Attached files

| file | filename |

|---|---|

| 8-K - 8-K - FIFTH THIRD BANCORP | d348485d8k.htm |

©

Fifth Third Bank | All Rights Reserved

Exhibit 99.1

UBS Global Financial Services Conference

Kevin T. Kabat

President & Chief Executive Officer

May 8, 2012

Please refer to earnings release dated April 19, 2012 for further information.

|

2

©

Fifth Third Bank | All Rights Reserved

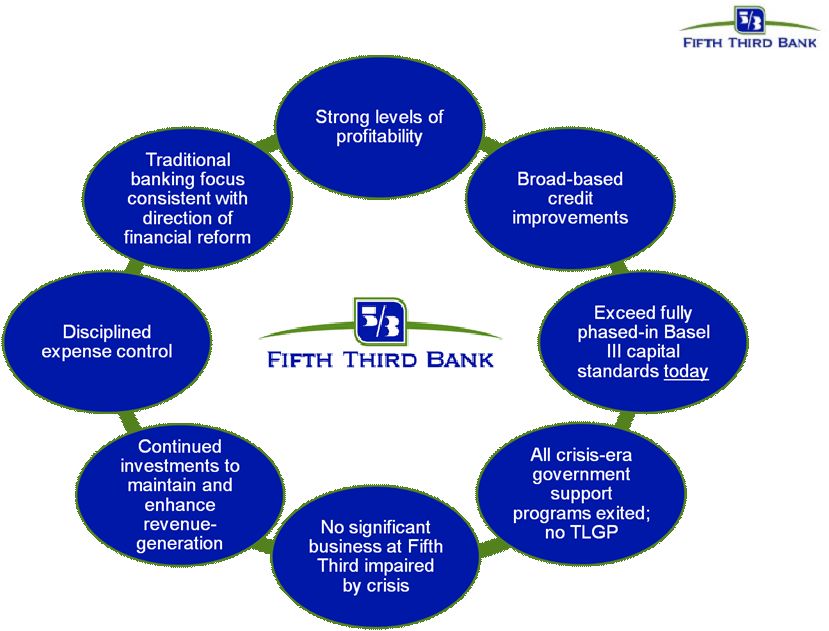

Well-positioned for success and leadership in new banking landscape

Key themes |

3

©

Fifth Third Bank | All Rights Reserved

Environment characterized by low growth

expectations and low interest rates

•

Prolonged low-rate environment, coupled

with modest economic growth

•

Lower securities reinvestment yields on

portfolio cash flows

•

Strong deposit flows

•

Competitive dynamics

•

Elevated mortgage refinance activity

•

Firms facing significant litigation related to:

–

Mortgage securitizations

–

GSE repurchases

–

Private label mortgage repurchases

•

Concerns about European banks and

sovereign debt

•

Higher capital standards; limitations on

dividend payout ratios; capital building

beyond targeted / required levels

•

Continued strong loan production

–

Rates on loan originations relatively stable

•

Careful management of liability costs

–

Disciplined pricing on deposits

–

Continued evaluation of term liabilities

including TruPS

•

Strong mortgage banking results

•

Mortgage risks manageable

–

Quarterly mortgage repurchase costs

~$20mm; claims inventory has declined

–

Total

mortgage securitizations outstanding

$19mm (2003 HELOC and performing well)

•

No direct European sovereign exposure

–

Total exposure to European peripheral

borrowers <$0.2bn*

–

Total exposure to European banks <$0.1bn

•

Strong profitability and capital in excess of

fully

phased-in

Basel

III

standards

today

–

2012 CCAR** plan to increase distributions

Fifth Third is well-positioned to deal with current environmental

challenges Characteristics of current environment

Fifth Third’s response / position

* Greece, Ireland, Italy, Portugal, Spain

** Comprehensive Capital Analysis & Review by Federal Reserve; subject to Board

of Directors and regulatory approval. |

4

©

Fifth Third Bank | All Rights Reserved

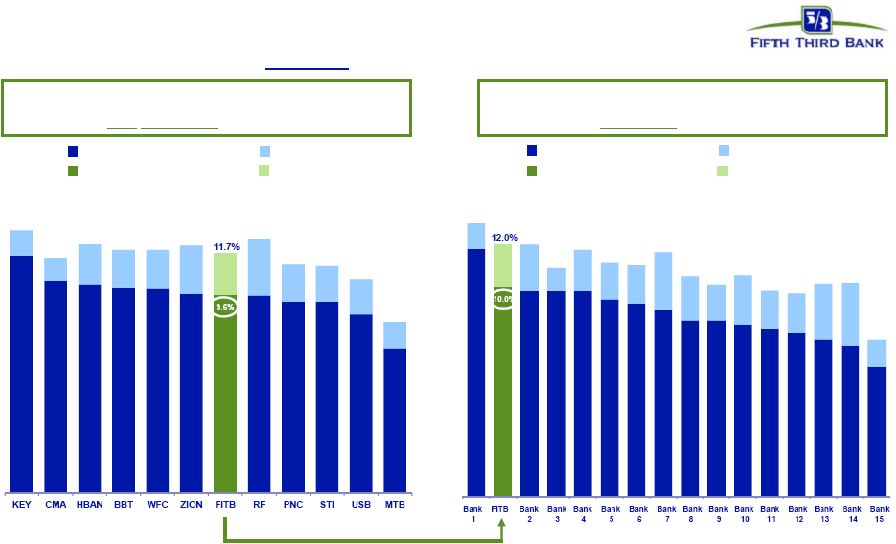

Balance sheet growth mitigates rate environment

Commercial Loan Growth^ ($bn)

Consumer Loan Growth^ ($bn)

•

Sustained growth in commercial loans driven by C&I

–

Growth is geographically diverse and across number

of industry segments, particularly manufacturing

•

Commercial line utilization stable at 32%; potential

source of future growth

•

CRE portfolio run-off at slowing rate, with modest

selective current origination volume

•

Consumer loan growth driven by auto and in-branch

mortgage originations

–

Managing auto volumes to ensure appropriate

returns; spread pressure due to competition

–

Branch mortgage refi product has FICO over 780, LTV

~60% and avg. term ~17 years while yielding above

market rates due to process convenience

^ Excluding loans held-for-sale

* Excludes CMA and PNC due to large acquisitions

Peer Banks include BBT, CMA, HBAN, KEY, MTB, PNC, RF, STI, USB, WFC, ZION. Source:

