Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - PEABODY ENERGY CORP | btu8k20120517.htm |

Exhibit 99.1

Energizing The World One BTU At A Time

Bank of America - Merrill Lynch Global Metals and Mining Conference

Gregory H. Boyce Chairman and Chief Executive Officer

May 17, 2012

Peabody Energy

Statement on Forward-Looking Information

Peabody Energy

Some of the following information contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, as amended, and is intended to come within the safe-harbor protection provided by those sections. Our forward-looking statements are based on numerous assumptions that the company believes are reasonable, but they are open to a wide range of uncertainties and business risks that may cause actual results to differ materially from expectations as of April 19, 2012. These factors are difficult to accurately predict and may be beyond the company's control. The company does not undertake to update its forward-looking statements. Factors that could affect the company's results include, but are not limited to: global demand for coal, including the seaborne thermal and metallurgical coal markets; price volatility, particularly in higher-margin products and in our trading and brokerage businesses; impact of alternative energy sources, including natural gas and renewables; impact of weather and natural disasters on demand, production and transportation; reductions and/or deferrals of purchases by major customers and ability to renew sales contracts; credit and performance risks associated with customers, suppliers, contract miners, co-shippers, and trading, banks and other financial counterparties; geologic, equipment, permitting and operational risks related to mining; transportation availability, performance and costs; availability, timing of delivery and costs of key supplies, capital equipment or commodities such as diesel fuel, steel, explosives and tires; integration of the newly acquired Macarthur Coal operations; successful implementation of business strategies; negotiation of labor contracts, employee relations and workforce availability; changes in postretirement benefit and pension obligations and funding requirements; replacement and development of coal reserves; availability, access to and related cost of capital and financial markets; effects of changes in interest rates and currency exchange rates (primarily the Australian dollar); effects of acquisitions or divestitures; economic strength and political stability of countries in which we have operations or serve customers; legislation, regulations and court decisions or other government actions, including new environmental and mine safety requirements; changes in income tax regulations or other regulatory taxes; litigation, including claims not yet asserted; and other risks detailed in the company's reports filed with the Securities and Exchange Commission (SEC). The use of “Peabody,” “the company,” and “our” relate to Peabody, its subsidiaries and majority-owned affiliates.

Adjusted EBITDA is defined as income from continuing operations before deducting net interest expense, income taxes, asset retirement obligation expense, depreciation, depletion and amortization, and amortization of basis difference associated with equity method investments. Adjusted EBITDA, which is not calculated identically by all companies, is not a substitute for operating income, net income or cash flow as determined in accordance with United States generally accepted accounting principles. Management uses Adjusted EBITDA as a key measure of operating performance and also believes it is a useful indicator of the company's ability to meet debt service and capital expenditure requirements.

Adjusted Income from Continuing Operations and Adjusted EPS are defined as income from continuing operations and diluted earnings per share excluding the impact of the remeasurement of foreign income tax accounts. Management has included these measures because, in management's opinion, excluding such impact is a better indicator of the company's ongoing effective tax rate and diluted earnings per share, and is therefore more useful in comparing the company's results with prior and future periods.

5/17/12

2

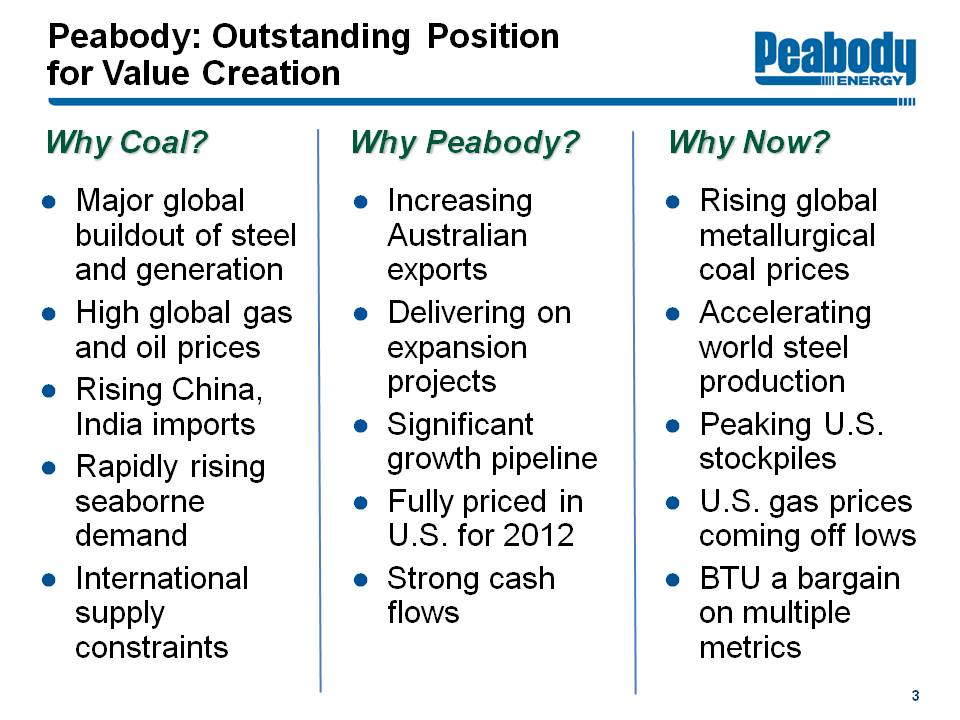

Peabody: Outstanding Position for Value Creation

Peabody Energy

Why Coal?

Major global buildout of steel and generation

High global gas and oil prices

Rising China, India imports

Rapidly rising seaborne demand

International supply constraints

Why Peabody?

Increasing Australian exports

Delivering on expansion projects

Significant growth pipeline

Fully priced in U.S. for 2012

Strong cash flows

Why Now?

