Attached files

| file | filename |

|---|---|

| EX-31.2 - EX-31.2 - FX Alliance Inc. | a2208530zex-31_2.htm |

| EX-21.1 - EX-21.1 - FX Alliance Inc. | a2208530zex-21_1.htm |

| EX-23.1 - EX-23.1 - FX Alliance Inc. | a2208530zex-23_1.htm |

| EX-32.1 - EX-32.1 - FX Alliance Inc. | a2208530zex-32_1.htm |

| EX-31.1 - EX-31.1 - FX Alliance Inc. | a2208530zex-31_1.htm |

| EX-32.2 - EX-32.2 - FX Alliance Inc. | a2208530zex-32_2.htm |

| EX-14.01 - EX-14.01 - FX Alliance Inc. | a2208530zex-14_01.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2011 |

||

OR |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to . |

||

Commission File Number: 001-35423

FX ALLIANCE INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware (State or Other Jurisdiction of Incorporation or Organization) |

20-5845576 (I.R.S. Employer Identification No.) |

|

909 Third Avenue, 10th Floor, New York, New York (Address of Principal Executive Offices) |

10022 (Zip Code) |

(646) 268-9900

(Registrant's Telephone Number, Including Area Code)

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Common Stock, $0.0001 par value per share | New York Stock Exchange |

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that it was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by checkmark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of the Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The registrant commenced the initial public offering of its common stock on February 9, 2012. Accordingly, there was no public market for the registrant's common stock as of June 30, 2011, the last business day of the registrant's most recently completed second fiscal quarter.

As of March 22, 2012, the Registrant had 28,315,437 shares of Common Stock outstanding.

TABLE OF CONTENTS

i

Cautionary Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains forward-looking statements that are subject to risks and uncertainties. All statements other than statements of historical fact included in this Annual Report on Form 10-K are forward looking statements. Forward-looking statements discuss our current expectations and projections relating to our financial condition, results of operations, plans, objectives, future performance and business. You can identify forward looking statements by the fact that they do not relate strictly to historical or current facts. These statements may include words such as "anticipate," "estimate," "expect," "forecast," "outlook," "potential," "project," "plan," "intend," "seek," "believe," "may," "will," "should," "can have," "likely," the negatives thereof and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events. For example, all statements we make relating to our estimated and projected earnings, revenues, costs, expenditures, cash flows, growth rates and financial results, our plans and objectives for future operations, growth or initiatives, strategies, or the expected outcome or impact of pending or threatened litigation are forward looking statements. All forward looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those that we expected, including:

- •

- failure to successfully execute our growth strategy, including failing to increase our FX trading volumes, grow and

maximize our existing institutional client relationships or effectively cross-sell our products to our clients;

- •

- economic conditions, such as the current Eurozone crisis, including their effect on the FX, financial and capital markets,

our vendors and business partners, employment levels, and inflation;

- •

- our loss of key personnel or our inability to hire additional personnel;

- •

- damage or interruption to our electronic trading platform or information systems;

- •

- the impact of governmental laws and regulations;

- •

- changes in the competitive environment in our industry and the markets in which we operate;

- •

- natural disasters, unusually adverse weather conditions, pandemic outbreaks, boycotts and geo-political

events; and

- •

- our failure to maintain effective internal controls.

While we believe that our assumptions are reasonable, we caution that it is very difficult to predict the impact of known factors, and, it is impossible for us to anticipate all factors that could affect our actual results. Important factors that could cause actual results to differ materially from our expectations, or cautionary statements, are disclosed under Item 1A. "Risk Factors" and Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations" in this Annual Report on Form 10-K. All forward looking statements are expressly qualified in their entirety by these cautionary statements. You should evaluate all forward looking statements made in this Annual Report on Form 10-K in the context of these risks and uncertainties.

1

Overview

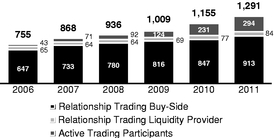

We are the leading independent global provider of electronic foreign exchange trading solutions, with over 1,000 institutional clients worldwide. We provide institutional clients with 24-hour direct access, five days per week, to the foreign exchange, or "FX," market, which is the world's largest and most liquid financial market. In a typical FX transaction, market participants buy one currency and simultaneously sell another currency, a combination known as a "currency pair." Our proprietary technology platform enables us to deliver efficient and reliable FX price discovery, trade execution and automation of pre-trade and post-trade transaction workflow for more than 400 currency pairs with access to a deep pool of liquidity from the world's leading banks and other liquidity providers. Our large and diversified institutional client base, including 58 of the S&P Global 100 and all of the top 25 banks in the FX industry globally, has grown steadily at an approximately 10% compound annual growth rate, or "CAGR," between 2007 and 2011. With offices around the world, we believe our global footprint provides us with access to a variety of high growth markets and diversifies our risk from regional economic conditions, as more than half of our trading volume is attributed to customers outside the United States.

Our comprehensive suite of electronic FX trading products, including FX spot, FX forwards, FX swaps and non-deliverable forwards, or "NDFs," is used by asset managers, banks, broker-dealers, corporations, hedge funds, prime brokers and other institutions worldwide. Our platform supports the over-the-counter, or "OTC," trading of gold and silver on a spot, forward or swap basis and provides access to bank deposits. We offer single point access to multiple execution mechanisms, including collaborative trading, request for stream, continuous streaming prices, and an anonymous electronic communication network, or "ECN," as well as execution mechanisms proprietary to specific liquidity providers. Our platform also supports advanced order types, such as limit, pegged, stop, and variable TWAP orders. In addition to facilitating our clients' FX transactions, we also license our technology for distribution under our clients' brands, which we refer to as white-labeled enterprise solutions.

As a trading technology provider, we facilitate trading between market participants, but do not act as a market maker, take principal positions for our own account or clear trades. Our clients settle their trades directly with their counterparties or prime brokers outside our platform. Our institutional clients' trading activities with us can be categorized into two types: relationship trading and active trading. Relationship trading includes our collaborative trading and request for stream systems, which are used primarily by corporations and asset managers to hedge commercial FX risk. Historically we have been focused on relationship trading. In 2011, relationship trading accounted for approximately 80% of our total trading volume and approximately 69% of transaction fee revenues. Active trading includes our continuous streaming prices and ECN systems, which are used primarily by banks, broker-dealers, hedge funds, prime brokers and other market participants who trade currencies as a central activity or profit center. In 2011, active trading accounted for approximately 20% of our total trading volume and approximately 31% of transaction fee revenues. During the four years from 2007 to 2011, the number of buy-side clients on our relationship trading systems has grown by 25% and the number of clients on our active trading platform has grown by 414%. For more information related to

2

relationship trading and active trading, see "—Trade Execution." The charts below highlight our client base and business mix:

| Total Clients |

Transaction Fees by Type in 2011

|

|

|

|

Notes: Total Clients is defined as trading entities that executed a trade generating a transaction fee during the year. Transaction fees represented 76% of our total revenues for the year ended December 31, 2011.