SNL Financial and Company Reports. EOP quarterly C&I loan growth^

•

C&I loans as a percent of total commercial loans was

68% at 1Q12 versus peer average of 61%

•

Year-over-year C&I growth 18% versus peer median of

12%* |

5

©

Fifth Third Bank | All Rights Reserved

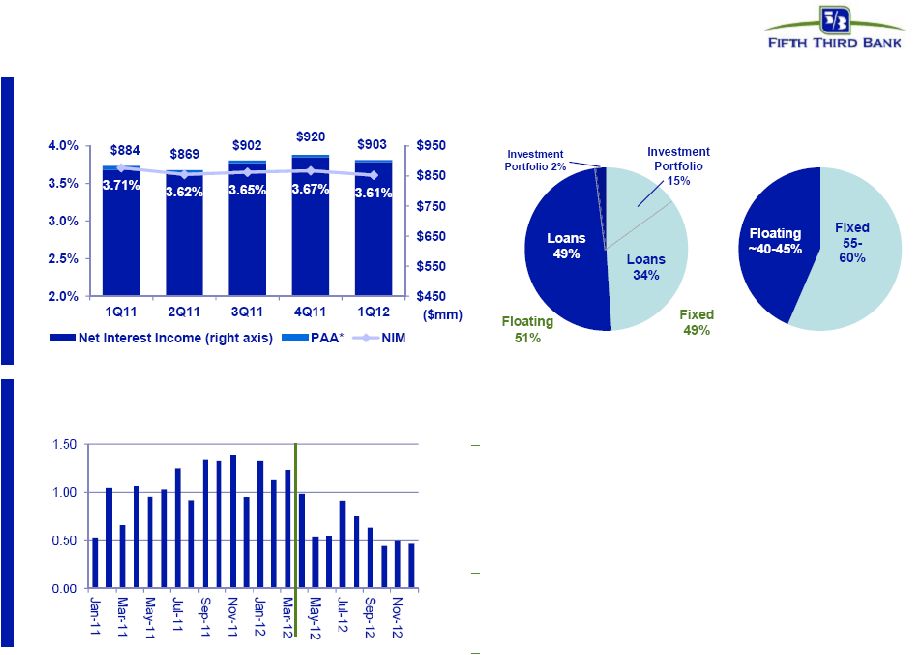

Rate of NIM pressure declining

* Represents purchase accounting adjustments included in net interest income.

^ Estimate; funding (DDAs + interest-bearing liabilities); liabilities

attributed to fixed or floating using terms and expected beta

Fixed / Floating Portfolio

•

Modest natural asset sensitivity creates near-

term NIM pressure but we expect it to be

manageable

~50% of assets, ~40-45% of funding

variable in nature

•

Coupons on new originations of variable rate

assets consistent with portfolio weighted

average coupons

Emphasis on variable rate C&I lending

•

Coupons on new fixed rate originations

converging with portfolio average coupons

Fixed rate securities only 15% earning

assets

Interest-Earning

Assets

Funding^

NII and NIM (FTE)

Trend: fixed rate origination coupons

relative to fixed portfolio weighted avg |

6

©

Fifth Third Bank | All Rights Reserved

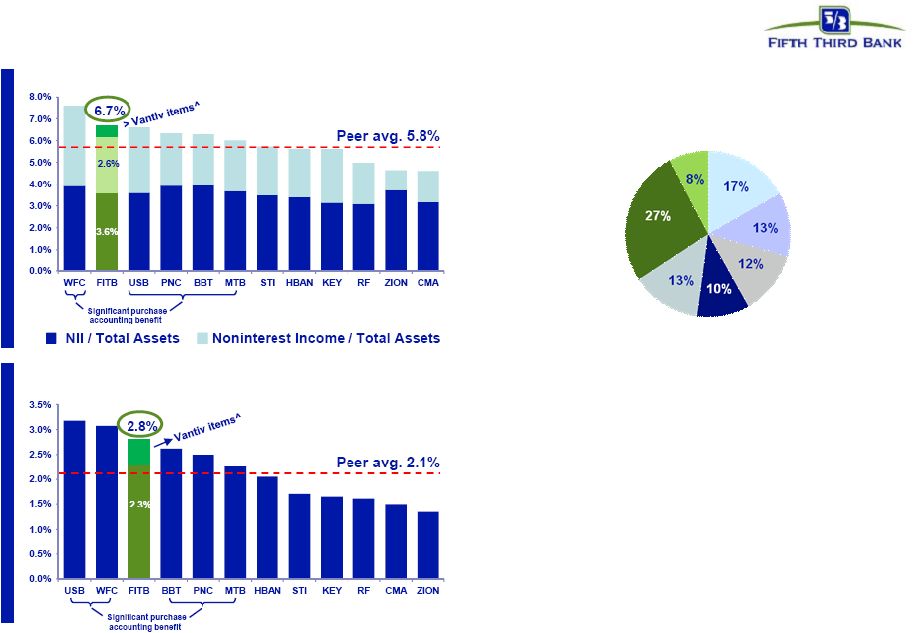

Strong revenue and profit generation

Source: SNL Financial and Company Reports.

* Non-GAAP measure. See Reg. G reconciliation in the Appendix to the

presentation. ^ ~50 bps of Vantiv items in noninterest income include $115mm

gains from Vantiv’s IPO, ~$36mm charge related to Vantiv's debt refinancing, and $46mm positive valuation adjustment on the

Vantiv warrant and put option.

Revenue / Avg. Int. Earning Assets

PPNR* / Avg. Int. Earning Assets

Deposit fees

Corporate

banking

Investment

advisors

Other

Mortgage

Card &

Processing

Fee Income Distribution

Vantiv^

•

Business mix provides higher than

average diversity among spread and

fee revenues (40+% of revenue)

•

Relatively strong margin and

relatively high fee income

contribution drives strong revenue

and PPNR generation profitability

•

Profitability remains strong despite

sluggish economy |

7

©

Fifth Third Bank | All Rights Reserved

Customer oriented solutions

•

Broad suite of product offerings with distinct value propositions appealing to

various customer segments

•

Implementation of new products, like DUO Card, Real Life Rewards, Relationship

Savings •

Letting customers choose how to pay for products and services they use

•

More straightforward, simpler suite of consumer deposit products

Providing customers with products and services they find valuable

•

Negative impact from debit interchange legislation and Reg E in run-rates

•

Initial impact of debit interchange legislation (~$30mm per quarter) expected to be

