Attached files

| file | filename |

|---|---|

| EX-21 - EXHIBIT 21 - NUMEREX CORP /PA/ | exhibit21.htm |

| EX-23 - EXHIBIT 23 - NUMEREX CORP /PA/ | exhibit23.htm |

| EX-11 - EXHIBIT 11 - NUMEREX CORP /PA/ | exhibit11.htm |

| EXCEL - IDEA: XBRL DOCUMENT - NUMEREX CORP /PA/ | Financial_Report.xls |

| EX-31.1 - EXHIBIT 31.1 - NUMEREX CORP /PA/ | exhibit311.htm |

| EX-31.2 - EXHIBIT 31.2 - NUMEREX CORP /PA/ | exhibit312.htm |

| EX-32.1 - EXHIBIT 32.1 - NUMEREX CORP /PA/ | exhibit321.htm |

| EX-32.2 - EXHIBIT 32.2 - NUMEREX CORP /PA/ | exhibit322.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

x

|

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

|

For the fiscal year ended December 31, 2011

|

¨

|

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

|

For the transition period from to

Commission File Number 0-22920

NUMEREX CORP.

(Name of Registrant as Specified in Its Charter)

|

Pennsylvania

|

11-2948749

|

|

|

(State or Other Jurisdiction

of Incorporation or Organization)

|

(I.R.S. Employer

Identification Number)

|

|

|

1600 Parkwood Circle, Suite 500, Atlanta, GA

|

30339

|

|

|

(Address of Principal Executive Offices)

|

(Zip Code)

|

|

(770) 693-5950

(Registrant’s Telephone Number, Including Area Code)

Securities Registered Pursuant to Section 12(b) of the Act:

|

Class A Common Stock, no par value

(Title of each class)

|

The NASDAQ Stock Market LLC

(Name of each exchange on which registered)

|

|

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15 (d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer Accelerated filer þ Non-accelerated filer Smaller Reporting Company

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No þ

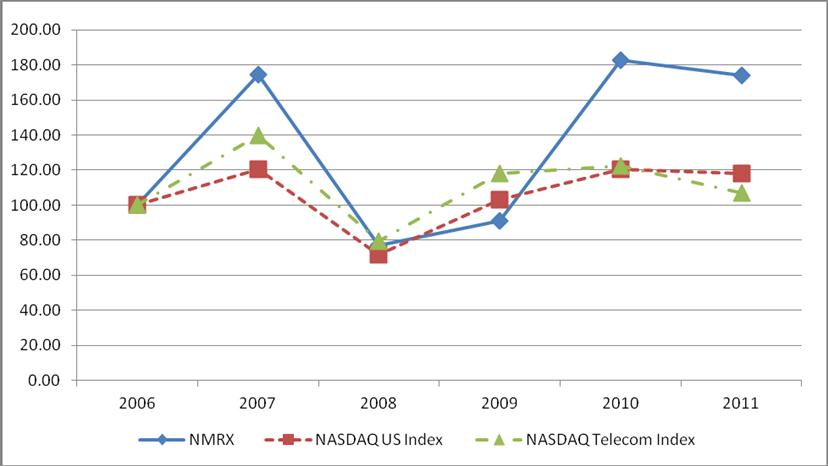

The aggregate market value of the registrant’s outstanding common stock held by non-affiliates of the registrant was $111.3 million based on a closing price of $9.73 on June 30, 2011, as quoted on the NASDAQ Global Market.

The number of shares outstanding of the registrant’s Class A Common Stock as of March 08, 2012, was 15,163,662 shares.

DOCUMENTS INCORPORATED BY REFERENCE

The registrant intends to file a definitive proxy statement pursuant to Regulation 14A within 120 days of the end of the fiscal year ended December 31, 2011. The proxy statement is incorporated herein by reference into the following parts of the Form 10-K:

Part III, Item 10, Directors, Executive Officers and Corporate Governance;

Part III, Item 11, Executive Compensation;

Part III, Item 12, Security Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters;

Part III, Item 13, Certain Relationships and Related Transactions, and Director Independence; and

Part III, Item 14, Principal Accountant Fees and Services.

