Attached files

| file | filename |

|---|---|

| EX-10.43 - EX-10.43 - TANGOE INC | a2208198zex-10_43.htm |

| EX-10.36 - EX-10.36 - TANGOE INC | a2208198zex-10_36.htm |

| EX-23.2 - EX-23.2 - TANGOE INC | a2208198zex-23_2.htm |

| EX-1.1 - EX-1.1 - TANGOE INC | a2208198zex-1_1.htm |

| EX-23.1 - EX-23.1 - TANGOE INC | a2208198zex-23_1.htm |

| EX-23.4 - EX-23.4 - TANGOE INC | a2208198zex-23_4.htm |

| EX-23.3 - EX-23.3 - TANGOE INC | a2208198zex-23_3.htm |

| EX-5.1 - EX-5.1 - TANGOE INC | a2208198zex-5_1.htm |

As filed with the Securities and Exchange Commission on March 23, 2012

Registration No. 333-180044

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

Amendment No. 1

to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

TANGOE, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 7372 | 06-1571143 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(IRS Employer Identification No.) |

35 Executive Boulevard

Orange, Connecticut 06477

(203) 859-9300

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

Albert R. Subbloie, Jr.

President and Chief Executive Officer

35 Executive Boulevard

Orange, Connecticut 06477

(203) 859-9300

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||

| John A. Burgess, Esq. David A. Westenberg, Esq. Wilmer Cutler Pickering Hale and Dorr LLP 60 State Street Boston, Massachusetts 02109 (617) 526-6000 |

Mark L. Johnson, Esq. Damien A. Grierson, Esq. Cooley LLP 500 Boylston Street, 14th Floor Boston, Massachusetts 02116 (617) 937-2300 |

|

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, Dated March 23, 2012

Tangoe, Inc.

8,000,000 Shares

Common Stock

We are offering 2,200,000 shares of our common stock. Selling stockholders, including executive officers, are offering an additional 5,800,000 shares of our common stock. We will not receive any proceeds from the sale of shares by the selling stockholders. Our common stock is listed on The NASDAQ Global Market under the symbol "TNGO."

On March 21, 2012, the last reported sale price of our common stock as reported on The NASDAQ Global Market was $17.57 per share.

Investing in our common stock involves risk. See "Risk Factors" beginning on page 10.

Neither the Securities and Exchange Commission nor any state securities commission or other regulatory body has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

| |

Per share |

Total |

||

|---|---|---|---|---|

Public offering price |

$ | $ | ||

Underwriting discounts and commissions |

$ | $ | ||

Proceeds, before expenses, to Tangoe, Inc. |

$ | $ | ||

Proceeds, before expenses, to the selling stockholders |

$ | $ |

The selling stockholders have granted the underwriters an option to purchase up to 1,200,000 additional shares of common stock.

| Deutsche Bank Securities | Barclays | Stifel Nicolaus Weisel | ||

Lazard Capital Markets |

||||

The date of this prospectus is , 2012.

This summary highlights information contained elsewhere in this prospectus. You should read the following summary together with the more detailed information appearing in this prospectus, including our consolidated financial statements and related notes, and the risk factors beginning on page 10, before deciding whether to purchase shares of our common stock. Unless the context otherwise requires, we use the terms "Tangoe," "our company," we," "us" and "our" in this prospectus to refer to Tangoe, Inc. and its subsidiaries.

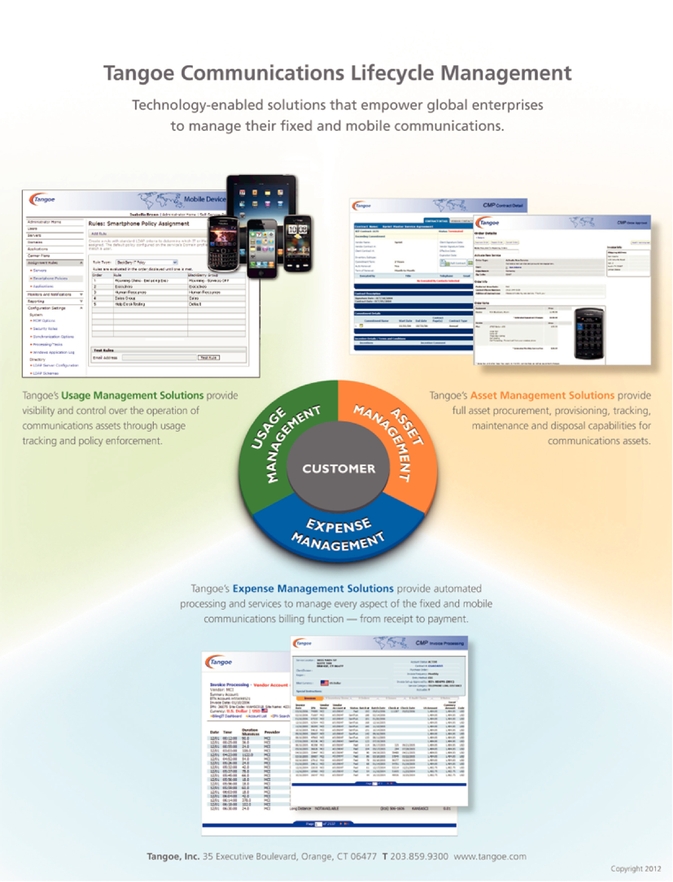

Tangoe is a leading global provider of communications lifecycle management, or CLM, software and services to a wide range of enterprises, including large and medium-sized businesses and other organizations. CLM encompasses the entire lifecycle of an enterprise's communications assets and services, including planning and sourcing, procurement and provisioning, inventory and usage management, mobile device management, invoice processing, expense allocation and accounting, and asset decommissioning and disposal. Our on-demand Communications Management Platform is a suite of software designed to manage and optimize the complex processes and expenses associated with this lifecycle for both fixed and mobile communications assets and services. Our customers can engage us through our client services group to manage their communications assets and services using our Communications Management Platform.

Our solution can provide a significant return on investment by enabling an enterprise to identify and resolve billing errors, to optimize communications service plans for its usage patterns and needs, to manage used and unused communications assets and services and to proactively monitor and prevent mobile bill overages. Our solution allows enterprises to improve the productivity of their employees by automating the provisioning of communications assets and services, and to reduce costs by controlling and allocating communications expenses. It also allows enterprises to enforce regulatory requirements and internal policies governing the use of communications assets and services.

In the year ended December 31, 2011, our total revenue increased 53% to $104.9 million over the prior year and revenue from our recurring technology and services increased 62% to $93.7 million over the same period. We sell our on-demand software and related services primarily on a subscription basis under contracts that typically have terms ranging from 24 to 60 months. We also provide strategic consulting services. As of December 31, 2011, we had more than 750 end customers.

Industry Background and Trends

An enterprise's communications infrastructure can be critical to nearly every aspect of its operations. In the past, communications infrastructures were largely fixed, consisting of telephones, lines, circuits, switches and fixed networks. These infrastructures have expanded to encompass a growing number of diverse technologies and assets, including Voice over IP, virtual networking, converged voice and data communications, mobile computing, video conferencing, text messaging and mobile devices. These advances in communications technologies and the proliferation of mobile devices have greatly increased the financial and personnel resources required for an enterprise to operate and manage its communications environment. We estimate that enterprises globally spend approximately $425 billion annually on their fixed and mobile communications services.

