Attached files

| file | filename |

|---|---|

| 8-K - 8-K - TFS Financial CORP | d342724d8k.htm |

Investor Conference Call

May 3, 2012

Exhibit 99.1 |

2

Forward-Looking Statements

This presentation contains forward-looking statements, which can be identified by the use of such

words as estimate, project, believe, intend, anticipate, plan, seek, expect and similar

expressions. These forward-looking statements include: Statements of our goals, intentions and expectations; Statements regarding our business plans and prospects and growth and operating strategies; Statements concerning trends in our provision for loan losses and charge-offs; Statements regarding the asset quality of our loan and investment portfolios; and Estimates of our risks and future costs and benefits. These forward-looking

statements are subject to significant risks, assumptions and uncertainties, including, among other things, the following

important factors that could affect the actual outcome of future events:

Significantly increased competition among depository and other financial institutions; Inflation and changes in the interest rate environment that reduce our interest margins or reduce the

fair value of financial instruments;

General economic conditions, either nationally or in our market areas, including employment prospects

and conditions that are worse than expected;

Decreased demand for our products and services and lower revenue and earnings because of a recession

or other events; Adverse changes and volatility in the securities and credit markets; Legislative or regulatory changes that adversely affect our business, including changes in regulatory

costs and capital requirements and changes related to our ability to pay dividends and the

ability of Third Federal Savings and Loan Association of Cleveland, MHC to waive dividends;

Our ability to enter new markets successfully and take advantage of growth opportunities, and the

positive short-term dilutive effect of potential acquisitions or de novo branches, if any; Changes in consumer spending, borrowing and savings habits; Changes in accounting policies and practices, as may be adopted by the bank regulatory agencies, the

Financial Accounting Standards Board and the Public Company Accounting Oversight Board; Future adverse developments concerning Fannie Mae or Freddie Mac; Changes in monetary and fiscal policy of the U.S. Government, including policies of the U.S. Treasury

and the Federal Reserve Board;

Changes in policy and/or assessment rates of taxing authorities that adversely affect us; The timing and the amount of revenue that we may recognize; Changes in expense trends (including, but not limited to, trends affecting non-performing assets,

charge offs and provisions for loan losses);

The impact of the continuing governmental effort to restructure the U.S. financial and regulatory

system; The extensive reforms enacted in the Dodd-Frank Act which will impact us; The adoption of implementing regulations by a number of different regulatory bodies under the

Dodd-Frank Act, and uncertainty in the exact nature, extent and timing of such

regulations and the impact they will have on us; The impact of coming under the jurisdiction of new federal regulators; Changes in our organization, or compensation and benefit plans; Inability of third-party providers to perform their obligations to us; Adverse changes and volatility in real estate markets; A slowing or failure of the moderate economic recovery; The strength or weakness of the real estate markets and of the consumer and commercial credit sectors

and its impact on the credit quality of our loans and other assets; and.

The ability of the U.S. Federal Government to manage federal debt limits. Because of these and

other uncertainties, our actual future results may be materially different from the results indicated by these forward-looking statements.

|

3

Organized in 1997 as the mid-tier stock holding company for Third

Federal Savings & Loan Association of Cleveland (“Thrift”), which

was founded in 1938 by Ben and Gerome Stefanski

Completed first step IPO conversion in April 2007

TFSL (NASDAQ)

Financials at 3/31/12:

Total Assets:

$11.3B

Total Deposits:

$ 8.8B

Shareholders’

Equity:

$ 1.8B

Market Capitalization:

$ 2.9B

As of March 31, 2012, there were 308.9 million shares outstanding,

of which 73.5% were held by the Mutual Holding Company

Overview of TFS Financial Corporation |

4

Strategic Overview

Our business model is to originate and service first mortgage loans and continue to

service

existing

home

equity

loans

and

lines,

which

we

fund

with

core

retail

deposits

Historically

a

fixed

rate

lender,

but

Smart

Rate

adjustable

rate

mortgage

product

has

been major part of originations since introduced to market in July 2010

ARM portion of production (58% current fiscal YTD; 55% fiscal 2011; 19% fiscal

2010) First mortgage loans and retail deposits have been generated

mainly in OH/FL footprint. New state expansion began in May 2011, offering

our Smart Rate adjustable rate mortgage

to

refinance

customers

through

our

Customer

Service

and

Internet

Channels

and

using

our

underwriting

standards

and

processing

requirements

of

our

traditional

markets.