NUMEREX CORP.

ANNUAL REPORT ON FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2011

TABLE OF CONTENTS

|

Page

|

||

|

PART I

|

||

|

Item 1.

|

Business

|

4

|

|

Item 1A.

|

Risk Factors

|

11

|

|

Item 1B.

|

Unresolved Staff Comments

|

21

|

|

Item 2.

|

Properties

|

21

|

|

Item 3.

|

Legal Proceedings

|

22

|

|

Item 4.

|

Mine Safety Disclosures

|

22

|

|

|

||

|

PART II

|

||

|

Item 5.

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity

|

|

|

Securities

|

22

|

|

|

Item 6.

|

Selected Consolidated Financial Data

|

24

|

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

25

|

|

Item 7A.

|

Quantitative and Qualitative Disclosures about Market Risk

|

37

|

|

Item 8.

|

Financial Statements and Supplementary Data

|

38

|

|

Item 9.

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

67

|

|

Item 9A.

|

Controls and Procedures

|

67

|

|

Item 9B.

|

Other Information

|

69

|

|

|

||

|

PART III

|

||

|

Item 10.

|

Directors, Executive Officers and Corporate Governance

|

69

|

|

Item 11.

|

Executive Compensation

|

69

|

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

69

|

|

Item 13.

|

Certain Relationships and Related Transactions and Director Independence

|

69

|

|

Item 14.

|

Principal Accounting Fees and Services

|

69

|

|

|

PART IV

|

|

|

Item 15.

|

Exhibits and Financial Statement Schedule

|

70

|

Forward-Looking Statements

This document may contain forward-looking statements with respect to Numerex future financial or business performance, conditions or strategies and other financial and business matters, including expectations regarding growth trends and activities. Forward-looking statements are typically identified by words or phrases such as "believe," "expect," "anticipate," "intend," "estimate," "assume," "strategy," "plan," "outlook," "outcome," "continue," "remain," "trend," and variations of such words and similar expressions, or future or conditional verbs such as "will," "would," "should," "could," "may," or similar expressions. Numerex cautions that these forward-looking statements are subject to numerous assumptions, risks and uncertainties, which change over time. These forward-looking statements speak only as of the date of this press release, and Numerex assumes no duty to update forward-looking statements. Actual results could differ materially from those anticipated in these forward-looking statements and future results could differ materially from historical performance.

The following factors, among others, could cause actual results to differ materially from forward-looking statements or historical performance: our inability to continue to expand our subscription-based sales mode; our ability to efficiently utilize cloud computing to expand our services; the risks that a substantial portion of revenues derived from government contracts may be terminated by the government at any time; variations in quarterly operating results; delays in the development, introduction, integration and marketing of new services; customer acceptance of services; economic conditions resulting in decreased demand for our products and services, including a prolonged deterioration of the housing market; the risk that our strategic alliances and partnerships will not yield substantial revenues; changes in financial and capital markets, the inability to raise growth capital on favorable terms, if at all; the inability to attain revenue and earnings growth; changes in interest rates; inflation; the introduction, withdrawal, success and timing of business initiatives and strategies; competitive conditions; the inability to realize revenue enhancements; disruption in key supplier relationships and/or related services; unexpected costs associated with our continued investments and expansion in international markets; and extent and timing of technological changes. Numerex SEC reports identify additional factors that can affect forward-looking statement.

PART I. BUSINESS

Numerex Corp (“Numerex,” the “Company” or “we”) is headquartered in Atlanta, Georgia, and organized under the laws of the Commonwealth of Pennsylvania.