Rising global metallurgical coal prices

Accelerating world steel production

Peaking U.S. stockpiles

U.S. gas prices coming off lows

BTU a bargain on multiple metrics

3

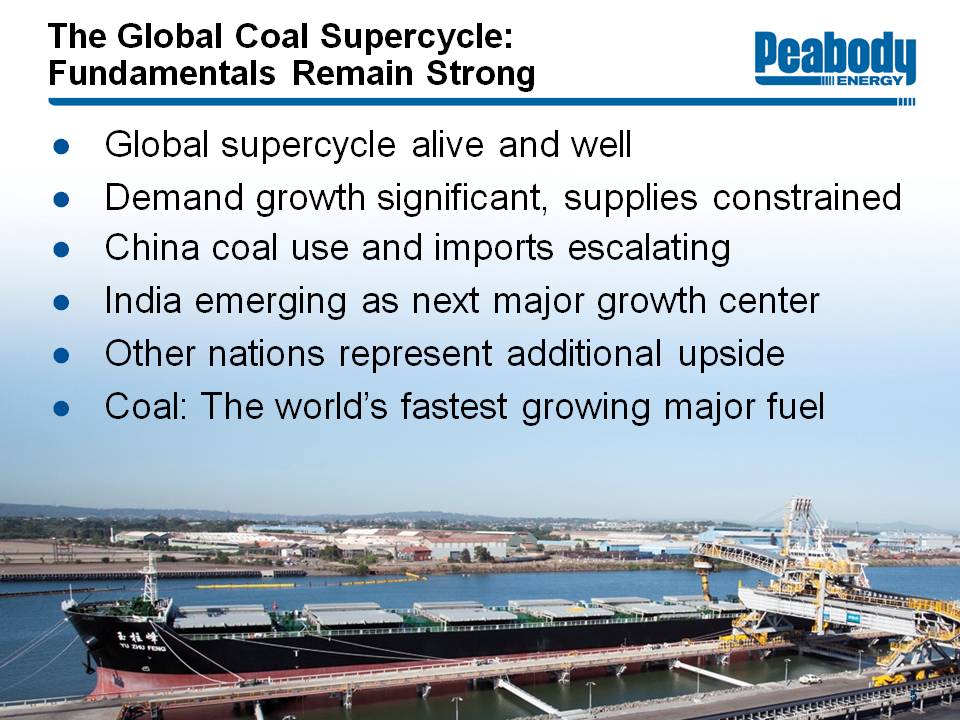

The Global Coal Supercycle is Alive and Well

The Global Coal Supercycle: Fundamentals Remain Strong

Peabody Energy

Global supercycle alive and well

Demand growth significant, supplies constrained

China coal use and imports escalating

India emerging as next major growth center

Other nations represent additional upside

Coal: The world's fastest growing major fuel

5

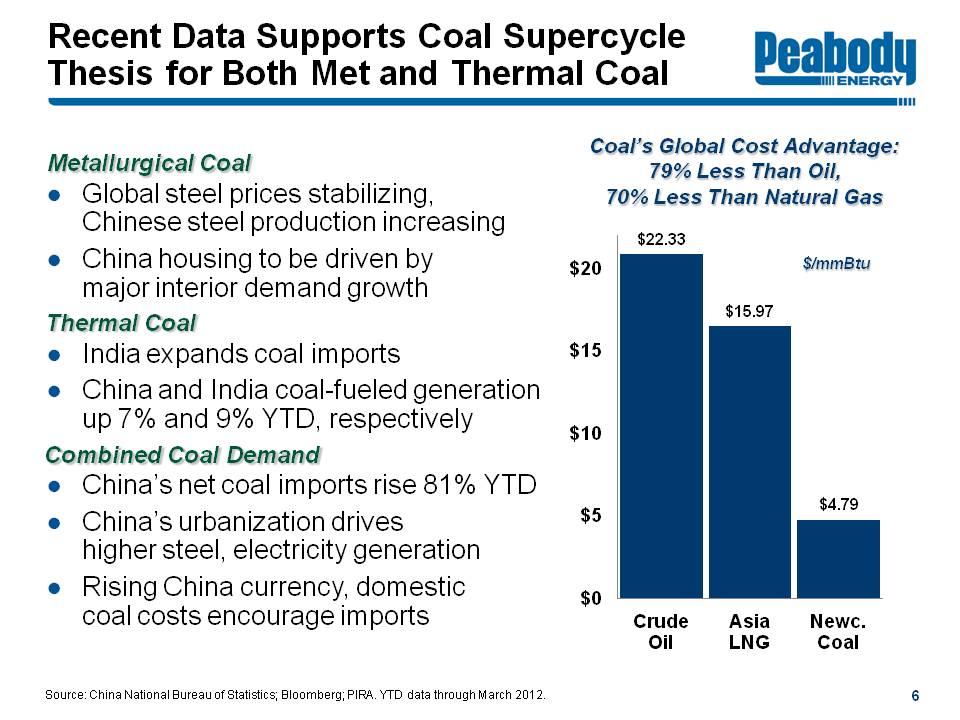

Recent Data Supports Coal Supercycle Thesis for Both Met and Thermal Coal

Peabody Energy

Metallurgical Coal

Global steel prices stabilizing, Chinese steel production increasing

China housing to be driven by major interior demand growth

Thermal Coal

India expands coal imports

China and India coal-fueled generation up 7% and 9% YTD, respectively

Combined Coal Demand

China's net coal imports rise 81% YTD

China's urbanization drives higher steel, electricity generation

Rising China currency, domestic coal costs encourage imports

Coal's Global Cost Advantage: 79% Less Than Oil, 70% Less Than Natural Gas

Crude Oil $22.33

Asia LNG $15.97

Newc. Coal $4.79

$/mmBtu

Source: China National Bureau of Statistics; Bloomberg; PIRA. YTD data through March 2012.

6

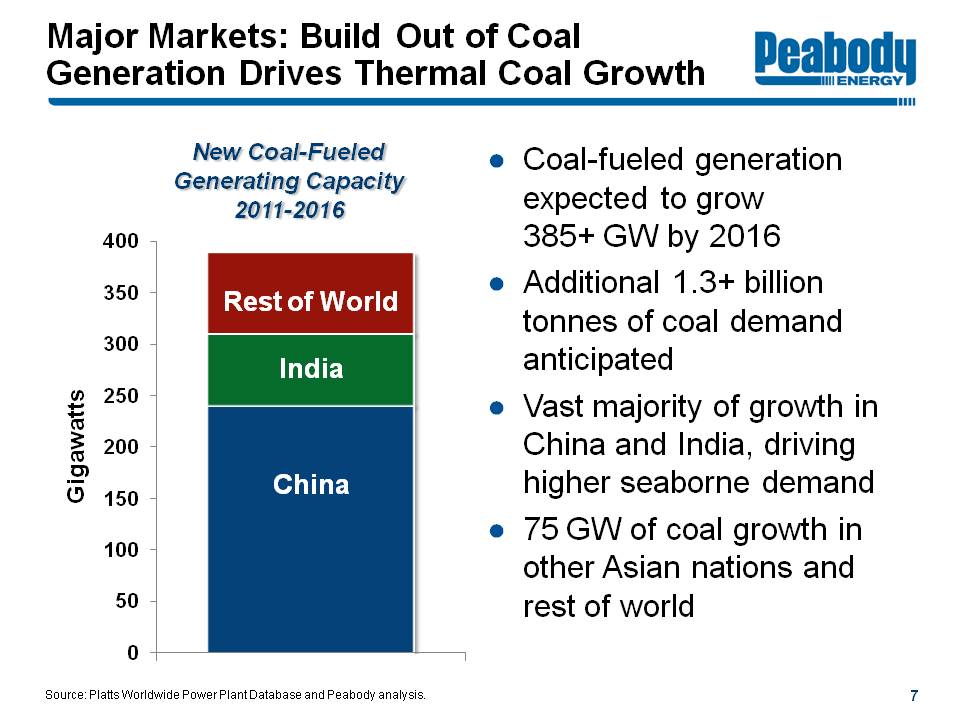

Major Markets: Build Out of Coal Generation Drives Thermal Coal Growth

Peabody Energy

New Coal-Fueled Generating Capacity 2011-2016

Gigawatts

Rest of World

India

China

Coal-fueled generation expected to grow 385+ GW by 2016

Additional 1.3+ billion tonnes of coal demand anticipated

Vast majority of growth in China and India, driving higher seaborne demand

75 GW of coal growth in other Asian nations and rest of world

Source: Platts Worldwide Power Plant Database and Peabody analysis.

7

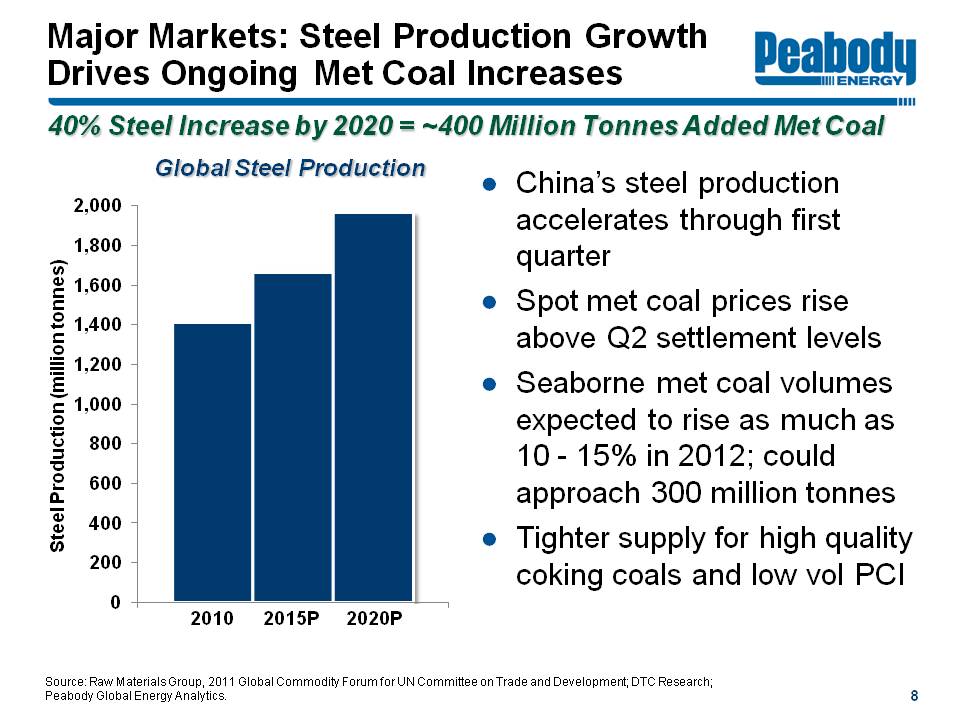

Major Markets: Steel Production Growth Drives Ongoing Met Coal Increases

Peabody Energy

40% Steel Increase by 2020 = ~400 Million Tonnes Added Met Coal

Global Steel Production

Steel Production (million tonnes)

2010 2015P 2020P

China's steel production accelerates through first quarter

Spot met coal prices rise above Q2 settlement levels

Seaborne met coal volumes expected to rise as much as 10 - 15% in 2012; could approach 300 million tonnes

Tighter supply for high quality coking coals and low vol PCI

Source: Raw Materials Group, 2011 Global Commodity Forum for UN Committee on Trade and Development; DTC Research; Peabody Global Energy Analytics.