The communications industry has also undergone significant competitive and regulatory changes that have resulted in the expansion of the number of service providers and offerings.

1

Enterprises need to manage an increasing number of service options and a growing volume and complexity of communications contracts and billing arrangements. Inefficient management of these expenses, including overpayments as a result of billing errors, often results in enterprises incurring significant avoidable expenses.

Enterprises are increasingly seeking solutions to manage their expanding communications assets, services, expenses and usage, and the CLM market provides solutions to help meet this demand. CLM solutions also seek to enable enterprises to utilize the data gained from each step of the communications lifecycle to more efficiently manage and optimize their communications assets and services. A number of trends have increased the demand for CLM solutions:

- •

- Growing complexity of communications service

plans. Service plans and pricing have grown in complexity as carrier offerings have expanded to include wireless, data, virtual

networking and Voice over IP.

- •

- Large volume and complexity of communications

bills. Carriers maintain a large number of disparate billing systems that result in thousands of invoice formats in many different

currencies and languages, making it difficult for global enterprises to normalize, aggregate and analyze their overall communications expenses.

- •

- Pervasive adoption of mobile devices. Increasing use of

advanced mobile devices and operating systems to conduct business and the increasing prevalence of corporate applications on employees' personal mobile devices is imposing significant financial,

support and administrative burdens on enterprises.

- •

- Increasing corporate risk and regulation. The

communication, dissemination and storage of data across thousands of mobile devices increase enterprises' need to implement policies in order to comply with applicable laws and to monitor devices

remotely in order to avoid inappropriate usage and disclosures.

- •

- Globalization of business. As enterprises become more global, they must manage their communications assets and services in a centralized fashion across carriers, countries of origin and languages while providing high levels of service at the local level.

A number of these trends manifest themselves in a phenomenon commonly referred to as "bill shock," where individuals and organizations are surprised by large mobile service bills that reflect unexpected usage and plan overages.

A variety of homegrown and third-party software products and services have been developed to manage communications assets and services, but have proven inadequate to address the growing complexity of communications technologies, devices, service offerings and billing arrangements. Enterprises increasingly are seeking a comprehensive CLM solution that can manage both fixed and mobile communications assets and services, provide global capabilities and integrate with third-party enterprise systems.

We are a leading global provider of CLM software and services. Our on-demand software and related services enable enterprises to manage and optimize the complex processes and expenses associated with the complete lifecycle of an enterprise's fixed and mobile communications assets and services. Key benefits of our solution include:

- •

- Comprehensive capabilities. Our solution manages the complete lifecycle of an enterprise's fixed and mobile communications assets and services, including planning and sourcing, procurement and provisioning, inventory and usage management, mobile

2

- •

- Reduced expenses. Our solution is designed to provide a

significant return on investment by enabling an enterprise to identify and resolve billing errors, to manage used and unused communications assets and services, to proactively monitor and prevent

wireless bill overages and to optimize service plans and asset use.

- •

- Increased productivity. Our solution enables continuous

enterprise connectivity through the rapid provisioning of communications assets and services to new and existing end users. Our solution helps ensure that these assets and services operate at optimal

levels, increasing workforce productivity. Our support of customer help desks can alleviate the internal information technology constraints of our customers and can provide more efficient support to

end users.

- •

- Optimized service agreements. Our extensive experience,

knowledge of current trends and familiarity with regulatory requirements enable us to assist enterprises in optimizing their service arrangements and configuring the appropriate service capabilities,

rate structures and business terms to meet their overall corporate objectives and needs.

- •

- Improved control and visibility. Our on-demand

software allows our customers to access, query and analyze their normalized billing and usage data. Improved control of the billing process helps enterprises ensure they pay their bills on time,

avoiding late payments and associated service interruptions.

- •

- Stronger risk and policy management. Our solution allows

our customers to manage the financial, legal and reputational risks associated with unauthorized or unintended use of their communications assets and services. It provides our customers with enhanced

device security capabilities, allowing additional control of sensitive data amidst the evolving dynamics of the modern communications environment.

- •

- Ease of adoption and use. Our on-demand model allows for rapid implementation and adoption of our software. Our software directly interfaces with carrier systems to enable enterprises to quickly transfer billing and order information to and from their service providers without the burden of costly and time-consuming customizations.

device management, invoice processing, expense allocation and accounting, and asset decommissioning and disposal.

Our strategy is to maintain and enhance our position as a leading global provider of CLM solutions. In order to build upon our market and technology leadership, we intend to:

- •

- Extend solution leadership by continuing to enhance our services

offerings, develop additional capabilities of our software, localize our applications for new geographies and integrate acquired technology;

- •

- Broaden existing customer relationships by leveraging our historical

customer satisfaction to increase the communications assets, expenses and services managed by our solution and to cross-sell additional functionality;

- •

- Acquire new customers by marketing our solution to enterprises that either

do not currently have a CLM solution or have an inadequate communications asset and service management solution;

- •

- Expand international presence by hiring additional international sales and

operations personnel and targeting new customers in foreign markets and global operations of existing customers;

- •

- Leverage strategic alliances to complement our direct selling efforts and

extend our market reach; and

- •

- Pursue strategic acquisitions to expand the functionality of our solution, provide access to new markets or customers, and otherwise complement our existing operations.

3

Recent Acquisitions

As part of our strategy to build upon our market and technology leadership through select acquisitions, we recently completed two acquisitions:

On January 10, 2012 we acquired all of the outstanding equity of Anomalous Networks Inc., or Anomalous, a leading provider of real-time telecommunications expense management software solutions. The consideration consisted of (i) approximately $3.5 million in cash paid at the closing, (ii) approximately $1.0 million in cash payable on the first anniversary of the closing, (iii) 165,775 unregistered shares of our common stock and (iv) 132,617 unvested and unregistered shares of our common stock with vesting based on achievement of revenue targets relating to sales of Anomalous products and services for periods through January 31, 2013. The objectives of our acquisition of Anomalous were the addition to our solution of capabilities for real-time telecommunications expense management as well as machine-to-machine expense management. The acquisition also has provided us with established strategic carrier alliance relationships through which to expand our sales channels for our existing solution capabilities.

On February 21, 2012, we acquired all of the issued share capital of ttMobiles Limited, or ttMobiles, a provider of mobile communications management solutions and services based in the United Kingdom. The purchase price was 5.5 million pounds sterling, which consisted of 4.0 million pounds sterling in cash paid at the closing and 1.5 million pounds sterling of deferred consideration, payable in cash on the first anniversary of the closing. The objectives of our acquisition of ttMobiles were the acceleration of our European expansion and enhancement of our ability to implement and service global programs by leveraging ttMobiles' industry experience and local expertise in Europe and the potential to cross-sell to the customers of ttMobiles the capabilities of our existing solution that were not encompassed by ttMobiles' prior solution.

