Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - AstroNova, Inc. | Financial_Report.xls |

| EX-21 - LIST OF SUBSIDIARIES OF THE COMPANY - AstroNova, Inc. | d272581dex21.htm |

| EX-10.8 - NON-EMPLOYEE DIRECTORS COMPENSATION PROGRAM - AstroNova, Inc. | d272581dex108.htm |

| EX-31.1 - CERTIFICATION OF CHIEF EXECUTIVE OFFICER PURSUANT TO SECTION 302 - AstroNova, Inc. | d272581dex311.htm |

| EX-31.2 - CERTIFICATION OF CHIEF FINANCIAL OFFICER PURSUANT TO SECTION 302 - AstroNova, Inc. | d272581dex312.htm |

| EX-32.1 - CERTIFICATION OF CHIEF EXECUTIVE OFFICER PURSUANT TO 18 U.S.C. SECTION 1350 - AstroNova, Inc. | d272581dex321.htm |

| EX-23.1 - CONSENT OF ERNST & YOUNG LLP - AstroNova, Inc. | d272581dex231.htm |

| EX-32.2 - CERTIFICATION OF CHIEF FINANCIAL OFFICER PURSUANT TO 18 U.S.C. SECTION 1350 - AstroNova, Inc. | d272581dex322.htm |

Table of Contents

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended January 31, 2012

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 0-13200

Astro-Med, Inc.

(Exact name of registrant as specified in its charter)

| Rhode Island | 05-0318215 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 600 East Greenwich Avenue, West Warwick, Rhode Island |

02893 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (401) 828-4000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| None | None |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $.05 Par Value

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by checkmark if disclosure of delinquent filers pursuant to Item 405 of regulation S-K is not contained herein, and will not be contained. To the best of the Registrant’s knowledge, in definitive proxy or information statement incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company x | |||

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): Yes ¨ No x

The aggregate market value of the registrant’s voting common equity held by non-affiliates at July 29, 2011 was approximately $43,368,741 based on the closing price on the Nasdaq Global Market on that date.

As of March 30, 2012 there were 7,427,773 shares of Common Stock (par value $0.05 per share) of the registrant outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company’s definitive Proxy Statement for the 2012 Annual Meeting of Shareholders are incorporated by reference into Part III of this Annual Report on Form 10-K where indicated.

Table of Contents

ASTRO-MED, INC.

FORM 10-K ANNUAL REPORT

| Page | ||||

| PART I | ||||

| Item 1. | 3-6 | |||

| Item 1A. | 6-10 | |||

| Item 1B. | 10 | |||

| Item 2. | 11 | |||

| Item 3. | 11 | |||

| Item 4. | 11 | |||

| PART II | ||||

| Item 5. | 12-14 | |||

| Item 6. | 14 | |||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

14-21 | ||

| Item 7A. | 21 | |||

| Item 8. | 22 | |||

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

22 | ||

| Item 9A. | 22-23 | |||

| Item 9B. | 23 | |||

| PART III | ||||

| Item 10. | 24-25 | |||

| Item 11. | 25 | |||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholders Matters |

25-26 | ||

| Item 13. | Certain Relationships, Related Transactions and Director Independence |

26 | ||

| Item 14. | 26 | |||

| PART IV | ||||

| Item 15. | 27 | |||

2

Table of Contents

ASTRO-MED, INC.

Forward-Looking Statements

Information included in this Annual Report on Form 10-K may contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are not statements of historical fact, but rather reflect our current expectations concerning future events and results. We generally use the words “believes,” “expects,” “intends,” “plans,” “anticipates,” “likely,” “continues,” “may,” “will,” and similar expressions to identify forward-looking statements. Such forward-looking statements, including those concerning our expectations, involve risks, uncertainties and other factors, some of which are beyond our control, which may cause our actual results, performance or achievements to be materially different from those expressed or implied by such forward-looking statements. These risks, uncertainties and factors include, but are not limited to, those factors set forth in this Annual Report on Form 10-K under “Item 1A. Risk Factors.” We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. The reader is cautioned not to unduly rely on such forward-looking statements when evaluating the information presented in this Annual Report on Form 10-K.

PART I

General

Unless otherwise indicated, references to “Astro-Med,” the “Company,” “we,” “our,” and “us” in this Annual Report on Form 10-K refer to Astro-Med, Inc. and its consolidated subsidiaries.

Astro-Med, Inc. designs, develops, manufactures and distributes a broad range of specialty printers and data acquisition and analysis systems, including both hardware and software, which incorporate advanced technologies in order to acquire, store, analyze, and present data in multiple formats. Target markets for hardware and software products of the Company include aerospace, apparel, automotive, avionics, chemicals, computer peripherals, communications, distribution, food and beverage, general manufacturing, life sciences, packaging and transportation.

The Company’s products are distributed through its own sales force and authorized dealers in the United States. We sell to customers outside of the United States primarily by using authorized dealers and international sales representatives, who are managed from our foreign branch offices. Approximately 30% of the Company’s sales in fiscal 2012 were to customers located outside the United States.

Astro-Med operates its business through three operating segments, Astro-Med Test & Measurement (T&M), QuickLabel Systems (QuickLabel) and Grass Technologies (Grass). Financial information by business segment and geographic area appears in Note 10 to the Consolidated Financial Statements of this Annual Report on Form 10-K. The following description of our business should be read in conjunction with “Management’s Discussion and Analysis of Financial Conditions and Results of Operations” on pages 14 through 18 of this Annual Report on Form 10-K.

Description of Business

Product Overview

Astro-Med, Inc. develops and manufactures specialty printers and data acquisition systems. The Company’s products sell under the brand names Astro-Med® Test & Measurement (T&M), Grass® Technologies (Grass®), and QuickLabel® Systems (QuickLabel®).

Products sold under the Astro-Med T&M brand acquire and record data and print the output onto charts or electronic media. Products sold under the Grass® brand electronically capture and record neurological data that is

3

Table of Contents

used to analyze and diagnose disorders such as epilepsy and sleep apnea. Products sold under the QuickLabel® brand digitally print custom labels used in product packaging and automatic identification applications.

The Company supplies a range of products and services that include hardware, software and consumables to customers who are in a variety of industries.

Astro-Med Test & Measurement products include the Dash® MX portable data acquisition system, TMX™ high-speed data acquisition system, ToughWriter® ruggedized cockpit printers, ToughSwitch® Ethernet switches, Dash® series data recorders, and Everest® telemetry recorders.

ToughWriter® ruggedized cockpit printers are used in the flight deck and in the cabins of military and commercial aircraft to print hard copies of landing strips, flight itineraries, weather maps, gate information, and ground communications. ToughSwitch® Ethernet switches are used in commercial and military aircraft and military vehicles to connect multiple computers or Ethernet devices together. These products are ruggedized to comply with rigorous military and commercial flightworthiness standards for operation under extreme environmental conditions. The Company is currently furnishing ToughWriter® cockpit printers for several airplanes made by Airbus, Boeing, Bombardier, and Lockheed.

The Company’s family of portable data recorders are used as maintenance and troubleshooting instruments in pulp and paper mills, metal mills, power generating plants, automotive R&D centers, manufacturing plants, and for aerospace applications. The TMX™ data acquisition system is designed for data capture of long-term testing in automotive, aerospace, and other industrial applications where the ability to monitor high channel counts, and accept and view a wide variety of input signals, including time-stamped and synchronized video capture data and audio notation, is important.

Everest® telemetry recorders are used widely in the aerospace industry to monitor and track space vehicles, aircraft, missiles and other systems in flight.

