Attached files

| file | filename |

|---|---|

| 8-K - 8-K - CONSUMERS ENERGY CO | d327240d8k.htm |

Exhibit 99.1

Midwest Utilities Seminar

April 5, 2012

Foote Hydro 1918

Zeeland 2007

Lake Winds 2012

This presentation is made as of the date hereof and contains “forward-looking statements” as defined in Rule 3b-6 of the Securities Exchange Act of 1934, as amended, Rule 175 of the Securities Act of 1933, as amended, and relevant legal decisions. The forward-looking statements are subject to risks and uncertainties. They should be read in conjunction with “FORWARD-LOOKING STATEMENTS AND INFORMATION” and “RISK FACTORS” sections of CMS Energy’s and Consumers Energy’s Form 10-K for the year ended December 31 and as updated in subsequent 10-Qs. CMS Energy’s and Consumers Energy’s “FORWARD-LOOKING STATEMENTS AND INFORMATION” and “RISK FACTORS” sections are incorporated herein by reference and discuss important factors that could cause CMS Energy’s and Consumers Energy’s results to differ materially from those anticipated in such statements. CMS Energy and Consumers Energy undertake no obligation to update any of the information presented herein to reflect facts, events or circumstances after the date hereof.

The presentation also includes non-GAAP measures when describing CMS Energy’s results of operations and financial performance. A reconciliation of each of these measures to the most directly comparable GAAP measure is included in the appendix and posted on our website at www.cmsenergy.com.

Reported earnings could vary because of several factors, such as legacy issues associated with prior asset sales. Because of those uncertainties, the company is not providing reported earnings guidance.

| 2 |

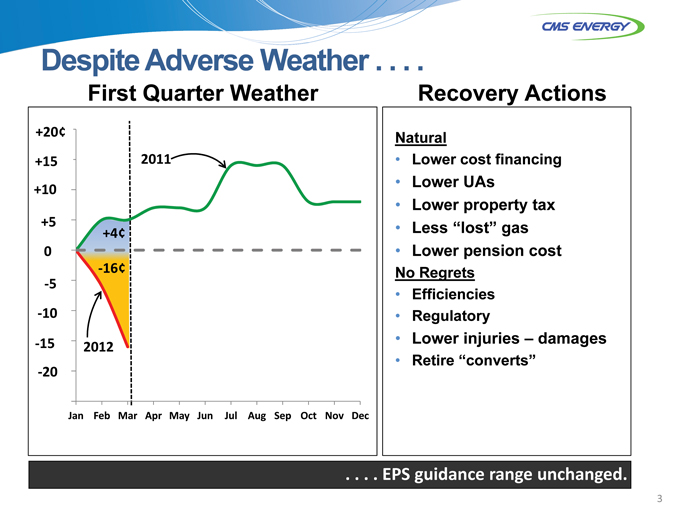

Despite Adverse Weather . . . .

First Quarter Weather

Recovery Actions

1.75 +20¢ +15 .70 +10 .65 1.60 +5 1.55 0 1.50 -5 1.45 -10—1.40 15 1.35 -20

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2011

+4¢

-16¢

2012

Natural

• Lower cost financing

• Lower UAs

• Lower property tax

• Less “lost” gas

• Lower pension cost

No Regrets

• Efficiencies

• Regulatory

• Lower injuries – damages

• Retire “converts”

. . . . EPS guidance range unchanged.

| 3 |

Business Model . . . .

RESULTS –Consistent Financial Performance

Investment

Risk Mitigation

Enablers

• Michigan Energy Law

• Supportive regulation

• Customer focus

• Cost control

• Base rates inflation

• Sales recovery

• Non-Utility improvements

• NOLs

Self-Imposed Limits

• Customer rates

• Capital

. . . . drivesrives strong performance.

