Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - CERES ABINGDON L.P. | Financial_Report.xls |

| EX-32.1 - SECTION 1350 CERTIFICATION OF PRESIDENT AND DIRECTOR - CERES ABINGDON L.P. | d293524dex321.htm |

| EX-32.2 - SECTION 1350 CERTIFICATION OF CHIEF FINANCIAL OFFICER - CERES ABINGDON L.P. | d293524dex322.htm |

| EX-31.2 - RULE 13A-14(A)/15D-14(A) OF CHIEF FINANCIAL OFFICER - CERES ABINGDON L.P. | d293524dex312.htm |

| EX-31.1 - RULE 13A-14(A)/15D-14(A) CERTIFICATION OF PRESIDENT AND DIRECTOR - CERES ABINGDON L.P. | d293524dex311.htm |

| EX-10.2.C - LETTER FROM THE GENERAL PARTNER EXTENDING MANAGEMENT AGREEMENT - CERES ABINGDON L.P. | d293524dex102c.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

þ ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2011

OR ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number 0-53210

ABINGDON FUTURES FUND L.P.

(Exact name of registrant as specified in its charter)

| New York | 20-3845005 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

c/o Ceres Managed Futures LLC

522 Fifth Avenue — 14th Floor

New York, New York 10036

(Address and Zip Code of principal executive offices)

(212) 296-1999

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Redeemable Units of Limited Partnership Interest

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to section 13 or section 15(d) of the Act.

Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this form 10-K þ.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer þ | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act)

Yes ¨ No þ

Limited Partnership Redeemable Units with aggregate values of $192,004,033 of Class A and $10,033,119 of Class D were outstanding and held by non-affiliates as of the last business day of the registrant’s most recently completed second fiscal quarter.

As of February 29, 2012, there were 196,572.2642 Limited Partnership Redeemable Units of Class A outstanding, 11,453.7739 Limited Partnership Redeemable Units of Class D outstanding and 566.2369 Limited Partnership Redeemable Units of Class Z outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

[None]

PART I

Item 1. Business.

(a) General Development of Business. Abingdon Futures Fund L.P. (the “Partnership”) is a limited partnership organized on November 8, 2005, under the partnership laws of the State of New York to engage, directly or indirectly, in the speculative trading of a diversified portfolio of commodity interests including futures contracts, options, swaps and forward contracts. The sectors traded include currencies, energy, grains, indices, U.S. and non-U.S. interest rates, livestock, lumber, metals and softs. The Partnership commenced trading on February 1, 2007. The commodity interests that are traded by the Partnership through its investment in the Master (as defined below) are volatile and involve a high degree of market risk. The Partnership privately and continuously offers redeemable units of limited partnership interest (“Redeemable Units”) in the Partnership to qualified investors. There is no maximum number of Redeemable Units that may be sold by the Partnership.

Subscriptions of additional Redeemable Units and additional general partner contributions and redemptions of Redeemable Units for the years ended December 31, 2011, 2010 and 2009 are reported in the Statements of Changes in Partners’ Capital on page 22 under “Item 8. Financial Statements and Supplementary Data.”

Ceres Managed Futures LLC, a Delaware limited liability company, acts as the general partner (the “General Partner”) and commodity pool operator of the Partnership. The General Partner is wholly owned by Morgan Stanley Smith Barney Holdings LLC (“MSSB Holdings”). Morgan Stanley, indirectly through various subsidiaries, owns a majority equity interest in MSSB Holdings. Citigroup Inc. (“Citigroup”) indirectly owns a minority equity interest in MSSB Holdings. Citigroup also indirectly owns Citigroup Global Markets (“CGM”), the commodity broker and selling agent for the Partnership. Prior to July 31, 2009, the date as of which MSSB Holdings became its owner, the General Partner was wholly owned by Citigroup Financial Products Inc., a wholly owned subsidiary of Citigroup Global Markets Holdings Inc., the sole owner of which is Citigroup. As of December 31, 2011, all trading decisions for the Partnership are made by the Advisor (defined below).

On April 1, 2011, the Redeemable Units offered pursuant to the Limited Partnership Agreement were deemed “Class A Units.” The rights, liabilities, risks, and fees associated with investment in the Class A Units did not change. In addition, beginning on April 1, 2011, Class D Units were offered and on August 1, 2011, Class Z Units were offered. Class A, Class D and Class Z will each be referred to as a “Class” and collectively referred to as the “Classes.” The Class of Redeemable Units that a limited partner receives upon a subscription will generally depend upon the amount invested in the Partnership, although the General Partner may determine to offer Redeemable Units to investors at its discretion. Class Z units were offered to certain employees of Morgan Stanley Smith Barney and its affiliates (and their family members).

On February 1, 2007, the Partnership allocated substantially all of its capital to the CMF Winton Master L.P. (the “Master”), a limited partnership organized under the partnership laws of the state of New York, having the same investment objective as the Partnership. The Partnership purchased 9,017.0917 units of the Master with cash equal to $12,945,000. The Master was formed in order to permit accounts managed by Winton Capital Management Limited (“Winton” or the “Advisor”) using the Diversified Program, the Advisor’s proprietary, systematic trading program, to invest together in one trading vehicle. A description of the trading activities and focus of the Advisor is included on page 8 under “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.” The General Partner is also the general partner of the Master. The General Partner and the Advisor believe that trading through this master/feeder structure promotes efficiency and economy in the trading process. Expenses to investors as a result of the investment in the Master are approximately the same and redemption rights are not affected.

The financial statements of the Master, including the Condensed Schedule of Investments, are contained, elsewhere in this report and should be read together with the Partnership’s financial statements.

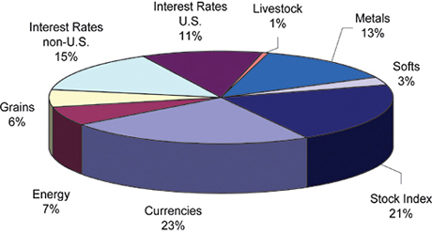

For the period January 1, 2011 through December 31, 2011, the approximate average market sector distribution for the Partnership was as follows:

As of December 31, 2011 and 2010, the Partnership owned approximately 29.2% and 18.3%, respectively, of the Master. The Partnership intends to continue to invest substantially all of its assets in the Master. The performance of the Partnership is directly affected by the performance of the Master.

The Master’s trading of futures, forwards, swaps and options contracts, if applicable, on commodities is done primarily on U.S. commodity exchanges and foreign commodity exchanges. The Master engages in such trading through a commodity brokerage account maintained with CGM.

The Partnership will be liquidated upon the first to occur of the following: December 31, 2025; when the net asset value per Redeemable Unit decreases to less than $400 per Redeemable Unit as of the close of business on any business day; a decline in net assets after trading commences to less than $1,000,000; or under certain circumstances as defined in the Limited Partnership Agreement of the Partnership (the “Limited Partnership Agreement”).

2

The General Partner administers the business and affairs of the Partnership. The Partnership pays the General Partner a monthly administrative fee in return for its services to the Partnership equal to 1/24 of 1% (0.5% per year) per class of month-end Net Assets per Class, for each outstanding Class. Month-end Net Assets per Class, for the purpose of calculating administrative fees are Net Assets, as defined in the Limited Partnership Agreement, prior to the reduction of the current month’s management fee, incentive fee accrual, the General Partner’s administrative fee and any redemptions or distributions as of the end of such month. This fee may be increased or decreased at the discretion of the General Partner.