Only non-commissioned Third Federal associates have been and continue to be

used to gather applications, underwrite and process the requests to generate

mortgage loans and home equity loans and lines

First

mortgage

originations

continue

to

be

made

using

stringent,

conservative

lending

standards. For first mortgages originated during the current fiscal year, the

average FICO score was 783, and the average LTV was 62%.

Being a low-cost provider is a critical strategic advantage

Historically, stock repurchases and dividends have supplemented shareholder

returns, but are currently suspended by regulatory action.

|

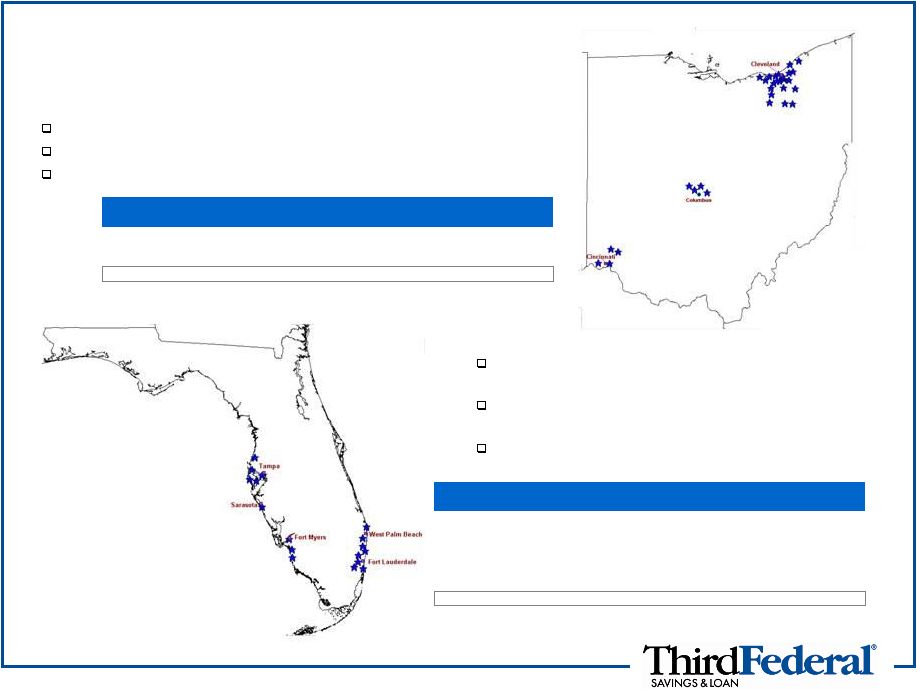

5

Ohio

22 full service branches in Northeast Ohio

4 loan production offices in the Columbus area (Central Ohio)

4 loan production offices in the Cincinnati area (Southwestern Ohio)

Markets of Operation

Florida

Organic, de novo expansion into Florida started in

2000

9 full service branches along the West Coast from

New Port Richey to Naples

8 full-service branches along the East Coast from

Palm Gardens to Hallandale

Source: SNL Financial for market data as of June 30, 2011

Deposits from Company data as of March 31, 2012

Deposits

Market

Market

MSA

Branches

($M)

Share (%)

Rank

Tampa-St.Petersburg-Clearwater, FL

5

1,159

1.86

8

Miami-Fort Lauderdale, FL

8

1,057

0.66

26

Cape Coral-Fort Myers, FL

2

275

2.14

14

Sarasota-Bradenton-Venice, FL

1

271

1.53

12

Naples-Marco Island, FL

1

128

1.18

17

Florida Totals

17

2,890

0.66

22

Deposits

Market

Market

MSA

Branches

($M)

Share (%)