mitigated over time; implementing carefully and deliberately through various

actions, including: –

Reduced costs associated with debit card offerings; changes and eliminations of

reward programs

–

Incorporation of debit usage into bundled deposit product offerings

–

Adjustment of product and fee structures relative to services provided

–

Charge card alternatives

–

Implementation of new products

Deliberate and multi-pronged approach to mitigation of regulatory / legislative

impacts •

In-depth discussions with customers to determine what matters most to them

•

Actively seeking input and feedback from customer base and prospective

customers •

Working carefully to ensure we align value to the customer with value to us

Listening to the voice of our customers |

8

©

Fifth Third Bank | All Rights Reserved

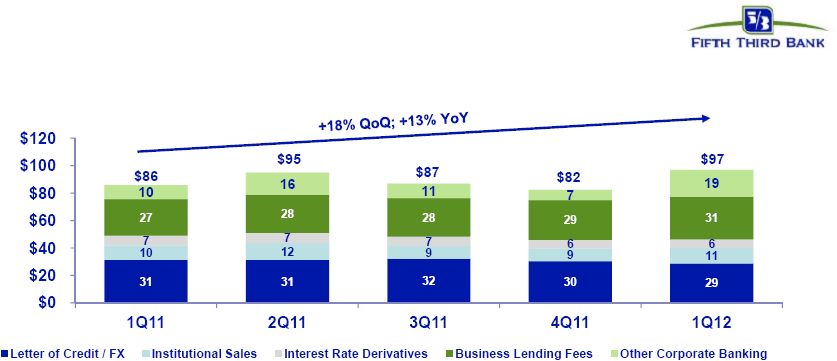

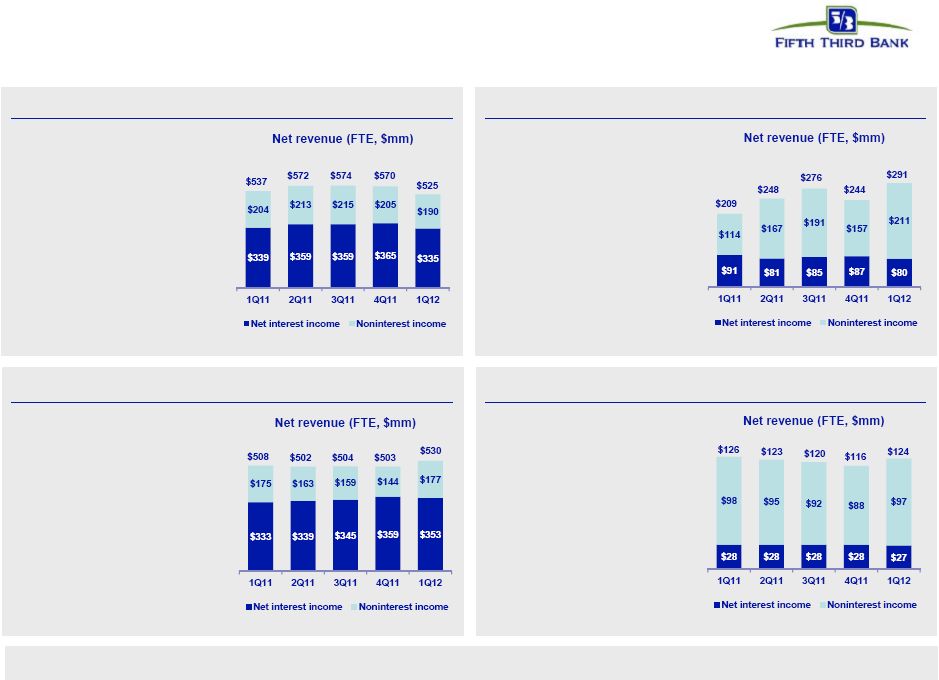

Momentum building in corporate banking

Corporate banking revenue ($mm)

•

Syndication fee revenue up

150% from 1Q11; fees from

lead transactions up 260%

from 1Q11 largely due to 11

lead syndications

transactions closed during

1Q12

•

Average fees on lead

transactions of ~$1mm in

1Q12 vs <$500k in 2011

Mid-corporate opportunity

•

Target clients: businesses

that generate $200mm to

$2B in revenue

•

Hired 20+ bankers in the

past 6 months

–

Have generated $1.2B in

committed credit and

more than $400mm in

funded loans

•

Cash-centric retail locations such as

quick service restaurants, convenience

stores, and specialty stores

•

Simplifies cash handling; improves cash

flow

•

Automates and streamlines account

reconciliation

•

Decreases employee theft (risk

management)

•

RCM locations have doubled since 2009,

with more than 6,400 locations as of

3/31/12

Syndications

Remote Currency Manager |

9

©

Fifth Third Bank | All Rights Reserved

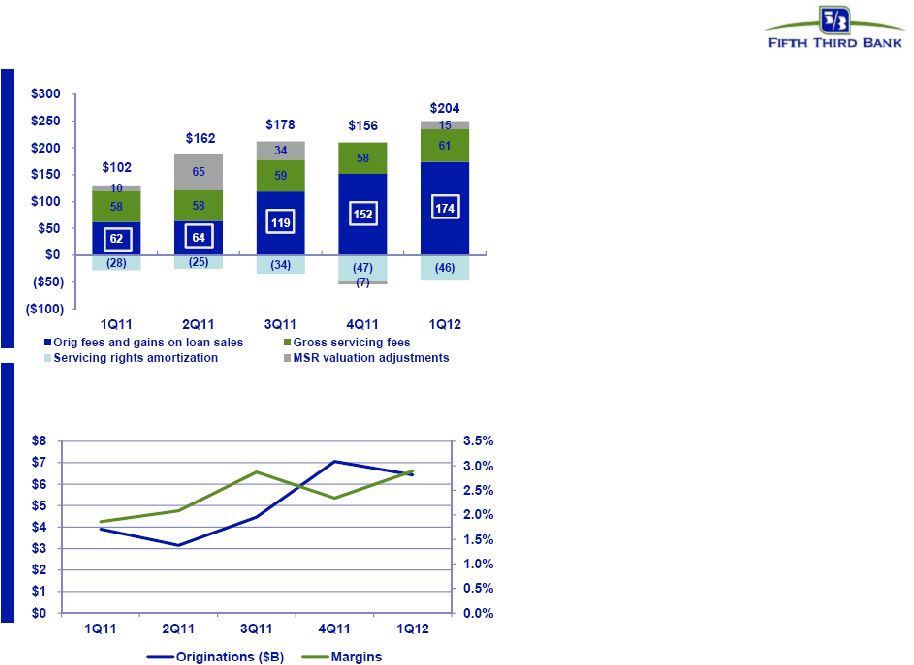

Strong mortgage banking results

•

Record origination fees and gain on

loan sales in 1Q12

Looking forward:

•

Continued strong originations /

deliveries in 2Q12

–

Continuing while rates remain low

•

Gain on sale margins benefitting

from:

–

Strong demand

–

Industry capacity constraints

–

Low prepayment expectations

(particularly on HARP 2.0

originations)

•

HARP 2.0 originations expected to

increase as percentage of total

originations

Mortgage originations and gain-on-sale margins

Mortgage Banking Revenue ($mm) |

10

©

Fifth Third Bank | All Rights Reserved

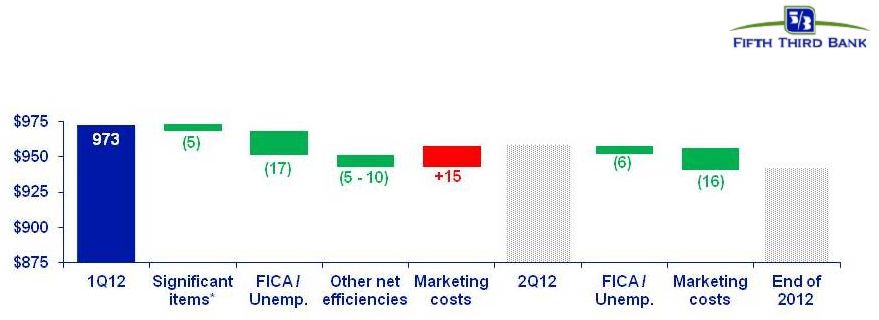

Disciplined expense management

•

Expenses trending downward: 1Q12 expenses down 2% from 4Q11

•

2Q12 expenses expected to decline ~2% despite temporary increase

in marketing costs

•

Expect further overall reduction in expenses in 2H12

•

Managing expenses carefully in response to revenue environment; continuous process of

expense evaluation

•

Expect efficiency ratio to move closer to 60% by year-end and target mid-50%

in normalized environment (with higher interest rate environment)

–

Current impact of credit costs on revenue and expenses; initial impact of regulatory

reforms (e.g., debit interchange)

–

Reflects below-capacity balance sheet and lower revenue than we expect and can

support longer term

Managing expenses for current revenue environment and long-term franchise

value 2012 expense trends ($mm)

