Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT ON FORM 8-K - WELLS FARGO & COMPANY/MN | d333074d8k.htm |

| EX-99.1 - THE PRESS RELEASE, DEEMED "FILED" UNDER THE SECURITIES EXCHANGE ACT OF 1934 - WELLS FARGO & COMPANY/MN | d333074dex991.htm |

1Q12 Quarterly Supplement

April 13, 2012

Exhibit 99.2 |

Wells Fargo

1Q12 Supplement 1

Appendix

Pages 22-40

-

Recent acquisitions and divestitures

23

-

Non-strategic/liquidating loan portfolio risk reduction

24

-

Purchased credit-impaired (PCI) portfolios

25

-

PCI nonaccretable difference

26

-

PCI accretable yield

27

-

PCI accretable yield (Commercial & Pick-a-Pay)

28

-

1Q12 Credit quality highlights

29

-

Commercial real estate (CRE) loan portfolio

30

-

Pick-a-Pay mortgage portfolio

31

-

Pick-a-Pay credit highlights

32

-

Real estate 1-4 family first mortgage portfolio

33

-

Home equity portfolio

34-35

-

Credit card portfolio

36

-

Auto portfolio

37

Forward-looking statements and

additional information

38

Tier 1 common equity under Basel I

39

Tier 1 common equity under Basel III

(Estimated)

40

Table of contents

1Q12 Results

-

1Q12 Results

Page 2

-

Continued strong diversification

3

-

Balance Sheet overview

4

-

Income Statement overview

5

-

Loans

6

-

Deposits

7

-

Net interest income

8

-

Noninterest income

9

-

Noninterest expense

10-11

-

Noninterest expense target

12

-

Community Banking

13

-

Wholesale Banking

14

-

Wealth, Brokerage and Retirement

15

-

Credit quality

16-17

-

Mortgage servicing

18-19

-

Capital

20

-

Summary

21 |

Wells Fargo

1Q12 Supplement 2

Record earnings of $4.2 billion, up 3% linked

quarter (LQ) and 13% year-over-year (YoY)

Record diluted earnings per share of $0.75, up

3% LQ and 12% YoY

Total revenue of $21.6 billion, up $1.0 billion LQ

on strong noninterest income

Pre-tax pre-provision profit

(1)

of $8.6 billion, up

$546 million LQ

Positive operating leverage

Improved credit quality including a 9% LQ

decline in net charge-offs

ROA = 1.31%, up 6 bps LQ and up 8 bps YoY

ROE = 12.14%, up 17 bps LQ and up 16 bps YoY

Capital levels continued to grow

-

9.95% Tier 1 common equity ratio under Basel I

and estimated Tier 1 common equity ratio under

Basel III of 7.81%

(2)

Quarterly common stock dividend rate increased

to $0.22 per share

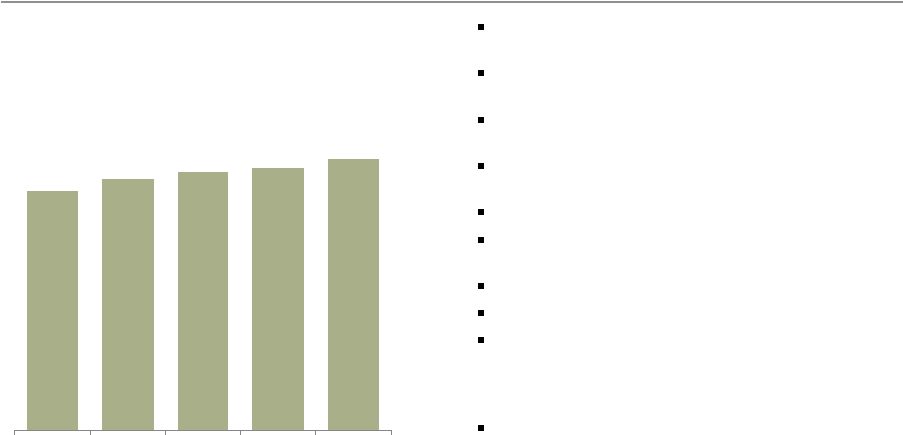

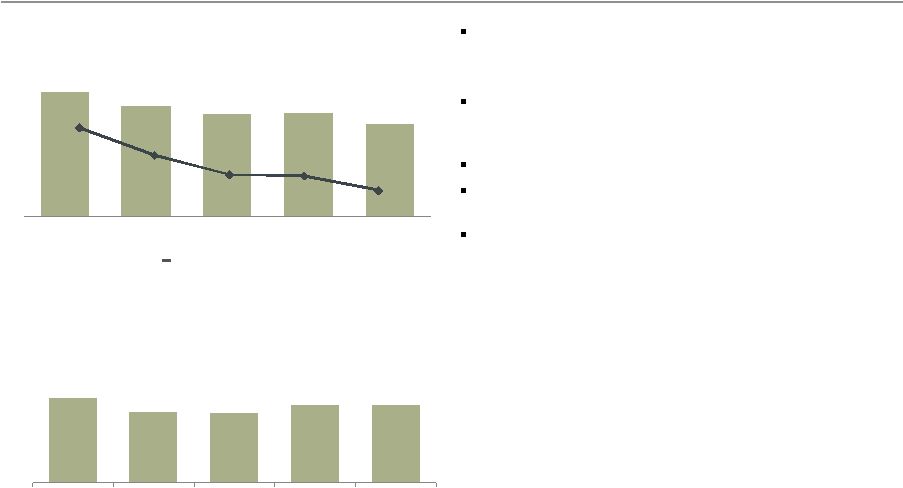

1Q12 Results

Wells Fargo Net Income

($ in millions)

3,759

3,948

4,055

4,107

4,248

1Q11

2Q11

3Q11

4Q11

1Q12

(1) Pre-tax pre-provision profit (PTPP) is total revenue less noninterest

expense. Management believes PTPP is a useful financial measure because it enables

investors and others to assess the Company’s ability to generate capital to cover credit losses through a credit cycle.

interpretation of current Basel III capital proposals.This pro forma calculation is subject to

change depending on final promulgation of Basel III capital rulemaking and

interpretations by regulatory authorities. See pages 39-40 for additional information regarding Tier 1 common equity ratios.

(2) 1Q12 capital ratios are preliminary estimates. Pro

forma Basel III calculation based on Tier 1 common equity, as adjusted to reflect management’s |

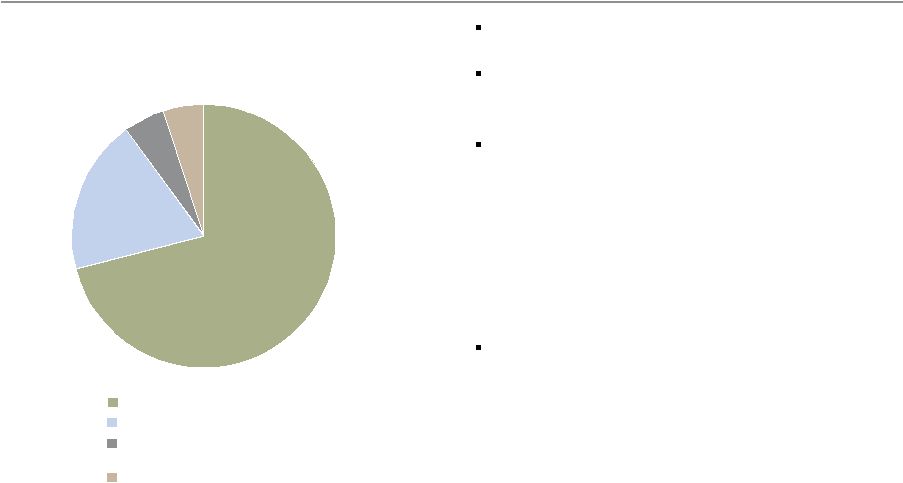

Wells Fargo

1Q12 Supplement 3

50%

50%

Balanced Spread and

Fee Income

Diversified Fee

Generation

10%

10%

17%

6%

10%

2%

24%

5%

6%

10%

Deposit Service Charges

10%

Card Fees

6%

Other Banking Fees

10%

Mortgage Servicing, net

2%

Insurance

5%

Net Gains from Trading

(1)

6%

Noninterest Income

50%

Net Interest Income

50%

All data is for 1Q12.

(1) Net gains from trading activities.