Products sold under the Grass® brand include neurophysiological recording instruments, software, stimulators, electrode preps, consumable products, and Grass’ industry-renowned electrodes. Grass® equipment detects and amplifies neurophysiological signals for acquisition, review, and analysis via special Grass® software.

Grass® clinical equipment is primarily sold into the Sleep Disorders (PSG), Routine/Ambulatory EEG, and Long-Term Epilepsy Monitoring (LTM) diagnostic markets, and is sold to hospitals, free-standing clinics, and private physicians’ offices. Current Grass® clinical products include the FDA-listed Grass® S12X Cortical Stimulator for stimulation mapping to aid in cortical resection procedures, the TREA® ambulatory EEG recorder, the SleepTrek®3 at-home sleep screener, the Comet-Plus® for routine and expanded PSG/EEG studies and TWin® Neurotrac-III Neuromonitoring Software for computing and displaying long-term trends during continuous EEG monitoring in the ICU, NICU, OR, and Seizure Monitoring units.

Grass® research products consist of square pulse stimulators, including the S88X dual-output with digital controls model and the SD9 student research model, as well as amplifiers, including the LP511 high performance AC model and P122 AC/DC Strain Gage model as well as the 15LT Amplifier System. Customers of the Grass® research line are typically university research centers or pharmaceutical companies engaged in drug research. The Grass® consumable products are comprised predominantly of precious metal recording electrodes as well as sensing devices used to collect physiological data and are utilized with the systems described above.

Products sold under the QuickLabel® brand include digital color label printers developed for in-house label printing and software, label and tag substrates, label printing inks including thermal transfer ribbons, toners, custom label printing services, and a range of printer accessories. The breadth of the product line allows QuickLabel sales and support staff to serve customers at virtually every level of their label printing needs.

With its broad range of entry-level, mid-range, and high-performance digital label printers, QuickLabel Systems is able to provide its customers a continuous path to upgrade to new labeling products. QuickLabel® products are primarily sold to end-user manufacturers, processors, and retailers who label products on a

4

Table of Contents

just-in-time basis. Users can benefit from the time and cost-savings of digitally printing their own labels on-demand. Industries that commonly benefit from short-run label printing include apparel, chemicals, cosmetics, food and beverage, medical products, and pharmaceuticals, among many other packaged goods.

Current QuickLabel® models include the Vivo!® Touch, a patented electrophotographic color label printer developed to print full-color variable information labels in an office or factory; the Zeo!®, an entry-level inkjet label printer developed in partnership with Hewlett-Packard; and the Xe series of digital color label printers utilizing thermal transfer technology. The Xe Series of label printers are unique in the industry in that they can be directly integrated with automated production lines and represent a novel, patented application of multi-color thermal transfer technology. QuickLabel also sells and supports its Pronto!® family of barcode printers which utilize single color-thermal transfer label printing technology.

Technology

The core technologies of Astro-Med relate to (1) acquiring data, (2) conditioning the data, (3) displaying the data on hard copy, monitor or electronic storage media, and (4) analyzing the data.

Patents and Copyrights

Astro-Med holds a number of product patents in the United States and in foreign countries. The Company copyrights its software and registers its brand trademarks. While we consider our patents to be important to the operation of our business, we do not believe that any existing patent, license, trademark or other intellectual property right is of such importance that its loss or termination would have a material adverse effect on the Company’s business taken as a whole.

Manufacturing and Supplies

Astro-Med designs its products and manufactures many of the component parts. The balance of the parts required for manufacture of our products are produced to our specifications by suppliers. Raw materials required for the manufacture of products, including parts produced to our specifications, are generally available from numerous suppliers. However, we do obtain certain components of our products and certain finished products from sole sources.

Product Development

Astro-Med maintains an active program of product research and development. During fiscal 2012 and 2011, we spent $5,243,000 and $5,020,000, respectively, on Company-sponsored product development. We are committed to continuous product development as a requisite to our organic growth and expect to continue our focus on research and development efforts in fiscal 2013 and beyond.

Marketing and Competition

The Company competes worldwide in many markets including clinical and research diagnostics, specialty printing systems, and data acquisition and analysis. We retain a competitive position in our respective markets by virtue of proprietary technology, product reputation, delivery, technical assistance, and service to customers. We market our products worldwide by advertising and promotion using major national and international trade journals, scientific meetings, trade shows, direct mailing campaigns, and the internet.

Our products are sold by direct field sales persons as well as independent dealers and representatives. In the United States, the Company has factory-trained direct field sales people located in major cities from coast to coast specializing in either Astro-Med® T&M products, QuickLabel® products, or Grass® Technologies products. Additionally, we have direct field sales and service centers in Canada, France, Germany and the United

5

Table of Contents

Kingdom staffed by our own employees. In the rest of the world, Astro-Med utilizes approximately 90 independent dealers and representatives selling and marketing our products in 70 countries.

Astro-Med has a number of competitors in each of the markets that it serves. In the T&M area, we believe that we are one of the leaders in data acquisition systems. In the digital color label printing field, we believe we lead the world in portable bench-top color label printing technology, and we were the first to market an electrophotographic color label printer capable of printing on continuous rollstock.

Our Grass Technologies products are devoted to clinical applications in electroencephalography (EEG), polysomnography (PSG), and Long Term Epilepsy Monitoring (LTM). There are approximately ten companies that compete in one or more of the three modalities (EEG, PSG, LTM), but none are the clear leader. We believe we offer superior products based upon our long history and pioneering efforts in the field since 1935. Additionally, we produce a range of life science products for the research market many of which eventually find their way into clinical applications.

No single customer accounted for 10% or more of our net sales in any of the last two fiscal years.

International Sales

In fiscal 2012 and 2011, net sales to customers in various geographic areas outside the United States, primarily in Canada and Western Europe, amounted to $24,189,000 and $20,402,000, respectively.

Order Backlog

Astro-Med’s backlog fluctuates regularly. It consists of a blend of orders for end user customers as well as original equipment manufacturer customers. Manufacturing is geared to forecasted demands and applies a rapid turn cycle to meet customer expectations. Accordingly, the amount of order backlog may not indicate future sales trends. Backlog at January 31, 2012 and 2011 was $6,220,000 and $7,114,000, respectively.

Employees

As of January 31, 2012, Astro-Med employed 372 people. We are generally able to satisfy our employment requirements. No employees are represented by a union. We believe that employee relations are good.

Other Information

The Company’s business is not seasonal in nature. However, our sales are impacted by the size of certain individual transactions, which can cause fluctuations in sales from quarter to quarter.

Available Information

We make available on our website (www.astro-medinc.com) the Company’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and, if applicable, amendments to those reports filed or furnished pursuant to Sections 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after the Company electronically files such material with, or furnishes it to, the Securities Exchange Commission. These filings are also accessible on the SEC’s website at http://www.sec.gov.

The following risk factors should be carefully considered in evaluating Astro-Med because such factors may have a significant impact on our business, operating results, liquidity and financial condition. As a result of the

6

Table of Contents

risk factors set forth below, actual results could differ materially from those projected in any forward-looking statements. Additional risks and uncertainties not presently known to us, or that we currently consider to be immaterial, may also impact our business operations.

Depressed general economic conditions, financial market disruptions, and uncertainties in the global credit and equity markets may adversely affect Astro-Med’s results of operation and financial position.