8

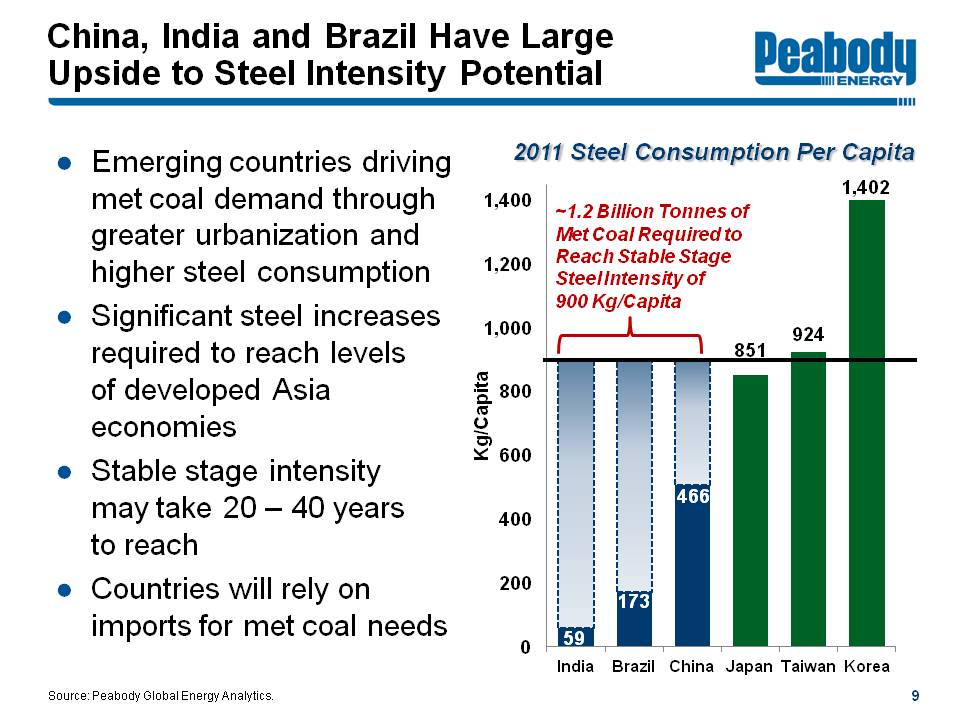

China, India and Brazil Have Large Upside to Steel Intensity Potential

Peabody Energy

Emerging countries driving met coal demand through greater urbanization and higher steel consumption

Significant steel increases required to reach levels of developed Asia economies

Stable stage intensity may take 20 - 40 years to reach

Countries will rely on imports for met coal needs

2011 Steel Consumption Per Capita

~1.2 Billion Tonnes of Met Coal Required to Reach Stable Stage Steel Intensity of 900 Kg/Capita

Kg/Capita

India 59

Brazil 173

China 466

Japan 851

Taiwan 924

Korea 1,402

Source: Peabody Global Energy Analytics.

9

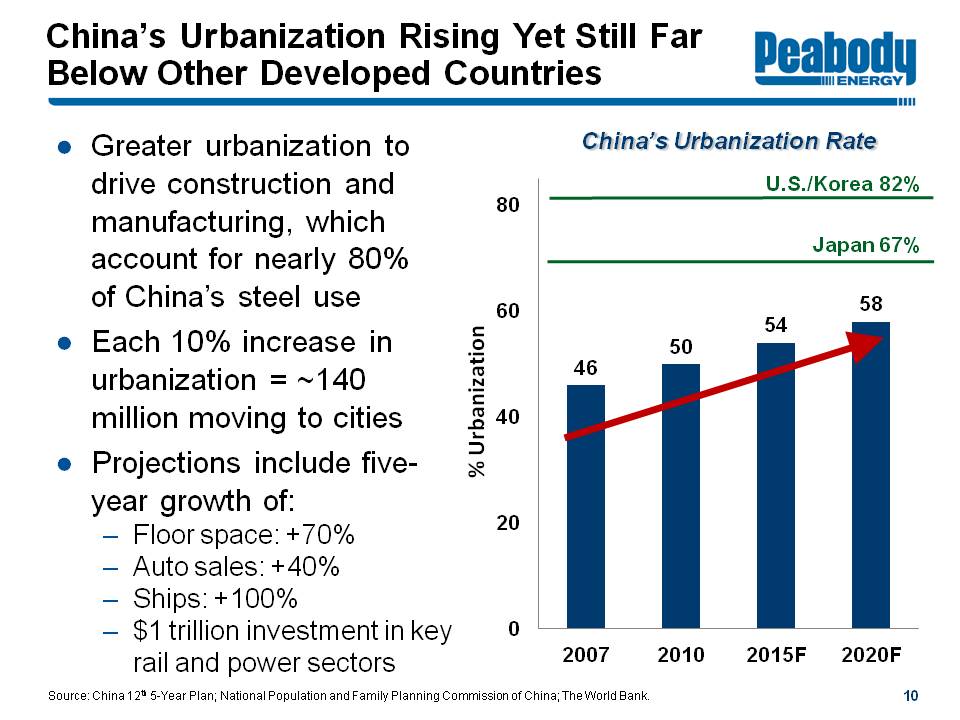

China's Urbanization Rising Yet Still Far Below Other Developed Countries

Peabody Energy

Greater urbanization to drive construction and manufacturing, which account for nearly 80% of China's steel use

Each 10% increase in urbanization = ~140 million moving to cities

Projections include five-year growth of:

Floor space: +70%

Auto sales: +40%

Ships: +100%

$1 trillion investment in key rail and power sectors

China's Urbanization Rate

% Urbanization

U.S./Korea 82%

Japan 67%

2007 46%

2010 50%

2015F 54%

2020F 58%

Source: China 12th 5-Year Plan; National Population and Family Planning Commission of China; The World Bank.

10

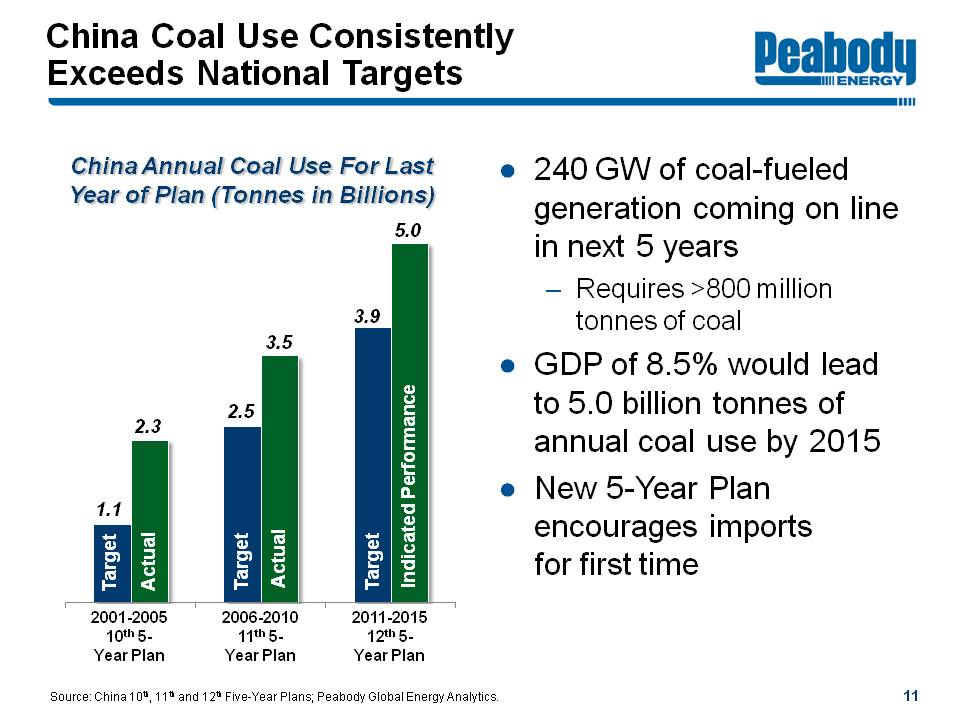

China Coal Use Consistently Exceeds National Targets

Peabody Energy

China Annual Coal Use For Last Year of Plan (Tonnes in Billions)

2001-2005 10th 5-Year Plan Target 1.1 Actual 2.3

2006-2010 11th 5-Year Plan Target 2.5 Actual 3.5

2011-2015 12th 5-Year Plan Target 3.9 Indicated Performance 5.0

240 GW of coal-fueled generation coming online in next 5 years

Requires >800 million tonnes of coal

GDP of 8.5% would lead to 5.0 billion tonnes of annual coal use by 2015

New 5-Year Plan encourages imports for first time

Source: China 10th, 11th and 12th Five-Year Plans; Peabody Global Energy Analytics.

