Attached files

| file | filename |

|---|---|

| 8-K - 8-K - M&T BANK CORP | d360248d8k.htm |

Sanford C. Bernstein

Strategic Decisions Conference 2012

May 31, 2012

Exhibit 99 |

2

Disclaimer

This presentation contains forward looking statements within the meaning of the Private

Securities Litigation Reform Act giving the Company's expectations or predictions of

future financial or business performance or conditions. Forward-looking

statements are typically identified by words such as "believe," "expect," "anticipate," "intend,"

"target," "estimate," "continue," "positions,"

"prospects" or "potential," by future conditional verbs such as "will,"

"would," "should," "could" or "may," or by variations of such

words or by similar expressions. These forward-looking statements are subject

to numerous assumptions, risks and uncertainties which change over time. Forward-looking

statements speak only as of the date they are made and we assume no duty to update

forward-looking statements.

In addition to factors previously disclosed in our SEC reports and those identified elsewhere

in this presentation, the following factors among others, could cause actual results to

differ materially from forward-looking statements or historical performance:

changes in asset quality and credit risk; the inability to sustain revenue and earnings growth;

changes in interest rates and capital markets; inflation; customer acceptance of M&T

products and services; customer borrowing, repayment, investment and deposit practices;

customer disintermediation; the introduction, withdrawal, success and timing of

business initiatives; competitive conditions; the inability to realize cost savings or

revenues or to implement integration plans and other consequences associated with mergers,

acquisitions and divestitures; economic conditions; and the impact, extent and timing

of technological changes, capital management activities, and other actions of the

Federal Reserve Board and legislative and regulatory actions and reforms, including

those associated with the Dodd-Frank Wall Street Reform and Consumer Protection Act.

Annualized, pro forma, projected and estimated numbers are used for illustrative purpose only,

are not forecasts and may not reflect actual results.

|

3

Top 20 US-based full-service commercial

bank holding company by assets and Top 15

by market cap

Founded in 1856

$79 billion total assets

761

domestic branches and more than 2,000

ATMs

15,479 employees located in New York,

Maryland, Pennsylvania, Washington, D.C.,

Virginia, West Virginia and Delaware

Over 2 million consumer/retail household

customers

208,000 commercial customers

M&T Bank Corporate Profile

As of 03/31/12 |

4

Most honored bank in 2011 Greenwich Excellence Awards for Small Business

Banking: 12 national awards and 2 regional awards

Highest number of awards among all 750 banks rated by business customers

Received the highest possible Community Reinvestment Act (CRA) rating on every

exam since 1982

M&T Charitable Foundation has contributed over $147 million to

not-for-profit organizations in its communities over the past 10

years Contributed $40 million to M&T Charitable Foundation in 2011

More than 3,000 M&T employees volunteer with

5,100 different not-for-profit organizations

Strong long-term returns for shareholders

Customers, Communities & Shareholders |

5

Strong Presence In Our Communities

#1 Small Business Administration

Lender in:

Baltimore

Binghamton

Buffalo

Philadelphia

Rochester

Syracuse

Washington, DC

Wilmington

Ranked 6

th

Nationally

Ranked 3

rd

in Eastern U.S.

#1 market share for lead bank

relationships

among middle market clients in:

(1)

Baltimore

Binghamton

Buffalo

Harrisburg

Northern Pennsylvania

Rochester

Syracuse

State of Maryland overall

State of Delaware overall

(1)

Independent 3

party market research

(2)

Reflects in-market deposits only

#1 or #2 deposit market share

in 8 of top 10 communities:

#2 in Baltimore

#1 in Binghamton

#1 in Buffalo

#2 in Harrisburg

#2 in Rochester

#1 in Syracuse

#1 Wilmington / State of Delaware

(2)

#1 in York

We lend in the markets where we live and work to people and enterprises whom we

know rd |

6

GAAP Earnings

2006

2007

2008

2009

2010

2011

1Q12

Net Income ($MM)

839

654

556

380

736

859

206

EPS ($ per share)

7.37

5.95

5.01

2.89

5.69

6.35

1.50

Net Operating Earnings

Net Operating Income ($MM)

881

704

599

455

755

884

218

Net Operating EPS ($ per share)

7.73

6.40

5.39

3.54

5.84

6.55

1.59

Earnings Summary

Net Operating Income and Net Operating EPS are non-GAAP financial measures (Excludes

merger-related gains and expenses and amortization expense associated with intangible

assets ). Refer to the Appendix for a reconciliation between these measures and GAAP |

7

Strong

credit

through

crisis

Focused

on returns

Consistent

capital

generation

(1)

The Efficiency Ratio and Pre-tax, Pre-provision Earnings are non-GAAP

financial measures. A reconciliation of GAAP to non-GAAP financial

measures is available in the appendix. The Efficiency Ratio reflects

non-interest expense (excluding amortization expense associated with

intangible assets and merger-related expenses) as a percentage of fully taxable

equivalent net interest income and non-interest revenues (excluding

gains or losses from securities transactions and merger-related gains).

