Attached files

| file | filename |

|---|---|

| 8-K - FIRST MERCHANTS CORPORATION - 1ST QUARTER 2012 EARNINGS PRESENTATION SLIDES - FIRST MERCHANTS CORP | f8kearningsslide04262012.htm |

1

First Merchants Corporation

1st Quarter 2012

Earnings Call

1st Quarter 2012

Earnings Call

April 26, 2012

2

Michael C. Rechin

President

and Chief Executive Officer

3

Forward-Looking Statement

FORWARD-LOOKING STATEMENT

The Corporation may make forward-looking statements about its

relative business outlook. These forward-looking statements and

all other statements made during this meeting that do not

concern historical facts are subject to risks and uncertainties that

may materially affect actual results.

Specific forward-looking statements include, but are not limited

to, any indications regarding the financial services industry, the

economy and future growth of the balance sheet or income

statement.

Please refer to our press releases, Form 10-Qs and 10-Ks

concerning factors that could cause actual results to differ

materially from any forward-looking statements.

4

1st QUARTER 2012 HIGHLIGHTS

• EPS

– $.46 per share (171% year-over-year growth)

– Core EPS: $.25 per share (47% year-over-year growth)

– SCB bargain purchase gain of $.21 per share

• SCB FDIC-Modified Whole-Bank Transaction

• Core Revenue Growth

– $1.7M increase year-over-year

• Balance Sheet Well Positioned for Growth

– Strong Core Funding Base

– Tangible Common Equity: 7.07%

– Tier 1 Common: 9.20%

– Lower Risk Profile

5

Mark K. Hardwick

Executive Vice President

and Chief Financial Officer

6

2010 2011 Q1-’11

Q1-’12

1. Investments

$ 827 $ 946 $ 886 $ 960

2. Loans 2,857 2,731 2,766 2,815

3. Allowance (83) (71) (81) (70)

4. CD&I & Goodwill 154 150 153 150

5. BOLI 97 124 102 123

6. Other 319 293 291 258

7. Total Assets $4,171 $4,173 $4,117 $4,236

($ in Millions)

TOTAL ASSETS

7

Loan Composition (as of 3/31/12)

YTD Yield = 5.17%

LOAN AND CREDIT DETAIL

8

INVESTMENT PORTFOLIO

(as of 3/31/12)

(as of 3/31/12)

9

2010 2011

Q1-’11 Q1-’12

1. Customer Non-Maturity

Deposits

$2,127 $2,196 $2,083 $2,273

2. Customer Time Deposits 996 816 943 836

3. Brokered Deposits 146 123 126 170

4. Borrowings 277 378 305 287

5. Other Liabilities 28 34 56 31

6. Hybrid Capital 142 111 142 111

7. Preferred Stock (CPP) 68 - 68 -

8. Preferred Stock (SBLF) - 91 - 91

9. Common Equity

387 424 394 437

10. Total Liabilities and Capital $4,171 $4,173 $4,117 $4,236

($ in Millions)

TOTAL LIABILITIES AND CAPITAL

10

DEPOSITS

(as of 3/31/12)

(as of 3/31/12)

11

CAPITAL RATIOS

2010 2011 Q1-’11 Q1-’12

1. Total Risk-Based

Capital Ratio 15.74% 16.54% 15.66% 16.39%

2. Tier 1 Risk-Based

Capital Ratio 12.82% 13.92% 13.05% 14.14%

3. Leverage Ratio 9.50% 10.17% 9.80% 10.61%

4. Tier 1 Common Risk-

Based Capital Ratio 7.64% 8.83% 7.75% 9.20%

5. TCE/TCA 5.86% 6.84% 6.16% 7.07%

12

|

|

Q1 - '10

|

Q2 - '10

|

Q3 - '10

|

Q4 - '10

|

Q1 - '11

|

Q2 - '11

|

Q3 - '11

|

Q4 - '11

|

Q1 - '12

|

|

Net Interest Income - FTE ($ in millions)