The General Partner, on behalf of the Partnership, has entered into a management agreement (the “Management Agreement”) with the Advisor. The Management Agreement provides that the Advisor has sole discretion in determining the investment of the assets of the Partnership allocated to the Advisor by the General Partner. The Partnership is obligated to pay the Advisor a monthly management fee equal to 1/12 of 1.5% (1.5% per year) of month-end Net Assets per Class, for each outstanding Class, allocated to the Advisor. Month-end Net Assets per Class, for each outstanding Class, for the purpose of calculating management fees are Net Assets per Class, as defined in the Limited Partnership Agreement, prior to the reduction of the current month’s management fee, incentive fee accrual, the General Partner’s administrative fee and any redemptions or distributions as of the end of such month. Effective April 1, 2011, the Advisor reduced the management fee it receives from the Partnership from an annual rate of 2% of adjusted net assets to an annual rate of 1.5% of adjusted net assets. The Management Agreement may be terminated upon notice by either party.

In addition, the Partnership is obligated to pay the Advisor an incentive fee, payable quarterly, equal to 20% of the New Trading Profits, as defined in the Management Agreement, allocated pro-rata from the Master, earned by the Advisor for the Partnership during each calender quarter. The Advisor will not be paid incentive fees until the Advisor recovers the net loss incurred and earns additional new trading profits for the Partnership.

The Partnership has entered into a customer agreement (the “Customer Agreement”) which provides that the Partnership will pay CGM a monthly brokerage fee equal to (i) 4.5% per year of month-end Net Assets for Class A units (ii) 1.875% per year of month-end Net Assets Class D units (iii) 1.125% per year of month-end Net Assets for Class Z units, each allocated pro rata from the Master, in lieu of brokerage fees on a per trade basis. Month-end Net Assets, for the purpose of calculating brokerage fees are Net Assets, as defined in the Limited Partnership Agreement, prior to the reduction of the current month’s brokerage fees, management fee, incentive fee accrual, the General Partner’s administrative fee, other expenses and any redemptions or distributions as of the end of such month. Brokerage fees will be paid for the life of the Partnership, although the rate at which such fees are paid may be changed. This fee may be increased or decreased at any time at CGM’s discretion upon written notice to the Partnership. CGM will pay a portion of its brokerage fees to other properly registered selling agents and to financial advisors who have sold Redeemable Units. All National Futures Association (“NFA”) fees, exchange, clearing, user, give-up and floor brokerage fees (collectively, the “clearing fees”) will be borne by the Master and allocated to the Partnership through its investment in the Master. The Partnership’s assets not held in the Master’s account at CGM are held in the Partnership’s account at CGM. The Partnership’s cash was deposited by CGM in segregated bank accounts to the extent required by Commodity Futures Trading Commission (“CFTC”) regulations. CGM will pay the Partnership interest on its allocable share of 80% of the average daily equity maintained in cash in the Master’s brokerage account during each month at a 30-day U.S. Treasury bill rate determined weekly by CGM based on the average noncompetitive yield on 3-month U.S. Treasury bills maturing in 30 days from the date on which such weekly rate is determined. The Customer Agreement between the Partnership and CGM and the Master and CGM gives the Partnership and the Master, respectively, the legal right to net unrealized gains and losses on open futures and forward contracts. The Customer Agreement may be terminated upon notice by either party.

(b) Financial Information about Segments. The Partnership’s business consists of only one segment, speculative trading of commodity interests. The Partnership does not engage in sales of goods or services. The Partnership’s net income (loss) from operations for the years ended December 31, 2011, 2010 and 2009 is set forth under “Item 6. Selected Financial Data.” The Partnership’s Capital as of December 31, 2011 was $237,068,136.

(c) Narrative Description of Business.

See Paragraphs (a) and (b) above.

(i) through (xii) — Not applicable.

(xiii) — The Partnership has no employees.

(d) Financial Information About Geographic Areas. The Partnership does not engage in sales of goods or services or own any long-lived assets, and therefore this item is not applicable.

3

(e) Available Information. The Partnership does not have an internet address. The Partnership will provide paper copies of its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to these reports free of charge upon request.

(f) Reports to Security Holders. Not applicable.

(g) Enforceability of Civil Liabilities Against Foreign Persons. Not applicable.

(h) Smaller Reporting Companies. Not applicable.

Item 1A. Risk Factors.

As a result of leverage, small changes in the price of the Partnership’s positions may result in major losses.

The trading of commodity interests is speculative, volatile and involves a high degree of leverage. A small change in the market price of a commodity interest contract can produce major losses for the Partnership. Market prices can be influenced by, among other things, changing supply and demand relationships, governmental, agricultural, commercial and trade programs and policies, national and international political and economic events, weather and climate conditions, insects and plant disease, purchases and sales by foreign countries and changing interest rates.

An investor may lose all of its investment.

Due to the speculative nature of trading commodity interests, an investor could lose all of its investment in the Partnership.

The Partnership will pay substantial fees and expenses regardless of profitability.

Regardless of its trading performance, the Partnership will incur fees and expenses, including brokerage and management fees. Fees will be paid to the trading Advisor even if the Partnership experiences a net loss for the full year.

An investor’s ability to redeem or transfer units is limited.

An investor’s ability to redeem units is limited, and no market exists for the units.

Conflicts of interest exist.

The Partnership is subject to numerous conflicts of interest including those that arise from the facts that:

| 1. | The General Partner and the Partnership’s/Master’s commodity broker are affiliates; |

| 2. | The Advisor, the Partnership’s/Master’s commodity broker and their principals and affiliates may trade in commodity interests for their own accounts; and |

| 3. | An investor’s financial advisor will receive ongoing compensation for providing services to the investor’s account. |

Investing in units might not provide the desired diversification of an investor’s overall portfolio.

The Partnership will not provide any benefit of diversification of an investor’s overall portfolio unless it is profitable and produces returns that are independent from stock and bond market returns.

Past performance is no assurance of future results.

The Advisor’s trading strategies may not perform as they have performed in the past. The Advisor has from time to time incurred substantial losses in trading on behalf of clients.

An investor’s tax liability may exceed cash distributions.

4

Investors are taxed on their share of the Partnership’s income, even though the Partnership does not intend to make any distributions.

Regulatory changes could restrict the Partnership’s operations.

Regulatory changes could adversely affect the Partnership by restricting its markets or activities, limiting its trading and/or increasing the taxes to which investors are subject. Pursuant to the mandate of the Dodd-Frank Wall Street Reform and Consumer Protection Act, signed into law on July 21, 2010, the CFTC and the Securities and Exchange Commission (the “SEC”) are in the process of promulgating rules to regulate swaps dealers, to require that swaps be traded on an exchange or swap execution facilities, to mandate additional reporting and disclosure requirements and to require that derivatives (such as those traded by the Partnership) be moved into central clearinghouses. These rules may negatively impact the manner in which swap contracts are traded and/or settled and limit trading by speculators (such as the Partnership) in futures and over-the-counter markets.

Speculative position and trading limits may reduce profitability.

The CFTC and U.S. exchanges have established speculative position limits on the maximum net long or net short positions which any person may hold or control in particular futures and options on futures. In addition, the CFTC has adopted new speculative position limits on economically equivalent futures, options and swaps. The trading instructions of an advisor may have to be modified, and positions held by the Partnership may have to be liquidated in order to avoid exceeding these limits. Such modification or liquidation could adversely affect the operations and profitability of the Partnership by increasing transaction costs to liquidate positions and foregoing potential profits.