Numerex long-term strategy has remained, at its core, the same: to generate long term and sustainable recurring revenue through the use of the Company’s integrated machine-to-machine ("M2M") horizontal platforms. These platforms incorporate the key M2M elements of Device (D), Network (N), and Application (A), and are offered, for the most part, on a subscription basis through a ‘service bureau’, simplifying and speeding the delivery of an M2M solution to any enterprise-based vertical market.

We provide a broad range of machine-to-machine (M2M) business services, technology, and products used in the development and support of M2M solutions for the enterprise and government markets worldwide. We have built innovative platforms that are cloud and service-centric to facilitate the development, deployment and use of our customers’ M2M solutions across a wide range of markets. At the end of 2011, Numerex supported over 1.4 million M2M subscriptions covering over 50 vertical and sub-vertical markets.

M2M consists of using a device (D) (e.g., sensor, meter, etc.) to capture an “event” (e.g., inventory level, location, environment status, etc.) relayed through a network (N) (e.g., wireless, wired or hybrid) to an application (A) (software program), which translates the captured data into actionable information (e.g., there is a breach, vending machine needs to be restocked, pipe is corroded, lost vehicle is located, tank level is too low, etc.)

Our subscription-based platform services, which generate streams of long-term high-margin recurring revenues, are the cornerstone of our business model. We create value by helping our customers bring their M2M solutions to market through one single source, rapidly, efficiently, reliably and securely. We put a strong emphasis on data security. Beyond the use of authentication, encryption and virtual private network (VPN) technologies to protect customer data, Numerex‘s whole internal organization has undergone ISO/IEC 27001:2005 (international information security standard) scrutiny and certification.

4

We operate in the Business-to-Business (B2B) market, and our customers, in general, serve the final end users. Numerex’s products and services are primarily sold to enterprise and government organizations, some of them with global needs. Our targeted vertical markets include security, energy and utilities, transportation, government, financial services, healthcare and supply chain.

We work with our customers to develop solutions that integrate Numerex DNA®, which is the necessary foundational components, i.e., smart device, cellular and satellite network and software application, of any M2M solution, which we offer through a single source, rather than requiring customers to utilize multiple vendors and partners. We also provide several enabling value-added services.

We accelerate the development process for our customers, through our cloud-based horizontal M2M platform Numerex FAST®, which can be accessed through three service delivery options, separately or combined: Network-as-a-Service (NaaS); Platform-as-a-Service (PaaS); and Software-as-a-Service (SaaS).

In addition to specifically configured business solutions, we sell unbranded, end-user ready (“white label”) solutions typically to channel partners who have well-defined markets that do not necessarily require a configured or customized solution. Examples of such “white label” platforms at Numerex include: security; Location-Based Services (LBS); and a number of additional fixed-wireless or “static” applications.

Our offerings use cellular, satellite, broadband and wireline networks worldwide. We handle all the aspects of international connectivity including any associated regulations, processes and data requirements.

We utilize a diverse range of manufacturing sources and telecommunications standards. We believe that our ability to manage disparate networks and devices while providing customers with a consolidated view of their activity is a unique strength of Numerex. We have repositioned our business to de-emphasize hardware-only sales and to focus on solution and service-based activity and sell hardware that we believe will connect to our platforms in order to generate a subscription and, as a result, recurring revenue.

Besides our above-described core offerings, we offer digital multimedia products and services such as PowerPlay™ to certain customers. They are marketed through value added resellers or VARs and system integrators and managed as a single group. These products and services are not core to the Company’s M2M business and currently comprise about 2% of our annual revenues.

HISTORY

We were first traded publicly in March 1994 on the Nasdaq stock market. At that time, the Company focused on “derived channel”, a wireline-based telemetry data communications solution (“telemetry” is eventually subsumed by the ‘M2M’ acronym) and served select vertical markets that included alarm security and line monitoring. In November 1999, we sold our wireline business to British Telecommunications PLC (“BT”) in order to focus on our nascent wireless data communications business.