*

Significant

items

include

$23mm

benefit

from

agreements

reached

on

certain

non-income

tax

related

assessments,

$13mm

in

additions

to

litigation

reserves,

$9mm

in

debt extinguishment charges, and $6mm in severance expense incurred in 1Q12

|

11

©

Fifth Third Bank | All Rights Reserved

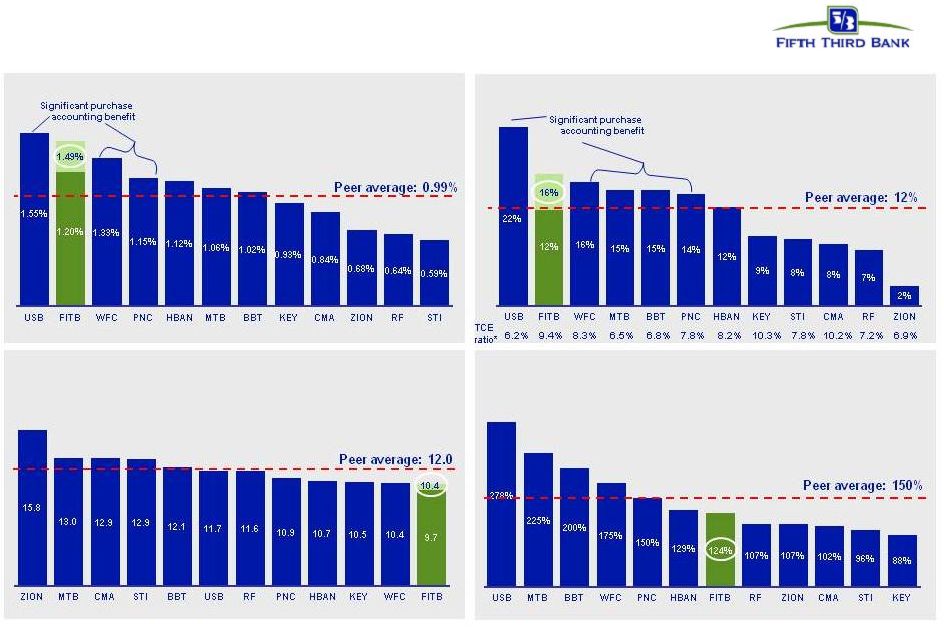

Credit trends continue to improve

with strong reserve coverage levels

Source: SNL Financial and Company Reports. Data as of 1Q12. HFI NPAs and NPLs

exclude loans held-for-sale and also exclude covered assets for BBT, USB, and ZION

*

Non-GAAP

measure.

See

Reg.

G

reconciliation

in

the

Appendix

to

the

presentation.

Reserves, pre-provision profits and capital levels significant in relation to

problem assets Reserves / NPLs

“Texas Ratio”

(HFI NPAs + Over 90s) / (Reserves + TCE*)

HFI NPA Ratio

•

Problem asset levels continue to

decline

•

Reserves remain significantly higher

than pre-crisis levels and peers, with

strong coverage of problem assets and

net charge-offs

•

PPNR levels and profitability provides

Fifth Third with strong ongoing loss

absorption capacity |

12

©

Fifth Third Bank | All Rights Reserved

Exceed fully phased-in Basel III

capital standards today

Source: SNL Financial, Company Reports, and third-party estimates. Data as of

1Q12. Risk-weighted assets for MTB, PNC, ZION as of 4Q11. *

Peers

include

BAC,

BBT,

C,

CMA,

COF,

HBAN,

JPM,

KEY,

MTB,

PNC,

RF,

STI,

USB,

WFC,

ZION

** Non-GAAP measure. See Reg. G reconciliation in the Appendix to the

presentation. Fifth Third’s capital position already well in excess of

established standards, likely standards, and most peers Tier 1 common

(peers) Tier 1 common (FITB)

Reserves

(Tier 1 common + reserves) / RWA**

(not

adjusted

for Basel III)

Peers* not in order of graph at left; estimated

(Tier 1 common + reserves) / RWA**

(adjusted

for Basel III)

Note:

Estimates

based

on

current

Basel

III

rules

released

by

the

Basel

Committee;

actual

rules subject to U.S. banking regulation. Assumes unrealized securities gains

included in Tier 1 common. Not adjusted for potential mitigation efforts.

Four large peers include estimated Basel 2 / 2.5 / 3 RWA impact based on

BIS proposals. Reserves

Tier 1 common (peers)

Tier 1 common (FITB)

Reserves (FITB)

Reserves (FITB) |

13

©

Fifth Third Bank | All Rights Reserved

Capital management philosophy

* Subject to Board of Directors and regulatory approval

** Subject to Federal Reserve non-objection to Comprehensive Capital Analysis

& Review capital plan Organic growth opportunities

•

Support growth of core banking franchise

•

Continued loan growth despite sluggish

economy

Strategic opportunities

*

•

Prudently expand franchise or increase

density in core markets via disciplined

acquisitions or selective de novos

•

Expect future acquisition activity although

less likely in near-term

•

Attain top 3 market position in 65% of

markets or more longer term

Return to more normal dividend policy

*^

•

Strong levels of profitability would support

higher dividend than current level

•

Move towards levels more consistent with

Fed’s near-term payout ratio guidance of

30%

Repurchases / Redemptions

*

•

Initiate common share repurchases to limit

and manage growth in excess capital levels^

–

Manage common equity in light of

regulatory environment, other

alternatives, maintenance of desired /

required buffers, and stock price

•

Potential redemption of $1.4bn in TruPS

–

Evaluated in context of desired capital

structure and regulatory developments

Intend to increase shareholder distributions with

Federal Reserve approval of capital plan**

Capital Deployment

Capital Return |

14

©

Fifth Third Bank | All Rights Reserved

Strong returns drive capital generation

Source: SNL Financial and Company Reports. Price as of 5/1/12

*1Q12

annualized. **FY2012 consensus estimate. Source: Thomson One

^Non-GAAP measure. See Reg. G reconciliation in the Appendix to the

presentation. Note: FITB light green shading represents1Q12 impact of Vantiv.

Well above average profitability and capital generation, well below average

valuation Price / Tangible Book Value^

Price / FY12 Earnings**

Return on Average Tangible Common Equity

*^

Return on Average Assets

* |

15

©

Fifth Third Bank | All Rights Reserved

Well-positioned for the future

•

Holding company cash currently sufficient for more than 3 years of obligations; no

holding company and minimal Bank unsecured debt maturities until 2013

•

Fifth Third has completely exited all crisis-era government support

programs –

Fifth Third is one of the few large banks that have no TLGP-guaranteed debt to

refinance in 2012 Superior capital and liquidity position

•

NCOs of 1.1%; 2.4x reserves / annualized NCOs

•

Substantial reduction in exposure to CRE since 1Q09; relatively low CRE exposure

versus peers •

Very low relative exposure to areas of concern, e.g. European financials, mortgage

repurchase risk Proactive approach to risk management

•

Traditional commercial banking franchise built on customer-oriented localized

operating model •

Strong market share in key markets with focus on further improving density

•

Fee income ~46% of total revenues

Diversified traditional banking platform

•

PPNR has remained strong throughout the credit cycle

•

PPNR substantially exceeds annual net charge-offs (315% PPNR / NCOs^ in

1Q12) •

1.5% ROAA; 16% return on average tangible common equity^

Industry leader in earnings power

^ Non-GAAP measure. See Reg. G reconciliation in the appendix to the

presentation. |

16

©

Fifth Third Bank | All Rights Reserved

Cautionary statement

This

report

contains

statements

that

we

believe

are

“forward-looking

statements”

within

the

meaning

of

Section

27A

of

the

Securities

Act

of

1933,

as

amended,

and

Rule

175

promulgated

thereunder,

and

Section

21E

of

the

Securities

Exchange

Act

of

1934,

as

amended,

and

Rule

3b-6

promulgated

thereunder.

These

statements

relate

to

our

financial

condition,

results

of

operations,

plans,

objectives,

future

performance

or

business.

