Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Allied World Assurance Co Holdings, AG | d344603d8k.htm |

Proxy Update:

Approval of New Share Repurchase Program (Proposal 4 on Proxy Card)

April 27, 2012

Exhibit 99.1 |

Forward-Looking Statements & Safe Harbor

2

This presentation may contain certain statements, estimates and forecasts with respect to future

performance and events. These statements, estimates and forecasts are

"forward-looking statements". In some cases, forward-looking

statements can be identified by the use of forward-looking terminology such as "may,"

“might,” “will," “should,” "expect," “plan,”

"intend," "estimate," "anticipate," "believe,” “predict,” “potential”

or "continue" or the negatives thereof or variations thereon or similar terminology. All

statements other than statements of historical fact included in this presentation are

forward-looking statements and are based on various underlying assumptions and

expectations and are subject to known and unknown risks, uncertainties and assumptions,

may include projections of our future financial performance based on our growth strategies

and anticipated trends in our business. These statements are only predictions based on our

current expectations and projections about future events. There are important

factors that could cause our actual results, level of activity, performance or

achievements to differ materially from the results, level of activity, performance or

achievements expressed or implied in the forward-looking statements. As a result, there can

be no assurance that the forward-looking statements included in this presentation will prove

to be accurate or correct. In light of these risks, uncertainties and assumptions,

the future performance or events described in the forward-looking statements in this

presentation might not occur. Accordingly, you should not rely upon

forward-looking statements as a prediction of actual results and we do not assume any

responsibility for the accuracy or completeness of any of these forward-looking

statements that may be made from time to time. We are under no obligation (and

expressly disclaim any such obligation) to update or revise any forward- looking

statements, whether as a result of new information, future developments or otherwise. |

Background

Allied World is a Swiss domiciled company whose shares have traded

on the New York Stock Exchange (NYSE: AWH) since its IPO in 2006

Allied World is recommending that shareholders approve a new $500

million, two year share repurchase program

For further information, please see Proposal 4 (pages 24-25) in the

company’s Definitive Proxy Statement, filed with the SEC on March

16, 2012. The proposal includes:

All common shares purchased under our new repurchase program

will be designated for cancellation

As required by Swiss law, cancellation of shares will be subject

to

shareholder approval at Allied World’s annual shareholder meeting

in 2013.

Allied World has effectively used share repurchases as part of a

broader capital management strategy to enhance shareholder value

3 |

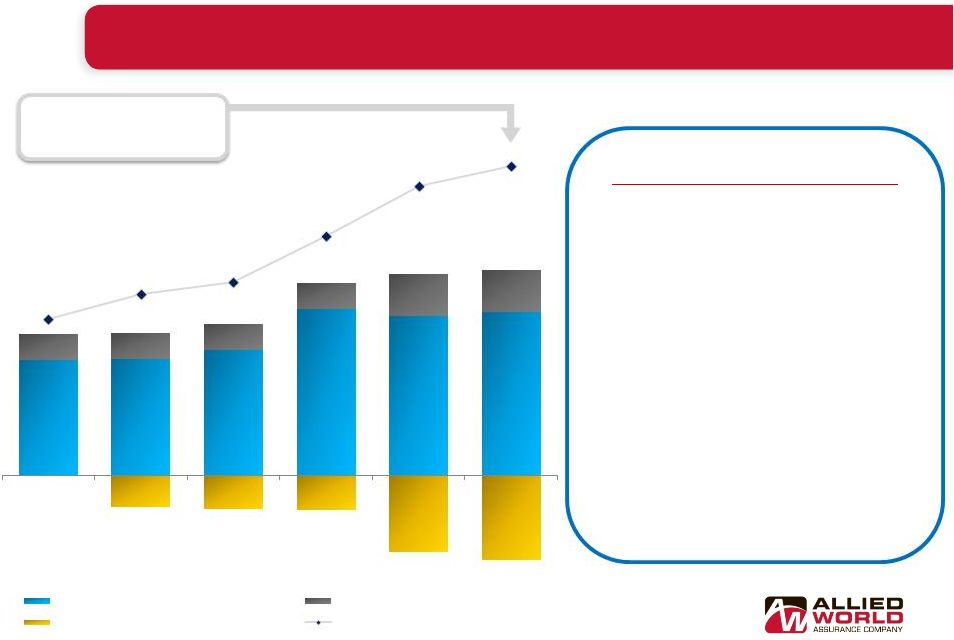

Active Capital

Management Improves Shareholder Value * Excludes $243.8 million syndicated loan

which was repaid on February 23, 2009 4

Capital Management History

o

$210 million of common dividends paid

since going public in 2006

o

$563 million of shares repurchased from

AIG in December 2007

o

Current $500 million share repurchase

program implemented in 2010

•

$174 million remaining capacity at

December 2011

o

$505 million of shares and warrants

repurchased from founders in 2010

o

$53.6 million warrant repurchased from

founder in first quarter 2011

(In millions, except for per share amounts)

Diluted book value per

share has more than

doubled since 2006

Shareholder's Equity

Debt

Accumulated Share Repurchases & Dividends Paid

Diluted Book Value per Share

-$611

-$646

-$682

-$1,475

-$1,658

-$9

$2,220

$2,240

$2,417

$3,213

$3,075

$3,149

$499

$499

$499

$499

$798

$798

$2,719

$2,739

$2,916

$3,712

$3,873

$3,947

$35.26

$42.53

$46.05

$59.56

$74.29

$80.11

2006

2007

2008*

2009

2010

2011 |

Growth in book

value per share calculated by taking change in diluted book value per share from December 2006 through

December 2011 adjusted for dividends paid or declared.