(2) Other noninterest income includes net losses on debt securities available for sale,

net gains from equity investments, operating leases and all other noninterest

income. Diversified Loan

Portfolio

Commercial Loans

40%

Consumer Loans

55%

Continued strong diversification

Foreign Loans

5%

Mortgage Orig./Sales, net

24%

Trust, Investment & IRA fees

10%

Commissions & All Other

Investment Fees

17%

55%

40%

5%

Other Noninterest Income

(2)

10% |

Wells Fargo

1Q12 Supplement 4

Balance Sheet overview

Loans

Total period-end loans down $3.1 billion; core loans grew $1.0 billion;

non-strategic/liquidating

portfolio

decreased

$4.1

billion

(1)

Acquired

$858

million

of

asset-based

commercial

loans

on

February

1

Securities available for

sale (AFS)

Balances up $7.7 billion as we continued to deploy cash, and new

investments were partially offset by runoff

Trading assets

Balances remained elevated as $12.1

billion of conforming agency

production was held over quarter-end in security form to facilitate best

execution

VaR

(2)

stable with an average daily VaR of $32 million in the quarter

Deposits

Balances up $10.2 billion on strong consumer deposit growth

Long-term debt

Balances up $4.4 billion as $8.0 billion in issuances were partially offset by

$4.2 billion in maturities

Common stock

repurchases

Purchased 7.6 million common shares in the quarter

st

Period-end balances, unless otherwise noted. All result comparisons are 1Q12

compared to 4Q11. (1) See pages 6 and 24 for additional information regarding core loans and the

non-strategic/liquidating portfolio, which comprises the Pick-a-Pay, liquidating home

equity, legacy WFF indirect auto, legacy WFF debt consolidation, Education

Finance-government guaranteed, and legacy Wachovia Commercial, Commercial Real

Estate, foreign and other PCI loan portfolios.

(2) Average one-day 99% Value-at-Risk (VaR).

|

Wells Fargo

1Q12 Supplement 5

Income Statement overview

Net interest income

Stable as growth in securities and the mortgage warehouse, as well as

disciplined deposit pricing, was offset by 1 less day in the quarter and

continued balance sheet repricing

Net interest margin (NIM) up 2 bps to 3.91%

Noninterest income

Mortgage banking up $506 million on higher origination volumes and

strong margins

Market sensitive revenues

(1)

up $458 million on strong equity

investment and trading gains

-

Equity investment gains up $303 million on stronger business results

and lower OTTI

(2)

-

Trading up $210 million on higher deferred compensation plan

investments (P&L neutral) and stronger customer-driven trading

Trust & investment fees up $181 million on higher retail brokerage

transaction activity and asset-based fees

Other income down $128 million from 4Q11, which included a gain on

the sale of H.D. Vest

Noninterest expense

Employee benefits expense up $596 million reflecting seasonally higher

payroll taxes, 401(k) matching on annual incentive compensation and

higher deferred compensation expense

Commission and incentive compensation increased $166 million on

annual equity awards to retirement-eligible employees as well as

higher revenue-based compensation in mortgage, retail brokerage and

insurance

Operating

losses

up

$314

million

primarily

reflecting

litigation

accruals

on various legal matters

Partially offset by previously implemented expense savings initiatives

All result comparisons are 1Q12 compared with 4Q11.

(1) Includes net gains from trading activities, net losses on debt securities available

for sale and net gains from equity investments. (2) Other-than-temporary

impairment. |

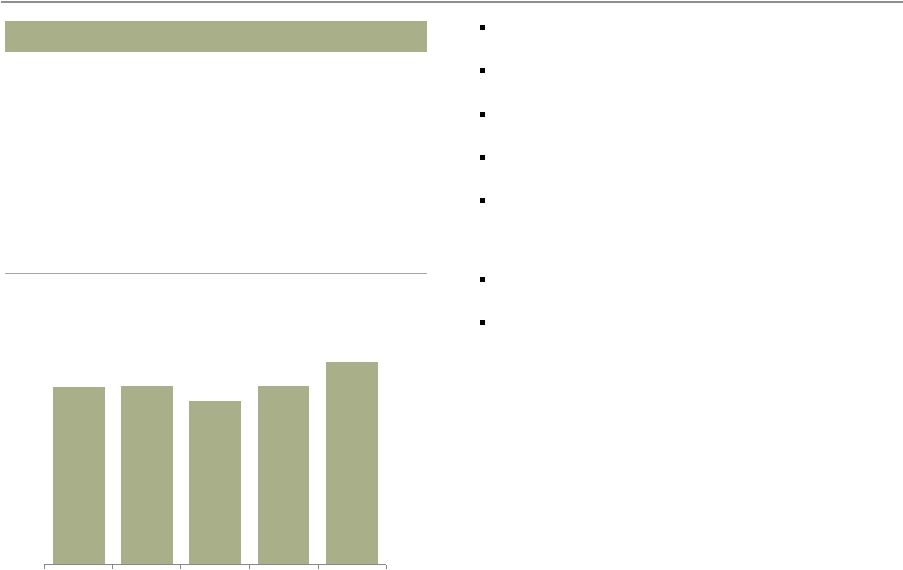

Wells Fargo

1Q12 Supplement 6

624.4

630.1

643.6

657.3

658.3

126.8

121.8

116.5

112.3

108.2

751.2

751.9

760.1

769.6

766.5

1Q11

2Q11

3Q11

4Q11

1Q12

Core loans

Non-strategic/liquidating loans

Loans

Decline reflects continued reduction in non-strategic/liquidating

portfolio Period-end loans down $3.1 billion from 4Q11

-

Commercial loans up $299 million as growth in

C&I was partially offset by lower CRE and

foreign

•

Included $858 million of asset-based loans

acquired from Burdale Capital Finance in February

($445 million in U.S. and $413 million in U.K.)

-

Consumer loans down $3.4 billion as growth in

auto and private student lending was more than

offset by a decline in junior lien mortgage and

seasonally lower credit card

Non-strategic/liquidating loans

(1)

down $4.1

billion from 4Q11

Core loans grew $1.0 billion from 4Q11

Total average loan yield of 4.81% stable LQ;

down 22 bps YoY due to runoff of higher-yielding

loans including the non-strategic/liquidating

portfolio

-

Weighted average yield of the non-strategic

portfolio was 5.40% in 1Q12

Period-end balances.

(1) See page 24 for additional information regarding the non-strategic/liquidating

portfolio, which comprises the Pick-a-Pay, liquidating home equity, legacy WFF

indirect auto, legacy WFF debt consolidation, Education Finance-government guaranteed, and

legacy Wachovia Commercial, Commercial Real Estate, foreign and other PCI loan

portfolios. Period–end Loans Outstanding

($ in billions)

(1)

Total average loan yield

5.03%

5.00%

4.87%

4.81%

4.81% |

Wells Fargo

1Q12 Supplement 7

647.8

665.4

668.4

193.1

246.7

246.6

840.9

912.1

915.0

1Q11

4Q11

1Q12

Interest-bearing deposits

Noninterest-bearing deposits

722.5

800.1

807.8

1Q11

4Q11

1Q12

0.30%

0.22%

0.20%

Deposits

Strong growth and reduced average cost

Average deposits up $2.9 billion LQ to $915.0

billion on growth in consumer deposits

Average core deposits of $870.5 billion up $5.6

billion from 4Q11 and up $73.7 billion, or

9% YoY

-

113% of average loans

-

Average retail core deposits up 6%

annualized LQ

Average core checking and savings up $7.7 billion,

or 1% from 4Q11, and up $85.3 billion, or

12%, YoY

-

93% of average core deposits

Consumer checking accounts

(1)

up a net

2.5% YoY

Average deposit cost of 20 bps down 2 bps from

4Q11 and 10 bps YoY

Average Deposits and Rates

($ in billions)

Average deposit cost

Average Core Checking and Savings

($ in billions)

(1) Checking account growth is 12-months ending February 2012.

|

Wells Fargo

1Q12 Supplement 8

Net interest income

Net Interest Income (TE)

(1)

($ in millions)

Tax-equivalent net interest income

(1)

stable from

4Q11; NIM up 2 bps

Average earning assets flat on:

-

$11.6 billion increase in AFS securities and $2.1

billion increase in mortgages held for sale

-

Short-term investments/cash down $12.0 billion

and trading assets down $1.7 billion

NIM increased 2 bps as increased balance sheet

efficiency and pricing discipline was largely offset

by balance sheet repricing

-

Interest-bearing deposit costs down 3 bps in

the quarter

10,812

10,851

10,714

11,083

11,058

1Q11

2Q11

3Q11

4Q11

1Q12

4.05%

4.01%

3.84%

3.89%

3.91%

Net Interest Margin (NIM)

(1) Tax equivalent net interest income is based on the federal statutory rate of 35% for

the periods presented. Net interest income was $10,651 million, $10,678 million,

$10,542 million, $10,892 million and $10,888 million for 1Q11, 2Q11, 3Q11, 4Q11 and 1Q12 respectively. |