(2)

Excludes merger-related gains and expenses and amortization expense associated

with intangible assets. Key Measures

2006

2007

2008

2009

2010

2011

1Q12

Net Interest Margin

3.70%

3.60%

3.38%

3.49%

3.84%

3.73%

3.69%

Efficiency

Ratio

-

Tangible

(1)

51.51%

52.77%

54.35%

56.50%

53.71%

60.43%

61.09%

Pre-tax, Pre-provision Earnings ($MM)

(1)

1,312

1,156

1,152

1,123

1,461

1,495

357

Allowance to Loans (As At)

1.51%

1.58%

1.61%

1.69%

1.74%

1.51%

1.49%

Net Charge-Offs to Loans

0.16%

0.26%

0.78%

1.01%

0.67%

0.47%

0.32%

Net Operating Return on

Tangible Assets

(2)

1.67%

1.27%

0.97%

0.71%

1.17%

1.26%

1.18%

Tangible Common Equity

(2)

29.55%

22.58%

19.63%

13.42%

18.95%

17.96%

16.79%

Common

Equity

to

Assets

-

Tangible

5.84%

5.01%

4.59%

5.13%

6.19%

6.40%

6.51%

Tier 1 Common Capital Ratio

6.42%

5.62%

6.08%

5.66%

6.51%

6.86%

7.04%

Tier 1 Capital Ratio

7.74%

6.84%

8.83%

8.59%

9.47%

9.68%

9.85%

Total Capital Ratio

11.78%

11.18%

12.83%

12.30%

13.08%

13.26%

13.43%

Leverage Ratio

7.20%

6.59%

8.35%

8.43%

9.33%

9.28%

9.53%

TBV per Share

28.57

27.98

25.94

28.27

33.26

37.79

38.89

Superior

pre-credit

earnings |

8

Efficiency Ratio

M&T’s Philosophy: Efficiently Delivering Banking Services

52.25%

60.43%

61.09%

56.28%

64.33%

65.02%

45%

50%

55%

60%

65%

70%

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

1Q12

MTB

Peer Median

Efficiency Ratio reflects non-interest expense (excluding amortization expense associated with

intangible assets, merger-related expenses and other non-recurring expenses) as a

percentage of fully taxable equivalent net interest income and non-interest revenues (excluding gains from securities

transactions and merger-related gains). The Efficiency Ratio is a non-GAAP

measure. See Appendix for a reconciliation to GAAP measures. 2011 & 1Q12 results influenced by Wilmington Trust