Our business is sensitive to changes in general economic conditions, both inside and outside the United States. As widely reported, financial markets throughout the world have experienced extreme disruption since 2008, including historically high volatility in securities prices, severely diminished liquidity and credit availability, rating downgrades of certain investments and declining value of others, failure of major financial institutions and unprecedented government support of financial institutions and corporations. Recurrence of these developments and a related economic downturn may adversely impact our business resulting in:

| • | Reduced demand for our products realized by diminished new orders and increases in order cancellations; |

| • | Increased risk of excess and obsolete inventories; |

| • | Increased pressure on the prices for our products and services; |

| • | Greater difficulty in collecting accounts receivables; |

| • | Greater risk of impairment to the value and liquidity of our investment portfolio: and |

| • | Greater risk that cost reduction actions may be necessary resulting in restructuring charges |

Astro-Med’s operating results and financial condition could be harmed if the markets into which we sell our product decline or do not grow as anticipated.

Any decline in our customers’ markets or in their general economic conditions, including declines related to the market disruptions as described above, would likely result in a reduction in demand for our products. For example, although we have experienced measured progress in fiscal 2012 and 2011, as sales have increased from prior years, we are still affected by the continued global economic downturn as some of our customers remain reluctant to make capital equipment purchases and are limiting consumable product purchases to quantities necessary to satisfy immediate needs with no provisions to stock supplies for future use. Also, if our customers’ markets decline, we may not be able to collect on outstanding amounts due to us. Such declines could harm our results of operations, financial position and cash flows and could limit our ability to continue to remain profitable.

Astro-Med’s future revenue growth depends on our ability to introduce new products and services on a timely basis and achieve market acceptance of these new products and services.

The markets for our products are characterized by rapidly changing technology and accelerating product introduction cycles. Our future success depends largely upon our ability to address the rapidly changing needs of our customers by developing and supplying high-quality, cost-effective products, product enhancements and services on a timely basis and by keeping pace with technological developments and emerging industry standards. The success of our new products will also depend on our ability to differentiate our offerings from our competitors’ offerings; price our products competitively; anticipate our competitor’s development of new products; and maintain high levels of product quality and reliability. Astro-Med spends a significant amount of time and effort related to the development of our Ruggedized and Color Printer products as well as our Test and Measurement products. Failure to further develop any of our new products and their related markets as anticipated could adversely affect our future revenue growth and operating results.

Astro-Med faces significant competition and our failure to compete successfully could adversely affect our results of operations and financial condition.

We operate in an environment of significant competition, driven by rapid technological advances, evolving industry standards, frequent new product introductions and the demands of customers to become more efficient.

7

Table of Contents

Our competitors range from large international companies to relatively small firms. We compete primarily on the basis of technology, performance, price, quality, reliability, brand, distribution and customer service and support. Our success in future performance is largely dependent upon our ability to compete successfully in the markets we currently serve and to expand into additional market segments. Additionally, current competitors or new market entrants may develop new products with features that could adversely affect the competitive position of our products. To remain competitive, we must develop new products, services and applications and periodically enhance our existing offerings. If we are unable to compete successfully, we could lose market share and important customers to our competitors which could materially adversely affect our results of operations and financial position.

Astro-Med is dependent upon contract manufacturers for some of our products. If these manufacturers do not meet our requirements, either in volume or quality, then we could be materially harmed.

During fiscal 2012, we subcontracted the manufacturing and assembly of certain of our products to an independent third party at facilities located in various countries. Relying on subcontractors involves a number of significant risks, including:

| • | Loss of control over the manufacturing process; |

| • | Potential absence of adequate production capacity; |

| • | Potential delays in production lead times; |

| • | Unavailability of certain process technologies; and |

| • | Reduced control over delivery schedules, manufacturing yields, quality and costs. |

If our significant subcontractor becomes unable or unwilling to continue to manufacture these products in required volumes, we will have to identify qualified alternate subcontractors or we will take over the manufacturing ourselves in as much as we own the designs, drawings, and bills of material for all our products. Additional qualified subcontractors may not be available, or may not be available on a timely or cost competitive basis. Any interruption in the supply of, or increase in the cost of, the products manufactured by third party subcontractors could have a material adverse effect on our business, operating results and financial condition.

For certain components and assembled products, Astro-Med is dependent upon single or limited source suppliers. If these suppliers do not meet demand, either in volume or quality, then we could be materially harmed.

If the supply of a key component or assembled products were to be delayed or curtailed or, in the event a key manufacturing or sole vendor delays shipment of such components or completed products, our ability to ship products in desired quantities and in a timely manner would be adversely affected. Our business, results of operations and financial position could also be adversely affected, depending on the time required to obtain sufficient quantities from the original source or, if possible, to identify and obtain sufficient quantities from an alternative source. Additionally, if any single or limited source supplier becomes unable or unwilling to continue to supply these components or assembled products in required volumes, we will have to identify and qualify acceptable replacements or redesign our products with different components. Alternative sources may not be available, or product redesign may not be feasible on a timely basis. Any interruption in the supply of or increase in the cost of the components and assembled products provided by single or limited source suppliers could have a material adverse effect on our business, operating results and financial condition.

Economic, political and other risks associated with international sales and operations could adversely affect Astro-Med’s results of operations and financial position.

Because we sell our products worldwide, our business is subject to risks associated with doing business internationally. Revenue from international operations, which includes both direct and indirect sales to customers outside the U.S. accounted for approximately 30% of our total revenue for fiscal year 2012 and we anticipate that international sales will continue to account for a significant portion of our revenue. In addition, many of our

8

Table of Contents

employees, suppliers, job functions and facilities are located outside the U.S. Accordingly, our future results could be harmed by a variety of factors, including:

| • | Interruption to transportation flows for delivery of parts to us and finished goods to our customers; |

| • | Customer and vendor financial stability; |

| • | Changes in foreign currency exchange rates; |

| • | Changes in a specific country’s or region’s environment including political, economic, monetary, regulatory or other conditions; |

| • | Trade protection measures and import or export licensing requirements; |

| • | Negative consequences from changes in tax laws; |

| • | Difficulty in managing and overseeing operations that are distant and remote from corporate headquarters; |

| • | Difficulty in obtaining and maintaining adequate staffing; |

| • | Differing labor regulations; |

| • | Differing protection of intellectual property; |

| • | Unexpected changes in regulatory requirements; and |

| • | Geopolitical turmoil, including terrorism and war. |

Astro-Med’s profitability is dependent upon our ability to obtain adequate pricing for our products and to improve our cost structure.

Our success depends on our ability to obtain adequate pricing for our products and services which provides a reasonable return to our shareholders. Depending on competitive market factors, future prices we obtain for our products and services may decline from previous levels. In addition, pricing actions to offset the effect of currency devaluations may not prove sufficient to offset further devaluations or may not hold in the face of customer resistance and/or competition. If we are unable to obtain adequate pricing for our products and services, our results of operations and financial position could be materially adversely affected.

We are continually reviewing our operations with a view towards reducing our cost structure, including but not limited to downsizing our employee base, exiting certain businesses, improving process and system efficiencies and outsourcing some internal functions. From time to time we also engage in restructuring actions to reduce our cost structure. If we are unable to maintain our cost base at or below the current level and maintain process and systems changes resulting from cost reduction and prior restructuring actions, our results of operations and financial position could be materially adversely affected.

Astro-Med could incur liabilities as a result of installed product failures due to design or manufacturing defects.

Astro-Med could incur liabilities as a result of installed product failures due to design or manufacturing defects. Our products may have defects despite testing internally or by current or potential customers. These defects could result in among other things, a delay in recognition of sales, loss of sales, loss of market share, failure to achieve market acceptance or substantial damage to our reputation. We could be subject to material claims by customers, and may need to incur substantial expenses to correct any product defects.