Risks Associated with Our Business

Our business is subject to a number of risks that you should understand before making an investment decision. These risks are discussed more fully in the section entitled "Risk Factors" following this prospectus summary. Some of these risks are:

- •

- we have had a history of losses since our incorporation in February 2000;

- •

- if the market for CLM services does not grow as we expect, our business will be harmed;

- •

- our quarterly operating results may fluctuate in the future, which could cause our stock price to decline;

- •

- we may experience difficulties in completing the integration of recent acquisitions or acquisitions we may conduct in the

future and we may not realize the anticipated benefits of these acquisitions;

- •

- if we are unable to retain existing customers, our revenue and results of operations would grow more slowly than expected

or decline and results of operations would be impaired; and

- •

- we face intense competition, which may intensify as a result of increasing consolidation.

4

We were incorporated in Delaware under the name TelecomRFQ, Inc. in February 2000 and changed our name to Tangoe, Inc. in December 2001. Our principal executive offices are located at 35 Executive Boulevard, Orange, Connecticut 06477, and our telephone number is (203) 859-9300. Our website address is www.tangoe.com. Information contained on our website is not incorporated by reference into this prospectus, and you should not consider information contained on our website to be part of this prospectus or in deciding whether to purchase shares of our common stock.

"Tangoe" and the Tangoe logo are registered trademarks of Tangoe, Inc. Other trademarks or service marks appearing in this prospectus are the property of their respective holders.

5

Common stock offered by us |

2,200,000 shares | |

Common stock offered by the selling stockholders |

5,800,000 shares |

|

Common stock to be outstanding after this offering |

36,430,959 shares |

|

Use of proceeds |

We intend to use our net proceeds from this offering for working capital and other general corporate purposes. We may also use a portion of our proceeds for the acquisition of, or investment in, businesses, services or technologies that complement our business. We will not receive any proceeds from the shares sold by the selling stockholders. See "Use of Proceeds" for more information. |

|

Risk Factors |

You should read the "Risk Factors" section and other information included in this prospectus for a discussion of factors to consider carefully before deciding to invest in shares of our common stock. |

|

NASDAQ Global Market symbol |

"TNGO" |

The number of shares of our common stock to be outstanding after this offering is based on the number of shares of common stock outstanding as of February 29, 2012, which includes 377,289 shares of common stock issued on the exercise of stock options following the December 31, 2011 date of our most recent balance sheet and excludes:

- •

- 73,113 shares of common stock issuable upon the exercise of warrants outstanding as of February 29, 2012 at a

weighted-average exercise price of $1.95 per share,

- •

- 7,837,372 shares of common stock issuable upon the exercise of stock options outstanding as of February 29, 2012 at

a weighted-average exercise price of $6.15 per share;

- •

- 130,500 shares of common stock issuable upon vesting of restricted stock units outstanding as of February 29, 2012;

and

- •

- 1,730,409 shares of common stock available for future issuance under our equity incentive plans as of February 29, 2012.

Except as otherwise noted, all information in this prospectus:

- •

- assumes no exercise by the underwriters of their option to purchase up to 1,200,000 additional

shares of common stock from the selling stockholders;

- •

- assumes that the additional 651,626 shares of common stock that may become exercisable in the

future under the warrant that we issued to IBM in October 2009, as amended in June 2011, if certain thresholds based on contractually committed annual recurring revenue are met are not

currently issuable; and

- •

- assumes that the 1,282,789 shares of common stock that may become exercisable in the future under the warrant that we issued to Dell Products L.P. in March 2011 if certain thresholds based on annual recurring revenue are met are not currently exercisable.

6

Summary Consolidated Financial Data

The following tables summarize our consolidated financial data. You should read this data together with our consolidated financial statements and related notes included elsewhere in this prospectus, as well as "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the other financial information included elsewhere in this prospectus. See Note 10 to our consolidated financial statements appearing elsewhere in this prospectus for an explanation of the method used to determine the number of shares used in computing net income (loss) per share.

| |

Years Ended December 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2009 | 2010 | 2011 | |||||||

| |

(dollars in thousands, except per share amounts) |

|||||||||

Statement of operations data: |

||||||||||

Revenue: |

||||||||||

Recurring technology and services |

$ | 46,005 | $ | 57,703 | $ | 93,671 | ||||

Strategic consulting, software licenses and other |

9,912 | 10,771 | 11,270 | |||||||

Total revenue |

55,917 | 68,474 | 104,941 | |||||||

Cost of revenue: |

||||||||||

Recurring technology and services |

20,538 | 26,349 | 44,814 | |||||||

Strategic consulting, software licenses and other |

4,360 | 3,874 | 5,165 | |||||||

Total cost of revenue (1) |

24,898 | 30,223 | 49,979 | |||||||

Gross profit |

31,019 | 38,251 | 54,962 | |||||||

Operating expense: |

||||||||||

Sales and marketing (1) |

9,793 | 12,281 | 16,648 | |||||||

General and administrative (1) |

9,547 | 11,709 | 17,777 | |||||||

Research and development (1) |

8,070 | 9,321 | 11,860 | |||||||

Depreciation and amortization |

3,537 | 3,529 | 4,551 | |||||||

Restructuring charge |

— | — | 1,549 | |||||||

Income from operations |

72 | 1,411 | 2,577 | |||||||

Other income (expense), net |

||||||||||

Interest expense |

(2,224 | ) | (2,007 | ) | (3,047 | ) | ||||

Interest income |

46 | 19 | 45 | |||||||

Other income |

— | 3 | — | |||||||

Increase in fair value of warrants for redeemable convertible preferred stock |

(184 | ) | (884 | ) | (1,996 | ) | ||||

Loss before income tax provision |

(2,290 | ) | (1,458 | ) | (2,421 | ) | ||||

Income tax provision |

264 | 294 | 534 | |||||||

Net loss |

(2,554 | ) | (1,752 | ) | (2,955 | ) | ||||

Preferred dividends |

(3,714 | ) | (3,715 | ) | (2,168 | ) | ||||

Accretion of redeemable convertible preferred stock |

(64 | ) | (64 | ) | (37 | ) | ||||

Loss applicable to common stockholders |

$ | (6,332 | ) | $ | (5,531 | ) | $ | (5,160 | ) | |

Basic and diluted loss per common share |

$ | (1.47 | ) | $ | (1.26 | ) | $ | (0.31 | ) | |

Basic and diluted weighted-average common shares outstanding |

4,311 | 4,399 | 16,412 | |||||||

|

||||||||||

7

| |

Years Ended December 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2009 | 2010 | 2011 | |||||||

| |

(dollars in thousands, except per share amounts) |

|||||||||

Other financial data: |

||||||||||

Adjusted EBITDA (2) |

$ | 4,358 | $ | 6,868 | $ | 12,657 | ||||

| |

|

|

||||||||

(1) Includes stock-based compensation as follows: |

||||||||||

Cost of revenue |

$ | 115 | $ | 323 | $ | 669 | ||||

Sales and marketing |

216 | 425 | 1,201 | |||||||

General and administrative |

329 | 1,032 | 1,934 | |||||||

Research and development |

89 | 148 | 176 | |||||||

|

$ | 749 | $ | 1,928 | $ | 3,980 | ||||

- (2)