11

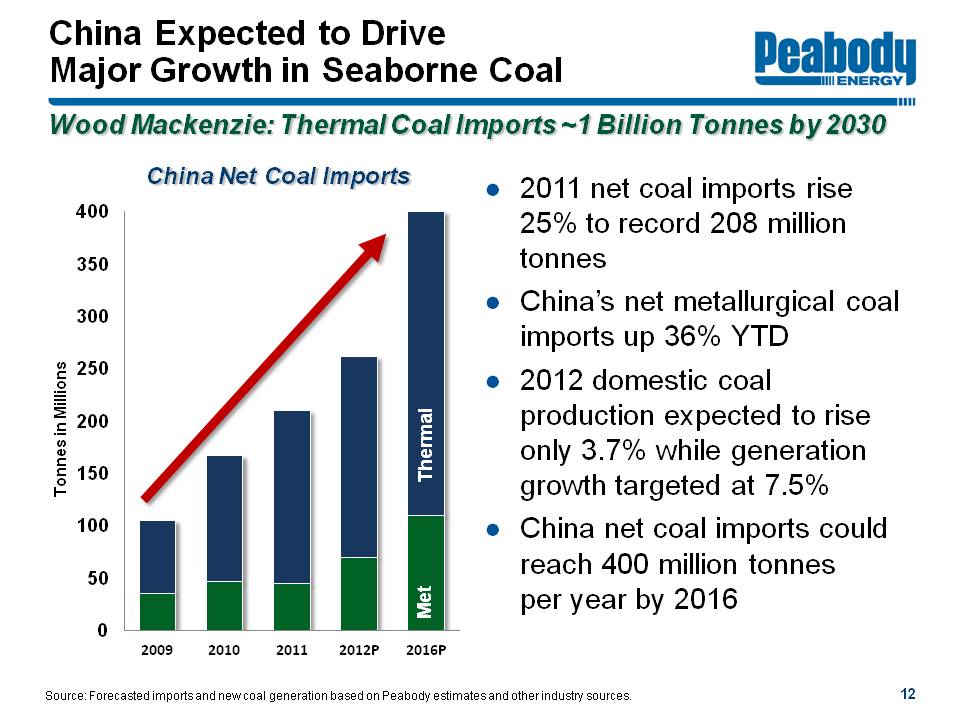

China's Expected to Drive Major Growth in Seaborne Coal

Peabody Energy

Wood Mackenzie: Thermal Coal Imports ~1 Billion Tonnes by 2030

China Net Coal Imports

Tonnes in Millions

2009 2010 2011 2012P 2016P Met Thermal

2011 net coal imports rise 25% to record 208 million tonnes

China's net metallurgical imports up 36% YTD

2012 domestic coal production expected to rise only 3.7% while generation growth targeted at 7.5%

China net coal imports could reach 400 million tonnes per year by 2016

Source: Forecasted imports and new coal generation based on Peabody estimates and other industry sources.

12

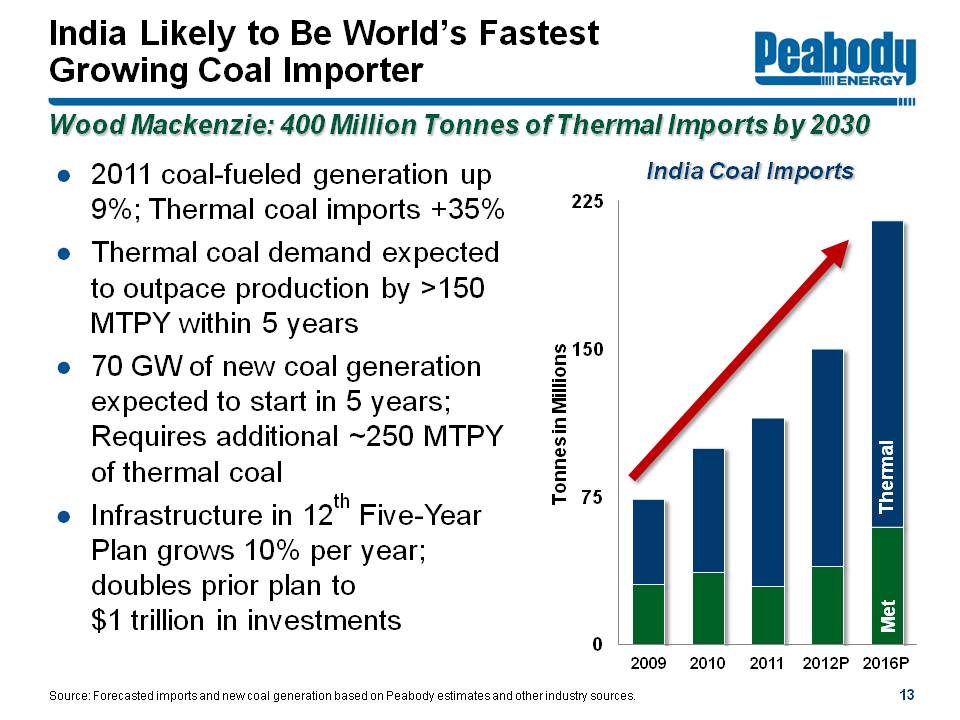

India Likely to Be World's Fastest Growing Coal Importer

Peabody Energy

Wood Mackenzie: 400 Million Tonnes of Thermal Imports by 2030

2011 Coal-Fueled Generation up 9%; Thermal Coal Imports +35%

Thermal coal demand expected to outpace production by >150 MTPY within 5 years

70 GW of new coal generation expected to start in 5 years; Requires additional ~250 MTPY of thermal coal

Infrastructure in 12th Five-Year Plan grows 10% per year; doubles prior plan to $1 trillion in investments

India Coal Imports

Tonnes in Millions

2009 2010 2011 2012P 2016P Met Thermal

Source: Forecasted imports and new coal generation based on Peabody estimates and other industry sources.

13

Major Supply Constraints Tighten Global Coal Markets

Peabody Energy

Metallurgical Coal Supply

Mine closures, weather and labor reduces 15 million tones of annualized met supplies YTD

Met coal in structural undersupply long-term

China experiencing higher costs and declining quality for met coal

Thermal Coal Supply

China thermal coal traveling much longer distances

India's thermal production below targets and shortfalls expected going forward

Combined Coal Supply

Domestic market needs challenge Indonesia, South Africa exports

Rail and port capacity trails demand in Australia, South Africa, Canada and U.S. West Coast

Permitting, geology and costs limit Eastern U.S. production

Infrastructure and labor issues exist in multiple markets

Coal trucks contribute to 60-mile traffic jam in China

14

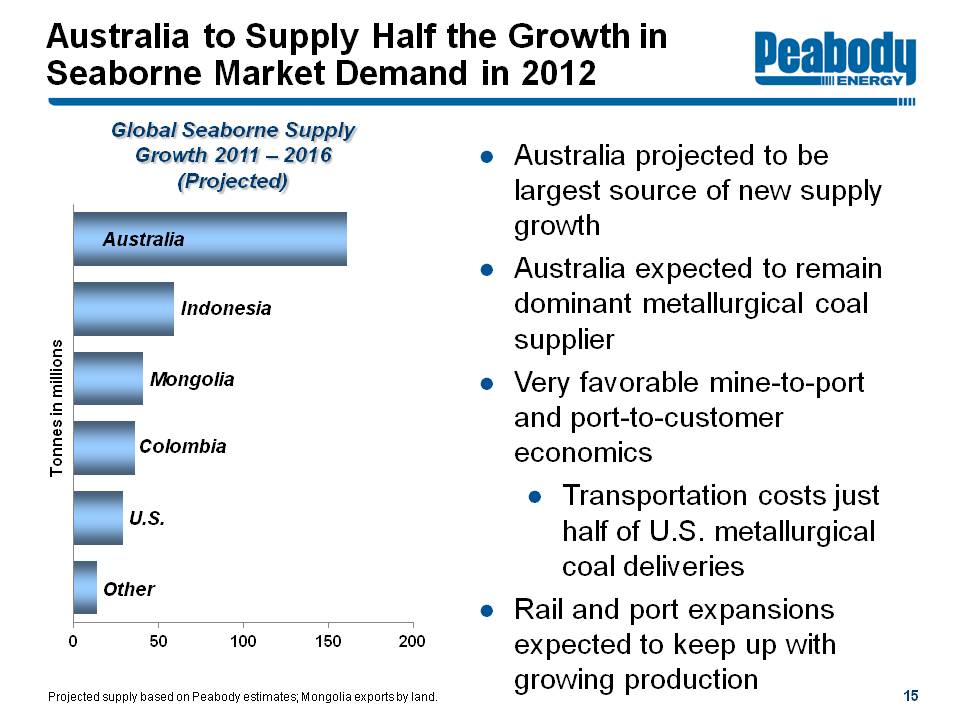

Australia to Supply Half the Growth in Seaborne Market Demand in 2012

Peabody Energy

Global Seaborne Supply Growth 2011 - 2016 (Projected)

Tonnes in millions

Australia

Indonesia

Mongolia

Colombia

U.S.

