Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period from to .

Commission file number 000-51860

PALADIN REALTY INCOME PROPERTIES, INC.

(Exact name of registrant as specified in its charter)

| Maryland | 20-0378980 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

| 10880 Wilshire Blvd., Suite 1400 Los Angeles, California |

90024 | |

| (Address of principal executive offices) | (Zip Code) |

(310) 996-8704

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Securities Exchange Act of 1934:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| None | None |

Securities registered pursuant to Section 12(g) of the Securities Exchange Act of 1934:

Common stock, par value $0.01 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

There is no established trading market for the registrant’s common stock, and therefore the aggregate market value of the registrant’s common stock held by non-affiliates cannot be determined.

As of March 16, 2012, there were 7,369,533 outstanding shares of common stock of Paladin Realty Income Properties, Inc.

Documents Incorporated by Reference

Part III of this Form 10-K incorporates by reference certain information (solely to the extent explicitly indicated) from the registrant’s proxy statement for the 2012 Annual Meeting of Stockholders filed or to be filed pursuant to Regulation 14A.

Table of Contents

PALADIN REALTY INCOME PROPERTIES, INC.

TABLE OF CONTENTS

Table of Contents

Special Note Regarding Forward-Looking Statements

Statements included in this annual report on Form 10-K (this “Annual Report”) that are not historical facts (including any statements concerning investment objectives, other plans and objectives of management for future operations or economic performance, or assumptions or forecasts related thereto) are forward-looking statements. These statements are only predictions. We caution you that such forward-looking statements are not guarantees. Actual events, or our actual investments and results of operations, as applicable, could differ materially from those expressed or implied in the forward-looking statements. Forward-looking statements are typically identified by the use of terms such as “may,” “will,” “should,” “expect,” “could,” “intend,” “plan,” “anticipate,” “estimate,” “believe,” “continue,” “predict,” “potential” or the negative of such terms and other comparable terminology.

The forward-looking statements included herein are based upon our current expectations, plans, estimates, assumptions and beliefs that involve numerous risks and uncertainties. Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond our control. Although we believe that the expectations reflected in such forward-looking statements are based on reasonable assumptions, our actual results and performance could differ materially from those set forth in the forward-looking statements. Factors which could have a material adverse effect on our operations and future prospects include, but are not limited to:

| • | Our ability to effectively raise sufficient proceeds in our offering to implement our business plans, or to effectively deploy the proceeds raised in our offering; |

| • | Changes in economic conditions generally and the real estate and securities markets specifically; |

| • | Legislative or regulatory changes (including changes to the laws governing the taxation of REITs); |

| • | Our continued qualification as a REIT; |

| • | The availability of capital; |

| • | Our ability to successfully identify, acquire, develop and/or manage properties on terms that are favorable to us; |

| • | Inherent risks in the real estate business, including tenant defaults, potential liability relating to environmental matters and liquidity of real estate investments; |

| • | Potential changes in the financial markets and interest rates; and |

| • | Changes to U.S. generally accepted accounting principles (“GAAP”). |

Any of the assumptions underlying forward-looking statements could be inaccurate. Our stockholders are cautioned not to place undue reliance on any forward-looking statements included in this Annual Report. All forward-looking statements are made as of the date of this Annual Report and the risk that actual results will differ materially from the expectations expressed in this Annual Report will increase with the passage of time. Except as otherwise required by the federal securities laws, we undertake no obligation to publicly update or revise any forward-looking statements after the date of this Annual Report, whether as a result of new information, future events, changed circumstances or any other reason. In light of the significant uncertainties inherent in the forward-looking statements included in this Annual Report, including, without limitation, the risks described under “Risk Factors,” the inclusion of such forward-looking statements should not be regarded as a representation by us or any other person that the objectives and plans set forth in this Annual Report will be achieved.

i

Table of Contents

| Item 1. | Business |

Overview

Paladin Realty Income Properties, Inc. (“Paladin REIT” or the “Company”) is a Maryland corporation formed on October 31, 2003 that elected to be taxed as a REIT commencing with the taxable year ended December 31, 2006. We were organized to invest in a diversified portfolio of high quality investments, focusing primarily on investments that produce current income. We seek to invest in a variety of types of real properties, either directly or through joint ventures, including apartments, office buildings, industrial buildings, shopping centers and hotels. We may also seek to invest in loans on real property such as mortgages and mezzanine loans, which we refer to as real estate related investments.

We owned interests in 14 income-producing properties through 13 joint venture investments as of December 31, 2011:

| Location |

Year Built |

Number of Units/Rentable Square Feet | ||||

| Multifamily Communities |

||||||

| Champion Farms Apartments |

Louisville, Kentucky | 2000 | 264 Units | |||

| Fieldstone at Glenwood Crossing Apartments |

Woodlawn, Ohio | 2001 | 244 Units1 | |||

| Pinehurst Apartment Homes |

Kansas City, Missouri | 1986 and 1988; renovated in 2006 | 146 Units | |||

| Pheasant Run Apartments |

Lee’s Summit, Missouri | 1985; renovated in 2003 and 2004 | 160 Units | |||

| The Retreat of Shawnee |

Shawnee, Kansas | 1984; renovated in 2004 and 2005 | 342 Units | |||

| Hilltop Village Apartments |

Kansas City, Missouri | 1986 | 124 Units | |||

| Conifer Crossing |

Norcross, Georgia | 1981 | 420 Units | |||

| Lofton Place Apartments |

Tampa, Florida | 1988 | 280 Units | |||

| Beechwood Gardens Apartments |

Philadelphia, Pennsylvania | 1967; renovated in 2003 and 2004 | 160 Units | |||

| Stone Ridge Apartments |

Columbia, South Carolina | 1975; renovated in 2008 | 191 Units | |||

| Evergreen at Coursey Place Apartments |

Baton Rouge, Louisiana | 2003 | 352 Units | |||

| Pines of York Apartments |

Yorktown, Virginia | 1976 | 248 Units | |||

| Office |

||||||

| Two and Five Governor Park (two properties) | San Diego, California | 1985 and 1989 | 22,470 Sq. Ft. and 53,048 Sq. Ft. | |||

| 1 | As originally constructed, the property had 266 units, 22 of which were damaged by a fire on February 20, 2011. The damaged units are being rebuilt and are expected to be available for occupancy in 2012. |

1

Table of Contents

Each of our existing joint venture investments is with unaffiliated third parties. We own a majority interest in ten of these joint ventures, and we own minority interests in three of the joint ventures. We are entitled to receive a priority preferred return ranging from 8.25% to 12.0% annually on our invested capital from each joint venture. With the exception of our investment in the joint ventures owning the properties at Conifer Crossing, Lofton Place Apartments, Evergreen at Coursey Place Apartments (“Coursey Place Apartments”) and Pines of York Apartments, following a sale of the property, we also receive a priority return of our invested capital before our co-venturer receives a return of its invested capital. We believe that structured transactions such as these provide us with a higher-than-market current return on our invested capital and greater protection of our invested capital, while preserving our ability to participate in property appreciation.

We own substantially all of our assets and conduct our operations through Paladin Realty Income Properties, L.P. (“Paladin OP”), which was organized in the State of Delaware on October 31, 2003 to serve as our operating partnership. We are the sole general partner of Paladin OP. Each limited partner of Paladin OP will have the right in certain circumstances to cause Paladin OP to redeem its limited partnership units for, at our option, cash equal to the value of an equivalent number of our shares or a number of our shares equal to the number of limited partnership units redeemed.