|

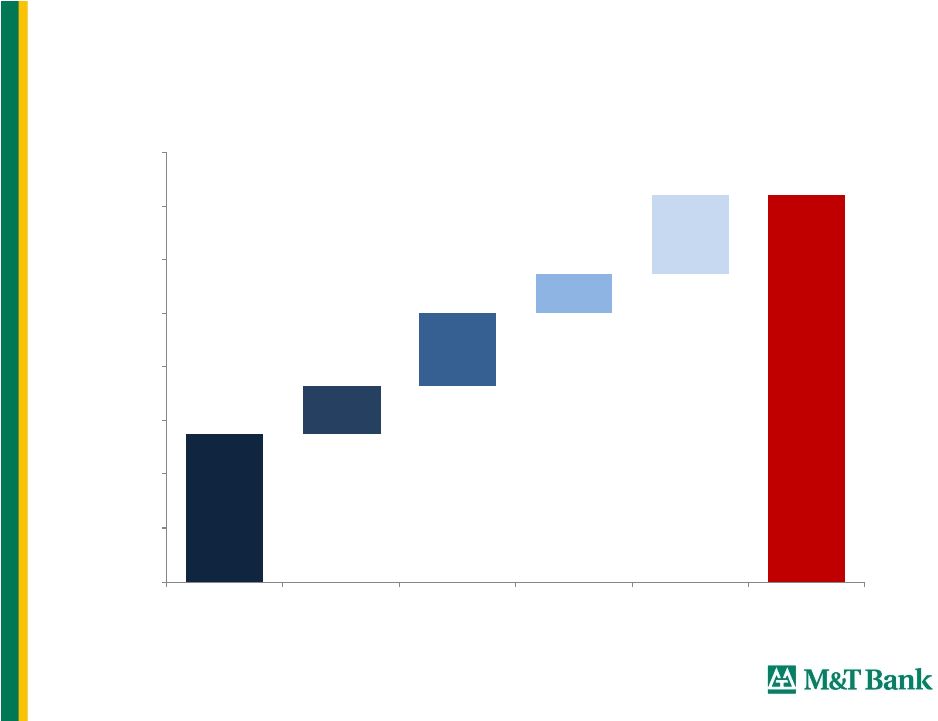

9

51.5%

60.4%

46.0%

48.0%

50.0%

52.0%

54.0%

56.0%

58.0%

60.0%

62.0%

MTB Efficiency

Ratio - 2006

Elevated Credit

Cycle Expenses

Higher FDIC

Expenses

Lower Revenue

from Reg E &

Durbin

Wilmington Trust

Impact

MTB Efficiency

Ratio - 2011

Drivers

of

Increase

in

Efficiency

Ratio

2006

-

2011

Estimated

Drivers

of

M&T’s

Increased

Efficiency

Ratio:

2006

-

2011

1.5 –

2.0%

2.5 –

3.0%

1.0 –

1.5%

2.5 –

3.0%

Efficiency

Ratio

reflects

non-interest

expense

(excluding

amortization

expense

associated

with

intangible

assets,

merger-related

expenses

and

other

non-recurring expenses) as a percentage of fully taxable equivalent net

interest income and non-interest revenues (excluding gains from securities

transactions and merger-related gains). |

10

M&T’s Community Lending –

Granular Loan Portfolio

Source: M&T Bank Corporation 2011 10-K

Key attributes: many small loans and moderate risk geography

Dollars in Billions

Total Commercial & Industrial

$4.1

$4.1

$6.3

$0.9

$0.2

$0.1

$15.7

Percent by Size

26%

26%

40%

6%

1%

1%

100%

Total Commercial Real Estate

$3.7

$7.8

$9.8

$1.7

$1.2

$0.2

$24.4

Percent by Size

15%

32%

40%

7%

5%

1%

100%

Total Commercial Loans

$7.8

$11.9

$16.1

$2.7

$1.4

$0.3

$40.1

Percent by Size

19%

30%

40%

7%

4%

1%

100%

Cumulative Percent by Size

19%

49%

89%

96%

99%

100%

Total

Commercial

Loans

-

$40.1

Billion

At December 31, 2011

Commercial Loan Granularity

$0-1

$1-5

$5-30

$30-50

$50-100

$100+

Million

Million

Million

Million

Million

Million

Totals |

11

Relative Loss Rate

(1)

BBT

CMA

COF

FITB

HBAN

KEY

MTB

PNC

RF

SNV

STI

ZION

BAC

C

JPM

USB

WFC

1991

39%

38%

NA

60%

40%

57%

61%

95%

22%

39%

61%

82%

159%

NA

230%

74%

60%

1992

40%

52%

NA

62%

59%

81%

68%

99%

28%

64%

55%

40%

94%

NA

154%

100%

62%

1993

28%

54%

NA

45%

43%

65%

76%

95%

32%

58%

60%

(36%)

60%

NA

187%

92%

84%

1994

35%

56%

NA

68%

56%

56%

55%

81%

54%

92%

57%

46%

69%

NA

265%

85%

113%

1995

71%

79%

NA

69%

74%

50%

70%

100%

52%

96%

64%

27%

82%

NA

119%

71%

137%

1996

96%

76%

NA

112%

91%

81%

101%

77%

51%

77%

77%

41%

93%

NA

101%

73%

142%

1997

118%

75%

NA

121%

100%

107%

111%

87%

81%

83%

61%

79%

102%

NA

67%

137%

172%

1998

76%

65%

NA

127%

90%

95%

95%

125%

100%

79%

91%

81%

164%

NA

96%

94%

338%

1999

75%

58%

NA

107%

75%

88%

85%

58%

113%

62%

79%

93%

101%

107%

119%

122%

127%

2000

60%

40%

NA

48%

70%

98%

43%

51%

90%

45%

35%

90%

100%

Bernstein bank analysis of Relative Loss Rates –

Focused on Long Term Underwriting Trends

Source: FDIC and Sanford Bernstein. (1) Expected loss

rates for each period are calculated by multiplying each bank's loan concentration by type by the actual industry-wide loss rate by

type. Dividing each bank's actual NCO rate by the expected loss rate yields the bank's relative

loss rate. JPM, PNC and WFC 2009 and 2010 results affected by recent acquisitions of WaMu,

