Attached files

| file | filename |

|---|---|

| 8-K - PR AND ANALYST SCHEDULES 8K - Frontier Communications Parent, Inc. | pranalsched8k.htm |

| EX-99.1 - PR AND ANALYST SCHEDULES - Frontier Communications Parent, Inc. | prandanalsched.htm |

Investor Update

First Quarter 2012

May 7, 2012

2

Safe Harbor Statement

Forward-Looking Language

This document contains forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from those expressed or implied in

the financial statements. Statements that are not historical facts are forward-looking statements made pursuant to the safe harbor provisions of The Private Securities Litigation

Reform Act of 1995. Words such as “believe,” “anticipate,” “expect” and similar expressions are intended to identify forward-looking statements. Forward-looking statements

(including oral representations) are only predictions or statements of current plans, which we review continuously. Forward-looking statements may differ from actual future results

due to, but not limited to, and our future results may be materially affected by, potential risks or uncertainties. You should understand that it is not possible to predict or identify all

potential risks or uncertainties. We note the following as a partial list: the risk that the growth opportunities from the Transaction may not be fully realized or may take longer to

realize than expected; the effects of greater than anticipated competition requiring new pricing, marketing strategies or new product or service offerings and the risk that we will not

respond on a timely or profitable basis; reductions in the number of our access lines that cannot be offset by increases in broadband subscribers and sales of other products and

services; the effects of competition from cable, wireless and other wireline carriers; our ability to maintain relationships with customers, employees or suppliers; the effects of

ongoing changes in the regulation of the communications industry as a result of federal and state legislation and regulation, or changes in the enforcement or interpretation of such

legislation and regulation; the effects of any unfavorable outcome with respect to any current or future legal, governmental or regulatory proceedings, audits or disputes; the effects

of changes in the availability of federal and state universal funding to us and our competitors; our ability to adjust successfully to changes in the communications industry and to

implement strategies for growth; continued reductions in switched access revenues as a result of regulation, competition or technology substitutions; our ability to effectively

manage service quality in our territories and meet mandated service quality metrics; our ability to successfully introduce new product offerings, including our ability to offer bundled

service packages on terms that are both profitable to us and attractive to customers; changes in accounting policies or practices adopted voluntarily or as required by generally

accepted accounting principles or regulations; our ability to effectively manage our operations, operating expenses and capital expenditures, and to repay, reduce or refinance our

debt; the effects of changes in both general and local economic conditions on the markets that we serve, which can affect demand for our products and services, customer

purchasing decisions, collectability of revenues and required levels of capital expenditures related to new construction of residences and businesses; the effects of technological

changes and competition on our capital expenditures and product and service offerings, including the lack of assurance that our network improvements will be sufficient to meet or

exceed the capabilities and quality of competing networks; the effects of increased medical and pension expenses and related funding requirements; changes in income tax rates,

tax laws, regulations or rulings, or federal or state tax assessments; the effects of state regulatory cash management practices that could limit our ability to transfer cash among

our subsidiaries or dividend funds up to the parent company; our ability to successfully renegotiate union contracts in 2012 and thereafter; changes in pension plan assumptions

and/or the value of our pension plan assets, which would require us to make increased contributions to the pension plan in 2013 and beyond; the effects of customer bankruptcies

and home foreclosures, which could result in difficulty in collection of revenues and loss of customers; adverse changes in the credit markets or in the ratings given to our debt

securities by nationally accredited ratings organizations, which could limit or restrict the availability, or increase the cost, of financing; limitations on the amount of capital stock that

we can issue to make acquisitions or to raise additional capital until July 2012; our indemnity obligation to Verizon for taxes which may be imposed upon them as a result of

changes in ownership of our stock may discourage, delay or prevent a third party from acquiring control of us during the two-year period ending July 2012 in a transaction that

stockholders might consider favorable; our ability to pay dividends on our common shares, which may be affected by our cash flow from operations, amount of capital

expenditures, debt service requirements, cash paid for income taxes and liquidity; and the effects of severe weather events such as hurricanes, tornadoes, ice storms or other

natural or man-made disasters. These and other uncertainties related to our business are described in greater detail in our filings with the Securities and Exchange Commission,

including our reports on Forms 10-K and 10-Q, and the foregoing information should be read in conjunction with these filings. We undertake no obligation to publicly update or

revise any forward-looking statements or to make any other forward-looking statement, whether as a result of new information, future events or otherwise unless required to do so

by securities laws.

