Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Fortune Brands Home & Security, Inc. | d352329d8k.htm |

JP

Morgan Home Building and Building Products Conference

May 16, 2012

Exhibit 99.1

Advantage:

Fortune Brands

Home & Security |

2

Fortune Brands

Home & Security

Disclaimer

Please note that the information included in this presentation

contains statements relating to future results, which are forward-

looking statements. We caution you that these forward-looking

statements speak only as of the date hereof, and we have no

obligation to update them. Actual results may differ materially

from those projected as a result of certain risks and uncertainties,

including the risks described in our annual report on Form 10-K as

filed with the SEC. For more information, including reconciliations

of certain non-GAAP financial information presented herein,

please

visit

the

“Investor

Center”

on

the

Company’s

website

at:

www.FBHS.com. |

3

Fortune Brands

Home & Security

Our solid business model, which was fortified by the downturn, is the

foundation on which strong performance and market share growth is built.

Market Recovery

Strong Free Cash Flow

Effective Capital Deployment

Market Recovery

Share Gains

Attractive Product Categories

Consumer Driven Innovation

Operational and Management Excellence

Demonstrated Ability to Outperform the Market

Strong Capital Structure

Solid

Business

Model |

4

Fortune Brands

Home & Security

We believe this foundation and the aggressive moves we’ve made over the

past 3 years will allow us to continue to grow our market share and

leverage the housing market recovery.

Attractive Product Categories

Consumer Driven Innovation

Operational and Management Excellence

Demonstrated Ability to Outperform the Market

Strong Capital Structure

Market Recovery

Share Gains

Organic Growth

Solid

Business

Model |

5

Fortune Brands

Home & Security

In addition, growing free cash flow and leveraging our strong balance sheet

can provide incremental growth opportunities.

Attractive Product Categories

Consumer Driven Innovation

Operational and Management Excellence

Demonstrated Ability to Outperform the Market

Strong Capital Structure

Free Cash Flow

Leverage Capital Structure

Market Recovery

Share Gains

Incremental Growth

Organic Growth

Solid

Business

Model |

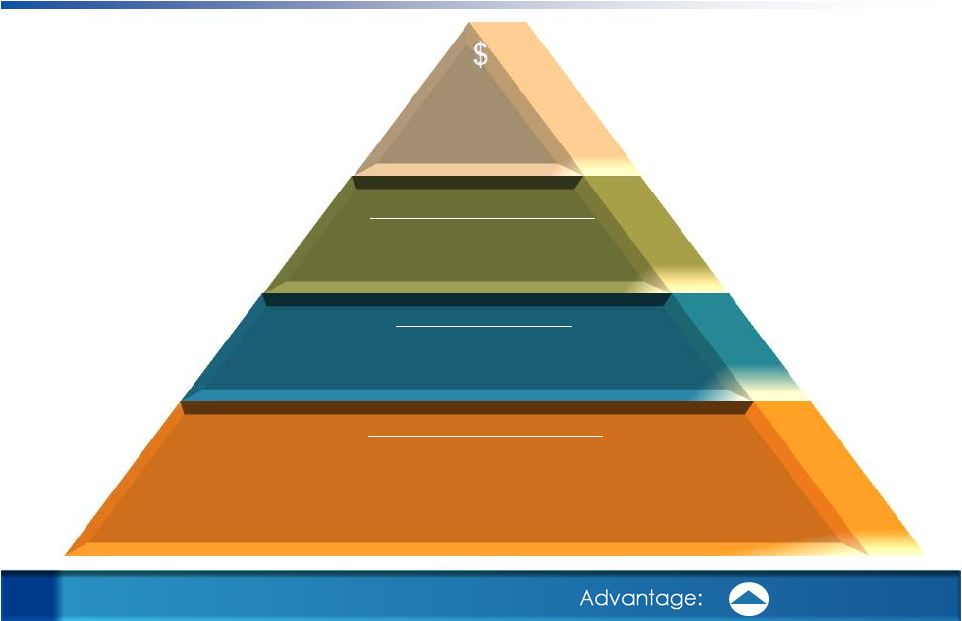

6

Fortune Brands

Home & Security

Long-term

Value

Creation

We believe our solid business model, growing free cash flow, and

strong

capital structure will create long-term shareholder value, both as the

market recovers and beyond the recovery.

Attractive Product Categories

Consumer Driven Innovation

Operational and Management Excellence

Demonstrated Ability to Outperform the Market

Strong Capital Structure

Long-term

Value

Creation

Free Cash Flow

Leverage Capital Structure

Incremental Growth

Market Recovery

Share Gains

Organic Growth

Attractive Product Categories

Consumer Driven Innovation

Operational and Management Excellence

Demonstrated Ability to Outperform the Market

Strong Capital Structure

Solid Business Model |

Brand Leadership

Position

We have leading brands and businesses in each segment, with

differentiated positions across categories and channels.