Rank

Cleveland-Elyria-Mentor, OH

19

5,416

11.23

3

Akron, OH

3

517

4.21

8

Ohio Totals

22

5,933

2.64

9 |

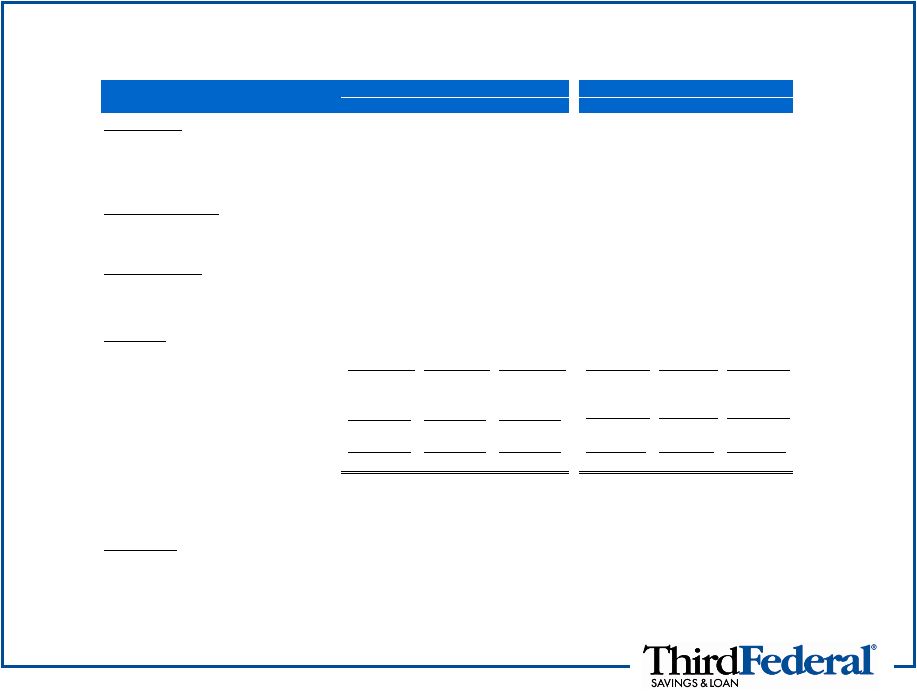

6

Financial Highlights

(Dollars in Thousands)

At, or for the year ended,

9/30/11

9/30/10

9/30/09

3/31/12

12/31/11

3/31/11

Balance Sheet

Assets ($)

10,892,948

11,076,027

10,598,840

11,286,768

11,058,126

10,885,060

Net Loans ($)

9,750,943

9,181,749

9,219,585

10,117,558

10,012,862

9,743,582

Deposits ($)

8,715,910

8,851,941

8,570,506

8,823,176

8,658,513

8,755,942

Common Equity ($)

1,773,924

1,752,897

1,745,865

1,799,803

1,795,960

1,752,982

Balance Sheet Ratios

Loans/ Deposits (%)

111.9

103.7

107.6

114.7

115.6

111.3

TCE / TA (%)

16.2

15.8

16.4

15.9

16.2

16.0

Thrift Only Ratios:

Core Capital Ratio (%)

13.9

12.1

12.5

13.5

13.8

13.7

Tier 1 Risk Based Ratio (%)

21.0

18.0

17.3

21.0

21.0

20.3

Total Risk Based Capital Ratio (%)

22.3

19.2

18.2

22.2

22.2

21.6

Profitability

Net Interest income ($)

247,648

227,506

230,075

65,785

64,255

60,901

Provision for loan losses ($)

(98,500)

(106,000)

(115,000)

(27,000)

(15,000)

(22,500)

Net Interest income after prov for loan losses ($)

149,148

121,506

115,075

38,785

49,255

38,401

Non-interest income ($)

30,982

58,638

67,384

6,411

5,709

8,267

Non-interest expense ($)

(168,055)

(161,933)

(162,388)

(43,320)

(42,479)

(43,975)

Income loss before income taxes ($)

12,075

18,211

20,071

1,876

12,485

2,693

Income tax benefit (expense) ($)