- We

define Adjusted EBITDA as net income (loss) plus interest expense, income tax provision (benefit), depreciation and amortization, stock-based

compensation expense, (increase) decrease in fair value of warrants for redeemable convertible preferred stock and restructuring charge less interest income and other income. Adjusted EBITDA is a

financial measure that is not calculated in accordance with GAAP. The table below provides a reconciliation of this non-GAAP financial measure to the most directly comparable financial

measure calculated and presented in accordance with GAAP. Adjusted EBITDA should not be considered as an alternative to net income (loss), operating income (loss) or any other measure of financial

performance calculated and presented in accordance with GAAP. Our Adjusted EBITDA may not be comparable to similarly titled measures of other organizations because other organizations may not

calculate Adjusted EBITDA in the same manner as we do. We prepare Adjusted EBITDA to eliminate the impact of items that we do not consider indicative of our core operating performance. You are

encouraged to evaluate these adjustments and the reason we consider them appropriate.

We believe that Adjusted EBITDA is useful to investors in evaluating our operating performance for the following reasons:

- •

- Adjusted EBITDA is widely used by investors to measure a company's operating performance without regard to

items, such as interest expense, interest income, income tax provision (benefit), depreciation and amortization, and stock-based compensation expense, that can vary substantially from company to

company depending upon their financing and accounting methods, the book value of their assets, their capital structures and the method by which their assets were acquired;

- •

- securities analysts use Adjusted EBITDA as a supplemental measure to evaluate the overall operating

performance of companies; and

- •

- we adopted the authoritative guidance for stock-based payments on January 1, 2006 and recorded

stock-based compensation expense of approximately $749,000, $1,928,000 and $3,980,000 for the years ended December 31, 2009, 2010 and 2011, respectively. Prior to January 1, 2006, we

accounted for stock-based compensation expense using the intrinsic value method under previously authorized guidance, which did not result in any stock-based compensation expense. By comparing our

Adjusted EBITDA in different historical periods, our investors can evaluate our operating results without the additional variations caused by stock-based compensation expense, which is not comparable

from year to year due to changes in accounting treatment and is a non-cash expense that is not a key measure of our operations.

Our management uses Adjusted EBITDA:

- •

- as a measure of operating performance because it does not include the impact of items not directly

resulting from our core business;

- •

- for planning purposes, including the preparation of our annual operating budget;

- •

- to evaluate the effectiveness of our business strategies; and

- •

- in communications with our board of directors concerning our financial performance.

We understand that, although Adjusted EBITDA is frequently used by investors and securities analysts in their evaluations of companies, Adjusted EBITDA has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our results of operations as reported under GAAP. Some of these limitations are:

- •

- Adjusted EBITDA does not reflect our cash expenditures or future requirements for capital expenditures or other contractual commitments;

8

- •

- Adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs;

- •

- Adjusted EBITDA does not reflect interest expense or interest income;

- •

- Adjusted EBITDA does not reflect cash requirements for income taxes; and

- •

- Adjusted EBITDA may not be calculated similarly from company to company.

The following table represents a reconciliation of Adjusted EBITDA to net loss, the most comparable GAAP measure, for each of the periods indicated.

| |

Years Ended December 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

Reconciliation of Adjusted EBITDA to Net Loss

|

2009 | 2010 | 2011 | ||||||||

| |

(dollars in thousands) |

||||||||||

Net loss |

$ | (2,554 | ) | $ | (1,752 | ) | $ | (2,955 | ) | ||

Interest expense |

2,224 | 2,007 | 3,047 | ||||||||

Interest income |

(46 | ) | (19 | ) | (45 | ) | |||||

Income tax provision |

264 | 294 | 534 | ||||||||

Depreciation and amortization |

3,537 | 3,529 | 4,551 | ||||||||

Stock-based compensation expense |

749 | 1,928 | 3,980 | ||||||||

Other income |

— | (3 | ) | — | |||||||

Restructuring charge |

— | — | 1,549 | ||||||||

Increase in fair value of warrants for redeemable convertible preferred stock |

184 | 884 | 1,996 | ||||||||

Adjusted EBITDA |

$ | 4,358 | $ | 6,868 | $ | 12,657 | |||||

The as adjusted data as of December 31, 2011 shown below assume the sale of the shares of common stock that we are offering under this prospectus at an assumed public offering price of $17.57 per share (the closing price of our common stock on The NASDAQ Global Market on March 21, 2012) and after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us.

| |

December 31, 2011 | ||||||

|---|---|---|---|---|---|---|---|

| |

Actual | As Adjusted | |||||

| |

(dollars in thousands) |

||||||

Balance sheet data: |

|||||||

Cash and cash equivalents |

$ | 43,407 | $ | 79,380 | |||

Accounts receivable, net |

25,311 | 25,311 | |||||

Working capital (excluding deferred revenue—current portion) (1) |

48,572 | 84,545 | |||||

Intangible assets—net |

28,800 | 28,800 | |||||

Goodwill |

36,266 | 36,266 | |||||

Total assets |

140,862 | 176,835 | |||||

Accounts payable and accrued expenses |

13,666 | 13,666 | |||||

Deferred revenue—current portion |

9,051 | 9,051 | |||||

Notes payable, including current portion |

16,194 | 16,194 | |||||

Stockholders' equity |

96,589 | 132,562 | |||||

- (1)

- This amount is derived by taking working capital of $39.5 million and excluding deferred revenue—current portion, which is a non-cash obligation.

9

Investing in our common stock involves a high degree of risk. You should carefully consider the following risk factors and all other information contained in this prospectus before purchasing our common stock. The risks and uncertainties described below are not the only ones that we face. Additional risks and uncertainties that we are unaware of, or that we currently deem immaterial, also may become important factors that affect us. If any of the following risks occur, our business, financial condition or results of operations could be materially and adversely affected. In that case, the trading price of our common stock could decline, and you may lose some or all of your investment.

Risks Related to Our Business and Our Industry

We have had a history of losses since our incorporation in February 2000.

We were incorporated in February 2000 and have not been profitable in any fiscal period since we were formed. We experienced net losses of $2.6 million in 2009, $1.8 million in 2010 and $3.0 million in 2011. We cannot predict if we will be able to attain profitability in the near future or at all. We expect to continue making significant future expenditures to develop and expand our business. In addition, as a public company, we incur additional significant legal, accounting and other expenses that we did not incur as a private company. As a result of these increased expenditures, we will have to generate and sustain substantially increased revenue to achieve and maintain profitability, which we may never do. We may also encounter unforeseen difficulties, complications, product delays and other unknown factors that require additional expenditures. In addition, the percentage growth rates we achieved in prior periods may not be sustainable and we may not be able to increase our revenue sufficiently in absolute dollars to ever reach or maintain profitability and we may incur significant losses for the foreseeable future.

If the market for communications lifecycle management services does not grow as we expect, our business will be harmed.

