Attached files

| file | filename |

|---|---|

| EX-5.1 - EXHIBIT 5.1 - BLACKSTRATUS, INC. | a2208510zex-5_1.htm |

| EX-23.1 - EX-23.1 - BLACKSTRATUS, INC. | a2208510zex-23_1.htm |

As filed with the Securities and Exchange Commission on April 13, 2012

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

BLACKSTRATUS, INC.

(Exact name of registrant as specified in its charter)

Delaware |

7371 (Primary Standard Industrial Classification Code Number) |

22-3687038 (IRS Employer Identification Number) |

1551 South Washington Avenue

Piscataway, New Jersey, 08854

(732) 393-6000

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

Dale W. Cline

Chief Executive Officer

BlackStratus, Inc.

1551 South Washington Avenue

Piscataway, New Jersey, 08854

(732) 393-6000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||

Francis J. Feeney, Jr., Esq. Michael S. Turner, Esq. DLA Piper LLP (US) 33 Arch Street, 26th Floor Boston, MA 02110 Tel: (617) 406-6000 Fax: (617) 406-6100 |

Yvan-Claude Pierre, Esq. William Haddad, Esq. Reed Smith LLP 599 Lexington Avenue New York, New York 10022 Tel: (212) 521-5400 Fax: (212) 521-5450 |

|

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the Registration Statement has been declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company ý |

CALCULATION OF REGISTRATION FEE

|

||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1) |

Amount of Registration Fee(2) |

||

|---|---|---|---|---|

Common stock, par value $0.0001 per share |

$20,000,000.00 | $2,292.00 | ||

|

||||

- (1)

- Estimated

solely for the purpose of calculating the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as

amended.

- (2)

- Calculated pursuant to Rule 457(o) based on an estimate of the proposed maximum aggregate offering price and includes the offering price of shares that the underwriters have the option to purchase to cover over-allotments, if any.

The registrant amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall hereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until the registration statement shall become effective on such date as the Commission, acting pursuant to Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS SUBJECT TO COMPLETION DATED APRIL 13, 2012

Shares

Common Stock

![]()

This is a firm commitment initial public offering of shares of common stock of BlackStratus, Inc. No public market currently exists for our shares. We anticipate that the initial public offering price of our shares of common stock will be between $ and $ per share.

We intend to apply to list our shares of common stock for trading on the NASDAQ Capital Market under the symbol "BLKS." No assurance can be given that our application will be approved.

Investing in our common stock involves a high degree of risk. See "Risk Factors" beginning on page 12 of this prospectus for a discussion of information that should be considered in connection with an investment in our common stock.

Neither the Securities and Exchange Commission nor any state or foreign securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| |

Per Share | Total | ||

|---|---|---|---|---|

Public offering price |

$ | $ | ||

Underwriting discounts and commissions(1) |

$ | $ |

- (1)

- Does

not include a non-accountable expense allowance equal to 1% of the gross proceeds of this offering payable to Aegis Capital Corp., the

underwriter. See "Underwriting" for a description of compensation payable to the underwriter.

We have granted a 45-day option to the underwriter to purchase up to additional shares of common stock solely to cover over-allotments, if any.

The underwriters expect to deliver our shares to purchasers in the offering on or about , 2012.

Aegis Capital Corp

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus. Neither we nor the underwriters have authorized anyone to provide you with information different from that contained in this prospectus. We and the underwriters are offering to sell shares of common stock and seeking offers to buy shares of common stock only in jurisdictions where such offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of common stock.

We own, have rights to or have applied for the trademarks and trade names that we use in conjunction with our business, including our logo. All other trademarks and trade names appearing in this prospectus are the property of their respective holders.

In this prospectus we rely on and refer to information and statistics regarding our industry. We obtained this market data from independent industry reports or other publicly available information. Some data is also based on our good faith estimates, which are derived from our review of internal surveys and studies, as well as independent industry reports.

The following summary highlights information contained in this prospectus and should be read in conjunction with the more detailed information contained in this prospectus and the consolidated financial statements and related notes appearing elsewhere in this prospectus. Before you decide to invest in our common stock, you should read the entire prospectus carefully, including the "Risk Factors" section in this prospectus.

Unless the context otherwise requires, we use the terms "BlackStratus," the "Company," "we," "us" and "our" in this prospectus to refer to BlackStratus, Inc. and its subsidiaries. Unless the context requires otherwise or we specifically indicate otherwise, the information in this prospectus assumes that the underwriters do not exercise their over-allotment option. Unless otherwise indicated, all share and per share numbers in the prospectus have been retroactively adjusted to reflect a 1-for- reverse stock split of our common stock, which was effective on , 2012.

Business Overview

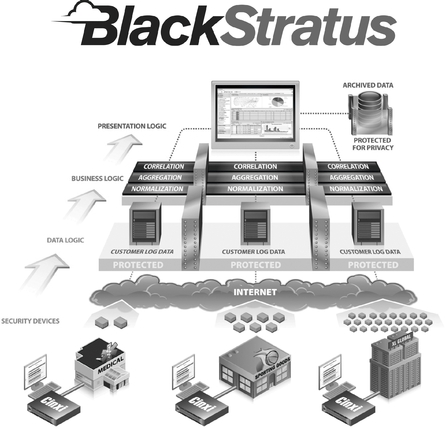

We are a leading provider of cloud-based security information and event management (SIEM) software solutions deployed and operated by "Security as a Service" (SECaaS) providers of all sizes, government agencies and individual enterprises. Our SIM One technology is used by organizations worldwide to detect, prevent and defend against both major and minor IT security breaches from the end point to the data center, to the "Cloud." The SIM One technology delivers a correlated and centralized, real-time view of alerts, status messages and a variety of security events generated by disparate third-party security products (such as firewalls, anti-virus products, intrusion detection software, etc.), allowing security professionals to identify and stop potential threats in real time. Specifically, our technology allows our SECaaS partners to sell multiple types of cloud-based security services to their customers, including security event analysis and notifications about real-time threats to the customer's IT infrastructure, in addition to providing continuous and secure logging of all of their customer's security event data for compliance and audit purposes. Further, our own direct enterprise and government customers deploy our technology within their own private clouds for multiple location and agency use, or deploy it within their individual data centers for use by their security operations team.

Formed in 1999 selling into enterprise security operations centers, BlackStratus changed its market focus beginning in late 2008 to service the rapid growing cloud-based SECaaS market. Since changing our focus we have achieved the following:

- •

- Transformed our revenue mix from primarily enterprise SIM One deployments in 2008 to a majority of SECaaS partners and

logging sales in 2011 (52%).

- •

- Architected our technology to address unique cloud security requirements such as multi-tenancy and the ability to have

multiple customers managed off of a single platform.

- •

- Signed and partnered with three multinational telecommunication carriers on three separate continents all with revenues in

excess of $20B US.

- •

- Had our technology adopted by over fifteen SECaaS partners worldwide.