(2,735)

(6,873)

(5,676)

(854)

(4,026)

(469)

Net income loss ($)

9,340

11,338

14,395

1,022

8,459

2,224

Net interest margin (%)

2.32

2.16

2.20

2.42

2.40

2.29

Non-interest expense to average assets (%)

1.54

1.50

1.51

1.55

1.55

1.61

Asset Quality

NPAs/ Assets (%)

2.3

2.7

2.6

1.8

1.7

2.5

NCOs/ Avg Loans (%)

0.8

0.7

0.7

0.9

3.0

0.8

Reserves/ Loans (%)

1.6

1.4

1.0

1.0

1.0

1.5

Texas Ratio (NPAs & TDRs / TCE & LLR) (%)

19.6

20.9

17.4

16.9

16.5

20.5

At, or for the three months ended, |

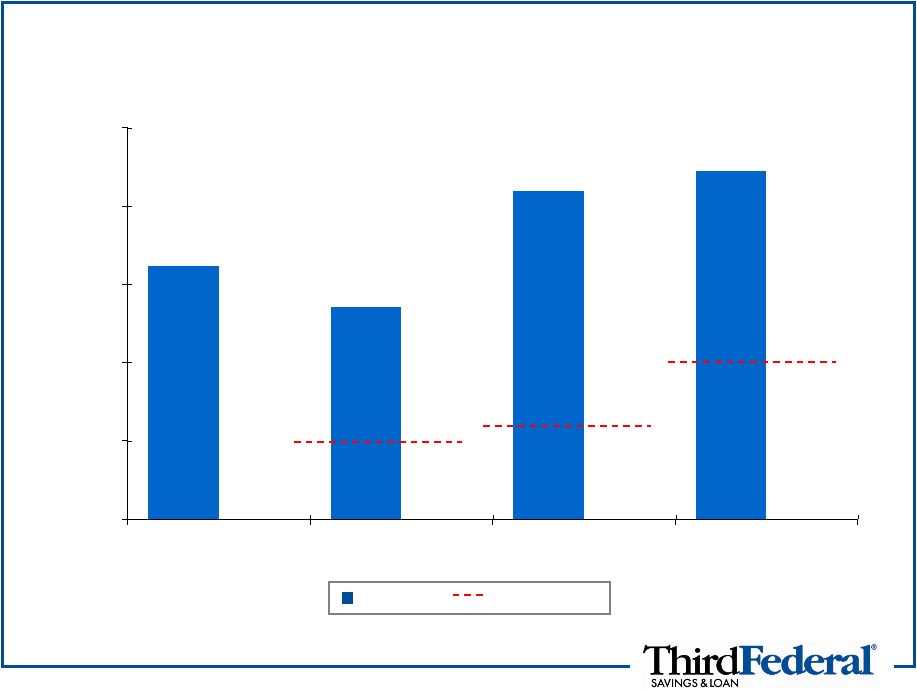

13.54%

21.33%

22.58%

15.87%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Tangible Common

Equity Ratio (TFSL)

Core Capital Ratio

(Thrift)

Tier 1 Risk-based Ratio

(Thrift)

Total Risk-Based

Capital Ratio (Thrift)