Because we will conduct all of our operations though an operating partnership, we are organized in what is referred to as an “UPREIT” structure, because it allows investors who desire to contribute property to Paladin REIT to transfer the property to Paladin OP in exchange for limited partnership units in Paladin OP and delay taxation of gain until the contributor redeems the limited partnership units for cash or shares as described above. The UPREIT structure gives us an advantage in acquiring properties from persons who may not otherwise transfer their properties because of unfavorable tax results. To avoid confusion, in this Annual Report:

| • | we refer to Paladin Realty Income Properties, L.P. as “Paladin OP”; and |

| • | the use of “we,” “us,” “our” and similar pronouns refers to either (1) Paladin REIT or (2) Paladin REIT and Paladin OP collectively, as required by the context in which such pronoun is used. |

Paladin Realty Advisors, LLC (“Paladin Advisors”) is our advisor pursuant to the sixth amended and restated advisory agreement dated July 20, 2011 and effective July 28, 2011 (the “Advisory Agreement”), and, as such, supervises and manages our day-to-day operations and selects our investments, subject to oversight by our board of directors. Paladin Advisors will also provide marketing, sales and client services on our behalf. Paladin Advisors was formed on October 31, 2003 and is an affiliate of our sponsor, Paladin Realty Partners, LLC (“Paladin Realty”). The senior officers of Paladin Advisors, who are also officers and directors of Paladin REIT, manage our operations and have primary responsibility for selecting our investments. Paladin Advisors is currently the sole limited partner of Paladin OP.

On February 23, 2005, we commenced an initial public offering of a maximum of $385,000,000 in shares of our common stock (the “Initial Offering”). The Initial Offering terminated on July 28, 2008 in connection with the commencement of our first follow-on offering of $850,000,000 in shares of our common stock (the “First Follow-On Offering”). Our First Follow-On Offering terminated on January 24, 2012 when the Registration Statement for our second follow-on offering (the “Second Follow-On Offering,” and collectively with the Initial Offering and the First Follow-On Offering, the “Offerings”), was declared effective on January 24, 2012.

KBR Capital Markets, LLC (“KBR Capital Markets”), formerly known as Paladin Realty Securities, LLC (“Paladin Securities”), serves as our dealer manager pursuant to a dealer manager agreement dated February 6, 2008 (the “Follow-On Dealer Manager Agreement”). KBR Capital Markets, which formerly operated as a wholly owned subsidiary of Paladin Advisors, is a licensed broker-dealer registered with the Financial Industry Regulatory Authority, Inc. (“FINRA”).

2

Table of Contents

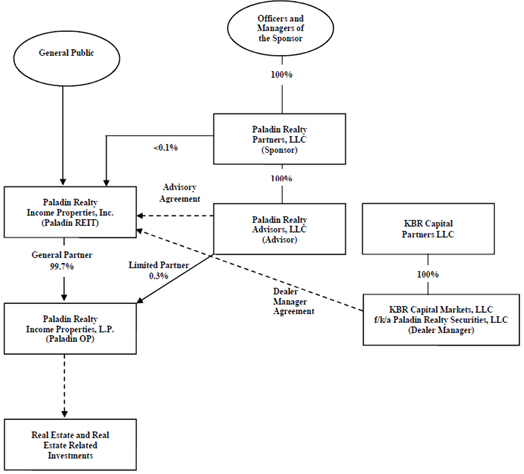

On September 1, 2011, Paladin Advisors transferred 100% of its ownership interest in KBR Capital Markets to KBR Capital Partners, LLC (“KBR Capital Partners”), which transfer remains subject to the approval of FINRA. Paladin Realty has entered into a joint venture agreement with KBR Capital Advisors, LLC, an affiliate of KBR Capital Partners, pursuant to which they may jointly sponsor additional public and private investment funds in the future.

The following chart indicates the relationship among us, KBR Capital Markets and KBR Capital Partners, and Paladin Advisors and certain of its affiliates, including Paladin Realty, as of December 31, 2011:

3

Table of Contents

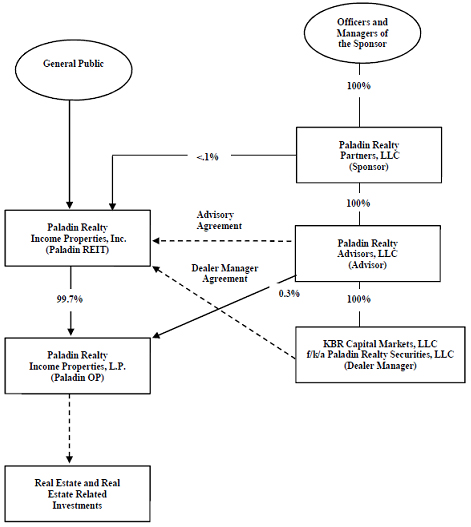

The following chart indicates the relationship among us, KBR Capital Markets, and Paladin Advisors and certain of its affiliates, including Paladin Realty, our sponsor and the managing member of Paladin Advisors, as of August 31, 2011:

As of December 31, 2011, we had sold 7,615,071 shares of our common stock for aggregate gross proceeds of $75,476,883 and as of March 16, 2012, we had sold 7,914,874shares of our common stock for aggregate gross proceeds of $78,434,545.

For the year ended December 31, 2011, we had total revenues of $24,197,962 and a net loss attributable to the Company of $3,983,368. As of December 31, 2011, our total assets were $221,521,688.

Our headquarters are located at 10880 Wilshire Boulevard, Suite 1400, Los Angeles, California 90024. Our telephone number is 1-866-725-7348. Our website is www.paladinreit.com. We are not incorporating the information on that website into this Annual Report, and the website and the information appearing on the website are not included in, and are not part of, this Annual Report.

4

Table of Contents

Current Investments

As of December 31, 2011, we owned interests in 14 income-producing properties through 13 joint venture investments. As discussed further below, our financial statements present the operations of each of our investments on a consolidated basis in accordance with GAAP. Consolidation requires us to reflect 100% of the income and expenses of property operations with a partial offset to account for the noncontrolling interests held by our joint venture partners.

801 Fiber Optic Drive

On April 28, 2011, PRIP 801, LLC, a joint venture between Paladin OP, and 801 FO, LLC, an unrelated third party, sold 801 Fiber Optic Drive, a 56,336 square foot industrial property distribution facility located on 10.95 acres in North Little Rock, Arkansas, for $4,175,000. At the time of sale, we owned a 79.0% interest in PRIP 801, LLC, and 801 FO, LLC owned the remaining 21.0% interest in PRIP 801, LLC.

The sales price exceeded the minimum selling price approved by our board of directors on February 18, 2011 and was $75,000 greater than the price we paid to acquire the property in November 2005. We recognized a gain on the sale of approximately $200,000. Since the purchase of the property, we received $777,117 in operating distributions. The sales price equaled $74 per square foot and an 8.1% cap rate on trailing twelve month net operating income. Proceeds from the sale were first used to repay debt and the closing costs of the transaction. The remaining net proceeds were distributed 79%, or $2,192,250, to us and 21% to 801 FO, LLC. At this time, we intend to redeploy the net proceeds into additional real estate and real estate related investments consistent with our investment strategy.

Champion Farms Apartments

Champion Farms Apartments is located at 3700 Springhurst Boulevard in Louisville, Kentucky 40241. Our interest in this property consists of a 70.0% membership interest in the entity that owns the property, Springhurst Housing Partners, LLC (“Springhurst”). Buckingham Springhurst, LLC, an affiliate of Buckingham Investment Corporation, an unaffiliated third party, owns the remaining 30.0% interest in Springhurst. The purchase price for our interest was approximately $4.79 million. By the terms of the joint venture for Champion Farms Apartments, we are entitled to 100% of available cash flow from the property as a priority distribution until we receive at least an 8.25% return on our invested capital. Champion Farms Apartments is a 264-unit luxury multifamily property consisting of 14 buildings located on 17.4 acres. The construction of the community was completed in 2000. The property has an aggregate of 248,442 square feet of rentable area and an average unit size of 941 square feet. Champion Farms Apartments is managed by Buckingham Management, LLC, for which it receives a customary management fee.