They

usually

can

be

identified

by

the

use

of

forward-looking

language

such

as

“will

likely

result,”

“may,”

“are

expected

to,”

“is

anticipated,”

“estimate,”

“forecast,”

“projected,”

“intends

to,”

or

may

include

other

similar

words

or

phrases

such

as

“believes,”

“plans,”

“trend,”

“objective,”

“continue,”

“remain,”

or

similar

expressions,

or

future

or

conditional

verbs

such

as

“will,”

“would,”

“should,”

“could,”

“might,”

“can,”

or

similar

verbs.

You

should

not

place

undue

reliance

on

these

statements,

as

they

are

subject

to

risks

and

uncertainties,

including

but

not

limited

to

the

risk

factors

set

forth

in

our

most

recent

Annual

Report

on

Form

10-K.

When

considering

these

forward-looking

statements,

you

should

keep

in

mind

these

risks

and

uncertainties,

as

well

as

any

cautionary

statements

we

may

make.

Moreover,

you

should

treat

these

statements

as

speaking

only

as

of

the

date

they

are

made

and

based

only

on

information

then

actually

known to us.

There

are

a

number

of

important

factors

that

could

cause

future

results

to

differ

materially

from

historical

performance

and

these

forward-

looking

statements.

Factors

that

might

cause

such

a

difference

include,

but

are

not

limited

to:

(1)

general

economic

conditions

and

weakening

in

the

economy,

specifically

the

real

estate

market,

either

nationally

or

in

the

states

in

which

Fifth

Third,

one

or

more

acquired

entities

and/or

the

combined

company

do

business,

are

less

favorable

than

expected;

(2)

deteriorating

credit

quality;

(3)

political

developments,

wars

or

other

hostilities

may

disrupt

or

increase

volatility

in

securities

markets

or

other

economic

conditions;

(4)

changes

in

the

interest

rate

environment

reduce

interest

margins;

(5)

prepayment

speeds,

loan

origination

and

sale

volumes,

charge-offs

and

loan

loss

provisions;

(6)

Fifth

Third’s

ability

to

maintain

required

capital

levels

and

adequate

sources

of

funding

and

liquidity;

(7)

maintaining

capital

requirements

may

limit

Fifth

Third’s

operations

and

potential

growth;

(8)

changes

and

trends

in

capital

markets;

(9)

problems

encountered

by

larger

or

similar

financial

institutions

may

adversely

affect

the

banking

industry

and/or

Fifth

Third;

(10)

competitive

pressures

among

depository

institutions

increase

significantly;

(11)

effects

of

critical

accounting

policies

and

judgments;

(12)

changes

in

accounting

policies

or

procedures

as

may

be

required

by

the

Financial

Accounting

Standards

Board

(FASB)

or

other

regulatory

agencies;

(13)

legislative

or

regulatory

changes

or

actions,

or

significant

litigation,

adversely

affect

Fifth

Third,

one

or

more

acquired

entities

and/or

the

combined

company

or

the

businesses

in

which

Fifth

Third,

one

or

more

acquired

entities

and/or

the

combined

company

are

engaged,

including

the

Dodd-Frank

Wall

Street

Reform

and

Consumer

Protection

Act;

(14)

ability

to

maintain

favorable

ratings

from

rating

agencies;

(15)

fluctuation

of

Fifth

Third’s

stock

price;

(16)

ability

to

attract

and

retain

key

personnel;

(17)

ability

to

receive

dividends

from

its

subsidiaries;

(18)

potentially

dilutive

effect

of

future

acquisitions

on

current

shareholders’

ownership

of

Fifth

Third;

(19)

effects

of

accounting

or

financial

results

of

one

or

more

acquired

entities;

(20)

difficulties

from

the

separation

of

Vantiv,

LLC,

formerly

Fifth

Third

Processing

Solutions

from

Fifth

Third;

(21)

loss

of

income

from

any

sale

or

potential

sale

of

businesses

that

could

have

an

adverse

effect

on

Fifth

Third’s

earnings

and

future

growth;

(22)

ability

to

secure

confidential

information

through

the

use

of

computer

systems

and

telecommunications networks; and (23) the impact of reputational

risk created by these developments on such matters as business

generation and retention, funding and liquidity.

You

should

refer

to

our

periodic

and

current

reports

filed

with

the

Securities

and

Exchange

Commission,

or

“SEC,”

for

further

information

on other factors, which could cause actual results to be significantly different

from those expressed or implied by these forward-looking statements.

|

17

©

Fifth Third Bank | All Rights Reserved

Appendix |

18

©

Fifth Third Bank | All Rights Reserved

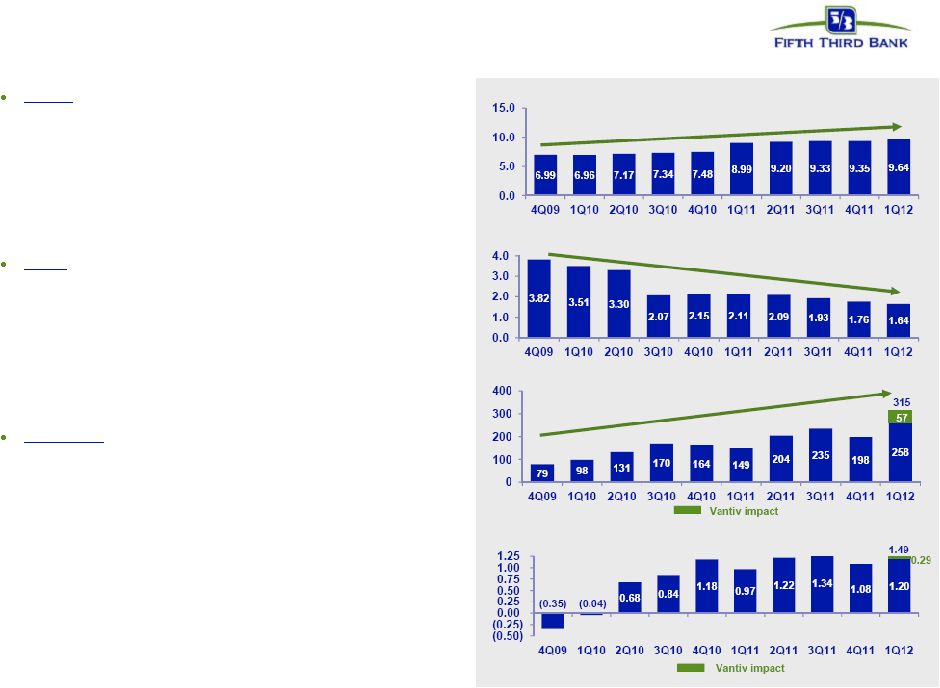

A foundation of continued robust results

Capital

–

exceeds required and targeted levels

—

Tier

1

common*

capital

up

~530bps

or

$5.2bn

from

4Q08

—

Capital base transformed through series of capital actions

–

~10.0% pro forma

1

Tier 1 common ratio* on a fully-phased in

Basel III-adjusted basis

—

Capital levels supplemented by strong reserve levels

–

Loan loss reserves 2.59% of loans and 157% of NPLs

Credit

–

ongoing steady improvement

—

Broad-based improvements in problem loans

–

~80% reduction in 90+ day delinquent loans since 3Q09

–

NCO ratio of 1.08%, lowest NCO level since 4Q07

–

315% PPNR / NCOs*; 258% excluding 1Q12 Vantiv

—

Balance sheet risk lowered through asset sales, resolutions

–

$1.6bn (54%) decline in NPLs since 4Q09

Profitability

–

strong relative and absolute results

—

PPNR* remained stable throughout cycle

—

8 consecutive profitable quarters

—

Return on assets 1.49%; 1.20% excluding 1Q12 Vantiv

—

Return on average tangible common equity

*

16%

* Non-GAAP measure; see Reg. G reconciliation on pages 28-29.