National City, Wachovia, respectively. 148%

86%

122%

111%

2001

65%

46%

NA

70%

103%

112%

53%

298%

81%

38%

46%

43%

111%

114%

85%

128%

98%

2002

67%

96%

NA

44%

121%

118%

59%

56%

62%

38%

62%

53%

87%

116%

117%

90%

81%

2003

71%

102%

NA

74%

106%

106%

44%

76%

71%

62%

52%

69%

82%

113%

85%

100%

79%

2004

94%

139%

NA

91%

93%

149%

58%

71%

128%

92%

53%

74%

89%

125%

100%

91%

103%

2005

92%

121%

136%

112%

118%

135%

62%

20%

130%

151%

56%

56%

119%

137%

84%

86%

135%

2006

98%

61%

171%

123%

117%

78%

62%

103%

144%

147%

72%

80%

116%

155%

80%

76%

144%

2007

77%

75%

147%

98%

332%

70%

56%

67%

75%

124%

67%

47%

94%

141%

87%

67%

129%

2008

63%

90%

166%

228%

156%

130%

69%

60%

132%

121%

94%

81%

105%

144%

98%

70%

134%

2009

67%

82%

133%

116%

165%

140%

46%

65%

101%

188%

104%

118%

107%

155%

109%

69%

83%

2010

103%

70%

117%

128%

115%

138%

33%

85%

155%

219%

115%

117%

105%

145%

107%

79%

97%

2011

108%

76%

95%

104%

85%

95%

36%

79%

181%

183%

125%

97%

108%

157%

88%

83%

96%

2008Q1

58%

141%

182%

133%

59%

74%

49%

66%

67%

127%

100%

78%

93%

135%

107%

63%

128%

2008Q2

54%

98%

168%

127%

58%

240%

77%

56%

80%

82%

81%

64%

97%

135%

98%

65%

100%

2008Q3

63%

86%

162%

145%

62%

107%

64%

51%

130%

101%

83%

74%

97%

132%

103%

70%

112%

2008Q4

57%

60%

152%

355%

289%

89%

66%

59%

169%

129%

87%

84%

104%

152%

82%

65%

133%

2009Q1

77%

78%

142%

109%

185%

136%

48%

51%

92%

181%

96%

87%

108%

164%

94%

70%

72%

2009Q2

64%

89%

113%

104%

143%

115%

46%

71%

85%

170%

94%

133%

108%

154%

106%

63%

74%

2009Q3

60%

84%

115%

122%

148%

133%

43%

57%

114%

234%

118%

139%

116%

145%

114%

66%

85%

2009Q4

55%

72%

124%

106%

168%

151%

36%

68%

103%

147%

90%

92%

94%

153%

109%

63%

84%

2010Q1

68%

78%

106%

106%

111%

146%

32%

67%

137%

181%

114%

100%

102%

118%

108%

68%

94%

2010Q2

100%

69%

96%

91%

140%

140%

30%

91%

144%

267%

111%

118%

102%

125%

88%

77%

93%

2010Q3

143%

65%

105%

215%

97%

124%

35%

73%

178%

154%

114%

117%

93%

149%

93%

76%

95%

2010Q4

87%

59%

104%

83%

89%

102%

29%

99%

163%

255%

104%

126%

93%

150%

104%

73%

91%

2011Q1

90%

79%

98%

109%

109%

107%

38%

86%

154%

177%

120%

109%

98%

166%

88%

78%

94%

2011Q2

106%

83%

91%

98%

67%

85%

30%

74%

188%

202%

114%

93%

108%

153%

87%

82%

90%

2011Q3

108%

76%

79%

91%

71%

78%

29%

70%

193%

184%

120%

92%

116%

144%

75%

76%

90%

2011Q4

105%

58%

100%

86%

68%

77%

39%

64%

174%

158%

117%

87%

101%

151%

97%

75%

94%

Cycle Cumul.

80%

77%

117%

129%

136%

120%

42%

70%

133%

178%

103%

103%

101%

145%

98%

70%

95%

10-Yr Avg

83%

85%

131%

120%

137%

123%

47%

71%

126%

161%

95%

97%

102%

141%

99%

78%

101%

5-Yr Avg

84%

78%

126%

135%

146%

125%

45%

73%

135%

183%

107%

105%

105%

152%

101%

73%

101%

Median

71%

75%

136%

98%

93%

95%

61%

79%

81%

83%

62%

74%

101%

141%

100%

86%

111%

St Dev

25%

25%

27%

42%

61%

30%

21%

53%

44%

53%

23%

34%

25%

19%

51%

21%

58% |

12

Industry Aggregate NCOs and MTB Relative Loss Rate

Source: Regulatory Data per SNL. Relative Loss Rate per Bernstein Research,

with post-publication updates 61% 68% 76% 55% 70%

101% 111% 95% 85% 43% 53% 59% 44% 58% 62% 62% 56% 69% 44% 32% 34%

MTB Relative

Loss Rate

MTB

vs.