In connection with our acquisition of our interest in Springhurst, we may be obligated to purchase up to 20% of the membership interests in Springhurst owned by Buckingham Springhurst at a fixed price of $67,500 per 1% additional interest. Buckingham Investment Corporation may exercise this right at any time after the first anniversary of the closing of the acquisition if certain financial requirements have been met. As of December 31, 2011, the financial requirements had not been met.

Fieldstone Apartments

Fieldstone at Glenwood Crossing Apartments (“Fieldstone Apartments”) is located at 10637 Springfield Pike in Woodlawn, Ohio 45246. Our interest in this property consists of an 83.0% membership interest in the entity that owns the property, Glenwood Housing Partners I, LLC (“Glenwood”). We originally purchased a 65.0% interest in Glenwood from Shiloh Crossing Partners II, LLC (“Shiloh II”). Shiloh II is unaffiliated with us and our affiliates, except that affiliates of Shiloh II participate in another joint venture with us relating to Champion Farms Apartments. We purchased an additional 18.0% interest in Glenwood from Shiloh II on July 1, 2008 pursuant to the right Shiloh II had to require us to purchase up to an additional 25.0% of the membership interests in Glenwood owned by Shiloh II. Shiloh II continues to own the remaining 17.0% interest in Glenwood, of which we may be required to purchase up to an additional 7.0% at a fixed price of $62,500 per 1% additional interest if certain financial requirements have been met. As of December 31, 2011, the financial requirements had not been met. The total purchase price

5

Table of Contents

for our interest was approximately $5.1 million. By the terms of the joint venture for Fieldstone Apartments, we are entitled to 100% of available cash flow from the property as a priority distribution until we receive at least an 8.25% return on our invested capital. At the completion of its construction in 2001, Fieldstone Apartments was a 266-unit multifamily rental community consisting of 12 buildings located on 15.2 acres. As more fully discussed below, one of the buildings containing 22 units was damaged by fire in February 2011. Construction is underway to rebuild the building and return the units to the rental pool in 2012. As of December 31, 2011, the property had an aggregate of approximately 229,000 square feet of rentable area and an average unit size of 938 square feet. Fieldstone Apartments is managed by Buckingham Management, LLC, for which it receives a customary management fee.

In connection with the acquisition, we also entered into a Phase II Option Agreement (“Option Agreement”) with Glenwood Housing Partners II, LLC (“Glenwood II”). Glenwood II owns a parcel of land adjacent to Fieldstone Apartments upon which it may construct 88 apartment units with an aggregate of 97,640 square feet of rentable space to be leased, managed and operated as Phase II of the Fieldstone Apartments. The Option Agreement grants us an ongoing option to purchase at least a 70% but not more than 90% beneficial ownership interest in Glenwood II or any affiliated entity that owns the parcel and developments thereon. We may exercise the option at any time after the completion of development and stabilization of the project. If exercised, the purchase price for the option interest will be determined by a formula that utilizes market-rate variables as of that future date.

On February 20, 2011, a fire ignited at Fieldstone Apartments causing significant damage to 22 units, or approximately 8% of available rentable space, and accordingly, we wrote-off approximately $1,520,784 of building and improvements and recognized a corresponding insurance receivable of $1,520,784, which is included in other assets in the consolidated balance sheet. In addition, we recovered $150,000 in insurance proceeds for lost rent. The casualty loss of $1,520,784 and corresponding insurance recovery as well as the recovery for lost rent are recorded net in other income in the consolidated statements of operations. Our loss related to the fire was limited to the $10,000 deductible under our property insurance policy.

Pinehurst Apartment Homes

Pinehurst Apartment Homes is located at 500 NW 63rd Street in Kansas City, Missouri 64118. Our interest in this property consists of a 97.5% membership interest in the entity that owns the property, KC Pinehurst Associates, LLC (“KC Pinehurst”). JTL Holdings, LLC and JTL Asset Management, Inc., both affiliates of JTL Properties, LLC, a Kansas City based real estate investment and management company, own the remaining 2.5% interest in KC Pinehurst. JTL Holdings, LLC, JTL Asset Management, Inc. and JTL Properties, LLC are unaffiliated with us and our affiliates except that JTL Holdings, LLC and JTL Asset Management, Inc. participate in two other joint ventures with us relating to Pheasant Run Apartments and the Retreat of Shawnee, and JTL Properties, LLC participates in another joint venture with us relating to Hilltop Village Apartments. The purchase price for our interest was approximately $2.4 million. By the terms of the joint venture for Pinehurst Apartment Homes, we are entitled to 100% of available cash flow from the property as a priority distribution until we receive at least a 9.0% return on our invested capital. Pinehurst Apartment Homes is a 146-unit multifamily rental community renovated in 2006, consisting of 10 buildings located on 11.3 acres. The property was developed in two phases in 1986 and 1988. The property has an aggregate of 119,150 square feet of rentable area and an average unit size of 816 square feet. Pinehurst Apartment Homes is managed by CRES Management, LLC, for which it receives a customary management fee.

Pheasant Run Apartments

Pheasant Run Apartments is located at 1102 NE Independence Avenue in Lee’s Summit, Missouri 64086. Our interest in this property consists of a 97.5% membership interest in the entity that owns the property, KC Pheasant Associates, LLC (“KC Pheasant”). JTL Holdings, LLC and JTL Asset Management, Inc. own the remaining 2.5% interest in KC Pheasant. The purchase price for our interest was approximately $2.64 million. By the terms of the joint venture for Pheasant Run Apartments, we are entitled to 100% of available cash flow from the property as a priority distribution until we receive at least a 9.0% return on our invested capital. Pheasant Run Apartments is a 160-unit multifamily rental community

6

Table of Contents

consisting of 10 two-story buildings and a clubhouse located on approximately 10 acres. The property was completed in 1985 and underwent a substantial renovation in 2003 and 2004. The property has an aggregate of 112,000 square feet of rentable area and an average unit size of 700 square feet. Pheasant Run Apartments is managed by CRES Management, LLC, for which it receives a customary management fee.

The Retreat of Shawnee

The Retreat of Shawnee (the “Retreat Apartments”) is located at 11128 West 76th Terrace in Shawnee, Kansas 66214. Our interest in this property consists of a 97.5% membership interest in the entity that owns the property, KC Retreat Associates, LLC (“KC Retreat”). JTL Holdings, LLC and JTL Asset Management, Inc. own the remaining 2.5% interest in KC Retreat. The purchase price for our interest was approximately $2.85 million. By the terms of the joint venture for the Retreat Apartments, we are entitled to 100% of available cash flow from the property as a priority distribution until we receive at least a 12.0% return on our invested capital. The Retreat Apartments is a 342-unit rental apartment community consisting of 10 three-story garden-style apartments and an attached clubhouse located on 16.43 acres. The property was developed in 1984 and renovated between 2004 and 2005. The property has an aggregate of 230,400 square feet of rentable area and an average unit size of 674 square feet. The Retreat Apartments is managed by CRES Management, LLC, for which it receives a customary management fee.

Hilltop Village Apartments

Hilltop Village Apartments (“Hilltop Apartments”) is located at 8601 Newton Avenue, Kansas City, Missouri 64138. Our interest in this property consists of a 49.0% membership interest in the entity that owns the property, Park Hill Partners I, LLC (“Park Hill Partners”). JTL Properties, LLC owns the remaining 51.0% interest in Park Hill Partners. The purchase price for our interest was $1.05 million. By the terms of the joint venture for Hilltop Apartments, we are entitled to 100% of available cash flow from the property as a priority distribution until we receive at least a 12.0% return on our invested capital. Hilltop Apartments is a 124-unit rental apartment community consisting of five two- and three-story garden-style apartment buildings arranged around a central pool area located on approximately 5 acres. The property was developed in 1986. The property has an aggregate of 78,720 square feet of rentable area and an average unit size of 635 square feet. Hilltop Apartments is managed by CRES Management, LLC, for which it receives a customary management fee.