Other

Australia projected to be largest source of new supply growth

Australia expected to remain dominant metallurgical coal supplier

Very favorable mine-to-port and port-to-customer economics

Transportation costs just half of U.S. metallurgical coal deliveries

Rail and port expansions expected to keep up with growing production

Projected supply based on Peabody estimates; Mongolia exports by land.

15

PRB and Illinois Basin Expected to Dual-Serve U.S. and Global Markets

Peabody Energy

U.S. port capacity could grow ~100 million tons within 5 years based on announcements

Two-thirds of growth in West Coast/Gulf Coast

U.S. basins expected to see significant demand shift

Lower-cost PRB and ILB regions growing due to:

New plants

Rising exports

Backfill to Eastern plants

Peabody has the number one position in the Southern Powder River Basin and Illinois Basin, which is expected to grow over the next five years even as other regions decline.

Source: Peabody Energy Global Analytics.

16

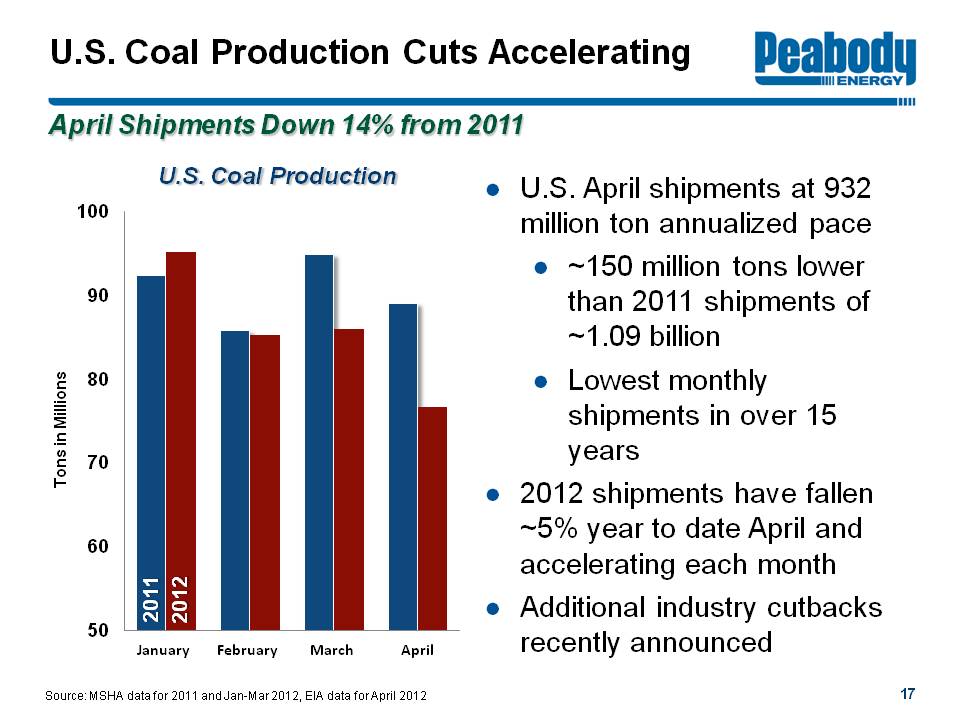

U.S. Coal Production Cuts Accelerating

Peabody Energy

U.S. April Shipments Down 14% from 2011

U.S. Coal Production

Tons in Millions

2011 2012

January February March April

April shipments at 932 million ton annualized pace

~150 million tons lower than 2011 shipments of ~1.09 billion

Lowest monthly shipments in over 15 years

2012 shipments have fallen ~5% year to date April and accelerating each month

Additional industry cutbacks recently announced

Source: MSHA data for 2011 and Jan-Mar 2012, EIA data for April 2012

17

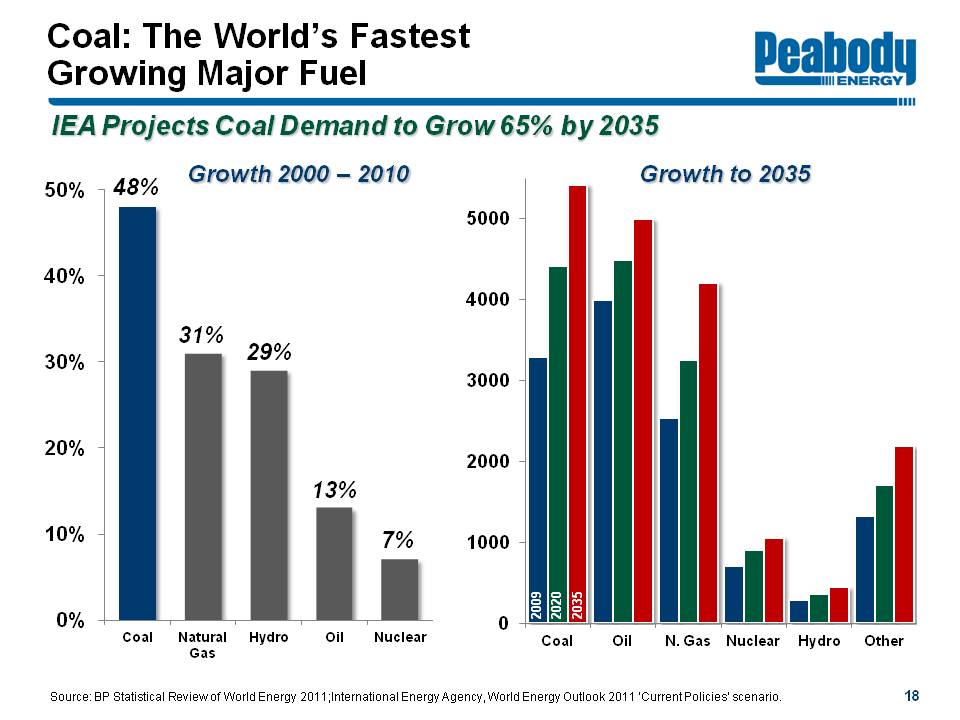

Coal: The World's Fastest Growing Major Fuel

Peabody Energy

IEA Projects Coal Demand to Grow 65% by 2035

Growth 2000-2010

Coal 48% Natural Gas 31% Hydro 29% Oil 13% Nuclear 7%

Growth to 2035

2009 2020 2035

Coal Oil N. Gas Nuclear Hydro Other

Source: BP Statistical Review of World Energy 2011; International Energy Agency, World Energy Outlook 2011 'Current Policies' scenario.

18

Peabody's Global Platform Drives Results

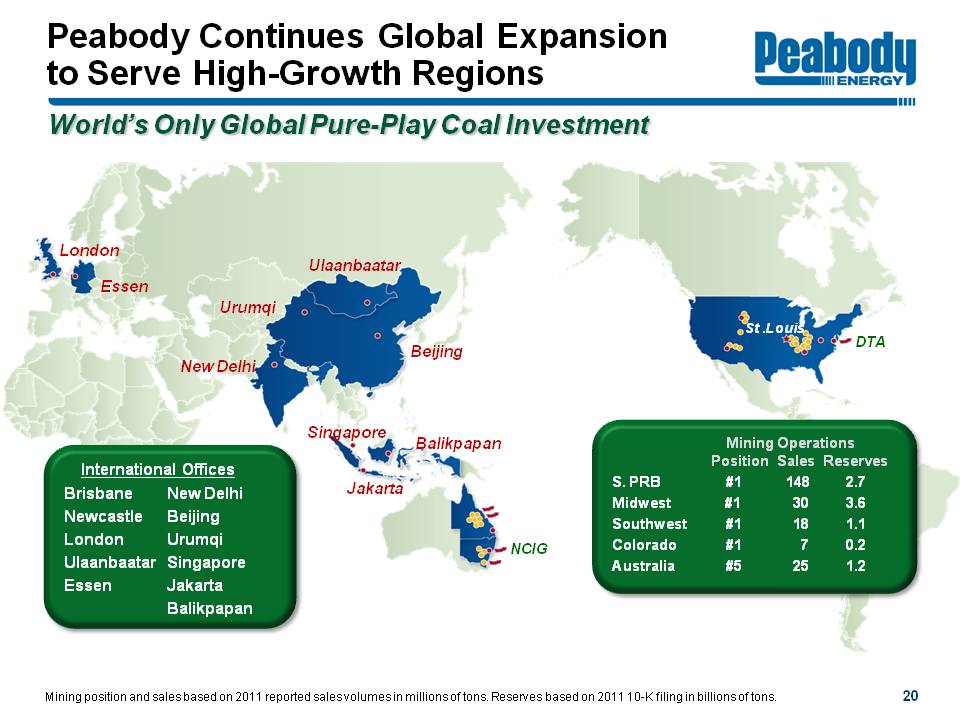

Peabody Continues Global Expansion to Serve High-Growth Regions

Peabody Energy

World's Only Global Pure-Play Coal Investment

London Essen New Delhi Urumqi Ulaanbaatar Beijing Singapore Jakarta Balikpapan NCIG St. Louis DTA