Wells Fargo

1Q12 Supplement 9

Noninterest income

Trust and investment fees up 7% LQ on higher retail

brokerage transaction activity and asset-based fees

Card fees down 4% LQ reflecting seasonally lower

credit card fees

Mortgage banking up $506 million, or 21%, LQ on an

8% increase in originations and higher margins

Insurance up 11% LQ on seasonally higher crop

insurance premiums

Trading gains up $210 million on $109 million higher

deferred compensation plan investment results (P&L

neutral) and stronger core customer accommodation

trading

Equity gains up $303 million LQ reflecting strong

business results and lower OTTI

Other income down $128 million LQ reflecting 4Q11

gain on sale of H.D. Vest

9,678

9,708

9,086

9,713

10,748

1Q11

2Q11

3Q11

4Q11

1Q12

vs

vs

($ in millions)

1Q12

4Q11

1Q11

Noninterest income

Service charges on deposit accounts

$

1,084

(1)

%

7

Trust and investment fees

2,839

7

(3)

Card fees

654

(4)

(32)

Other fees

1,095

-

11

Mortgage banking

2,870

21

42

Insurance

519

11

3

Net gains from trading activities

640

49

5

(7)

n.m.

(96)

Net gains from equity investments

364

n.m.

3

Operating leases

59

(2)

(23)

Other

631

(17)

54

Total nonterest income

$

10,748

11

%

11

Net losses on debt securities available

for sale |

Wells Fargo

1Q12 Supplement 10

Noninterest expense

Noninterest expense up $485 million from 4Q11

driven by higher personnel expense and

operating losses; up $260 million from 1Q11

-

Commission and incentive compensation

increased $166 million, or 7%, on annual equity

awards to retirement-eligible employees as well

as higher revenue-based compensation in

mortgage, retail brokerage and insurance

-

Employee benefits expense up $596 million

reflecting seasonally higher payroll taxes and

401(k) matching on annual incentive

compensation as well as $120 million higher

deferred compensation expense (P&L neutral)

-

Other expenses up $62 million and included:

•

$314 million higher operating losses primarily

reflecting litigation accruals on various legal

matters

1Q12 expenses included:

-

$27 million in expense initiative severance

expense vs. $133 million in 4Q11

-

~$100 million in mortgage servicing regulatory

consent orders expense in line with 4Q11

-

$218 million of merger integration costs vs.

$374 million in 4Q11

vs

vs

($ in millions)

1Q12

4Q11

1Q11

Noninterest expense

Salaries

$

3,601

(3)

%

4

Commission and incentive compensation

2,417

7

3

Employee benefits

1,608

59

16

Equipment

557

(8)

(12)

Net occupancy

704

(7)

(6)

Core deposit and other intangibles

419

(10)

(13)

FDIC and other deposit assessments

357

14

17

Other

3,330

(2)

(1)

Total noninterest expense

$

12,993

4

2

12,733

12,475

11,677

12,508

12,993

1Q11

2Q11

3Q11

4Q11

1Q12 |

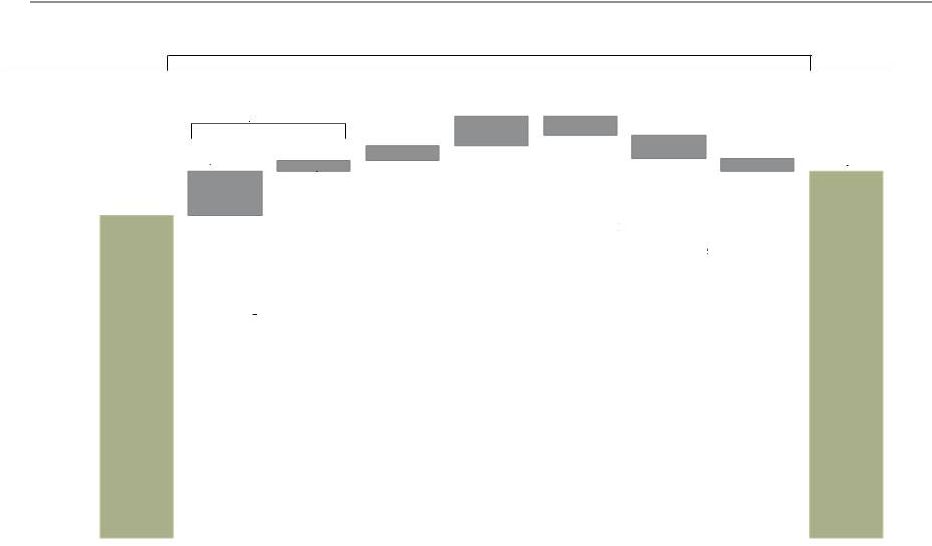

Wells Fargo

1Q12 Supplement 11

1Q12 up from 4Q11

($ in millions)

4Q11

Noninterest

Expense

1Q12

Noninterest

Expense

Noninterest expense

$12,508

$12,993

$476

$120

$166

$314

Seasonally

higher

payroll

taxes and

401(k)

matching

Higher

deferred

compensation

expense

Higher

commission

and

incentive

compensation

Higher

operating

losses

(primarily

litigation

accruals)

~($200)

($262)

($129)

Reduction

from

easonally

higher

4Q11

equipment

and

foreclosed

expense

Lower

merger

expenses

and

Compass

severance

expense

Lower all

other

expenses

s

asset

Higher employee

benefits expense of

$596 |

Wells Fargo

1Q12 Supplement 12

$12,993

~$11,250

1Q12

Noninterest

Expense

4Q12 Targeted

Noninterest

Expense

(1)

Noninterest expense projected to decline through 2012

($ in millions)

Expected 2Q12 to 4Q12

decline to be driven by:

(1) Reflects management’s current targeted noninterest expense in 4Q12.

Future 2012 noninterest expense expectations are subject to change and may be affected

by a variety of factors, including business and economic cyclicality, seasonality, changes in

our business composition and operating environment, growth in our business and/or

acquisitions, and unexpected expenses relating to, among other things, litigation and regulatory matters.

Expected 1Q12 to 2Q12

decline of $500-$700

million to be driven by:

Lower personnel expense due

to absence of 1Q12

seasonally higher

compensation, benefits and

payroll taxes

Elimination of merger

integration expenses

Lower mortgage volume-

related costs

Lower severance-related

expense

Compass initiative savings

Lower personnel expense

Lower litigation-related costs |

Wells Fargo

1Q12 Supplement 13

Community Banking

Earnings reflect strong mortgage banking results

Average loans decreased 1% as lower home equity

and credit card balances were partially offset by

growth in core auto and private student lending

Regional Banking

Continued franchise and cross-sell growth

(1)

-

Consumer checking

(2)

up a net 2.5% from 1Q11

-

Business checking

(2)

up a net 3.8% from 1Q11

-

Retail bank cross-sell of 5.98 products per

household up from 5.76 in 1Q11

•

West cross-sell = 6.35

•

East cross-sell = 5.49

Consumer Lending

Credit card penetration

(1) (3)

rose to 29.9%, up

from 29.2% in 4Q11 and 27.2% in 1Q11

Record consumer auto originations of $6 billion, up

25% LQ and 10% YoY

Mortgage originations up $9 billion from 4Q11 and

application volumes up 20%

-

15% of originations were from HARP

(4)

Quarter-end pipeline of $79 billion up 10%

from 4Q11

Managed residential mortgage servicing of $1.8

trillion up 2% YoY

vs

vs

($ in millions)

1Q12

4Q11

1Q11

Net interest income

$

7,326

(1)

%

(3)

Noninterest income

6,095

9

20

Provision for credit losses

1,878

(7)

(9)

Noninterest expense

7,825

7

3

Income tax expense

1,293

19

74

Segment earnings

$

2,348

(6)

%

8

($ in billions)

Avg loans, net

$

486.1

(1)

(4)

Avg core deposits

575.2

1

5

1Q12

4Q11

1Q11

Regional Banking

Consumer checking account growth

(1)(2)

2.5

%

3.9

7.5

Business checking account growth

(1)(2)

3.8

3.7

5.1

Retail Bank household cross-sell

(1)

5.98

5.93

5.76

vs

vs

($ in billions)

1Q12

4Q11

1Q11

Consumer Lending

Credit card penetration

(1)

29.9

%

71

bps

277

Home Mortgage

Applications

$

188

20

%

84

Application pipeline

79

10

76

Originations

129

8

54

Managed residential

mortgage servicing

($ in trillions)

$

1.8

1

2

(1) Metrics reported on a one-month lag from reported quarter-end; for

example 1Q12 cross-sell is as of February 2012. Previously reported

metrics have been restated to reflect the lagged reporting. (2) Checking

account growth is 12-months ending February 2012.