| 4 |

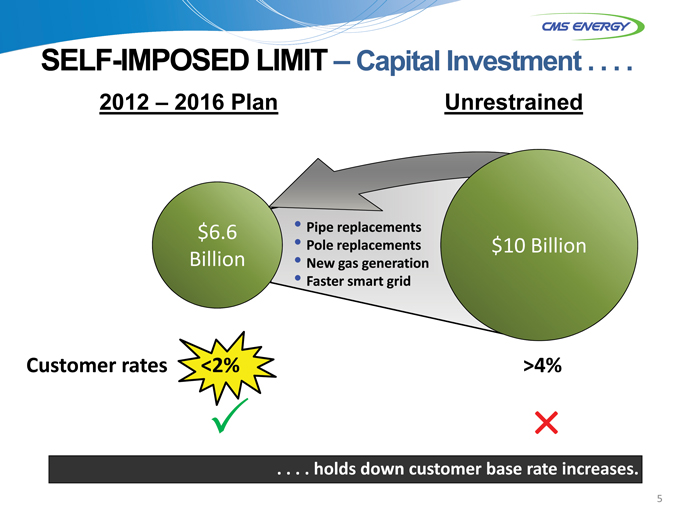

SELF-IMPOSED LIMIT – Capital Investment . . . .

2012 – 2016 Plan

Unrestrained

$6.6 Billion

• Pipe replacements

• Pole replacements

• New gas generation

• Faster smart grid

$10 Billion

Customer rates

<2%

>4%

. . . . holdsolds down customer base rate increases.

| 5 |

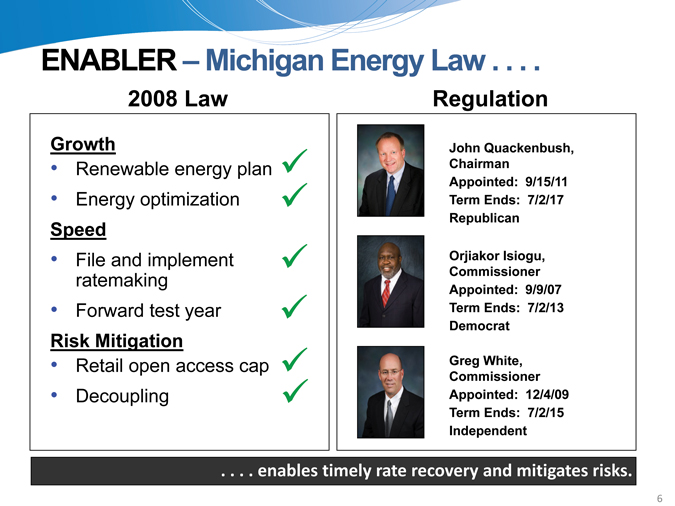

ENABLER – Michigan Energy Law . . . .

2008 Law

Growth

• Renewable energy plan

• Energy optimization

Speed

• File and implement ratemaking

• Forward test year

Risk Mitigation

• Retail open access cap

• Decoupling

Regulation

John Quackenbush, Chairman Appointed: 9/15/11 Term Ends: 7/2/17 Republican

Orjiakor Isiogu, Commissioner Appointed: 9/9/07 Term Ends: 7/2/13 Democrat

Greg White, Commissioner Appointed: 12/4/09 Term Ends: 7/2/15 Independent

. . . . enables timely rate recovery and mitigates risks.

| 6 |

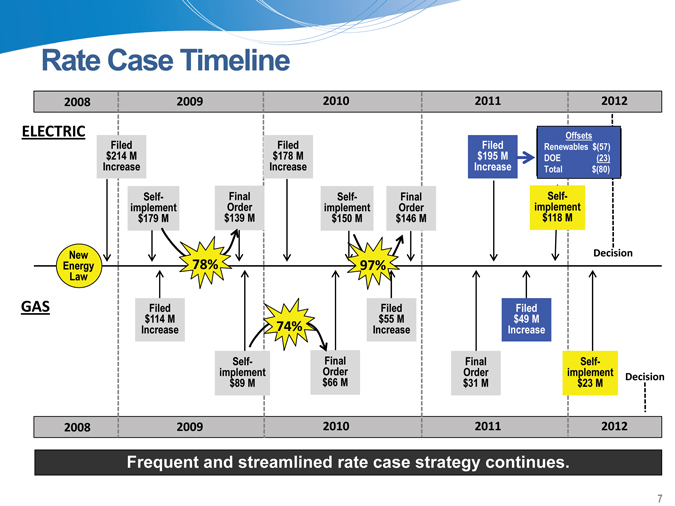

Rate Case Timeline

2008

2009

2010

2011

2012

ELECTRIC

$Filed 214 M Increase

$Filed 178 M Increase

$Filed 195 M Increase

Offsets Renewables $(57) DOE (23) Total $(80)

implement Self- $179 M

Order Final $139 M

implement Self- $150 M

Order Final $146 M

implement Self- $118 M

Energy New Law

78%

97%%

Decision

GAS

$Filed 114 M Increase

74%

implement Self-

$89 M

Order Final

$66 M

$ Filed 55 M Increase

Order Final

$31 M

implement Self-

$23 M

$ Filed 49 M Increase

Decision

2008

2009

2010

2011

2012

Frequent and streamlined rate case strategy continues.

| 7 |

Ongoing Regulatory Strategy . . . .