5

Item 2. Properties.

The Partnership does not own or lease any properties. The General Partner operates out of facilities provided by MSSB Holdings.

Item 3. Legal Proceedings.

This section describes the major pending legal proceedings, other than ordinary routine litigation incidental to the business, to which CGM or its subsidiaries is a party or to which any of their property is subject. There are no material legal proceedings pending against the Partnership or the General Partner.

CGM is a New York corporation with its principal place of business at 388 Greenwich St., New York, New York 10013. CGM is registered as a broker-dealer and futures commission merchant (“FCM”), and provides futures brokerage and clearing services for institutional and retail participants in the futures markets. CGM and its affiliates also provide investment banking and other financial services for clients worldwide.

There have been no material administrative, civil or criminal actions within the past five years against CGM (formerly known as Salomon Smith Barney) or any of its individual principals and no such actions are currently pending, except as follows.

Mutual Funds

Several issues in the mutual fund industry have come under the scrutiny of federal and state regulators. Citigroup has received subpoenas and other requests for information from various government regulators regarding market timing, financing, fees, sales practices and other mutual fund issues in connection with various investigations. Citigroup is cooperating with all such reviews. Additionally, CGM has entered into a settlement agreement with the SEC with respect to revenue sharing and sales of classes of funds.

In May 2007, CGM finalized settlements agreement with the NYSE and the New Jersey Bureau of Securities relating to alleged improper market-timing of mutual funds by certain of its brokers prior to September 2003. The allegations included failure to supervise trading of mutual fund shares and variable annuity mutual fund sub-accounts, failure to prevent market-timing by its brokers and failure to comply with applicable recordkeeping requirements. CGM neither admitted nor denied any wrongdoing or liability, and paid $50 million in disgorgement and penalties.

FINRA Settlement

On October 12, 2009, FINRA announced its acceptance of an Award Waiver and Consent (“AWC”) in which CGM, without admitting or denying the findings, consented to the entry of the AWC and a fine and censure of $600,000. The AWC includes findings that CGM failed to adequately supervise the activities of its equities trading desk in connection with swap and related hedge trades in U.S. and Italian equities that were designed to provide certain perceived tax advantages. CGM was charged with failing to provide for effective written procedures with respect to the implementation of the trades, failing to monitor Bloomberg messages and failing to properly report certain of the trades to the NASDAQ.

Auction Rate Securities

On May 31, 2006, the SEC instituted and simultaneously settled proceedings against CGM and 14 other broker-dealers regarding practices in the auction rate securities market. The SEC alleged that the broker-dealers violated Section 17(a)(2) of the Securities Act of 1933, as amended. The broker-dealers, without admitting or denying liability, consented to the entry of an SEC cease-and-desist order providing for censures, undertakings and penalties. CGM paid a penalty of $1.5 million.

On August 7, 2008, Citigroup reached a settlement with the New York Attorney General, the SEC, and other state regulatory agencies, pursuant to which Citigroup agreed to offer to purchase at par auction rate securities from all Citigroup individual investors, small institutions (as defined by the terms of the settlement), and charities that purchased auction rate securities from Citigroup prior to February 11, 2008. In addition, Citigroup agreed to pay a $50 million fine to the State of New York and a $50 million fine to the other state regulatory agencies.

Beginning in March 2008, Citigroup and certain of its affiliates, including CGM, have been named as defendants in numerous actions and proceedings brought by Citigroup shareholders and customers concerning auction-rate securities (“ARS”), many of which have been resolved. These have included, among others: (i) numerous lawsuits and arbitrations filed by customers of Citigroup and its affiliates seeking damages in connection with investments in ARS; (ii) a consolidated putative class action asserting claims for federal securities violations, which has been dismissed and is now pending on appeal; (iii) two putative class actions asserting violations of Section 1 of the Sherman Act, which have been dismissed and are now pending on appeal; and (iv) a derivative action filed against certain Citigroup officers and directors, which has been dismissed. In addition, based on an investigation, report and recommendation from a committee of Citigroup’s Board of Directors, the Board refused a shareholder demand that was made after dismissal of the derivative action. Additional information relating to certain of these actions is publicly available in court filings under the docket numbers 08 Civ. 3095 (S.D.N.Y.) (Swain, J.), 10-722 (2d Cir.); 10-867 (2d Cir.); 11-1270 (2d Cir.).

Subprime Mortgage-Related Litigation and Other Matters

The SEC, among other regulators, is investigating Citigroup’s subprime and other mortgage-related conduct and business activities, as well as other business activities affected by the credit crisis, including an ongoing inquiry into Citigroup’s structuring and sale of CDOs. Citigroup is cooperating fully with the SEC’s inquiries.

On July 29, 2010, the SEC announced the settlement of an investigation into certain of Citigroup’s 2007 disclosures concerning its subprime-related business activities. The SEC alleged misleading statements about the extent of its holdings of assets backed by subprime mortgages. On October 19, 2010, the United States District Court for the District of Columbia entered a Final Judgment approving the settlement, pursuant to which Citigroup agreed to pay a $75 million civil penalty and to maintain certain disclosure policies, practices and procedures for a three-year period. Additional information relating to this action is publicly available in court filings under the docket number 10 Civ. 1277 (D.D.C.) (Huvelle, J.).

On October 19, 2011, the SEC and Citigroup announced a settlement, subject to judicial approval, in connection with the SEC’s investigation into the structuring and sale of CDOs. Pursuant to the proposed settlement, CGM agreed to pay $160 million in disgorgement, $30 million in prejudgment interest, and a civil penalty of $95 million relating to CGM’s role in the structuring and sale of the Class V Funding III CDO transaction. On November 28, 2011, the United States District Court for the Southern District of New York declined to approve the settlement on the grounds that the court was not presented with enough facts to approve the settlement. A trial date was set for July 16, 2012. On December 15 and 19, 2011, respectively, the SEC and s filed notices of appeal. On December 27, 2011, the United States Court of Appeals for the Second Circuit granted an emergency stay of further proceedings in the district court, pending the Second Circuit’s ruling on the SEC’s motion to stay the district court proceedings during the pendency of the appeals. Additional information relating to this matter is publicly available in court filings under the docket number 11 Civ. 7387 (S.D.N.Y.) (Rakoff, J.).

Citigroup and certain of its affiliates have also been named as defendants in actions brought by counterparties and investors that have suffered losses as a result of the credit crisis. Those actions include claims asserted by investors in CDO-related transactions, including Moneygram Payment Systems, Inc., which filed a lawsuit in Minnesota state court on October 26, 2011, alleging misstatements in connection with the sale of CDO securities. Additional information relating to this action is publicly available in court filings under docket number 102611H-10 (Minn. 4th Judicial District, Hennepin Cnty.). Additional actions asserting claims related to investments or participation in CDO-related transactions may be filed in the future.