1

Current estimate (non-GAAP), subject to final rule-making and clarification

by U.S. banking regulators; currently assumes unrealized securities gains

are included in common equity for purposes of this calculation

2

Nonperforming

loans

and

leases

as

a

percent

of

portfolio

loans,

leases

and

other

assets,

including other real estate owned (does not include nonaccrual loans

held-for-sale) 3

3Q10 excludes $510mm net charge-offs attributable to credit actions

Tier 1 common ratio (%)*

NPL / Loans²

(%)

PPNR / Net charge-offs (%)³*

Return on assets (%)

57 |

19

©

Fifth Third Bank | All Rights Reserved

Diverse business mix

Branch Banking

Consumer Lending

Commercial Banking

Investment Advisors

•

Professionals committed to

understanding customers’

unique needs, providing

options and identifying the

right solution

•

Top 5 market share within

the non-captive prime auto

lending space

•

Top 13

mortgage

origination share

•

$1.0bn total FY11 revenue

•

Holistic approach to branch

banking combined with

mobile convenience to

improve the banking

experience and be the

trusted financial partner for

our customers

•

1,315 full-service banking

centers

•

2,404 full-service ATMs

•

$2.3bn total FY11 revenue

•

Comprehensive product and

service offering including

commercial lending,

treasury management, and

capital markets

•

Innovative products,

advancements in

technology, and exceptional

customer service

•

$2.0bn total FY11 revenue

•

Provide financial insight, a

wide array of leading-edge

products and services, and

a professional team to

help develop a strategy for

clients’

financial success

•

$486mm total FY11

revenue

•

$26bn assets under

management

•

$296bn assets under care

•

39% interest in Vantiv, LLC, formerly Fifth Third Processing Solutions, LLC

|

20

©

Fifth Third Bank | All Rights Reserved

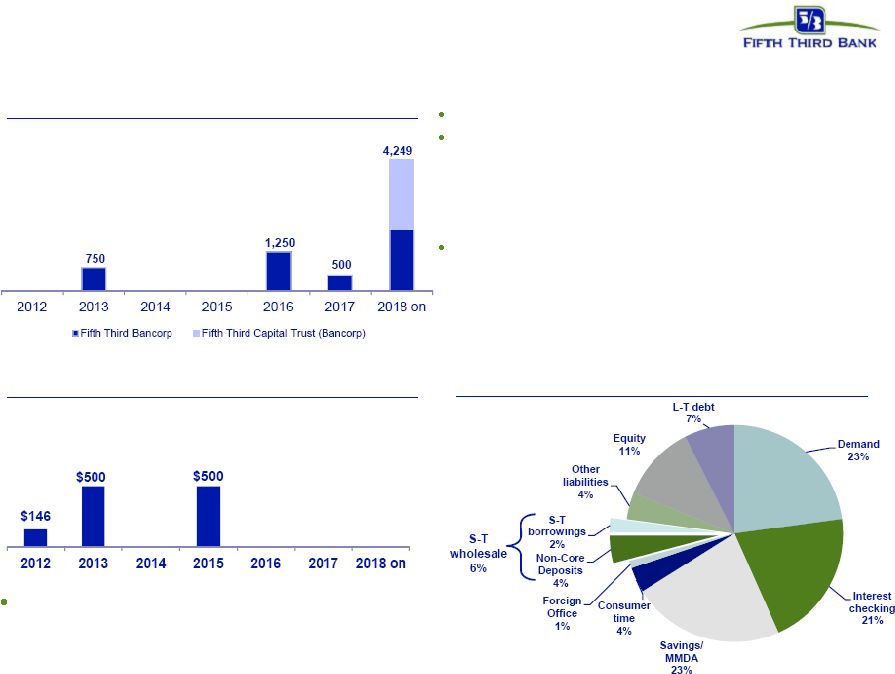

Available and contingent borrowing capacity (1Q12):

–

FHLB ~$11B

–

Federal Reserve ~$24B

Holding Company cash at 3/31/12: $3.2B

Cash currently sufficient to satisfy all fixed obligations

in a stressed environment for more than 3 years

(debt maturities, common and preferred dividends,

interest and other expenses) without accessing capital

markets; relying on dividends from subsidiaries;

proceeds from asset sales

Expected cash obligations over the next 24 months

—

~$591mm common dividends

—

~$70mm Series G preferred dividends

—

~$889mm interest and other expenses

Holding company unsecured debt maturities ($mm)

Bank unsecured debt maturities ($mm –

excl. Brokered CDs)

Heavily core funded

Strong liquidity profile |

21

©

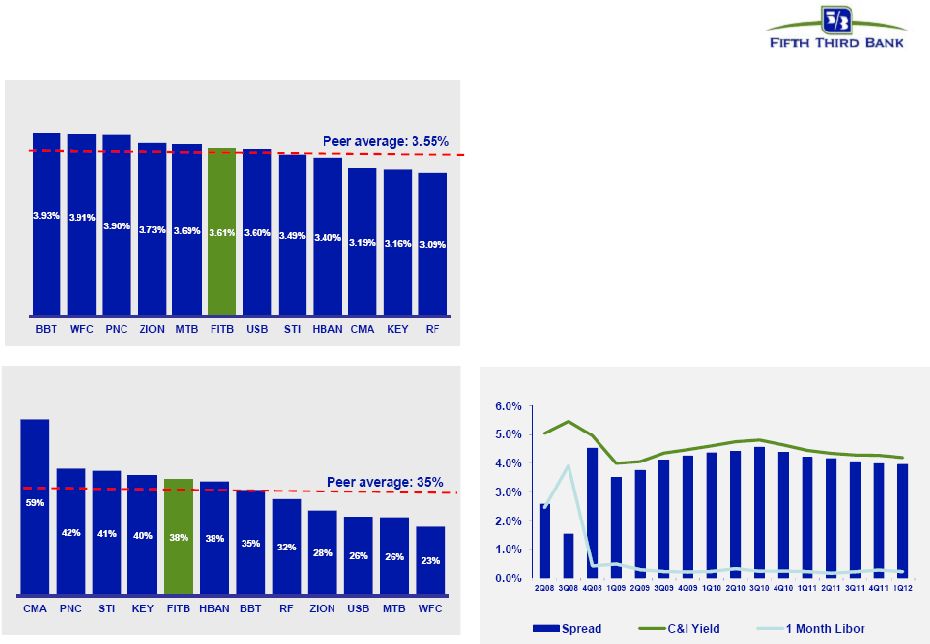

Fifth Third Bank | All Rights Reserved

C&I/Total Loans*^

NIM

•

NIM supported by balance sheet and business

mix

–

Heavy emphasis on traditional C&I lending,

much of which is variable

•

Pricing discipline on commercial loans

–

Spreads have narrowed from post-crisis

levels but remain attractive

–

Loan origination rates have stabilized the

past several months

Relatively strong NIM results

due to balance sheet and business mix

Source: SNL Financial and Company Reports. Data as of 1Q12.