•

Primary

strength

in

dealer

channel

•

Fully

integrated

platform

•

Poised

to

leverage

scale

across

multiple

brands,

channels

and

price

points

•

Trusted

by

consumers

for

delivering

durable

dependable

products

•

Strength

with

builders

creates

wholesale

demand

•

Powerful

engine

for

growth

and

profitability

•

Leaders poised to leverage

the market recovery

•

Accelerating innovation

•

Building momentum

in global safety

•

Exceptional brand with growth

potential well beyond padlocks

•

More stable market not tied

to housing cycle

Kitchen & bath cabinet

manufacturer in

North America

Faucet brand in

North America

Fiberglass residential entry

door brand in U.S.

Padlock brand in

North America

#1

#1

#1

#1

Winner of two consumer

and five builder awards

from J.D. Power

Fortune Brands

Home & Security

7

Advantage:

Kitchen

& Bath

Cabinetry

Plumbing

&

Accessories

Advanced Material

Windows & Door

Systems

Security

&

Storage |

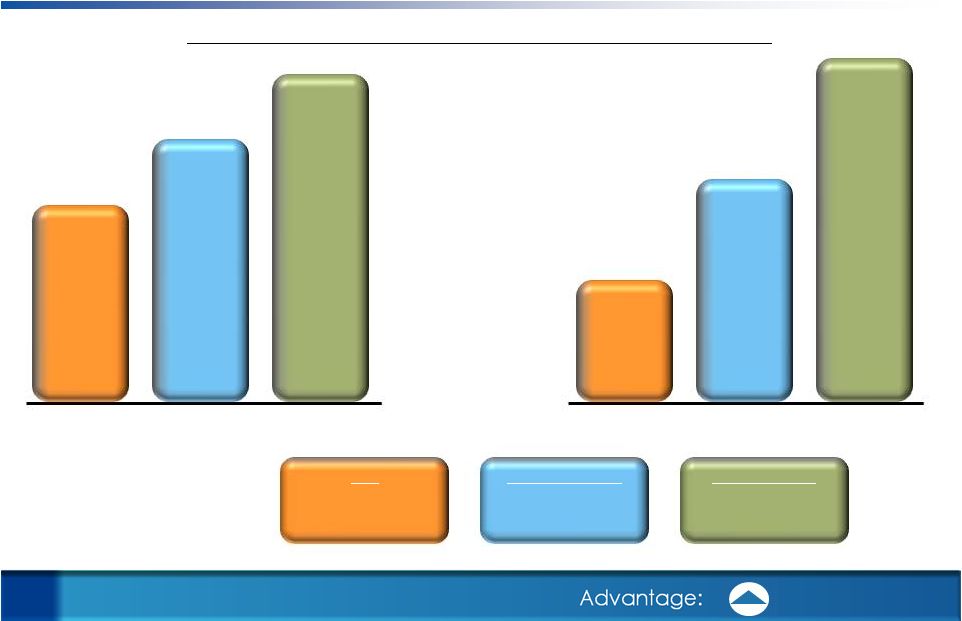

8

Fortune Brands

Home & Security

Sales

are

balanced

across

four

segments,

with

Cabinets

and

Windows

&

Doors

having

above

average

potential

to

leverage

in

a

recovery

while

Plumbing

and

Security

&

Storage

operate

with

higher

returns

across

all

cycles.

We

believe

all

segments

have

the

potential

to

return

to

2006

sales

levels

in

a

full

recovery.

2011 Net Sales by Segment

Net Sales

$ millions

Kitchen &

Bath Cabinetry

38%

Plumbing &

Accessories

29%

Advanced Material

Windows & Door Systems

16%

Security &

Storage

17%

Kitchen & Bath Cabinetry

$2,133

$1,256

Plumbing & Accessories

$1,125

$ 963

Windows & Door Systems

$ 850

$ 553

Security & Storage

$ 586

$ 557

2006

2011 |

9

Fortune Brands

Home & Security

We have a balanced, diverse business mix that is more repair & remodel driven

today; but we expect to see new construction mix grow in a recovery.

International is 17% of sales with Canada 12% and China 3%.

by End

Market* by Channel* *Source:

Company internal estimates for year ended December 31, 2011 Domestic Home Products

Market* 2011 Sales

Repair & Remodel

47%

New Construction

19%

Security & Storage

13%

4%

Commercial

International

17%

Wholesale

29%

Home Centers

29%

Dealer

14%

Other Retail

8%

International

17%

Builder Direct

3%

Repair & Remodel

72%

New

Construction

28% |

10

Fortune Brands

Home & Security

Consumer driven innovation has led to consistently winning profitable new

business and has driven long-term outperformance to the market.