- •

- In 2009, completed the successful acquisition of HighTower Software expanding our product offerings and market reach.

BlackStratus technology plays an important role in managing the growing big data security challenges and scale issues created by the rise of three interrelated market forces, cloud computing, mobile device proliferation, and the rise of social networks. Whether placing their customer

1

information into the Cloud through SalesForce.com, allowing employees access to email on their iPhones, or having employees post to Facebook from the company network, IT administrators are now overwhelmed by the serious security exposure these trends have unleashed on their networks. BlackStratus technology actively and in real time, detects, prevents and defends against the growing and challenging multitude of security challenges wrought by these productive but disruptive technology trends. Our ability to consume and correlate millions of events at a time through the Cloud or a network and identify and prevent security breaches in real time is a mission critical component of our customers and partners ability to manage through these market forces and to meet the legal obligations of their service level agreements (SLAs) with their customers.

Our Industry

Managed Security Service Partners (MSSPs) offer end-user customers their expertise to manage security on-site in the customer's environment and, increasingly, off-site and in the Cloud through SECaaS offerings. The rapid growth of and demand for MSSP providers and SECaaS solutions is primarily the result of companies and enterprises responding to increasing regulatory requirements, decreasing IT budgets, the capital expense involved in deploying security technology and the difficulty and expense of hiring and retaining qualified IT personnel with the requisite security expertise.

According to the November 2011 Gartner Magic Quadrant report, MSSPs realized North American revenue of $2.3 billion in 2010, up from $1.8 billion in 2009. The report estimated that MSSP revenue would increase to $2.8 billion in 2011. The report also states that the global economic environment continues to drive businesses to limit hiring and increase demand for managed services. Gartner expects growth to continue at a compound annual growth rate of 14% from 2011 to 2015, which suggests that it will be one of the higher growth sectors in the IT industry.

Our Solutions and Products

Our SIM One platform detects, prevents and defends against security breaches at the local network level as well as in the Cloud. It identifies in real-time both potential and actual high severity security events presenting the data in a rich, consolidated graphical view for security professionals to prioritize responses to threats and risks in their, or their customer's, cloud and IT infrastructure. The platform collects security event data from diverse sources including firewalls, intrusion prevention systems, servers and desktops as well as many others. It then applies through its patented engine technology, multiple levels of sophisticated correlation that identify potential and real security problems that a single point product with no correlation, such as a firewall, might miss. Once a threat has been identified an operator can prevent the occurrence and or remediate the security breach through the use of our Incident Response Manager.

Our Cinxi One appliance is a fully integrated as well as stand alone component of the SIM One platform that provides an efficient and scalable storage solution for the preservation of security event logs which are often required by regulatory agencies for compliance purposes and for creating a legal chain of custody in the case of a prosecution of a hacker.

2

We have designed our products to provide a comprehensive solution to meet the challenge of identifying and resolving security threats. The principal ways in which our solutions address these challenges include:

- •

- Carrier Class Technology and Architecture. We designed our

solutions to perform in the largest and most demanding IT environments in the world where "up time" and quality of service are paramount to meet increasingly stringent service level agreements.

- •

- Interoperability. Our ability to identify, collect and

normalize data from a broad range of disparate and heterogeneous third-party devices allows us to rapidly deploy our platform inside our MSSP and enterprise customers' IT infrastructures.

- •

- Scalability. We designed our SIM One platform and Cinxi

One appliance to consume thousands of security events per second and hundreds of millions of security events per day.

- •

- Real-Time Correlation and Actionable Security

Intelligence. Our multi-level correlation processes network security events through multiple levels of memory filtering to identify

security breaches and policy violations as the events occur, allowing organizations to take preventive action prior to a violation as opposed to corrective action after the violation has

occurred.

- •

- Multi-Tenant Architecture. In order to provide SECaaS offerings to their customers, our MSSP partners must be able to manage hundreds of multiple customers through a single instance of our platform. Our multi-tenant architecture provides this capability.

In late 2008, we strategically realigned to focus on the emerging MSSP and SECaaS markets. We redesigned our platform to provide additional and expanded capabilities to address the unique requirements associated with providing real-time security event correlation in and through the Cloud. Our 2009 acquisition of the High Tower Software gave us an appliance-based logging and SIEM application and added both customer premise and cloud-based logging to our platform.

3

Our Strategy

Our objective is to be the premier provider of cloud-based SECaaS through our MSSP and Managed Service Partners (MSP) partners worldwide. We characterize SECaaS offerings to include Logging, Monitoring, Management, Auditing and Proactive Prescription, and we intend to make SECaaS readily available to individual enterprises by providing our solution to power our partners' multi-tenant SECaaS platforms. We have segmented our partner market into three tiers to better address their distinct needs:

1. Tier 1 partners include broad based telecommunication companies, large MSSPs and other hosting companies.

2. Tier 2 partners include geographic and industry specific MSSPs.

3. Tier 3 partners include MSPs who primarily offer network management services to their customers today as opposed to security management services.

Key elements of our strategy include:

- •

- Growing Our MSSP Partner Base. We plan to increase our

presence globally by expanding our sales and marketing team with the objective of adding additional MSSP and MSP partners to our existing base.

- •

- Deepening Our Penetration With Our Existing Tier 1 and Tier 2

Partners. We intend to facilitate expanded deployments within our existing partners through the introduction of new products and

services. We expect the virtualization of our Cinxi One logging appliance to generate opportunities for additional sales through our partners.

- •

- Expanding Our Tier 1 and Tier 2 Partner

Base. We intend to aggressively add new MSSP specific partners to our distribution reach through the expanded use of our modular

deployment methodology including the release of a "turnkey" customer-facing portal and reporting package which will further reduce the time to market for our partners.

- •

- Extending Our Partner Network to the Tier 3 Partners Through A "White Label" SECaaS. For many potential MSSP and MSP partners the expense of deploying and operating our platform inside their own data centers is a barrier to using our platform. We intend to deploy our

4

- •

- Deepening Our Penetration With Our Existing Enterprise

Customers. We intend to facilitate expanded deployments within our existing enterprise customers by introducing new product offerings

including a SECaaS based offering of our SIM One product.

- •

- Expanding Our Portfolio Of Offerings And Capabilities. We will continue to add products and services that enhance our platform's capability to deliver the full range of SECaaS offerings required by our partners, their customers and our enterprise customers.

platform via the Cloud, utilizing our own labor and expertise, and provide it as a SECaaS offering to MSSP and MSP partners who can resell it under their own label and brand.

5

Risks Affecting Us

Our business is subject to numerous risks. These risks may affect our future sales and related profitability. These risks may affect our operating margins and the future success of our business. Some of these risks include:

- •

- We have shifted our business focus in the last three years away from direct sales to the enterprise customer in favor of

sales through MSSP and MSP partners. We have a limited operating history in this new market and face unknown challenges.