The market for communications lifecycle management, or CLM, services is developing, and it is not certain whether these services will achieve market acceptance and sustain high demand. Some businesses have invested substantial personnel and financial resources into developing internal solutions for CLM, so they may not perceive the benefit of our external solution. If businesses do not perceive the benefits of outsourced CLM services, the CLM market may not continue to develop or may develop more slowly than we expect, either of which would reduce our revenue and profitability.

Our quarterly operating results may fluctuate in the future. As a result, we may fail to meet or exceed the expectations of research analysts or investors, which could cause our stock price to decline.

Our quarterly operating results may fluctuate as a result of a variety of factors, many of which are outside of our control. If our quarterly operating results or guidance fall below the expectations of research analysts or investors, the price of our common stock could decline substantially. Fluctuations in our quarterly operating results or guidance may be due to a number of factors, including, but not limited to:

- •

- our ability to attract new customers, obtain renewals from existing customers and increase sales to existing customers;

- •

- the purchasing and budgeting cycles of our customers;

10

- •

- changes in our pricing policies or those of our competitors;

- •

- the amount and timing of operating costs and capital expenditures related to the operation, maintenance and expansion of

our business;

- •

- service outages or security breaches;

- •

- the timing and success of new service introductions and upgrades by us or our competitors;

- •

- the timing of costs related to the development or acquisition of technologies, services or businesses;

- •

- the financial condition of our customers; and

- •

- general economic, industry and market conditions.

In addition, the accounting treatment of the warrant shares that may become issuable to IBM and Dell and of the unvested earn-out shares issued in connection with our acquisition of Anomalous Networks in January 2012 could have an impact on our quarterly operating results. We currently value the warrant shares that are deemed probable of becoming exercisable on a mark-to-market basis until they are earned, and will value the unvested earn-out shares that are deemed probable of becoming vested and earned on a mark-to-market basis until they are vested and earned. Increases or decreases in our stock price will affect the mark-to-market adjustments of the common stock warrant shares and unvested earn-out shares, which will increase or decrease contra-revenue charges. The value of the warrant shares and unvested earn-out shares will fluctuate until the warrant shares are deemed exercisable or the unvested earn-out shares are deemed vested and earned, as the case may be, and the value is fixed. This accounting treatment is applicable whether or not our IBM, Dell or Anomalous related revenue actually increases or decreases in line with the market value of our common stock, and thus could cause significant fluctuations in our quarterly operating results.

Because we collect and recognize revenue over the terms of our customer agreements, the lack of customer renewals or new customer agreements may not be immediately reflected in our operating results.

We collect and recognize revenue from our customers over the terms of their customer agreements with us. As a result, the aggregate effect of a decline in new or renewed customer agreements in any one quarter would not be fully recognized in our revenue for that quarter and would negatively affect our revenue in future quarters. Consequently, the aggregate effect of significant downturns in sales of our solution would not be fully reflected in our results of operations until future periods. For instance, as a result of the financial crisis in the second half of 2008, we experienced a higher-than-normal cancellation rate in the first three months of 2009, much of which was attributable to customers that had gone out of business. As a result of such cancellations, our total revenue for the following periods was negatively affected. Our subscription model also makes it difficult for us to rapidly increase our revenue through additional sales in any period, as revenue from new customers is generally collected and recognized over the applicable contract term.

11

If we are unable to retain our existing customers, our revenue and results of operations would grow more slowly than expected or decline and results of operations would be impaired.

We sell our software products pursuant to agreements that are generally two to five years in duration. Our customers have no obligation to renew their agreements after their terms expire and some of our customers may terminate their agreements for convenience. These agreements may not be maintained or renewed on the same or on more profitable terms. As a result, our ability to both maintain and grow our revenue depends in part on customer renewals. We may not be able to accurately predict future trends in customer renewals, and our customers' renewal rates may decline or fluctuate because of several factors, including their satisfaction or dissatisfaction with our software products, the prices of our software products, the prices of products and services offered by our competitors or reductions in our customers' spending levels. In addition, customers that are acquired by companies using competing service offerings may be required to begin using those competing service offerings, rather than renew their license arrangements with us. If our customers do not renew their agreements for our software products, renew on less favorable terms, or do not purchase additional functionality, our revenue may grow more slowly than expected or decline.

We face intense competition, and our failure to compete successfully would make it difficult for us to add and retain customers and would impede the growth of our business.

The CLM market is highly fragmented, competitive and rapidly evolving. We compete with other technology and outsourced service providers selling telecommunications expense management and/or mobile device management solutions as well as with solutions developed internally by enterprises seeking to manage their communications expenses and assets. We compete with other technology and outsourced service providers primarily on the basis of customer references, ability to deliver, breadth of solution and pricing. We and other technology and outsourced service providers compete with internally developed CLM solutions primarily on the basis of the relative cost of implementing a third-party solution as compared to inefficiencies or lack of functionality in internally developed CLM solutions.

The intensity of competition in the CLM market has resulted in pricing pressure as the market has developed. We expect the intensity of competition to increase in the future as existing competitors develop their capabilities and as new companies, which could include one or more large communications carriers, enter our market. Some of these competitors, such as large communications carriers, may offer telecommunications expense management and/or mobile device management solutions as part of a broad outsource offering for mobile communications services. Increased competition could result in additional pricing pressure, reduced sales, shorter term lengths for customer contracts, lower margins or the failure of our solution to achieve or maintain broad market acceptance. If we are unable to compete effectively, it will be difficult for us to maintain our pricing rates and add and retain customers, and our business, financial condition and results of operations will be harmed.

Some of our actual and potential competitors may enjoy competitive advantages over us, such as greater name recognition, longer operating histories, more varied services and larger marketing budgets, as well as greater financial, technical and other resources. As a result, our competitors may be able to respond more quickly than we can to new or changing opportunities, technologies, standards or customer requirements or devote greater resources to the promotion and sale of their products and services than we can.

12

Industry consolidation may result in increased competition.

The CLM market is highly fragmented, and we believe that it is likely that some of our existing competitors will consolidate or will be acquired. Some of our competitors have made or may make acquisitions or may enter into partnerships or other strategic relationships to offer a more comprehensive solution than they individually had offered. In addition, new entrants not currently considered to be competitors may enter the market through acquisitions, partnerships or strategic relationships, such as with Vodafone's acquisitions of TnT Expense Management and Quickcomm in October 2010, Emptoris' acquisition of Rivermine in January 2011 and the subsequent acquisition of Emptoris/Rivermine by IBM in February 2012. We expect these trends to continue as companies attempt to strengthen or maintain their market positions. The companies resulting from such combinations may create more compelling service offerings and may offer greater pricing flexibility than we can or may engage in business practices that make it more difficult for us to compete effectively, including on the basis of price, sales and marketing programs, technology or service functionality. In addition, combinations such as IBM's acquisition of Emptoris/Rivermine may result in situations in which we may begin to compete in some CLM offerings with companies with which we have partnerships or strategic relationships. Any of the competitive pressures described above could result in a substantial loss of customers or a reduction in our revenue.