International Offices

Brisbane New Delhi Newcastle Beijing London Urumqi Ulaanbaatar Singapore Essen Jakarta Balikpapan

Mining Operations

Position S. PRB #1 Midwest #1 Southwest #1 Colorado #1 Australia #5

Sales S. PRB 148 Midwest 30 Southwest 18 Colorado 7 Australia 25

Reserves S. PRB 2.7 Midwest 3.6 Southwest 1.1 Colorado 0.2 Australia 1.2

Mining position and sales based on 2011 reported sales volumes in millions of tons. Reserves based on 2011 10-K filing in billions of tons.

20

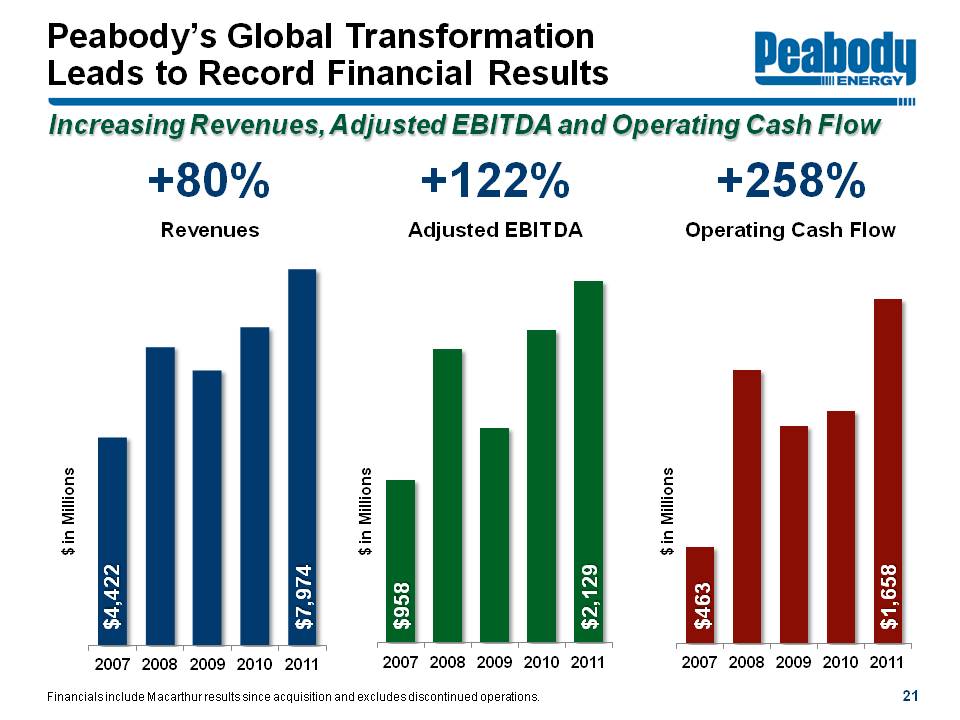

Peabody's Global Transformation Leads to Record Financial Results

Peabody Energy

Increasing Revenues, Adjusted EBITDA and Operating Cash Flow

+80% Revenues $ in Millions 2007 $4,422 2008 2009 2010 2011 $7,974

+122% Adjusted EBITDA $ in Millions 2007 $958 2008 2009 2010 2011 $2,129

+258% Operating Cash Flow $ in Millions 2007 $463 2008 2009 2010 2011 $1,658

Financials include Macarthur results since acquisition and excludes discontinued operations.

21

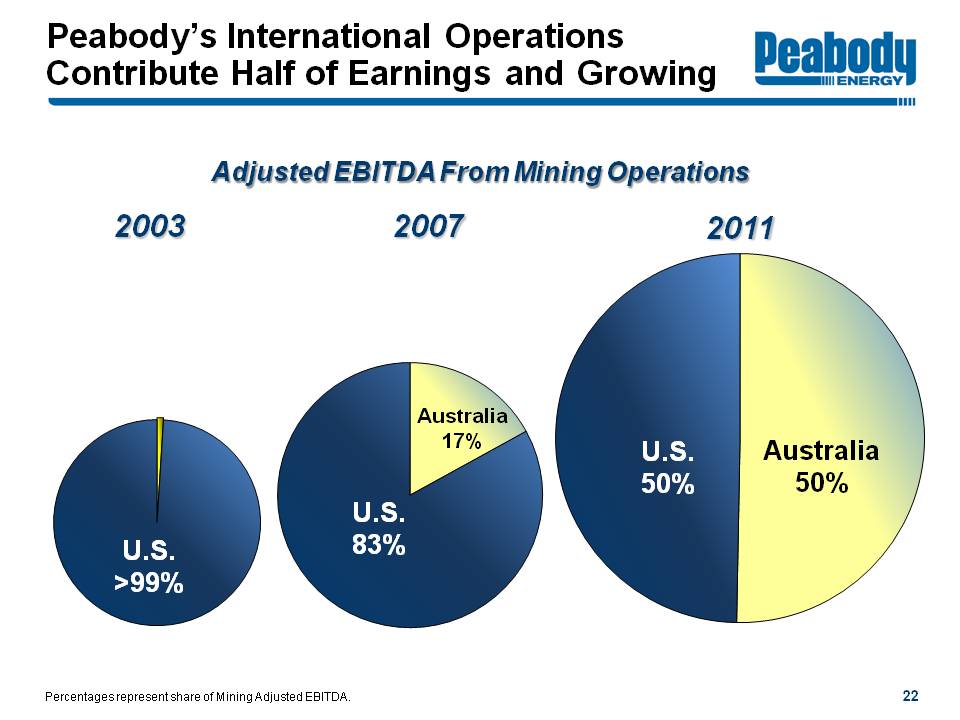

Peabody's International Operations Contribute Half of Earnings and Growing

Peabody Energy

Adjusted EBITDA From Mining Operations

2003 U.S. > 99%

2007 U.S. 83% Australia 17%

2011 U.S. 50% Australia 50%

Percentages represent share of Mining Adjusted EBITDA.

22

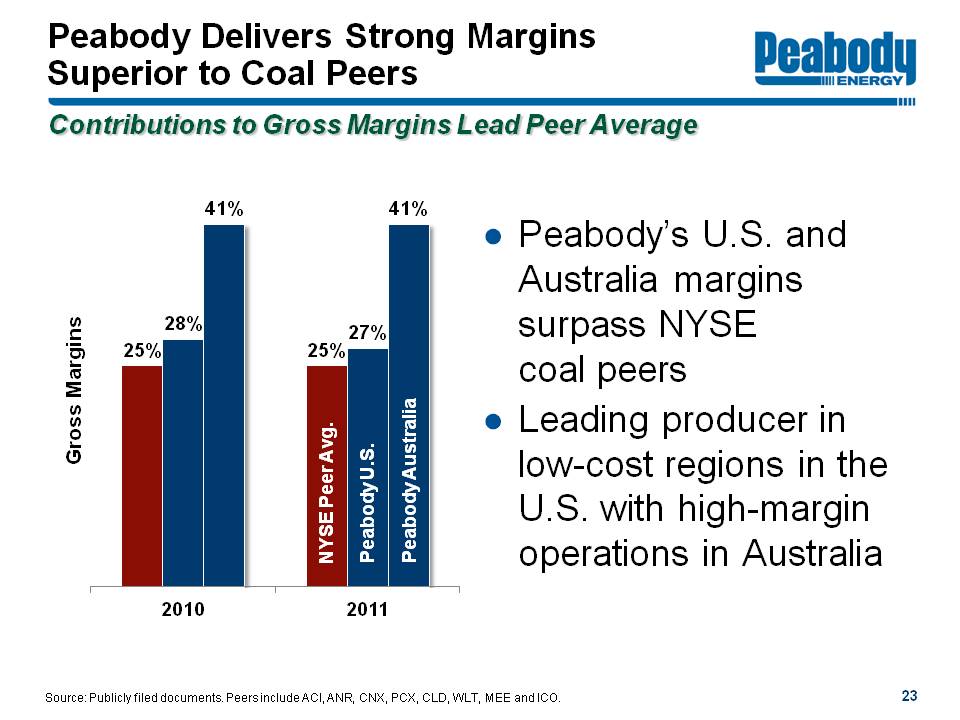

Peabody Delivers Strong Margins Superior to Coal Peers

Peabody Energy

Contributions to Gross Margins Lead Peer Average

Gross Margins

2010 25% 28% 41% 2011 NYSE Peer Avg. 25% Peabody U.S. 27% Peabody Australia 41%

Peabody's U.S. and Australia margins surpass NYSE coal peers

Leading producer in low-cost regions in the U.S. with high-margin operations in Australia

Source: Publicly filed documents. Peers include ACI, ANR, CNX, PCX, CLD, WLT, MEE and ICO.