|

$37.8 |

$37.7

|

$37.2 |

$36.7

|

$36.9

|

$37.3 |

$37.3

|

$37.6 |

$37.6 |

|

Tax Equivalent Yield on Earning

Assets |

5.39%

|

5.38%

|

5.38%

|

5.13%

|

5.11%

|

5.04%

|

5.01%

|

4.83%

|

4.74%

|

|

Cost of Supporting Liabilities

|

1.57%

|

1.48%

|

1.45%

|

1.30%

|

1.16%

|

1.05%

|

0.99%

|

0.84%

|

0.78%

|

|

Net Interest Margin

|

3.82%

|

3.90%

|

3.93%

|

3.83%

|

3.95%

|

3.99%

|

4.02%

|

3.99%

|

3.96%

|

|

|

NET INTEREST MARGIN

13

2010 2011 Q1-’11 Q1-’12

1. Service Charges on Deposit Accounts $13.3 $12.0 $

2.8 $2.8

2. Trust

Fees 7.7 7.7 2.0

2.0

3. Insurance Commission Income 6.2 5.7 1.9 1.7

4. Electronic Card Fees 6.1

6.5 1.5 1.7

5. Cash Surrender Value of Life Ins 2.1 2.6 0.6 1.4

6. Gains on Sales Mortgage Loans 6.8 7.4 1.9 2.0

7. Securities Gains/Losses 1.9 2.0 0.1 0.8

8. Gain on FDIC-Modified Whole-Bank

Transaction - -

- 9.1

9. Other 4.4 5.2 1.1 1.2

10. Total $48.5 $49.1 $11.9 $22.7

11. Adjusted Non-Interest Income1 $46.6 $47.1 $11.8 $12.8

1Adjusted for Bond Gains & Losses and Gain on FDIC-Modified Whole-Bank Transaction

($ in Millions)

NON-INTEREST INCOME

14

NON-INTEREST EXPENSE

2010

2011

Q1-’11 Q1-’12

1. Salary & Benefits $73.3 $74.7 $17.2 $19.4

2. Premises & Equipment 17.2 16.9 4.5 4.4

3. Core Deposit Intangible 4.7 3.5 1.1 0.5

4. Professional Services 1.4 2.2 0.6 0.7

5. OREO/Credit-Related Expense 14.6

10.6 3.2 2.2

6. FDIC Expense 8.1 5.5 2.1 1.1

7. Outside Data Processing 5.1 5.7 1.4 1.4

8. Marketing 2.0 2.0 0.4 0.4

9. Other 15.9 14.8 3.4 3.9

10. Total $142.3 $135.9 $33.9 $34.0

($ in Millions)

15

EARNINGS

2010

2011 Q1-’11 Q1-’12

1. Net Interest Income-FTE $149.4 $149.1 $36.9 $37.6

2. Non Interest

Income1 46.6 47.1 11.8 12.8

3. Non Interest Expense

(142.3) (135.9) (33.9) (34.0)

4. Pre-Tax Pre-Provision Earnings $53.7 $60.3 $14.8 $16.4

5. Provision

(46.5) (22.6) (5.6) (4.9)

6. Adjustments1

1.9 2.0 0.1 9.9

7. Taxes - FTE (2.3)

(14.4) (3.8) (7.1)

8. Gain/(Loss) on CPP/Trust Preferred 10.1 (12.3) — —

9. Preferred Stock Dividend (5.2) (4.0)

(1.0) (1.1)

10. Net Income Avail. for Distribution $11.7 $ 9.0 $ 4.5 $13.2

11. EPS $0.48 $0.34

$0.17 $0.46

1Adjusted for Bond Gains & Losses and Gain on FDIC-Modified Whole-Bank Transaction

($ in Millions)

16

EARNINGS PER SHARE

1

1

2

2010 Q1 Q2 Q3 Q4 Total

1. Actual $ .01 $ .35 $ .02 $ .10 $ .48

2. Adjusted $ .01 ($.05) $ .02 $ .10 $ .08

2011 Q1 Q2 Q3 Q4 Total

3. Actual $ .17 $ .18 ($.25) $ .24 $ .34

4. Adjusted $ .17 $ .18 $ .21 $ .24 $ .80

2012

Q1 Q2 Q3 Q4 Total

5. Actual $ .46 - - - $ .46

6. Adjusted $ .25 - - - $ .25

1Adjusted for gains and losses on CPP/Trust Preferred refinance and repayment net of

taxes (Line 8 on slide 15)