On February 9, 2012, Citigroup announced that CitiMortgage, along with other mortgage servicers, had reached an agreement in principle with the United States and with the Attorneys General for 49 states (Oklahoma did not participate) and the District of Columbia to settle a number of related investigations into residential loan servicing and origination practices. In conjunction with this settlement, Citigroup and certain of its affiliates, including CGM, also entered into a settlement with the United States Attorney’s Office for the Southern District of New York of a “qui tam” action. This action alleged that, as a participant in the Direct Endorsement Lender program, CitiMortgage had certified to the United States Department of Housing and Urban Development and the Federal Housing Administration (“FHA”) that certain loans were eligible for FHA insurance when in fact they were not. The settlement releases Citigroup from claims arising out of its acts or omissions relating to the origination, underwriting, or endorsement of all FHA-insured loans prior to the effective date of the settlement. Under the settlement, Citigroup will pay the United States $158.3 million, for which Citigroup had fully provided as of December 31, 2011. CitiMortgage will continue to participate in the Direct Endorsement Lender program. Additional information relating to this action is publicly available in court filings under the docket number 11 Civ. 5423 (S.D.N.Y.) (Marrero, J.).

The Federal Reserve Bank, the OCC and the FDIC, among other federal and state authorities, are investigating issues related to the conduct of certain mortgage servicing companies, including Citigroup affiliates, in connection with mortgage foreclosures. Citigroup is cooperating fully with these inquiries.

Credit Crisis Related Matters

Beginning in the fourth quarter of 2007, certain of Citigroup’s, and CGM’s regulators and other state and federal government agencies commenced formal and informal investigations and inquiries, and issued subpoenas and requested information, concerning Citigroup’s subprime mortgage-related conduct and business activities. Citigroup and certain of its affiliates, including CGM, are involved in discussions with certain of its regulators to resolve certain of these matters.

Certain of these regulatory matters assert claims for substantial or indeterminate damages. Some of these matters already have been resolved, either through settlements or court proceedings, including the complete dismissal of certain complaints or the rejection of certain claims following hearings.

In the course of its business, CGM, as a major futures commission merchant and broker-dealer, is a party to various civil actions, claims and routine regulatory investigations and proceedings that the General Partner believes do not have a material effect on the business of CGM. GCM may establish reserves from time to time in connections with such actions.

Item 4. Mine Safety Disclosures. Not applicable.

6

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

(a) Market Information. The Partnership has issued no stock. There is no public market for the Redeemable Units.

(b) Holders. The number of holders of Redeemable Units as of December 31, 2011 was 1,784.

(c) Dividends. The Partnership did not declare a distribution in 2011 or 2010. The Partnership does not intend to declare distributions in the foreseeable future.

(d) Securities Authorized for Issuance Under Equity Compensation Plans. None.

(e) Performance Graph. Not Applicable.

(f) Recent Sales of Unregistered Securities; Use of Proceeds from Registered Securities. For the twelve months ended December 31, 2011, the aggregate subscriptions, of the classes were 100,330.3744 Redeemable Units totaling $115,980,924 and 2,212.7189 General Partner unit equivalents totaling $2,190,348. For the twelve months ended December 31, 2010, there were additional subscriptions of 46,787.6554 Redeemable Units totaling $51,731,500 and 189.5034 General Partner unit equivalents totaling $200,000. For the twelve months ended December 31, 2009, there were additional subscriptions of 50,991.4781 Redeemable Units totaling $58,153,000 and 945.3583 General Partner unit equivalents totaling $1,000,000.

The Redeemable Units were issued in reliance upon applicable exemptions from registration under Section 4(2) of the Securities Act of 1933, as amended, and Section 506 of Regulation D promulgated thereunder. The Redeemable Units were purchased by accredited investors, as described in Regulation D. In determining the applicability of the exemption, the General Partner relied on the face that the Redeemable Units were purchased by accredited investors in a private offering.

Proceeds of net offering were used for the trading of commodity interests including futures contracts, options, swaps and forward contracts.

(g) Purchases of Equity Securities by the Issuer and Affiliated Purchasers.

The following chart sets forth the purchases of Redeemable Units by the Partnership.

| Period | (a) Total Class A of Number of Redeemable Units Purchased* |

Class

A (b) Average Price Paid per Redeemable Unit** |

(c) Total Number Redeemable Units Plans or Programs |

(d) Maximum Number May Yet Be Purchased Under the |

||||||||||||||||||

| October 1, 2011— October 31, 2011 |

3,954.8516 | $ | 1,165.90 | N/A | N/A | |||||||||||||||||

| November 1, 2011— November 30, 2011 |

3,912.7620 | $ | 1,171.96 | N/A | N/A | |||||||||||||||||

| December 1, 2011— December 31, 2011 |

1,311.0980 | $ | 1,186.26 | N/A | N/A | |||||||||||||||||

| 9,178.7116 | $ | 1,171.39 | ||||||||||||||||||||

| * | Generally, limited partners are permitted to redeem their Redeemable Units as of the end of each month on three business days’ notice to the General Partner. Under certain circumstances, the General Partner can compel redemption, although to date the General Partner has not exercised this right. Purchases of Redeemable Units by the Partnership reflected in the chart above were made in the ordinary course of the Partnership’s business in connection with effecting redemptions for limited partners. |

| ** | Redemptions of Redeemable Units are effected as of the last day of each month at the net asset value per Redeemable Unit as of that day. |

7

Item 6. Selected Financial Data.

Net realized and unrealized trading gains (losses), interest income, net income (loss), increase (decrease) in net asset value per unit and net asset value per unit for the years ended December 31, 2011, 2010, 2009, and 2008 and for the period from February 1, 2007 (commencement of trading operations) to December 31, 2007, and total assets at December 31, 2011, 2010, 2009, 2008 and 2007 were as follows:

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

| Net realized and unrealized trading gains (losses) net of expenses allocated from Master and brokerage fees (including clearing fees) of $9,261,975, $6,320,914, $5,574,180, $5,061,166 and $2,526,887, respectively |

$ | 9,501,119 | $ | 15,962,149 | $ | (11,732,036) | $ | 21,503,248 | $ | 9,521,062 | ||||||||||

| Interest income allocated from Master |

49,042 | 124,011 | 86,538 | 1,127,937 | 1,825,352 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| $ | 9,550,161 | $ | 16,086,160 | $ | (11,645,498) | $ | 22,631,185 | $ | 11,346,414 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

$ | 3,856,266 | $ | 12,299,168 | $ | (15,052,188) | $ | 15,682,974 | $ | 8,236,695 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total assets |

$ | 240,025,121 | $ | 161,871,435 | $ | 123,296,613 | $ | 119,320,005 | $ | 92,726,408 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Increase (decrease) in net asset value per unit |

||||||||||||||||||||

| Class A |

$ | 22.59 | $ | 97.13 | $ | (137.66 | ) | $ | 161.77 | $ | 42.43 | |||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Class D |

$ | 28.28 | — | — | — | — | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Class Z |

$ | 12.87 | — | — | — | — | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net asset value per unit |

||||||||||||||||||||

| Class A |

$ | 1,186.26 | $ | 1,163.67 | $ | 1,066.54 | $ | 1,204.20 | $ | 1,042.43 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Class D |

$ | 1,028.28 | $ | — | $ | — | $ | — | $ | — | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Class Z |

$ | 1,012.87 | $ | — | $ | — | $ | — | $ | — | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Overview

The Partnership, through its investment in the Master, aims to achieve substantial capital appreciation through speculative trading, directly and indirectly, in U.S. and international markets for currencies, interest rates, stock indices, agricultural and energy products and precious and base metals. The Partnership, through its investment in the Master may employ futures, options on futures, forward and swap contracts in those markets.