- •

- Our operating history has been turbulent. We are a small business with less than 100 employees and we have

struggled in response to market conditions and macro-economic events. We have incurred significant losses since our inception and have an accumulated deficit of approximately $58.9 million at

December 31, 2011. Our management team and employees may not be able to execute on our business plan which could continue our losses.

- •

- Without the funding from this offering or other events effecting our liquidity (including the conversion of promissory

notes to common stock, restructuring of debt instruments or other funding events), we may have difficulty continuing as a going concern.

- •

- Our quarterly operating results are likely to vary significantly and be unpredictable due to the length and

unpredictability of our sales cycle as well as the purchasing and budget practices of our partners within the context of the macro economy and IT market sector.

- •

- We will rely on channel partners (MSSPs) for a significant portion of our revenue and growth, and our ability to retain

and manage these partners will impact our ultimate success. If we are unsuccessful in developing deeper penetration into our existing MSSP partner base or fail to attract more MSSP customers, our

revenues could decline and our growth prospects could suffer.

- •

- The market in which we operate is highly competitive and many of our established competitors have significantly greater resources then we do. Our customers and partners may choose to develop and customize their own solutions rather then purchase our products and services, and new technology also may emerge which may diminish the utility of our products and negatively impact our sales and operating results.

Recent Developments

In January and February 2012, we borrowed an aggregate of $1.5 million principal amount under convertible notes, obtained a $700,000 line of credit from (together, the Sigma Convertible Notes and Line of Credit), and sold at $0.0001 per share 1,500,000 shares of our common stock to, entities affiliated with Sigma Capital Partners, in a bridge financing under the terms of a purchase and credit agreement. Pursuant to the agreement, if we consummate an offering of our equity securities, including this offering, by September 30, 2012, Sigma is permitted to elect to (i) convert the Sigma Convertible Notes and Line of Credit into shares of common stock at a 20% discount from the offering price, or (ii) be repaid in full. Sigma has indicated that it intends to elect to be repaid in full in connection with this offering, and such election is reflected in this prospectus. The Sigma Convertible Notes and Line of Credit bears interest at a rate of 18% per annum and any interest accrued shall be repayable in cash to Sigma.

We also entered into (i) an advisory services agreement pursuant to which we sold to Sigma 250,000 additional shares of our common stock at $0.0001 per share and (ii) an escrow agreement which requires us to issue to Sigma up to 700,000 additional shares of our common stock at $0.0001 per share in connection with borrowings from the Sigma Line of Credit. Sigma is permitted to put to us for $0.10 per share up to 2,450,000 (assuming the issuance of the 700,000 shares subject to the escrow agreement) of our shares of common stock owned by Sigma upon the earlier to occur of February 28, 2013 and a "deemed liquidation event," as such term is defined in the purchase and credit agreement, which includes this offering.

6

In connection with the Sigma transaction, we paid Liberty Partners Holdings 27, L.L.C. an aggregate of $314,174 in full satisfaction of all outstanding indebtedness under the senior subordinated note, which was in default, we issued to them in February 2009 in connection with our acquisition of certain intellectual property assets.

Our Corporate History and Information

BlackStratus, Inc. was originally incorporated as netForensics.com, Inc. on August 4, 1999 in the State of New Jersey. On January 7, 2002, netForensics, Inc., a wholly-owned subsidiary of netForensics.com, Inc., was incorporated in the State of Delaware. On April 30, 2002, netForensics.com, Inc. was merged into netForensics, Inc., in a tax-free reorganization and netForensics, Inc. became the surviving entity. In April 2003, netForensics, Inc. formed a wholly-owned subsidiary in the United Kingdom named netForensics Limited, which was dissolved in January 2011. On March 5, 2012, netForensics, Inc. changed its name to BlackStratus, Inc. Our corporate headquarters are located at 1551 South Washington Avenue, Piscataway, New Jersey 08854, and our telephone number is (732) 393-6000. Our website address is www.blackstratus.com. The information on, or that can be accessed through, our website is not part of this prospectus.

7

Common stock offering by BlackStratus |

shares |

|

Common stock to be outstanding after this offering |

shares |

|

Use of proceeds |

We expect to receive net proceeds from this offering of approximately $ million, based on an initial public offering price of $ , which is the midpoint of the range listed on the cover page of this prospectus, and after deducting underwriting discounts and commissions and estimated offering expenses that we must pay. We intend to use the net proceeds as follows: |

|

|

• up to $ for the repayment of the Sigma Convertible Notes and Line of Credit, to the extent not converted (See "—Recent Developments"); and |

|

|

• the remaining proceeds for general corporate purposes, including the potential funding of strategic acquisitions or investments, the continued expansion of our sales and marketing activities and the expanded funding of our research and development efforts. |

|

|

See the section entitled "Use of Proceeds." |

|

NASDAQ Capital Market symbol |

"BLKS" |

|

Risk Factors |

Investing in our common stock involves a high degree of risk. Please see the section entitled "Risk Factors" starting on page 14 of this prospectus to read about risks that you should consider carefully before buying shares of our common stock. |

The number of shares of our common stock to be outstanding after this offering is based on 6,484,351 shares of our common stock outstanding as of February 29, 2012, and excludes:

- •

- 8,846,675 shares of our common stock subject to options granted as of February 29, 2012 and having a weighted

average exercise price of $0.02 per share;

- •

- 23,437,500 shares of our common stock issuable upon the conversion of the Sigma Convertible Notes and Line of Credit

outstanding at February 29, 2012, at a twenty percent (20%) discount to the initial public offering price per share of our common stock (shares excluded based upon intended repayment of

indebtedness discussed above);

- •

- 2,461,781 shares of our common stock issuable upon the conversion of shares of our Series B-1 convertible preferred stock issuable upon the conversion of the Cline Short Term Note

8

- •

- 3,286,471 additional shares of our common stock reserved as of February 29, 2012 for future issuance under our stock-based compensation plans.

outstanding at February 29, 2012 (shares excluded based upon the holder's stated intent not to convert); and

Unless we specifically state otherwise, the share information in this prospectus is as of February 29, 2012 and reflects or assumes:

- •

- a 1-for- reverse stock split of our common stock effected

on , 2012;

- •

- the conversion of all Investor Convertible Promissory Notes and accrued interest outstanding at February 29, 2012

into 46,056,377 shares of our common stock immediately upon the closing of this offering;

- •

- the exercise of the SVB Warrant to purchase common stock outstanding at February 29, 2012, at a weighted average

exercise price per share of $23.46, into 426 shares of our common stock immediately upon the closing of this offering;

- •

- the conversion of all shares of our Series A-1 convertible preferred stock outstanding at

February 29, 2012 into 30,299,199 shares of our common stock immediately upon the closing of this offering;

- •

- the exercise of all Investor Warrants to purchase Series B-1 convertible preferred stock outstanding at

February 29, 2012, at a weighted average exercise price per share of $0.10, into 37,999,843 shares of our Series B-1 convertible preferred stock and the conversion of such

shares of our Series B-1 convertible preferred stock into 37,999,843 shares of our common stock immediately upon the closing of this offering;

- •

- the filing of our Fourth Amended and Restated Certificate of Incorporation and the adoption of our Amended and Restated

By-laws immediately prior to the effectiveness of this offering;

- •

- the filing of our Fifth Amended and Restated Certificate of Incorporation upon the closing of this offering;

and

- •

- the underwriters' over-allotment option to purchase up to an additional shares of our common stock is not exercised.