Track

Record

of

Leading

New

Product

Launches

across

All

Business

Segments

Vented Sidelites

New

Glass

Styles

2012

2011

The Original

Adding value for customers and winning

new business

Cabinets:

•

Martha Stewart Living

cabinetry at Home

Depot

stores

in

the

US

and

Canada

•

In-stock cabinetry at Lowe’s

•

Logix

System -

our proprietary tools simplify

organization and storage

Plumbing:

•

Moen’s

MotionSense

for a hands-free

kitchen faucet experience,

Spot Resist

finish,

Reflex

kitchen pull-down system and

the

Twist

multi-function handheld shower

Security & Storage:

•

Master Lock’s

PulseCode

electronic lock and

the

dialSpeed

electronic combination lock

•

Growing Safety and Commercial business

24% of 2011 sales came from products

introduced in the last three years

Kitchen

& Bath

Cabinetry

Plumbing

&

Accessories

Advanced Material

Windows & Door

Systems

Security

&

Storage |

11

Fortune Brands

Home & Security

We have demonstrated growth that has exceeded the market over an

extended period of time and through multiple cycles. Sales performance

reflects both organic growth and acquisitions.

includes housing recessions of ‘90-’91, ‘94-’96,

‘00-’01, ‘06-’11 Sales Growth Rate

1989 2011 FBHS Organic Sales

U.S. Home Products Market

New Construction and

Replace & Remodel

FBHS

GAAP Sales

1

Excludes impact of acquisitions and divestitures.

~2%

4%

9%

1 |

12

Fortune Brands

Home & Security

We quickly and strategically restructured early in the downturn (2007-

2009), and believe our operating platform is more efficient and scalable

to support revenue up to $5B with normal capital spending levels.

Substantially improved cost structures by proactively reducing footprint

nearly 40% from 2006 to 2009 and creating more flexible supply chains

Increased productivity through continuous improvement investments

Maintaining capacity to ramp up with industry-leading service levels and lead times

Can support revenue of up to $5B without capital spending above normal levels

Operating Margin

1

Manufacturing Facilities

Sales:

1

Before charges/gains.

2006

2007

2008

2009

2010

$4.7B

$4.6B

$3.8B

$3.0B

$3.2B

2011

$3.3B

2011

14.4%

12.3%

8.1%

5.8%

4.9%

64

56

47

41

40

38

2.7%

2010

2009

2008

2007

2006 |

13

Fortune Brands

Home & Security

Market Outlook —

We have raised our growth expectations for

the overall housing market from low-single digits to mid-single

digits

based

on

the

broad

firming

that

we

saw

in

the

1

quarter.

Growth Rate Assumption:

4%

Mid-to-High Teens

Mid-Single Digits

Initial

January

Updated

April

1-2%

Mid-Single Digits

2%

Replace & Remodel Market:

New Construction Market:

FBHS Market:

st |

14

Fortune Brands

Home & Security

Growth opportunities initially reflect significant organic growth…but we are also focused

beyond the recovery, as we look for opportunities to leverage cash and a strong balance

sheet to expand into new markets and adjacent categories and return cash to

shareholders. “Capitalize on the Recovery”

-Organic Growth through Home Recovery

and the Impact of Share Gains

“Sustain Growth Beyond the Recovery”

-Market Expansion and Acquisitions with

Free Cash Flow and Capital Structure

Leverage brand building and consumer driven

innovation

Continue to gain market share and expand into

new channels

Drive organic international market growth

Continue to refine to our operating platform

Accelerate investment in market expansion

internationally for some segments

Acquire

to

expand

in

adjacent

markets

–

both

domestically and globally

Return cash to shareholders through some

combination of dividends and/or share

repurchases

Time |

15

Fortune Brands

Home & Security

While the housing market slump has significantly reduced sales and profit, we believe the

business is positioned to return to previous levels when the housing market recovers. The

benefits of the more efficient operating platform should offset a potentially leaner

product mix. $ millions

2

Including incremental standalone corporate expenses.

Net Sales

$4,694

$3,007

$3,234

$3,329

% Growth

13%

(20%)

8%

3%

Operating Income

1

$ 678

$ 81

$ 187

$ 163

% Operating Margin

1

14%

3%

6%

5%

EBITDA

1

$ 826

$ 195

$ 296

$ 261

% EBITDA Margin

1

18%

6%

9%

8%

Unlevered Free Cash Flow

2

$ 464

$ 280

$ 146

$ 130

1

Before charges/gains.

2011

2010

2009

2006

Fiscal Year Ending December 31 |

16

Fortune Brands

Home & Security

2012 is off to a solid start as we outperformed a market

that was stronger than anticipated.

$ millions, except EPS

Net Sales

$799

$715

12%

Market Growth

4%

Operating Income

$21

$3

533%

EBITDA

$45

$28

62%

% EBITDA Margin

6%

4%

EPS

$0.08

$0.00

2

Before charges/gains.

1

Company internal estimate of growth in the market for our home products.

1

2

2

2

2

2012

2011

% Change

Fiscal Q1 Ending March 31 |

17

Fortune Brands

Home & Security

Flexible capital structure through a strong balance sheet and cash flow

should result in reduced risk and fuel incremental opportunities.