From 2007 to 2011, the average daily trading volume on our platform, calculated by counting one side of a transaction, grew from $50.6 billion in 2007 to $83.4 billion in 2011, representing a CAGR of 13.3%. In July 2011, we experienced record trading volume of $140 billion in a single day resulting from increased trading across all our trading systems. In 2011, we generated $118.3 million in total revenues and $26.1 million of net income, which have grown at CAGRs of 10.5% and 12.8%, respectively, since 2007.

We have offices in New York, Boston, Washington D.C., London, Zurich, Tokyo, Singapore, Hong Kong, Mumbai and Sydney, and are qualified to do business in over 68 countries. We believe that our global footprint provides us with access to a variety of high growth markets and diversifies our risk from regional economic conditions, as more than half of our trading volume is attributed to customers outside the United States. Our FX trading activities are regulated in a number of different markets by regional regulators.

Our Industry

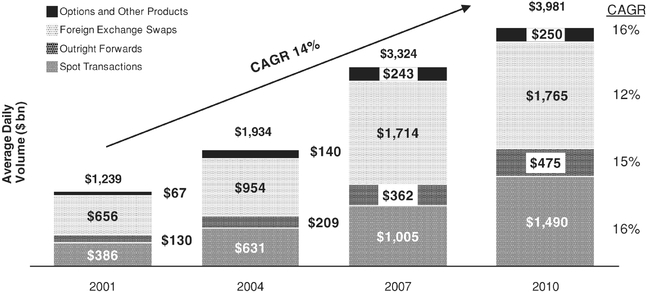

The global FX market is the largest and one of the fastest growing liquid markets in the world. Traders in this market include large banks, asset managers, hedge funds, central banks, broker-dealers, corporations, governments, other financial institutions and retail investors. According to the 2010 Triennial Central Bank Survey from the Bank for International Settlements, the average daily volume in the global FX market grew approximately 20%, from approximately $3.3 trillion in 2007 to approximately $4.0 trillion in 2010. The chart below highlights trends in the average daily volume and product mix in the FX market from 2001 to 2010.

3

Source: 2010 Triennial Central Bank Survey from the Bank for International Settlements

There are a variety of FX contracts. An FX spot trade is the exchange of one currency against another at an agreed rate for immediate delivery (generally two business days after the trade date). An FX forward (or outright forward) is an agreement to purchase or sell a set amount of a foreign currency at a specified price for delivery at a predetermined future date. An FX swap involves the actual exchange of two currencies (principal amount only) on a specific date at a rate agreed at the time of the conclusion of the contract (the short leg), and a reverse exchange of the same two currencies at a date further in the future at a rate (generally different from the rate applied to the short leg) agreed at the time of the contract (the long leg). An NDF is an FX forward contract that is net cash settled (often in U.S. dollars) upon expiration based on the difference between the contracted forward rate and the prevailing reference rate for the currency at maturity. In an NDF transaction, there is no physical exchange of currencies. An FX option is an agreement that provides the owner the right, but not the obligation, to purchase or sell a set amount of a foreign currency at a specified price for future delivery.

We believe that the increase in average daily FX trading volumes from 2001 to 2010 can be attributed to various factors, including: the rising importance of foreign exchange as an asset class, the increased trading activity of hedge funds and high frequency traders during this period and the growth of electronic execution methods, which have lowered transaction costs, increased market liquidity and attracted greater participation from many types of clients. In addition, the trading volumes of mutual funds, insurance companies, pension funds and other asset managers grew during this period, in part, as a result of increasing international assets under management. Corporations also continue to actively manage their FX exposure as their businesses expand globally. According to Standard and Poor's, foreign sales accounted for more than 40% of total 2010 revenues for S&P 500 companies that reported foreign sales in 2010. While we believe the long-term growth drivers of the FX industry remain intact, based on our own experience, FX volumes have recently been, and are expected to continue to be, adversely affected due to the uncertainties resulting from the current Eurozone crisis.

According to the Aite Group, the electronic FX trading market accounts for over 65% of total global FX volumes. The benefits of electronic FX trading include lower processing costs, an increased ability to audit, enhanced price transparency and greater access to liquidity. Additionally, electronic execution of FX trades makes post-trade processing easier and less manual. For these reasons, we expect electronic trading of FX to grow faster than the FX market overall.

4

A large majority of FX contracts trade OTC as opposed to being traded on an exchange. The OTC market offers deep liquidity with greater flexibility to tailor transaction terms, including amounts, settlement dates and execution mechanisms to fit the commercial requirements of diverse participants. The OTC FX market is also operationally efficient, with an extensive infrastructure developed by the industry over many years to facilitate trade processing, settlement and risk management of large trading volumes.

FX is traded OTC in a number of ways, including through multibank systems, single bank platforms, ECNs and interdealer platforms. Multibank systems enable trading with a number of different banks and other market participants on the same platform, as opposed to single bank platforms which are sponsored by a single liquidity provider and generally require clients to trade with that liquidity provider. ECNs provide a central limit order book where participants may trade on bids and offers from other participants, as well as enter their own bids and offers for display to the participants, typically anonymously. Interdealer platforms enable liquidity providers to hedge trading positions with each other.

Our Competitive Strengths

We believe that our competitive strengths include the following:

- •

- Market leader in the large and fast-growing electronic FX

market. We are a market leader in the largest, most liquid financial market in the world. We have been ranked as the top multibank and

independent platform by Euromoney magazine for ten consecutive years and as best independent online FX trading system by Global Finance magazine every year since 2005. Due to the size and liquidity of

the FX market, we anticipate significant growth in global FX volumes driven by increases in global trade, investments, and international assets under management, as well as new participants trading FX

and a demand for transparent markets. We believe that our deep pool of liquidity from a wide range of market participants creates a network effect that attracts more participants as it grows, leading

to increased transaction fees.

- •

- Comprehensive suite of award winning FX products and execution and workflow management

solutions. Our solutions cover the entire transaction cycle including pre trade, trade and post trade solutions. We deliver low-latency, resilient,

software-as-a-service trading platforms and workflow solutions to cater to the comprehensive and diverse needs of over 1,000 institutional clients globally. Our

range of relationship trading and active trading systems enable us to serve multiple market structures, including multi-bank, ECN and interdealer. Additionally, our white-labeled

enterprise solutions allow us to serve the single bank market. By processing trades electronically, our platform provides trade workflow automation for each stage in the trading cycle and supports

best practices with respect to trade execution, including competitive dealing, role-based permissioning, straight through processing, or "STP," automated confirmations and audit trails to

improve execution, control and risk management. We provide market participants with multiple trading mechanisms and our Settlement Center product provides comprehensive post trade processing to

enhance efficiency and reduce errors. We believe the quality and breadth of our products, execution services and trade workflow solutions are evidenced by the industry awards that we have received and

our strong customer satisfaction.