• Michigan investment

• Base rate increases inflation

• Rate “offsets”

• Communication and alignment

. . . . balances customer interests and investor certainty.

| 8 |

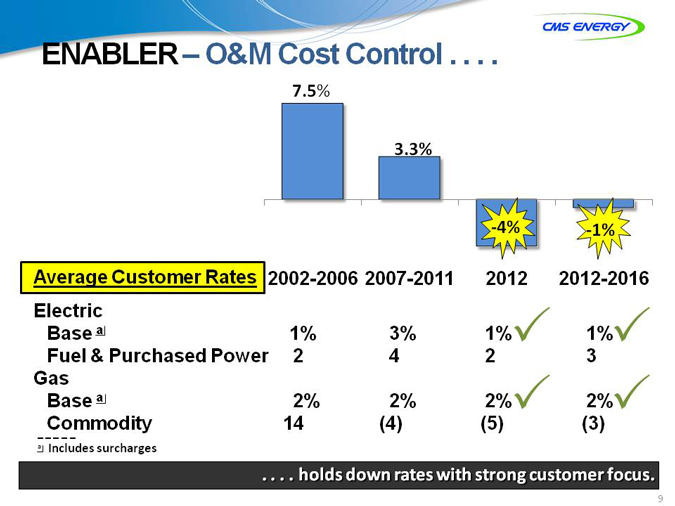

ENABLER – O&M Cost Control . . . .

7.5%

3.3%

-4%

-1%

Average Customer Rates

2002-2006 2007-2011

2012 2012-2016

Electric Base a

Fuel & Purchased Power Gas Base a Commodity

a Includes surcharges

1% 3% 1% 1%

| 2 |

4 2 3 |

2% 2% 2%32% 3

14 (4) (5) (3)

. . . . holds down rates with strong customer focus.

9

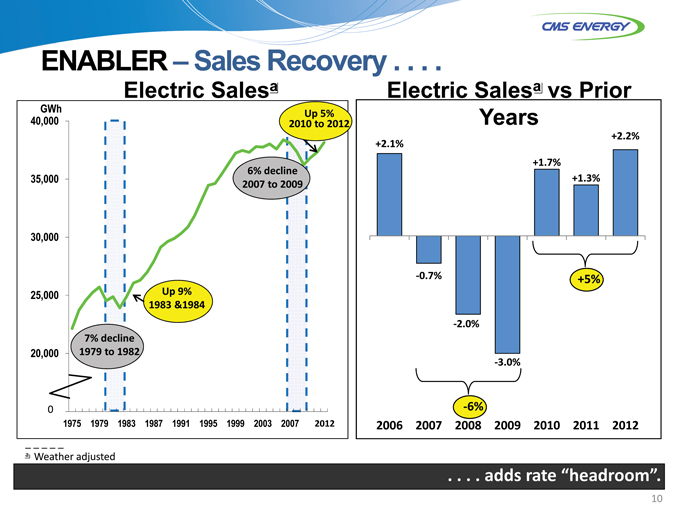

ENABLER – Sales Recovery . . . .

Electric Salesa

GWh 40,000

35,000 30,000 25,000 20,000 15,000 0

1975 1979 1983 1987 1991 1995 1999 2003 2007 2011 2012

7% decline 1979 to 1982

Up 9% 1983 &1984

6% decline 2007 to 2009

2010 Up to 5% 2012

Electric Salesa vs Prior

Years

+2.1%

+1.7%

+1.3%

+2.2%

-0.7%

-2.0%

-3.0%

+5%

-6%

2006 2007 2008 2009 2010 2011 2012

a Weather adjusted

. . . adds rate “headroom”.