Industry

-

relative

loss

experience,

after

adjusting

MTB

loan

mix

to

industry

loan

mix

Industry Aggregate Net Charge-off Ratio

MTB Net Charge-off Ratio

Over the long-term, M&T recorded significantly less net charge-offs vs.

the Industry |

13

17.5%

16.0%

11.1%

10.3%

9.6%

9.3%

8.0%

7.8%

6.9%

6.0%

5.1%

3.1%

Peer Median

8.6%

Industry 9.6%

0%

5%

10%

15%

20%

Peer 1

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6

Peer 7

Peer 8

Peer 9

Peer 10

Peer 11

MTB

Total Loans

9.3%

9.1%

8.7%

8.5%

7.5%

7.1%

4.8%

4.1%

4.0%

3.8%

2.8%

0.6%

Peer Median

5.9%

Industry 3.6%

0%

3%

6%

9%

12%

Peer 1

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6

Peer 7

Peer 8

Peer 9

Peer 10

Peer 11

MTB

Comm. Real Estate

15.7%

11.0%

8.9%

8.5%

7.7%

6.7%

6.1%

5.0%

4.9%

4.5%

3.4%

2.9%

Peer Median

6.4%

Industry 6.0%

0%

5%

9%

14%

18%

Peer 1

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6

Peer 7

Peer 8

Peer 9

Peer 10

Peer 11

MTB

Commercial & Industrial

36.5%

33.2%

29.9%

26.4%

21.3%

20.8%

19.8%

16.6%

15.7%

15.3%

10.2%

8.0%

Peer Median

20.3%

Industry 17.5%

0%

10%

20%

30%

40%

Peer 1

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6

Peer 7

Peer 8

Peer 9

Peer 10

Peer 11

MTB

Construction

12.0%

11.2%

9.8%

8.7%

8.2%

5.5%

5.0%

4.7%

4.7%

4.4%

3.9%

2.7%

Peer Median

5.2%

Industry 6.8%

0%

3%

6%

9%

12%

15%

Peer 1

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6

Peer 7

Peer 8

MTB

Peer 9

Peer 10

Peer 11

Residential Mortgage

26.4%

14.3%

9.8%

9.1%

7.3%

5.3%

5.2%

5.2%

4.5%

3.3%

3.3%

1.8%

Peer Median

5.3%

Industry 10.2%

0%

6%

12%

18%

24%

30%

Peer 1

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6

Peer 7

Peer 8

Peer 9

Peer 10

Peer 11

MTB

HELOC

Strong Underwriting Across All Portfolios

*Represents cumulative net credit losses from 3Q07 through 4Q11 as a percentage of

average loans over that period. Note: Industry data reflects an aggregate of

commercial bank data per SNL. Loss

experience

through

the

financial

crisis

3Q07

–

4Q11* |

14

M&T Ranks Lowest for Volatility in FDIC’s Core Earnings Metric

(1)

Core Earnings Ratio per the FDIC. Volatility calculated as the standard deviation of change in

4qtr core earnings / average 5qtr end of period assets (Core earnings = net income, excl.

securities gain / loss and extraordinary items).

Source: Regulatory FR-Y9C reported data per SNL

Financial. Earnings

Earnings

Negative Core Earnings

Large Cap Banks

Volatility

(1)

Rank

Volatility

(1)

Rank

(# of Quarters)

MTB

2.8%

2

7.6%

1

0

USB

17.5%

13

9.1%

2

0

BBT

8.9%

11

14.0%

3

0

WFC

4.0%

6

17.6%

4

0

JPM

33.2%

14

41.3%

5

0

PNC

58.8%

15

44.2%

6

0

BAC

378.2%

16

78.0%

7

6

CMA

6.7%

9

135.6%

8

4

RF

2.5%

1

166.3%

9

11

COF

NA

NA

183.4%

10

3

SNV

3.8%

4

187.7%

11

14

STI

3.9%

5

200.4%

12

7

ZION

7.2%

10

212.9%

13

10

KEY

5.9%

8

345.2%

14

9

C

4.6%

7

412.1%

15

8

FITB

3.2%

3

683.4%

16

5

HBAN

9.2%

12

2791.4%

17

7

Large Cap Median

6.3%

166.3%

5

10 Years

:

1991 -

2000

10 Years

:

2001 -

2011

M&T has been a uniquely strong and stable performer, through good times and

bad |

15

M&T’s strength during economic crises has provided

growth opportunities |

16

M&T’s long-term superior profitability demonstrated:

Operating returns on Avg. Tangible Common Equity

26.0%

13.4%

18.9%

18.0%

21.1%

-12.0%

5.5%

10.9%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

MTB

Peer Median

Operating Return on Avg. Tangible Common Equity = Operating Earnings divided by

Avg. Tangible Common Equity. Operating Earnings = Net Income Available

to Common less Nonrecurring Revenue & Expense (as reported by SNL for Peer banks) and

Amortization Expense.