Astro-Med is subject to laws and regulations; failure to address or comply with these laws and regulations could harm our business and adversely affect our results of operations.

Our operations are subject to laws, rules, regulations, including environmental regulations, government policies and other requirements in each of the jurisdictions in which we conduct business. Changes in laws, rules, regulations, policies or requirements could result in the need to modify our products and could affect the demand

9

Table of Contents

for our products, which may have an adverse impact on our future operating results. In addition, we must comply with new regulations restricting our ability to include lead and certain other substances in our products. If we do not comply with applicable laws, rules and regulations we could be subject to costs and liabilities and our business may be adversely impacted.

A number of our products from our Grass Technologies product group are subject to regulation by the United States Food and Drug Administration (“FDA”) and certain similar foreign regulatory agencies. If we or any of our suppliers or distributors fail to comply with FDA and other applicable regulatory requirements or are perceived potentially to have failed to comply, we may face, among other things, adverse publicity affecting both us and our customers; investigations or notices of non-compliance; fines, injunctions and civil penalties; partial suspensions or total shutdown of production facilities or the imposition of operating restrictions; increased difficulty in obtaining required FDA clearances or approvals; seizures or recalls of our products or those of our customers, and/or the inability to sell our products.

Adverse conditions in the global banking industry and credit markets may adversely impact the value of our investments or impair our liquidity.

At the end of fiscal 2012, we had cash and cash equivalents of approximately $11.7 million invested or held in a mix of money market funds and bank demand deposit accounts. The continued disruptions in the financial markets may, in some cases, result in an inability to access assets such as money market funds that traditionally have been viewed as highly liquid. Any failure of our counterpart financial institutions or funds in which we have invested may adversely impact our cash and cash equivalent positions and, in turn, our results of operations and financial position. As of January 31, 2012, we also had an approximate $11.3 million portfolio of securities available for sale. This portfolio consists of state and municipal securities with various maturity dates, all of which have a credit rating of AA or above at the original purchase date; however, failure of any of these securities may result in an adverse impact on our portfolio.

Astro-Med may not be able to effectively integrate businesses or assets acquired.

We may identify and pursue acquisitions of complementary companies and strategic assets, such as customer bases, products and technology. However, there can be no assurance that we will be able to identify suitable acquisition opportunities. In any acquisition that we complete we cannot be certain that:

| • | We will successfully integrate the operations of the acquired business with our own; |

| • | All the benefits expected from such integration will be realized; |

| • | Management’s attention will not be diverted or divided, to the detriment of current operations; |

| • | Amortization of acquired intangible assets will not have a negative effect on operating results or other aspects of our business; |

| • | Delays or unexpected costs related to the acquisition will not have a detrimental effect on our business, operating results and financial condition; |

| • | Customer dissatisfaction with, or performance problems at, an acquired company will not have an adverse effect on our reputation; and |

| • | Respective operations, management and personnel will be compatible. |

In certain instances as permitted by applicable law and NASDAQ rules, acquisitions may be consummated without seeking and obtaining shareholder approval, in which case shareholders will not have an opportunity to consider and vote upon the merits of such an acquisition. Although we will endeavor to evaluate the risks inherent in a particular acquisition, there can be no assurance that we will properly ascertain or assess such risks.

Item 1B. Unresolved Staff Comments

None

10

Table of Contents

The following table sets forth information regarding the Company’s principal owned properties, all of which are included in the consolidated balance sheet appearing elsewhere in this report.

| Location |

Approximate Square Footage |

Principal Use | ||||

| West Warwick, Rhode Island, USA |

135,500 | Corporate headquarters, research and development, manufacturing, sales and service | ||||

| Rockland, Massachusetts, USA | 36,000 | Manufacturing | ||||

| Slough, England | 1,700 | Sales and service | ||||

Astro-Med also leases facilities in various other locations. The following information pertains to each location:

| Location |

Approximate Square Footage |

Principal Use | ||||

| Rodgau, Germany |

8,300 | Manufacturing, sales and service | ||||

| Brossard, Quebec, Canada |

7,900 | Manufacturing, sales and service | ||||

| Trappes, France |

2,164 | Sales and service | ||||

| Schaumburg, Illinois, USA | 630 | Sales | ||||

| El Dorado Hills, California, USA | 273 | Sales | ||||

| Newport Beach, California, USA | 151 | Sales | ||||

We believe our facilities are well maintained, in good operating condition and generally adequate to meet our needs for the foreseeable future.

There are no pending or threatened legal proceedings against the Company believed to be material to the financial position or results of operations of the Company.

Item 4. Mine Safety Disclosures

Not applicable.

11

Table of Contents

PART II

| Item 5. | Market for the Registrant’s Common Stock, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Astro-Med’s common stock trades on The NASDAQ Global Market under the symbol “ALOT.” The following table sets forth the range of high and low closing prices and dividend data, as furnished by NASDAQ, for the years ended January 31:

| High | Low | Dividends Per Share |

||||||||||

| 2012 |

||||||||||||

| First Quarter |

$ | 8.07 | $ | 7.48 | $ | 0.07 | ||||||

| Second Quarter |

$ | 9.00 | $ | 7.64 | $ | 0.07 | ||||||

| Third Quarter |

$ | 8.18 | $ | 6.94 | $ | 0.07 | ||||||

| Fourth Quarter |

$ | 8.15 | $ | 7.07 | $ | 0.07 | ||||||

| 2011 |

||||||||||||

| First Quarter |

$ | 8.05 | $ | 7.31 | $ | 0.07 | ||||||

| Second Quarter |

$ | 7.75 | $ | 6.93 | $ | 0.07 | ||||||

| Third Quarter |

$ | 7.49 | $ | 6.60 | $ | 0.07 | ||||||

| Fourth Quarter |

$ | 7.95 | $ | 6.90 | $ | 0.07 | ||||||

Astro-Med had approximately 301 shareholders of record as of March 23, 2012, which does not reflect shareholders with beneficial ownership in shares held in nominee name.

12

Table of Contents

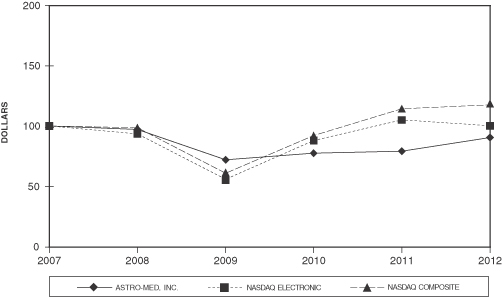

Stock Performance Graph

The graph below shows a comparison of the cumulative total return on the Company’s common stock against the cumulative total returns for the NASDAQ Composite Index and the NASDAQ Electronic Index for the period of five fiscal years ended January 31, 2012. The NASDAQ Composite Index is calculated using all companies trading on the NASDAQ Global Select, NASDAQ Global Market and the NASDAQ Capital Markets through January 31, 2012. The Index is weighted by the current shares outstanding and assumes dividends reinvested. The NASDAQ Electronic Index, designated as the Company’s peer group index, is comprised of companies classified as electronic equipment manufacturers.

| Cumulative Total Returns* | ||||||||||||||||||||||||

| 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | |||||||||||||||||||

| Astro-Med, Inc. |

$ | 100.00 | $ | 95.12 | $ | 70.21 | $ | 75.74 | $ | 78.66 | $ | 90.58 | ||||||||||||

| NASDAQ Electronic Index |

$ | 100.00 | $ | 94.71 | $ | 56.56 | $ | 87.78 | $ | 104.98 | $ | 100.59 | ||||||||||||

| NASDAQ Composite Index |

$ | 100.00 | $ | 97.62 | $ | 60.84 | $ | 89.31 | $ | 113.69 | $ | 119.63 | ||||||||||||

| * | Assumes $100 invested on February 1, 2007 with reinvestment of dividends |

Dividend Policy

Astro-Med began a program of paying quarterly cash dividends in fiscal 1992 and has paid a dividend for 82 consecutive quarters. During fiscal 2012, we paid a quarterly dividend of $0.07 per share. We anticipate that we will continue to pay comparable cash dividends on a quarterly basis.