the financial statements. Statements that are not historical facts are forward-looking statements made pursuant to the safe harbor provisions of The Private Securities Litigation

Reform Act of 1995. Words such as “believe,” “anticipate,” “expect” and similar expressions are intended to identify forward-looking statements. Forward-looking statements

(including oral representations) are only predictions or statements of current plans, which we review continuously. Forward-looking statements may differ from actual future results

due to, but not limited to, and our future results may be materially affected by, potential risks or uncertainties. You should understand that it is not possible to predict or identify all

potential risks or uncertainties. We note the following as a partial list: the risk that the growth opportunities from the Transaction may not be fully realized or may take longer to

realize than expected; the effects of greater than anticipated competition requiring new pricing, marketing strategies or new product or service offerings and the risk that we will not

respond on a timely or profitable basis; reductions in the number of our access lines that cannot be offset by increases in broadband subscribers and sales of other products and

services; the effects of competition from cable, wireless and other wireline carriers; our ability to maintain relationships with customers, employees or suppliers; the effects of

ongoing changes in the regulation of the communications industry as a result of federal and state legislation and regulation, or changes in the enforcement or interpretation of such

legislation and regulation; the effects of any unfavorable outcome with respect to any current or future legal, governmental or regulatory proceedings, audits or disputes; the effects

of changes in the availability of federal and state universal funding to us and our competitors; our ability to adjust successfully to changes in the communications industry and to

implement strategies for growth; continued reductions in switched access revenues as a result of regulation, competition or technology substitutions; our ability to effectively

manage service quality in our territories and meet mandated service quality metrics; our ability to successfully introduce new product offerings, including our ability to offer bundled

service packages on terms that are both profitable to us and attractive to customers; changes in accounting policies or practices adopted voluntarily or as required by generally

accepted accounting principles or regulations; our ability to effectively manage our operations, operating expenses and capital expenditures, and to repay, reduce or refinance our

debt; the effects of changes in both general and local economic conditions on the markets that we serve, which can affect demand for our products and services, customer

purchasing decisions, collectability of revenues and required levels of capital expenditures related to new construction of residences and businesses; the effects of technological

changes and competition on our capital expenditures and product and service offerings, including the lack of assurance that our network improvements will be sufficient to meet or

exceed the capabilities and quality of competing networks; the effects of increased medical and pension expenses and related funding requirements; changes in income tax rates,

tax laws, regulations or rulings, or federal or state tax assessments; the effects of state regulatory cash management practices that could limit our ability to transfer cash among

our subsidiaries or dividend funds up to the parent company; our ability to successfully renegotiate union contracts in 2012 and thereafter; changes in pension plan assumptions

and/or the value of our pension plan assets, which would require us to make increased contributions to the pension plan in 2013 and beyond; the effects of customer bankruptcies

and home foreclosures, which could result in difficulty in collection of revenues and loss of customers; adverse changes in the credit markets or in the ratings given to our debt

securities by nationally accredited ratings organizations, which could limit or restrict the availability, or increase the cost, of financing; limitations on the amount of capital stock that

we can issue to make acquisitions or to raise additional capital until July 2012; our indemnity obligation to Verizon for taxes which may be imposed upon them as a result of

changes in ownership of our stock may discourage, delay or prevent a third party from acquiring control of us during the two-year period ending July 2012 in a transaction that