Avg. Tang Common Equity = Avg. Common Equity less Avg. Intangible Assets.

|

17

Consistent Earnings & Dividends: 1983 –

1Q12

Note:

Data

prior

to

1998

does

not

include

provisions

of

SFAS

No.

123

and

No.

148

stock

option

expensing.

Net Operating Income and Net Operating EPS are non-GAAP financial measures.

Refer to the Appendix for a reconciliation between these measures and

GAAP M&T maintained its dividend and experienced no losses through the

recent crisis |

18

For FY2012, expect NIM lower than FY2011’s 3.73%

Expect continued pressure to core NIM

2Q12 inflows of trust deposits will also impact NIM but not NII

Credit trends continue moderate improvement

Expect some lumpiness in credit metrics

Expect normal decline from 1Q12 seasonally high compensation expense

Remaining Wilmington Trust systems integration targeted for end of 2Q 2012

Outlook Consistent with Remarks on April earnings call |

19

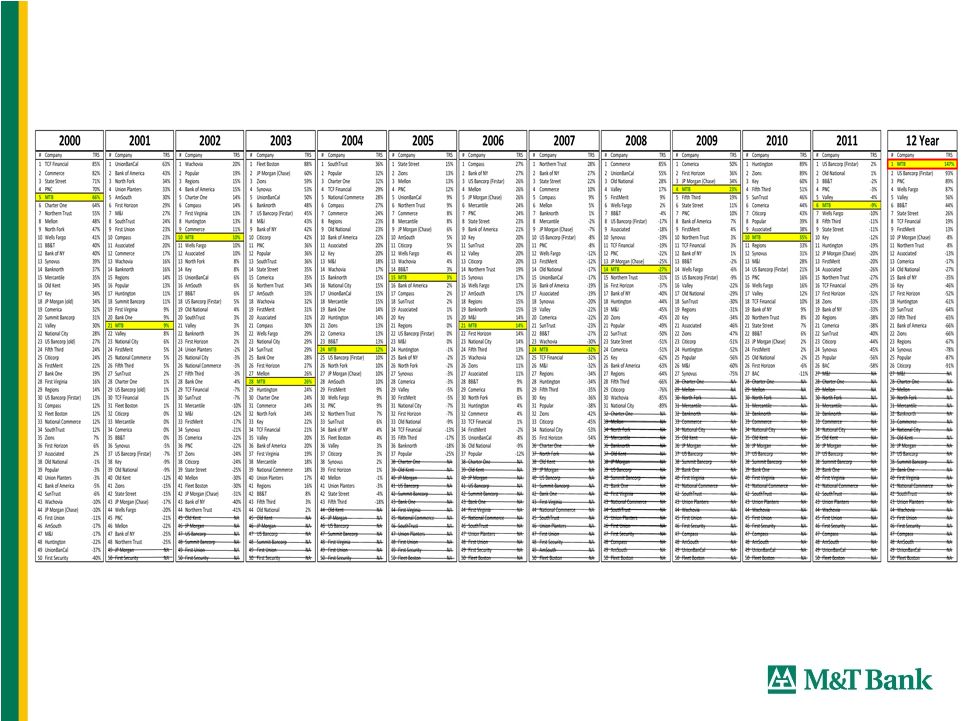

Strong Long-term Returns to Shareholders

Highest annual stock price appreciation among top 100 banks since 1983

19.3% annual total return since 1980

Highest total return among top 50 banks since 2000

$3,418 invested in M&T in 1980 would be worth $1 million today

|

Sanford C. Bernstein

Strategic Decisions Conference 2012

May 31, 2012 |

21

Appendix |

22

1 1983 Stock Prices Source: Compustat and/or SNL

Of the largest 100

banks operating in

1983, only 23 remain

today

Among the

remaining, M&T

ranks 1

st

in stock

price growth

M&T Bank Corporation…

a solid investment

Stock

Closing Price at

Return

4/30/2012

3/31/1983

CAGR

Rank

Company Name

Ticker

($)

($)

1

(%)

1

M&T Bank Corporation

MTB

86.27

1.34

15.4

2

State Street Corporation

STT

46.22

1.06

13.9

3

U.S. Bancorp

USB

32.17

0.92

13.0

4

Northern Trust Corporation

NTRS

47.56

1.51

12.6

5

Wells Fargo & Company

WFC

33.42

1.18

12.2

23

—

—

2.6

Median

—

—

7.8

MTB Price @ Median Growth Rate

11.96

1.34

7.8 |

23

19.3% Annual rate of return since 1980*

–

22

nd

best

return

of

the

entire

universe

of

over

700

U.S.

based

stocks that have traded publicly since 1980

$3,418 invested in M&T in 1980 would be worth $1 million today

*CAGR calculated assuming reinvestment of dividends through February 29,

2012. M&T Bank Corporation…

a solid investment

Rank

Company Name

Industry

Annual Return

1

Eaton Vance Corp.