- •

- Blue-chip and diversified institutional client base. We have an impressive, diversified and blue-chip institutional client base consisting of asset managers, banks, broker dealers, corporations, hedge funds and prime brokers. As of December 31, 2011, our clients include 58 of the S&P Global 100, 132 of the Fortune 500, 55 of the top 100 European institutional asset managers, 27 of the top 100 U.S. institutional asset managers, six of the top ten hedge

5

- •

- Embedded and scalable technology. Our platform is embedded

in our clients' trading workflow and risk management controls making it central to their FX trading processes. We design our proprietary systems to be deployable, scalable, flexible, fast, and fault

tolerant. We have been issued five patents for our technology, and spend a significant amount enhancing our core technology base as well as our client facing systems. We provide a service that we

believe is financially compelling to both our liquidity providers and our market participant clients. The scalable nature of our technology allows us to add new clients in a cost-effective

manner, and has facilitated our rapid growth.

- •

- Trusted independent FX platform. We believe our

independence makes us a trustworthy partner for the institutional FX industry. Because we do not make markets, take positions or trade for our own account, clients trade FX on our platform and consult

with us regarding their execution strategies with the knowledge that we will not take principal positions against them and can offer unbiased information. We believe that this independence allows us

to be a preferred provider of FX trading technology, data and execution quality reports for institutional clients.

- •

- Proven and experienced management team. Since our inception, we have consistently been an innovator in the FX markets, introducing new functionality to our platform to meet the needs of institutional clients. Our management team consists of a number of seasoned executives who have been with us since our founding in 2000, as well as a number of respected executives with an average of 16 years of electronic trading industry experience. Our leadership team, led by Philip Z. Weisberg, has successfully built the leading independent electronic FX platform for institutional clients over the last 11 years. Mr. Weisberg has received numerous awards and other recognition, including Institutional Investor's 2011 "Tech 50" list of top innovators in financial technology, FX Week's 2011 e-FX Achievement Award, and Profit & Loss's 2011 "Hall of Fame," which recognize individuals who have made a significant contribution to the growth of the FX industry.

funds and all of the top 25 banks in the FX industry globally, with no single client accounting for more than 9% of total revenues. Our diversification across institutional client categories helps increase the stability of our trading volumes and revenues. We believe we are well-positioned to leverage our trading relationships to deliver liquidity and drive additional market share gains through the network effect. In addition, our broad buy-side distribution platform, spanning asset managers, corporate treasurers, active traders and market makers, provides us with unique insights into the FX market.

Our Growth Strategies

We plan to enhance our competitive position by increasing our volumes and market share as well as broadening our product set.

- •

- Increase our FX trading volumes and market share. We expect our FX volumes to benefit from the growth in overall electronic FX volumes. According to the 2010 Triennial Central Bank Survey from the Bank for International Settlements, the global FX market has grown at an average annual rate of 14% from 2001 to 2010, with overall growth in electronic volumes growing faster than the market. Even though we are one of the largest institutional FX trading platforms, our current market share represents only 2% of the global FX average daily trading volume of approximately $4.0 trillion. We plan to increase this share by continuing to grow our client base, and increasing the percentage of our clients' overall FX trading volume transacted on our platform. We believe we are uniquely positioned to serve every major category of institutional clients and to capture greater trading volumes as more firms seek to increase the sophistication of their FX trading capabilities.

6

- •

- Grow and maximize our existing institutional client

relationships. We believe that there are significant opportunities to cross-sell additional products to our existing

clients. Embedding more of our services with our clients will enable us to capture a greater percentage of their volume tradable through our platform and will result in incremental user fees, driving

revenues with little to no incremental investment. In addition, we seek to expand our presence within current clients to business units that do not currently transact through us. We also see another

large opportunity to grow our licensing of white-labeled technology to our many bank clients.

- •

- Expand our product offering. We intend to grow our

business by offering our clients additional products and features that are complementary to our existing suite of products, such as FX options. Additionally, we are creating more pre- and

post-trade services and workflow tools that we believe will be of interest to our clients. We plan to cross sell these new capabilities to existing clients, as well as use them as

competitive differentiators to attract new clients. These new products are expected to drive incremental trading volume through our systems, increasing and further diversifying our revenues.

- •

- Capitalize on opportunities related to regulatory

reform. Approximately 99% of our trading volume consists of institutional FX spot, FX forwards and FX swaps transactions, which are

generally exempt from regulation. Recent regulatory changes, such as the Dodd-Frank Wall Street Reform and Consumer Protection Act, or the "Dodd-Frank Act," will require the

centralized clearing of FX NDFs and FX options as well as execution through a regulated entity, such as a swap execution facility, or "SEF." We believe that our investments in technology and market

knowledge would facilitate our becoming a SEF. Accordingly, we believe that there is an opportunity to increase the products and services that we offer clients on our platform.

- •

- Pursue strategic alliances and acquisitions. We intend to selectively consider opportunities to grow through strategic alliances or acquisitions that are additive to our business. These opportunities may enhance our existing capabilities or enable us to enter new markets or provide new products or services, such as our acquisition of Lava Trading, Inc. ("LTI") in December 2009, which bolstered our active trading client base. We intend to focus on opportunities that we believe can enhance or benefit from our technology platform, provide significant market share and profitability and are consistent with our corporate culture. We believe that the establishment of a public trading market for our common stock will enhance our ability to pursue strategic opportunities by providing an additional form of currency with which to execute future acquisitions..

Our predecessor business, FX Alliance, LLC, was formed in the State of Delaware in June 2000. Our business was reincorporated as FX Alliance Inc. in the State of Delaware in September 2006.

Our principal executive offices are located at 909 Third Avenue, 10th Floor, New York, New York 10022. Our telephone number is (646) 268-9900. The address of our website is www.fxall.com.

Our Products and Services

We offer a variety of technology solutions that enable our institutional clients to view FX prices and execute transactions across over 400 currency pairs with selected counterparties in a manner of their choosing. Our systems are designed to execute transactions across a number of different FX products including FX spot, FX forwards, FX swaps and NDFs, as well as bank deposits and precious metals.

Our solutions can be accessed either through our front-end trading platform installed on the client's desktops, or via an application programming interface, or "API," providing a direct connection

7

to the client's own trading systems. Our products and services span pre trade, trade, and post trade activities and include trade workflow automation, risk management and compliance solutions and execution quality analysis.

FXall's Broad Range of Products and Capabilities

In addition to facilitating our clients' FX transactions, we also license our technology for distribution under our clients' brands, which we refer to as white-labeled enterprise solutions. We believe there is a significant opportunity to expand our enterprise solutions franchise over time based on our understanding of the workflow and technology, our expertise in delivering software-as-a-service, as well as our reputational credibility.

Our primary source of revenue is transaction fees from trade executions. We are also compensated for pre-trade and post-trade services through a combination of user fees for system access and support, trade confirmation and other post-trade events and other fees for premium services. Some of our services do not have fees associated with them, including basic market data, basic connectivity and STP, controls, basic reporting and analytics, but serve as features that attract customers to our platform.