10

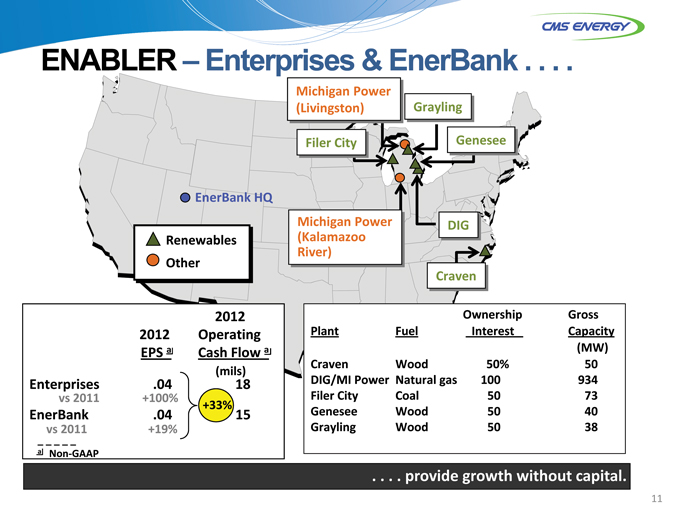

ENABLER – Enterprises & EnerBank . . . .

Michigan Power (Livingston)

Grayling

Filer City

Genesee

EnerBank HQ

Michigan Power (Kalamazoo River)

Renewables Other

DIG

Craven

2012 2012 Operating EPS a Cash Flow a Enterprises .04 (mils) 18

vs 2011 +100%

+33%

EnerBank .04 15

vs _ 2011 +19% a Non-GAAP

Ownership Gross Plant Fuel Interest Capacity (MW) Craven Wood 50% 50 DIG/MI Power Natural gas 100 934 Filer City Coal 50 73 Genesee Wood 50 40 Grayling Wood 50 38

. . . . provide growth without capital.

11

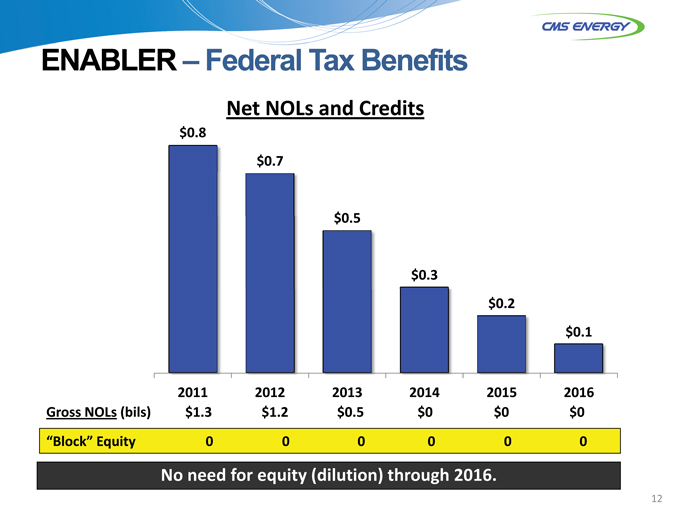

ENABLER – Federal Tax Benefits

Net NOLs and Credits

$0.8

$0.7

$0.5

$0.3

$0.2

$0.1

2011 2012 2013 2014 2015 2016 Gross NOLs (bils) $1.3 $1.2 $0.5 $0 $0 $0

“Block” Equity 0 0 0 0 0 0

No need for equity (dilution) through 2016.

12

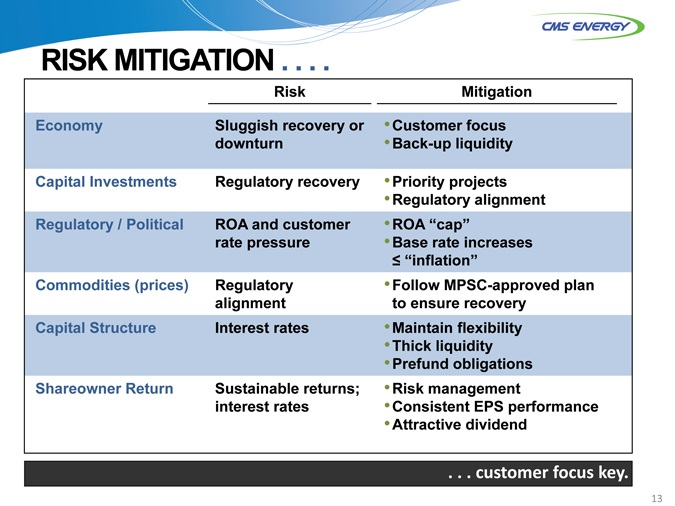

RISK MITIGATION . . . .