Financials

25.1

2

Limited Brands Inc.

Consumer Discretionary

23.3

3

Gap Inc.

Consumer Discretionary

22.8

4

Progressive Corp.

Financials

22.8

5

TJX Cos.

Consumer Discretionary

22.6

6

Stryker Corp.

Health Care

22.2

7

Wal-Mart Stores Inc.

Consumer Staples

21.8

8

Hasbro Inc.

Consumer Discretionary

21.6

9

Mylan Inc.

Health Care

21.6

10

Precision Castparts Corp.

Industrials

21.4

11

Leucadia National Corp.

Financials

20.9

12

Raven Industries Inc.

Industrials

20.9

13

Valspar Corp.

Materials

20.7

14

State Street Corp.

Financials

20.3

15

HollyFrontier Corp.

Energy

20.3

16

Danaher Corp.

Industrials

20.3

17

Berkshire Hathaway Inc. Cl A

Financials

20.2

18

Robert Half International Inc.

Industrials

19.8

19

Forest Laboratories Inc.

Health Care

19.8

20

Family Dollar Stores Inc.

Consumer Discretionary

19.4

21

Graco Inc.

Industrials

19.4

22

M&T Bank Corp.

Financials

19.3 |

24

Total Returns to Shareholders

(1)

Largest 50 banks by market capitalization as of January 1, 2000

(1) Total Return To Shareholder from 12/31/1999 to 12/31/2011, as sourced

from Barclays Capital and SNL Financial. |

25

2011 Peer Group -

Largest 12 Regional Banks

BB&T Corporation

M&T Bank Corporation

Capital One Financial Corporation

PNC Financial Services Group, Inc.

Comerica Incorporated

Regions Financial Corporation

Fifth Third Bancorp

Synovus Financial Corp.

SunTrust Banks, Inc.

Huntington Bancshares Incorporated

Zions Bancorporation

KeyCorp |

26

Reconciliation of GAAP and Non-GAAP Measures

Net Income

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1Q12

$'s in millions

Net income

$268.2

$353.1

$456.7

$573.9

$722.5

$782.2

$839.2

$654.3

$555.9

$379.9

$736.2

$859.5

$206.5

Intangible amortization*

56.1

99.4

32.5

47.8

46.1

34.7

38.5

40.5

40.5

39.0

35.3

37.6

10.2

Merger-related items*

16.4

4.8

-

39.2

-

-

3.0

9.1

2.2

36.5

(16.3)

(12.8)

1.7

Net operating income

$340.7

$457.3

$489.2

$660.9

$768.6

$816.9

$880.7

$703.8

$598.6

$455.4

$755.2

$884.3

$218.4

Pre-Tax, Pre-Provision

Income

Net Income for EPS

$268.2

$353.1

$456.8

$573.9

$722.5

$782.2

$839.2

$654.3

$555.1

$332.0

$675.9

$781.8

$188.2

Preferred Div., Amort. of Pref. Stock

& Unvested Stock Awards

$0.0

$0.0

$0.0

$0.0

$0.0

$0.0

$0.0

$0.0

$0.8

$47.9

$60.3

$77.7

$18.2

Income Taxes

$154.1

$198.6

$219.2

$276.7

$344.0

$388.7

$392.5

$309.3

$183.9

$139.4

$356.6

$365.1

$102.0

GAAP Pre-tax Income

$422.3

$551.6

$675.9

$850.7

$1,066.5

$1,170.9

$1,231.6

$963.5

$739.8

$519.3

$1,092.8

$1,224.6

$308.4

Provision for credit losses

38.0

103.5

122.0

131.0

95.0

88.0

80.0

192.0

412.0

604.0

368.0

270.0

49.0

Pre-Tax, Pre-Provision Income

$460.3

$655.1

$797.9

$981.7

$1,161.5

$1,258.9

$1,311.6

$1,155.5

$1,151.8

$1,123.3

$1,460.8

$1,494.6

$357.4

Earnings Per Share

Diluted earnings per share

$3.24

$3.58

$4.78

$4.95

$6.00

$6.73

$7.37

$5.95

$5.01

$2.89

$5.69

$6.35

$1.50

Intangible amortization*

0.67

1.00

0.34

0.41

0.38

0.30

0.33

0.37

0.36

0.34

0.29

0.30

0.08

Merger-related items*

0.20

0.05

-

0.34

-

-

0.03

0.08

0.02

0.31

(0.14)