9

SUMMARY CONSOLIDATED FINANCIAL DATA

The following tables present our summary consolidated financial information for the periods indicated and should be read in conjunction with the information contained in "Selected Consolidated Financial Information," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and related notes appearing elsewhere in this prospectus. Historical operating information may not be indicative of our future performance. The consolidated financial statements are reported in United States dollar amounts and have been prepared in accordance with generally accepted accounting principles in the United States (GAAP). The consolidated financial statements for the years ending December 31, 2011 and 2010 have been audited by EisnerAmper LLP, an independent registered public accounting firm.

| |

Years Ended December 31, |

||||||

|---|---|---|---|---|---|---|---|

| |

2011 | 2010 | |||||

| |

(in thousands) |

||||||

Consolidated Statements of Operation Data: |

|||||||

Revenues |

|||||||

Software licenses |

$ | 1,638 | $ | 3,301 | |||

Post contract support and services |

6,361 | 7,427 | |||||

Recurring security services |

1,222 | 1,083 | |||||

Total revenues |

9,221 | 11,811 | |||||

Cost of revenues |

2,086 |

2,078 |

|||||

Gross profit |

7,135 | 9,733 | |||||

Operating expenses |

|||||||

Research and development |

2,090 | 2,919 | |||||

Sales and marketing |

3,257 | 5,824 | |||||

General and administrative |

2,634 | 2,866 | |||||

Total operating expenses |

7,981 | 11,609 | |||||

Loss from operations |

(846 | ) | (1,876 | ) | |||

Other income (expense) |

|||||||

Other income |

— | 1 | |||||

Realized currency translation |

(328 | ) | — | ||||

Interest expense |

(479 | ) | (378 | ) | |||

Total other income (expense), net |

(807 | ) | (377 | ) | |||

Loss before income tax benefit |

(1,653 | ) | (2,253 | ) | |||

Income tax benefit |

248 | — | |||||

Net loss |

(1,405 | ) | (2,253 | ) | |||

Undeclared dividends on Series A-1 convertible preferred stock |

(1,288 | ) | (1,288 | ) | |||

Net loss available for common stockholders |

$ | (2,693 | ) | $ | (3,541 | ) | |

10

| |

As of December 31, 2011 (unaudited) | ||||||

|---|---|---|---|---|---|---|---|

| |

(in thousands) |

||||||

| |

Actual | Pro Forma(1) | Pro Forma As Adjusted(2) |

||||

Consolidated Balance Sheet Data: |

|||||||

Cash and cash equivalents |

$ | 483 | |||||

Total assets |

2,423 | ||||||

SVB Line of Credit |

777 |

||||||

Sigma Convertible Notes and Line of Credit |

— | ||||||

Investor Convertible Promissory Notes, net |

3,656 | ||||||

Founder Contingent Notes |

2,750 | ||||||

Cline Short Term Note |

250 | ||||||

Accrued Interest |

1,306 | ||||||

Total liabilities |

14,426 | ||||||

SVB Warrant to purchase common stock |

— | ||||||

Series A-1 convertible preferred stock |

12,946 | ||||||

Investor Warrants to purchase Series B-1 convertible preferred stock |

— | ||||||

Series B-1 convertible preferred stock |

— | ||||||

Total stockholders' equity (deficit) |

$ | (12,003 | ) | ||||

- (1)

- The

pro forma balance sheet data reflects (a) the conversion of all outstanding shares of our Series A-1 convertible preferred

stock into shares of our common stock immediately upon the closing of this offering, (b) the exercise of all outstanding Investor Warrants into shares of our Series B-1

convertible preferred stock and the conversion of such stock into shares of our common stock immediately upon the closing of this offering, (c) the conversion of all outstanding Investor

Convertible Promissory Notes into shares of our common stock immediately upon the closing of this offering, and (d) the exercise of all outstanding SVB Warrants into shares of our common stock

immediately upon the closing of this offering.

- (2)

- The pro forma as adjusted balance sheet data reflects (a) our receipt of estimated net proceeds of $ million from our sale of shares of our common stock that we are offering at an assumed public offering price of $ per share, which is the midpoint of the range listed on the cover page of this prospectus, and after deducting estimated underwriting discounts and commissions, and estimated offering expenses payable by us, and (b) the application of the estimated net proceeds therefrom as described in "Use of Proceeds".

11

Any investment in our common stock involves a high degree of risk. You should consider carefully the specific risk factors described below in addition to the other information contained in this prospectus, including our consolidated financial statements and related notes included elsewhere in the prospectus, before making a decision to invest in our common stock. If any of these risks actually occurs, our business, financial condition, results of operations or prospects could be materially and adversely affected. This could cause the trading price of our common stock to decline and a loss of all or part of your investment.

Risks Related to Our Business

We may need to seek additional financing to operate our business in the next 12 months and therefore we may not be able to continue as a going concern. Our auditors have raised substantial doubt as to our ability to continue as a going concern in their audit report.

We have a history of net losses and negative cash flow from our operating activity and working capital deficiency. Subject to the results of this offering, we may need to seek additional financing to operate our business in the next twelve months. Thus, there is a substantial doubt about our ability to continue as a going concern. Our ability to continue as a going concern depends on our ability to generate positive cash flow from operations, raise further adequate funds (whether through this offering or otherwise), and pay or restructure our existing indebtedness. Based on our expected cash flow and available credit and assuming there will be no acceleration of payments due under our indebtedness, we currently have approximately eight months of capital resources available, and we estimate the additional financing required to operate our business in the next twelve months at approximately $0.5 million. Further, our line of credit with SVB contains certain covenants and restrictions and expires June 30, 2012 and there is no assurance that it will be renewed. Our auditors have noted this risk in their audit opinion included in this prospectus. If we do not raise sufficient funds in this offering or otherwise, we may not be able to continue as a going concern.

We are operating in an emerging market, we have a history of losses, and we are unable to forecast the extent of any future losses or when, if ever, we will achieve profitability in the future.

We launched our SIM One products in 2008 and acquired our Cinxi One products in 2009. Because the market for our products is rapidly evolving it is difficult for us to forecast our operating results and the ultimate size of the market for our products. We have a history of losses from operations, incurring losses from operations of $0.8 million and $1.9 million for the fiscal years ended December 31, 2011 and 2010, respectively. As of December 31, 2011, our accumulated deficit was $58.9 million. We expect our operating expenses to increase over the next several years as we hire additional sales and marketing personnel, expand our partner distribution channels and develop our technology and new products and advertise and promote our security solutions. In addition, as a public company, we will incur significant legal, accounting and other expenses that we did not incur as a private company. If our revenues do not increase to offset these expected increases in operating expenses, we will continue to incur significant losses and will not become profitable. If we are unable to become profitable, the market price of our common stock may fall. Even if we do achieve profitability, we may not be able to sustain or increase profitability on a consistent basis, which may result in a decline in the market price of our common stock price.