7

Capital Position as of March 31, 2012

Well Capitalized

6.00%

10.00%

5.00%

TFSL/Thrift |

8

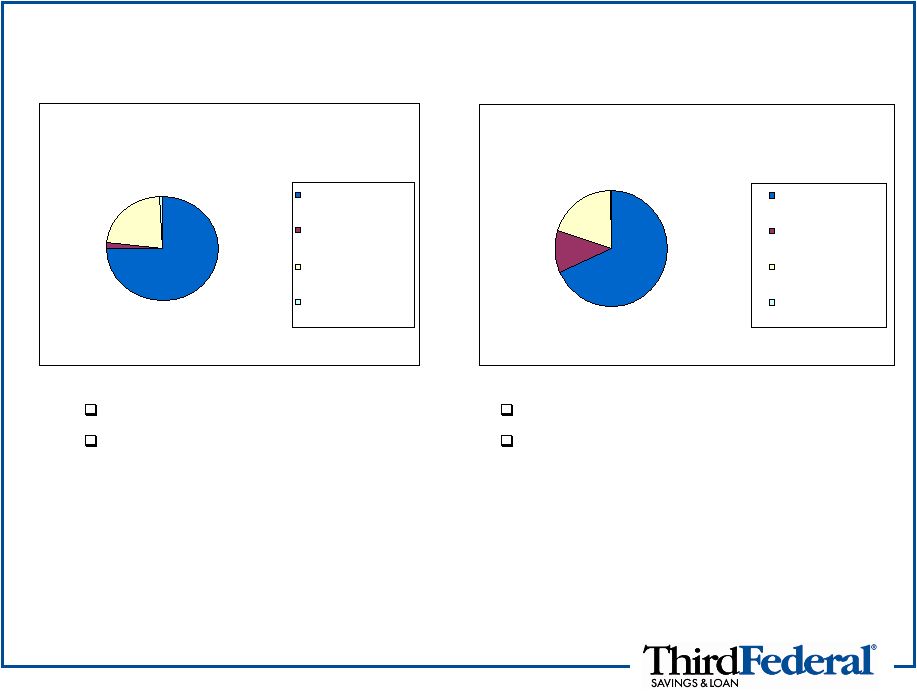

Loan and Deposit Balances

*About

Home

Today:

An

affordable

housing

program

targeted

toward

low

and

moderate

income

home

buyers

that

is

designed

to

teach the essential skills needed for successful homeownership. Most loans supported by private

mortgage insurance. Cumulative loan originations under this program have been less than