(0.10)

0.01

Diluted net operating

earnings per share

$4.11

$4.63

$5.12

$5.70

$6.38

$7.03

$7.73

$6.40

$5.39

$3.54

$5.84

$6.55

$1.59

Efficiency Ratio

$'s in millions

Non-interest expenses

$718.6

$980.6

$961.6

$1,448.2

$1,516.0

$1,485.1

$1,551.7

$1,627.7

$1,727.0

$1,980.6

$1,914.8

$2,478.1

$639.7

less: intangible amortization

69.6

121.7

51.5

78.2

75.4

56.8

63.0

66.5

66.6

64.3

58.1

61.6

16.8

less: merger-related expenses

26.0

8.0

-

60.4

-

-

5.0

14.9

3.5

89.2

0.8

83.7

2.7

Non-interest operating expenses

$623.0

$850.9

$910.1

$1,309.6

$1,440.6

$1,428.3

$1,483.7

$1,546.3

$1,656.8

$1,827.2

$1,856.0

$2,332.8

$620.2

FTE net interest income

$864.7

$1,175.8

$1,261.6

$1,615.1

$1,751.9

$1,811.6

$1,837.2

$1,871.0

$1,961.6

$2,077.6

$2,291.5

$2,415.6

$627.1

plus: Other Income

$324.7

$477.5

$512.0

$831.1

$943.0

$949.7

$1,045.9

$933.1

$939.0

$1,048.1

$1,108.1

$1,582.9

$376.7

less: gain/(loss) on sale of securities

(3.1)

1.9

(0.6)

2.5

2.9

1.2

2.6

1.2

34.4

1.2

2.8

150.2

0.0

less: net OTTI losses recognized

-

-

-

-

-

(29.4)

-

(127.3)

(182.2)

(138.3)

(86.3)

(77.0)

(11.5)

less: merger-related gains

-

-

-

-

-

-

-

-

-

29.1

27.5

64.9

-

Denominator for efficiency ratio

$1,192.5

$1,651.4

$1,774.2

$2,443.7

$2,692.0

$2,789.5

$2,880.5

$2,930.2

$3,048.4

$3,233.7

$3,455.6

$3,860.5

$1,015.3

Net operating efficiency ratio

52.3%

51.5%

51.3%

53.6%

53.5%

51.2%

51.5%

52.8%

54.4%

56.5%

53.7%

60.4%

61.1%

*Net of tax |

27

Reconciliation of GAAP and Non-GAAP Measures

Average Assets

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1Q12

$'s in millions

Average assets

23,670

$

30,842

$

31,935

$

45,349

$

51,517

$

54,135

$

55,839

$

58,545

$

65,132

$

67,472

$

68,380

$

73,977

$

78,026

$

Goodwill

(641)

(1,126)

(1,098)

(2,456)

(2,904)

(2,904)

(2,908)

(2,933)

(3,193)

(3,393)

(3,525)

(3,525)

(3,525)

Core deposit and other

intangible assets

(125)

(196)

(143)

(233)

(201)

(135)

(191)

(221)

(214)

(191)

(153)

(168)

(168)

Deferred taxes

30

56

46

-

-

52

38

24

30

33

29

43

48

Average tangible assets

22,934

$

29,576

$

30,740

$

42,660

$

48,412

$

51,148

$

52,778

$

55,415

$

61,755

$

63,921

$

64,731

$

70,327

$

74,381

$

Average Common Equity

$'s in millions

Average common equity

2,045

$

2,975

$

3,026

$

4,941

$

5,701

$

5,798

$

6,041

$

6,247

$

6,423

$

6,616

$

7,367

$

8,207

$

8,510

$

Goodwill

(641)

(1,126)

(1,098)

(2,456)

(2,904)

(2,904)

(2,908)

(2,933)

(3,193)

(3,393)

(3,525)

(3,525)

(3,525)

Core deposit and other

intangible assets

(125)

(196)

(143)

(233)

(201)

(135)

(191)

(221)

(214)

(191)

(153)

(168)

(168)

Deferred taxes

30

56

46

68

76

52

38

24

30

33

29

43

48

Average tangible common equity

1,309

$

1,709

$

1,831

$

2,320

$

2,672

$

2,811

$

2,980

$

3,117

$

3,046

$

3,065

$

3,718

$

4,557

$

4,866

$ |