Risk

Mitigation

Economy Sluggish recovery or •Customer focus downturn •Back-up liquidity

Capital Investments Regulatory recovery •Priority projects •Regulatory alignment

Regulatory / Political ROA and customer •ROA “cap” rate pressure •Base rate increases

“inflation”

Commodities (prices) Regulatory •Follow MPSC-approved plan alignment to ensure recovery

Capital Structure Interest rates •Maintain flexibility •Thick liquidity •Prefund obligations

Shareowner Return Sustainable returns; •Risk management interest rates •Consistent EPS performance •Attractive dividend

. . . customerustomer focus key.

13

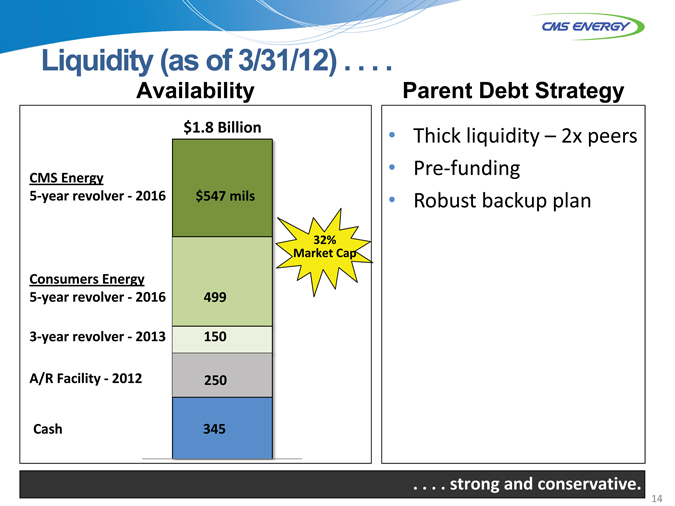

Availability

CMS Energy

5-year revolver—2016

Consumers Energy

5-year revolver—2016

3-year revolver—2013 A/R Facility—2012 Cash

$1.8 Billion

$547 mils

499

150

250

345

• Thick liquidity – 2x peers

• Pre-funding

• Robust backup plan

Parent Debt Strategy

. . . . strongtrong and conservative.

14

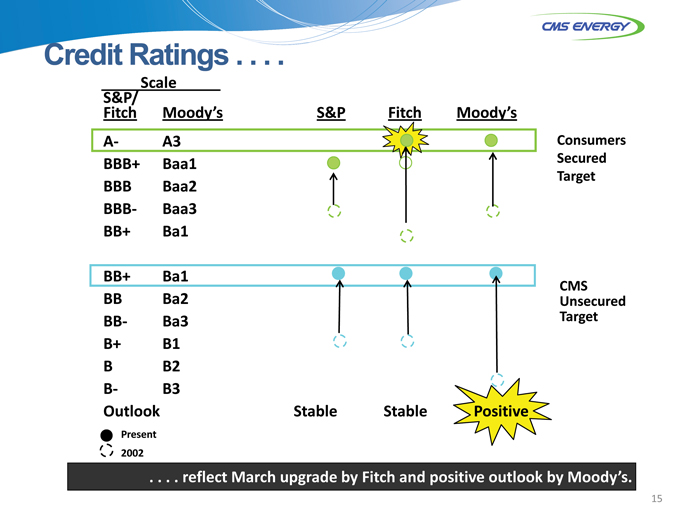

Credit Ratings . . . .

S&P/Fitch Moody’s

BBB+ Baa1 BBB Baa2 BBB- Baa3 BB+ Ba1

S&P Fitch Moody’s

Consumers Secured Target

BB+ Ba1 BB Ba2 BB- Ba3 B+ B1 B B2 B- B3 Outlook

Present 2002

Stable Stable

CMS Unsecured Target

. . . . reflect March upgrade by Fitch and positive outlook by Moody’s.