(3) Household penetration as of February 2012 and defined as the

percentage of retail banking deposit households that have a credit

card with Wells Fargo. Household penetration has been redefined to

include legacy Wells Fargo Financial accounts. (4) Home Affordable

Refinance Program. |

Wells Fargo

1Q12 Supplement 14

Wholesale Banking

Record revenue and PTPP

Net interest income up 4%

-

Average loans up $3.5 billion driven by new

loans from existing customers, new customer

growth and the Burdale acquisition

Noninterest income up 22% LQ driven by strong

capital markets, insurance and equity investment

results

Provision expense up $64 million LQ on $50

million lower reserve release

Expenses up 4% LQ driven by higher personnel

and crop insurance expenses while efficiency

ratio improved to 50.6%

(3)

Treasury Management

Commercial card spend volume of $3.68 billion

up 7% LQ and 27% YoY

Investment Banking

U.S. investment banking market share

(2)

of

4.8% down from 5.1% in FY2011

Asset Management

Total AUM down 2% LQ

-

Money market outflows were offset by higher

equity assets reflecting both higher market

valuations and positive net flows

(1) Approved and initiated.

(2) Source: Dealogic U.S. investment banking fee market share.

(3) Efficiency ratio is noninterest expense divided by total revenue (net interest

income and noninterest income). vs

vs

($ in millions)

1Q12

4Q11

1Q11

Net interest income

$

3,181

4

%

17

Noninterest income

2,852

22

5

Provision for credit losses

95

n.m.

(29)

Noninterest expense

3,054

4

10

Income tax expense

1,016

25

18

Segment earnings

$

1,868

14

%

14

($ in billions)

Avg loans, net

$

268.6

1

14

Avg core deposits

220.9

(1)

20

vs

vs

($ in billions)

1Q12

4Q11

1Q11

Key Metrics:

Commercial card spend

volume

$

3.68

7

%

27

CEO Mobile Wire volume

(1)

3.3

49

156

U.S. investment banking

market share %

(2)

4.8

%

Total AUM

$

444

(2)

(10)

Advantage Funds AUM

210

(2)

(10)

|

Wells Fargo

1Q12 Supplement 15

Wealth, Brokerage and Retirement

Net interest income down 4% LQ primarily due to

lower loan yields

Noninterest income up 2% LQ despite 4Q11 gain

on the sale of H.D. Vest

Total revenue increased 1%; excluding the 4Q11

$153 million H.D. Vest gain, revenue was up 6%

on higher retail brokerage asset-based fees,

transaction revenues and securities gains

-

Brokerage managed account asset fees priced at

beginning of quarter, reflecting 12/31/2011

market valuations

Provision expense up on lower reserve release

and recoveries

Expenses up 1% LQ on higher personnel expense

including higher revenue-based costs and

deferred compensation expense

Retail Brokerage

Managed account assets up 10% LQ and 11%

YoY driven by strong net flows and market

performance

Wealth Management

Wealth

Management

client

assets

up

2%

LQ

Retirement

IRA assets up 7% LQ

Institutional Retirement plan assets up 9% LQ

(1) Includes deposits.

(2) Data as of February 2012.

vs

vs

($ in millions)

1Q12

4Q11

1Q11

Net interest income

$

701

(4)

%

-

Noninterest income

2,361

2

(4)

Provision for credit losses

43

n.m.

8

Noninterest expense

2,547

1

-

Income tax expense

181

(5)

(14)

Segment earnings

$

296

(5)

%

(14)

($ in billions)

Avg loans, net

$

42.5

(1)

-

Avg core deposits

135.6

-

8

vs

vs

($ in billions, except where noted)

1Q12

4Q11

1Q11

Key Metrics:

WBR Clients Assets

(1)

($ in trillions)$

1.4

5

%

-

Cross-sell

(2)

10.16

9

bps

31

Retail Brokerage

Financial Advisors

15,134

(1)

%

(1)

Managed account assets

$

279

10

11

Client assets

(1)

($ in trillions)

1.2

6

-

Wealth Management

Client assets

(1)

202

2

(1)

Retirement

IRA Assets

287

7

1

Institutional Retirement

Plan Assets

257

9

5 |

Wells Fargo

1Q12 Supplement 16

2.21

1.84

1.81

2.04

2.00

1Q11

2Q11

3Q11

4Q11

1Q12

3.21

2.84

2.61

2.64

2.40

1Q11

2Q11

3Q11

4Q11

1Q12

Credit quality

Improved performance with lower net charge-offs

$2.4 billion net charge-offs, down $245 million LQ

and down 56% from 4Q09 peak

-

1.25% net charge-off rate, down 11 bps LQ

Provision expense of $2.0 billion, down $45

million from 4Q11, includes a $400 million reserve

release

(1)

in 1Q12 vs. $600 million in 4Q11

Allowance for credit losses = $19.1 billion

Remaining PCI nonaccretable = 25.8% of

remaining UPB

(2)

Credit metrics:

-

$678 million LQ increase in NPAs reflects $1.7

billion in additional junior lien nonaccruals

resulting from January 2012 interagency

guidance

(3)

; excluding the $1.7 billion in junior

lien nonaccruals, NPLs fell $948 million on

declines in all categories

-

Early stage consumer delinquency balances

declined 18% and rates improved 40 bps LQ

driven by seasonality

(1) Reserve release represents the amount by which net charge-offs exceed the

provision for credit losses. (2) Unpaid principal balance for PCI loans that have

not had a UPB charge-off. (3)

Interagency

Supervisory

Guidance

on

Allowance

for

Loan

and

Lease

Losses

Estimation

Practices

for

Loans

and

Lines

of

Credit

Secured

by

Junior

Liens

on

1-4 Family Residential Properties issued January 31, 2012.

Net Charge-offs

($ in billions)

1.73%

1.52%

1.37%

1.36%

1.25%

Net charge-off rate

Provision Expense

($ in billions) |

Wells Fargo

1Q12 Supplement 17

1.7

1.5

1.5

1.5

1.2

0.7

0.3

0.4

0.5

0.4

2.4

1.8

1.9

2.0

1.6

1Q11

2Q11

3Q11

4Q11

1Q12

Consumer

Commercial

Credit quality

Nonperforming Assets

($ in billions)

Consumer Loans 30-89 DPD & Still Accruing

(Balances and rates)

Loans 90+ DPD and Still Accruing

($ in billions)

(1)

Includes

$1.7

billion

at

March

31,

2012,

resulting

from

implementation

of

Interagency

Supervisory

Guidance

on

Allowance

for

Loan

and

Lease

Losses

Estimation

Practices for Loans and Lines of Credit Secured by Junior Liens on 1-4 Family Residential

Properties issued January 31, 2012. (2)

Excludes mortgage loans insured/guaranteed by the FHA or VA, reverse mortgages, margin loans

and student loans whose repayments are predominantly guaranteed by guarantee agencies

on behalf of the U.S. Department of Education under the Federal Family Education Loan Program. Also excludes the carrying value of PCI loans

contractually delinquent.

(3)

Consumer includes mortgage loans held for sale 30-89 days and 90 days or more past due and

still accruing. (1)

25.0

23.0

21.9

21.3

22.0

5.5

4.9

4.9

4.7

4.6

30.5

27.9

26.8

26.0

26.6

1Q11

2Q11

3Q11

4Q11

1Q12

Nonaccrual loans

Foreclosed assets

2.36%

2.32%

2.37%

2.40%

2.00%

8.3

8.1

8.2

8.3

6.8

$0

$5

$10

1Q11

2Q11

3Q11

4Q11

1Q12

(2) (3)

(2) (3) |

Wells Fargo

1Q12 Supplement 18

71%

19%

5%

5%

Mortgage servicing

Wells Fargo has a high quality servicing portfolio

Residential Mortgage Servicing Portfolio

$1.8 Trillion

(as of March 31, 2012)

Agency

Retained and acquired portfolio

Non-agency securitizations of

WFC originated loans

Non-agency acquired servicing

and private whole loan sales

71% of the portfolio is with the Agencies (FNMA,

FHLMC and GNMA)