We are currently integrating the operations of several businesses that we recently acquired and may in the future expand by acquiring or investing in other businesses, which may divert our management's attention and consume resources that are necessary to sustain our business.

We are currently integrating the operations of five businesses that we acquired during 2011 and the first quarter of 2012. With respect to three of these businesses, we are migrating their former customers to our platform. If we encounter unforeseen technical or other challenges in the migration of these customers or the integration of these acquired businesses, our business and results of operations could be harmed. For example, with respect to one of the acquisitions during the first quarter of 2011, we have entered into an agreement for the provision of CLM services by a third party to certain of these customers during their migration and we are obligated to maintain a firewall with respect to the service provider's software. If the availability of these outsourced services were disrupted during the customer migration process, or if we were unable to maintain the firewall required under this agreement, we could incur substantial costs in arranging for alternative services or substantial liabilities arising out the breach of our obligations.

Our business strategy includes the potential future acquisition of, or investment in, complementary businesses, services or technologies. These acquisitions, investments or new business relationships may result in unforeseen difficulties and expenditures. We may encounter difficulties assimilating or integrating the businesses, technologies, products, services, personnel or operations of companies we have acquired or companies that we may in the future acquire. These difficulties may arise if the key personnel of the acquired company choose not to work for us, the company's technology or services do not easily integrate with ours or we have difficulty retaining the acquired company's customers due to changes in its management or for other reasons. These acquisitions may also disrupt our business, divert our resources and require significant management attention that would otherwise be available for development of our business. Moreover, the anticipated benefits of any acquisition, investment or business relationship may not be realized or we may be exposed to unknown liabilities. In addition, any future acquisition may require us to:

- •

- issue additional equity securities that would dilute our stockholders;

13

- •

- use cash that we may need in the future to operate our business;

- •

- incur debt on terms unfavorable to us or that we are unable to repay;

- •

- incur large charges or substantial liabilities; or

- •

- become subject to adverse tax consequences, substantial depreciation or deferred compensation charges.

If any of these risks materializes, our business and operating results would be harmed.

Our sales cycles can be long, unpredictable and require considerable time and expense, which may cause our operating results to fluctuate.

Our sales cycle, which is the time between initial contact with a potential customer and the ultimate sale, is often lengthy and unpredictable. Some of our potential customers already have partial CLM solutions in place under fixed-term contracts, which limits their ability to commit to purchase our solution in a timely fashion. In addition, our potential customers typically undertake a significant evaluation process that can last six to nine months or more, and which requires us to expend substantial time, effort and money educating them about the capabilities of our offerings and the potential cost savings they can bring to an organization. Furthermore, the purchase of our solution typically also requires coordination and agreement across many departments within a potential customer's organization, which further contributes to our lengthy sales cycle. As a result, we have limited ability to forecast the timing and size of specific sales. Any delay in completing, or failure to complete, sales in a particular quarter or year could harm our business and could cause our operating results to vary significantly.

If a communications carrier prohibits customer disclosure of communications billing and usage data to us, the value of our solution to customers of that carrier would be impaired, which may limit our ability to compete for their business.

Certain of the software functionality and services we offer depend on our ability to access a customer's communications billing and usage data. For example, our ability to offer outsourced or automated communications bill auditing, billing dispute resolution, bill payment, cost allocation and expense optimization depends on our ability to access this data. If a communications carrier were to prohibit its customers from disclosing this information to us, those enterprises would only be able to use these billing-related aspects of our solution on a self-serve basis, which would impair the value of our solution to those enterprises. This in turn could limit our ability to compete with the internally developed CLM solutions of those enterprises, require us to incur additional expenses to license access to that billing and usage data from the communications carrier, if such a license is made available to us at all, or put us at a competitive disadvantage against any third-party CLM service provider that licenses access to that data.

Our long-term success depends, in part, on our ability to expand the sales of our solution to customers located outside of the United States, and thus our business is susceptible to risks associated with international sales and operations.

We are currently expanding our international sales and operations, including through the acquisition of Anomalous Networks, based in Canada, and ttMobiles, based in the United Kingdom. This international expansion will subject us to new risks that we have not faced in

14

the United States and the countries in which we currently conduct business. These risks include:

- •

- continued geographic localization of our software products, including translation into foreign languages and adaptation

for local practices and regulatory requirements;

- •

- lack of familiarity with and unexpected changes in foreign regulatory requirements;

- •

- longer accounts receivable payment cycles and difficulties in collecting accounts receivable;

- •

- difficulties in managing and staffing international implementations and operations;

- •

- challenges in integrating our software with multiple country-specific billing or communications support systems for

international customers;

- •

- challenges in providing procurement, help desk and fulfillment capabilities for our international customers;

- •

- fluctuations in currency exchange rates;

- •

- potentially adverse tax consequences, including the complexities of foreign value added or other tax systems and

restrictions on the repatriation of earnings;

- •

- the burdens of complying with a wide variety of foreign laws and legal standards;

- •

- increased financial accounting and reporting burdens and complexities;

- •

- potentially slower adoption rates of CLM services internationally;

- •

- political, social and economic instability abroad, terrorist attacks and security concerns in general; and

- •

- reduced or varied protection for intellectual property rights in some countries.

Operating in international markets also requires significant management attention and financial resources. The investment and additional resources required to establish operations and manage growth in other countries may not produce desired levels of revenue or profitability.

Further expansion into international markets could require us to comply with additional billing, invoicing, communications, data privacy and similar regulations, which could make it costly or difficult to operate in these markets.

Many international regulatory agencies have adopted regulations related to where and how communications bills may be sent and how the data on such bills must be handled and protected. For instance, certain countries, such as Germany, restrict communications bills from being sent outside of the country, either physically or electronically, and certain countries, such as Brazil, Germany, Italy and Spain, require that certain information be encrypted or redacted before bills may be transmitted electronically. These regulations vary from jurisdiction to jurisdiction and international expansion of our business could subject us to additional similar regulations. Failure to comply with these regulations could result in significant monetary penalties and compliance with these regulations could require expenditure of significant financial and administrative resources.

In addition, personally identifiable information is increasingly subject to legislation and regulations in numerous jurisdictions around the world, the intent of which is to protect the privacy of personal information that is collected, processed and transmitted in or from the governing jurisdiction. Our failure to comply with applicable privacy laws and regulations or any security breakdown that results in the unauthorized release of personally identifiable

15

information or other customer data could result in fines or proceedings by governmental agencies or private individuals, which could harm our results of operations.

If we fail to effectively manage and develop our strategic relationships with our channel partners, or if those third parties choose not to market and sell our solution, our operating results would suffer.

The successful implementation of our strategic goals is dependent in part on strategic relationships with our channel partners to offer our solution to a larger customer base than we can reach through our current direct sales and marketing efforts. Some of our strategic relationships, such as our relationships with IBM and Dell Products L.P., are relatively new and, therefore, it is uncertain whether these third parties will be able to market and sell our solution successfully or provide the volume and quality of customers that we currently expect.