The General Partner manages all business of the Partnership/Master. The General Partner has delegated its responsibility for the investment of the Partnership’s assets to the Advisor. The Partnership has invested these assets in the Master. The General Partner employs a team of approximately 47 professionals whose primary emphasis is on attempting to maintain quality control among the advisors to the partnerships operated or managed by the General Partner. A full-time staff of due diligence professionals use proprietary technology and on-site evaluations to monitor new and existing futures money managers. The accounting and operations staff provides processing of subscriptions and redemptions and reporting to limited partners and regulatory authorities. The General Partner also includes staff involved in marketing and sales support. In selecting the Advisor for the Partnership/Master, the General Partner considered past performance, trading style, volatility of markets traded and fee requirements. The General Partner may modify or terminate the allocation of assets to the Advisor at any time.

Responsibilities of the General Partner include:

| • | due diligence examinations of the Advisor; |

| • | selection, appointment and termination of the Advisor; |

| • | negotiation of the Management Agreement; and |

| • | monitoring the activity of the Advisor. |

In addition, the General Partner prepares the books and records and provides the administrative and compliance services that are required by law or regulation, from time to time, in connection with the operation of the Partnership/Master. These services include the preparation of required books and records and reports to limited partners, government agencies and regulators; computation of net asset value; calculation of fees; assistance in connection with subscriptions, redemptions and limited partner communications; and preparation of offering documents and sales literature.

The General Partner seeks the best prices and services available in its commodity futures brokerage transactions.

The Partnership’s assets allocated to the Advisor for trading are not invested in commodity interests directly. The Advisor’s allocation of the Partnership’s assets is currently invested in the Master. The Advisor trades the Master’s, and thereby the

8

Partnership’s, assets in accordance with its Diversified Program, a proprietary, systematic trading system. The Diversified Program trades approximately 95 futures and forward contracts on U.S. and non-U.S. exchanges and markets.

Winton employs a fully systematic, computerized, technical, trend-following trading system developed by its principals. This system tracks the daily price movements from these markets around the world, and carries out certain computations to determine each day how long or short the portfolio should be in an attempt to maximize profit within a certain range of risk. If rising prices in a particular market are anticipated, a long position will be established in that market; if prices in a particular market are expected to fall, a short position in that market will be established.

Technical analysis refers to analysis based on data intrinsic to a market, such as price and volume. In contrast, fundamental analysis relies on factors external to a market, such as supply and demand. The Diversified Program employs no fundamental factors.

A trend-following system is one that attempts to take advantage of the observable tendency of the markets to trend, and to tend to make exaggerated movements in both upward and downward directions as a result of such trends. These exaggerated movements are largely explained as a result of the influence of crowd psychology or the “herd instinct” among market participants.

A trend-following system does not anticipate a trend. In fact, trend-following systems are frequently unprofitable for long periods of time in particular markets or market groups, and occasionally they are unprofitable for periods of more than a year. However, the principals believe that such an approach will, in the long term, be profitable.

Trade selection is not subject to intervention by Winton’s principals and therefore is not subject to the influences of individual judgment. As a mechanical trading system, the Winton model embodies all the expert knowledge required to analyze market data and direct trades, thus eliminating the risk of basing a trading program on one indispensable person. Equally as important is the fact that mechanical systems can be tested in simulation for long periods of time and the model’s empirical characteristics can be measured.

The system’s output is rigorously adhered to in trading the portfolio and intentionally no importance is given to any external or fundamental factors. While it may be seen as unwise to ignore information of obvious value, such as that pertaining to political or economic developments, Winton believes that the disadvantage of this approach is far outweighed by the advantage of the discipline that rigorous adherence to such a system instills. Winton believes that significant profits may be realized by the Winton system by holding on to positions for much longer than conventional wisdom would dictate. Winton believes that a trader who pays attention to day-to-day events could be distracted from the chance of fully capitalizing on such trends.

The Winton system trades in all liquid U.S. and non-U.S. futures and forward contracts. Forward markets include major currencies and precious and base metals, the latter two categories being traded on the London Metal Exchange. Winton seeks out new opportunities to add additional markets to the portfolio, with the goal of increasing the portfolio’s diversification.

Winton believes that taking positions in a variety of unrelated markets will, over time, decrease system volatility. By employing a sophisticated and systematic method for placing orders in a wide array of markets, Winton believes that profits can be realized over time.

As a managed futures partnership, the Partnership’s/Master’s performance is dependent upon the successful trading of the Partnership’s/Master’s Advisor to achieve the Partnership’s/Master’s objectives. It is the business of the General Partner to monitor the Advisor’s performance to ensure compliance with the Partnership’s/Master’s trading policies and to determine if the Advisor’s performance is meeting the Partnership’s/Master’s objectives.

(a) Liquidity.

The Partnership does not engage in sales of goods or services. Its only assets are its investment in the Master and cash. The Master does not engage in sales of goods of services. The Master’s only assets are its equity in its trading accounts, consisting of cash and cash equivalents, net unrealized appreciation on open futures contracts, net unrealized appreciation on forward contracts, options and swaps, if applicable. Because of the low margin deposits normally required in commodity futures trading, relatively small price movements may result in substantial losses to the Partnership, through its investment in the Master. While substantial losses could lead to a material decrease in liquidity, no such illiquidity occurred during the year ended December 31, 2011.

9

To minimize the risk relating to low margin deposits, the Master follows certain trading policies, including:

| (i) | The Master invests its assets only in commodity interests that the Advisor believes are traded in sufficient volume to permit ease of taking and liquidating positions. Sufficient volume, in this context, refers to a level of liquidity that the Advisor believes will permit it to enter and exit trades without noticeably moving the market. |

| (ii) | The Advisor will not initiate additional positions in any commodity if these positions would result in aggregate positions requiring a margin of more than 66 2/3% of the Master’s net assets allocated to the Advisor. |

| (iii) | The Master may occasionally accept delivery of a commodity. Unless such delivery is disposed of promptly by retendering the warehouse receipt representing the delivery to the appropriate clearinghouse, the physical commodity position is fully hedged. |

| (iv) | The Master does not employ the trading technique commonly known as “pyramiding,” in which the speculator uses unrealized profits on existing positions as margin for the purchases or sale of additional positions in the same or related commodities. |

| (v) | The Master does not utilize borrowings other than short-term borrowings if the Master takes delivery of any cash commodities. |

| (vi) | The Advisor may, from time to time, employ trading strategies such as spreads or straddles on behalf of the Master. “Spreads” and “Straddles” describe commodity futures trading strategies involving the simultaneous buying and selling of futures contracts on the same commodity but involving different delivery dates or markets. |

| (vii) | The Master will not permit the churning of its commodity trading account. The term “churning” refers to the practice of entering and exiting trades with a frequency unwarranted by legitimate efforts to profit from the trades, indicating the desire to generate commission income. |

From January 1, 2011 through December 31, 2011, the Partnership’s average margin to equity ratio (i.e., the percentage of assets on deposit required for margin) was approximately 7.4%. The foregoing margin to equity ratio takes into account cash held in the Partnership’s name, as well as the allocable value of the positions and cash held on behalf of the Partnership in the name of the Master.