Conifer Crossing

Conifer Crossing is located at 3383 Holcomb Bridge Road NW, Norcross, Georgia 30092. Our interest in this property consists of a 42.5% membership interest in the entity that owns the property, FPA/PRIP Conifer, LLC (“FPA/PRIP Conifer”). FPA Conifer Investors, LLC owns the remaining 57.5% interest in FPA/PRIP Conifer. The purchase price for our interest was $4.5 million. By the terms of the joint venture for Conifer Crossing, we are entitled to 100% of available cash flow from the property as a priority distribution until we receive at least an 8.5% return on our invested capital. Conifer Crossing is a 420-unit rental apartment community consisting of 50 wood-frame, two-story, garden-style apartment buildings located on 53.84 acres. The property was developed in 1981. The property has an aggregate of 517,894 square feet of rentable area and an average unit size of 1,233 square feet. Conifer Crossing is managed by Trinity Property Consultants, LLC, for which it receives a customary management fee.

Two and Five Governor Park

Two and Five Governor Park are located at 6310 Greenwich Drive, San Diego, California 92122 and 5060 Shoreham Place, San Diego, California 92122. Our interest in these properties consists of a 47.7% membership interest in the entity that owns the properties, FPA Governor Park Associates, LLC (“FPA Governor Park Associates”). FPA Governor Park Investors, LLC (“FPA Governor Park Investors”) owns the remaining 52.35% interest in FPA Governor Park Associates. The purchase price for our interest was approximately $2.5 million. By the terms of the joint venture for Two and Five Governor Park, we are entitled to 100% of available cash flow from each property as a priority distribution until we receive at least a 9.0% return on our invested capital. Two and Five Governor Park are two steel frame office buildings located in the Governor Park office park. Two Governor Park is a two-story office building that was developed in 1985. It has 22,460 square feet of rentable area and sits on a 1.41 acre site. Five Governor

7

Table of Contents

Park is a three-story office building that was developed in 1989. It has 53,048 square feet of rentable area and sits on a 2.96 acre site. Two and Five Governor Park are managed by Trinity Property Consultants, LLC, for which it receives a customary management fee.

Lofton Place Apartments

Lofton Place Apartments is located at 5412 Deerbrook Creek Circle, Tampa, Florida 33624. Our interest in this property consists of a 60% membership interest in the entity that owns the property, Evergreen at Lofton Place, LLC (“Evergreen at Lofton Place”). NVR Lofton Place, LP (“NVR Lofton Place”) and BH Lofton, LLC (“BH Lofton”) own 34% and 6% membership interests, respectively. The purchase price for our interest was $3 million. By the terms of the joint venture for Lofton Place Apartments, we are entitled to 100% of available cash flow from the property as a priority distribution until we receive at least a 10.0% return on our invested capital. Lofton Place Apartments is a Class B+, 280 unit rental apartment community consisting of twelve, two- and three-story, garden-style apartment buildings located on an 18-acre site. The property was built in 1988. The property has an aggregate of 264,591 rentable square feet and an average unit size of 945 square feet. Lofton Place Apartments is managed by BH Management, for which it receives a customary management fee.

Beechwood Gardens Apartments

Beechwood Gardens Apartments is located at 9805 Haldeman Avenue, Philadelphia, Pennsylvania 19115. Our interest in this property consists of an 82.3% membership interest in the entity that owns the property, Morgan Beechwood, LLC (“Morgan Beechwood”). Morgan Management, LLC (“Morgan Management”) owns the remaining interest in Morgan Beechwood. The purchase price for our interest was $2.55 million. By the terms of the joint venture for Beechwood Gardens Apartments, we are entitled to 100% of available cash flow from the property as a priority distribution until we receive at least a 10.0% return on our invested capital. Beechwood Gardens Apartments is a stabilized Class B, 160 unit rental apartment community consisting of eight, three-story, walk-up apartment buildings located on a 5.83-acre parcel. The property was built in 1967 and renovated between 2003 and 2004. The property has an aggregate of 140,000 rentable square feet and an average unit size of 875 square feet. Beechwood Gardens Apartments is managed by Morgan Management, for which it receives a customary management fee.

Stone Ridge Apartments

Stone Ridge Apartments is located at 1000 Watermark Place, Columbia, South Carolina 29210. We originally acquired a 50.0% membership interest in DT Stone Ridge, LLC (“DT Stone Ridge”), the entity that owns the property, and The DT Group acquired the remaining 50.0% interest in DT Stone Ridge. We also made a $250,000 loan to the DT Group. On June 24, 2011, we converted the $250,000 member loan to equity in DT Stone Ridge and contributed an additional $250,000 of equity to DT Stone Ridge. The DT Group made no additional contributions. As a result, we now own a 68.5% membership interest in DT Stone Ridge, and the DT Group owns the remaining 31.5% membership interest. The total purchase price of our membership interest was $1,850,000. By the terms of the joint venture for Stone Ridge Apartments, we are entitled to 100% of available cash flow from the property as a priority distribution until we receive at least a12.0% return on our invested capital. Stone Ridge Apartments is a 191-unit rental apartment community consisting of 12 two- and three-story garden-style apartment buildings located on a 14.33 acre site. The property was built in 1975 and was most recently renovated in 2008. The property has an aggregate of 199,226 rentable square feet and an average unit size of 1,043 square feet. Stone Ridge Apartments is managed by Pegasus Residential, LLC for which it receives a customary management fee.

Coursey Place Apartments

Coursey Place Apartments is located at 13675 Coursey Boulevard, Baton Rouge, LA 70817. Our interest in this property consists of a 51.7% interest in the entity that indirectly owns the property, Coursey Place Sole Member, LLC (“Coursey Place Sole Member”). ERES Coursey LLC holds the remaining 48.3% interest in Coursey Place Sole Member. The purchase price for our interest was $5 million. By the terms of the joint venture for Coursey Place Apartments, we are entitled to 100% of available cash flow from the property as a priority distribution until we receive at least a 10.0% return on our invested capital. Coursey Place Apartments is a Class A rental apartment community

8

Table of Contents

consisting of 18 two- and three-story garden-style apartment buildings located on a 25.6 acre site. The property was built in 2003 and has an aggregate of 351,608 rentable square feet and an average unit size of 999 square feet. Coursey Place Apartments is managed by Pegasus Residential, LLC for which it receives a customary management fee.

Pines of York Apartments

Pines of York Apartments is located at 3100 Hampton Highway, Yorktown, Virginia 23693. Our interest in Pines of York Apartments consists of a 90% membership interest in the entity that owns the property, FP-1, LLC. (“FP-1”). DF Pines of York, LLC owns the remaining 10% interest in FP-1. The purchase price for our interest was approximately $5.5 million. By the terms of the joint venture for Pines of York Apartments, we are entitled to 100% of available cash flow from the property as a priority distribution until we receive at least a 10.0% return on our invested capital. Pines of York Apartments is a Class B rental apartment community consisting of 31 two-story apartment buildings located on a 23.2 acre site. The property was built in 1976 and has an aggregate of 244,640 rentable square feet and an average unit size of 987 square feet. Pines of York Apartments is managed by Drucker & Falk, LLC, for which it receives a customary management fee.