*ZION & BBT exclude government guaranteed loans; ZION presented as end of

period data. ^Presented on an average basis; Excluding held-for-sale

loans. C&I Spread to 1-month LIBOR |

22

©

Fifth Third Bank | All Rights Reserved

Core funded balance sheet and pricing discipline

•

Strong, deposit-rich core funding mix supports

relatively low cost of funds

–

High percentage of funding base in low cost

transaction deposits and noninterest-

bearing DDA accounts

–

Low reliance on wholesale funding

SOURCE: SNL Financial and Company Reports. Data as of 1Q12

Transaction deposits defined as DDA, NOW and Savings/MMDA accounts; Cost of Funds

defined as interest incurred on interest-bearing liabilities as a percentage of average noninterest-bearing deposits and interest-

bearing liabilities; Transaction deposits/Total deposits presented on an average

basis; DDA/Total deposits presented on end-of-period basis. Transaction

Deposits / Total Deposits Cost of Funds

DDA/Total Deposits |

23

©

Fifth Third Bank | All Rights Reserved

Continued improvement in credit trends

Peer average includes: BBT, CMA, HBAN, KEY, MTB, PNC, RF, STI, USB, WFC, and

ZION Source: SNL Financial and company filings. All ratios exclude loans

held-for-sale and covered assets for peers where appropriate. *

4Q08

NCOs

included

$800mm

in

NCOs

related

to

commercial

loans

moved

to

held-for-sale;

3Q10

NCOs

included

$510mm

in

NCOs

related

to

loans

sold

or

moved

to

held-for-sale

FITB credit metrics are in line with or better than peers

NPA ratio vs. peers

Net charge-off ratio vs. peers

Loans 90+ days delinquent % vs. peers

Loans 30-89 days delinquent % vs. peers |

24

©

Fifth Third Bank | All Rights Reserved

NPL HFI Rollforward

Commercial

1Q11

2Q11

3Q11

4Q11

1Q12

Beginning NPL Amount

1,214

1,211

1,253

1,155

1,058

Transfers to nonperforming

329

340

217

189

168

Transfers to performing

(2)

(10)

(11)

-

(1)

Transfers to performing (restructured)

-

-

(1)

-

(2)

Transfers from held for sale

-

-

-

4

-

Transfers to held for sale

(16)

(15)

(58)

(3)

(3)

Loans sold from portfolio

(12)

(7)

(17)

(21)

(8)

Loan paydowns/payoffs

(108)

(91)

(77)

(149)

(94)

Transfer to other real estate owned

(37)

(39)

(20)

(14)

(36)

Charge-offs

(164)

(141)

(136)

(113)

(101)

Draws/other extensions of credit

7

5

5

10

7

Ending Commercial NPL

1,211

1,253

1,155

1,058

988

Consumer

1Q11

2Q11

3Q11

4Q11

1Q12

Beginning NPL Amount

466

434

386

383

380

Transfers to nonperforming

232

214

201

205

184

Transfers to performing

(35)

(34)

(33)

(28)

(36)

Transfers to performing (restructured)

(50)

(41)

(39)

(39)

(36)

Transfers to held for sale

-

-

-

-

-

Loans sold from portfolio

(1)

(21)

-

-

(4)

Loan paydowns/payoffs

(18)

(27)

(27)

(26)

(28)

Transfer to other real estate owned

(18)

(15)

(16)

(30)

(18)

Charge-offs

(144)

(126)

(91)

(87)

(80)

Draws/other extensions of credit

2

2

2

2

2

Ending Consumer NPL

434

386

383

380

364

Total NPL

1,645

1,639

1,538

1,438

1,352

Total new nonaccrual loans - HFI

561

554

418

394

352

NPL rollforward

Significant improvement in NPL inflows over past year

Note: Numbers may not sum due to rounding |

25

©

Fifth Third Bank | All Rights Reserved

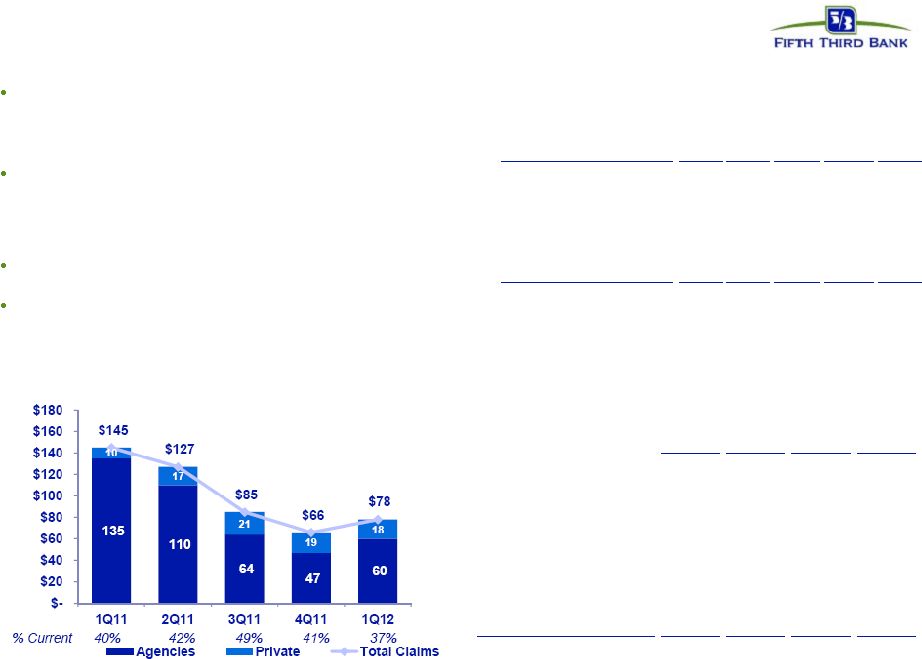

Mortgage repurchase overview

18% rise in 1Q12 outstanding claims balance from prior

quarter

—

Within recent norms of quarterly increases and

decreases

Virtually all sold loans and the majority of new claims relate

to agencies

—

98% of outstanding balance of loans sold

—

77% of current quarter outstanding claims

Majority of outstanding balances of the serviced for others

portfolio relates to origination activity in 2009 and later

Private claims and exposure relate to whole loan sales (no

outstanding first mortgage securitizations)

—

Preponderance of private sales prior to 2006

Repurchase Reserves* ($ in millions)

Outstanding Counterparty Claims ($ in millions)

Outstanding Balance of Sold Loans ($ in millions)

1Q11

2Q11

3Q11

4Q11

1Q12

Beginning balance

101

87

80

69

72

Net reserve additions

10

15

20

20

17

Repurchase losses

(23)

(23)

(31)

(17)

(17)

Ending balance

87

80

69

72

71

2005 and prior

GSE

GNMA

Private

Total

$6,680

$273

$492

$7,445

2006

1,550

55

250

1,855

2007

2,509

80

215

2,804

2008

2,406

633

0.3

3,039

2009

9,462

3,563

0.7

13,026

2010 and later

26,338

5,884

0.3

32,222

Total

$48,945

$10,488

$958

$60,391

* Includes reps and warranty reserve ($55mm) and reserve for loans sold with

recourse ($17mm) Note: Numbers may not sum due to rounding

|

26

©

Fifth Third Bank | All Rights Reserved

Troubled debt restructurings overview

Successive improvement in vintage performance during

2008 and 2009 as volume of modification increased

Fifth Third’s mortgage portfolio TDRs have redefaulted

at a lower rate than GSE composites

Of $1.8B in consumer TDRs, $1.6B were on accrual

status and $201mm were nonaccruals

—

$1.2B of TDRs are current and have been on the

books 6 or more months; within that, ~$1B of

TDRs are current and have been on the books for

more than a year

As current TDRs season, their default propensity

declines significantly

—

We see much lower defaults on current loans after

a vintage approaches 12 months since

modification

TDR performance has improved in newer vintages

Redefault benchmarks

Source: Fifth Third and OCC/OTS data through 3Q11

Mortgage TDR 60+ redefault trend by vintage*

Mortgage TDR 60+ redefault rate: Fifth Third comparison

(January 1, 2008 through December 2011)*

$1.3B current consumer TDRs (%)