Even if we complete this offering, we may need additional financing in the future, which we may be unable to obtain.

As of December 31, 2011, we had cash and cash equivalents of approximately $0.5 million. In addition, as of December 31, 2011, we had total indebtedness, including accrued interest and capital leases, of approximately $9.1 million. After giving effect to the net proceeds from this offering and

12

repaying the indebtedness as described in the section entitled "Use of Proceeds," we will have cash and cash equivalents of approximately $ million. We believe such funds will enable us to fund our operations and growth strategy for three years following the consummation of the offering. We may need additional funds to finance our operations in the future, as well as to enhance our solutions and services, respond to competitive pressures or acquire complementary businesses or technologies. We may be unable to obtain financing on terms favorable to us, if at all. Poor financial results, unanticipated expenses or unanticipated opportunities that require financial commitments could give rise to additional financing requirements sooner than we currently expect. If we raise additional funds through the issuance of equity or convertible debt securities, this may reduce the percentage ownership of our existing stockholders, and these securities might have rights, preferences or privileges senior to those of our common stock. Debt financing may also require us to comply with restrictive covenants that could impair our business and financial flexibility or grant security interests in our assets. If adequate funds are not available or are not available on commercially acceptable terms, our ability to enhance our solutions and services, respond to competitive pressures or take advantage of business opportunities would be significantly limited, and we might need to significantly restrict our operations.

Our operating results may fluctuate from year to year and by quarter within each year, which makes our operating results difficult to predict and could cause our revenues, expenses and profitability to differ from expectations during certain periods, which would likely cause the market price of our common stock to decline.

Our operating results may fluctuate from year to year or by quarter within certain years as a result of a number of factors, many of which are outside of our control. Given these potential fluctuations and our focus on new markets, you should not rely on our past results as an indication of future performance. Each of the risks described in this section, as well as other factors, may affect our operating results. For example, factors that could affect our revenues and operating results include, but may not be limited to, the following:

- •

- our ability to develop, introduce and deploy new products and product enhancements that meet customer requirements in a

timely manner;

- •

- our ability to control our operating expenses;

- •

- changes in our pricing and distribution terms or those of our competitors;

- •

- the possibility that our customers may defer purchases of our software in anticipation of new software or updates from us

or our competitors;

- •

- the timing of new product releases or upgrades by us or our competitors;

- •

- the possibility that our customers may cancel, defer or limit purchases as a result of reduced information technology

budgets;

- •

- fluctuations in the demand for our products and post contract support, including professional services;

- •

- the timing and size of customer orders, including the concentration of orders at the end of each quarter, and the average

unit sale price per transaction;

- •

- changes in general economic conditions in our domestic and international markets;

- •

- the timing and costs associated with new product releases;

- •

- seasonality associated with demand for our products and services;

13

- •

- the timing of recognizing revenue as a result of revenue recognition rules, under generally accepted accounting principles

in the United States; and

- •

- our ability to access capital and the costs and restrictions thereof.

We believe that period-to-period comparisons of our results of operations are not a good indication of our future performance. In addition, the above factors could negatively impact our results of operations and cause us to fail to meet the financial performance expectations of securities industry research analysts or investors in future periods, which would likely cause the market price of our common stock to decline.

Our business model is evolving and we may be unable to monetize our MSSP and MSP penetration sufficiently to increase or maintain our profitability.

Our business model has evolved in recent years toward our current strategy to penetrate the managed service provider (MSP) market rather than drawing revenue primarily from managed security service provider (MSSP) partners licensing our premium products. To expand our customer base, we have added and plan to continue to add new products and online services to our product portfolio, broadening our focus beyond security software and appliance licenses and increasing our "Security as a Service" (SECaaS) and "White Label" offering. The evolution of our business model is ongoing and may depart further from the license-based model we used for much of our operating history.

We may be unsuccessful in executing our new business model of adding compelling new products and online services. Our primary means to date of monetizing our security solutions has been through license and contract support revenue based on devices under management. Our new products and online services, in addition to helping to expand our customer base, will generate revenue more directly via the sale of SECaaS and "White Label" offerings. If we cannot find additional methods of monetizing our active customer base with additional products and online services that customers find compelling, we will not be able to increase our revenue, margins or profitability.

We must maintain and expand our relationships with our existing MSSP partners and attract new MSP customers if we are to continue to expand and improve the quality of our customer base, which we may be unable to do.

To continue to expand our customer base, we must retain our existing MSSP partners and continuously attract new MSSP and MSP customers. Any failure in continuing to expand our customer base could have a material adverse effect on our business, operating results and financial condition.

In addition, our ability to monetize our active customer base is dependent on many diverse characteristics of those customers, including level of engagement with our products, amount and nature of Internet and computing activities, geographic location and income level. If we are unable to retain existing and recruit new customers whose characteristics contribute to a customer base with optimum potential for monetization, our business, operating results and financial condition could suffer materially.

Our sales cycle is long and unpredictable, and our sales efforts require considerable time and expense. As a result, our revenues are difficult to predict and may vary substantially from quarter to quarter, which may cause our operating results to fluctuate.

Our operating results may fluctuate, in part, because of the intensive nature of our sales efforts, required customer engagement at multiple levels and departments, the length and variability of the sales cycle of our SIM One product and the short-term difficulty in adjusting our operating expenses. Because decisions to purchase products such as our SIM One product involve significant capital commitments by customers, potential customers generally have our software evaluated at multiple levels

14

within an organization, each often having specific and conflicting requirements. Enterprise customers make product purchasing decisions based in part on factors not directly related to the features of the products, including but not limited to the customers' projections of business growth, capital budgets and anticipated cost savings from implementation of the software. As a result of these factors, licensing our software products often requires an extensive sales effort throughout a customer's organization. Our sales efforts often involve educating our customers, who are often relatively unfamiliar with our products and their value, including their technical capabilities and potential cost savings to the organization. We spend substantial time, effort and money in our sales efforts without any assurance that our efforts will produce any sales.

The length of our sales cycle, from initial evaluation to delivery of software, tends to be long and varies substantially from customer to customer. Our sales cycle is typically six to twelve months but can extend to more than a year for some sales. We typically recognize a substantial majority of our product revenues in the last few weeks of a quarter. It is difficult to predict exactly when, or even if, we will actually make a sale with a potential customer. As a result, large individual sales have, in some cases, occurred in quarters subsequent to those we anticipated, or have not occurred at all. The loss or delay of one or more large product transactions in a quarter could impact our operating results for that quarter and any future quarters into which revenues from that transaction are delayed. As a result of these factors, it is difficult for us to accurately forecast product revenues in any quarter. Because a substantial portion of our expenses are relatively fixed in the short term, our operating results will suffer if revenues fall below our expectations in a particular quarter, which could cause the market price of our common stock to decline significantly.

