding equity awards that will vest in accordance with the recipients severance agreements. This liability will be marked to market each reporting period in accordance with the provisions of ASC 718 until the vesting date, which is within 12 months.

During the nine months ending April 30, 2011, the Company recorded a net restructuring expense of $0.4 million as a result of modifying its sublease assumptions and adjusting the liability for common area maintenance charges associated with the facilities vacated in 2009, offset by a reduction to accrued severance costs based on a change in estimate.

The net cash paid for restructuring expense during the nine months ended April 30, 2012 and 2011 represents cash severance costs, lease payments under the leases for the facilities vacated in 2009 and with respect to the nine months ended April 30, 2012 only, termination of leases in 2012, offset in each period by income from subleases.

The following table sets forth the Company’s restructuring accrual activity for the nine months ended April 30, 2012 and April 30, 2011 (in thousands):

| Restructuring Activity |

Severance Costs |

Facility Leases |

Total | |||||||||

| Balance July 31, 2011 |

$ | 6 | $ | 4,761 | $ | 4,767 | ||||||

| Addition to expense |

836 | 90 | 926 | |||||||||

| Accretion |

— | 135 | 135 | |||||||||

| Non-cash RSU Vesting (offset to additional paid-in capital) |

(15 | ) | — | (15 | ) | |||||||

| Cash paid |

(150 | ) | (1,145 | ) | (1,295 | ) | ||||||

|

|

|

|

|

|

|

|||||||

| Balance April 30, 2012 |

$ | 677 | $ | 3,841 | $ | 4,518 | ||||||

|

|

|

|

|

|

|

|||||||

| Included in the Company’s Consolidated Balance Sheet: |

||||||||||||

| Accrued expenses |

$ | 677 | $ | 1,107 | $ | 1,784 | ||||||

| Other long-term liabilities |

— | $ | 2,734 | $ | 2,734 | |||||||

| Severance Costs |

Facility Leases |

Total | ||||||||||

| Balance July 31, 2010 |

$ | 84 | $ | 5,810 | $ | 5,894 | ||||||

| Addition to expense |

(24 | ) | 387 | 363 | ||||||||

| Accretion |

— | 100 | 100 | |||||||||

| Cash paid |

(16 | ) | (1,188 | ) | (1,204 | ) | ||||||

|

|

|

|

|

|

|

|||||||

| Balance April 30, 2011 |

$ | 44 | $ | 5,109 | $ | 5,153 | ||||||

|

|

|

|

|

|

|

|||||||

| Included in the Company’s Consolidated Balance Sheet: |

||||||||||||

| Accrued expenses |

$ | 44 | $ | 1,444 | $ | 1,488 | ||||||

| Other long-term liabilities |

$ | — | $ | 3,665 | $ | 3,665 | ||||||

5. COMMITMENTS AND CONTINGENCIES

The Company is subject to various legal proceedings, claims and litigation which arise in the ordinary course of operations. In the opinion of management, the amount of liability, if any, with respect to these actions would not materially affect the Company’s financial position, results of operations or cash flows.

In the ordinary course of business, the Company agrees from time to time to indemnify certain customers against certain third party claims for property damage, bodily injury, personal injury or intellectual property infringement arising from the operation or use of the Company’s products. Also, from time to time in agreements with suppliers, licensors and other business partners, the Company agrees to indemnify these partners against certain liabilities arising out of the sale or use of the Company’s products. The maximum potential amount of future payments the Company could be required to make under these indemnification obligations in the aggregate is theoretically unlimited; however, the Company has general and umbrella insurance policies that enable it to recover a portion of any amounts paid and many of its agreements contain a limit on the maximum amount, as well as limits on the types of damages recoverable. Based on the Company’s experience with such indemnification claims, it believes the estimated fair value of these obligations is minimal. Accordingly, the Company has no liabilities recorded for these agreements as of April 30, 2012 or July 31, 2011.

13

Table of Contents

Subject to certain limitations, the Company indemnifies its current and former officers and directors in certain circumstances in connection with their services as directors and officers of the Company. Although the maximum potential amount of future payments the Company could be required to make under these agreements is theoretically unlimited, as there were no known or pending claims, the Company has not accrued a liability for these agreements as of April 30, 2012 or July 31, 2011.