Stock Repurchases

On August 22, 2011, Astro-Med’s Board of Directors approved an increase in the number of shares authorized for repurchase from 254,089 to 500,000 shares of common stock. This is an ongoing authorization without any expiration date.

13

Table of Contents

During the fourth quarter of fiscal 2012, the Company made the following repurchases of its common stock:

| Total Number of Shares Repurchased |

Average Price paid Per Share |

Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs |

Maximum Number of Shares That May Be Purchased Under The Plans or Programs |

|||||||||||||

| October 30 – November 26 |

— | — | — | 500,000 | ||||||||||||

| November 27 – December 24 |

— | (a)(b) | — | — | 500,000 | |||||||||||

| December 25 – January 31 |

— | (c) | — | — | 500,000 | |||||||||||

| (a) | On November 29, 2011, the Company’s Chief Executive Officer delivered 7,893 shares of the Company’s common stock to satisfy the exercise price for 14,300 stock options exercised. The shares delivered were valued at $7.99 per share and are included with treasury stock in the consolidated balance sheet. This transaction did not impact the number of shares authorized for repurchase under the Company’s current repurchase program. |

| (b) | On November 29, 2011, the Company’s Vice President and Chief Technology Officer delivered 2,547 shares of the Company’s common stock to satisfy the exercise price for 7,562 stock options exercised. The shares delivered were valued at $7.99 per share and are included with treasury stock in the consolidated balance sheet. This transaction did not impact the number of shares authorized for repurchase under the Company’s current repurchase program. |

| (c) | On January 6, 2012, the Company’s Marketing Manager delivered 716 shares of the Company’s common stock to satisfy the exercise price for 2,062 stock options exercised. The shares delivered were valued at $7.76 per share and are included with treasury stock in the consolidated balance sheet. This transaction did not impact the number of shares authorized for repurchase under the Company’s current repurchase program. |

Item 6. Selected Financial Data

We are a “smaller reporting company” and, as such, are not required to provide this information.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Overview

Astro-Med is a multi-national enterprise, which designs, develops, manufactures, distributes and services a broad range of products that acquire, store, analyze and present data in multiple formats. The Company organizes its structure around a core set of competencies, including research and development, manufacturing, service, marketing and distribution. It markets and sells its products and services through the following three sales product groups:

| • | Test and Measurement Product Group (T&M)—offers a suite of Ruggedized Printer products designed for military and commercial applications to be used in the avionics industry to print weather maps, communications and other critical flight information. T&M also comprises a suite of telemetry recorder products sold to the aerospace and defense industries, as well as portable data acquisition recorders, which offer diagnostic and test functions to a wide range of manufacturers including automotive, energy, paper and steel fabrication. |

| • | QuickLabel Systems Product Group (QuickLabel)—offers label printer hardware, labeling software, servicing contracts, and label and ink consumable products that digitally print color labels on a broad range of label and tag substrates. |

| • | Grass Technologies Product Group (Grass)—offers monitoring and diagnostic instrumentation that serves the clinical and research neurophysiology and life sciences markets, as well as a range of consumable supplies. |

14

Table of Contents

Astro-Med markets and sells its products and services globally through a diverse distribution structure of direct sales personnel, manufacturer’s representatives and authorized dealers that deliver a full complement of branded products and services to customers in our respective markets.

Our growth strategy centers on organic growth through product innovation made possible by research and development initiatives, as well as strategic acquisitions that fit into existing core businesses. Research and development activities are funded and expensed by the Company at approximately 6.6% of annual sales for fiscal 2012. We also continue to invest in sales and marketing initiatives by expanding the existing sales force and using various marketing campaigns to achieve our goals of sales growth and increased profitability notwithstanding today’s challenging economic environment.

Results of Operations

| ($ in thousands) | 2012 | 2011 | ||||||||||||||||||

| Net Sales |

As a % of Total Net Sales |

% Change Over Prior Year |

Net Sales |

As a % of Total Net Sales |

||||||||||||||||

| T&M |

$ | 17,138 | 21.7 | % | 15.5 | % | $ | 14,837 | 20.9 | % | ||||||||||

| QuickLabel |

43,586 | 55.0 | % | 10.3 | % | 39,500 | 55.6 | % | ||||||||||||

| Grass |

18,469 | 23.3 | % | 10.7 | % | 16,679 | 23.5 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total |

$ | 79,193 | 100.0 | % | 11.5 | % | $ | 71,016 | 100.0 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Fiscal 2012 compared to Fiscal 2011

Astro-Med’s sales in fiscal 2012 were $79,193,000, representing an 11.5% increase as compared to prior year sales of $71,016,000. Domestic sales of $55,004,000 increased 8.7% from the prior year sales of $50,614,000. International sales of $24,189,000 includes a favorable impact of $705,000 due to foreign exchange rates and reflects an 18.6% increase as compared to the prior year.

Hardware sales in fiscal 2012 were $34,767,000, a 21.2% increase as compared to prior year’s sales of $28,686,000. All three product groups achieved double-digit growth in the current year, with T&M hardware sales up 21.0%, QuickLabel hardware sales up 37.5% and Grass Technologies’ hardware sales up 12.4%. The primary drivers of this increase relates to the increase in T&M’s Ruggedized product sales, the increase in sales of QuickLabel’s Vivo! and Zeo! product lines and the increase in Grass’ clinical line of diagnostic systems, especially EEG and Long Term Epilepsy Monitoring Systems. The increase in the current year’s hardware sales was tempered by lower sales of T&M’s recorder and data acquisition product lines.

Consumable sales in fiscal 2012 were $39,269,000, representing a 5.8% increase as compared to prior year sales of $37,113,000. The overall increase in consumable sales for the current fiscal year was primarily traceable to sales of digital color printer supplies within the QuickLabel product group, which were up 38.9% over the prior year. Also contributing to the current year increase were sales of Grass’ electrodes and cream products which increased 10.7% as compared to the prior year. This overall increase in consumable sales was somewhat tempered by a decrease in sales of chart paper within the T&M group, as well as lower sales of QuickLabel’s thermal transfer ribbon product lines as compared to the prior year.

Service and other sales revenue in fiscal 2012 were $5,157,000, a 1.2% decrease compared to prior year sales of $5,217,000 due to lower repair and parts revenue.

The Company achieved $31,783,000 in gross profit for fiscal 2012 and generated a gross profit margin of 40.1%, a slight decrease as compared to prior year’s gross profit margin of 40.4%. The nominal decline in gross profit margin for the current year is due to higher manufacturing costs, as the Company incurred an increase in raw material costs this year as a result of the higher cost of precious sensitive material and paper stock.