In the normal course of business, the Partnership, through its investment in the Master, is party to financial instruments with off-balance sheet risk, including derivative financial instruments and derivative commodity instruments. These financial instruments may include forwards, futures, options and swaps, whose values are based upon an underlying asset, index, or reference rate, and generally represent future commitments to exchange currencies or cash balances, to purchase or sell other financial instruments at specific terms at specified future dates, or, in the case of derivative commodity instruments, to have a reasonable possibility to be settled in cash, through physical delivery or with another financial instrument. These instruments may be traded on an exchange or over-the-counter (“OTC”). Exchange-traded instruments are standardized and include futures and certain forwards and option contracts. OTC contracts are negotiated between contracting parties and include swaps and certain forwards and option contracts. Specific market movements of commodities of futures contracts underlying an option cannot accurately be predicted. The purchaser of an option may lose the entire premium paid for the option. The writer, or seller, of an option has unlimited risk. Each of these instruments is subject to various risks similar to those related to the underlying financial instruments including market and credit risk. In general, the risks associated with OTC contracts are greater than those associated with exchange-traded instruments because of the greater risk of default by the counterparty to an OTC contract. The General Partner estimates that at any given time approximately 3.0% to 12.6% of its contracts are traded OTC.

The risk to the limited partners that have purchased Redeemable Units limited to the amount of their capital contributions to the Partnership and their share of the Partnership’s assets and undistributed profits. This limited liability is a result of the organization of the Partnership as a limited partnership under New York law.

Market risk is the potential for changes in the value of the financial instruments traded by the Partnership/Master due to market changes, including interest and foreign exchange rate movements and fluctuations in commodity or security prices. Market risk is directly impacted by the volatility and liquidity in the markets in which the related underlying assets are traded. The Partnership/Master is exposed to a market risk equal to the value of futures and forward contracts purchased and unlimited liability on such contracts sold short.

Credit risk is the possibility that a loss may occur due to the failure of a counterparty to perform according to the terms of a contract. The Partnership’s/Master’s risk of loss in the event of a counterparty default is typically limited to the amounts recognized in the Statements of Financial Condition and not represented by the contract or notional amounts of the instruments. The Partnership’s/Master’s risk of loss is reduced through the use of legally enforceable master netting agreements with counterparties that permit the Partnership/Master to offset unrealized gains and losses and other assets and liabilities with such counterparties upon the occurrence of certain events. The Partnership/Master have credit risk and concentration risk as CGM or a CGM affiliate is the sole counterparty or broker with respect to the Partnership’s/Master’s assets. Credit risk with respect to exchange-traded instruments is reduced to the extent that through CGM, the Partnership’s/Master’s counterparty is an exchange or clearing organization.

As both a buyer and seller of options, the Master pays or receives a premium at the outset and then bears the risk of unfavorable changes in the price of the contract underlying the option. Written options expose the Master to potentially unlimited liability; for

10

purchased options, the risk of loss is limited to the premiums paid. Certain written put options permit cash settlement and do not require the option holder to own the reference asset. The Master does not consider these contracts to be guarantees.

The General Partner monitors and attempts to control the Master’s risk exposure on a daily basis through financial, credit and risk management monitoring systems, and accordingly, believes that it has effective procedures for evaluating and limiting the credit and market risks to which the Master may be subject. These monitoring systems generally allow the General Partner to statistically analyze actual trading results with risk-adjusted performance indicators and correlation statistics. In addition, online monitoring systems provide account analysis of futures, forwards, swaps and options positions by sector, margin requirements, gain and loss transactions and collateral positions. (See also “Item 8. Financial Statements and Supplementary Data” for further information on financial instrument risk included in the notes to financial statements.)

Other than the risks inherent in commodity futures and other derivatives trading, the Master knows of no trends, demands, commitments, events or uncertainties which will result in or which are reasonably likely to result in the Master’s liquidity increasing or decreasing in any material way. The Limited Partnership Agreement provides that the General Partner may, in its discretion, cause the Partnership to cease trading operations under certain circumstances including a decrease in net asset value per Redeemable Unit to less than $400 as of the close of business on any business day.

(b) Capital Resources.

(i) The Partnership has made no material commitments for capital expenditures.

(ii) The Partnership’s capital consists of the capital contributions of the partners as increased or decreased by gains or losses on trading and by expenses, interest income, redemptions of Redeemable Units and distributions of profits, if any. Gains or losses on trading cannot be predicted. Market movements in commodities are dependent upon fundamental and technical factors which the Advisor may or may not be able to identify, such as changing supply and demand relationships, weather, government agricultural, commercial and trade programs and policies, national and international political and economic events and changes in interest rates. Partnership expenses consist of, among other things, brokerage fees, advisory fees and administrative fees. The level of these expenses is dependent upon trading performance and the level of Net Assets maintained. In addition, the amount of interest income payable by CGM is dependent upon interest rates over which the Partnership has no control.

No forecast can be made as to the level of redemptions in any given period. A limited partner may require the Partnership to redeem their Redeemable Units at their net asset value per Redeemable Unit as of the last day of any month on three business days’ notice to the General Partner. There is no fee charged to limited partners in connection with redemptions. Redemptions generally are funded out of the Partnership’s cash holdings. For the year ended December 31, 2011, 34,488.0029 Redeemable Units were redeemed of Class A totaling $40,552,499, 1,878.6760 General Partner unit equivalents of Class A were redeemed totaling $2,190,348 and 73.0000 Redeemable Units of Class Z were redeemed totaling $74,248. For the year ended December 31, 2010, 24,572.2721 Redeemable Units of Class A were redeemed totaling $27,158,954. For the year ended December 31, 2009, 32,096.1158 Redeemable Units of Class A were redeemed totaling $36,076,960 and 1,877.9696 General Partner unit equivalents totaling $1,982,873.

For the year ended December 31, 2011, there were additional subscriptions of 88,367.6340 Redeemable Units of Class A totaling $103,880,764, subscriptions of 11,453.7739 Redeemable Units of Class D totaling $11,584,785, subscriptions of 508.9665 Redeemable Units of Class Z totaling $515,375 and 2,212.7189 General Partner unit equivalents of Class Z totaling $2,190,348. For the year ended December 31, 2010, there were additional subscriptions of 46,787.6554 Redeemable Units of Class A totaling $51,731,500 and 189.5034 General Partner unit equivalents of Class A totaling $200,000. For the year ended December 31, 2009, there were additional subscriptions of 50,991.4781 Redeemable Units of Class A totaling $58,153,000 and 945.3583 General Partner unit equivalents of Class A totaling $1,000,000.

(c) Results of Operations.

For the year ended December 31, 2011, the net asset value per unit for Class A increased 1.9% from $1,163.67 to $1,186.26. For the year ended December 31, 2011, the net asset value per unit for Class D increased 2.8% from $1,000.00 to $1,028.28 from April 1, 2011 to December 31, 2011. For the year ended December 31, 2011, the net asset value per unit for Class Z increased 1.3% from $1,000.00 to $1,012.87 from August 1, 2011 to December 31, 2011. For the year ended December 31, 2010, the net asset value per unit increased 9.1% from $1,066.54 to $1,163.67. For the year ended December 31, 2009, the net asset value per unit decreased 11.4% from $1,204.20 to $1,066.54.

The Partnership, through its investment in the Master, experienced a net trading gain before brokerage fees and related fees of $18,903,064 for the year ended December 31, 2011. Gains were primarily attributable to the Master’s trading of currencies, energy, metals, softs and U.S. and non-U.S. interest rates and were partially offset by losses in grains, livestock and indices. The net trading gain (or loss) realized from the Partnership’s investment in the Master is disclosed on page 22 under “Item 8. Financial Statements and Supplementary Data.”