The Company had approximately $17.8 million and $9.6 million, respectively, of non-cancelable inventory commitments with outsourced suppliers as of April 30, 2012 and July 31, 2011. The Company expects to consume the inventory through normal operating activity.

The Company has operating lease commitments for certain facilities and equipment. Minimum lease payments under non-cancelable leases at April 30, 2012, are as follows:

Lease Commitments:

| For the fiscal year ending July 31, |

Amount | |||

| (in thousands) | ||||

| Remainder of 2012 |

$ | 1,428 | ||

| 2013 |

5,335 | |||

| 2014 |

5,041 | |||

| 2015 |

4,449 | |||

| 2016 |

4,018 | |||

| Thereafter |

6,707 | |||

|

|

|

|||

| Total minimum lease payments |

$ | 26,978 | ||

|

|

|

|||

6. ACCRUED EXPENSES

Other accrued expenses consisted of the following at April 30, 2012 and July 31, 2011:

| (in thousands) | ||||||||

| April 30, 2012 |

July 31, 2011 |

|||||||

| Accrued compensation |

$ | 7,101 | $ | 10,340 | ||||

| Warranty reserve |

1,573 | 2,281 | ||||||

| Accrued restructuring |

1,784 | 1,350 | ||||||

| Accrued taxes |

1,028 | 1,274 | ||||||

| Accrued professional fees |

779 | 964 | ||||||

| Accrued vendor liability |

331 | 2,442 | ||||||

| Other accrued expenses |

5,601 | 6,026 | ||||||

|

|

|

|

|

|||||

| Total accrued expenses |

$ | 18,197 | $ | 24,677 | ||||

|

|

|

|

|

|||||

7. FAIR VALUE MEASUREMENTS

The Company determines its fair value measurements for assets and liabilities based upon the provisions of FASB ASC Topic 820, Fair Value Measurements and Disclosures.

The Company holds short-term money market investments and certain other financial instruments which are carried at fair value. The Company determines fair value based upon quoted prices, when available, or through the use of alternative approaches when market quotes are not readily accessible or available.

Valuation techniques for fair value are based upon observable and unobservable inputs. Observable inputs reflect market data obtained from independent sources, while unobservable inputs reflect the Company’s best estimate, considering all relevant information. These valuation techniques involve some level of management estimation and judgment. The valuation process to determine fair value also includes making appropriate adjustments to the valuation model outputs to consider risk factors.

The fair value hierarchy of the Company’s inputs used in the determination of fair value for assets and liabilities during the current period consists of three levels. Level 1 inputs are composed of unadjusted, quoted prices in active markets for identical assets or liabilities at the measurement date. Level 2 inputs include quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; inputs other than quoted prices that are observable for the asset or liability; and inputs that are derived principally from or corroborated by observable market data by correlation or other means.

14

Table of Contents

Level 3 inputs incorporate the Company’s own best estimate of what market participants would use in pricing the asset or liability at the measurement date where consideration is given to the risk inherent in the valuation technique and the risk inherent in the inputs to the model. If inputs used to measure an asset or liability fall within different levels of the hierarchy, the categorization is based on the lowest level input that is significant to the fair value measurement of the asset or liability. The Company’s assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment, and considers factors specific to the asset or liability.

The following table presents financial assets and liabilities measured at fair value and their related valuation inputs as of April 30, 2012 and as of July 31, 2011:

| Fair Value Measurements at Reporting Date Using

(in thousands) |

||||||||||||||||

| April 30, 2012 |

Total Fair Value of Asset or Liability |

Quoted Prices in Active Markets for Identical Assets (Level 1) |

Significant Other Observable Inputs (Level 2) |

Significant Unobservable Inputs (Level 3) |

||||||||||||

| Cash and cash equivalents (1) |

$ | 35,339 | $ | 34,974 | $ | 365 | $ | — | ||||||||

| Marketable securities (2) |

98,727 | 2,472 | 96,255 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total Assets |

$ | 134,066 | $ | 37,446 | $ | 96,620 | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| July 31, 2011 |

Total Fair Value of Asset or Liability |

Quoted Prices in Active Markets for Identical Assets (Level 1) |

Significant Other Observable Inputs (Level 2) |

Significant Unobservable Inputs (Level 3) |

||||||||||||

| Cash and cash equivalents (1) |

$ | 123,198 | $ | 122,698 | $ | 500 | $ | — | ||||||||

| Marketable securities (2) |

35,419 | 10,031 | 25,388 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total Assets |