$ millions

Capital Structure:

(as of 3/31/12)

Term Loan

$350

Revolver ($650 facility)

70

Subsidiary Debt

11

Total Debt

$431

Net Debt/EBITDA

(as of 3/31/12)

1.1x

Balance

Sheet

Statistics:

(as

of

3/31/12)

Assets

$3,648

Total

Debt

431

Total

Liabilities

1,464

Equity

2,184

Trailing

12

Month

EBITDA

278

Debt-to-Capital

~16% |

18

Fortune Brands

Home & Security

We raised our 2012 full year outlook based on an improved market

assumption, and we plan to continue to meaningfully outperform our market.

1

Before charges/gains.

EPS:

$0.77 –

$0.87

1

Net Sales:

High-Single Digit Growth

FBHS Market Assumption:

Mid-Single Digit Growth

Overall Housing Market Assumption:

Mid-Single Digit Growth |

19

Fortune Brands

Home & Security

Longer term, we do not expect organic growth to be dependent on a full

market recovery for solid returns and cash flow, although returning to

“steady state”

is very attractive.

Potential Organic Market Recovery Scenarios

Operating Income

1

$200

$450

$700+

1

Before charges/gains.

Sales

Annual $ in B

$3

$4

$5

EBITDA

Annual $ in M

$300

$550

$800+

flat

~600,000

~0%

mid-recovery

~1,000,000

~3 –

4%

steady state

~1,500,000

~5 –

6%

Housing Starts

R&R Growth

1 |

20

Fortune Brands

Home & Security

Free Cash Flow¹

Maintain 1.25x

Debt/EBITDA

Potential cash

available to drive

shareholder

value

Strong

cumulative

free

cash

flow

plus

maintaining

an

appropriate

debt

level

over

a

hypothetical

5-year

“steady

state”

recovery

cycle

could

fuel

exceptional value-creation opportunities.

$2.0B+

$1.4B

$600M+

1

Free cash flow is cash flow from operations less net capital expenditures plus proceeds from

the exercise of stock options. |

21

Fortune Brands

Home & Security

Continue to invest in current businesses

-

products, markets, brands, supply chains

Return cash to shareholders

-

share buybacks and/or dividends

Pursue accretive acquisitions

In addition to investing in organic growth, we plan to use cash flow to create

additional returns and maximize shareholder value. The magnitude of potential

cash available could result in use of any or all of these strategies.

Primary focus on core categories

Fit within our market

attractiveness criteria

Ability to leverage existing capabilities,

market positions and structure

Good companies to be made great,

not turnarounds

New home & security categories

under two conditions:

–

Truly differentiated leader

with a capable management team

–

Clear path for organic growth

Acquisition Criteria |

22

Fortune Brands

Home & Security

Long-term

Value

Creation

We believe our solid business model, growing free cash flow and strong

capital structure will create long-term shareholder value, both as the

market recovers and beyond the recovery.

Attractive Product Categories

Consumer Driven Innovation

Operational and Management Excellence

Demonstrated Ability to Outperform the Market

Strong Capital Structure

Free Cash Flow

Leverage Capital Structure

Market Recovery

Share Gains

Solid Business Model

Organic Growth

Incremental Growth

$ |

Thank You

Advantage:

Fortune Brands

Home & Security |

Reconciliation of FBHS Net Sales Growth Rate to FBHS Organic Sales Growth

| Home & Security |

||||

| 1989-2011 Projected |

||||

| CAGR* |

||||

| Net sales growth (GAAP) |

9% | |||

| Net impact of acquisitions/divestitures |

(5)% | |||

|

|

|

|||

| Organic sales growth |

4% | |||

|

|

|

|||

* Compounded annual growth rate

Organic sales growth is the rate of compound annual net sales growth from 1989 through 2011, excluding the impact of acquisitions and divestitures. Organic sales growth is not a measure derived in accordance with GAAP. Management believes this measure provides useful supplemental information regarding the underlying level of sales growth. This measure may be inconsistent with similar measures presented by other companies.

Reconciliation of Operating Income before charges/gains to GAAP Operating Income (Loss)

| 2006 | 2009 | 2010 | 2011 | Q1 2011 | Q1 2012 | % change | ||||||||||||||||||||||

| (in millions) |

||||||||||||||||||||||||||||

| Operating income before charges/gains (1) |

$ | 678 | $ | 81 | $ | 187 | $ | 163 | $ | 3 | $ | 21 | 533 | % | ||||||||||||||

| Standalone corporate expenses (2) |

20 | 20 | 20 | 14 | 5 | — | (100 | )% | ||||||||||||||||||||

| Restructuring and other charges (3) |

(26 | ) | (52 | ) | (13 | ) | (20 | ) | (0 | ) | (2 | ) | 300 | % | ||||||||||||||

| Contingent acquisition consideration adjustment (4) |

— | — | — | — | — | 2 | — | |||||||||||||||||||||

| Business separation costs (5) |

— | — | — | (3 | ) | — | — | — | ||||||||||||||||||||

| Asset impairment charges |

— | — | — | (90 | ) | — | — | — | ||||||||||||||||||||

| Defined benefit plan accounting change (6) |

0 | 5 | 4 | (80 | ) | — | — | — | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| GAAP operating income (loss) |