15

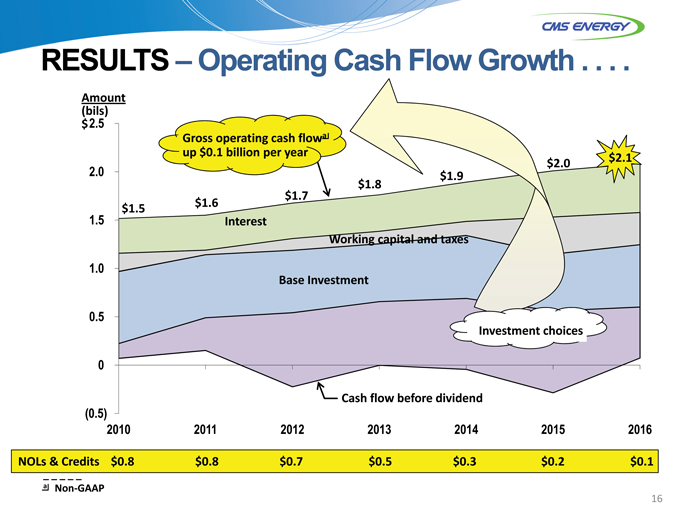

RESULTS – Operating Cash Flow Growth . . . .

Amount (bils)

$2.5 2.0 1.5 1.0 0.5 0.0 (0.5)

2010 2011 2012 2013 2014 2015 2016

NOLs & Credits $0.8 $0.8 $0.7 $0.5 $0.3 $0.2 $0.1

a Non-GAAP

Cash flow before dividend

Investment choices

Base Investment

Working capital and taxes

Interest

$1.5

$1.6

$1.7

$1.8

$1.9

$2.0

$2.1

Gross operating cash flowa up $0.1 billion per year

16

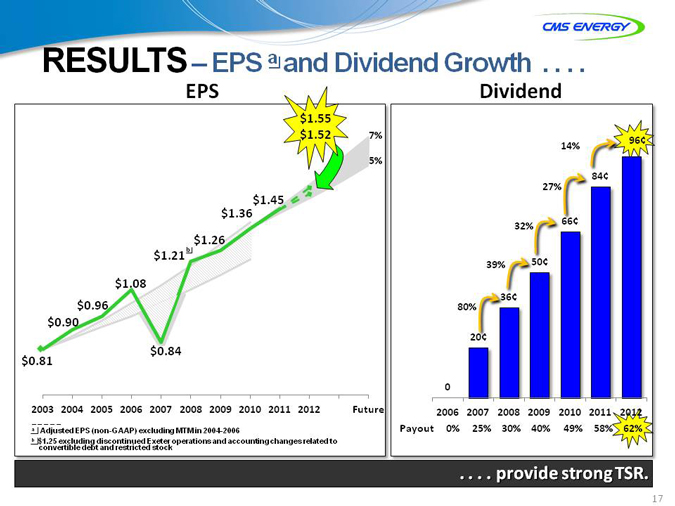

RESULTS– EPS a and Dividend Growth . . . .

EPS

$0.81

$0.90

$0.96

$1.08

$1.21 b

$1.26

$1.36

$1.45

$1.55 $1.52

7%

5%

$0.84

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Future

a Adjusted EPS (non-GAAP) excluding MTM in 2004-2006 b $1.25 excluding discontinued Exeter operations and accounting changes related to convertible debt and restricted stock

Dividend

14%

27%

32%

39%

80%

0

20¢

36¢

50¢

66¢

84¢

96¢

Payout 0% 25% 30% 40% 49% 58% 62%

2006 2007 2008 2009 2010 2011 2012

. . . . providerovide strong TSR.

17

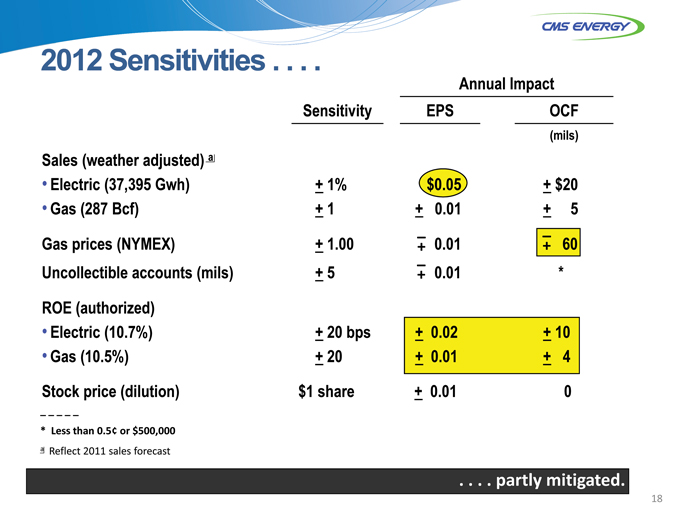

2012 Sensitivities . . . .

Annual Impact

Sensitivity

EPS OCF

(mils) Sales (weather adjusted) a • Electric (37,395 Gwh)