8

Pre-Trade

Order and Execution Management

Prior to trading, clients may use our platform to prepare orders for execution using two systems:

- •

- Portfolio Order Management System, or "POMS": POMS allows

users to upload amounts to be purchased or sold, which we refer to as "trade requirements," directly through an integration with their treasury or order management system, import order files, copy and

paste orders from a spreadsheet, or manually input individual requirements. POMS includes a trading blotter for staging and execution of FX orders. The trading blotter enables users to automatically

group trade requirements and aggregate and net multiple requirements in the same currencies to simplify trading of a batch and minimize transaction costs.

- •

- Aggregator: Aggregator is an execution management tool providing the ability to execute orders dynamically at the best prices taking into account both (a) prices from liquidity providers using Bank Stream and (b) bids and offers displayed in Order Book. Users can control whether to trade on Bank Stream, Order Book, or both. Aggregator will determine and display the best bid and offer prices from the selected liquidity sources given a currency pair and order size. Users may enter limit orders that may be executed from either source.

Trade Execution

Our electronic trading execution platform provides single point access to multiple execution methods or trading mechanisms to meet the diverse needs of our institutional clients. Because different trading protocols are attractive to different types of clients and accommodate a range of FX products and market conditions, the diversity and flexibility of our protocols is a key differentiator.

- •

- Request for Stream (QuickTrade): Through QuickTrade, users

can submit a request for stream inquiry to obtain pricing from banks with which they have trading relationships to trade on a disclosed bilateral basis. Clients have the flexibility to trade FX spot,

swaps, forwards and NDFs in any currency pair, for any value date, in any amount and to select the best price from competing liquidity providers. QuickTrade users typically have identified a specific

trade requirement that they wish to cover immediately in a single transaction and typically have trading relationships with multiple liquidity providers.

- •

- Collaborative Trading: Our collaborative trading system

provides an efficient mechanism for trading complex batches of currencies which may comprise trade requirements in multiple currencies and value dates. When a user directs a batch to a liquidity

provider for pricing, a salesperson or trader at the liquidity provider can view and provide price quotes for the batch using our interface for liquidity providers, called Treasury Center.

Built-in chat functionality enables the client and salesperson to communicate special instructions or additional information. This collaborative approach is also effective when a client

wishes to transfer the risk of a large portfolio of trade requirements at one time or the participant and liquidity provider wish to negotiate terms online.

- •

- Dealer Proprietary Orders: Clients may execute trades using execution mechanisms proprietary to specific liquidity providers. Examples include benchmark fixings which apply algorithms to published FX prices to determine executable prices at pre-set times. Benchmark fixings provide the opportunity to trade large amounts at a competitive independently verified and efficient price.

Relationship Trading Mechanisms:

9

- •

- Continuous Stream (Bank Stream): Bank Stream provides the

ability to trade on continuous streaming spot prices in major currency pairs. A key benefit of Bank Stream is execution speed, which is important for clients who trade frequently in response to market

fluctuations. Trading on continuous streams is fast because the client has immediate access to the current price without needing to request a stream each time it trades. Like request for stream,

continuous stream enables the client to trade on a disclosed bilateral basis with multiple liquidity providers with whom the client has a trading relationship.

- •

- Anonymous Electronic Communications Network (Order

Book): Order Book allows clients to trade spot currencies by entering bids and offers for display to other participants, or by trading

on bids and offers from other participants. Clients may settle trades through a prime broker, which enables the client to trade without disclosing its identity to its counterparties. Using a prime

broker, clients have access to bids and offers from many other participants with whom the client does not have a trading relationship. Order Book is generally used by clients who seek to trade

currencies actively for a profit, rather than to hedge commercial risks. Order Book allows advanced order types to be placed such as, enhanced TWAP, limit, discretion, peg, reserve and hidden

orders.

- •

- Interdealer Trading: We connect dealers to liquidity from other dealers, enabling dealers to hedge positions and manage currency exposures generated by their market making activity. Interdealer trading uses Order Book including advanced order types effective for block trading.

Active Trading Mechanisms:

Post-Trade

Settlement Center

Clients use our Settlement Center to manage post-trade messaging with a network of approximately 390 bank settlement counterparties, custodians and prime brokers. Settlement Center does not settle trades itself; it facilitates settlement between clients by creating trade confirmations, matching trades, determining settlement paths, managing settlement instructions, automatically generating settlement netting payments, determining eligibility for CLS Bank settlement, and delivering secure third-party notifications. Our trading systems and Settlement Center support trades split into multiple allocations for settlement purposes, an important feature for asset managers responsible for trading on behalf of multiple funds or separate accounts. Users can automatically book trades after execution for real-time STP. Settlement Center supports trades executed on FXall as well as trades not executed on FXall.

Other Products and Features

Our other products and features support or enable our clients' trading activities. We are compensated for these products and features through standalone fees or indirectly, through transaction fees.

Market Data

We provide our trading clients with comprehensive real-time market data, including: indicative bids and offers on over 80 currency pairs and over 2,300 calculated crosses; spot rates as well as forward points for multiple tenors from one week to one year; and access to all executable Order Book bids and offers, including amounts and rates. Market data is available through APIs or graphical user interfaces, or "GUIs."

10

Connectivity and Straight-Through Processing

We provide integration tools that provide connectivity and STP to and from our clients' enterprise systems to increase efficiency and control in their trade and operational workflows. STP allows a client to upload its orders and trade requirements automatically to our trading system where they can trade. After trades are complete, STP delivers trade execution details to the client's systems. We support multiple standard and customized proprietary formats to meet our clients' needs.

- •

- Financial Information Exchange, or "FIX": Our FIX

messaging gateway provides clients with a fast and cost-effective means of integrating FXall with the client's trading systems. The FIX protocol is an industry-standard series of messaging

specifications for the electronic communication of trade-related messages.

- •

- Application Programming Interface: Clients not accessing

our GUI can access FXall liquidity using our proprietary trading API. Trade requirements from order management systems can be programmed to be executed automatically. Systematic traders can use the

API to fully automate the execution of their FX trading strategies.

- •

- QuickConnect: For clients who do not use FIX or

proprietary APIs, we offer an STP solution that interprets varied public and proprietary message formats to automate trading workflows between treasury and portfolio management

systems.

- •

- Partner Channel Program: We established our Partner Channel Program to offer clients access to a network of approximately 50 qualified sell-side and buy-side system technology vendors who work with us to provide superior levels of workflow and STP solutions for mutual clients. A dedicated integration team works with clients, vendors and integration consultants that include the leading treasury and order management system providers, aggregators and connectivity providers to streamline the FX trading and settlement process. New vendors are added in response to client requests and market research.

Controls

Our robust, flexible role-based permissioning and approval tools let clients establish multiple levels of segregation to help enforce compliance with the client's trade preparation, review and authorization procedures.