$ | 672 | $ | 54 | $ | 198 | $ | (16 | ) | $ | 8 | $ | 21 | 170 | % | |||||||||||||

| (1) | Operating income before charges/gains is GAAP operating income (loss) adjusted to (i) exclude actuarial gains (losses) associated with the Company’s defined benefit plans, (ii) exclude asset impairment charges, (iii) exclude restructuring and other charges (iv) exclude business separation costs, (v) exclude income from a contingent acquisition consideration adjustment and (vi) include stand-alone corporate costs for the periods preceding the separation of the Company from Fortune Brands, Inc. Operating income before charges/gains is a measure not derived in accordance with GAAP. Management uses this measure to determine the returns generated by the Company and to evaluate and identify cost-reduction initiatives. Management believes this measure provides investors with helpful supplemental information regarding the underlying performance of the Company from year to year. This measure may be inconsistent with similar measures presented by other companies. |

| (2) | The Company estimates that it would have incurred approximately $14 million of incremental corporate expenses if it had functioned as an independent standalone public company for the twelve months ended December 31, 2011, approximately $20 million for each of the prior years and approximately $5 million in the three months ended March 31, 2011. |

| (3) | Restructuring charges are costs incurred to implement significant cost reduction initiatives and include workforce reduction costs and asset write-downs; “other charges” represent charges directly related to restructuring initiatives that cannot be reported as restructuring under GAAP. Such costs may include losses on disposal of inventories, trade receivables allowances from exiting product lines and accelerated depreciation resulting from the closure of facilities. |

| (4) | Represents gain attributable to reduction of estimated liability for contingent consideration associated with a business acquisition. |

| (5) | Business separation costs are costs related to non-cash non-recurring costs associated with the modification of share-based compensation awards as a result of the spin-off of the Company from Fortune Brands, Inc. |

| (6) | Defined benefit plan accounting change represents the impact on defined benefit plan expense of the actuarial gains (losses) associated with the Company’s defined benefit plans. |

Reconciliation of Before charges/gains Operating Margin to GAAP Operating Margin

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | |||||||||||||||||||

| Before charges/gains operating margin (1) |

14.4 | % | 12.3 | % | 8.1 | % | 2.7 | % | 5.8 | % | 4.9 | % | ||||||||||||

| Standalone corporate expenses (2) |

0.4 | % | 0.4 | % | 0.5 | % | 0.7 | % | 0.6 | % | 0.4 | % | ||||||||||||

| Restructuring and other charges (3) |

(0.6 | )% | (2.0 | )% | (1.5 | )% | (1.7 | )% | (0.4 | )% | (0.6 | )% | ||||||||||||

| Business separation costs (4) |

— | — | — | — | — | (0.1 | )% | |||||||||||||||||

| Asset impairment charges |

— | — | (22.6 | )% | — | — | (2.7 | )% | ||||||||||||||||

| Defined benefit plan accounting change (5) |

0.0 | % | 0.2 | % | (2.6 | )% | 0.2 | % | 0.1 | % | (2.4 | )% | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| GAAP operating margin |

14.3 | % | 10.9 | % | (18.0 | )% | 1.8 | % | 6.1 | % | (0.5 | )% | ||||||||||||

| (1) | Before charges/gains operating margin is operating margin derived in accordance with GAAP adjusted to (i) exclude actuarial gains (losses) associated with the Company’s defined benefit plans, (ii) exclude asset impairment charges, (iii) exclude restructuring and other charges (iv) exclude business separation costs, (v) exclude income from a contingent acquisition consideration adjustment and (vi) include stand-alone corporate costs for the periods preceding the separation of the Company from Fortune Brands, Inc. Before charges/gains operating margin is a measure not derived in accordance with GAAP. Management uses this measure to determine the returns generated by the Company and to evaluate and identify cost-reduction initiatives. Management believes this measure provides investors with helpful supplemental information regarding the underlying performance of the Company from year to year. This measure may be inconsistent with similar measures presented by other companies. |

| (2) | The Company estimates that it would have incurred approximately $14 million of incremental corporate expenses if it had functioned as an independent standalone public company for the twelve months ended December 31, 2011, approximately $20 million for each of the prior years and approximately $5 million in the three months ended March 31, 2011. |

| (3) | Restructuring charges are costs incurred to implement significant cost reduction initiatives and include workforce reduction costs and asset write-downs; “other charges” represent charges directly related to restructuring initiatives that cannot be reported as restructuring under GAAP. Such costs may include losses on disposal of inventories, trade receivables allowances from exiting product lines and accelerated depreciation resulting from the closure of facilities. |

| (4) | Business separation costs are costs related to non-cash non-recurring costs associated with the modification of share-based compensation awards as a result of the spin-off of the Company from Fortune Brands, Inc. |

| (5) | Defined benefit plan accounting change represents the impact on defined benefit plan expense of the actuarial gains (losses) associated with the Company’s defined benefit plans. |