stockholders might consider favorable; our ability to pay dividends on our common shares, which may be affected by our cash flow from operations, amount of capital

expenditures, debt service requirements, cash paid for income taxes and liquidity; and the effects of severe weather events such as hurricanes, tornadoes, ice storms or other

natural or man-made disasters. These and other uncertainties related to our business are described in greater detail in our filings with the Securities and Exchange Commission,

including our reports on Forms 10-K and 10-Q, and the foregoing information should be read in conjunction with these filings. We undertake no obligation to publicly update or

revise any forward-looking statements or to make any other forward-looking statement, whether as a result of new information, future events or otherwise unless required to do so

by securities laws.

3

Non-GAAP Financial Measures

The Company uses certain non-GAAP financial measures in evaluating its performance. These include free cash flow, EBITDA or “operating cash flow,” which

we define as operating income plus depreciation and amortization (“EBITDA”), and Adjusted EBITDA; a reconciliation of the differences between EBITDA and

free cash flow and the most comparable financial measures calculated and presented in accordance with GAAP is included in the appendix. The non-GAAP

financial measures are by definition not measures of financial performance under GAAP and are not alternatives to operating income or net income reflected in

the statement of operations or to cash flow as reflected in the statement of cash flows and are not necessarily indicative of cash available to fund all cash flow

needs. The non-GAAP financial measures used by the Company may not be comparable to similarly titled measures of other companies.

we define as operating income plus depreciation and amortization (“EBITDA”), and Adjusted EBITDA; a reconciliation of the differences between EBITDA and

free cash flow and the most comparable financial measures calculated and presented in accordance with GAAP is included in the appendix. The non-GAAP

financial measures are by definition not measures of financial performance under GAAP and are not alternatives to operating income or net income reflected in

the statement of operations or to cash flow as reflected in the statement of cash flows and are not necessarily indicative of cash available to fund all cash flow

needs. The non-GAAP financial measures used by the Company may not be comparable to similarly titled measures of other companies.

The Company believes that the presentation of non-GAAP financial measures provides useful information to investors regarding the Company’s financial

condition and results of operations because these measures, when used in conjunction with related GAAP financial measures, (i) together provide a more

comprehensive view of the Company’s core operations and ability to generate cash flow, (ii) provide investors with the financial analytical framework upon

which management bases financial, operational, compensation and planning decisions and (iii) presents measurements that investors and rating agencies

have indicated to management are useful to them in assessing the Company and its results of operations. In addition, the Company believes that free cash

flow and EBITDA, as the Company defines them, can assist in comparing performance from period to period, without taking into account factors affecting cash

flow reflected in the statement of cash flows, including changes in working capital and the timing of purchases and payments.

condition and results of operations because these measures, when used in conjunction with related GAAP financial measures, (i) together provide a more

comprehensive view of the Company’s core operations and ability to generate cash flow, (ii) provide investors with the financial analytical framework upon

which management bases financial, operational, compensation and planning decisions and (iii) presents measurements that investors and rating agencies

have indicated to management are useful to them in assessing the Company and its results of operations. In addition, the Company believes that free cash

flow and EBITDA, as the Company defines them, can assist in comparing performance from period to period, without taking into account factors affecting cash

flow reflected in the statement of cash flows, including changes in working capital and the timing of purchases and payments.

The Company has shown adjustments to its financial presentations to exclude certain costs because investors have indicated to management that such

adjustments are useful to them in assessing the Company and its results of operations. These adjustments are detailed in the Appendix for the reconciliation

of free cash flow and operating cash flow.

adjustments are useful to them in assessing the Company and its results of operations. These adjustments are detailed in the Appendix for the reconciliation

of free cash flow and operating cash flow.