Reporting and Analytical Tools

We deliver clients a wide range of reporting analytics to assist in tracking and evaluating trade execution activity and quality, including full audit trail reports and execution performance reviews.

All clients have access to a basic reporting and analytics package that covers administration, which provides details around accounts, users, user entitlements, trading limits and standard audit reports around the set-up of accounts and mappings by provider. Additional details are provided relating to client billing, trade activity details, and Settlement Center analysis including review of settlement instructions. Specific reports include trade activity analysis, details of unmatched deals, client savings, money market summary, prime broker summary, and deal and time analysis. We also provide a trading summary of activity by liquidity provider. Trade ticket details are available with full audit trail.

- •

- Execution Quality Analysis, or "EQA": EQA is our comprehensive proprietary reporting tool available to clients on a monthly or quarterly basis to analyze the client's historical trading activity on FXall to provide insight into the client's trading strategies and highlight opportunities to improve performance. Analyses include currency pair and provider volume distributions, spreads by time of day, trades compared to the day's high-low range and benchmark fixing rates, response times, provider breakdowns, and netting opportunities.

11

White-labeled Enterprise Solutions

We license our systems on a white-labeled basis to large financial institutions. The systems available for white labeling include:

- •

- Customer Order Management System, or "COMS": COMS allows

bank sales and trading teams to automate the handling of their institutional client orders for spot FX, NDFs and precious metals through real-time blotter windows that effectively monitor

client order activity.

- •

- FXone White Label: FXone White Label is a

full-trade lifecycle solution designed to meet the FX trading needs of banks' internal customers. Banks maintain full ownership of client relationships as the front-end

execution technology provided by us is bank branded. FXone enables banks to offer clients a highly-developed foreign exchange trading solution without paying to develop and support the

product.

- •

- Internal Matching Technology: Using our Order Book trade matching technology, a bank can manage a proprietary liquidity pool, with liquidity from multiple sources. Internal matching reduces the number of external trade requirements resulting in lower transaction costs and fewer operational risks. The bank can also make the internal liquidity pool available to select clients via an API or GUI connection.

Sales and Marketing

We promote our products and services through direct and indirect sales and marketing strategies. Our global staff of 55 sales and relationship management professionals is responsible for promoting the benefits of electronic foreign exchange trading, attracting new clients and increasing use of our services by our existing clients. The sales and relationship management team is organized geographically, with staff in New York, Boston, London, Zurich, Tokyo, Singapore, Hong Kong, Mumbai and Sydney. Commission programs provide incentives for sales persons and relationship managers to grow trading volumes and revenues from their clients. We employ various strategies including advertising, direct marketing programs, participation in industry conferences and dedicated client events to increase awareness of our brand and our electronic trading platform. We also provide market data on a daily basis through our public website. Additionally we look to educate the market about the benefits of our end-to-end workflow solutions as an industry best practice through publications, webinars and public relations efforts. Our marketing and communications team, located in New York and London, supports these efforts.

Customer Service

Our Client Interaction Center, or "CIC," provides a central resource for customer support and provides 24-hour coverage during the trading week with professional staff in three centers: London, New York and Singapore. The CIC team answers client inquiries via telephone, email and live chat, and tracks service requests using a ticketing and client relationship management system. The CIC works with our application support team to monitor and support the platform.

Technology and Infrastructure

All of our systems are built to be deployable, scalable, flexible, fast and fault tolerant. Our core software solutions span the trading lifecycle and include order management, execution management, trading, post-trade confirmation and messaging, reporting and analytics, connectivity and straight-through processing. Our front-end user interfaces are desktop applications so that our users can experience high-fidelity solutions with advanced functionality. We also offer APIs for high-performance computer-to-computer capabilities. These APIs are typically geared towards our liquidity providers and

12

users of our active trading systems. Our server-side applications are high-performance, scalable applications that are monitored and scaled to provide the performance and capacity that tracks our growth. We regularly test our systems' performance and capacity to handle projected volumes. We utilize load-balancing technologies and clustered storage and computing solutions to guard against workflows lacking sufficient compute cycles.

A significant portion of our operating budget is dedicated to system design, development, and operations in order to achieve high levels of overall system performance. We continually monitor our performance metrics and upgrade our capacity configurations and requirements to handle anticipated peak transactions in our highest volume products.

Distribution and Connectivity

Our electronic trading platform is accessible via the Internet. Additionally, our latency-sensitive clients and liquidity providers have the option to connect directly to our matching engines by co-locating their routing engines in our data center to remove the latency of the Internet. These methods of connectivity have allowed us to connect to over 1,000 buy-side clients, as well as 84 active liquidity providers.

Product Development and Architecture Principles

We are deploying the Agile product development approach that facilitates continuous releases of the most important product features. This approach allows us to be opportunistic in what we decide to release at any point in time, and to not wait until less important features are delivered before we realize the benefits of the key features. Agile product development also allows us to inject newly identified opportunities into the product lifecycle without being disruptive to the development process.

Our current architectural principles are based on providing high performance and scalability, while making operations easy to monitor and control. We have designed our own enterprise platform to which every business component is intended to connect. Our objective is that every platform component is able to communicate with the other components and that if any communications are dropped for whatever reason, they can be recovered on-demand. The goal is to provide absolute fault-tolerance and real-time scalability. Each new business component we add to the infrastructure is completely independent of the other components, and has discrete operations to perform. Using our architectural principles, every new component is built to scale on demand and has detailed monitoring and command capabilities.

Security and Disaster Recovery

Physical and digital security is critical to our business. We utilize physical access controls at all of our offices and data centers. We employ digital security technologies and processes, including encryption technologies, multiple firewalls, VLANs, authentication technologies, intrusion detection and internal access controls.

At the network level, we have multiple levels of firewalls and virtual networks. We also limit access to white-listed internet protocol addresses to ensure that only designated clients (by IP address) have access to the appropriate level of network access. We have also incorporated several protective features into our electronic trading applications to authenticate users and limit data distribution to exact provisioning entitlements. We constantly monitor connectivity, and our global Operations team is alerted if there are any suspect events. Users are issued unique IDs and passwords, and must authenticate themselves to make changes or reset passwords.

13

In case of a catastrophic failure, we would seek to operate out of our secondary data center. Our back-up site has constant data replication, and in the event of an emergency, we would redirect connectivity to that site.

Transaction data is archived and backed up at secure off-site locations, and we maintain at least five years of such data.

Technology Partners, Vendors and Suppliers

We utilize a host of external technology partners, vendors and suppliers. These services include staff augmentation, software licensing, hosting facilities and continuous learning. If, however, any of our contracts with key partners are terminated, we believe that we would be able to gain access to products and services of comparable quality.

Research & Development

Our research and development activity primarily relates to software and other system improvements to our platform, including investments that seek to improve functionality, speed, capacity or reliability. We capitalize employee compensation, related benefits and consultant's costs that are engaged in software development that is used for internal use. Research and development expenditures were $9.4 million, $7.4 million and $4.9 million for the years ended December 31, 2011, 2010 and 2009, respectively.