In May 1998, Numerex Corp, BellSouth Corporation and BellSouth Wireless, (which became Cingular in 2001 and AT&T in January 2007, following the merger between BellSouth and ATT in December 2006), completed a transaction whereby Cellemetry LLC, a joint venture between Numerex and Cingular, was formed. Cellemetry LLC provided a cost-effective, two-way wireless data communications network throughout the United States, Canada, Mexico, Colombia, Argentina, Paraguay, the Dutch Antilles, and Puerto Rico. On March 28, 2003, we acquired Cingular’s interest in Cellemetry LLC.

During this period, we developed a Short Message Service Center (SMSC)-operated service bureau, “Data1Source,” providing SMS-related services to tier 2 and 3 carriers throughout the USA. While the Data1Source revenue base was subsequently sold, the related technology infrastructure was retained and it helped advance our technical expertise in GSM and CDMA, providing a solid foundation on which to build our current network platforms. In parallel, we expanded our technical platform to serve the mobile tracking and alarm monitoring markets.

At the beginning of 2006, the Company further enhanced its portfolio of wireless products and services through the acquisition of the assets of Airdesk, Inc. Airdesk’s wireless data solutions, network access and technical support have been fully integrated into the Company’s operations.

5

In 2007, Numerex acquired the assets of Orbit One Communications, Inc., which provides satellite data products and services to government agencies and the emergency service market.

In January 2008, Numerex was awarded the international ISO/IEC 27001:2005 Certification (ISO 27001) by BSI Management Systems. ISO 27001 is ISO’s highest security certification for information security that ensures data confidentiality, integrity and availability every step of the way. The ISO 27001 certification facilitates compliance with an array of information security-related legislation and regulations in Numerex’s target markets such as utilities (NERC CIP Cyber Security mandates), financial services (GLBA and PCI DSS), healthcare (HIPAA), government (FISMA), and across markets (state laws governing security breach notification and Sarbanes Oxley Act). In January 2011, Numerex completed the three-year ISO 27001 standard re-certification.

In October 2008, Numerex acquired Ublip, a privately-held M2M software and service company headquartered in Dallas, Texas. With this acquisition, Numerex gained an infusion of technology and expertise, including middleware designed to simplify and jumpstart application development and deployment.

SERVICE DEVELOPMENT PLATFORM AND ENABLING SERVICES

|

v

|

Numerex FAST®

|

Our broad cloud-based M2M horizontal service development platform (Numerex FAST) is an M2M solution foundation with three service delivery options, which can be delivered individually or together: Network-as-a-Service (NaaS); Platform-as-a-Service (PaaS); and Software-as-a-Service (SaaS).

Through Numerex NaaS™,Numerex offers and integrates a variety of cellular, satellite, wired, Wi-Fi and short range wireless options together with critical add-on functionality such as automated activation and provisioning, policy and threshold management, and fraud detection. Numerex NaaS also enables customers to manage devices across multiple network technologies, centralizing account control as well as facilitating network migration strategies.

For M2M developers who want to avoid upfront capital expenditures, minimize risk and benefit from immediate availability of production capabilities, Numerex PaaS™ provides an environment through which they can easily and rapidly develop, run and test their applications. Central to Numerex PaaS, is the ability to have access to a wide range of Numerex-hosted web services such as device management, provisioning, location, mapping, geofencing, geocoding, data mining, and business intelligence.

Numerex SaaS™ gives customers access to specific Numerex-developed M2M applications with various hosting possibilities.

In addition, Numerex has developed a user-friendly customer portal within FAST 3.0, Numerex Passport™, which provides seamless access to critical solution management information as well as all Numerex M2M services including customer care. Numerex Passport is one of the SaaS applications built upon the web services in Numerex PaaS. Customers can use it as a graphical user interface (GUI) outright or incorporate these device management web services into their own application.