19% are loans that we retained or acquired

-

Loss exposure handled through loan loss

reserves and PCI nonaccretable

5% are private securitizations where Wells Fargo

originated the loan and therefore has some

repurchase risk

-

79% prime at origination

-

58% from pre-2006 vintages

-

Insignificant amount of home equity and no

option ARMs

-

~50% do not have traditional reps and

warranties

5% are non-agency acquired servicing and

private whole loan sales

-

4% is acquired servicing where Wells Fargo

did not underwrite and securitize and has

repurchase recourse with the originator

-

1% are private whole loan sales

•

Less than 2% subprime at origination

•

Loans sold to others and subsequently

securitized are included in private

securitizations above |

Wells Fargo

1Q12 Supplement 19

Mortgage servicing

Delinquency

ratios

lower

than

peers

and

total

repurchase

demands

stable

As of 4Q11, the delinquency and foreclosure ratio

of Wells Fargo’s servicing portfolio continued to

be lower than peers, per industry data

Wells Fargo’s total delinquency and foreclosure

ratio for 1Q12 was 6.89%, down from a peak of

8.96% in 4Q09

Total repurchase demands down modestly LQ

and down approximately 25% YoY

Agency

-

Agency repurchase demands outstanding down

from 4Q11

•

Agency new demands for 2006-2008 vintages

are down slightly in 1Q12

•

Demand on newer vintage originations continue

to emerge consistent with our estimates

-

Demands and losses continued to be concentrated

in the 2006 -

early 2008 vintages

Non-Agency

-

Non-agency repurchase demands outstanding,

which includes non-agency securities, whole loans

sold and acquired servicing, up from 4Q11, but

continued to be a small percentage of total

demands outstanding

(1) Inside Mortgage Finance, data as of December 31, 2011. Industry excluding WFC

performance calculated based on IMF data.

(2) Industry is all large servicers ($6.8 trillion) including WFC, C, JPM and BAC.

(3) Includes mortgage insurance rescissions.

Total

Outstanding

Repurchase

Demands

(3)

and

Agency

New

Demands

for

2006-2008

Vintages

4Q11 Servicing Portfolio Delinquency

Performance

(1)

$3.76

$4.31

$3.84

$2.95

$2.49

$2.24

$2.02

$2.01

$1.86

(1,000)

1,000

3,000

5,000

7,000

9,000

11,000

13,000

15,000

17,000

19,000

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

Number of Outstanding Demands

Agency New Demands for 2006

-2008 Vintages

Original Loan Balance of Outstanding Demands ($ in B)

5.63%

5.99%

6.56%

9.83%

7.21%

7.79%

2.33%

2.51%

5.01%

3.89%

3.67%

4.15%

Wells Fargo

Citi

JPM Chase

Bank of

America

Industry

Industry ex

WFC

Foreclosure Rate

Delinquency Rate

7.96%

8.50%

11.57%

13.72%

10.88%

11.94%

(2) |

Wells Fargo

1Q12 Supplement 20

Capital

Capital remained strong and continued to grow internally

8.93%

9.15%

9.34%

9.46%

9.95%

1Q11

2Q11

3Q11

4Q11

1Q12

Tier 1 common equity ratio increased 49 bps

in 1Q12

Tier 1 common equity ratio under Basel III is

estimated to be 7.81% at 3/31/12

(1)

Increased common stock quarterly dividend rate

to $0.22 per share in 1Q12

Purchased 7.6 million common shares in 1Q12

Called $875 million of 6.38% trust preferred

securities; to be redeemed on 4/13/12

See

Appendix

page

39

for

additional

information

on

Tier

1

common

equity.

1Q12 capital ratios are preliminary estimates.

(1)

Pro

forma

Basel

III

calculation

based

on

Tier

1

common

equity,

as

adjusted

to

reflect

management’s

interpretation

of

current

Basel

III

capital

proposals.

This

pro forma calculation is subject to change depending on final promulgation of Basel III

capital rulemaking and interpretations thereof by regulatory authorities. See page 40

for additional information. Tier 1 Common Equity Ratio |

Wells Fargo

1Q12 Supplement 21

Summary

Record earnings of $4.2 billion

Robust revenue growth on strong noninterest income

Expenses up on higher revenues and seasonality

-

2Q12

expense

currently

expected

to

decline

$500

-

$700

million

-

Noninterest

expense

expected

to

decline

to

~$11,250

million

in

4Q12

(1)

Higher pre-tax pre-provision profit

(2)

of $8.6 billion

Positive operating leverage

Improved credit quality

Solid returns

-

ROA = 1.31%

-

ROE = 12.14%

Capital levels continued to grow

Rewarded shareholders with additional returns on their investment

-

Increased common stock quarterly dividend rate to $0.22 per share in 1Q12

(1) Reflects management’s current targeted noninterest expense in 4Q12. Future 2012

noninterest expense expectations are subject to change and may be affected by a variety

of factors, including business and economic cyclicality, seasonality, changes in our business composition and operating environment, growth in our

business and/or acquisitions, and unexpected expenses relating to, among other things,

litigation and regulatory matters. (2) Pre-tax pre-provision profit (PTPP)

is total revenue less noninterest expense. Management believes that PTPP is a useful financial measure because it enables

investors and others to assess the Company’s ability to generate capital to cover credit

losses through a credit cycle. |

Wells Fargo

1Q12 Supplement 22

Appendix |

Wells Fargo

1Q12 Supplement 23

Recent acquisitions and divestitures

Acquired from / Divestiture of

Date

2012

Pending

BNP Paribas North American Energy Lending

Estimated April 2012

Complete

Burdale Financial Holdings Limited

1Q12

EverKey Global Partners

1Q12

2011

Loan portfolio purchases

Irish Bank Resolution Corp.

4Q11

Bank of Ireland

3Q11

Allied Irish

2Q11

Acquisitions

LaCrosse Holdings, LLC

4Q11

CP Equity, LLC (remaining equity interest)

3Q11

Foreign Currency Exchange Corp. (certain assets)

3Q11

Insurance brokerage firms

7 transactions

2Q11-3Q11

Divestitures

H.D. Vest Financial Services

4Q11

Wells Fargo Third Party Administrator, Inc.

4Q11

WFF Canadian, Guam and Saipan receivables

4Q11

American E&S

2Q11 |

Wells Fargo

1Q12 Supplement 24

(1) Net of purchase accounting adjustments.

-$64.0

Non-strategic/liquidating loan portfolio risk reduction

-$5.0

-$82.6

-$5.3

-$4.2

-$4.1

($ in billions)

1Q12

4Q11

3Q11

2Q11

1Q11

4Q08

Pick-a-Pay mortgage

(1)

$

64.0

65.7

67.4

69.6

71.5

95.3

Liquidating home equity

5.5

5.7

6.0

6.3

6.6

10.3

Legacy WFF indirect auto

1.9

2.5

3.1

3.9

4.9

18.2

Legacy WFF debt consolidation

16.0

16.5

17.2

17.7

18.4

25.3

Education

Finance

-

gov't guaranteed

14.8

15.4

15.6

16.3

16.9

20.5

Legacy WB C&I, CRE and foreign PCI loans

(1)

5.2

5.7

6.3

7.0

7.5

18.7

Legacy WB other PCI loans

(1)

0.8

0.8

0.9

1.0

1.0

2.5

Total

$

108.2

112.3

116.5

121.8

126.8

190.8 |

Wells Fargo

1Q12 Supplement 25

Purchased credit-impaired (PCI) portfolios

Legacy Wachovia PCI loans continued to perform better than originally expected

(1)

there will be a loss of contractually due amounts upon final resolution of the loan.

(2) Reflects releases of $1.8 billion for loan resolutions and $4.4 billion from the

reclassification of nonaccretable difference to the accretable yield, which will result

in increasing income over the remaining life of the loan or pool of loans. ($ in

billions) Adjusted unpaid principal balance

(1)

December 31, 2008

$

29.2

62.5

6.5

98.2

December 31, 2011

8.5

36.9

1.8

47.2

March 31, 2012

7.8

35.8

1.8

45.4

Nonaccretable difference rollforward

12/31/08 Nonaccretable difference

$

10.4

26.5

4.0

40.9

Addition of nonaccretable difference due to acquisitions

0.2

-

-

0.2

Losses from loan resolutions and write-downs

(6.9)

(15.5)

(2.6)

(25.0)

Release of nonaccretable difference since merger

(3.0)

(2.4)

(0.8)

(6.2)

(2)

3/31/12 Remaining nonaccretable difference

0.7

8.6

0.6

9.9

Life-to-date net performance

Additional provision since 2008 merger

$

(1.7)

-

(0.1)

(1.8)

Release of nonaccretable difference since 2008 merger

3.0

2.4

0.8

6.2

(2)

Net performance

1.3

2.4

0.7

4.4

Commercial

Pick-a-Pay

Other

consumer

Total

Includes write-downs taken on loans where severe delinquency (normally 180 days) or other

indications of severe borrower financial stress exist that indicate |

Wells Fargo

1Q12 Supplement 26

(1)

settlement. Pick-a-Pay and Other consumer PCI loans do not reflect nonaccretable

difference releases for settlements with borrowers due to pool accounting for

those

loans,

which

assumes

that

the

amount

received

approximates

the

pool

performance

expectations.