23

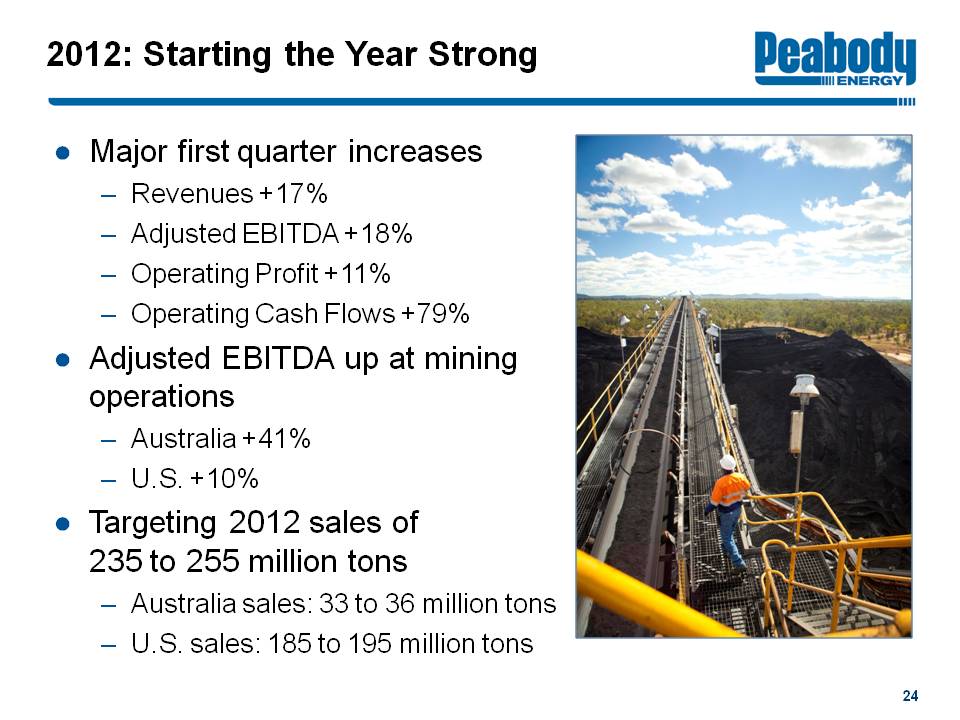

2012: Starting the Year Strong

Peabody Energy

Major first quarter increases

Revenues +17%

Adjusted EBITDA +18%

Operating Profit +11%

Operating Cash Flows +79%

Adjusted EBITDA up at mining operations

Australia +41%

U.S. +10%

Targeting 2012 sales of 235 to 255 million tons

Australia sales: 33 to 36 million tons

U.S. sales: 185 to 195 million tons

24

Peabody Focusing on Four Key Areas in 2012

Peabody Energy

Maintain Intense Focus on Operational Excellence

Integrate Acquisition into Australian Platform

Advance Organic Growth Projects

Strengthen Balance Sheet

25

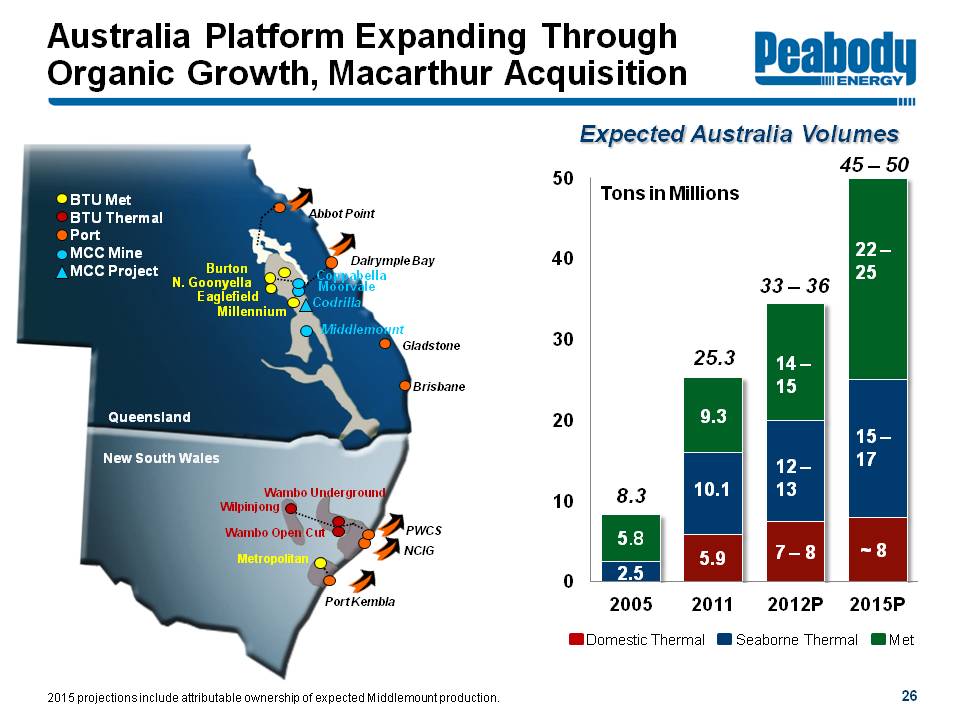

Australia Platform Expanding Through Organic Growth, Macarthur Acquisition

Peabody Energy

Queensland

Port Abbot Point Dalrymple Bay Gladstone Brisbane

BTU Met Burton N. Goonyella Eaglefield Millennium

MCC Mine Coppabella Moorvale Middlemount

MCC Project Codrilla

New South Wales

Port PWCS NCIG Port Kembla

BTU Thermal Wilpinjong Wambo Underground Wambo Open Cut

BTU Met Metropolitan

Expected Australia Volumes

Tons in Millions

2005 Seaborne Thermal 2.5 Met 5.8 Total 8.3

2011 Domestic Thermal 5.9 Seaborne Thermal 10.1 Met 9.3 Total 25.3

2012P Domestic Thermal 7-8 Seaborne Thermal 12-13 Met 14-15 Total 33-36

2015P Domestic Thermal ~8 Seaborne Thermal 15-17 Met 22-25 Total 45-50

2015 projections include attributable ownership of expected Middlemount production.