Numerex FAST enables multiple devices to be connected to multiple wireless networks through a single application. We offer branding, hosting services, gateway development, extensive device management and application monitoring tools. The availability of Numerex’s application building blocks for “turnkey” use or assembly into more customer-specific solutions allows any developer to quickly build a branded web-based application. Our network features include international roaming service, granular fraud detection, low latency, and managed Quality-of-Service SMS delivery.

|

v

|

Enabling Services

|

We offer an extensive range of products and services that work with our hosted platforms and make integration between smart device, network, and application a seamless process. From asset tracking on a global scale to stationary, or ‘static’, solutions that involve monitoring, measuring, and metering applications, our team of M2M on-boarding specialists and engineers work to optimize commercialization of a solution. Examples of enabling services include: 24x7 customer support; flexible billing; integration services; automated provisioning; device management

6

portal; network operations center; network redundancy; product certification and ancillary services such as but not limited to warehousing and fulfillment.

SALES, MARKETING AND DISTRIBUTION

We sell our configured solutions and related services to, with, and through our strategic partner channels such as system integrators, consultative groups, wireless networks operators, key supply chain partners and large end-user enterprises.

We primarily employ an indirect sales model for our unbranded (“white label”) products through VARs, vertically focused System Integrators (SIs) and Original Equipment Manufacturers (OEMs) who integrate our products and services into their own solutions. We also indirectly market and sell certain Numerex branded products and services through distribution and dealer channels, specifically the Uplink platform. Uplink alarm security products are sold “off the shelf” into distribution and dealers throughout North America.

KEY CUSTOMERS

We have no single customer that accounts for more than 10% of our total revenue.

SUPPLIERS

We rely on third-party contract manufacturers and wireless network operators/ carriers, both in the United States and overseas, to manufacture most of the equipment used to provide our wireless M2M solutions, networking equipment and products, and to provide the underlying network service infrastructure that we use to support our M2M data network, respectively.

COMPETITION

The market for our technology and platforms remains characterized by rapid technological change. The principal competitive factors in this market continue to be product performance, ease of use, reliability, price, breadth of product lines, sales and distribution capability, technical support and service, customer relations, and general industry and economic conditions.

Several businesses that share our M2M space can be viewed as competitors, such as application service providers, Mobile Virtual Network Operators (MVNOs), system integrators, and wireless operators/carriers that offer a variety of the components and services required for the delivery of complete M2M solutions. We believe that we have a competitive advantage and are uniquely positioned since it provides all of the key components of the M2M value chain, including cloud-based enabling platforms, multiple wireless technologies, custom applications, and wireless network services through one single source. We market and sell complete network-enabled solutions, or individual components, based upon the specific needs of the customer. Some module manufacturers have started to market application development platforms while other M2M players offer airtime services, making available to their customers integration capabilities. In addition, there are also a limited number of companies offering end-to-end service delivery platforms.

We believe that our current M2M services, combined with the continuing development of our network offerings and technology, positions us to compete effectively with emerging providers of M2M solutions using Global System for Mobile Communications (GSM), Code Division Multiple Access (CDMA) and satellite technology. Other potentially competitive offerings may include “wireless fidelity” (Wifi), World Interoperability for Microwave Access (WiMAX) and other 3G and 4G (third and fourth generations of cellular wireless standards) technologies and networks. We believe that principal competitive factors when selecting an M2M service or network-only provider are a single interface, network reliability, data security, and customer support.

Our Uplink security products and services have three primary competitors in the existing channels of distribution — Honeywell’s AlarmNet, Telular’s Teleguard and DSC, the security division of Tyco. We believe that the principal competitive factors when making a product selection in the business and consumer security industry are hardware

7

price, service price, reliability, industry certification status and feature requirements for specific security applications, for example fire, burglary, bank vault, etc. Additional competitors have entered the market in the last several years with a focus on blending security monitoring and home automation. These products and services are targeted for the do-it-yourself market as opposed to traditional security dealers. Several companies offer OEM versions or include alarm monitoring technology and network services provided by Numerex. Regarding the transition to 3G, Numerex and its partners intend to continue supporting 2G well into this decade, providing reliable 2G network services while at the same time introducing 3G products for more advanced services. We remain committed to the security marketplace and will always work with our customers to provide the services required to meet their security customer’s needs.