We have limited experience with sale, delivery, service and support of our proposed "White Label" SECaaS offerings to MSPs.

We are developing our "White Label" SECaaS offering in conjunction with targeted MSPs and intend to introduce the service in 2013. This SECaaS offering will bring to market an entirely new user experience across the BlackStratus product portfolio with an API base access method for MSP's scalability. Although we will partner with experienced and financially successful MSPs, we cannot forecast with a high degree of certainty the additional staffing that will be required given the service level agreements (SLAs) that we expect to enter into. To successfully implement this service, we will need to hire additional software developers, as well as automation and quality assurance engineers. To successfully operate this service, we will require highly technical analysts to monitor the operations and work with the MSPs when security issues are detected. If we do not correctly forecast the services requirements we could be in breach of SLAs, which could impact our ability to partner with other MSPs, as well as negatively impact our reputation and the perceived value of our other products. Further, if we do not correctly price the service, or hire redundant staff, our revenues and profitability could be negatively impacted which could cause the market price of our common stock to decline significantly.

Because we derive a substantial majority of our revenues from SIM One and related products and services, any failure of this product to satisfy customer demands or to achieve increased market acceptance will harm our business, operating results, financial condition and growth prospects.

We have derived a substantial majority of our revenues from SIM One and related services. We expect this to continue for the foreseeable future. For example, in fiscal 2011, license, maintenance and service revenue attributable to SIM One represented 79.3% of revenues, with the balance coming from transactions involving our Cinxi One appliance products. As a result, although we introduced our complementary Cinxi One appliance products in fiscal 2009 to more fully serve the enterprise security and compliance management market, our revenues and operating results will continue to depend substantially on the demand for our SIM One product. Demand for SIM One is affected by a number

15

of factors beyond our control, including the timing of development and release of new products by us and our competitors, technological change, and lower-than-expected growth or a contraction in the worldwide market for enterprise security and compliance management solutions or other risks described in this prospectus. If we are unable to continue to meet customer demands or to achieve more widespread market acceptance of SIM One, our business, operating results, financial condition and growth prospects will be adversely affected.

If we are unable to successfully market to MSSPs and MSPs, successfully develop new products, make enhancements to our existing products or expand our offerings into new markets, our business may not grow and our operating results may suffer.

We introduced our Cinxi One products in fiscal 2009 and are currently developing new versions of these products and our SIM One platform, as well as new complementary products. Our growth strategy and future financial performance will depend, in part, on our ability to market and sell these products and to diversify our offerings by successfully developing, timely introducing and gaining customer acceptance of new products.

The software in our products is especially complex because it must recognize, effectively interact with and manage a wide variety of devices and applications, and effectively identify and evaluate to new and increasingly sophisticated security threats and other risks, while not impeding the high network performance demanded by our partners and their end customers. The typical development cycle for a patch to our SIM One software is one to three months and a new version or major sub-version is nine to twelve months. Partners, customers and industry analysts expect speedy introduction of software to respond to new threats and risks and to add new functionality, and we may be unable to meet these expectations. Since developing new products or new versions of, or add-ons to, existing products is complex, the timetable for their commercial release is difficult to predict and may vary from our historical experience, which could result in delays in their introduction from anticipated or announced release dates. We may not offer updates as rapidly as new threats affect our customers and their end customers. If we do not quickly respond to the rapidly changing and rigorous needs of our customers and their end customers by developing and introducing on a timely basis new and effective products, upgrades and services that can respond adequately to new security threats, our competitive position, business and growth prospects will be harmed.

Diversifying our product offerings and expanding into new markets will require significant investment and planning, will bring us more directly into competition with software providers that may be better established or have greater resources than we do, may complicate our relationships with existing MSSP partners and will entail significant risk of failure. Sales of our Cinxi One product and other products that we may develop and market may reduce revenues of our flagship SIM One product and our overall margin by offering a subset of features or capabilities at a reduced price with a lower gross margin. Moreover, increased emphasis on the sale of our appliance products, add-on products or new product lines could distract us from sales of our core SIM One offering, negatively affecting our overall sales. If we fail or delay in diversifying our existing offerings or expanding into new markets, or we are unsuccessful competing in these new markets, our business, operating results and prospects may suffer.

If we are not able to promote, maintain and enhance our brand, our business and operating results may be harmed.

We believe that maintaining and enhancing our brand identity is critical to our relationships with, and to our ability to attract, new customers and partners. The successful promotion of our brand will depend largely upon our marketing and public relations efforts, our ability to continue to offer high-quality products and services, and our ability to successfully differentiate our products and services from those of our competitors, especially to the extent that our competitors integrate or bundle competitive offerings with a

16

broader array of products and services that they may offer. Our brand promotion activities may not be successful or yield increased revenues. In addition, extension of our brand to products and uses different from our traditional products and services may dilute our brand, particularly if we fail to maintain the quality of our products and services in these new areas. The promotion of our brand will require us to make substantial expenditures, and we anticipate that the expenditures will increase as our market becomes more competitive and as we expand into new markets. To the extent that these activities yield increased revenues, these revenues may not offset the expenses we incur. If we do not successfully maintain and enhance our brand, our business may not grow, we may have reduced pricing power relative to competitors with stronger brands, and we could lose customers and partners, all of which would harm our business, operating results and financial condition.

In addition, independent industry analysts often provide reviews of our products and services, as well as those of our competitors, and perception of our products in the marketplace may be significantly influenced by these reviews. We have no control over what these industry analysts report, and because industry analysts may influence current and potential customers, our brand could be harmed if they do not provide a positive review of our products and services or view us as a market leader.

We face intense competition in our market, especially from larger, better-known companies, and we may lack sufficient financial or other resources to maintain or improve our competitive position.

The market for enterprise security and compliance management, log archiving and response products is intensely competitive, and we expect competition to increase in the future. A significant number of companies have developed, or are developing, products that currently, or in the future are likely to, compete with some or all of our products. We may not compete successfully against our current or potential competitors, especially those with significantly greater financial resources or brand name recognition. Companies competing with us may introduce products that are more competitively priced, have greater performance or functionality or incorporate technological advances that we have not yet developed or implemented.

Our competitors include large software companies, software or hardware network infrastructure companies, smaller software companies offering more narrowly focused enterprise security and compliance management, log archiving and response products and small and large companies offering point solutions that compete with components of our platform or individual products offered by us. Existing competitors for a security and compliance management software platform solution such as our SIM One platform primarily are larger companies such as EMC, IBM, Novell, HP, Tipco and TrustWave, through their acquisitions of Network Intelligence, and Micromuse and Consul, e-Security, ArcSight, LogLogic and Intellitactics, respectively. Current competitors for sales of our Cinxi One product include specialized, privately-held companies, such as Splunk and Sensage. In addition to these current competitors, we expect to face competition for our appliance products from existing large, diversified software and hardware companies, from specialized, smaller companies and from new companies that may seek to enter this market.