Intellectual Property

We rely on a combination of trademark, copyright, trade secret and fair business practice laws in the United States and other jurisdictions to protect our proprietary technology, intellectual property rights and our brand. We have been issued five patents for our technology, and spend a significant amount enhancing our core technology and client facing systems. We also own a number of registered foreign trademarks and service marks. Our practice is to apply for patents with respect to our technology and seek trademark registration for our marks from time to time when management determines that it is competitively advantageous and cost effective for us to do so. In that regard, we have not registered all the marks that we use, and it is possible that a third party may have registered marks that we use. We also enter into confidentiality and invention assignment agreements with our employees and consultants and confidentiality agreements with other third parties and rigorously control access to proprietary technology.

Competition

The electronic trading industry is highly competitive and we expect competition to intensify in the future. In general, we compete on the basis of a number of key factors, including: the liquidity available through the platform; the quality and speed of execution; total transaction costs; technology capabilities, including the ease of use of our electronic trading platform; and range of products and services offered.

We face five main areas of competition:

- •

- Single bank systems: The major global and regional investment and commercial banks offer institutional clients electronic FX trade execution through proprietary systems branded with the banks' names. Many of these banks expend considerable resources on product development, sales and support to promote their single-bank systems. The single-bank FX systems may be offered as part of a multi-product offering, including fixed income securities, commodities and derivatives.

14

- •

- Other multi-bank, interdealer and ECN electronic trading

platforms: There are numerous other electronic trading platforms. These include ICAP through its EBS offering; Reuters; FX Connect and

Currenex, both owned by State Street Bank; BGC Partners through its eSpeed offering; Knight Capital through its Hotspot offering; 360T Trading Networks; Integral Development Corp. and others.

- •

- Telephone: We compete with FX business conducted over the

telephone between banks and broker-dealers and their institutional clients. Institutional clients have historically purchased foreign currencies by telephoning FX sales professionals at one or more

banks or broker-dealers and inquiring about the price and market liquidity of currencies. Non-electronic trading including by voice remains the manner in which approximately 35% of FX

trades are conducted between market participants, according to a 2010 report by Aite Group.

- •

- Market data and information vendors: Several large market

data and information providers currently have a presence on a large number of institutional trading desks, including Bloomberg and Reuters. Some of these entities currently offer varying forms of

electronic trading of FX.

- •

- Interdealer voice brokers: The major interdealer brokers offer voice broking between banks in FX products, including FX forwards, NDFs and options. Many of these firms have developed or may develop electronic trading systems. While they are primarily focused on interdealer trading, they may in the future offer their services to non-dealer clients.

We believe that we compete favorably with respect to these factors and we continue to build technology solutions that serve the needs of the FX markets. We target primarily institutional customers who value the ability to be presented with prices from multiple liquidity sources, or to present prices to multiple market participants, for a potential transaction. Our competitive position is also enhanced by the breadth of our trade workflow functionality that covers the entire transaction cycle including pre-trade, trade and post-trade solutions. Since our founding in 2000, we have steadily added and improved trade workflow tools to address the comprehensive and diverse needs of various segments of our institutional client base. We deliver low-latency, resilient, software-as-a-service trading platforms and workflow solutions to cater to over 1,000 institutional clients globally. By processing trades electronically, our platform provides trade workflow automation for each stage in the trading cycle and supports best practices with respect to trade execution, including competitive dealing, role-based permissioning, STP, automated confirmations and audit trails to improve execution, control and risk management. We provide market participants with multiple trading mechanisms and our Settlement Center product provides comprehensive post-trade processing to enhance efficiency and reduce errors.

Many of our current and potential competitors are more established and substantially larger than we are, and have substantially greater market presence, as well as greater financial, engineering, technical, marketing and other resources. These competitors may reduce their pricing to enter into market segments in which we have a leadership position today, potentially subsidizing any losses with profits from trading in other securities. In addition, many of our competitors offer a wider range of services, have broader name recognition and have larger client bases than we do. Some of them may be able to respond more quickly to new or evolving opportunities, technologies and client requirements than we can and may be able to undertake more extensive promotional activities.

Any combination of our competitors or our current broker-dealer clients may enter into joint ventures or consortia to provide services similar to those provided by us. Current and new competitors may be able to launch new platforms at a relatively low cost. Others may acquire the capabilities necessary to compete with us through acquisitions. Significant consolidation has occurred in our industry and these firms, as well as others that may undertake such consolidation in the future, are potential competitors.

15

Regulation

Overview

Our operating subsidiaries are regulated in a number of jurisdictions, including the United States, the United Kingdom (where our registration with the Financial Services Authority has been "passported" to a number of European Economic Area jurisdictions), Hong Kong, India and Australia. In these jurisdictions, government regulators and self-regulatory organizations oversee the conduct of our business; several have the ability to conduct examinations to monitor our compliance with applicable statutes and regulations. In addition, in two jurisdictions in which we are currently regulated, certain of our subsidiaries are subject to minimum regulatory capital requirements.

U.S. Regulation

In the United States, foreign exchange trading activities are regulated by the CFTC under authority conveyed by the Commodities Exchange Act, or the "CEA." Generally, foreign exchange trading conducted by "eligible contract participants" (as defined in the CEA) is exempt from the provisions of the CEA. As noted above, our client base is institutional, and within the United States those institutional clients have also represented to us that they are eligible contract participants. Accordingly, our operations are currently exempt from the CFTC's regulations under the CEA.

The Dodd-Frank Act introduces significant changes to financial industry regulation, including a wholesale change to the regulation of derivatives. Title VII of the Dodd-Frank Act, among other things, provides for the registration and comprehensive regulation of swap dealers and major swap participants; imposes clearing and trade execution requirements on swaps; creates recordkeeping and real-time reporting regimes; and enhances the CFTC's rulemaking and enforcement authorities with respect to all registered entities and intermediaries subject to the CFTC's oversight.

The Dodd-Frank Act includes "foreign exchange swaps" and "foreign exchange forwards" in the definition of "swap" for Title VII purposes but allows the Treasury Secretary, after making certain findings, to exempt these products from the clearing requirements of the swap regulation. The Treasury Secretary has proposed such an exemption but has not yet finalized it. Even if the Treasury Secretary does exempt "foreign exchange swaps" and "foreign exchange forwards" from the definition of "swap" for most purposes, some products currently traded on our platforms or that may be traded on our platforms in the future are unlikely to qualify for the exemption. In particular, we believe that NDFs and FX options will both be considered swaps and will not qualify for the exemption.