+ 1%

$0.05

+

$20

• Gas (287 Bcf)

+ 1 +

0.01 +

5

Gas prices (NYMEX)

+ 1.00

–+

0.01

–+

60

Uncollectible accounts (mils)

+

5

–+

0.01

* ROE (authorized)

• Electric (10.7%)

+ 20 bps

+ 0.02

+ 10

• Gas (10.5%)

+

20

+

0.01

+

4

Stock price (dilution)

$1 share

+

0.01

0

* Less than 0.5¢ or $500,000 a Reflect 2011 sales forecast

. . . . partly mitigated.

18

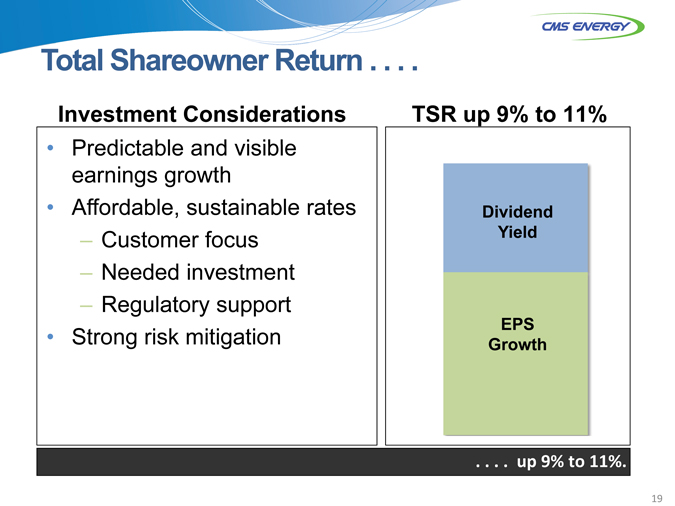

Total Shareowner Return . . . .

Investment Considerations

TSR up 9% to 11%

• Predictable and visible earnings growth

• Affordable, sustainable rates

– Customer focus

– Needed investment

– Regulatory support

• Strong risk mitigation

Dividend Yield

EPS Growth

. . . . upp 9% to 11%.

19

APPENDIX

|

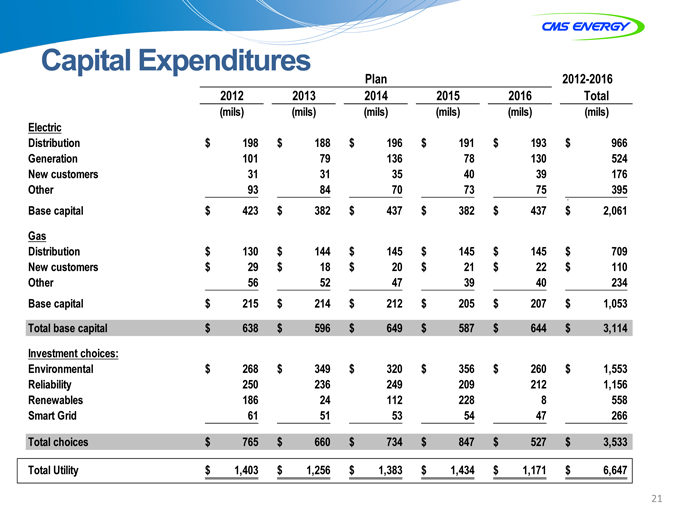

Capital Expenditures

Plan

2012-2016

2012

2013

2014

2015

2016

Total

(mils)

(mils)

(mils)

(mils)

(mils)

(mils)