$ | 158,617 | $ | 132,729 | $ | 25,888 | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Accrued expenses (Foreign exchange contract (3) |

$ | 187 | $ | — | $ | 187 | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total Liabilities |

$ | 187 | $ | — | $ | 187 | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | Cash and cash equivalents as of April 30, 2012 and July 31, 2011 includes cash held in operating accounts of approximately $35.3 million and $10.9 million, respectively, that are not subject to fair value measurements. For purposes of this disclosure they are included as having Level 1 inputs. |

| (2) | Marketable securities as of April 30, 2012 and July 31, 2011 exclude approximately $2.8 million and $4.0 million, respectively, of commercial paper which is held to maturity and not subject to fair value measurements. |

| (3) | Accrued expenses as of July 31, 2011 include a derivative not designated as a hedging arrangement related to a foreign exchange contract of approximately $0.2 million. |

The carrying value of accounts receivable, prepaid expenses and accounts payable approximates fair value due to their short-term nature.

There were no assets or liabilities measured at fair value on a non-recurring basis requiring valuation disclosures as of April 30, 2012 or as of July 31, 2011.

8. STOCKHOLDERS’ EQUITY

Stock Repurchases

On September 15, 2011, the Company announced that its Board of Directors had authorized a stock repurchase program for up to $25 million of shares of the Company’s common stock. Under this program, the Company is authorized to repurchase shares of its common stock from time to time in open market transactions. The Company will determine the timing and amount of the transactions based on its evaluation of market conditions and other factors. The repurchase program may be suspended or discontinued at any time and has no expiration date. Cumulatively, as of April 30, 2012, the Company has repurchased 1,121,600 shares of common stock for a total purchase price of $6.1 million.

15

Table of Contents

2010 Plan

On November 5, 2010, the Company’s Board of Directors adopted, subject to shareholder approval, the Company’s 2010 Stock Plan, and subsequently amended it on November 26, 2010 (“2010 Plan”). Under the terms of the 2010 Plan, the Company may issue up to 4,800,000 shares of the Company’s common stock (subject to adjustment in the event of stock splits and other similar events) pursuant to awards granted under the 2010 Plan. In addition, any unissued shares of the Company’s common stock, and any unused shares of the Company’s common stock as a result of termination, surrender, cancellation or forfeiture of outstanding awards under the Credence 2005 Plan, as amended and restated, and the LTX Corporation 2004 Plan (together the “Prior Plans”) will be available for grant under the 2010 Plan. The 2010 Plan was approved by the Company’s shareholders at the annual meeting on December 7, 2010. All future grants of equity awards will be made out of the 2010 Plan, and no additional grants will be made under the Prior Plans.

Reverse Stock Split

On September 15, 2010, the Company’s Board of Directors approved a one-for-three reverse stock split of the Company’s common stock, pursuant to a previously obtained stockholder authorization. The Company filed Restated Articles of Organization on September 30, 2010 in order to effect the reverse stock split, and on a post-split basis, to set the number of authorized shares of its common stock at 150,000,000. The Restated Articles of Organization were approved by the Company’s stockholders at the Special Meeting of Stockholders held on July 8, 2010.

Upon the effective time of the Restated Articles of Organization, each outstanding share of the Company’s common stock was automatically converted into one-third of a share of common stock. No fractional shares were issued in connection with the reverse stock split. Holders of common stock who would otherwise have received a fractional share of common stock pursuant to the reverse stock split received cash in lieu of the fractional share. The reverse stock split became effective for trading purposes at the opening of the Nasdaq Global Market on October 1, 2010. The effect of the reverse stock split has been retroactively applied to all periods presented.

9. RECENT ACCOUNTING PRONOUNCEMENTS

In May 2011, the FASB issued ASU No. 2011-04, Fair Value Measurement. This ASU clarifies the concepts related to highest and best use and valuation premise, blockage factors and other premiums and discounts, the fair value measurement of financial instruments held in a portfolio and of those instruments classified as a component of shareholders’ equity. The guidance includes enhanced disclosure requirements about recurring Level 3 fair value measurements, the use of nonfinancial assets, and the level in the fair value hierarchy of assets and liabilities not recorded at fair value. The provisions of this ASU are effective prospectively for interim and annual periods beginning on or after December 15, 2011. Early application is prohibited. This ASU requires changes in presentation only and adoption of this update did not have material impact on the Company’s consolidated financial statements.