5

Peer Average = 80%

Five Year Growth in Diluted Book Value per Share

2007 -

2011

Active Capital Management Improves Shareholder Value

139%

118%

93%

89%

86%

80%

79%

76%

75%

53%

46%

AWH

ACGL

ENH

AHL

HCC

RLI

AXS

WRB

NAVG

MKL

AGII |

ISS

Recommendation ISS proxy advisory services is recommending shareholders vote

“Against” Allied World’s new $500 million share repurchase program

stating that the “proposal would allow the company to repurchase more than 10

percent of its share capital”

•

In continental European markets, ISS supports share repurchase plans

subject to the following limitations:

1.

The company is allowed to hold no more than 10% of share capital

in treasury

2.

The plan is subject to a duration of no more than 5 years

3.

The plan includes a repurchase limit equal to 10% of share capital

•

Our understanding is that ISS has no such limitation on repurchase activity

for U.S. domiciled companies

ISS

does

note

“this

notwithstanding,

some

shareholders

may

be

less

concerned about the potential volume of the company’s share repurchase

plans since shares acquired under this authorization would be designated for

cancellation at a future annual meeting of shareholders and would not be

used for reissuance.”

6 |

Allied

World’s View While AWH is a Swiss-domiciled company, it trades on the NYSE with a

significant U.S. shareholder base

However, even if ISS limitations are viewed within European framework:

1.

The repurchased shares are being designated for cancellation, will not be re-

issued for any purpose and therefore will not be subject to the Swiss statutory

provisions that prohibit the company from holding in treasury more than 10%

of its aggregate shares

2.

The duration of the share repurchase program is two years; well within the five

year prescribed window

3.

Given that the Allied World program has a two year duration, on an annualized

basis it is unlikely that Allied World would exceed ISS’

10% limitation

7 |

Allied World

Recommendation Allied World has exhibited a long history of prudent capital

management which has been accretive to shareholder value

Diluted book value per share has more than doubled since 2006

Allied World has maintained a strong capital base and credit ratings:

Current Financial Strength ratings are “A”

(Excellent) from A.M. Best, “A”

(Strong) from S&P and “A2”

(Good) from Moody’s

Current senior bond ratings are BBB+ from S&P and Baa1 from Moody’s

8

We

believe

it

is

in

the

best

interest

of

shareholders

to

provide

Allied World

with the flexibility to repurchase shares as outlined in the Proxy Statement

Allied World recommends shareholders vote “For”

all of Allied World’s

proposals at its 2012 Annual Shareholder Meeting, including Proposal 4 to

approve our new $500 million share repurchase program |

Non-GAAP

Financial Measures In

presenting

the

company's

results,

management

has

included

and

discussed in this

presentation a financial measure that is not a generally accepted accounting principle

("non- GAAP") within the meaning of Regulation G as promulgated by the U.S.

Securities and Exchange Commission. Management believes that this non-GAAP measure,

which may be defined differently by other companies, better explains the company's

results of operations in a

manner

that

allows

for

a

more

complete

understanding

of

the

underlying trends in the

company's business. However, this measure should not be viewed as a substitute for those

determined in accordance with generally accepted accounting principles ("U.S.

GAAP"). The company has included "diluted book value per share" because it

takes into account the effect of dilutive securities; therefore, the company believes

it is an important measure of calculating shareholder returns. See slide 10 for a

reconciliation of the non-GAAP measure used in this presentation to its most

directly comparable GAAP measure. 9 |

Non-GAAP

Financial Measures - Reconciliations

10

ALLIED WORLD ASSURANCE COMPANY HOLDINGS, AG

UNAUDITED DILUTED BOOK VALUE PER SHARE RECONCILIATION

(Expressed in thousands of United States dollars, except share and per share amounts)

As of

As of

December 31,

December 31,

2011

2010

Price per share at period end

62.93

$

59.44

$

Total shareholders' equity

3,149,022

$

3,075,820

$

Basic common shares outstanding

37,742,131

38,089,226

Add: unvested restricted share units

249,251

571,178

Add: Performance based equity awards

889,939

1,440,017

Add: employee share purchase plan

11,053

10,576

Add: dilutive options/warrants outstanding

1,525,853

3,272,739

Weighted average exercise price per share

45.72

$

35.98

$

Deduct: options bought back via treasury method

(1,108,615)

(1,980,884)

Common shares and common share

equivalents outstanding

39,309,612

41,402,852

Basic book value per common share

83.44

$

80.75

$

Diluted book value per common share

80.11

$

74.29

$

|