2Adjusted for Gain on FDIC-Modified Whole-Bank Transaction

17

John J. Martin

Senior Vice President

and Chief Credit Officer

18

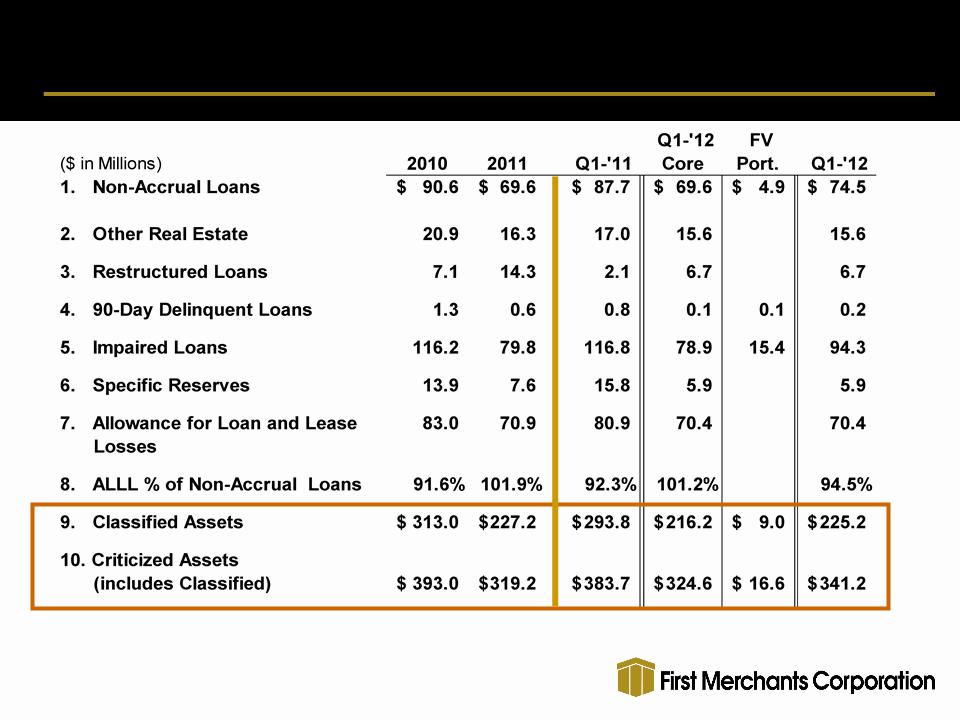

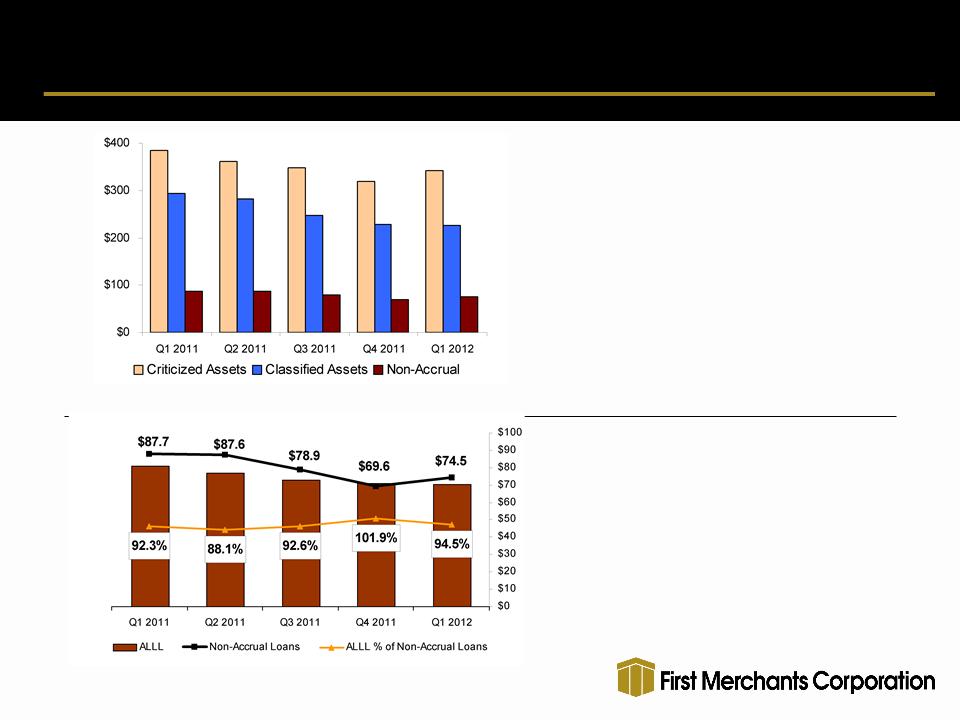

ASSET QUALITY SUMMARY

19

CREDIT METRICS AND ALLL COVERAGE

Criticized Assets down 11.1% Q1-’12

compared to Q1-’11 and up 6.9% linked

quarter

compared to Q1-’11 and up 6.9% linked

quarter

Classified Assets down 23.3% Q1-’12

compared to Q1-’11 and down .9% linked

quarter

compared to Q1-’11 and down .9% linked

quarter

Non-Accrual Loans down 15.1% Q1-’12

compared to Q1-’11 and up 7.0% linked

quarter

compared to Q1-’11 and up 7.0% linked

quarter

*Q1 2012 includes loans acquired at Fair Value

Allowance for Loan and Lease

Losses as a % of Non-Accrual

Loans reduced to 94.5%

Losses as a % of Non-Accrual

Loans reduced to 94.5%

Acquired Fair Value portfolio with

$4.9M in newly identified Non-

Accruals; Core Non-Accruals flat for

quarter.