* Fifth Third data includes changes made to align with OCC/OTS methodology (i.e.

excludes government loans, closed loans and OREO from calculations) |

27

©

Fifth Third Bank | All Rights Reserved

Total

Exposure

Funded

Exposure

Total

Exposure

Funded

Exposure

Total

Exposure

Funded

Exposure

Total

Exposure

Funded

Exposure

(amounts in $mm)

Peripheral Europe

-

-

11

-

168

124

179

124

Other Eurozone

-

-

44

34

1,275

742

1,319

776

Total Eurozone

-

-

55

34

1,443

866

1,498

900

Other Europe

-

-

23

18

820

496

843

514

Total Europe

-

-

77

52

2,263

1,362

2,340

1,414

Sovereigns

Financial Institutions

Non-Financial Entities

Total

European exposure

Total exposure includes funded and unfunded commitments, net of collateral; funded

exposure excludes unfunded exposure Peripheral Europe includes Greece,

Ireland, Italy, Portugal and Spain Eurozone includes countries participating

in the European common currency (Euro)

Other Europe includes European countries not part of the Euro (primarily the United

Kingdom and Switzerland) Data above includes exposure to U.S. subsidiaries of

Europe-domiciled companies Note: Numbers may not sum due to

rounding •

International exposure primarily related to trade finance and financing activities of

U.S. companies with foreign parent or overseas activities of U.S.

customers •

No European sovereign exposure (total international sovereign exposure $3mm)

•

Total exposure to European financial institutions <$80mm

•

Total exposure to five peripheral Europe countries <$200mm

•

$900mm in funded exposure to Eurozone-related companies (~1% of total loan

portfolio) |

28

©

Fifth Third Bank | All Rights Reserved

Regulation G Non-GAAP reconciliation

Fifth Third Bancorp and Subsidiaries

Regulation G Non-GAAP Reconcilation

$ and shares in millions

(unaudited)

March

December

September

June

March

December

September

June

March

December

2012

2011

2011

2011

2011

2010

2010

2010

2010

2009

Income before income taxes (U.S. GAAP)

$603

$418

$530

$506

$377

417

$

303

$

242

$

(22)

$

(214)

$

Add:

Provision expense (U.S. GAAP)

91

55

87

113

168

166

457

325

590

776

Pre-provision net revenue (a)

694

473

617

619

545

583

760

567

568

562

Annualized PPNR (c)

2,791

1,877

2,448

2,483

2,210

2,313

3,015

2,274

2,304

2,230

Net income available to common shareholders (U.S. GAAP)

421

Add:

Intangible amortization, net of tax

3

Tangible net income available to common shareholders

424

Tangible net income available to common shareholders (annualized) (b)

1,705

Average Bancorp shareholders' equity (U.S. GAAP)

13,366

Less:

Average preferred stock

398

Average goodwill

2,417

Average intangible assets

38

Average tangible common equity (c)

10,513

Total Bancorp shareholders' equity (U.S. GAAP)

13,560

Less:

Preferred stock

(398)

Goodwill

(2,417)

Intangible assets

(36)

Tangible common equity, including unrealized gains / losses (d)

10,709

Less: Accumulated other comprehensive income / loss

(468)

Tangible common equity, excluding unrealized gains / losses (e)

10,241

Total assets (U.S. GAAP)

116,747

Less:

Goodwill

(2,417)

Intangible assets

(36)

Tangible assets, including unrealized gains / losses (f)

114,294

Less: Accumulated other comprehensive income / loss, before tax

(720)

Tangible assets, excluding unrealized gains / losses (g)

113,574

Common shares outstanding (h)

920

Net charge-offs

220

239

262

304

367

356

446

434

582

708

Annualized net charge-offs (i)

885

948

1,039

1,219

1,488

1,412

1,769

1,741

2,360

2,809

Average interest earning assets (j)

100,492

Ratios:

Return on average tangible common equity (b) / (c)

16.2%

Tangible common equity (excluding unrealized gains/losses) (e) / (g)

9.02%

Tangible common equity (including unrealized gains/losses) (d) / (f)

9.37%

Tangible book value per share (d) / (h)

11.64

Pre-provision net revenue / net charge-offs (a) / (i)

315%

198%

235%

204%

149%

164%

170%

131%

98%

79%

Pre-provision net revenue / avg. int. earning assets (a) / (j)

2.8%

For the Three Months Ended |

29

©

Fifth Third Bank | All Rights Reserved

Regulation G Non-GAAP reconciliation

Fifth Third Bancorp and Subsidiaries

Regulation G Non-GAAP Reconcilation

$ and shares in millions

(unaudited)

March

December

September

June

March

December

September

June

March

December

2012

2011

2011

2011

2011

2010

2010

2010

2010

2009

Total Bancorp shareholders' equity (U.S. GAAP)

$13,560

$13,201

$13,029

$12,572

$12,163

$14,051

$13,884

$13,701

$13,408

$13,497

Goodwill and certain other intangibles

(2,518)

(2,514)

(2,514)

(2,536)

(2,546)

(2,546)

(2,525)

(2,537)

(2,556)

(2,565)

Unrealized gains

(468)

(470)

(542)

(396)

(263)

(314)

(432)

(440)

(288)

(240)

Qualifying trust preferred securities

2,248

2,248

2,273

2,312

2,763

2,763

2,763

2,763

2,763

2,763

Other

38

38

20

20

12

11

8

(25)

(30)

(27)

Tier I capital

12,860

12,503

12,266

11,972

12,129

13,965

13,698

13,462

13,297

13,428

Less:

Preferred stock

(398)

(398)

(398)

(398)

(398)

(3,654)

(3,642)

(3,631)

(3,620)

(3,609)

Qualifying trust preferred securities

(2,248)

(2,248)

(2,273)

(2,312)

(2,763)

(2,763)

(2,763)

(2,763)

(2,763)

(2,763)

Qualifying noncontrolling interest in consolidated subsidiaries

(50)

(50)

(30)

(30)

(30)

(30)

(30)

-

-

-

Tier I common equity (a)

10,164

9,807

9,565

9,232

8,938

7,518

7,263

7,068

6,914

7,056

Unrealized gains

468

Disallowed deferred tax assets

-

Disallowed MSRs

78

Other

11

Less:

10% of individual deferred tax assets, MSRs, investment in financial entitie

-

15% of aggregate deferred tax assets, MSRs, investment in financial entiti

-

Tier 1 common equity, Basel III proforma (b)

10,721

Risk-weighted assets, determined in accordance with

prescribed regulatory requirements (c)

105,412

104,945

102,562

100,320

99,392

100,561

98,904

98,604

99,281

100,933

Regulatory deductions not deducted from Tier 1 common equity,

risk-weighted at 250%

1,582

Risk-weighted assets, Basel III proforma (d)

106,994

Ratios:

Tier I common equity (a) / (c)

9.64%

9.35%

9.33%

9.20%

8.99%

7.48%

7.34%

7.17%

6.96%

6.99%

Tier I common equity, Basel III proforma (b) / (d)

10.02%

For the Three Months Ended

Add: |