Management uses these non-GAAP financial measures to (i) assist in analyzing the Company’s underlying financial performance from period to period, (ii)

evaluate the financial performance of its business units, (iii) analyze and evaluate strategic and operational decisions, (iv) establish criteria for compensation

decisions, and (v) assist management in understanding the Company’s ability to generate cash flow and, as a result, to plan for future capital and operational

decisions. Management uses these non-GAAP financial measures in conjunction with related GAAP financial measures. These non-GAAP financial measures

have certain shortcomings. In particular, free cash flow does not represent the residual cash flow available for discretionary expenditures, since items such as

debt repayments and dividends are not deducted in determining such measure. EBITDA has similar shortcomings as interest, income taxes, capital

expenditures, debt repayments and dividends are not deducted in determining this measure. Management compensates for the shortcomings of these

measures by utilizing them in conjunction with their comparable GAAP financial measures. The information in this document should be read in conjunction with

the financial statements and footnotes contained in our documents filed with the U.S. Securities and Exchange Commission.

evaluate the financial performance of its business units, (iii) analyze and evaluate strategic and operational decisions, (iv) establish criteria for compensation

decisions, and (v) assist management in understanding the Company’s ability to generate cash flow and, as a result, to plan for future capital and operational

decisions. Management uses these non-GAAP financial measures in conjunction with related GAAP financial measures. These non-GAAP financial measures

have certain shortcomings. In particular, free cash flow does not represent the residual cash flow available for discretionary expenditures, since items such as

debt repayments and dividends are not deducted in determining such measure. EBITDA has similar shortcomings as interest, income taxes, capital

expenditures, debt repayments and dividends are not deducted in determining this measure. Management compensates for the shortcomings of these

measures by utilizing them in conjunction with their comparable GAAP financial measures. The information in this document should be read in conjunction with

the financial statements and footnotes contained in our documents filed with the U.S. Securities and Exchange Commission.