Investment Objectives

Our investment objectives are:

| • | to preserve, protect and return our investor’s capital contribution; |

| • | to make regular cash distributions; |

| • | to realize growth in the value of our investments upon our ultimate sale of such investments; and |

| • | to provide our investors with liquidity for their investment by listing our shares on a national securities exchange by February 23, 2015, or, if our shares are not listed prior to that date, by commencing an orderly liquidation of our investments and distributing the cash to our investors. |

Description of Real Property Investments and Real Estate Related Investments

We have sought and will continue to seek to acquire a diversified portfolio of high quality investments, including investments in real properties and real estate related investments, focusing primarily on investments that produce current income. We will seek to invest in a variety of types of real properties, either directly or through joint ventures, including apartments, office buildings, industrial buildings, shopping centers and hotels. We may also seek to invest in loans on real property such as mortgage and mezzanine loans, which we refer to as real estate related investments.

Although we are not limited as to the geographic area where we may conduct our operations, we currently do not intend to invest in properties located outside of the United States. If Paladin Advisors in the future determines that it is in our best interests to make investments outside the United States, we may make investments in other countries in North America in the same types of properties that we will acquire within the United States, but we would not expect those investments to comprise a significant portion of our investment portfolio. We are not specifically limited in the number or size of real property investments or real estate related investments we may make or on the percentage of our assets that we may invest in a single property or investment. The number and mix of properties we acquire and other investments we make will depend upon real estate and market conditions and other circumstances existing at the time we are acquiring our properties and making our investments and the amount of proceeds we raise in this and potential future offerings.

Borrowing Policies

We intend to use secured and unsecured debt as a means of providing additional funds for the acquisition of real property and real estate related investments.

Our charter provides that our independent directors must approve any borrowing in excess of 300% of the value of our net assets and the justification for such excess borrowing must be disclosed to our

9

Table of Contents

stockholders in our next quarterly report. Net assets for purposes of this calculation are defined to be our total assets (other than intangibles), valued at cost prior to deducting depreciation, reserves for bad debts and other non-cash reserves, less total liabilities. The preceding calculation is generally expected to approximate 75% of the aggregate cost of our assets before non-cash reserves and depreciation. As of December 31, 2011, our borrowings did not exceed 300% of the value of our net assets. As of December 31, 2011, the Company had $168,924,800 in mortgages payable.

In order to allow us to promptly invest the proceeds of our First Follow-On Offering in income-producing investments, we may incur short-term financing associated with new investments during the early stages of our operations, which may also cause us to exceed our charter’s leverage guidelines.

Under our charter, there is no limitation on the amount we may borrow to acquire any single investment.

We may not borrow money from any of our directors or from Paladin Advisors and its affiliates unless such loan is approved by a majority of our directors, including a majority of the independent directors, not otherwise interested in the transaction, as fair, competitive and commercially reasonable and no less favorable to us than comparable loans between unaffiliated parties. In addition, Paladin Advisors or its affiliates may borrow funds from unaffiliated third parties under negotiated agreements which may include revolving credit facilities, term loans or other types of loans. We may borrow from Paladin Advisors or its affiliates to provide a portion of the purchase price of a particular real property investment or real estate related investment. Such loans may be secured by a first or junior mortgage on any property so acquired. In addition to conforming with the requirements on all loans to us from Paladin Advisors described above, any such loan from Paladin Advisors or its affiliates will be made at the same interest rate and on substantially the same other terms as the loan made by the unaffiliated third party to Paladin Advisors or its affiliates.

Competition

We compete with many other entities engaged in real estate investment activities, including individuals, corporations, bank and insurance company investment accounts, pension funds, other REITs, real estate limited partnerships and foreign investors, many of which have greater resources than we do. As of December 31, 2011, our real estate investments included Champion Farms Apartments, Fieldstone Apartments, Pinehurst Apartment Homes, the Pheasant Run Apartments, the Retreat Apartments, Hilltop Apartments, Conifer Crossing, Two and Five Governor Park, Lofton Place Apartments, Beechwood Gardens Apartments, Stone Ridge Apartments, Coursey Place Apartments and Pines of York Apartments. The competitive conditions of each of these investments are favorable. Champion Farms Apartments is located in an affluent and growing neighborhood of Louisville, with access to nearby retail centers, schools and transportation routes. Fieldstone Apartments is located in an affluent suburb on the north side of Cincinnati with high barriers of entry for new development. Pinehurst Apartment Homes is located in a mature submarket approximately nine miles north of the Kansas City central business district. Pheasant Run Apartments is located in a southeastern suburb of the Kansas City metropolitan area close to major retail centers, with easy highway access to employment centers. The Retreat Apartments is located in a residential community approximately twelve miles southwest of downtown Kansas City with access to the airport, area employment centers and shopping. Hilltop Village is located in Kansas City with proximity to employment centers, schools, shopping and recreation. Conifer Crossing is located in a northeastern suburb of the Atlanta metropolitan area with easy highway access. Two and Five Governor Park is located 10 miles north of downtown San Diego in a submarket known as the Golden Triangle, which is home to leading industries and research centers. Lofton Place Apartments is located in Carrollwood, 10 miles northwest of downtown Tampa via I-275 and seven miles north of Tampa International Airport and the Westhore office submarket, via the Veteran’s Expressway (SR 589). Beechwood Gardens occupies a site at the intersection of Bustleton and Haldeman Avenues in Philadelphia, Pennsylvania and has excellent visibility, access and curb appeal. Stone Ride Apartments is located in a northwestern suburb of Columbia just outside the central business district with easy highway access to retail and employment centers. Coursey Place Apartments is located approximately 11 miles east of the Baton Rouge central business district and is favorably placed near major suburban employment nodes, four medical centers and the retail destination anchored by the 1.6 million square foot Mall of Louisiana. Pine of York Apartments is located in the desirable York County region of the Hampton Roads metropolitan statistical area in a highly rated school district with excellent access to major employers and retail centers.

10

Table of Contents

Tax Status

We elected to be taxed as a REIT for U.S. federal income tax purposes beginning with the taxable year ended December 31, 2006, under Sections 856 through 860 of the Internal Revenue Code of 1986, as amended. We believe that we operate in such a manner as to qualify for treatment as a REIT for federal income tax purposes. Accordingly, we generally will not be subject to federal income tax on our taxable income that is currently distributed to our stockholders, provided that distributions to our stockholders equal at least 90 percent of our taxable income, subject to certain adjustments. If we fail to qualify as a REIT in any taxable year without the benefit of certain relief provisions, we will be subject to federal income taxes on our taxable income at regular corporate income tax rates. We may also be subject to certain state or local income taxes, or franchise taxes.

Employees

We do not have employees. Pursuant to the Advisory Agreement, Paladin Advisors supervises and manages our day-to-day operations and selects our real property investments and real estate related investments, subject to oversight by our board of directors.

Available Information

We are subject to the reporting and information requirements of the Securities Exchange Act of 1934 (the “Exchange Act”) and, as a result, file periodic reports, proxy statements and other information with the SEC. We make these filings available on our website (http://www.paladinreit.com), as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The SEC maintains a website (http://www.sec.gov) that contains our annual, quarterly and current reports, proxy and information statements and other information we file electronically with the SEC. Unless specifically incorporated by reference herein, information on our website does not constitute part of this Annual Report on Form 10-K.

11

Table of Contents

| Item 1A. | Risk Factors |

Investment Risks

There is currently no public market for the shares of our common stock. Therefore, it will likely be difficult for our stockholders to sell their shares and, if our stockholders are able to sell their shares, they will likely sell them at a substantial discount.