In September 2011, the FASB issued ASU No. 2011-08, Testing Goodwill for Impairment. This revised standard is intended to reduce the cost and complexity of the annual goodwill impairment test by providing entities an option to perform a “qualitative” assessment to determine whether further impairment testing is necessary. The revised standard is effective for annual and interim goodwill impairment tests performed for fiscal years beginning after December 15, 2011. The Company is currently evaluating the impact of adoption of this revised standard on its financial statements.

Item 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion should be read together with the Consolidated Financial Statements and Notes thereto appearing in Part I, Item 1 in this quarterly report on Form 10-Q. Certain statements in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” are forward-looking statements that involve risks and uncertainties. Words such as may, will, could, should, would, anticipates, expects, intends, plans, predicts, projects, believes, seeks, estimates and similar expressions identify such forward-looking statements. The forward-looking statements contained herein are based on current expectations and entail various risks and uncertainties that could cause actual results to differ materially and adversely from those expressed in such forward-looking statements. Factors that might cause such a difference include, among other things, those set forth under “Risk Factors” in the Company’s Annual Report filed on Form 10-K with the SEC on October 14, 2011 and those appearing elsewhere in this quarterly report on Form 10-Q. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof and reflect management’s estimates and analysis only as of the date hereof. We assume no obligations to update these forward-looking statements to reflect actual results or changes in factors or assumptions affecting forward-looking statements.

16

Table of Contents

Overview

We provide market-focused, cost-optimized automated test equipment (ATE) solutions. We design, manufacture, market and service ATE solutions that address the broad, divergent test requirements of the wireless, computing, automotive and digital consumer market segments. Semiconductor designers and manufacturers worldwide use our equipment to test their devices during the manufacturing process. After testing, these devices are then incorporated in a wide range of products, including computers, mobile internet equipment such as wireless access points and interfaces, broadband access products such as cable modems and set top boxes, personal communication products such as mobile phones and personal digital music players, consumer products such as televisions, videogame systems, digital cameras and automobile electronics, and power management in portable and automotive electronics. We also sell hardware and software support and maintenance services for our test systems.

We focus our marketing and sales efforts on integrated device manufacturers (IDMs), outsource assembly and test providers, (OSATs), which perform manufacturing services for the semiconductor industry, and fabless companies, which design integrated circuits but have no manufacturing capability. We offer our customers a comprehensive portfolio of test systems and provide a global network of strategically deployed applications and support resources.

Industry Conditions and Outlook

We sell capital equipment and services to companies that design, manufacture, assemble or test semiconductor devices. The semiconductor industry is highly cyclical, causing in turn a cyclical impact on our financial results. As a capital equipment provider, our revenue is driven by the capital expenditure budgets and spending patterns of our customers, who often delay or accelerate purchases in reaction to variations in their business. The level of capital expenditures by these semiconductor companies depends on the current and anticipated market demand for semiconductor devices and the products that incorporate them. Therefore, demand for our semiconductor test equipment is dependent on growth in the semiconductor industry. In particular, three primary characteristics of the semiconductor industry drive the demand for semiconductor test equipment:

| • | increases in unit production of semiconductor devices; |

| • | increases in the complexity of semiconductor devices used in electronic products; and |

| • | the emergence of next generation device technologies. |

On March 20, 2012 we launched the Diamondx test product, that we believe will enable us to expand our addressable market into the digitally-centric application specific standard product (or ASSP) device market. We believe the new Diamondx test product for digitally-centric ASSP devices, which are primarily used in mobility applications, will be a new source of revenue growth for us as we enter the next semiconductor cycle.