The Dodd-Frank Act amended the CEA to mandate that if a swap is required to be cleared, it must be executed on a registered trading platform, i.e., a SEF or designated contract market, or "DCM," unless no SEF or DCM makes the swap available to trade. The Dodd-Frank Act outlines a comprehensive regulatory regime for SEFs. On January 7, 2011, the CFTC published a proposed rule that would require SEFs to, among other things: comply with significant self-regulatory duties; establish, monitor, enforce and investigate violations of trading rules, trade processing rules and participant rules; report trade information to the CFTC, swap data repositories and the public; maintain automated trade surveillance systems and audit trail programs; maintain business continuity and emergency authority plans; and appoint chief compliance officers. Furthermore, registered SEFs will also be subject to certain capital requirements (see "—Net Capital Requirements" discussion below).

The only instruments we currently offer that would likely be considered swaps subject to the trade execution requirements are NDFs, which currently comprise approximately 1% of our trading volume worldwide. FX options, which we are planning to launch, would also likely be considered swaps subject to the trade execution requirements.

We believe that the Dodd-Frank Act will likely have a significant impact on the derivatives trading markets generally, including the foreign exchange markets in which we operate. The

16

Dodd-Frank Act may affect the ability of FX clients to do business or affect the prices and terms on which they do business. The Dodd-Frank Act may also affect the structure, size, depth and liquidity of the FX markets generally. These effects may adversely impact our ability to provide our services to our clients and could have an adverse effect on our business and profitability.

International Regulation

Outside the United States, we are regulated by, among others:

- •

- the Financial Services Authority in the United Kingdom;

- •

- the Hong Kong Monetary Authority in Hong Kong;

- •

- the Australian Securities and Investment Commission in Australia; and

- •

- the Foreign Exchange Dealers Association of India in India.

The European Economic Area has been examining practices in the derivatives markets. The European Parliament and the European Commission have proposed a Regulation on OTC derivatives, central counterparties and trade repositories that will require central clearing of OTC derivatives. We anticipate that the European Parliament and the European Commission will propose a revision to the Markets in Financial Instruments Directive, or "MiFID II," that will address the trading of derivatives, but we expect that MiFID II will follow the lead of the United States and the Proposed Treasury Determination and exempt all foreign exchange instruments from its coverage except for foreign exchange NDFs and foreign exchange options.

Although the developments in the European Economic Area lag somewhat the analogous developments in the United States, we believe that they will likely have significant impact on the derivatives trading markets, including the foreign exchange markets in which we operate. Like the Dodd-Frank Act, they may affect the ability of our clients to do business, the prices and terms on which our clients do business, and the structure, size, depth and liquidity of the FX markets generally. These effects may adversely impact our ability to provide our services to our clients and could have an adverse effect on our business and profitability.

In jurisdictions in which we are not regulated by governmental bodies and/or self-regulatory organizations, we conduct our business in a manner which we believe is in compliance with applicable local law but which does not require local registration, licensing or authorization. In any such jurisdiction, there is a possibility that a regulatory authority could assert jurisdiction over our extraterritorial activities and seek to subject us to the laws, rules and regulations of that jurisdiction. The conclusion that the conduct of our business in any such jurisdiction does not require local registration, licensing or authorization is often premised on any of the following factors: our clients are professional, sophisticated, high net worth institutions; we do not maintain a presence (such as an office or data center) in the jurisdiction; we do not act as principal/counterparty to our clients in transactions; we do not hold clients' assets; and we act only as an "arranger" of transactions between counterparties.

We have consulted with local legal counsel for advice regarding whether we are operating in compliance with local laws and regulations (including whether we are required to be licensed or authorized in such local jurisdiction). We are exposed to the risk that our legal and regulatory analysis is subsequently determined by a local regulatory agency or other authority to be incorrect and that we have not been in compliance with local laws or regulations (including local licensing or authorization requirements) and to the risk that the regulatory environment in a jurisdiction may change. In any of these circumstances, we may be subject to sanctions, fines and restrictions on our business or other civil or criminal penalties. Any such action in one jurisdiction could also trigger similar actions in other jurisdictions. We may also be required to cease the conduct of business with clients in any such

17

jurisdiction and/or we may determine that compliance with the laws or licensing, authorization or other regulatory requirements for continuance of the business are too onerous to justify making the necessary changes to continue that business. In addition, any such event could impact our relationship with the regulators or self-regulatory organizations in the jurisdictions where we are subject to regulation, including our regulatory compliance or authorizations.

Net Capital Requirements

Certain of our subsidiaries are subject to jurisdictional specific minimum net capital requirements, designed to maintain the general financial integrity and liquidity of a regulated entity. In general, net capital requirements require that at least a minimum specified amount of a regulated entity's assets be kept in relatively liquid form, usually cash or cash equivalents. Net capital is generally defined as net worth, assets minus liabilities, plus qualifying subordinated borrowings and discretionary liabilities, and less mandatory deductions that result from excluding assets that are not readily convertible into cash and from valuing conservatively other assets.

If a firm fails to maintain the minimum required net capital, its regulator and the self-regulatory organization may suspend or revoke its registration and ultimately could require its liquidation. The net capital requirements may prohibit payment of dividends, redemption of stock, prepayment of subordinated indebtedness and issuance of any unsecured advance or loan to a stockholder, employee or affiliate, if the payment would reduce the firm's net capital below minimum required levels.

As of December 31, 2011, we had $1.0 million in regulatory capital requirements at our regulated subsidiaries, the majority of which related to our India subsidiary. We remain relatively unregulated in the United States and do not presently have any regulatory capital requirements in the United States. We anticipate that the implementation of the regulations to be adopted by the CFTC in respect of SEFs will require us to maintain adequate capital in respect of any SEF we establish. In general, the regulatory capital required for a SEF would be an amount equal to the SEF's annual operating expenses, determined on a rolling one-year basis.

Employees

As of December 31, 2011, we had a total of 205 full-time employees and 34 full-time contractors, of which 171 were based in the United States and 68 of which were based outside the United States. None of our employees are covered by collective bargaining agreements. We believe that our relations with our employees are good.

Available Information

We maintain a website at www.fxall.com. The information on or available through our website is not, and should not be considered, a part of this report. You may access our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to these reports, as well as other reports relating to us that are filed with or furnished to the Securities and Exchange commission (or "SEC") free of charge at our website as soon as reasonably practicable after such material is electronically filed with, or furnished to, the SEC. In addition, you may read and copy any materials we file with the SEC at the SEC's Public Reference Room at 450 Fifth Street, N.W., Washington, DC 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC also maintains an Internet site, www.sec.gov, that contains reports, proxy and information statements, and other information that we file electronically with the SEC.

18

You should carefully consider the following risk factors, which we believe are the most significant risks related to our business, as well as the other information contained in this document.

Risks Related to Our Business

Our revenues and profitability are influenced by FX trading volume and currency volatility, which are directly impacted by domestic and international market and economic conditions that are beyond our control.