4

Quarterly Snapshot

5

Summary

● Solid quarter of customer metrics, expanding margins, and

stable leverage

stable leverage

Solid quarter of customer metrics, expanding margins, and

stable leverage

stable leverage

● Invested $209M into our network to reach 40,000 new homes

and increase broadband speeds

and increase broadband speeds

Invested $209M into our network to reach 40,000 new homes

and increase broadband speeds

and increase broadband speeds

● Acquisition systems integration successfully completed with

final 9-State conversion in March 2012

final 9-State conversion in March 2012

Acquisition systems integration successfully completed with

final 9-State conversion in March 2012

final 9-State conversion in March 2012

● Focus on revenue improvement, broadband penetration and

operational excellence

operational excellence

Focus on revenue improvement, broadband penetration and

operational excellence

operational excellence

● New organizational structure with all customer-facing activities

reporting to Daniel McCarthy, President & Chief Operating

Officer

reporting to Daniel McCarthy, President & Chief Operating

Officer

New organizational structure with all customer-facing activities

reporting to Daniel McCarthy, President & Chief Operating

Officer

reporting to Daniel McCarthy, President & Chief Operating

Officer

6

Executing on Our Strategy

Keep the Customer in the Center of our Go-to-Market

|

Drive Revenue

Growth |

|

Lead With

Broadband |

|

Deliver

Operational Excellence |

|

Create

Shareholder Value |

|

|

|

|

|

|

|

|

|

§ Double + Triple

Play Bundles § WiFi + Mobility

• VoIP

• Cloud

• Security

• Home

Automation

• CPE

|

|

§ Reach / Access

§ Speeds

|

|

§ Process

Simplification |

|

§ Improve Free

Cash Flow |

7

Financial Highlights

● Access line loss of 7.9% lowest to date, and expanding

broadband and video net subscriber additions

broadband and video net subscriber additions

Access line loss of 7.9% lowest to date, and expanding

broadband and video net subscriber additions

broadband and video net subscriber additions

● Residential ARPU grew sequentially, 44% reduction in

sequential revenue loss

sequential revenue loss

Residential ARPU grew sequentially, 44% reduction in

sequential revenue loss

sequential revenue loss

● Business ARPU grew sequentially, key products (Ethernet,

DIA, wireless backhaul, CPE) grew 6.6% annually

DIA, wireless backhaul, CPE) grew 6.6% annually

Business ARPU grew sequentially, key products (Ethernet,

DIA, wireless backhaul, CPE) grew 6.6% annually

DIA, wireless backhaul, CPE) grew 6.6% annually

● Adjusted EBITDA grew 1% sequentially; margin 49%, strongest

to date on $13M of incremental synergies and organic cost

control

to date on $13M of incremental synergies and organic cost

control

Adjusted EBITDA grew 1% sequentially; margin 49%, strongest

to date on $13M of incremental synergies and organic cost

control

to date on $13M of incremental synergies and organic cost

control

● FCF of $253M on track to achieve $900M-$1.0B guidance

FCF of $253M on track to achieve $900M-$1.0B guidance

8

Business Update

Organization

Organization

● Metro Ethernet revenues +5.6% yr/yr in 1Q12; Wireless

backhaul revenues +16% yr/yr in 1Q12

backhaul revenues +16% yr/yr in 1Q12

Metro Ethernet revenues +5.6% yr/yr in 1Q12; Wireless

backhaul revenues +16% yr/yr in 1Q12

backhaul revenues +16% yr/yr in 1Q12

● Continued focus on value-added services, higher speeds,

and strategic partnerships

and strategic partnerships

Continued focus on value-added services, higher speeds,

and strategic partnerships

and strategic partnerships

● Financial improvements driven by network enhancement

and local engagement

and local engagement

Financial improvements driven by network enhancement

and local engagement

and local engagement

● Opportunity for incremental revenues: Frontier Secure with

identity protection, WiFi, mobility, video

identity protection, WiFi, mobility, video

Opportunity for incremental revenues: Frontier Secure with

identity protection, WiFi, mobility, video

identity protection, WiFi, mobility, video

Commercial

Commercial

Residential

Residential

9

Conversion Impacts

● Acquired West Virginia metrics

continue to improve dramatically

continue to improve dramatically

Acquired West Virginia metrics

continue to improve dramatically

continue to improve dramatically

● Oct 1, 2011 conversion of 4 states

(NC,SC,IN,MI) already showing

traction

(NC,SC,IN,MI) already showing

traction

Oct 1, 2011 conversion of 4 states

(NC,SC,IN,MI) already showing

traction

(NC,SC,IN,MI) already showing

traction

● On track for Acquired to reach 8%

access line decline goal as we enter

2013

access line decline goal as we enter

2013

On track for Acquired to reach 8%

access line decline goal as we enter

2013

access line decline goal as we enter

2013

Notes: Broadband availability for 2Q10 updated for current data and methodology.

Notes: Broadband availability for 2Q10 updated for current data and methodology.

10

Key Metrics

● Broadband net adds

+25% sequentially led

by DSL

+25% sequentially led

by DSL

Broadband net adds

+25% sequentially led

by DSL

+25% sequentially led

by DSL

● Video selling well in

bundles. Net adds led

by DISH and lower

FiOS disconnects

bundles. Net adds led

by DISH and lower

FiOS disconnects

Video selling well in

bundles. Net adds led

by DISH and lower

FiOS disconnects

bundles. Net adds led

by DISH and lower

FiOS disconnects

● Line loss improved

sharply to 7.9%

sharply to 7.9%

Line loss improved

sharply to 7.9%

sharply to 7.9%

● Churn steady;

showed minor

conversion impacts

showed minor

conversion impacts

Churn steady;

showed minor

conversion impacts

showed minor

conversion impacts

Notes: (1) Comparisons to amounts prior to 7/1/10 pro forma for the Acquired Properties. Subscriber units in 000s

Notes: (1) Comparisons to amounts prior to 7/1/10 pro forma for the Acquired Properties. Subscriber units in 000s