15

Table of Contents

Operating expenses for the current year were $27,185,000, representing a 4.5% increase from prior year’s operating expenses of $26,011,000. Specifically, selling and marketing expenses increased 7.7% from prior year to $17,980,000 in fiscal 2012, representing 22.7% of sales, a slight decrease as compared to the prior year’s 23.5% of sales. The increase in selling and marketing was primarily the result of higher personnel cost, as well as increased commissions due to sales growth. The increase in selling and marketing was also impacted by the increase in outside service spending for fiscal 2012. General and administrative (G&A) expenses declined 7.9% from prior year to $3,962,000 in fiscal 2012. The reduced G&A expense was primarily due to a decrease in professional service fees as compared to the prior year. Funding of research & development (R&D) in fiscal 2012 has increased 4.5% to $5,243,000. The increase in R&D for fiscal 2012 is primarily due to the increase in personnel costs and increase in prototype spending, offset by lower outside research and development spending. The R&D spending level for fiscal 2012 represents 6.6% of net sales, a decline from the prior year’s level of 7.1%.

In fiscal 2012, the Company recognized a $681,000 loss on the sale of our manufacturing operations in Asheboro, while in fiscal 2011 the Company reported a $104,000 gain on legal settlement for interest and attorney fees recognized as a result of damages collected from a lawsuit filed against a former employee and competitor business.

Other income in fiscal 2012 was $316,000 as compared to $24,000 in fiscal 2011. This increase in other income for the current year is primarily the result of the $300,000 of income recognized related to the disposition of a key-man life insurance policy, as well as increases in investment income and lower foreign exchange losses recognized in the current year.

Astro-Med’s fiscal 2012 pretax income was reduced by approximately $208,000 related to stock-based compensation expense as compared to fiscal 2011 pretax income, which was reduced by approximately $333,000 in stock-based compensation expense.

During fiscal 2012, the Company recognized income tax expense of $1,101,000 and had an effective tax rate of 26.0%. The current year’s income tax expense includes a benefit of $157,000 related to a favorable adjustment in the filing of the prior year’s tax returns. This compares to income tax expense of $722,000 and an effective tax rate of 25.9% in fiscal 2011 which includes a benefit of $241,000 related to the resolution of a previously uncertain tax position and a benefit of $143,000 related to a favorable adjustment in the filing of the prior year’s tax returns.

Net income for fiscal 2012 was $3,132,000, providing a return of 4.0% on sales and generating an EPS of $0.42 per diluted share. Included in net income is a $450,000 loss, net of tax, related to the sale of the Asheboro operations, equal to $0.06 per diluted share; income of $300,000 related to key-man life insurance proceeds received, equal to $0.04 per diluted share; and a $157,000 tax benefit equal to $0.02 per diluted share relating to a favorable adjustment in the filing of the prior year’s tax returns. On a comparative basis, fiscal 2011 net income was $2,062,000, providing a return of 2.9% on sales and an EPS of $0.28 per diluted share. Included in net income is a $63,000 gain, net of tax, related to the settlement of a legal matter equal to $0.01 per diluted share; $241,000 tax benefit pertaining to previously uncertain tax positions realized equal to $0.03 per diluted share; and a $143,000 tax benefit relating to a favorable adjustment in the filing of the prior year’s tax returns equal to $0.02 per diluted share.

Segment Analysis

Astro-Med reports three segments consistent with its sales product groups: Test & Measurement (T&M), QuickLabel Systems (QuickLabel) and Grass Technologies (Grass). Segment performance is evaluated based on the operating segment’s profit before corporate and financial administration expenses.

16

Table of Contents

The following table summarizes selected financial information by segment:

| (Dollars in thousands) | Net Sales | Segment Operating Profit | Segment Operating Profit as a % of Net Sales |

|||||||||||||||||||||

| 2012 | 2011 | 2012 | 2011 | 2012 | 2011 | |||||||||||||||||||

| T&M |

$ | 17,138 | $ | 14,837 | $ | 2,425 | $ | 1,200 | 14.1 | % | 8.1 | % | ||||||||||||

| QuickLabel |

43,586 | 39,500 | 2,553 | 1,847 | 5.9 | % | 4.7 | % | ||||||||||||||||

| Grass |

18,469 | 16,679 | 3,592 | 3,358 | 19.5 | % | 20.1 | % | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total |

$ | 79,193 | $ | 71,016 | 8,570 | 6,405 | 10.8 | % | 9.0 | % | ||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Corporate Expenses |

3,972 | 3,749 | ||||||||||||||||||||||

| Loss on Sale of Asheboro Operations* |

(681 | ) | — | |||||||||||||||||||||

| Gain on Legal Settlement |

— | 104 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Operating Income |

3,917 | 2,760 | ||||||||||||||||||||||

| Other Income, Net |

316 | 24 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Income Before Income Taxes |

4,233 | 2,784 | ||||||||||||||||||||||

| Income Tax Provision |

1,101 | 722 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Net Income |

$ | 3,132 | $ | 2,062 | ||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| * | The Asheboro operations were part of the QuickLabel System segment. |

Test & Measurement

T&M’s sales increased 15.5% in fiscal 2012 to $17,138,000 from $14,837,000 in the prior year. The increase is primarily due to the double-digit growth in the Ruggedized printer product line due to increased contract sales. Also contributing to the increase in sales was the continued increase in demand for the TMX product line, as current year sales grew 23.1% as compared to prior year sales. The current year sales increase is tempered by declining sales in the Dash data acquisition and recorder product lines as compared to the prior year. T&M’s segment operating profit was $2,425,000 in fiscal 2012, reflecting a profit margin of 14.1%, an improvement as compared to the prior year’s segment operating profit of $1,200,000 and related profit margin of 8.1%. The fiscal 2012 increase in operating profit is an outgrowth of higher sales and lower selling and marketing expenses.

QuickLabel Systems

QuickLabel Systems sales increased 10.3% in fiscal 2012 to $43,586,000 from sales of $39,500,000 in the prior year. The increase in current year is primarily attributable to the hardware product lines which grew 37.5% from the prior year. Within the hardware line, sales of the Vivo! and Zeo! products, which includes the new Vivo! Touch, made a significant contribution to the overall growth rate. Current year revenues from QuickLabel’s consumable product lines also reflected an increase over the previous year’s sales, primarily attributable to the increase in sales of Vivo! and Zeo! supplies, as current year sales represents a 38.9% increase as compared to the prior year. QuickLabel’s fiscal 2012 segment operating profit was $2,553,000 reflecting a profit margin of 5.9%, compared to prior year’s segment profit margin of 4.7%. The increase in operating margin for fiscal 2012 is due to higher sales and favorable mix of higher margin products included in our net sales.

Grass Technologies

Grass sales in fiscal 2012 were $18,469,000, a 10.7% increase as compared to sales of $16,679,000 in the prior year. The increase is primarily attributed to sales of the Clinical and Research hardware product lines, which increased 12.4%. Within the Clinical hardware product line, the primary contributors to the sales growth were the Electroencephalography systems (EEG) and Long Term Epilepsy Monitoring systems (LTM) as both product lines reported double digit sales increments. Also contributing to the increase in sales for the current year are the consumable products of electrodes and creams, as sales have increased 10.7%, as compared to the

17

Table of Contents

prior year. Grass’ segment operating profit was $3,592,000 in fiscal 2012, representing a profit margin of 19.5%, as compared to prior year’s segment operating profit of $3,358,000 and related profit margin of 20.1%. The fiscal 2012 increase in operating profits is an outgrowth of higher sales and favorable product mix of higher margin products included in net sales, as well as lower manufacturing costs.

Liquidity and Capital Resources

The Company expects to finance its future working capital needs, capital expenditures and acquisition requirements through internal funds and believes that cash provided by operations will be sufficient to meet our operating and capital needs for at least the next twelve months. To the extent our capital and liquidity requirements are not satisfied internally, we may utilize a $5.0 million revolving bank line of credit, all of which is currently available. Borrowings under this line of credit bear interest at either a fluctuating rate equal to 75 basis points below the base rate, as defined in the agreement, or at a fixed rate equal to 150 basis points above LIBOR.