$4.9M in newly identified Non-

Accruals; Core Non-Accruals flat for

quarter.

($ in Millions)

($ in Millions)

20

NON-PERFORMING ASSET RECONCILIATION

|

($ in millions)

|

Q4-’10

|

Q1-’11

|

Q2-’11

|

Q3-’11

|

Q4-’11

|

Q1-’12*

|

|

1. Beginning Balance NPAs & 90+ Days Delinquent

|

$ 130.8

|

$ 120.0

|

$ 107.6

|

$ 109.5

|

$ 106.7

|

$ 100.8

|

|

Non-Accrual

|

|

|

|

|

|

|

|

2. Add: New Non-Accruals*

|

27.4

|

11.7

|

26.7

|

21.4

|

10.2

|

16.4

|

|

3. Less: To Accrual/Payoff/Restructured

|

( 14.5)

|

( 3.2)

|

( 8.3)

|

( 8.7)

|

( 7.6)

|

( 2.7)

|

|

4. Less: To OREO

|

( 7.0)

|

( 2.0)

|

( 1.6)

|

( 9.7)

|

( 1.2)

|

( 2.5)

|

|

5. Less: Charge-offs*

|

( 13.9)

|

( 9.4)

|

(16.9)

|

(11.6)

|

( 10.7)

|

( 6.3)

|

|

6. Increase /(Decrease): Non-Accrual Loans

|

(8.0)

|

( 2.9)

|

( .1)

|

(8.6)

|

(9.3)

|

4.9

|

|

Other Real Estate Owned (ORE)

|

|

|

|

|

|

|

|

7. Add: New ORE Properties

|

7.2

|

2.2

|

1.6

|

9.7

|

1.2

|

2.5

|

|

8. Less: ORE Sold

|

(4.2)

|

( 3.6)

|

( 1.6)

|

( 5.0)

|

(3.3)

|

( 1.8)

|

|

9. Less: ORE Losses (write-downs)

|

( 3.6)

|

( 2.5)

|

( 1.6)

|

( 0.7)

|

(1.1)

|

( 1.4)

|

|

10. Increase /(Decrease): ORE

|

( .6)

|

( 3.9)

|

( 1.6)

|

4.0

|

( 3.2)

|

( .7)

|

|

11. Increase /(Decrease): 90 Days Delinquent*

|

( 4.0)

|

( 0.6)

|

( 0.5)

|

1.4

|

( 1.0)

|

( 0.4)

|

|

12. Increase /(Decrease): Restructured Loans

|

1.8

|

( 5.0)

|

4.1

|

.4

|

7.6

|

(7.6)

|

|

13. Total NPA Change

|

(10.8)

|

(12.4)

|

1.9

|

(2.8)

|

(5.9)

|

(3.8)

|

|

14. Ending Balance NPAs & 90+ Days Delinquent

|

$ 120.0

|

$ 107.6

|

$ 109.5

|

$ 106.7

|

$ 100.8

|

$ 97.0

|

25.8%

*Q1-’12 Includes FV portfolio loans acquired.

21

NET CHARGE-OFFS, PROVISION AND ALLOWANCE

($ in Millions)

22

Credit Summary

• Asset quality trends continue to improve

• Decrease in Restructured Loans following their return to

market terms, demonstrated performance and loss

recognition

market terms, demonstrated performance and loss

recognition

• Charge-offs and provision expense lower and in line with

improvement in credit quality

improvement in credit quality

• Total loan pipeline improving driven by mortgage and

commercial loans

commercial loans

• Fair Value portfolio of $89.7M with a composition similar

to core portfolio

to core portfolio

23

Michael C. Rechin

President

and Chief Executive Officer

24

Overview of 2012 Strategy and Tactics

“Growth and Top-Tier Performance”

“Growth and Top-Tier Performance”

• Shelby County Bank integration

• Grow revenue by intensifying revenue-generating

activity:

activity:

– Market coverage tactics . . . including SCB

– Additional investment in business banking professionals in key

markets

markets

– Retail CRM and sales management system

• Implement systems and processes to improve efficiency:

– Banking center rationalization

– Enhance systems in consumer collections, human resources

and finance

and finance

• Seek non-organic growth opportunities

25

CONTACT INFORMATION

First Merchants Corporation common stock is

traded on the NASDAQ Global Select Market

under the symbol FRME.

traded on the NASDAQ Global Select Market

under the symbol FRME.

Additional information can be found at

www.firstmerchants.com

Investor inquiries:

David L. Ortega

Investor Relations

Telephone: 765.378.8937

dortega@firstmerchants.com