11

Revenues

● Regulatory

revenues 11.7% of

1Q12 total

revenues 11.7% of

1Q12 total

Regulatory

revenues 11.7% of

1Q12 total

revenues 11.7% of

1Q12 total

● Switched access

5.5% and

subsidies 3.8% of

total revenue 2

5.5% and

subsidies 3.8% of

total revenue 2

Switched access

5.5% and

subsidies 3.8% of

total revenue 2

5.5% and

subsidies 3.8% of

total revenue 2

Notes: $ Millions; Numbers may not sum due to rounding. (1) as a percentage of Customer Revenue. (2) Excludes

surcharges

surcharges

Notes: $ Millions; Numbers may not sum due to rounding. (1) as a percentage of Customer Revenue. (2) Excludes

surcharges

surcharges

● Business

represents 52% of

total customer

revenues

represents 52% of

total customer

revenues

Business

represents 52% of

total customer

revenues

represents 52% of

total customer

revenues

● Business ARPU

up 9% yr/yr to

$637

up 9% yr/yr to

$637

Business ARPU

up 9% yr/yr to

$637

up 9% yr/yr to

$637

● High exposure to

business and

broadband

revenues. Key

focus on raising

this level.

business and

broadband

revenues. Key

focus on raising

this level.

High exposure to

business and

broadband

revenues. Key

focus on raising

this level.

business and

broadband

revenues. Key

focus on raising

this level.

12

Residential & Business

● Acquired Residential

ARPU has +8% upside

to Legacy levels

ARPU has +8% upside

to Legacy levels

Acquired Residential

ARPU has +8% upside

to Legacy levels

ARPU has +8% upside

to Legacy levels

● Residential products-

per-customer +6.4%

yr/yr to 2.5 driven by

broadband

per-customer +6.4%

yr/yr to 2.5 driven by

broadband

Residential products-

per-customer +6.4%

yr/yr to 2.5 driven by

broadband

per-customer +6.4%

yr/yr to 2.5 driven by

broadband

● Mix of larger

customers favorably

impacting ARPU.

1Q12 seasonality on

CPE sales

customers favorably

impacting ARPU.

1Q12 seasonality on

CPE sales

Mix of larger

customers favorably

impacting ARPU.

1Q12 seasonality on

CPE sales

customers favorably

impacting ARPU.

1Q12 seasonality on

CPE sales

Notes: 1) Sequential quarterly change.

Notes: 1) Sequential quarterly change.