$20 million over the last three years. 79% of first mortgages in Ohio

Also service $4.6 billion in loans for

others

No brokered deposits

Average branch has $226 million in deposits

Gross Loan Balances 3/31/2012

2%

1%

23%

75%

Residential non-Home

Today

Residential Home

Today

Equity loans and lines of

credit

Other

Deposit Data 3/31/2012

0%

68%

12%

20%

Certificates of Deposit

Negotiable Order of

Withdrawal

Savings

Accrued Interest |

9

Adjustable Rate Loan Production

Smart Rate adjustable product began July 2010

In the six months ended 3/31/12, total loan production of $1.34 billion was

58% ARM and 42% fixed

Average credit score of quarter ended 3/31/12 ARM production was

782,

with average LTV of 60%

% Fixed vs. % Adjustable First Mortgage Loan Production

0

10

20

30

40

50

60

70

80

90

100

110

FY 2009

FY 2010

FY 2011

6 mo. ended

3/31/12

Variable

Fixed |

10

Adjustable Rate Growth

As of 3/31/12, 45% of all real estate loans, including equity loan products,

are adjustable rate

Total ARMs of $2.4 billion represents 31% of all first mortgages

at 3/31/12,

compared to 14% of all first mortgages as of 9/30/10

In May 2011, we began expansion of our Smart Rate adjustable rate

mortgage into 10 new states

PA, NJ, IL, NC, VA, CT, TN, CO, OR and WA

New state expansion represents $106 million in closed loans as of 3/31/12

0

5

10

15

20

25

30

35

Adjustable Mortgages as a Percentage of Total

First Mortgage Portfolio |

11

Loan Delinquencies and Charge-offs

3/31/12 loan balances include $246 million of loans held for sale

Charge-offs for quarter ended 12/31/11 impacted by charge-off of SVA,

which had a balance of $55.5 million at 9/30/11

Dollars in millions

Loan

Balances

3/31/12

3/31/12

9/30/11

9/30/10

3/31/12

12/31/11

9/30/11

9/30/10

Residential non-Home Today

Ohio

$6,063

1.1%

1.4%

1.9%

$4

$9

$9

$5

Florida

$1,327

3.4%

5.1%

5.2%

4

18

9

7

Other

264

0.3%

0.7%

1.5%

-

-

-

-

Total

$7,654

1.5%

2.1%

2.5%

$8

$27

$18

$12

Residential Home Today

Ohio

$221

20.3%

30.0%

34.8%

$6

$23

$7

$5

Florida

10

16.6%

32.1%

32.1%

-

1

-

-

Total

$231

20.1%

30.1%

34.6%

$6

$24

$7

$5

Home Equity Loans and Lines of Credit

Ohio

$902

1.2%

1.6%

2.0%

$1

$5

$10

$7

Florida

669

1.9%

3.3%

4.1%

3

14

29

33

California

279

1.0%

1.4%

1.5%

1

1

5

4

Other

466

1.3%

2.1%

2.4%

4

3

5

5

Total

$2,316

1.4%

2.2%

2.6%

$9

$23

$49

$49

Other

$62

0.7%

4.3%

4.2%

$0

$1

$1

$2

Overall Total

$10,263

1.9%

2.9%

3.5%

$23

$75

$75

$68

Quarter-end

Net Charge Offs

Delinquencies at:

FYE |

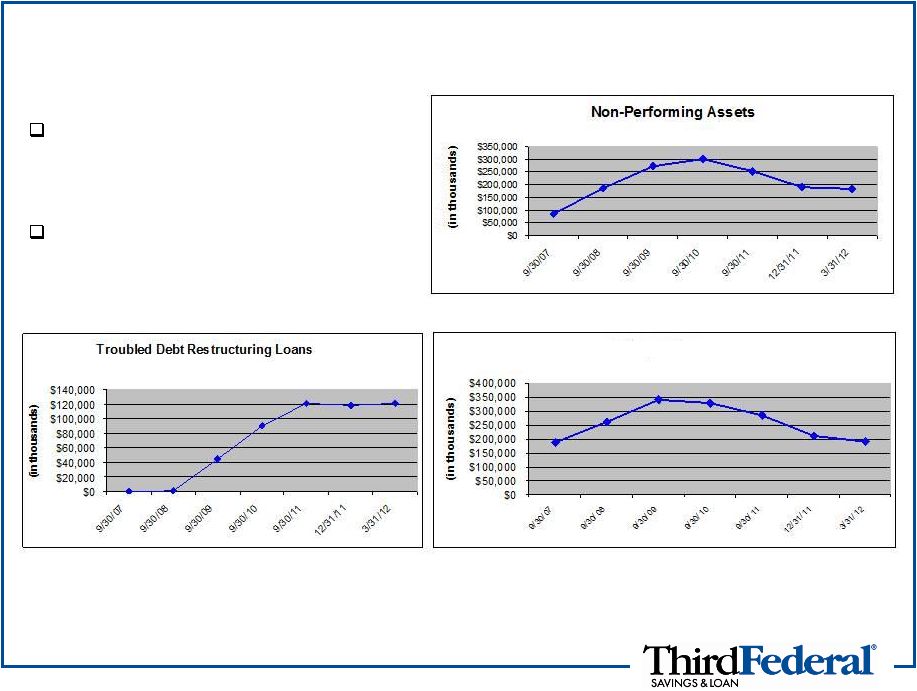

12

Loan Portfolio Trends

Non-performing assets and

delinquencies are trending

downward

Troubled debt restructuring

loans have leveled off

Delinquencies |

13

Regulatory Status

Company believes it has met all the key provisions of the February 7,

2011 MOU received from the OTS, subject to OCC/Fed regulatory

exam validation. We are awaiting results from the validation process

but

would

not

anticipate

final

actions

until

early

in

the

fourth

fiscal

quarter.

Interagency guidance suggests that performing junior liens that are

subordinate to non-accrual first liens should be considered non-accrual.

$14.5 million of performing ELOCs at March 31, 2012, were reclassified

as non-accrual. Minimal income statement or allowance impact, but the

non-performing assets increased accordingly.

Regulatory bodies: OCC (for thrift); Federal Reserve (holding

company); CFPB; FDIC

Dividends and stock buyback program still subject to regulatory 45-day

non-objection

No direction on proposed Fed rules for MHC dividend waivers

|

14

Investor Conference Call

May 3, 2012

Investor Questions |