M2M STANDARDIZATION INVOLVEMENT

We believe that sharing our M2M expertise with international groups and forums focused on standards and the industry’s growth is mutually beneficial. Our Chief Technology Officer, Dr. Jeffrey O. Smith completed his term as Chair of Telecommunications Industry Association (TIA) TR-50 Standards Committee on Smart Device Communications, at the end of January 2012. During his term, TIA TR-50 released its first Smart Device Communications Reference Architecture standard in December 2011. Dr. Smith was also confirmed in November 2011 as Chair of the Global Standards Collaboration (GSC) M2M Standardization Task Force (MSTF), which is comprised of all major Standards Developing Organizations from around the world. GSC’s mandates include supporting the International Telecommunication Union (ITU), a specialized agency of the United Nations, as the preeminent global telecommunication and radiocommunication standards development organization. The goal of the GSC MSTF is to foster global coordination and harmonization in the area of M2M standardization. In addition, Numerex’s CEO, Mr. Stratton J. Nicolaides was elected to the board of directors of TIA, a leader in setting standards in the telecommunications arena.

ENGINEERING AND DEVELOPMENT

Our success depends, in part, on our ability to enhance our existing products and introduce new products and applications on a timely basis. We plan to continue to devote a portion of our resources to research and development. Our engineering and development expenses were $2.7 million for the year ended December 31, 2011.

We continue to invest in new services and improvements to our various technologies, especially networks and digital fixed and mobile solutions. We primarily focus on the development of M2M services and enabling platforms, enhancement of our gateway and network services, reductions in the cost of delivery of our solutions, and enhancements and expansion of our application capabilities.

PRODUCT WARRANTY AND SERVICES

Our M2M business typically provides a limited, one-year repair or replacement warranty on all hardware-based products. Our digital multimedia business typically provides a limited one-year warranty on parts and labor. To date, warranty costs and the cost of maintaining our warranty programs have not been material to our business.

INTELLECTUAL PROPERTY

We hold patents either directly (under Numerex Corp) or through our subsidiaries covering the technologies we have developed in support of our product and service offerings in the United States and various other countries. United States Patents have a limited legal lifespan, typically 20 years from the filing date for a utility patent filed on or after June 8, 1995. Our patents expire between March 11, 2014 and September 30, 2028. It is our practice to apply for patents as we develop new technologies, products, or processes suitable for patent protection. No assurance can be given about the scope of the patent protection.

We also hold other intellectual property rights including, without limitation, copyrights, trademarks, and trade secret protections relating to our technology, products, and processes. We believe that rapid technological developments in the telecommunications and locate-bases services industries may limit the protection afforded by patents.

8

In an effort to maintain the confidentiality and ownership of our trade secrets and proprietary information, we require all of our employees and consultants to sign confidentiality agreements. Employees and consultants involved in technical endeavors also sign invention assignment agreements.

REGULATION

Federal, state, and local telecommunications laws and regulations have not posed any significant impediments to either the delivery of wireless data signals/messaging or services using our various platforms. However, we may be subject to certain governmentally imposed taxes, surcharges, fees, and other regulatory charges, as well as new laws and regulations governing fixed and mobile communications devices, associated services, our business and markets. As we expand our international sales, we may be subject to telecommunications regulations in those foreign jurisdictions.

Employees

As of March 15, 2012, we had 133 employees in the U.S., consisting of 29 in sales, marketing and customer service, 71 in engineering and operations and 33 in management and administration. We have experienced no work stoppages and none of our employees are represented by collective bargaining arrangements. We believe our relationship with our employees is good.