11

The most significant gains during the year were achieved within the global interest rate sector, primarily during the third quarter, from long positions in European, U.S., and Australian fixed income futures as prices advanced due to concern about the European sovereign debt crisis and a faltering global economy. Additional gains were recorded within this sector during December from long positions in European and U.S. fixed income futures as prices increased while European leaders struggled to find funding for the euro-zone rescue plan. Within the metals markets, gains were recorded during February from long futures positions in gold and silver as gold futures prices reached an all-time high and silver futures prices extended a rally to a 30-year high. Further gains were experienced during April due to long positions in gold futures as prices continued their upward trend, reaching a new all-time high. During July and August, long positions in gold futures resulted in further gains after prices increased as escalating concern that the global economy is slowing boosted demand for the precious metal. Gains were recorded within the currency markets, primarily during April, from long positions in the Swiss franc, Australian dollar, and New Zealand dollar versus the U.S. dollar as the value of these currencies rose against the U.S. dollar after better-than-expected corporate earnings reports and signs of global growth spurred demand for higher-yielding currencies. Additional gains were experienced in this sector during December from short positions in the euro and Swiss franc versus the U.S. dollar as the value of these European currencies declined after European consumer confidence dropped more than economists forecast in December to the lowest level in more than two years. Within the energy sector, gains were achieved primarily during the first four months of the year from long futures positions in crude oil and its related products as prices rose amid an escalation in political instability in the Middle East and North Africa. Small gains were also recorded within the agricultural complex from long positions in cotton futures as prices increased on signs that global output may fail to keep pace with rising demand in China, the world’s biggest buyer of the fiber. A portion of the Partnership’s gains for the year was offset by losses incurred within the global stock index markets during June, July, and August as prices fell amid concern about the European sovereign debt crisis and a faltering global economy. Within the agricultural complex, losses were recorded primarily during June from long positions in corn futures as prices declined sharply after the U.S. Department of Agriculture revealed larger-than-expected plantings.

The Partnership, through its investment in the Master, experienced a net trading gain before brokerage fees and related fees of $22,418,528 for the year ended December 31, 2010. Gains were primarily attributable to the Master’s trading of currencies, grains, U.S. and non-U.S. interest rates, livestock, metals and softs, and were partially offset by losses in energy and indices.

Most financial risk assets recovered well in 2010 due to expansionary monetary and fiscal policies adopted by most central banks. However, this recovery came amidst global unrest due to geographically localized crises, such as the European sovereign debt crisis and inflationary headwinds in emerging markets. Global weather conditions also played a significant role in 2010 in affecting commodity prices. Many agricultural products remained at record price levels as extreme weather conditions such as drought, floods and winter storms affected production.

The Partnership was profitable in agricultural markets, currencies, interest rates and metals, while registering losses in the energy sector and equity indices.

In the agricultural sector, prices of products such as wheat, corn, sugar, cotton, coffee and soybeans reached record price levels. In the case of cotton, prices reached 140-year highs. Extreme weather conditions in some of the biggest exporters of these products significantly disrupted the global supply. Several exporting countries even imposed an export ban to meet the internal demand. The Partnership capitalized on the strong trends in such agricultural products and remained profitable in this sector.

In currencies, the Partnership registered its most significant gains in the Australian dollar, euro and Japanese yen. As the European debt crisis loomed, the euro dropped to some of the lowest levels against the U.S. dollar. Separately, Japanese yen reached its highest level in 14 years compared to the U.S. dollar. The Australian dollar also strengthened considerably against the U.S. dollar due to strong economic growth and materials exports. The Partnership was favorably positioned to profit from these trends.

In metals, the Partnership was profitable in precious and some industrial metals as they reached record prices. Precious metals, such as gold and silver, appealed to many investors as both inflation hedges and a flight to quality. Industrial metals such as copper and tin also reached record prices due to demand from resilient emerging markets such as China and India.

In interest rates, the Partnership recorded gains in both U.S. and non-U.S. interest rates. The Federal Reserve kept U.S. interest rates at historically low levels amid a consistently high unemployment rate at above 9%. Also, as the European debt crisis seemed to engulf several countries, most notably Greece and Ireland, investors flocked to U.S. and German bonds as a flight to quality. Thus the yields remained at historically low levels reaffirming the trend from earlier in the year.

In equity indices, the Partnership recorded losses earlier in the year as global equities sharply corrected. The European debt crisis and “Flash crash” of equities on May 6th came around the time that many economists were actively discussing the possibility of a double dip recession. Equity indices recovered from the lowest levels following the announcement of a European Union bailout of troubled nations within the European Union. Also, later in the year, the U.S. Federal Reserve announced a second round of quantitative easing which increased the appetite for risk assets.

12

The Partnership registered losses in the energy sector, primarily from crude oil and its derivatives, as oil remained range bound on concerns over global economic growth. Oil markets remained very volatile through most of the year and reacted sharply to global events and economic factors.

Interest income on 80% of the Partnership’s daily average equity allocated to it by the Master was earned at a 30-day U.S. Treasury bill rate determined weekly by CGM based on the average non-competitive yield on 3-month U.S. Treasury bills maturing in 30 days. Interest income allocated from the Master for the three and twelve months ended December 31, 2011 decreased by $36,137 and $74,969, respectively, as compared to the corresponding periods in 2010. The decrease in interest income is primarily due to lower U.S. Treasury bill rates during the three and twelve months ended December 31, 2011 as compared to the corresponding periods in 2010. Interest earned by the Partnership will increase the net asset value of the Partnership.

Brokerage fees are calculated as a percentage of the Partnership’s adjusted net asset value on the last day of each month and are affected by trading performance, subscriptions and redemptions. Accordingly, they must be compared in relation to the fluctuations in the monthly net asset values. Brokerage fees for the three and twelve months ended December 31, 2011 increased by $783,443 and $2,941,061, respectively, as compared to the corresponding periods in 2010. The increase in brokerage fees is due to higher net assets during the three and twelve months ended December 31, 2011 as compared to the corresponding periods in 2010.

Management fees are calculated as a percentage of the Partnership’s adjusted net asset value as of the end of each month and are affected by trading performance, subscriptions and redemptions. Management fees for the three and twelve months ended December 31, 2011 increased by $95,302 and $571,979, respectively, as compared to the corresponding periods in 2010. The increase in management fees is due to higher net assets during the three and twelve months ended December 31, 2011 as compared to the corresponding periods in 2010.

Administrative fees are calculated as a percentage of the Partnership’s adjusted net asset value as of the end of each month and are affected by trading performance, additions and redemptions. Administrative fees for the three and twelve months ended December 31, 2011 increased by $96,617 and $349,591, respectively, as compared to the corresponding periods in 2010. The increase in administrative fees is due to higher net assets during the three and twelve months ended December 31, 2011 as compared to the corresponding periods in 2010.

Incentive fees paid by the Partnership are based on the new trading profits generated by the Advisor at the end of the quarter, as defined in the management agreement. Trading performance for the three and twelve months ended December 31, 2011 resulted in an incentive fee accrual of $0 and $948,965, respectively. There were no incentive fees earned for the three and twelve months ended December 31, 2010. The Advisor will not be paid incentive fees until the Advisor recovers the net loss incurred and earns additional new trading profits for the Partnership.

13

The Partnership pays professional fees, which generally include legal and accounting expenses. Professional fees for the years ended December 31, 2011 and 2010 were $283,453 and $234,872, respectively.

The Partnership pays other expenses, which generally include filing, reporting and data processing fees. Other expenses for the years ended December 31, 2011 and 2010 were $44,743 and $56,956, respectively.