Reconciliation of EBITDA Before Charges/Gains to GAAP Net Income (in millions)

| 2006 | 2009 | 2010 | 2011 | |||||||||||||

| EBITDA before charges/gains(1) |

$ | 826 | $ | 195 | $ | 296 | $ | 261 | ||||||||

| Depreciation(2) |

(105 | ) | (97 | ) | (92 | ) | (86 | ) | ||||||||

| Amortization of intangible assets |

(30 | ) | (16 | ) | (16 | ) | (14 | ) | ||||||||

| Restructuring and other charges(3) |

(26 | ) | (52 | ) | (13 | ) | (20 | ) | ||||||||

| Contingent acquisition consideration adjustment(4) |

— | — | — | — | ||||||||||||

| Business separation costs (5) |

— | — | — | (3 | ) | |||||||||||

| Related party interest expense, net |

(169 | ) | (85 | ) | (116 | ) | (23 | ) | ||||||||

| External interest expense |

(1 | ) | (0 | ) | (0 | ) | (3 | ) | ||||||||

| Standalone corporate expenses (6) |

20 | 20 | 20 | 14 | ||||||||||||

| Asset impairment charges |

— | — | — | (90 | ) | |||||||||||

| Defined benefit plan accounting change(7) |

0 | 5 | 4 | (80 | ) | |||||||||||

| Income tax (provision) benefit |

(180 | ) | (8 | ) | (18 | ) | 9 | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) |

$ | 335 | $ | (38 | ) | $ | 65 | $ | (35 | ) | ||||||

| Noncontrolling interests |

(1 | ) | (1 | ) | (1 | ) | (1 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) attributable to Home & Security |

$ | 334 | $ | (39 | ) | $ | 64 | $ | (36 | ) | ||||||

| Q1 2011 | Q1 2012 | % change |

TTM Q1 2012 | |||||||||||||

| EBITDA before charges/gains(1) |

$ | 28 | $ | 45 | 62% | $ | 278 | |||||||||

| Depreciation(2) |

(21 | ) | (21 | ) | 0% | (86 | ) | |||||||||

| Amortization of intangible assets |

(4 | ) | (3 | ) | (19)% | (13 | ) | |||||||||

| Restructuring and other charges(3) |

(0 | ) | (2 | ) | 0% | (22 | ) | |||||||||

| Contingent acquisition consideration adjustment(4) |

— | 2 | — | 2 | ||||||||||||

| Business separation costs (5) |

— | — | — | (3 | ) | |||||||||||

| Related party interest expense, net |

(23 | ) | — | (100)% | — | |||||||||||

| External interest expense |

(0 | ) | (2 | ) | — | (5 | ) | |||||||||

| Standalone corporate expenses (6) |

5 | — | (100)% | 9 | ||||||||||||

| Asset impairment charges |

— | — | — | (90 | ) | |||||||||||

| Defined benefit plan accounting change(7) |

— | — | — | (80 | ) | |||||||||||

| Income tax (provision) benefit |

5 | (6 | ) | (228)% | (2 | ) | ||||||||||

|

|

|

|

|

|

|

|

||||||||||

| Net income (loss) |

$ | (10 | ) | $ | 13 | (231)% | $ | (12 | ) | |||||||

| Noncontrolling interests |

(0 | ) | (0 | ) | 100% | (1 | ) | |||||||||

|

|

|

|

|

|

|

|

||||||||||

| Net income (loss) attributable to Home & Security |

$ | (10 | ) | $ | 13 | (225)% | $ | (13 | ) | |||||||

| (1) | EBITDA before charges/gains is net income (loss) derived in accordance with GAAP adjusted to (i) exclude depreciation, (ii) exclude amortization of intangible assets, (iii) exclude restructuring and other charges, (iv) exclude income from a contingent acquisition consideration adjustment, (v) exclude business separation costs, (vi) exclude related party interest expense, net, (vi) exclude external interest expense, (viii) exclude asset impairment charges, (ix) exclude actuarial gains (losses) associated with the Company’s defined benefit plans, (x) exclude income taxes, and (xi) include stand-alone corporate costs for the periods preceding the separation of the Company from Fortune Brands, Inc. EBITDA before charges/gains is a measure not derived in accordance with GAAP. Management uses this measure to assess returns generated by the Company. Management believes this measure provides investors with helpful supplemental information about the Company’s ability to fund internal growth, make acquisitions and repay debt and related interest. This measure may be inconsistent with similar measures presented by other companies. |