17

Table of Contents

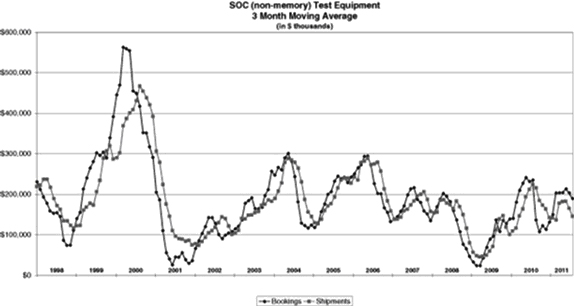

The following graph shows the cyclicality in semiconductor test equipment orders and shipments from fiscal 1997 through fiscal 2011 (using the three month moving average), as calculated by SEMI, an industry trade organization:

Consistent with our business strategy, we invest significant amounts in engineering and product development to design and enhance our tester platforms throughout the semiconductor business cycle. During periods of industry weakness, we implement cost reduction measures, such as the strict oversight and reduction in discretionary travel and other variable overhead expenses. We believe that these reductions in operating costs preserve our ability to fund critical engineering and product development efforts and continue to provide our customers with the levels of responsiveness and service they require. We believe that our competitive advantage in the semiconductor test industry is primarily driven by the ability of our combined tester platforms to meet or exceed the cost and technical specifications required for the testing of advanced semiconductor devices. Our current investment in engineering and product development is focused on enhancements and additions to our product offerings with new options and instruments designed for specific market segments. We believe this will continue to differentiate our tester platforms from the product offerings of our competitors.

We have transitioned the manufacture of certain components and subassemblies to contract manufacturers, thereby reducing our fixed manufacturing costs associated with direct labor and overhead. We believe that transforming product manufacturing costs into variable costs allows us to improve our performance in the highly cyclical semiconductor equipment industry.

We are exposed to the risks associated with the volatility of the U.S. and global economies. The lack of visibility regarding whether or when there will be sustained growth periods for the sale of electronic goods and information technology equipment, and uncertainty regarding the amount of sales, underscores the need for caution in predicting growth in the semiconductor test equipment industry in general and in our revenues and profits specifically. Slow or negative growth in the U.S. and global economies may materially and adversely affect our business, financial condition and results of operations. Our results of operations would also be adversely affected if we were to experience lower than anticipated order levels, cancellations of orders in backlog, extended customer delivery requirements or pricing pressure as a result of a slowdown. At lower levels of revenue, there is a higher likelihood that these types of changes in our customers’ requirements would adversely affect our results of operations because in any particular quarter a limited number of transactions accounts for an even greater portion of sales for the quarter.

Critical Accounting Policies and the Use of Estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amount of assets, liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities. We base these estimates and assumptions on historical experience and evaluate them on an on-going basis to ensure they remain reasonable under current conditions. Actual results could differ from those estimates. We believe that our most critical accounting policies upon which our financial reporting depends and which involve the most complex and subjective decisions or assessments are as follows: revenue recognition, inventory reserves, income taxes, warranty, goodwill and other intangibles, impairment of long-lived assets and allowances for doubtful accounts.

18

Table of Contents

A summary of those accounting policies and estimates that we believe to be most critical to fully understand and evaluate our financial results is set forth below. The summary should be read in conjunction with our Consolidated Financial Statements and Notes and related disclosures in Part I, Item 1 in this quarterly report on Form 10-Q.

Revenue Recognition

Our revenue recognition policy is described in Note 2, Summary of Significant Accounting Policies, contained in the Notes to Consolidated Financial Statements included in Part 1, Item 1 in this quarterly report on Form 10-Q. We recognize revenue when persuasive evidence of an arrangement exists, delivery or customer acceptance (if required) has occurred or services have been rendered, the price is fixed or determinable and collectability is reasonably assured.

Inventory

We sell capital equipment to companies that design, manufacture, assemble and test semiconductor devices. We are exposed to a number of economic and industry factors that could result in portions of our inventory becoming either obsolete or in excess of anticipated usage. These factors include, but are not limited to, changes in our customers’ capital expenditures, technological changes in our markets, our ability to meet changing customer requirements, competitive pressures in products and prices, and the availability of key components from our suppliers. Our policy is to establish inventory reserves when conditions exist that suggest our inventory may be in excess of anticipated demand or is obsolete based upon our assumptions about future demand for our products or market conditions. We regularly evaluate the ability to realize the value of our inventory based on a combination of factors including the following: historical usage rates, forecasted sales or usage, estimated product end of life dates, estimated current and future market values and new product introductions. Purchasing and alternative usage options are also explored to mitigate inventory exposure. When recorded, our reserves are intended to reduce the carrying value of our inventory to its net realizable value. Such reserves are not reversed until the related inventory is sold or otherwise disposed.