There currently is no public market for our shares of common stock and we have no obligation or current plans to apply for quotation or listing on any public securities market. Therefore, it will be difficult for our stockholders to sell their shares promptly or at all. If our stockholders are able to sell their shares, they may only be able to sell them at a substantial discount from the price they paid. This may be the result, in part, of the fact that, at the time we make our investments, the amount of funds available for investment will be reduced by between 11.3% and 12.6% of the gross offering proceeds which will be used to pay fees and expenses of our First Follow-On Offering. The price per share could also be reduced as a result of other factors including those described elsewhere in this “Risk Factors” section. Unless our aggregate investments increase in value to compensate for these up-front fees and expenses, which may not occur, it is unlikely that our stockholders will be able to sell their shares, whether pursuant to our share redemption plan or otherwise, without incurring a substantial loss. We cannot assure our stockholders that their shares will ever appreciate in value to equal the price paid for their shares. Thus, our stockholders should consider the purchase of our shares as illiquid and a long-term investment, and must be prepared to hold their shares for an indefinite length of time.

We have experienced annual net losses which could adversely impact our ability to conduct operations, make investments and pay distributions.

We had a net loss of $3,983,368, $2,826,134 and $4,471,922, respectively, for the years ended December 31, 2011, December 31, 2010 and December 31, 2009. In the event that our annual net losses continue, we will have less money available to make investments and pay distributions, and our ability to conduct our operations may be adversely impacted.

To date, our distributions declared and paid have constituted a return of capital.

All of our distributions declared and paid to date have constituted a return of capital for federal income tax purposes. Distributions that are treated as a return of capital for federal income tax purposes generally will not be taxable as a dividend to a stockholder, but will reduce the stockholder’s basis in its shares (but not below zero) and therefore can result in the stockholder having a higher gain upon a subsequent sale of such shares. Return of capital distributions in excess of a stockholder’s basis generally will be treated as gain from the sale of such shares.

We have not identified any further investments that we will make with any net proceeds we will receive from our First Follow-On Offering or our Second Follow-On Offering. If we are unable to find suitable investments, we may not be able to achieve our investment objectives.

As of December 31, 2011, we own 14 property investments, which are joint venture interests in Champion Farms Apartments, Fieldstone Apartments, Pinehurst Apartment Homes, Pheasant Run Apartments, the Retreat Apartments, Hilltop Apartments, Conifer Crossing, Two and Five Governor Park, Lofton Place Apartments, Beechwood Gardens Apartments, Stone Ridge Apartments, Coursey Place Apartments and Pines of York Apartments. Paladin Advisors has not yet identified any real property investments or real estate related investments that it is reasonably probable we will make with any additional net proceeds we will receive from our First Follow-On Offering or our Second Follow-On Offering. As a result, investors in our First Follow-On Offering or our Second Follow-On Offering will be unable to evaluate the manner in which the net proceeds are invested and the economic merits of potential investments prior to the investor making an investment decision. Additionally, our stockholders will not have the opportunity to evaluate the transaction terms or other financial or operational data concerning our future real property investments and real estate related investments. Our stockholders must rely on Paladin Advisors, our advisor, to evaluate our investment opportunities, and Paladin Advisors may not be able to achieve our investment objectives, may make unwise decisions or may make decisions that are not in our

12

Table of Contents

best interest because of conflicts of interest. Further, we cannot assure our stockholders that acquisitions of real property investments or real estate related investments made using the proceeds of our First Follow-On Offering or our Second Follow-On Offering will produce a return on their investment or will generate cash flow to enable us to make distributions to our stockholders.

You may be unable to sell your shares because your ability to redeem your shares pursuant to our share redemption program is subject to significant restrictions and limitations.

Even though our share redemption program may provide you with a limited opportunity to sell your shares to us after you have held them for a period of one year, you should be fully aware that our share redemption program contains significant restrictions and limitations. Redemption of shares, when requested, will generally be made quarterly. We will limit the number of shares redeemed pursuant to our share redemption program as follows: (1) during any calendar year, we will not redeem in excess of 5% of the weighted-average number of shares outstanding during the prior calendar year; and (2) funding for the redemption of shares requested to be redeemed during a calendar quarter will come exclusively from the proceeds we receive from the sale of shares under our distribution reinvestment plan in the month following such calendar quarter, and if we do not receive sufficient funds in such month to fulfill all such redemption requests, the remaining amounts will be funded with proceeds received from the distribution reinvestment plan in subsequent months. In addition our board of directors, in its sole discretion, may choose to terminate the share redemption program or to reduce the number of shares purchased under the share redemption program upon 30 days’ notice. Therefore, you may not have the opportunity to make a redemption request prior to a potential termination of the share redemption program, or you may not be able to sell any of your shares of common stock back to us pursuant to our share redemption program because of the limitations. Moreover, if you do sell your shares of common stock back to us pursuant to the share redemption program, you will not receive the same price you paid for any shares of our common stock being redeemed.

Because we established the offering price on an arbitrary basis, it may not be indicative of the price at which our shares would trade if they were actively traded.

Our board of directors has arbitrarily determined the selling price of the shares of common stock offered hereby and such price bears no relationship to our book or asset values, or to any other established criteria for valuing issued or outstanding shares. Our offering price may not be indicative of the price at which our shares would trade if they were listed on an exchange or inter-dealer quotation system or actively traded by brokers or of the proceeds that a stockholder would receive if we were liquidated or dissolved.

Stockholders who purchased shares of our common stock in our First Follow-On Offering may have incurred, as of December 31, 2011, dilution in the net tangible book value per share of our common stock from the price paid in our First Follow-On Offering. Investors purchasing shares in our First Follow-On Offering or our Second Follow-On Offering may experience further dilution if we issue additional equity.

Net tangible book value is used as a measure of net worth that reflects certain dilution in the value of our common stock from the issue price as a result of (a) accumulated depreciation and amortization of real estate investments, (b) fees paid in connection with our public offerings, (c) the fees and expenses paid to our advisor and its affiliates in connection with the selection, acquisition, management and sale of our investments and (d) our operating and administrative expenses.

As of December 31, 2011, our net tangible book value per share was $4.52, calculated as our net tangible book value as of December 31, 2011 (consisting of stockholders’ equity, excluding certain identified intangible assets such as deferred financing and leasing costs, acquired above-market leases net of acquired below-market leases and acquired in-place lease value) divided by the 7,124,027 shares of our common stock outstanding as of December 31, 2011, as compared to our offering price of $10.00 per share in our First Follow-On Offering as of December 31, 2011. Net tangible book value does not reflect our estimated value per share nor does it necessarily reflect the value of our assets upon an orderly liquidation of us in accordance with our investment objectives.

13

Table of Contents

Additionally, investors who purchase shares in our Second Follow-On Offering will experience dilution in the percentage of their equity investment in us as we sell additional common stock in the future pursuant to our Second Follow-On Offering, if we sell securities that are convertible into common stock or if we issue shares upon the exercise of options, warrants or other rights.

Risks Relating to Our Business

We and Paladin Advisors have limited operating histories, and we may not be able to operate successfully.

We and Paladin Advisors were each formed in connection with the commencement of our Initial Offering and had no prior operating history, and our investors should not rely upon the past performance of other real estate investment programs sponsored by Paladin Realty to predict our future results. Other than our current investments, we have not identified any additional probable investments. Additionally, none of our officers, Paladin Advisors, its affiliates or their respective employees have operated any other public company or an entity that has elected to be taxed as a REIT. Our investors should consider our prospects in light of the risks, uncertainties and difficulties frequently encountered by companies that are, like us, in their early stage of development. To be successful, we must, among other things:

| • | Identify and acquire investments that further our investment objectives; |

| • | Increase awareness of the Paladin name within the investment products market; |

| • | Establish and maintain contacts with licensed securities brokers and other agents to successfully raise capital in our First Follow-On Offering and our Second Follow-On Offering; |

| • | Attract, integrate, motivate and retain qualified personnel to manage our day-to-day operations; |

| • | Respond to competition for our targeted real property investments and real estate related investments as well as for potential investors in our shares; |

| • | Continue to build and expand our operations structure to support our business; and |

| • | Maximize the value of our investments upon sale. |

Our failure, or Paladin Advisor’s failure, to operate successfully or profitably could have a material adverse effect on our ability to generate cash flow to make distributions to our stockholders and could cause our stockholders to lose all or a portion of their investment in our shares of common stock.