| (2) | Depreciation excludes accelerated depreciation included in restructuring and other charges. |

| (3) | Restructuring charges are costs incurred to implement significant cost reduction initiatives and include workforce reduction costs and asset writ downs; “other charges” represent charges directly related to restructuring initiatives that cannot be reported as restructuring under GAAP. Such costs may include losses on disposal of inventories, trade receivables allowances from exiting product lines and accelerated depreciation resulting from the closure of facilities. |

| (4) | Represents gain attributable to reduction of estimated liability for contingent consideration associated with a business acquisition. |

| (5) | Business separation costs are costs related to non-cash non-recurring costs associated with the modification of share-based compensation awards as a result of the spin-off of the Company from Fortune Brands, Inc. |

| (6) | The Company estimates that it would have incurred approximately $14 million of incremental corporate expenses if it had functioned as an independent standalone public company for the twelve months ended December 31, 2011, approximately $20 million for each of the prior years and approximately $5 million in the three months ended March 31, 2011. |

| (7) | Defined benefit plan accounting change represents the impact on defined benefit plan expense of the actuarial gains (losses) associated with the Company’s defined benefit plans. |

Reconciliation of Before charges/gains EBITDA margin to GAAP Net Income margin

| 2006 | 2009 | 2010 | 2011 | Q1 2011 | Q1 2012 | |||||||||||||||||||

| Before charges/gains EBITDA margin (1) |

18 | % | 6 | % | 9 | % | 8 | % | 4 | % | 6 | % | ||||||||||||

| Depreciation (2) |

(2 | %) | (3 | %) | (3 | %) | (3 | %) | (3 | %) | (3 | %) | ||||||||||||

| Amortization of intangible assets |

(1 | %) | (1 | %) | (0 | %) | (0 | %) | (1 | %) | (0 | %) | ||||||||||||

| Restructuring and other charges (3) |

(1 | %) | (2 | %) | (0 | %) | (1 | %) | (0 | %) | (0 | %) | ||||||||||||

| Contingent acquisition consideration adjustment (4) |

— | — | — | — | — | 0 | % | |||||||||||||||||

| Business separation costs (5) |

— | — | — | (0 | ) | 0 | % | — | ||||||||||||||||

| Related party interest expense, net |

(4 | %) | (3 | %) | (4 | %) | (1 | %) | (3 | %) | 0 | % | ||||||||||||

| External interest expense |

(0 | %) | (0 | %) | (0 | %) | (0 | %) | (0 | %) | (0 | %) | ||||||||||||

| Standalone corporate expenses (6) |

0 | % | 1 | % | 1 | % | 0 | % | 1 | % | — | |||||||||||||

| Asset impairment charges |

— | — | — | (3 | %) | — | — | |||||||||||||||||

| Defined benefit plan accounting change (7) |

0 | % | 0 | % | 0 | % | (2 | %) | — | — | ||||||||||||||

| Income tax (provision) benefit |

(4 | %) | (0 | %) | (1 | %) | 0 | % | 1 | % | (1 | %) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| GAAP Net income (loss) margin |

7 | % | (1 | %) | 2 | % | (1 | %) | (1 | %) | 2 | % | ||||||||||||

| (1) | Before charges/gains EBITDA margin is net income (loss) derived in accordance with GAAP adjusted to (i) exclude depreciation, (ii) exclude amortization of intangible assets, (iii) exclude restructuring and other charges, (iv) exclude income from a contingent acquisition consideration adjustment, (v) exclude business separation costs, (vi) exclude related party interest expense, net, (vi) exclude external interest expense, (viii) exclude asset impairment charges, (ix) exclude actuarial gains (losses) associated with the Company’s defined benefit plans, (x) exclude income taxes, and (xi) include stand-alone corporate costs for the periods preceding the separation of the Company from Fortune Brands, Inc. EBITDA before charges/gains is a measure not derived in accordance with GAAP. Management uses this measure to assess returns generated by the Company. Management believes this measure provides investors with helpful supplemental information about the Company’s ability to fund internal growth, make acquisitions and repay debt and related interest. This measure may be inconsistent with similar measures presented by other companies. |

| (2) | Depreciation excludes accelerated depreciation included in restructuring and other charges. |

| (3) | Restructuring charges are costs incurred to implement significant cost reduction initiatives and include workforce reduction costs and asset write-downs; “other charges” represent charges directly related to restructuring initiatives that cannot be reported as restructuring under GAAP. Such costs may include losses on disposal of inventories, trade receivables allowances from exiting product lines and accelerated depreciation resulting from the closure of facilities. |

| (4) | Represents gain attributable to reduction of estimated liability for contingent consideration associated with a business acquisition. |

| (5) | Business separation costs are costs related to non-cash non-recurring costs associated with the modification of share-based compensation awards as a result of the spin-off of the Company from Fortune Brands, Inc. |

| (6) | The Company estimates that it would have incurred approximately $14 million of incremental corporate expenses if it had functioned as an independent standalone public company for the twelve months ended December 31, 2011, approximately $20 million for each of the prior years and approximately $5 million in the three months ended March 31, 2011. |

| (7) | Defined benefit plan accounting change represents the impact on defined benefit plan expense of the actuarial gains (losses) associated with the Company’s defined benefit plans. |