Our success depends in part on the ultimate success of our channel partners and their ability to market and sell our solution. Some of these third parties have previously entered, and may in the future enter, into strategic relationships with our competitors. For example, IBM acquired Emptoris in February 2012, and Rivermine is a subsidiary of Emptoris. Further, many of our channel partners have multiple strategic relationships and they may not regard us as significant to their businesses. Our channel partners may terminate their respective relationships with us, pursue other partnerships or relationships, or attempt to develop or acquire products or services that compete with our solution. Our channel partners also may interfere with our ability to enter into other desirable strategic relationships.

If we are unable to manage and develop our strategic relationships, our potential customer base may grow more slowly than we anticipate and we may have to devote substantially more resources to the distribution, sales and marketing of our solution, which would increase our costs and decrease our earnings.

We have experienced rapid growth in recent periods. If we fail to manage our growth effectively, we may be unable to execute our business plan, maintain high levels of service or address competitive challenges adequately.

We increased our number of full-time employees from 184 at December 31, 2007, to 347 at December 31, 2008, to 439 at December 31, 2009, to 541 at December 31, 2010 and to 1,004 at December 31, 2011, and our total revenue from $21.0 million in 2007, to $37.5 million in 2008, to $55.9 million in 2009, to $68.5 million in 2010 and to $104.9 million in 2011. Our growth has placed, and may continue to place, a significant strain on our managerial, administrative, operational, financial and other resources. We intend to further expand our overall business, customer base, headcount and operations both domestically and internationally. Growing and managing a global organization and a geographically dispersed workforce will require substantial management effort and significant additional investment in our infrastructure. We will be required to continue to improve our operational, financial and management controls and our reporting procedures and we may not be able to do so effectively.

The loss of key personnel or an inability to attract and retain additional personnel may impair our ability to grow our business.

We are highly dependent upon the continued service and performance of our senior management team and key technical and sales personnel, including our founder, President and Chief Executive Officer, and none of these individuals is party to an employment agreement with us. The replacement of these individuals likely would involve expenditure of

16

significant time and financial resources, and their loss might significantly delay or prevent the achievement of our business objectives.

We plan to continue to expand our work force both domestically and internationally to increase our customer base and revenue. We face intense competition for qualified individuals from numerous technology, software and communications companies. Our ability to achieve significant revenue growth will depend, in large part, on our success in recruiting, training and retaining sufficient numbers of personnel to support our growth. New hires may require significant training and may take significant time before they achieve full productivity. Our recent hires and planned hires may not become as productive as we expect, and we may be unable to hire or retain sufficient numbers of qualified individuals. If our recruiting, training and retention efforts are not successful or do not generate a corresponding increase in revenue, our business will be harmed.

Our software manages and interfaces with our customers' mission-critical networks and systems. Disruptions in the functioning of these networks and systems caused by our software could subject us to substantial liability and damage our reputation.

We assist our customers in the management of their mission-critical communications networks and systems and our software directly interfaces with these networks and systems as well as with enterprise resource planning and other enterprise software and systems. Failures of software could result in significant interruptions in our customers' communications capabilities and enterprise operations. For example, unknown defects in our mobile device management software, or unknown incompatibilities of this software with our customers' mobile devices, could result in losses of functionality of these devices. If such interruptions occur, we may not be able to remedy them in a timely fashion and our customers' ability to operate their enterprises could be severely compromised. Such interruptions could cause our customers to lose revenue and could damage their reputations. In turn, these disruptions could subject us to substantial liabilities and result in irreparable damage to our reputation, delays in payments from our customers or refusals by our customers to make such payments, any of which could harm our business, financial condition or results of operations.

The emergence of one or more widely used, standardized communications devices or billing or operational support systems could limit the value and operability of our solution and our ability to compete with the manufacturers of such devices or the carriers using such systems in providing CLM services.

Our solution derives its value in significant part from our software's ability to interface with and support the interoperation of diverse communications devices, billing systems and operational support systems. The emergence of a single or a small number of widely used communications devices, billing systems or operational support systems using consolidated, consistent sets of standardized interfaces for the interaction between communications service providers and their enterprise customers could significantly reduce the value of our solution to our customers and potential customers. Furthermore, any such communications device, billing system or operational support system could make use of proprietary software or technology standards that our software might not be able to support. In addition, the manufacturer of such device, or the carrier using such billing system or operational support system, might actively seek to limit the interoperability of such device, billing system or operational support system with our software products for competitive or other reasons. The resulting lack of compatibility of our software products would put us at a significant competitive disadvantage, or entirely prevent us from competing, in that segment of the potential CLM market if such manufacturer or carrier, or its authorized licensees, were to develop one or more CLM solutions competitive with our solution.

17

A continued proliferation and diversification of communications technologies or devices could increase the costs of providing our software products or limit our ability to provide our software products to potential customers.

Our ability to provide our software products is dependent on the technological compatibility of our systems with the communications infrastructures and devices of our customers and their communications service providers. The development and introduction of new communications technologies and devices requires us to expend significant personnel and financial resources to develop and maintain interoperability of our software products with these technologies and devices. The communications industry has recently been characterized by rapid change and diversification in both product and service offerings. Continued proliferation of communications products and services could significantly increase our research and development costs and increase the lag time between the initial release of new technologies and products and our ability to provide support for them in our software products, which would limit the potential market of customers that we have the ability to serve.

We may not successfully develop or introduce new and enhanced software and service offerings, and as a result we may lose existing customers or fail to attract new customers and our revenue may suffer.

Our future financial performance and revenue growth depend upon the successful development, introduction and customer acceptance of new and enhanced versions of our software and service offerings. We are continually seeking to develop and acquire enhancements to our solution as well as new offerings to supplement our existing solution and we are subject to all of the risks inherent in the development and integration of new technologies, including unanticipated performance, stability, and compatibility problems, any of which could result in material delays in introduction and acceptance, significantly increased costs, adverse publicity and loss of sales. If we are unable to deliver new solutions or upgrades or other enhancements to our existing solution on a timely and cost-effective basis, our business will be harmed.

We may not be able to respond to rapid technological changes with new software products and services, which could harm our sales and profitability.

The CLM market is characterized by rapid technological change and frequent new product and service introductions, driven in part by frequent introductions of new technologies and devices in the communications industry, frequent changes in, and resulting inconsistencies between, the billing platforms utilized by major communications carriers and the changing demands of customers regarding the means of delivery of CLM solutions. To achieve and maintain market acceptance for our solution, we must effectively anticipate these changes and offer software products and services that respond to them in a timely manner. Customers may require features and capabilities that our current solution does not have. If we fail to develop software products and services that satisfy customer preferences in a timely and cost-effective manner, our ability to renew our agreements with existing customers and our ability to create or increase demand for our solution will be harmed.

Actual or perceived breaches of our security measures could diminish demand for our solution and subject us to substantial liability.