We differ from prior programs sponsored by Paladin Realty in a number of respects, and therefore the past performance of those programs may not be indicative of our future results.

The past performance of other investment programs sponsored by Paladin Realty may not be indicative of our future results, and we may not be able to successfully implement and operate our business, which is different in a number of respects from the operations of those programs. The returns to our stockholders will depend in part on the mix of investments that we make, the stage of investment and our place in the capital structure for our investments. As our portfolio is unlikely to mirror in any of these respects the portfolios of the prior Paladin programs, the returns to our stockholders will vary from those generated by those prior programs. We are also the first publicly-offered investment program sponsored by Paladin Realty or any of its affiliates. Therefore, the prior Paladin programs, which were conducted through privately-held entities, were not subject to either the up-front commissions, fees and expenses associated with our offerings or to many of the laws and regulations to which we are subject. We are the first program sponsored by Paladin Realty or any of its affiliates that intends to make or acquire mortgage loans or mezzanine loans. None of Paladin Realty, Paladin Advisors or any of their affiliates has experience making such investments or in operating any other REIT or a publicly-offered investment program. As a result of all these factors, our stockholders should not assume that they will experience returns, if any, comparable to those experienced by investors in the prior programs sponsored by Paladin Realty and its affiliates.

14

Table of Contents

Our ability to successfully conduct our First Follow-On Offering and our Second Follow-On Offering is dependent in part on the ability of our dealer manager to successfully establish, operate and maintain a network of broker-dealers.

The dealer manager for our First Follow-On Offering and our Second Follow-On Offering is KBR Capital Markets. KBR Capital Markets is a wholly owned subsidiary of KBR Capital Partners, LLC. KBR Capital Markets has a limited operating history and, other than serving as dealer manager for a portion of our Initial Offering, our First Follow-On Offering and our Second Follow-On Offering, has not previously acted as a dealer manager for a public offering. The success of our First Follow-On Offering and our Second Follow-On Offering, and correspondingly our ability to implement our business strategy, is dependent upon the ability of the dealer manager to maintain and expand its network of licensed securities brokers-dealers and other agents. If KBR Capital Markets fails to perform, we may not be able to raise adequate proceeds through our First Follow-On Offering and our Second Follow-On Offering to implement our investment strategy. If we are unsuccessful in implementing our investment strategy, our stockholders could lose all or a part of their investment.

Because our First Follow-On Offering and our Second Follow-On Offering are “best efforts” offerings, the dealer manager and the participating broker-dealers are only required to use their best efforts to sell our shares. If we are unable to raise substantial funds in our First Follow-On Offering and our Second Follow-On Offering, we will be limited in the number and type of investments we may make, which will result in a less diversified portfolio.

Our Follow-On Offering and our Second Follow-On Offering are being made on a “best efforts” basis, whereby the dealer manager and the broker-dealers participating in our First Follow-On Offering and our Second Follow-On Offering are only required to use their best efforts to sell our shares and have no firm commitment or obligation to purchase any of our shares. As a result, we cannot assure our stockholders as to the amount of proceeds that will be raised in our First Follow-On Offering and our Second Follow-On Offering. If we are unable to raise sufficient funds, we will have limited diversification in terms of the number of investments owned, the geographic regions in which our investments are located and the types of investments that we make. Your investment in our shares will be subject to greater risk to the extent that we lack a diversified portfolio of investments. In such event, the likelihood of our profitability being affected by the performance of any one of our investments will increase.

Payment of fees, distributions and expense reimbursements to Paladin Advisors and its affiliates will reduce cash available for investment and for distribution to our stockholders.

Paladin Advisors and its affiliates perform services for us in connection with the offer and sale of our shares, the selection and acquisition of our investments, the asset management of our investments and administrative and other services. Paladin Advisors and its affiliates will be paid acquisition fees or origination fees, asset management fees and subordinated disposition fees for these services pursuant to the Advisory Agreement. In addition, distributions may be payable to Paladin Advisors pursuant to the subordinated participation interest it holds in Paladin OP, upon a distribution of net sales proceeds to our stockholders, the listing of our shares or the termination of Paladin Advisors as our advisor. In addition, Paladin Advisors and its affiliates have provided and will continue to provide administrative services to us for which they are entitled to reimbursement at cost. These fees, distributions and expense reimbursements are substantial and will reduce the amount of cash available for investment or distribution to our stockholders.

15

Table of Contents

To date, cash flows from operations have been insufficient to pay our operating and administrative expenses and to cover the distributions we have paid and/or declared. In order to permit us to pay distributions to our stockholders, we have used cash distributions from our investments and offering proceeds and Paladin Advisors has paid expenses on our behalf and deferred the reimbursement of such expense payments and its receipt of fees we owe Paladin Advisors. We cannot assure our stockholders that in the future we will be able to achieve cash flows necessary to pay both our operating and administrative expenses and distributions at our historical per share amounts, or to maintain distributions at any particular level, if at all.

Because our cash flows from operations have been insufficient to pay our operating and administrative expenses and the distributions we have paid or declared to our stockholders through December 31, 2011, we cannot assure our stockholders that we will be able to continue paying distributions to our stockholders at our historical per-share amounts, or that the distributions we pay will not decrease or be eliminated in the future. For the years ended December 31, 2011, 2010 and 2009, we have paid $3,535,347, $2,843,251 and $2,410,031, respectively, in distributions to our stockholders and we intend to continue paying distributions to our stockholders in the future. In order to permit us to pay our distributions declared to date, we have used cash distributions from our investments, offering proceeds, Paladin Advisors has paid expenses on our behalf, and Paladin Advisors has deferred the reimbursement of expense payments and its receipt of asset management and acquisition fees.

In accordance with our charter and pursuant to the Advisory Agreement, Paladin Advisors must pay the us quarterly for any amount of operating expenses paid by us that in the 12 months then ended exceed the greater of (1) 2% of our average invested assets or (2) 25% of our net income, which we refer to as the “2%/25% Rule,” and we will not reimburse Paladin Advisors for operating expenses incurred on our behalf that in any fiscal year exceed the 2%/25% Rule unless a majority of our independent directors determine, based on unusual and non-recurring factors which they deem sufficient, that such excess was justified. During the previous twelve months, our operating expenses, including expenses incurred on behalf of us by Paladin Advisors and its affiliates did not exceed the 2%/25% Rule. Our general and administrative expenses, which are the equivalent of total operating expenses for purposes of the 2%/25% Rule, as a percentage of average invested assets were 1.0% and 1.0% for the years ended December 31, 2011 and 2010, respectively. For the years ended December 31, 2011 and 2010, we paid Paladin Advisors asset management fees of $413,475 and $380,880, respectively. For the years ended December 31, 2011 and 2010, we paid Paladin Advisors acquisition fees of $644,092 and $0, respectively.

As of December 31, 2011, Paladin Advisors and its affiliates have incurred on our behalf $7,857,099 in organization and offering costs. In addition, Paladin Advisors and its affiliates paid on our behalf $2,709,621 in general and administrative expenses in accordance with the 2%/25% Rule, of which $2,355,715 has been reimbursed by us to Paladin Advisors and $353,906 has been recorded as due to affiliates on our consolidated balance sheet.

Paladin Advisors is not obligated to either pay expenses on our behalf beyond the term of the Advisory Agreement or defer reimbursements of expense payments or fees in future periods.