(2) Release

of

the

nonaccretable

difference

as

a

result

of

sales

to

third

parties

increases

noninterest

income

in

the

period

of

the

sale.

(3)

Reclassification

of

nonaccretable

difference

to

accretable

yield

for

loans

with

increased

cash

flow

estimates

will

result

in

increased

interest

income

as

a

prospective

yield

adjustment

over

the

remaining

life

of

the

loan

or

pool

of

loans.

(4)

Write-downs to net realizable value of PCI loans are absorbed by the nonaccretable

difference when severe delinquency (normally 180 days) or other indications of severe

borrower financial stress exist that indicate there will be a loss of contractually due amounts upon final resolution of the loan.

(5) Unpaid principal balance of loans without write-downs.

$9.9 billion in nonaccretable difference remains to absorb losses on PCI loans

-

Remaining

nonaccretable

=

25.8%

of

unpaid

principal

balance

(UPB)

(5)

•

Remaining

Pick-a-Pay

nonaccretable

=

28.3%

of

Pick-a-Pay

UPB

(5)

PCI nonaccretable difference

Analysis of nonaccretable difference for PCI loans

($ in millions)

Pick-a-Pay

Total

Balance at December 31, 2011

$

929

9,126

Addition of nonaccretable difference due to acquisitions

-

-

-

Release of nonaccretable difference due to:

Loans

resolved

by

settlement

with

borrower

(1)

(28)

-

-

Loans

resolved

by

sales

to

third

parties

(2)

-

-

-

Reclassification

to

accretable

yield

for

loans

with

improving

credit-related

cash

flows

(3)

(108)

-

Use of nonaccretable difference due to:

Losses

from

loan

resolutions

and

write-downs

(4)

(45)

(505)

Balance at March 31, 2012

$

748

8,621

-

(127)

(19)

(28)

-

(235)

(569)

Commercial

652

10,707

Other

consumer

506

9,875

Release of the nonaccretable difference for settlement with borrower, on individually

accounted PCI loans, increases interest income in the period of |

Wells Fargo

1Q12 Supplement 27

1Q12 results included accretion of $514 million, down modestly from 4Q11 as balances and yields

declined Balance of $15.8 billion expected to accrete to income over the remaining life

of the underlying loans PCI accretable yield

(1) Includes accretable yield released as a result of settlements with borrowers, which

is included in interest income. (2) Includes accretable yield released as a

result of sales to third parties, which is included in noninterest income. (3)

Represents changes in cash flows expected to be collected due to changes in interest rates on variable rate PCI loans, changes in prepayment assumptions

and the impact of modifications.

Cumulative

Accretable yield rollforward

since

($ in millions)

1Q12

4Q11

merger

Total, beginning of period

$

15,961

16,896

10,447

Addition of accretable yield due to acquisitions

-

124

128

Accretion

into

interest

income

(1)

(514)

(551)

(7,713)

Accretion

into

noninterest

income

due

to

sales

(2)

-

(1)

(237)

Reclassification from nonaccretable difference for loans with improving cash flows

235

55

4,448

Changes

in

expected

cash

flows

that

do

not

affect

nonaccretable

difference

(3)

81

(562)

8,690

Total, end of period

$

15,763

15,961

15,763 |

Wells Fargo

1Q12 Supplement 28

PCI accretable yield (Commercial and Pick-a-Pay)

Includes both legacy Wachovia PCI loans as well as recently purchased PCI loans.

Commercial PCI Accretable Yield

($ in millions)

1Q12

4Q11

3Q11

PCI interest income

Accretion

$

182

198

220

Resolution income

28

44

65

Average carrying value

6,638

6,812

6,672

Accretable yield percentage

Accretion

10.94

%

11.62

13.20

Accretable yield balance

$

1,347

1,363

1,303

Weighted average life (years)

2.8

3.2

2.7

Pick-a-Pay PCI Accretable Yield

($ in millions)

1Q12

4Q11

3Q11

PCI interest income

Accretion

$

311

326

310

Average carrying value

28,734

29,331

30,168

Accretable yield percentage

4.32

%

4.45

4.11

Accretable yield balance

$

13,709

14,018

14,989

Weighted average life (years)

11.0

11.0

11.0

|

Wells Fargo

1Q12 Supplement 29

1Q12 Credit quality highlights

Net charge-offs of $2.4 billion down $245 million LQ

–

Commercial losses down $86 million as higher CRE

construction losses were more than offset by

declines in all other categories

–

Consumer losses down $159 million on declines

across all asset classes

Total NPAs of $26.6 billion up $678 million

–

Nonaccrual loans up $722 million on:

•

$1.7

billion

in

junior

lien

nonaccruals

(1)

on

implementation of interagency guidance

12% were 30+ DPD

•

Partially offset by declines in all other categories

–

Foreclosed assets down $44 million

•

57% of the balance are government guaranteed

loans and loans written down through purchase

accounting

$1.4 billion, or 29%, are government

guaranteed

$1.3 billion, or 28%, reflects shift from

PCI loans to REO ($432 million consumer

and $875 million C&I and CRE)

Currently expect future reserve releases absent

significant deterioration in the economy

(1) Resulting from implementation of Interagency Supervisory Guidance on Allowance for

Loan and Lease Losses Estimation Practices for Loans and Lines of Credit Secured by

Junior Liens on 1-4 Family Residential Properties issued January 31, 2012. Total

($ in millions)

Wells Fargo

Commercial loans

$

6,254

339,495

345,749

Consumer loans

29,280

391,492

420,772

Total period-end loans

$

35,534

730,987

766,521

Total nonaccrual loans

$

22,026

Total foreclosed assets

4,617

Total NPAs

$

26,643

as % of loans

3.48

%

Provision for credit losses

$

1,995

Net charge-offs

2,395

as % of avg loans

1.25

%

Commercial

0.45

Consumer

1.91

%

Allowance for credit losses

19,129

as % of loans

2.50

%

as % of nonaccrual loans

87

%

1Q12

PCI loans

Non PCI

loans

$ |

Wells Fargo

1Q12 Supplement 30

Commercial real estate (CRE) loan portfolio

Outstandings down modestly from 4Q11

Nonaccruals down $185 million, or 12 bps, on

lower real estate construction NPLs

Net charge-offs stable LQ

($ in millions)

1Q12

4Q11

CRE outstandings

Real estate mortgage

$

105,874

105,975

Real estate construction

18,549

19,382

Total CRE outstandings

124,423

125,357

Nonaccrual loans

Real estate mortgage

$

4,081

4,085

Real estate construction

1,709

1,890

Total nonaccrual loans

5,790

5,975

as % of loans

4.65

%

4.77

Net charge-offs (recoveries)

Real estate mortgage

$

46

117

Real estate construction

67

(5)

Total net charge-offs

113

112

as % of avg loans

0.36

%

0.36

|

Wells Fargo

1Q12 Supplement 31

Pick-a-Pay mortgage portfolio

Carrying

value

of

$64.0

billion

in

first

lien

loans

outstanding,

down

$1.7

billion

from

4Q11

and

down

$31.3

billion from 4Q08 on paid-in-full loans and loss mitigation efforts

–

Adjusted unpaid principal balance of $71.2 billion, down $2.1 billion from 4Q11 and down $44.5

billion from 4Q08

–

$4.0 billion in modification principal forgiveness since acquisition reflects over 103,000

completed full-term modifications; additional $616 million of conditional

forgiveness that can be earned by borrowers through performance over the next 3 years

–

Modification redefault rate has been consistently better than the industry average (as

measured by 60+ DPD after six months)

($ in millions)

Product type

Adjusted

unpaid

principal

balance

% of total

Adjusted

unpaid

principal

balance

% of total

Adjusted

unpaid

principal

balance

% of total

Option payment loans

(1)

$

37,251

52

%

$

39,164

53

%

$

99,937

86

%

Non-option payment adjustable-rate and

fixed-rate loans

(1)

9,673

14

9,986

14

15,763

14

Full-term loan modifications

(1)

24,284

34

24,207

33

-

-

Total adjusted unpaid principal balance

(1)

$

71,208

100

%

$

73,357

100

%

$

115,700

100

%

Total carrying value

63,983

65,652

95,315

At 12/31/2011

At 3/31/2012

At 12/31/2008

(1)

Adjusted unpaid principal includes write-downs taken on loans where severe delinquency

(normally 180 days) or other indications of severe borrower financial stress exist that

indicate there will be a loss of contractually due amounts upon final resolution of the loan. |

Wells Fargo

1Q12 Supplement 32

Pick-a-Pay credit highlights

Non-PCI portfolio

Loans down 3% driven by loans paid-in-full

85% of portfolio current

Nonaccrual loans consistent with 4Q11 levels

–

$130 million of nonaccrual TDRs reclassified to

accruing TDR status based on borrower payment

performance

$3.9 billion in nonaccruals includes $1.0 billion

of nonaccruing TDRs and an annualized loss rate

of 2.21%

Net charge-offs of $200 million in 1Q12,

consistent with expectations

41% of portfolio with LTV

(2)

80%

PCI portfolio

Carrying value down 2%

69% of portfolio current vs. 67% in 4Q11

Life-of-loan losses continued to be lower than

originally projected at time of merger

(1)

The carrying value, which does not reflect the allowance for loan losses, includes purchase

accounting adjustments, which, for PCI loans, are the nonaccretable difference

and

the

accretable

yield,

and

for

all

other

loans,

an

adjustment

to

mark

the

loans

to

a

market

yield

at

date

of

merger

less

any

subsequent

charge-offs.