A greater source of competition is represented by the custom efforts undertaken by potential customers to analyze and manage the information produced from their existing customers' devices and applications to identify and remediate threats. Many companies, in particular large corporate enterprises, have developed internally software that is an alternative to our enterprise security and compliance management, log archiving and response products. Wide adoption of our security information and event management (SIEM) software and hardware solutions, which we are promoting as a standard for intelligently filtering and remediating event logs generated by security and other products, may facilitate this internal development. It may also allow our competitors to offer products with a degree of compatibility similar to ours or may facilitate new entrants into our business. New competitors may emerge and rapidly acquire significant market share due to factors such as greater brand name recognition, larger installed customer bases and significantly greater financial, technical, marketing and other resources and experience. If these new competitors are successful, we would lose market share and our revenues would likely decline.

17

Mergers or consolidations among these competitors, or acquisitions of our competitors by large companies, present heightened competitive challenges to our business. For example, in recent years IBM has acquired Internet Security Systems, Inc., Micromuse and Consul, Novell acquired e-Security, EMC acquired Network Intelligence, Hewlett-Packard acquired Opsware and ArcSight, Tipco acquired LogLogic and TrustWave acquired Intellitactics. We believe that the trend toward consolidation in our industry will continue. These acquisitions will make these combined entities potentially more formidable competitors to us if their products and offerings are effectively integrated. Continued industry consolidation may impact customers' perceptions of the viability of smaller or even medium-sized software firms and consequently customers' willingness to purchase from those firms.

Many of our existing and potential competitors enjoy substantial competitive advantages, such as:

- •

- greater name recognition and longer operating histories;

- •

- larger sales and marketing budgets and resources;

- •

- the capacity to leverage their sales efforts and marketing expenditures across a broader portfolio of products;

- •

- broader distribution and established relationships with distribution partners;

- •

- access to larger customer bases;

- •

- greater customer support;

- •

- greater resources to make acquisitions;

- •

- lower labor and development costs; and

- •

- substantially greater financial, technical and other resources.

As a result, they may be able to adapt more quickly and effectively to new or emerging technologies and changing opportunities, standards or customer requirements. In addition, these companies have reduced, and could continue to reduce, the price of their enterprise security and compliance management, log archiving and response products and managed security services, which intensifies pricing pressures within our market.

Increased competition could result in fewer customer orders, price reductions, reduced operating margins and loss of market share. Our larger competitors also may be able to provide customers with different or greater capabilities or benefits than we can provide in areas such as technical qualifications, geographic presence, the ability to provide a broader range of services and products, and price. In addition, large competitors may have more extensive relationships within large enterprises, the federal government or foreign governments, which may provide them with an advantage in competing for business with those potential customers. Our ability to compete will depend upon our ability to provide better performance than our competitors at a competitive price. We may be required to make substantial additional investments in research, development, marketing and sales in order to respond to competition, and we cannot assure you that we will be able to compete successfully in the future.

We may not be able to compete effectively with companies that integrate or bundle products similar to ours with their other product offerings.

Many large, integrated software companies offer suites of products that include software applications for security and compliance management. In addition, hardware vendors, including diversified, global entities, offer products that address the security and compliance needs of the enterprises and government agencies that comprise our target market. Further, several companies currently sell software products that our customers and potential customers have broadly adopted, which may provide them a substantial advantage when they sell products that perform functions

18

substantially similar to some of our products. Competitors that offer a large array of security or software products may be able to offer products or functionality similar to ours at a more attractive price than we can by integrating or bundling them with their other product offerings. The trend toward consolidation in our industry increases the likelihood of competition based on integration or bundling. Customers may also increasingly seek to consolidate their enterprise-level software purchases with a small number of larger companies that can purport to satisfy a broad range of their requirements. If we are unable to sufficiently differentiate our products from the integrated or bundled products of our competitors, such as by offering enhanced functionality, performance or value, we may see a decrease in demand for those products, which would adversely affect our business, operating results and financial condition. Similarly, if customers seek to concentrate their software purchases in the product portfolios of a few large providers, we may be at a competitive disadvantage.

If we are unable to develop and introduce new products or enhancements to existing products and respond to technological changes, if our new products or enhancements do not achieve market acceptance or if we fail to manage product transitions, our results of operations and competitive position will suffer.

Our ability to compete in this highly competitive market depends in large part upon our ability to continuously anticipate and identify changing customer needs and to introduce and market new products, technologies, features and functionalities that meet those needs in a timely manner. As a result, we spend substantial amounts of time and money to research, develop and market new products and enhanced versions of our products to incorporate additional features, improve functionality or provide other enhancements. We have had to curtail certain projects due to our liquidity concerns and cost reduction pressures.

When we develop a new product or an advanced version of an existing product, we typically expend significant money and effort upfront to market, promote and sell the new offering. Therefore, if our new products or enhancements do not achieve adequate acceptance in the market, our competitive position will be impaired, our revenue will be diminished and the effect on our operating results may be particularly acute because of the significant research, development, marketing, sales and other expenses we incurred in connection with the new product or enhancement.

In addition, the introduction of new products or enhancements by us in future periods may also reduce demand for our existing products. As new or enhanced products are introduced, we must successfully manage the transition from older products in order to minimize disruption in customers' ordering patterns and avoid having to support excessive levels of older installed product.

We may not receive significant revenues from our current research and development efforts for several years, if at all.

Developing software is expensive, and the investment in product development may involve a long payback cycle. Our research and development expenses were $2.1 million, or 23% of total revenues, in fiscal 2011, and $2.9 million, or 25% of total revenues, in fiscal 2010. Our future plans include significant investments in software research and development and related product opportunities. We believe that we must continue to dedicate a significant amount of resources to our research and development efforts to maintain our competitive position. However, we do not expect to receive significant revenues from these investments for several years, if at all.

We face risks related to existing relationships with MSSPs.

We currently sell to large system integrators or MSSPs. To date we have developed a number of successful relationships with MSSPs, however they may develop or acquire their own technologies rather than purchasing our products for use in provision of managed security services.

19

We face risks related to our reliance on key customers.

Many of our customers are large telephone companies and Tier 1 MSSPs that typically involve multi-year programs that represent significant license fees and professional services when implemented, but which may not provide significant revenues subsequent to the implementation. This reliance on major customers and their continued development of large projects could result in uneven or declining revenues if they do not continue to expand their services and customer base or we do not participate in subsequent projects.

We face risks related to our dependence on software technology licensed from a key vendor.