26

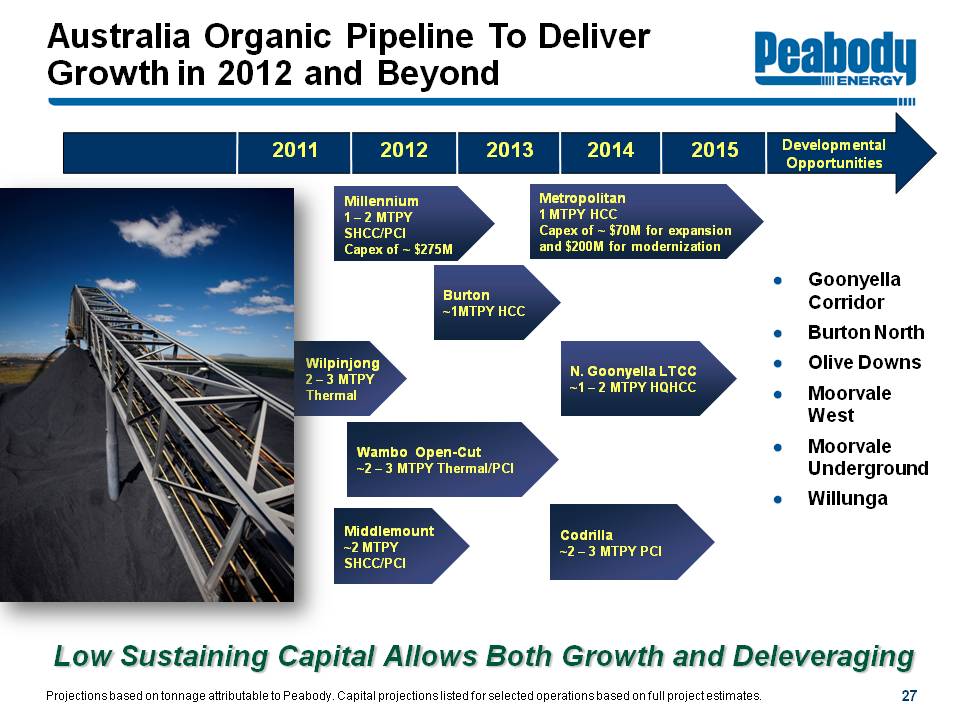

Australia Organic Pipeline To Deliver Growth in 2012 and Beyond

Peabody Energy

2011 2012 2013 2014 2015

Wilpinjong 2 - 3 MTPY Thermal

Millennium 1 - 2 MTPY SHCC/PCI Capex of ~$275M

Wambo Open-Cut ~2 - 3 MTPY Thermal/PCI

Middlemount ~2 MTPY SHCC/PCI

Burton ~1MTPY HCC

Metropolitan 1 MTPY HCC Capex of ~$70M for expansion and $200M for modernization

N. Goonyella LTCC ~1 - 2 MTPY HQHCC

Codrilla ~2 - 3 MTPY PCI

Developmental Opportunities Goonyella Corridor Burton North Olive Downs Moorevale West Moorevale Underground Willunga

Low Sustaining Capital Allows Both Growth and Deleveraging

Projections based on tonnage attributable to Peabody. Capital projections listed for selected operations based on full project estimates.

27

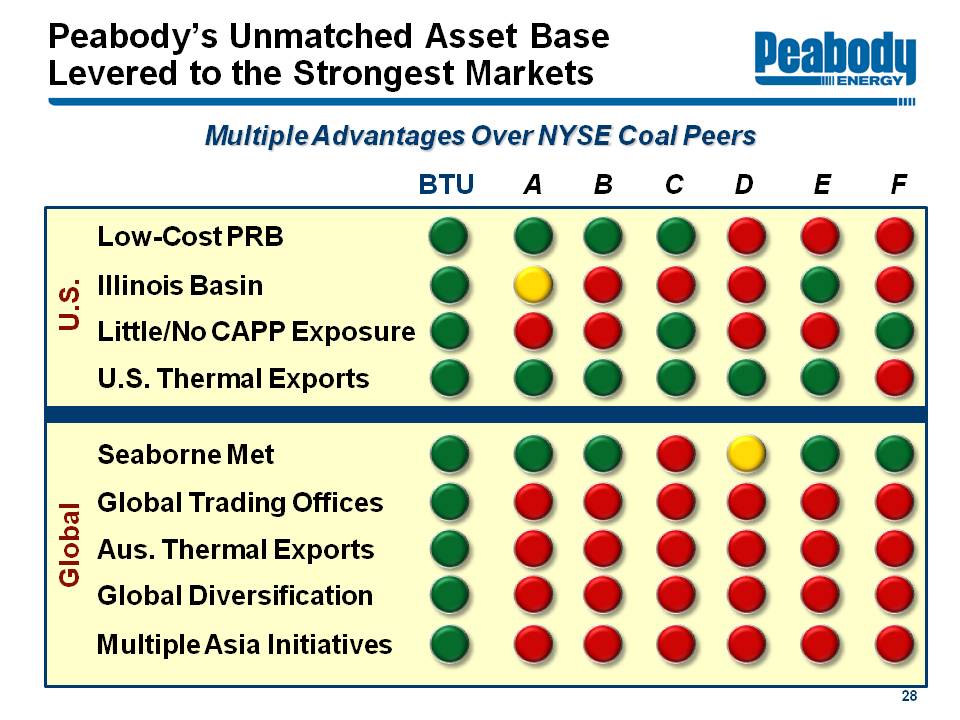

Peabody's Unmatched Asset Base Levered to the Strongest Markets

Peabody Energy

Multiple Advantages Over NYSE Coal Peers

BTU A B C D E F

U.S. Low-Cost PRB Illinois Basin Little/No CAPP Exposure U.S. Thermal Exports

Global Seaborne Met Global Trading Offices Aus. Thermal Exports Global Diversification Multiple Asia Initiatives

28

BTU: Multiple Catalysts for Value Creation in 2012

Peabody Energy

Record results and strong financial position

Targeting 2012 Australia growth of 8 - 11 million tons; further expansion in 2013

Significant pipeline for future growth

Fully contracted in U.S. for 2012, leader in low-cost regions

Platform, markets offer volume and price upside potential

29

Energizing The World One BTU At A Time

Bank of America - Merrill Lynch Global Metals and Mining Conference

Gregory H. Boyce Chairman and Chief Executive Officer

May 17, 2012

Peabody Energy

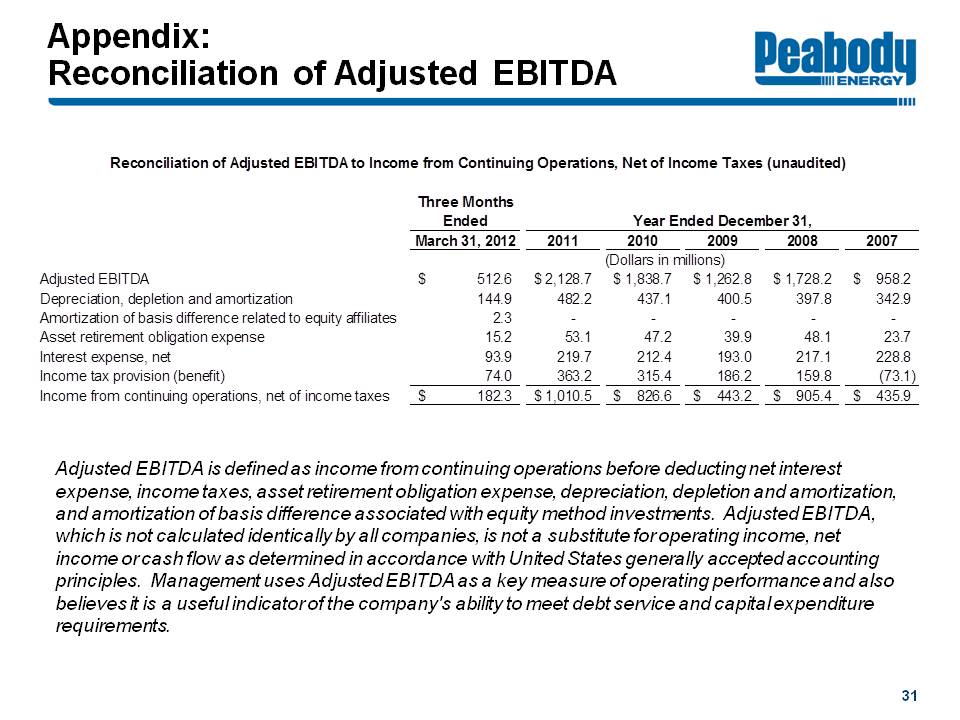

Appendix: Reconciliation of Adjusted EBITDA

Peabody Energy

Reconciliation of Adjusted EBITDA to Income from Continuing Operations, Net of Income Taxes (unaudited)

Three Months Ended March 31, 2012 Year Ended December 31, 2011 2010 2009 2008 2007

(Dollars in millions)

Adjusted EBITDA $512.6 $2,128.7 $1,838.7 $1,262.8 $1,728.2 $958.2

Depreciation, depletion and amortization 144.9 482.2 437.1 400.5 397.8 342.9

Amortization of basis difference related to equity affiliates 2.3 - - - - -

Asset retirement obligation expense 15.2 53.1 47.2 39.9 48.1 23.7

Interest expense, net 93.9 219.7 212.4 193.0 217.1 228.8

Income tax provision (benefit) 74.0 363.2 315.4 186.2 159.8 (73.1)

Income from continuing operations, net of income taxes $182.3 $1,010.5 $826.6 $443.2 $905.4 $435.9

Adjusted EBITDA is defined as income from continuing operations before deducting net interest expense, income taxes, asset retirement obligation expense, depreciation, depletion and amortization, and amortization of basis difference associated with equity method investments. Adjusted EBITDA, which is not calculated identically by all companies, is not a substitute for operating income, net income or cash flow as determined in accordance with United States generally accepted accounting principles. Management uses Adjusted EBITDA as a key measure of operating performance and also believes it is a useful indicator of the company's ability to meet debt service and capital expenditure requirements.

31