13

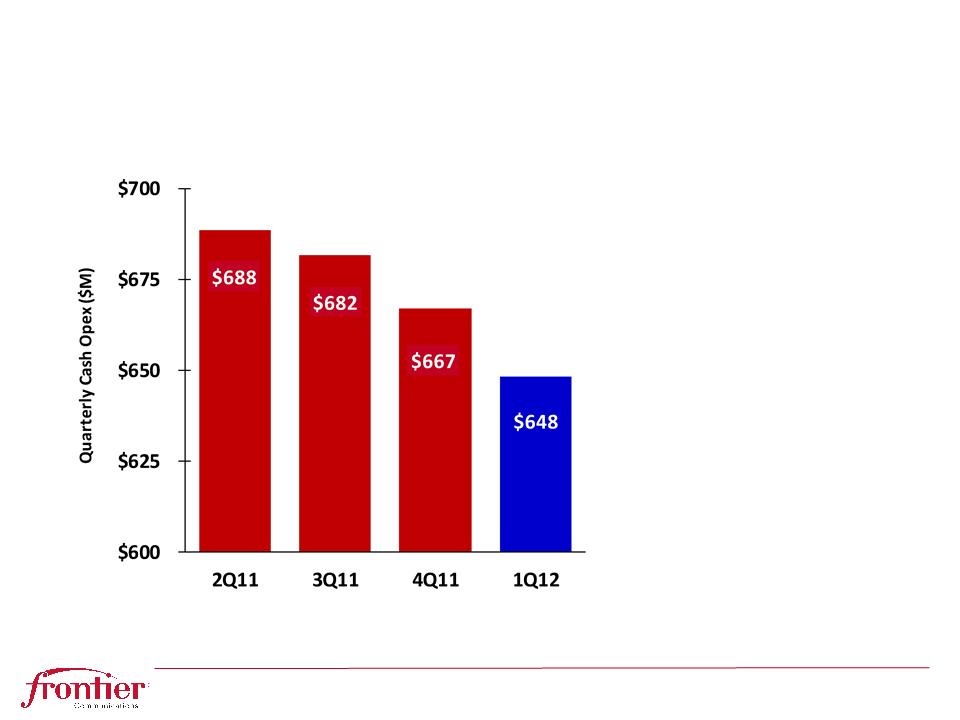

Cash Operating Expenses

Notes: $ Millions; Please see Non-GAAP reconciliations in Appendix.

Notes: $ Millions; Please see Non-GAAP reconciliations in Appendix.

● Cash operating

expenses down $19M

sequentially

expenses down $19M

sequentially

Cash operating

expenses down $19M

sequentially

expenses down $19M

sequentially

● Continued extensive

focus and discipline

on synergy list

focus and discipline

on synergy list

Continued extensive

focus and discipline

on synergy list

focus and discipline

on synergy list

$19 Million

Reduction

Reduction

14

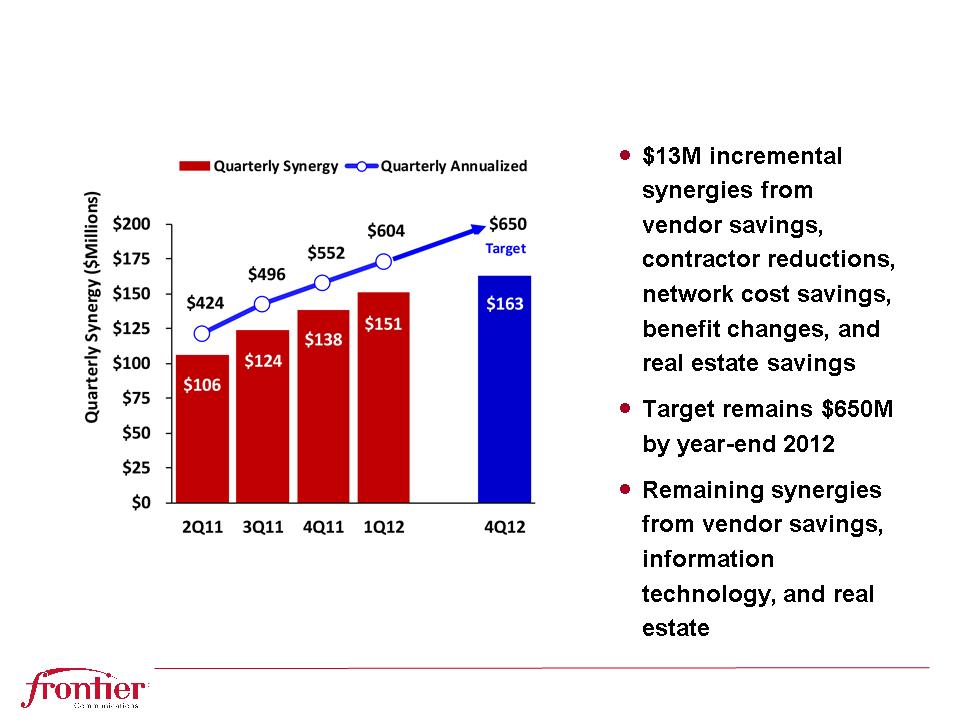

Cost Savings

Notes: $ Millions

Notes: $ Millions

15

Capital Expenditures

Notes: $ Millions. Numbers may not sum due to rounding.