The Partnership, through its investment in the Master, experienced a net trading loss before brokerage fees and related fees of $6,064,987 for the year ended December 31, 2009. Losses were primarily attributable to the Master’s trading of currencies, energy, indices, U.S. and non-U.S. interest rates, lumber and softs and were partially offset by gains in grains, livestock, and metals.

2009 was a volatile year for the financial markets. The U.S. stock market entered 2009 reeling from the financial turmoil of 2008. The results of the sub-prime fallout, bank bailouts, auto industry bankruptcies, and capitulating economic data overwhelmed not just stock prices, but fueled extraordinarily high levels of risk aversion. The market’s recovery was driven by stability in the banking sector and a rapid recovery in global markets. By mid-year 2009, the market had hit bottom in March, banks were seeking to return TARP bailout money and other leading indicators were recovering.

The Partnership recorded losses in currencies, energy, fixed income, softs and stock indices and profits in grains, livestock and metals.

In currencies, the Partnership registered losses as the U.S. dollar reversed the strong trend earlier in the year and started weakening against the other major currencies. Trading in Japanese yen also contributed to these losses following speculation that the Japanese government may interfere in the markets to reverse a strong yen. In the energy sector, most of the products did not exhibit any strong trends and mostly remained range bound after the reversals earlier in the year. This pattern of sharp reversal followed by non-directional volatility attributed to the losses in this sector. The fixed-income sector also incurred losses. With the economic backdrop of 2008, yields started to exhibit asymmetric volatility due to extreme uncertainty prevailing in the longer time horizon. Encouraged by the continuing fiscal and monetary efforts of the U.S. government to stabilize the economy, the markets finally began to recover. In softs, the Partnership recorded losses in cocoa, cotton and coffee. In stock indices, the sharp reversal of trends earlier in the year caused losses that could be only modestly offset by the gains later in the year when strong bullish trends emerged.

In agricultural commodities, gains were recorded primarily from wheat trading. In livestock, the Partnership was profitable in hogs and cattle futures trading. The Partnership recorded gains in the metals sector primarily from gold. Investors across the world chose to buy gold through ETFs and bullion as a hedge against inflation, driven by the massive monetary influx of the central banks.

14

In the General Partner’s opinion, the Advisor continues to employ its trading methods in a consistent and disciplined manner and its results are consistent with the objectives of the Partnership and expectations for the Advisor’s programs. The General Partner continues to monitor the Advisor’s performance on a daily, weekly, monthly and annual basis to ensure that these objectives are met.

Commodity markets are highly volatile. Broad price fluctuations and rapid inflation increase the risks involved in commodity trading, but also increases the possibility of profit. The profitability of the Partnership depends on the existence of major price trends and the ability of the Advisor to correctly identify those price trends. Price trends are influenced by, among other things, changing supply and demand relationships, weather, governmental, agricultural, commercial and trade programs and policies, national and international political and economic events and changes in interest rates. To the extent that market trends exist and the Advisor is able to identify them, the Partnership expects to increase capital through operations.

In allocating substantially all of the assets of the Partnership to the Master, the General Partner considers the Advisor’s past performance, trading style, volatility of markets traded and fee requirements. The General Partner may modify or terminate the allocation of assets to the Advisor at any time.

(d) Off-Balance Sheet Arrangements. None.

(e) Contractual Obligations. None.

(f) Operational Risk.

The Partnership, through its investment in the Master is directly exposed to market risk and credit risk, which arise in the normal course of its business activities. Slightly less direct, but of critical importance, are risks pertaining to operational and back office support. This is particularly the case in a rapidly changing and increasingly global environment with increasing transaction volumes and an expansion in the number and complexity of products in the marketplace.

Such risks include:

Operational/Settlement Risk — the risk of financial and opportunity loss and legal liability attributable to operational problems, such as inaccurate pricing of transactions, untimely trade execution, clearance and/or settlement, or the inability to process large volumes of transactions. The Partnership/Master are subject to increased risks with respect to their trading activities in emerging market securities, where clearance, settlement, and custodial risks are often greater than in more established markets. Additionally, the General Partner’s computer systems may be vulnerable to unauthorized access, mishandling or misuse, computer viruses or malware, cyber attacks and other events that could have a security impact on such systems. If one or more of such events occur, this potentially could jeopardize a limited partner’s personal, confidential, proprietary or other information processed and stored in, and transmitted through, the General Partner’s computer systems, and adversely affect the Partnership’s business, financial condition or results of operations.

Technological Risk — the risk of loss attributable to technological limitations or hardware failure that constrain the Partnership’s/Master’s ability to gather, process, and communicate information efficiently and securely, without interruption, to customers, and in the markets where the Partnership/Master participates.

Legal/Documentation Risk — the risk of loss attributable to deficiencies in the documentation of transactions (such as trade confirmations) and customer relationships (such as master netting agreements) or errors that result in noncompliance with applicable legal and regulatory requirements.

Financial Control Risk — the risk of loss attributable to limitations in financial systems and controls. Strong financial systems and controls ensure that assets are safeguarded, that transactions are executed in accordance with management’s authorization, and that

15

financial information utilized by management and communicated to external parties, including the Partnership’s Redeemable Unit holders, creditors, and regulators, is free of material errors.

(g) Critical Accounting Policies.

Partnership’s Investments. The Partnership values its investment in the Master at its net asset value per unit as calculated by the Master. The Master values its investments as described in note 2 of the Master’s notes to the annual financial statements as of December 31, 2011.

Partnership’s and Master’s Fair Value Measurements. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date under current market conditions. The fair value hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1) and the lowest priority to fair values derived from unobservable inputs (Level 3). The level in the fair value hierarchy within which the fair value measurement in its entirety falls shall be determined based on the lowest level input that is significant to the fair value measurement in its entirety. The Management has concluded that based on available information in the marketplace, the Master’s Level 1 assets and liabilities are actively traded.

U.S. generally accepted accepted accounting principles (“GAAP”) also requires the use of judgment in determining if a formerly active market has become inactive and in determining fair values when the market has become inactive. Management has concluded that based on available information in the marketplace, there has not been a significant decrease in the volume and level of activity in the Partnership’s and the Master’s Level 2 assets and liabilities.

The Partnership and the Master will separately present purchases, sales, issuances, and settlements in their reconciliation of Level 3 fair value measurements (i.e., to present such items on a gross basis rather than on a net basis), and makes disclosures regarding the level of disaggregation and the inputs and valuation techniques used to measure fair value for measurements that fall within either Level 2 or Level 3 of the fair value hierarchy as required under GAAP.

The Partnership values its investments in the Master where there are no other rights or obligations inherent within the ownership interest held by the Partnership based on the end of the day net asset value of the Master (Level 2). The value of the Partnership’s investment in the Master reflects its proportional interest in the Master. As of and for the years ended December 31, 2011 and 2010, the Partnership did not hold any derivative instruments that were based on unadjusted quoted prices in active markets for identical assets (Level 1) or priced at fair value using unobservable inputs through the application of management’s assumptions and internal valuation pricing models (Level 3).

The Master considers prices for exchange-traded commodity futures, forwards and options contracts to be based on unadjusted quoted prices in active markets for identical assets (Level 1). The values of non-exchange-traded forwards, swaps and certain options contracts for which market quotations are not readily available are priced by broker-dealers who derive fair values for those assets from observable inputs (Level 2). As of and for the years ended December 31, 2011 and 2010, the Master did not hold any derivative that are priced at fair value using unobservable inputs through the application of management’s assumptions and internal valuation pricing models (Level 3).