Reconciliation of Unlevered Free Cash Flow to GAAP Cash Flow from Operations

(in millions)

| 2006 | 2009 | 2010 | 2011 | |||||||||||||

| Unlevered Free Cash Flow |

$ | 464 | $ | 280 | $ | 146 | $ | 130 | ||||||||

| Add: |

||||||||||||||||

| Capital Expenditures |

128 | 43 | 58 | 68 | ||||||||||||

| Standalone corporate expenses, net of tax |

13 | 13 | 13 | 9 | ||||||||||||

| Less: |

||||||||||||||||

| Proceeds from the disposition of assets |

11 | 11 | 3 | 4 | ||||||||||||

| Related party interest expense, net of tax |

110 | 56 | 75 | 15 | ||||||||||||

| External interest expense, net of tax |

0 | 0 | 0 | 2 | ||||||||||||

| Proceeds from the exercise of stock options |

— | — | — | 11 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Cash flow from operations |

$ | 484 | $ | 269 | $ | 139 | $ | 175 | ||||||||

Unlevered free cash flow is cash flow from operations (i) less net capital expenditures (capital expenditures less proceeds from the sale of assets including property, plant and equipment) and estimated incremental standalone corporate expenses, net of tax, (ii) plus related party interest expense, net of tax, external interest expense, net of tax, and proceeds from the exercise of stock options. In computing unlevered free cash flow, net of tax reconciling items assume an income tax rate of 35%. Unlevered free cash flow is a measure not derived in accordance with GAAP. Management believes that unlevered free cash flow provides investors with helpful supplemental information about the Company’s ability to fund internal growth, make acquisitions, repay debt and related interest, pay dividends, and repurchase common stock. This measure may be inconsistent with similar measures presented by other companies.

DILUTED EPS BEFORE CHARGES/GAINS RECONCILIATION

Diluted EPS before charges/gains is net income (loss) calculated on a diluted per-share basis adjusted to reflect the borrowing arrangements and debt levels that actually existed immediately after the separation of the Company from Fortune Brands, Inc. as of October 4, 2011, the 1:1 share distribution resulting from the separation of the Company from Fortune Brands, Inc., standalone corporate costs and an adjusted pro forma effective tax rate of 35% and excludes restructuring and other charges and income from a contingent acquisition consideration adjustment.

For the first quarter of 2012, diluted EPS before charges/gains is net income calculated on a per-share basis excluding $1.6 million ($1.1 million after tax or $0.01 per diluted share) of restructuring and other charges, and income from a contingent acquisition consideration of $2.0 million ($1.3 million after tax or $0.01 per diluted share).

For the first quarter of 2011, diluted EPS before charges/gains is net income calculated on a per-share basis excluding $0.5 million ($0.3 million after tax) of restructuring and other charges, standalone corporate costs of $5.0 million ($3.1 million after tax or $0.02 per diluted share), capital structure changes of $19.8 million ($12.3 million after tax or $0.08 per diluted share), and an adjusted pro forma tax rate adjustment of $1.0 million ($0.01 per diluted share).

Diluted EPS before charges/gains is a measure not derived in accordance with GAAP. Management uses this measure to evaluate the overall performance of the Company and believes this measure provides investors with helpful supplemental information regarding the underlying performance of the Company from period to period. This measure may be inconsistent with similar measures presented by other companies.

| Three Months Ended March 31, | ||||||||||||

| 2012 | 2011 | % Change | ||||||||||

| Earnings Per Common Share - Diluted |

||||||||||||

| EPS Before Charges/Gains |

$ | 0.08 | $ | — | — | |||||||

| Restructuring and other charges |

(0.01 | ) | — | — | ||||||||

| Contingent acquisition consideration adjustment |

0.01 | — | — | |||||||||

| Standalone corporate costs |

— | 0.02 | (100.0 | ) | ||||||||

| Capital structure change |

— | (0.08 | ) | 100.0 | ||||||||

| Adjusted pro forma tax rate adjustment |

— | (0.01 | ) | 100.0 | ||||||||

|

|

|

|

|

|

|

|||||||

| Diluted EPS (GAAP) |

$ | 0.08 | $ | (0.07 | ) | 214.3 | ||||||

RECONCILIATION OF FULL YEAR 2012 EARNINGS GUIDANCE TO GAAP

For the full year, the Company is targeting diluted EPS before charges/gains to be in the range of $0.77 to $0.87 per share. On a GAAP basis, the Company is targeting diluted EPS to be in the range of $0.76 to $0.86 per share.