Notes: $ Millions. Numbers may not sum due to rounding.

16

Cash Flow

● 1Q12 Adjusted

EBITDA margin 49%

EBITDA margin 49%

1Q12 Adjusted

EBITDA margin 49%

EBITDA margin 49%

● 1Q12 FCF payout

ratio of 39%

ratio of 39%

1Q12 FCF payout

ratio of 39%

ratio of 39%

● Building cash for debt

repayment and

business investment

repayment and

business investment

Building cash for debt

repayment and

business investment

repayment and

business investment

Notes: $ Millions; See Appendix for calculation of Free Cash Flow (FCF).

Notes: $ Millions; See Appendix for calculation of Free Cash Flow (FCF).

Credit & Liquidity

● Leverage (Net Debt /

EBITDA) has reduced

slightly

EBITDA) has reduced

slightly

Leverage (Net Debt /

EBITDA) has reduced

slightly

EBITDA) has reduced

slightly

● $1.3B of current

liquidity.

liquidity.

$1.3B of current

liquidity.

liquidity.

Notes: $ Millions. (1) Includes Restricted Cash; (2) Calculation excludes $63M of escrow cash.

Notes: $ Millions. (1) Includes Restricted Cash; (2) Calculation excludes $63M of escrow cash.

17

18

Debt Profile

● Annualized 1Q12 FCF after dividends of $613M

Annualized 1Q12 FCF after dividends of $613M

● 7.9% Weighted Average Cost of Debt. Next significant maturity is

$581M 6.25% notes due 1/15/13

$581M 6.25% notes due 1/15/13

7.9% Weighted Average Cost of Debt. Next significant maturity is

$581M 6.25% notes due 1/15/13

$581M 6.25% notes due 1/15/13

● Expect to file a new SEC shelf registration statement in the near

future to replace expired shelf

future to replace expired shelf

Expect to file a new SEC shelf registration statement in the near

future to replace expired shelf

future to replace expired shelf

19

Guidance

Notes: $ Millions. See Appendix for calculation of Free Cash Flow.

Notes: $ Millions. See Appendix for calculation of Free Cash Flow.

● Capital expenditures in 2012 include increased broadband expansion

and speed, fiber-to-the-cell, and other strategic investments

and speed, fiber-to-the-cell, and other strategic investments

Capital expenditures in 2012 include increased broadband expansion

and speed, fiber-to-the-cell, and other strategic investments

and speed, fiber-to-the-cell, and other strategic investments

● Expect additional integration expense and capital resulting from March

2012 conversion and other cost synergy initiatives

2012 conversion and other cost synergy initiatives

Expect additional integration expense and capital resulting from March

2012 conversion and other cost synergy initiatives

2012 conversion and other cost synergy initiatives

20

Appendix

21

Access Lines by State

22

Reconciliation of Non-GAAP Financial Measures

Notes: (1) The definition of free cash flow has been revised to add back severance and early retirement costs, with all prior periods conformed to the current

calculation.

calculation.

Notes: (1) The definition of free cash flow has been revised to add back severance and early retirement costs, with all prior periods conformed to the current

calculation.

calculation.

Notes: Numbers may not sum due to rounding.

Notes: Numbers may not sum due to rounding.

Three Months Ended

Three Months Ended

23

Reconciliation of Non-GAAP Financial Measures

Notes: Numbers may not sum due to rounding.

Notes: Numbers may not sum due to rounding.

Three Months Ended

Three Months Ended

24

Frontier Communications Corp.

(NASDAQ: FTR)

Investor Relations

Investor Relations

Frontier Communications Corp.

Frontier Communications Corp.

3 High Ridge Park

3 High Ridge Park

Stamford, CT 06905

Stamford, CT 06905

203.614.4606

203.614.4606

IR@FTR.com

IR@FTR.com