In the processing of communications transactions, we receive, transmit and store a large volume of sensitive customer information, including call records, billing records, contractual terms, and financial and payment information, including credit card information, and we have

18

entered into contractual obligations to maintain the confidentiality of certain of this information. Any person who circumvents our security measures could steal proprietary or confidential customer information or cause interruptions in our operations and any such lapse in security could expose us to litigation, substantial contractual liabilities, loss of customers or damage to our reputation or could otherwise harm our business. We incur significant costs to protect against security breaches and may incur significant additional costs to alleviate problems caused by any breaches.

If customers believe that our systems and software products do not provide adequate security for the storage of confidential information or its transmission over the Internet or corporate extranets, or are otherwise inadequate for Internet or extranet use, our business will be harmed. Customers' concerns about security could deter them from using the Internet to conduct transactions that involve confidential information, including transactions of the types included in our solution, so our failure to prevent security breaches, or the occurrence of well-publicized security breaches affecting the Internet in general, could significantly harm our business and financial results.

If we are unable to protect our intellectual property rights and other proprietary information, it will reduce our ability to compete for business.

If we are unable to protect our intellectual property rights and other proprietary information, our competitors could use our intellectual property to market software products similar to our own, which could decrease demand for our solution. We rely on a combination of patent, copyright, trademark, service mark and trade secret laws, as well as confidentiality procedures and contractual restrictions, to establish and protect our intellectual property rights and proprietary information, all of which provide only limited protection. We have twelve issued patents and eleven patent applications pending. We cannot assure you that our issued patents, any patents that may issue from our patent applications pending or any other intellectual property rights that we currently hold or may in the future acquire will prove to be enforceable in actions against alleged infringers or otherwise provide sufficient protection of any competitive advantages that we may have. In addition, any action that we take to enforce our patents or other intellectual property rights may be costly, time-consuming and a significant diversion of management attention from the continued growth and development of our business.

We endeavor to enter into agreements with our employees and contractors and agreements with parties with whom we do business to limit access to and disclosure of our proprietary information. The steps we have taken, however, may not prevent unauthorized use or the reverse engineering of our technology. Moreover, others may independently develop technologies that are competitive with ours or infringe our intellectual property. Enforcement of our intellectual property rights also depends on our successful legal actions against these infringers, but these actions may not be successful, even when our rights have been infringed.

Furthermore, effective patent, copyright, trademark, service mark and trade secret protection may not be available in every country in which we offer our software products.

Assertions by a third party that our software products or technology infringes its intellectual property, whether or not correct, could subject us to costly and time-consuming litigation or expensive licenses.

There is frequent litigation in the communications and technology industries based on allegations of infringement or other violations of intellectual property rights. As we face increasing competition and become increasingly visible as a publicly traded company, the

19

possibility of intellectual property rights claims against us may grow. These claims, whether or not successful, could:

- •

- divert management's attention;

- •

- result in costly and time-consuming litigation;

- •

- require us to enter into royalty or licensing agreements, which may not be available on acceptable terms, or at all; or

- •

- require us to redesign our software products to avoid infringement.

As a result, any third-party intellectual property claims against us could increase our expenses and impair our business.

In addition, although we have licensed proprietary technology, we cannot be certain that the owners' rights in such technology will not be challenged, invalidated or circumvented. Furthermore, many of our customer agreements require us to indemnify our customers for certain third-party intellectual property infringement claims, which could increase our costs as a result of defending such claims and may require that we pay damages if there were an adverse ruling related to any such claims. These types of claims could harm our relationships with our customers, may deter future customers from purchasing our software products or could expose us to litigation for these claims. Even if we are not a party to any litigation between a customer and a third party, an adverse outcome in any such litigation could make it more difficult for us to defend our intellectual property in any subsequent litigation in which we are a named party.

We outsource certain of our research and development activities to third-party contractors, and a loss of or deterioration in these relationships could adversely affect our ability to introduce new software products or enhancements in a timely fashion.

Certain of our research and development activities are carried out by third-party contractors, located both in the United States and abroad. The loss of or deterioration in any of these relationships for any reason could require us to establish alternative relationships or to complete these research and development activities using our internal research and development staff, either of which could result in increased costs to us and impair our ability to introduce new software products or enhancements in a timely fashion. Our use of such third-party contractors also increases the risk that our intellectual property could be misappropriated or otherwise disclosed to our competitors, either of which could harm our competitiveness and harm our future revenue.

Defects or errors in our software products could harm our reputation, impair our ability to sell our products and result in significant costs to us.

Our software products are highly complex and may contain undetected defects or errors, including defects and errors arising from the work of our outsourced development teams, that may result in product failures or otherwise cause our software products to fail to perform in accordance with customer expectations. Because our customers use our software products for important aspects of their businesses, any defects or errors in, or other performance problems with, our software products could hurt our reputation and may damage our customers' businesses. If that occurs, we could lose future sales or our existing customers could elect to not renew their customer agreements with us. Product performance problems could result in loss of market share, failure to achieve market acceptance and the diversion of development resources from software enhancements. If our software products fail to perform or contain a technical defect, a customer might assert a claim against us for damages. We may not have

20

contractual limitations on damages claims that could be asserted against us. Whether or not we are responsible for our software's failure or defect, we could be required to spend significant time and money in litigation, arbitration or other dispute resolution, and potentially pay significant settlements or damages.

We use a limited number of data centers to deliver our software products. Disruption of service at these facilities could harm our business.

We host our software products and serve all of our customers from eight third-party data center facilities. We do not control the operation of these facilities. American Internet Services operates our data center in San Diego, California; AT&T operates our data center in Secaucus, New Jersey; Data Foundry operates our data center in Austin, Texas; iWeb Technologies operates our data center in Montreal, Canada; NTT Communications operates our data centers in London and Slough, United Kingdom; Savvis operates our data center in Piscataway, New Jersey; and Verizon Business operates our data center in Billerica, Massachusetts. Our agreements for the use of these data center facilities vary in term length, some being month-to-month and others expiring during 2013, 2014 and 2015. The owners of these facilities have no obligation to continue such arrangements beyond their current terms, which are as short as the current month in the case of month-to-month arrangements, nor are they obligated to renew their agreements with us on commercially reasonable terms, or at all. If we are unable to continue such arrangements or renew these agreements on commercially reasonable terms, we may be required to transfer to new data center facilities and we may incur significant costs in connection with doing so. Any changes in third-party service levels at our data centers or any errors, defects, disruptions or other performance problems with our software products could harm our reputation and damage our business. Interruptions in the availability of our software products might reduce our revenue, cause us to issue credits to customers, subject us to potential liability, cause customers to terminate their subscriptions or harm our renewal rates.

While we take precautions such as data redundancy, back-up and disaster recovery plans to prevent service interruptions, our data centers are vulnerable to damage or interruption from human error, intentional bad acts, pandemics, earthquakes, hurricanes, floods, fires, war, terrorist attacks, power losses, hardware failures, systems failures, communications failures and similar events. The occurrence of a natural disaster or an act of terrorism, or vandalism or other misconduct, a decision to close the facilities without adequate notice or other unanticipated problems could result in lengthy interruptions in the availability of our software products.

If we fail to maintain proper and effective internal controls, our ability to produce accurate and timely financial statements could be impaired, which could harm our operating results, our ability to operate our business and investors' views of us.