Astro-Med’s Statements of Cash Flows for the two years ended January 31, 2012 and 2011 are included on page 34. Net cash flows provided by operating activities was $5,472,000 in the current year compared to net cash provided by operating activities of $1,348,000 in the previous year. The increase in net cash flow from operations for the current year is attributed to the positive cash flow generated from net income and reduced working capital requirements. Accounts receivables increased to $11,800,000 at January 31, 2012, as compared to $11,112,000 at January 31, 2011. The accounts receivable collection cycle decreased to 51 days sales outstanding at January 31, 2012 as compared to 54 days outstanding at prior year end. Inventory balances decreased to $14,129,000 at January 31, 2012, compared to $14,405,000 at the end of the previous year due to the sale of the Asheboro manufacturing operations. Inventory days on hand also decreased to 105 days on hand at the end of the current fiscal year from 124 days at prior year end.

Net cash flow provided by investing activities for fiscal 2012 was $430,000, which included cash used for capital expenditures of approximately $1,155,000 including $480,000 for machinery and equipment, $335,000 for tools and dies, $228,000 for information technology, $102,000 for land and building improvements and $10,000 for furniture and fixtures.

Included in net cash flow used by financing activities for fiscal 2012 were dividends paid of $2,055,000. Dividends paid in fiscal 2011 were $2,036,000. The Company’s annual dividend per share was $0.28 in fiscal 2012 and 2011. The Company has not repurchased any shares of its common stock in fiscal 2012; however, since the inception of the common stock buy back program in fiscal 1997, the Company has repurchased a total of 1,420,010 shares of its common stock. At January 31, 2012, the Company’s Board of Directors has authorized the purchase of an additional 500,000 shares of the Company’s common stock in the future.

Contractual Obligations, Commitments and Contingencies

Astro-Med is subject to contingencies, including legal proceedings and claims arising out of its businesses that cover a wide range of matters, such as: contract and employment claims; workers compensation claims; product liability claims; warranty claims; and claims related to modification, adjustment or replacement of component parts of units sold. While it is impossible to ascertain the ultimate legal and financial liability with respect to contingent liabilities, including lawsuits, we believe that the aggregate amount of such liabilities, if any, in excess of amounts provided or covered by insurance, will not have a material adverse effect on our consolidated financial position or results of operations. It is possible, however, that results of operations for any particular future period could be materially affected by changes in our assumptions or strategies related to these contingencies or changes out of the Company’s control.

18

Table of Contents

Critical Accounting Policies and Estimates

Astro-Med’s discussion and analysis of financial condition and results of operations are based upon the Company’s Consolidated Financial Statements, which have been prepared in accordance with accounting principles generally accepted in the United States. Certain of our accounting policies require the application of judgment in selecting the appropriate assumptions for calculating financial estimates. By their nature, these judgments are subject to an inherent degree of uncertainty. We periodically evaluate the judgments and estimates used for our critical accounting policies to ensure that such judgments and estimates are reasonable for our interim and year-end reporting requirements. These judgments and estimates are based on the Company’s historical experience, current trends and information available from other sources, as appropriate. If different conditions result from those assumptions used in our judgments, the results could be materially different from our estimates. We believe the following are our most critical accounting policies as they require significant judgments and estimates in the preparation of our financial statements:

Revenue Recognition: Our product sales are recognized when all of the following criteria have been met: persuasive evidence of an arrangement exists; price to the buyer is fixed or determinable; delivery has occurred and legal title and risk of loss have passed to the customer; and collectability is reasonably assured. When other significant obligations remain after products are delivered, revenue is recognized only after such obligations are fulfilled. Returns and customer credits are infrequent and are recorded as a reduction to sales. Rights of return are not included in sales arrangements. Revenue associated with products that contain specific customer acceptance criteria is not recognized before the customer acceptance criteria are satisfied. When a sale arrangement involves training or installation, the deliverables in the arrangement are evaluated to determine whether they represent multiple element arrangements. This evaluation occurs at inception of the arrangement and as each item in the arrangement is delivered. The total fee from the arrangement is allocated to each unit of accounting based on its relative fair value. Fair value for each element is established generally based on the sales price charged when the same or similar element is sold separately. We allocate revenue to each element in our multiple-element arrangements based upon their relative selling prices. We determine the selling price for each deliverable based on a selling price hierarchy. The selling price for a deliverable is based on our vendor specific objective evidence (VSOE) if available, third-party evidence (TPE) if VSOE is not available, or estimated selling price (ESP) if neither VSOE nor TPE is available. Revenue allocated to each element is then recognized when the basic revenue recognition criteria for that element have been met. The amount of product revenue recognized is affected by our judgments as to whether an arrangement includes multiple elements.

Infrequently, Astro-Med recognizes revenue for non-recurring engineering (NRE) fees for product modification orders upon completion of agreed-upon milestones. Revenue is deferred for any amounts received prior to completion of milestones. Certain of our NRE arrangements include formal customer acceptance provisions. In such cases, we determine whether we have obtained customer acceptance for the specific milestone before recognizing revenue.

Infrequently, the Company receives requests from customers to hold product being purchased from us for the customers’ convenience. We recognize revenue for such bill and hold arrangements provided the transaction meets the following criteria: a valid business purpose for the arrangement exists; risk of ownership of the purchased product has transferred to the buyer; there is a fixed delivery date that is reasonable and consistent with the buyer’s business purpose; the product is ready for shipment; the payment terms are customary; we have no continuing performance obligation in regards to the product and the product have been segregated from our inventories.

Warranty Claims and Bad Debts: Provisions for the estimated costs for future product warranty claims and bad debts are recorded in cost of sales and general and administrative expense, respectively, at the time a sale is recorded. The amounts recorded are generally based upon historically derived percentages while also factoring in any new business conditions that might impact the historical analysis such as new product introduction for warranty and bankruptcies of particular customers for bad debts. We also periodically evaluate the adequacy of

19

Table of Contents

our reserves for warranty and bad debts recorded in its consolidated balance sheet as a further test to ensure the adequacy of the recorded provisions. Warranty and bad debt analysis often involves subjective analysis of a particular customer’s ability to pay. As a result, significant judgment is required in determining the appropriate amounts to record and such judgments may prove to be incorrect in the future. We believe that our procedures for estimating such amounts are reasonable and historically have not resulted in material adjustments in subsequent periods when the estimates are adjusted to the actual amounts.

Inventories: Inventories are stated at the lower of cost (first-in, first-out) or market. The Company records provisions to write-down obsolete and excess inventory to its estimated net realizable value. The process for evaluating obsolete and excess inventory consists of analyzing the inventory supply on hand and estimating the net realizable value of the inventory based on historical experience, current business conditions and anticipated future sales. We believe that our procedures for estimating such amounts are reasonable and historically have not resulted in material adjustments in subsequent periods when the estimates are adjusted to actual experience.

Income Taxes: A valuation allowance is established when it is “more-likely-than-not” that all or a portion of deferred tax assets will not be realized. A review of all available positive and negative evidence must be considered, including our performance, the market environment in which we operate, length of carryforward periods, existing sales backlog and future sales projections. If actual factors and conditions differ materially from the estimates made by management, the actual realization of the net deferred tax assets or liabilities could vary materially from the amounts previously recorded. At January 31, 2012, the Company has provided valuation allowances for future tax benefits resulting from certain R&D tax credits which could expire unused.