For the three months and nine months ended April 30, 2012, we recorded sales of $0.7 million and $5.9 million, respectively, of previously reserved inventory, which represents gross cash received from the customer. We released reserves of $0.4 million and $1.5 million for the three months and nine months ended April 30, 2012, respectively, related to these sales.

For the three months and nine months ended April 30, 2011, we recorded sales of $8.3 million and $13.2 million, respectively, of previously reserved inventory, which represents gross cash received from the customer. We released reserves of $2.0 million and $3.4 million for the three months and nine months ended April 30, 2012, respectively, related to these sales.

As of April 30, 2012 and July 31, 2011, our inventory of $28.6 million and $21.1 million, respectively, is stated net of inventory reserves of $41.8 million and $43.0 million, respectively, and primarily consists of Sapphire, X-Series, ASL, Diamond, and Diamondx test products.

Income Taxes

In accordance with Financial Accounting Standards Board Accounting Standards Codification (“FASB ASC”) Topic 740, Income Taxes (“ASC 740”), we recognize deferred income taxes based on the expected future tax consequences of differences between the financial statement basis and the tax basis of assets and liabilities calculated using enacted tax rates for the year in which the differences are expected to be reflected in the tax return. We established valuation allowances when necessary to reduce deferred taxes to the amount we expect to be realized.

We have deferred tax assets resulting from tax credit carryforwards, net operating losses and other deductible temporary differences, which will reduce taxable income in future periods. ASC 740 requires that a valuation allowance be established when it is “more likely than not” that all or a portion of deferred tax assets will not be realized. A review of all available positive and negative evidence needs to be considered, including a company’s performance, the market environment in which it operates, the length of carryback and carryforward periods, existing sales backlog and future sales projections. Where there are cumulative losses in recent years, ASC 740 creates a strong presumption that a valuation allowance is needed. This presumption can be overcome in very limited circumstances. As a result of our cumulative loss position in recent years and the increased uncertainty relative to the timing of profitability in future periods, we continue to maintain a valuation allowance for our entire net deferred tax assets. The valuation allowance totaled $194.5 million and $223.4 million as of July 31, 2011 and July 31, 2010, respectively, a decrease of $28.9 million. The decrease in our valuation allowance compared to the prior year was primarily due to (i) a decrease in deferred tax assets associated with state net operating loss and credit carryforwards that are subject to annual limitations as defined in sections 382 and 383 of the Internal Revenue Code (IRC) and (ii) a decrease in deferred tax assets associated with an accounting method change for spares.

We expect to record a full valuation allowance on future tax benefits until we can sustain an appropriate level of profitability. Until such time, we would not expect to recognize any significant tax benefits in our future results of operations. We will continue to monitor the recoverability of our deferred tax assets on a periodic basis. As a result of the merger with Credence Systems Corporation and IRC Section 382 guidance, the future utilization of our net operating loss deductions will be significantly limited.

19

Table of Contents

Valuation of Goodwill

In accordance with FASB ASC Topic 350, Intangibles—Goodwill and Other (“ASC 350”), we are required to review goodwill by reporting unit for impairment at least annually or more often if there are indicators of impairment present. We have determined our entire business represents one reporting unit. Historically, we have performed our annual impairment analysis during the fourth quarter of each year. The provisions of ASC 350 require that a two-step impairment test be performed for goodwill. In the first step, we compare the fair value of each reporting unit to which goodwill has been allocated to its carrying value. If the fair value of the reporting unit exceeds the carrying value of the net assets assigned to that reporting unit, goodwill is considered not impaired and we are not required to perform further testing. If the carrying value of the net assets assigned to the reporting unit exceeds the fair value of the reporting unit, then we must perform the second step of the impairment test in order to determine the implied fair value of the reporting unit’s goodwill. If the carrying value of a reporting unit’s goodwill exceeds its implied fair value, then we would record an impairment loss equal to the difference. As of April 30, 2012 and July 31, 2011, the fair value of our reporting unit exceeded the carrying value of the reporting unit’s net assets and therefore no impairment existed as of those dates.

Valuation of Identifiable Intangible Assets