The performance of our products is dependant on software products licensed from a third party. Because of our reliance on this software, we are subject to a number of risks. In addition to pricing risks, we may face development and capability risks as we enhance our products' capabilities, since we may be dependent on the development schedule and priorities of our supplier which could negatively impact our ability to introduce functionality desired by our partners and end-user customers. As part of our research and development activities we attempt to identify alternate technology vendors to provide customers and partners the best possible solutions and reduce reliance on any one vendor. However, there can be no assurance that we will be able to diversify our suppliers and reduce our dependence on any one supplier.

Our business depends, in part, on sales to the public sector, and significant changes in the contracting or fiscal policies of the public sector could have a material adverse effect on our business.

We derive a portion of our revenues from contracts with federal, state, local and foreign governments and government agencies, and we believe that the success and growth of our business will continue to depend on our successful procurement of government contracts. For example, we have historically derived, and expect to continue to derive, a significant portion of our revenues from sales to agencies of the U.S. federal government, either directly by us or through MSSPs and other channel partners. In fiscal 2011 and 2010, we derived 16% and 15% of our revenues, respectively, from contracts with agencies of the U.S. federal government. Accordingly:

- •

- changes in fiscal or contracting policies or decreases in available government funding;

- •

- changes in government programs or applicable requirements;

- •

- the adoption of new laws or regulations or changes to existing laws or regulations;

- •

- changes in political or social attitudes with respect to security issues;

- •

- potential delays or changes in the government appropriations process; and

- •

- delays in the payment of our invoices by government payment offices

could cause governments and governmental agencies to delay or refrain from purchasing the products and services that we offer in the future or could otherwise have an adverse effect on our business, financial condition and results of operations.

Failure to comply with laws or regulations applicable to our business could cause us to lose U.S. government customers or our ability to contract with the U.S. government.

We must comply with laws and regulations relating to the formation, administration and performance of U.S. government contracts, which affect how we and our partners do business in connection with U.S. federal agencies. These laws and regulations may impose added costs on our business, and failure to comply with these or other applicable regulations and requirements, including non-compliance in the past, could lead to claims for damages from our channel partners, penalties, termination of contracts and suspension or debarment from government contracting for a period of time. Any such damages, penalties, disruption or limitation in our ability to do business with the U.S.

20

federal government could have a material adverse effect on our business, operating results and financial condition.

Our government contracts may limit our ability to move development activities overseas, which may impair our ability to optimize our software development costs and compete for non-government contracts.

Increasingly, software development is being shifted to lower-cost countries, such as India. However, some contracts with U.S. government agencies require that at least 50% of the components of each of our products be of U.S. origin. Consequently, our ability to optimize our software development by conducting it overseas may be hampered. Some of our competitors do not rely on contracts with the U.S. government to the same degree as we do and may develop software off-shore. If we are unable to develop software as cost-effectively as our competitors, our ability to compete for our non-government customers may be reduced and our customer sales may decline, resulting in decreased revenues.

Real or perceived errors, failures or bugs in our products could adversely affect our operating results and growth prospects.

Because we offer very complex products, undetected errors, failures or bugs may occur, especially when products are first introduced or when new versions are released. Our products are often installed and used in large-scale computing environments with different operating systems, system management software and equipment and networking configurations, which may cause errors or failures in our products or may expose undetected errors, failures or bugs in our products. Despite testing by us, errors, failures or bugs may not be found in new products or releases until after commencement of commercial shipments. In the past, we have discovered software errors, failures, and bugs in some of our product offerings after their introduction.

In addition, our products could be perceived to be ineffective for a variety of reasons outside of our control. Hackers could circumvent our customers' and their end customers' security measures, and customers may misuse our products resulting in a security breach or perceived product failure. We provide a top-level enterprise security and compliance management solution that integrates a wide variety of other elements in a customer's IT and security infrastructure offerings, and we may receive blame for a security breach that was the result of the failure of one of the other elements.

Real or perceived errors, failures or bugs in our products could result in negative publicity, loss of or delay in market acceptance of our products, loss of competitive position, or claims by customers for losses sustained by them or their end customers. In such an event, we may be required, or may choose, for customer relations or other reasons, to expend additional resources in order to help correct the problem. Our product liability insurance may not be adequate. Further, provisions in our license agreements with end users that limit our exposure to liabilities arising from such claims may not be enforceable in some circumstances or may not fully protect us against such claims and related liabilities and costs. Defending a lawsuit, regardless of its merit, could be costly and could limit the amount of time that management has available for day-to-day execution and strategic planning or other matters.

Many of our enterprise customers use our products in applications that are critical to their businesses and may have a greater sensitivity to defects in our products than to defects in other, less critical, software products. In addition, if an actual or perceived breach of information integrity or availability occurs in one of our enterprise customer's systems, regardless of whether the breach is attributable to our products, the market perception of the effectiveness of our products could be harmed. Alleviating any of these problems could require significant expenditures of our capital and other resources and could cause interruptions, delays or cessation of our product licensing, which could cause us to lose existing or potential customers and could adversely affect our operating results and growth prospects.

In addition, because we are a leading provider of enterprise security products and services, "hackers" and others may try to access our data or compromise our systems. If we are the subject of a

21

successful attack, then our reputation in the industry and with current and potential customers may be compromised and our sales and operating results could be adversely affected.

Incorrect or improper use of our complex products, our failure to properly train customers on how to utilize our products or our failure to properly provide consulting and implementation services could result in customer dissatisfaction and negatively affect our results of operations and growth prospects.

Our SIM One and Cinxi One products are complex and are deployed in a wide variety of network environments. The proper use of our products, particularly our SIM One platform, requires training of the end user. If our software products are not used correctly or as intended, inadequate performance may result. Our customers or our professional services personnel may incorrectly implement or use our products. Our products may also be intentionally misused or abused by customers, their employees, their end customers or third parties who obtain access and use of our products. Because our customers rely on our product, services and maintenance offerings to manage a wide range of sensitive security, network and compliance functions for their end customers, the incorrect or improper use of our products, our failure to properly train customers on how to efficiently and effectively use our products or our failure to properly provide consulting and implementation services and maintenance to our customers may result in negative publicity or legal claims against us.

Our international sales and operations subject us to additional risks that can adversely affect our operating results.

In fiscal 2011 and 2010, we derived 48% and 58% of our revenues, respectively, from customers outside the United States, and we are continuing to expand our international operations as part of our growth strategy. We do not currently have sufficient resources supporting our international operations. Our international operations subject us to a variety of risks, including:

- •

- increased management, travel, infrastructure and legal compliance costs associated with having multiple international

operations;

- •

- procurement of resources to represent us in selected international markets;

- •

- longer payment cycles and difficulties in collecting accounts receivable, especially in emerging markets, and the

likelihood that revenues from international resellers and customers may need to be recognized when cash is received, at least until satisfactory payment history has been established;

- •

- the need to localize our products and licensing programs for international customers;

- •

- differing regulatory and legal requirements and possible enactment of additional regulations or restrictions on the use,