The calculation of tax liabilities involves significant judgment in estimating the impact of uncertainties in the application of complex tax laws and regulations in a multitude of jurisdictions. Although guidance on the accounting for uncertain income taxes prescribes the use of a recognition and measurement model, the determination of whether an uncertain tax position has met those thresholds will continue to require significant judgment by management. If the ultimate resolution of tax uncertainties is different from what we have estimated, our income tax expense could be materially impacted.

Long-Lived Assets and Goodwill: The impairment of long-lived assets to be held and used are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of such assets may not be recoverable. Determination of recoverability is based on an estimate of undiscounted future cash flows resulting from the use of the asset and its eventual disposition. Measurement of an impairment loss for long-lived assets that management expects to hold and use is based on the fair value of the asset.

Management evaluates the recoverability of goodwill annually or more frequently if events or changes in circumstances, such as declines in sales, earnings or cash flows, or material adverse changes in the business climate, indicate that the carrying value of an asset might be impaired. During the fourth quarter of fiscal 2012, we adopted new accounting guidance which simplifies goodwill impairment testing. Under the new guidance, goodwill is first qualitatively assessed to determine whether further impairment testing is necessary. Factors that management considers in this assessment include macroeconomic conditions, industry and market considerations, overall financial performance (both current and projected), changes in management and strategy and changes in the composition or carrying amount of net assets. If this qualitative assessment indicates that it is more likely than not that the fair value of a reporting unit is less than its carrying amount, a two step process is then performed. Step one compares the fair value of the reporting unit with its carrying value, including goodwill. If the carrying amount exceeds the fair value of the reporting unit, step two is required to determine if there is an impairment of the goodwill. Step two compares the implied fair value of the reporting unit goodwill to the carrying amount of the goodwill. We estimate the fair value of our reporting units using the income approach based upon a discounted cash flow model. We believe that this approach is appropriate because it provides a fair value estimate based upon the reporting unit’s expected long–term operating cash flow performance. In addition, the Company uses the market approach, which compares the reporting unit to publicly-traded companies and transactions involving similar business, to support the conclusions based upon the income approach. The income approach requires the use of many assumptions and estimates including future revenue, expenses, capital expenditures, and working capital, as well as discount factors and income tax rates.

20

Table of Contents

We performed a qualitative assessment for our 2012 analysis of goodwill. Based on this assessment, management does not believe that it is more likely than not that the carrying value of the reporting units exceed their fair values. Accordingly, no further testing was performed as management believes that there are no impairment issues in regards to goodwill at this time.

Share-Based Compensation: Share-based compensation expense is based on the estimated fair value of each option on the date of grant using the Black-Scholes option-pricing model. Our estimate of share-based compensation requires a number of complex and subjective assumptions including our stock price volatility, employee exercise patterns (expected life of the options) the risk free interest rate and the Company’s dividend yield. The stock price volatility assumption is based on the historical weekly price data of our common stock over a period equivalent to the weighted average expected life of our options. Management evaluated whether there were factors during that period which were unusual and would distort the volatility figure if used to estimate future volatility and concluded that there were no such factors. In determining the expected life of the option grants, the Company has observed the actual terms of prior grants with similar characteristics and the actual vesting schedule of the grant and has assessed the expected risk tolerance of different option groups. The risk-free interest rate used in the model is based on the actual U.S. Treasury zero coupon rates for bonds matching the expected term of the option as of the option grant date. The dividend assumption is based upon the prior year’s average dividend yield. No compensation expense is recognized for options that are forfeited for which the employee does not render the requisite service.

Recent Accounting Pronouncements

Reference is made to Note 1 of our Consolidated Financial Statements included herein.

Item 7A. Quantitative and Qualitative Disclosures about Market Risk

The registrant is a smaller reporting company and is not required to provide this information.

21

Table of Contents

Item 8. Financial Statements and Supplementary Data

The consolidated financial statements required under this item are submitted as a separate section of this report on the pages indicated at Item 15(a)(1). The supplementary data regarding quarterly results of operations is set forth in the following table.

QUARTERLY FINANCIAL DATA (Unaudited)

(Dollars in Thousands, Except Per Share Amounts)

| 2012 | ||||||||||||||||

| Q1 | Q2 (1) | Q3 (2) | Q4 (3) | |||||||||||||

| Net Sales |

$ | 18,860 | $ | 20,336 | $ | 19,569 | $ | 20,429 | ||||||||

| Gross Profit |

$ | 7,501 | $ | 7,901 | $ | 8,014 | $ | 8,367 | ||||||||

| Net Income |

$ | 431 | $ | 1,046 | $ | 800 | $ | 854 | ||||||||

| Net Income Per Common Share—Basic |

$ | 0.06 | $ | 0.14 | $ | 0.11 | $ | 0.12 | ||||||||

| Net Income Per Common Share—Diluted |

$ | 0.06 | $ | 0.14 | $ | 0.11 | $ | 0.11 | ||||||||

| 2011 | ||||||||||||||||

| Q1 (4) | Q2 | Q3 (5) | Q4 | |||||||||||||

| Net Sales |

$ | 17,077 | $ | 17,753 | $ | 18,329 | $ | 17,857 | ||||||||

| Gross Profit |

$ | 6,865 | $ | 7,024 | $ | 7,401 | $ | 7,376 | ||||||||

| Net Income |

$ | 430 | $ | 323 | $ | 792 | $ | 517 | ||||||||

| Net Income Per Common Share—Basic |

$ | 0.06 | $ | 0.04 | $ | 0.11 | $ | 0.07 | ||||||||

| Net Income Per Common Share—Diluted |

$ | 0.06 | $ | 0.04 | $ | 0.11 | $ | 0.07 | ||||||||

| (1) | Second quarter fiscal year 2012 net income includes $300,000 or $0.04 per share related to the proceeds of a key-man life insurance policy. |

| (2) | Third quarter fiscal year 2012 net income includes a tax benefit of $113,000 or $0.02 per share recorded as a result of a favorable adjustment in the filing of the prior year’s tax returns. |

| (3) | Fourth quarter fiscal 2012 net income includes a loss on the sale of the Asheboro operations, net of taxes of $450,000 or $0.06 per share and a tax benefit of $44,000 or $0.01 per share related to the favorable adjustment in the filing of the prior year’s tax return. |

| (4) | First quarter fiscal year 2011 net income includes gain on legal settlement, net of taxes of $63,000 or $0.01 per share. |

| (5) | Third quarter fiscal year 2011 net income includes a tax benefit of $241,000 or $0.03 per share related to the resolution of a previously uncertain tax position and a benefit of $143,000 or $0.02 per share recorded as a result of a favorable adjustment in the filing of the prior year’s tax returns. |

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

None

Item 9A. Controls and Procedures

Evaluation of Disclosure Controls and Procedures

Our management has evaluated, under the supervision and with the participation of our Chief Executive Officer and Chief Financial Officer, the effectiveness of our disclosure controls and procedures as of the end of the period covered by this Annual Report on Form 10-K pursuant to Rules 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934, as amended (Exchange Act). Based on that evaluation, our Chief Executive Officer and our Chief Financial Officer have concluded that our disclosure controls and procedures are effective at January 31, 2012 to ensure that the information required to be disclosed in our Exchange Act reports is (1) recorded, processed, summarized and reported in a timely manner and (2) accumulated and communicated to our management, including our Chief Executive Officer and our Chief Financial Officer, as appropriate, to allow timely decisions regarding required disclosure.

22

Table of Contents

Management’s Annual Report on Internal Control over Financial Reporting