(2) The current loan-to-value (LTV) ratio is calculated as the net carrying

value (defined in (1) above) divided by the collateral value. (3) The adjusted

unpaid principal balance includes write-downs taken on loans where severe delinquency (normally 180 days) or other indications of severe borrower

financial stress exist that indicate there will be a loss of contractually due amounts upon

final resolution of the loan. ($ in millions)

1Q12

4Q11

Non-PCI loans

Carrying value

(1)

$

35,563

36,596

Nonaccrual loans

3,918

3,909

as a % of loans

11.02

%

10.68

Net charge-offs

$

200

196

as % of avg loans

2.21

%

2.11

90+ days past due

as % of loans

10.27

10.07

Current average LTV

(2)

86

%

86

Current average FICO

681

681

Contractual average loan size

$

208,000

210,000

Contractual average age of loans

8.04

years

7.79

% of loans in California

49

%

49

($ in millions)

PCI loans

Adjusted unpaid principal balance

(3)

$

35,785

36,905

Carrying value

(1)

28,420

29,056

Current average LTV

(2)

90

%

91

Current average FICO

612

610

Contractual average loan size

$

310,000

311,000

Contractual average age of loans

6.00

years

5.75

% of loans in California

68

%

68 |

Wells Fargo

1Q12 Supplement 33

Real estate 1-4 family first mortgage portfolio

First lien mortgage loans stable as growth in core

first lien mortgage was offset by continued run-off

in the liquidating portfolio

-

Pick-a-Pay non-PCI portfolio down 3%

-

PCI portfolio down 2%

-

Debt consolidation first lien down 3%

-

Core first lien up $2.2 billion, or 1%, reflecting

strong origination volumes

Core first lien mortgage nonaccruals down $260

million, or 23 bps

Core net charge-offs down $19 million

(1) Ratios on WFF debt consolidation first mortgage loan portfolio only.

(2) Ratios on non runoff first lien mortgage loan portfolio only.

($ in millions)

1Q12

4Q11

Total real estate 1-4 family first mortgage

$

228,885

228,894

Less consumer non-strategic/liquidating portfolios:

Pick-a-Pay non-PCI first lien mortgage

35,563

36,596

PCI first lien mortgage

29,082

29,746

WFF debt consolidation first mortgage portfolio

15,610

16,117

Core first lien mortgage

148,630

146,435

Nonaccrual loans

$

2,284

2,263

as % of loans

14.63 %

14.04

Net charge-offs

$

195

233

as % of average loans

4.91 %

5.67

Nonaccrual loans

$

4,481

4,741

as % of loans

3.01 %

3.24

Net charge-offs

$

396

415

as % of loans

1.07 %

1.12

WFF

debt

consolidation

first

mortgage

loan

performance

(1)

Core

first

lien

mortgage

loan

performance

(2) |

Wells Fargo

1Q12 Supplement 34

Home equity portfolio

Core Portfolio

(1)

Outstandings

down 3%

-

High quality new originations with weighted

average CLTV of 62%, 778 FICO, and 31% total

debt service ratio

1Q12 losses increased $3 million, or 12 bps

2+ delinquencies decreased $292 million

Delinquency rate for loans with a CLTV >100%

declined 43 bps

Liquidating

Portfolio

Outstandings down 4%

1Q12 losses down $21 million, or 98 bps

2+ delinquencies declined $29 million

Continued decline in delinquency rate for loans

with a CLTV >100%, 33 bps improvement

Excludes purchased credit-impaired loans.

(1) Includes equity lines of credit and closed-end junior liens associated with the

Pick-a-Pay portfolio totaling $1.5 billion at March 31, 2012, and December 31,

2011.

(2) CLTV

is

calculated

based

on

outstanding

balance

plus

unused

lines

of

credit

divided

by

estimated

home

value.

Estimated

home

values

are

determined

predominantly based on automated valuation models updated through March 2012.

(3) Unsecured balances, representing the percentage of outstanding balances above the most

recent home value. ($ in millions)

1Q12

4Q11

Core Portfolio

(1)

Outstandings

98,009

100,882

Net charge-offs

721

718

as % of avg loans

2.91

%

2.79

2+ payments past due

2,854

3,146

as % loans

2.92

%

3.13

% CLTV > 100%

(2)

37

36

2+ payments past due

3.99

4.42

% Unsecured balances

(3)

18

17

% 1st lien position

21

20

Liquidating Portfolio

Outstandings

5,456

5,710

Net charge-offs

113

134

as % of avg loans

8.11

%

9.09

2+ payments past due

241

270

as % loans

4.41

%

4.73

% CLTV > 100%

(2)

74

74

2+ payments past due

4.69

5.02

% 1st lien position

4

4 |

Wells Fargo

1Q12 Supplement 35

$103.5 billion home equity portfolio

-

20%

in

1 lien

position

-

40%

in

junior

lien

position

behind

WFC

owned

or

serviced

1

lien

-

Excludes purchased credit-impaired loans.

(1) Delinquency represents two or more payments past due as of February 2012.

Home equity portfolio

Delinquency Status

Current 1

st

lien, Current junior lien

95.7

%

Current 1

st

lien, Delinquent junior lien

1.1

Delinquent 1

st

lien, Current junior lien

1.5

Delinquent 1

st

lien, Delinquent junior lien

1.7

st

st

40%

in

junior

lien

position

behind

third

party

1

lien

st

Delinquency Status

(1)

of

Junior

Liens

Behind

a

Wells

Fargo

1

st

Lien

Outstanding Balance % |

Wells Fargo

1Q12 Supplement 36

Credit card portfolio

$22.0 billion credit card outstandings down 4%

from 4Q11 as seasonally lower balances offset

new customer growth

–

New accounts increased 23% in the quarter with

household penetration increasing to 29.9%

(1)

•

East penetration of 20.4%

(1)

vs. 19.2% in

November 2011

–

Purchase dollar volume decreased 7% and

transactions fell 7% from 4Q11

Net charge-offs down $14 million LQ, or 23 bps,

reflecting continued steady improvement

(1) Household penetration as of February 2012 and defined as the percentage of retail

banking deposit households that have a credit card with Wells Fargo. Household

penetration has been redefined to include Wells Fargo Financial accounts. ($ in

millions) 1Q12

4Q11

Credit card outstandings

$

21,998

22,836

Net charge-offs

242

256

as % of avg loans

4.40

%

4.63 |

Wells Fargo

1Q12 Supplement 37

($ in millions)

1Q12

4Q11

Direct

Auto outstandings

$

2,380

2,529

Nonaccrual loans

56

67

as % of loans

2.35

%

2.66

Net charge-offs

$

7

16

as % of avg loans

1.09

%

2.43

30+ days past due

$

31

75

as % of loans

1.31

%

2.98

Indirect

Auto outstandings

$

40,908

39,647

Nonaccrual loans

9

9

as % of loans

0.02

%

0.02

Net charge-offs

$

54

68

as % of avg loans

0.57

%

0.69

30+ days past due

$

447

571

as % of loans

1.09

%

1.44

Auto outstandings

$

6,043

5,660

Nonaccrual loans

-

6

as % of loans

-

%

0.11

Net charge-offs (recoveries)

$

(3)

(1)

as % of avg loans

n.m.

%

n.m.