During the past few years, there has been significant disruption and volatility in the global financial markets. Many countries, including the United States, have recently experienced recessionary conditions. Our revenues are influenced by the general level of trading activity in the FX market. Our revenues and operating results may vary significantly from period to period due primarily to movements and trends in the world's currency markets and to fluctuations in trading levels. While we have generally experienced greater trading volume in periods of volatile currency markets, volatility may be associated with other market factors such as a decline in equity values, credit markets and liquidity, which lead to lower trading volumes. For example, we experienced a decrease in total average daily trading volumes of approximately 7% in the fourth fiscal quarter of 2011 as compared to the prior quarter, including a 3% decline in relationship trading and a 20% decline in active trading. We believe this decrease was consistent with industry trends as a result of the Eurozone crisis, which has created uncertainty in the FX and more general trading environment. We expect these conditions to continue in the near term into 2012 pending additional certainty as to the resolution of the crisis. See "—The current economic environment and uncertainty in the European Union could materially adversely affect our results of operations." In the event we experience lower levels of trading volume, our revenues and profitability will be negatively affected.

Like other financial services firms, our business and profitability are directly affected by elements that are beyond our control, such as economic and political conditions, broad trends in business and finance, changes in the volume of foreign currency transactions, changes in supply and demand for currencies, movements in currency exchange rates, changes in the level of global trade and investment, changes in the value of international assets under management, changes in the financial strength of market participants, legislative and regulatory changes, changes in the markets in which such transactions occur, changes in how such transactions are processed and other market disruptions. Any one or more of these factors, or other factors, may adversely affect our business and results of operations and cash flows. A weakness in equity markets, such as the recent economic slowdown, could result in reduced trading activity in the FX market and, therefore, could have a material adverse effect on our business, financial condition, results of operations and cash flows. As a result, period-to-period comparisons of our operating results may not be meaningful and our future operating results may be subject to significant fluctuations or declines.

The current economic environment and uncertainty in the European Union could materially adversely affect our results of operations.

The failure of the European Union to stabilize the fiscal condition and creditworthiness of its member economies, such as Greece, Portugal, Spain, Ireland, and Italy, could have significant implications on FX trading markets and on financial institutions, including many of our clients, particularly in the active trading business. Certain European Union member states have significant fiscal obligations, which has caused investor concern over such countries' ability to continue to service their debt and foster economic growth. Currently, the European debt crisis has caused liquidity to be less abundant. A weaker European economy has caused and may continue to cause market participants to lose confidence in the safety and soundness of European financial institutions and the stability of European Union member economies, and may likewise affect other global institutions and the stability of the global financial markets.

19

Given that our business is significantly dependent on the availability of liquidity on our platform and the willingness of financial institutions to trade with one another, such uncertainty and reductions in liquidity and trading could have a material impact on our business and volumes in future periods. For example, we experienced a decrease in total average daily trading volumes of approximately 7% in the fourth fiscal quarter of 2011 as compared to the prior quarter, including a 3% decline in relationship trading and a 20% decline in active trading. We believe this decrease was consistent with industry trends as a result of the Eurozone crisis, which has created uncertainty in the FX and more general trading environment. We expect these conditions to continue in the near term into 2012 pending additional certainty as to the resolution of the crisis.

In addition, the possible abandonment of the Euro currency by one or more members of the European Union could materially affect our business in the future. Despite measures taken by the European Union to provide funding to certain European Union member states in financial difficulties and by a number of European countries to stabilize their economies and reduce their debt burdens, it is possible that the Euro could be abandoned as a currency in the future by countries that have already adopted its use. This could lead to the re-introduction of individual currencies in one or more European Union member states, or in more extreme circumstances, the dissolution of the European Union. The effects on our business of a potential dissolution of the European Union, the exit of one or more European Union member states from the European Union or the abandonment of the Euro as a currency, are impossible to predict, and any such events could have a material adverse effect on our business, trading volumes and results of operations, particularly in the near term.

We face significant competition. Many of our competitors and potential competitors have larger client bases, more established brand recognition and greater financial, marketing, technological and personnel resources than we do, which could put us at a competitive disadvantage. In addition, certain of our existing bank stockholders currently have investments in and may make future investments in FX platforms or similar businesses that compete with us.

We compete with single bank systems, other multibank, interdealer and ECN electronic trading platforms, telephone brokers and various other forms of competition. Furthermore, certain of our existing bank stockholders or their affiliates, as is typical for a large number of major banks, already have their own single bank or other competing FX trading platforms and frequently invest in and acquire ownership interests in similar businesses and these businesses may compete with us. We compete in the market for FX trading based on our ability to provide a trading platform with deep liquidity, competitive prices and comprehensive pre-trade, trade and post-trade functionality, to retain our existing clients and to attract new clients. Certain of our competitors, particularly certain non-independent platforms, have larger client bases, more established name recognition, a greater market share in certain markets or client categories, and greater financial, marketing, technological and personnel resources than we do. These advantages may enable them, among other things, to:

- •

- develop products and services that are similar to ours, or that are more attractive to clients than ours, in one or more

of our markets;

- •

- provide products and services we do not offer;

- •

- provide execution and clearing services that are more rapid, reliable or efficient, or less expensive than ours;

- •

- offer products and services at prices below ours to gain market share and to promote other businesses, such as listed FX

futures and options contracts, contracts for difference, including contracts for precious metals, energy and stock indices, and OTC derivatives;

- •

- adapt at a faster rate to market conditions, new technologies and client demands;

- •

- offer better, faster and more reliable technology;

20

- •

- outbid us for desirable acquisition targets;

- •

- market, promote and sell their products and services more effectively; and

- •

- develop stronger relationships with clients.

We may not be able to compete effectively against these firms, particularly those with greater financial resources, and our failure to do so could materially and adversely affect our business, financial condition and results of operations and cash flows. In addition, our existing bank stockholders may decide to invest in or shift business to alternative trading platforms, which could have an adverse effect on our business.

System failures could cause interruptions in our services or decreases in the responsiveness of our services, which could harm our business.

Our ability to facilitate transactions successfully and provide high quality customer service depends on the efficient and uninterrupted operation of our computer and communications hardware and software systems. If our systems fail to perform as we expect, we could experience disruptions in our operations, prolonged trading outages, slower response times or decreased customer service and customer satisfaction. Our systems, including our data centers, also are vulnerable to damage or interruption from human error, natural disasters, fires, acts of terrorism, power loss, telecommunication failures, break-ins, security breaches, sabotage, computer viruses, intentional acts of vandalism and similar events. We do not have fully redundant capabilities. While we currently maintain a disaster recovery plan, which is intended to minimize service interruptions and secure data integrity, such plan may not work effectively during an emergency. In addition, system failures could take an extended period of time to remediate. Any system failure that causes an interruption in our services, decreases the responsiveness of our services or affects access to our platform and services could adversely impact our reputation, damage our brand name and materially adversely affect our business, financial condition and results of operations and cash flows.

Our computer infrastructure may be vulnerable to security breaches. Any such problems could jeopardize confidential information transmitted over the Internet, cause interruptions in our operations or give rise to liabilities to third parties.