Our directors will determine the amount and timing of future cash distributions to our stockholders based on many factors, including the amount of funds available for distribution, our financial condition, requirements we must meet to qualify to be taxed as a REIT, whether to reinvest or distribute such funds, capital expenditures and reserve requirements and general operational requirements. The amount of cash available for distribution will be affected by our ability to identify and make real property investments or real estate related investments as offering proceeds become available, the returns on those real property investments or real estate related investments we make and our operating and administrative expense levels, as well as many other variables. We cannot predict how long it may take to identify additional real property investments or real estate related investments, to raise sufficient proceeds or to make real property investments or real estate related investments. We likewise cannot predict whether we will generate sufficient cash flow to continue to pay distributions at historical levels or at all.

In addition, differences in timing between the recognition of income and the related cash receipts or the effect of required debt amortization payments could require us to borrow money, use proceeds from the

16

Table of Contents

issuance of securities or sell assets to pay out enough of our taxable income to satisfy the requirement that we distribute at least 90% of our taxable income subject to certain adjustments, in order to qualify as a REIT.

We are uncertain of our sources of debt or equity for funding future capital needs. If we are not able to locate sources of funding, our ability to make necessary capital improvements to our properties may be impaired or delayed.

The gross proceeds of our First Follow-On Offering and our Second Follow-On Offering have been and will be used to make real property investments, directly or through joint ventures, make real estate related investments and to pay various fees and expenses. In addition, to be taxed as a REIT, we generally must distribute to our stockholders at least 90% of our taxable income each year, subject to certain adjustments. Because of this distribution requirement, it is not likely that we will be able to fund a significant portion of our future capital needs from retained earnings. While we have used short term borrowings since the commencement of our offerings, including borrowings from affiliates of Paladin Advisors, we have not identified any sources of debt or equity for future funding. Paladin Advisors is not required to facilitate any future affiliated loans for us, and we cannot assure our stockholders that adequate sources of funding will be available to us on favorable terms or at all. If we do not have access to sufficient funding in the future, we may not be able to make necessary capital improvements to our properties, pay other expenses or expand our business.

Our success will be dependent on the performance of Paladin Advisors as well as key employees of Paladin Advisors, the loss of any of whom could be detrimental to our business.

Our ability to achieve our investment objectives and to make distributions is dependent upon the performance of Paladin Advisors and key personnel of Paladin Advisors in identifying and acquiring investments, the determination of any financing arrangements, the asset management of our investments and operation of our day-to-day activities. Our stockholders will have no opportunity to evaluate the terms of transactions or other economic or financial data concerning our investments that are not described in public documents. We will rely entirely on the management ability of Paladin Advisors, subject to the oversight of our board of directors. If Paladin Advisors suffers or is distracted by adverse financial or operational problems in connection with its operations unrelated to us, Paladin Advisors may be unable to allocate time and resources to our operations. If Paladin Advisors is unable to allocate sufficient resources to oversee and perform our operations for any reason, we may be unable to achieve our investment objectives or to make distributions to our stockholders.

Certain key personnel of Paladin Advisors, including James R. Worms, Michael B. Lenard and John A. Gerson, would be difficult to replace. None of Paladin Advisors’ key personnel are currently subject to employment agreements with Paladin Advisors, nor do we maintain any key person life insurance on Paladin Advisors’ key personnel. If any of Paladin Advisors’ key personnel were to cease employment with Paladin Advisors, our operating results could suffer. We also believe that our future success depends, in large part, upon our ability, and the ability of Paladin Advisors, to attract and retain highly skilled managerial, operational and marketing personnel. Competition for such personnel is intense, and we cannot assure our stockholders that we or Paladin Advisors will be successful in attracting and retaining such skilled personnel.

We may structure investments in real properties in exchange for limited partnership units in Paladin OP on terms that could limit our liquidity or our flexibility.

We may make investments in real properties by issuing limited partnership units in Paladin OP in exchange for a property owner contributing property to Paladin OP. If we enter into such transactions, in order to induce the contributors of such properties to accept units in Paladin OP, rather than cash, in exchange for their properties, it may be necessary for us to provide them additional incentives. For instance, Paladin OP’s partnership agreement provides that any holder of units may exchange limited partnership units on a one-for-one basis for shares of our common stock, or, at our option, cash equal to the value of an equivalent number of our shares. We may, however, enter into additional contractual arrangements with contributors of property under which we would agree to repurchase a contributor’s units

17

Table of Contents

for shares of common stock or cash, at the option of the contributor, at set times. If the contributor required us to repurchase units for cash pursuant to such a provision, it would limit our liquidity and thus our ability to use cash to make other investments, satisfy other obligations or make distributions to stockholders. Moreover, if we were required to repurchase units for cash at a time when we did not have sufficient cash to fund the repurchase, we might be required to sell one or more properties to raise funds to satisfy this obligation. Furthermore, we might agree that if distributions the contributor received as a limited partner in Paladin OP did not provide the contributor with a defined return, then upon redemption of the contributor’s units we would pay the contributor an additional amount necessary to achieve that return. Such a provision could further negatively impact our liquidity and flexibility. Finally, in order to allow a contributor of a property to defer taxable gain on the contribution of property to Paladin OP, we might agree not to sell a contributed property for a defined period of time or until the contributor exchanged the contributor’s units for cash or shares. Such an agreement would prevent us from selling those properties, even if market conditions made such a sale favorable to us.

Our results of operations, our ability to make distributions to our stockholders and our ability to dispose of our investments are subject to general economic and regulatory factors we cannot control or predict.

Our results of operations are subject to the risks of a national economic slowdown or disruption, other changes in national or local economic conditions or changes in tax, real estate, environmental or zoning laws. The following factors may affect income from our real property investments and real estate related investments, our ability to dispose of our investments, and yields from our investments:

| • | Poor economic times may result in defaults by tenants of our real properties and borrowers under our real estate related investments. We may also be required to provide rent concessions or reduced rental rates to maintain or increase occupancy levels; |

| • | Job transfers and layoffs may cause vacancies to increase and a lack of future population and job growth may make it difficult to maintain or increase occupancy levels; |

| • | Increases in supply of competing properties or decreases in demand for our real properties may impact our ability to maintain or increase occupancy levels; |

| • | Changes in interest rates and availability of debt financing could render the sale of properties difficult or unattractive; |

| • | Periods of high interest rates may reduce cash flow from leveraged properties; |

| • | Increased insurance premiums, real estate taxes, energy costs or other expenses may reduce funds available for distribution or, to the extent such increases are passed through to tenants, may lead to tenant defaults. Also, any such increased expenses may make it difficult to increase rents to tenants on turnover, which may limit our ability to increase our returns; and |

| • | Hotels that we may own could suffer substantial reductions in occupancy or room rate for an extended period of time as a result of national or local economic trends affecting travel or tourism. |

Some or all of the foregoing factors may affect the returns we receive from our investments, our results of operations, our ability to make distributions to our stockholders or our ability to dispose of our investments.

Risks Related To Conflicts of Interest

We are subject to conflicts of interest arising out of relationships among us, our officers, Paladin Advisors, KBR Capital Markets and their respective affiliates, including the material conflicts discussed below. All references to affiliates of Paladin Advisors include Paladin Realty, KBR Capital Markets and each other affiliate of Paladin Realty, KBR Capital Markets or Paladin Advisors.

Paladin Advisors and its affiliates will face conflicts of interest relating to time management and allocation of resources, and our results of operations may suffer as a result of these conflicts of interest.

Affiliates of Paladin Advisors are general partners and sponsors of other real estate programs having investment objectives similar to ours or to which they have legal and fiduciary obligations similar to those they owe to us and our stockholders. Because affiliates of Paladin Advisors have interests in other real

18

Table of Contents