Commercial Portfolio

Core Consumer Portfolios

Auto portfolios

(1)

Core Consumer Portfolio

Core auto outstandings of $43.2 billion up 3% LQ

and up 8% YoY

Originations were up 25% LQ and 10% YoY

reflecting growth across the credit spectrum

Net charge-offs were down $23 million, or 27%,

LQ on low delinquencies and continued strong

used car values

March Manheim index of 126.2, up 1% LQ and up

2% from March 2011

30+ days past due decreased $168 million LQ, or

43 bps, reflecting continued improvement in

portfolio quality as well as seasonal improvement

Commercial Portfolio

Loans of $6.0 billion increased 7% LQ reflecting

improved demand in floor plan lending

Nonaccrual loans down $6 million on continued

strong performance of the portfolio

(1) Legacy Wells Fargo Financial indirect portfolio balance as of March 31, 2012, was

$1,907 million. |

| Wells Fargo

1Q12 Supplement 38

Forward-looking statements and additional information

Forward-looking statements:

This Quarterly Supplement and management’s related presentation contain

forward-looking statements about our future financial performance.

These

forward-looking

statements

include

statements

using

words

such

as

“believe,”

“expect,”

“anticipate,”

“estimate,”

“target”, “should,”

“may,”

“can,”

“will,”

“outlook,”

“appears”

or similar expressions. These forward-looking statements may include,

among others, statements about: expected or estimated future losses in our loan portfolios,

including our belief that the allowance for loan losses is expected to decline;

expected or estimated loan loss reserve releases; mortgage repurchase exposure; exposure

related to mortgage practices, including foreclosures and servicing; our noninterest expense,

including our targeted noninterest expense for second quarter 2012 and fourth quarter

2012 as part of our expense management initiatives; the future economic environment;

loan growth; our net interest margin; reduction or mitigation of risk in our loan portfolios; future effects of loan

modification programs; life-of-loan loss estimates; the estimated impact of regulatory

reform on our financial results and business and expectations regarding our efforts to

mitigate such impact; and our estimated Tier 1 common equity ratio as of March 31, 2012,

under proposed Basel capital rules. Investors are urged to not unduly rely on

forward-looking statements as actual results could differ materially

from

expectations.

Forward-looking

statements

speak

only

as

of

the

date

made,

and

we

do

not

undertake

to

update

them

to reflect changes or events that occur after that date. For more information about factors

that could cause actual results to differ materially from expectations, refer to page

13 of Wells Fargo’s press release announcing our first quarter 2012 results, as well as

Wells

Fargo’s

reports

filed

with

the

Securities

and

Exchange

Commission,

including

the

discussion

under

“Risk

Factors”

in

our

Annual

Report on Form 10-K for the year ended December 31, 2011.

Purchased credit-impaired loan portfolio:

Loans that were acquired from Wachovia that were considered credit impaired were written down

at acquisition date in purchase accounting to an amount estimated to be collectible and

the related allowance for loan losses was not carried over to Wells Fargo’s

allowance. In addition, such purchased credit-impaired loans are not classified as

nonaccrual or nonperforming, and are not included in loans that were contractually 90+

days past due and still accruing. Any losses on such loans are charged against the nonaccretable

difference established in purchase accounting and are not reported as charge-offs (until

such difference is fully utilized). As a result of accounting for purchased loans with

evidence of credit deterioration, certain ratios of the combined company are not comparable to a

portfolio that does not include purchased credit-impaired loans.

In certain cases, the purchased credit-impaired loans may affect portfolio credit ratios

and trends. Management believes that the presentation of information adjusted to

exclude the purchased credit-impaired loans provides useful disclosure regarding the credit

quality of the non-impaired loan portfolio. Accordingly, certain of the loan balances and

credit ratios in this Quarterly Supplement have been adjusted to exclude the purchased

credit-impaired loans. References in this Quarterly Supplement to impaired loans mean

the

purchased

credit-impaired

loans.

Please

see

pages

30-32

of

the

press

release

for

additional

information

regarding

the

purchased

credit-impaired loans. |

Wells Fargo

1Q12 Supplement 39

Tier 1 common equity under Basel I

(1)

Quarter ended

Mar. 31,

Dec. 31,

Sept. 30,

June 30,

Mar. 31,

2012

2011

2011

2011

2011

$

146.8

141.7

139.2

137.9

134.9

(1.3)

(1.5)

(1.5)

(1.5)

(1.5)

145.5

140.2

137.7

136.4

133.4

(10.6)

(10.6)

(10.6)

(10.6)

(10.6)

(33.7)

(34.0)

(34.4)

(34.6)

(35.1)

3.7

3.8

4.0

4.1

4.2

(0.9)

(0.8)

(0.7)

(0.9)

(0.9)

(4.1)

(3.1)

(3.7)

(5.3)

(4.9)

(0.4)

(0.4)

(0.4)

(0.3)

(0.1)

(A)

$

99.5

95.1

91.9

88.8

86.0

(B)

$

1,000.1

1,005.6

983.2

970.2

962.9

(A)/(B)

9.95

%

9.46

9.34

9.15

8.93

(1)

(2)

MSRs over specified limitations

Wells Fargo & Company and Subsidiaries

($ in billions)

Total equity

Noncontrolling interests

Total Wells Fargo stockholders' equity

Adjustments:

FIVE

QUARTER

TIER

1

COMMON

EQUITY

UNDER

BASEL

I

(1)

Preferred equity

Goodwill and intangible assets (other than MSRs)

Applicable deferred taxes

Total risk-weighted assets

(2)

Tier 1 common equity to total risk-weighted assets

Cumulative other comprehensive income

Under the regulatory guidelines for risk-based capital, on-balance sheet assets and credit

equivalent amounts of derivatives and off-balance sheet items are assigned to one of several broad risk

categories according to the obligor or, if relevant, the guarantor or the nature of any collateral. The

aggregate dollar amount in each risk category is then multiplied by the risk weight associated with

that category. The resulting weighted values from each of the risk categories are aggregated for

determining total risk-weighted assets. The Company's March 31, 2012, preliminary risk-weighted

assets reflect estimated on-balance sheet risk-weighted assets of $831.2 billion and derivative

and off-balance sheet risk-weighted assets of $169.0 billion. Tier

1

common

equity

is

a

non-generally

accepted

accounting

principle

(GAAP)

financial

measure

that

is

used

by

investors,

analysts

and

bank

regulatory

agencies

to

assess

the

capital

position

of

financial services companies. Management reviews Tier 1 common equity along with other measures of

capital as part of its financial analyses and has included this non-GAAP financial information, and

the corresponding reconciliation to total equity, because of current interest in such information on

the part of market participants. Other

Tier 1 common equity |

Wells Fargo

1Q12 Supplement 40

Tier 1 common equity under Basel III (Estimated)

(1)

Quarter ended

Mar. 31,

2012

$

99.5

4.1

0.9

Other

0.6

(C)

105.1

(D)

$

1,346.0

(C)/(D)

7.81

%

Wells Fargo & Company and Subsidiaries

($ in billions)

Tier 1 common equity under Basel I

Adjustments from Basel I to Basel III:

Impact

of

threshold

deductions

defined

under

Basel

III

(2)

(3)

Tier 1 common equity anticipated under Basel III

Total

risk-weighted

assets

anticipated

under

Basel

III

(4)

Tier 1 common equity to total risk-weighted assets

anticipated under Basel III

(1 ) Tier 1 common equity is a non-generally accepted

accounting principle (GAAP) financial measure that is used by investors, analysts and

bank regulatory agencies to assess the capital position of financial

services companies. Management reviews Tier 1 common equity along

with other measures of capital as part of its financial analyses and

has included this non-GAAP financial information, and the

corresponding reconciliation to total equity, because of current

interest in such information on the part of market participants. (2) Volatility in interest rates can have a

significant impact on the valuation of cumulative other comprehensive income and MSRs and

therefore, impact adjustments under Basel III in future

reporting periods. (3) Threshold deductions under Basel III include

individual and aggregate limitations, as a percentage of Tier 1 common equity (as defined

under Basel III), with respect to MSRs, deferred tax assets and

investments in unconsolidated financial companies. (4) Under current Basel proposals,

risk-weighted assets incorporate different classifications of assets, with certain risk weights based on a

borrower's credit rating or Wells Fargo's own risk models, along with

adjustments to address a combination of credit/counterparty, operational and market risks, and other Basel III

elements. The amount of risk-weighted assets anticipated under Basel III is preliminary

and subject to change depending on final promulgation of Basel III

capital rulemaking and interpretations thereof by regulatory authorities.

Cumulative other comprehensive income

(2)

(1)

TIER 1 COMMON EQUITY UNDER BASEL III (ESTIMATED) |