Electric

Distribution

$198

$188

$196

$191

$193

$966

Generation

101

79

136

78

130

524

New customers

31

31

35

40

39

176

Other

93

84

70

73

75

$395

Base capital

$423

$382

$437

$382

$437

$2,061

Gas

Distribution

$130

$144

$145

$145

$145

$709

New customers

$29

$18

$20

$21

$22

$110

Other

56

52

47

39

40

234

Base capital

$215

$214

$212

$205

$207

$1,053

Total base capital

$638

$596

$649

$587

$644

$3,114

Investment choices:

Environmental

$268

$349

$320

$356

$260

$1,553

Reliability

250

236

249

209

212

1,156

Renewables

186

24

112

228

8

558

Smart Grid

61

51

53

54

47

266

Total choices

$765

$660

$734

$847

$527

$3,533

Total Utility

$1,403

$1,256

$1,383

$1,434

$1,171

$6,647

21

GAAP RECONCILIATION

CMS ENERGY CORPORATION

Earnings Per Share By Year GAAP Reconciliation

(Unaudited)

| 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | ||||||||||||||||||||||||||||

| Reported earnings (loss) per share - GAAP |

$ | (0.30 | ) | $ | 0.64 | $ | (0.44 | ) | $ | (0.41 | ) | $ | (1.02 | ) | $ | 1.20 | $ | 0.91 | $ | 1.28 | $ | 1.58 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| After-tax items: |

||||||||||||||||||||||||||||||||||||

| Electric and gas utility |

0.21 | (0.39 | ) | — | — | (0.07 | ) | 0.05 | 0.33 | 0.03 | 0.00 | |||||||||||||||||||||||||

| Enterprises |

0.74 | 0.62 | 0.04 | (0.02 | ) | 1.25 | (0.02 | ) | 0.09 | (0.03 | ) | (0.11 | ) | |||||||||||||||||||||||

| Corporate interest and other |

0.16 | (0.03 | ) | 0.04 | 0.27 | (0.32 | ) | (0.02 | ) | 0.01 | * | (0.01 | ) | |||||||||||||||||||||||

| Discontinued operations (income) loss |

(0.16 | ) | 0.02 | (0.07 | ) | (0.03 | ) | 0.40 | (* | ) | (0.08 | ) | 0.08 | (0.01 | ) | |||||||||||||||||||||

| Asset impairment charges, net |

— | — | 1.82 | 0.76 | 0.60 | — | — | — | — | |||||||||||||||||||||||||||

| Cumulative accounting changes |

0.16 | 0.01 | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Adjusted earnings per share, including MTM - non-GAAP |

$ | 0.81 | $ | 0.87 | $ | 1.39 | $ | 0.57 | $ | 0.84 | $ | 1.21 | (a) | $ | 1.26 | $ | 1.36 | $ | 1.45 | |||||||||||||||||

| Mark-to-market impacts |

0.03 | (0.43 | ) | 0.51 | ||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Adjusted earnings per share, excluding MTM - non-GAAP |

NA | $ | 0.90 | $ | 0.96 | $ | 1.08 | NA | NA | NA | NA | NA | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| * | Less than $500 thousand or $0.01 per share. |

| (a) | $1.25 excluding discontinued Exeter operations and accounting changes related to convertible debt and restricted stock. |

CMS Energy

Reconciliation of Gross Operating Cash Flow to GAAP Operating Activities

(unaudited)

(mils)

| 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | |||||||||||||||||||||||||

| Consumers Operating Income + Depreciation & Amortization |

$ | 1,248 | $ | 1,498 | $ | 1,527 | $ | 1,645 | $ | 1,735 | $ | 1,860 | $ | 1,976 | $ | 2,051 | ||||||||||||||||

| Enterprises Project Cash Flows |

16 | 39 | 24 | 25 | 27 | 33 | 35 | 35 | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Gross Operating Cash Flow |

$ | 1,264 | $ | 1,537 | $ | 1,551 | $ | 1,670 | $ | 1,762 | $ | 1,893 | $ | 2,011 | $ | 2,086 | ||||||||||||||||

| Other operating activities including taxes, interest payments and working capital |

(416 | ) | (578 | ) | (382 | ) | (420 | ) | (412 | ) | (443 | ) | (756 | ) | (776 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Net cash provided by operating activities |

$ | 848 | $ | 959 | $ | 1,169 | $ | 1,250 | $ | 1,350 | $ | 1,450 | $ | 1,255 | $ | 1,310 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||