Available Information

We make available free of charge through our website at www.numerex.com our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, and all amendments thereto filed or furnished pursuant to 13(a) or 15(d) of the Securities and Exchange act of 1934, as soon as reasonably practicable after such reports are filed with or furnished to the Securities and Exchange Commission. Our filings are also available through the Securities and Exchange Commission via their website, http://www.sec.gov. You may also read and copy any materials we file with the SEC at the SEC's Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The information contained on our website is not incorporated by reference in this annual report on form 10-K and should not be considered a part of this report.

Executive Officers of the Registrant

Our executive officers, and all persons chosen to become executive officers, and their ages and positions as of March 15, 2012, are as follows:

|

Name

|

Age

|

Position

|

|

Stratton J. Nicolaides*

|

58

|

Chairman of the Board of Directors, Chief Executive Officer

|

|

Michael A. Marett

|

57

|

Chief Operating Officer

|

|

Alan B. Catherall

|

58

|

Chief Financial Officer

|

|

Louis Fienberg

|

57

|

Executive Vice President, Corporate Development

|

|

Jeff Smith, PhD

|

51

|

Chief Technology Officer

|

*Member of the Board of Directors

Mr. Nicolaides has served as Chief Executive Officer of the Company since April 2000, having served as Chief Operating Officer from April 1999 until March 2000 and as Chairman of the Board since December 1999. Mr. Nicolaides is a member of the Board of Directors for the Telecommunications Industry (TIA) as well as the Taylor Hooten Foundation..

9

Mr. Marett has been an Officer of the Company since February 2001. In February 2005 he was named Chief Operating Officer. From 1999 to 2001, Mr. Marett was Vice President, Sales and Marketing, of TManage, Inc., which provided planning, installation, and support services to companies with large remote workforces. From 1997 to 1999 Mr. Marett was Vice President, Business Development, of Mitel Business Communications Systems, a division of Mitel Corporation. Prior to 1997, Mr. Marett held a number of executive positions at Bell Atlantic.

Mr. Catherall has been the Chief Financial Officer of the Company since June 2003. From 1998 to 2002, Mr. Catherall served as Chief Financial Officer of AirGate PCS, a NASDAQ-listed wireless company. From 1996 to 1998, Mr. Catherall was a partner in Tatum CFO LLP, a financial services consulting company. Prior to 1996, he held a number of executive and management positions at MCI Communications.

Mr. Fienberg serves as the Company’s Executive Vice President for Corporate Development and has been with the Company since July 2004. From August 2003 to July 2004, Mr. Fienberg served as Managing Director of an investment banking firm. From 1992 to 2003, Mr. Fienberg was a Senior Vice President and merger and acquisition specialist with Jefferies and Company, Inc.

Dr. Smith has served as the Chief Technology Officer since October 9, 2008. From June 2007 to October 2008, he served as the President and Chief Executive Officer of Ublip, Inc. a provider of M2M and location based services that Dr. Smith founded. From January 2002 until June 2007, Dr. Smith served as President and Chief Executive Officer of SensorLogics, Inc., an M2M application service provider that he also founded. From June 1996 until January 2000, Dr. Smith served as regional President and director of NTT/Verio, an internet service provider and web hosting company. From October 1993 until January 1997, he served as President and Chief Executive Officer of OnRamp Technologies, an internet service provider that he co-founded.

10

Item 1A. Risk Factors

An investment in our common stock involves a high degree of risk. You should carefully consider the following information about these risks before buying shares of our common stock. The following risks and uncertainties are not the only ones facing us. Additional risks and uncertainties of which we are unaware or we currently believe are not material could also adversely affect us. In any case, the value of our common stock could decline, and you could lose all or part of your investment. You should also refer to the other information contained in this Annual Report on Form 10-K for the year ended December 31, 2011 (the Annual Report) or incorporated herein by reference, including our consolidated financial statements and the notes to those statements. See also, “Special Note Regarding Forward-Looking Statements.”

We have a history of losses and are uncertain as to our future profitability.

We have had mixed success with regard to generating profits. While we were profitable in 2011, we incurred losses in 2008, 2009, and 2010. As a holding company our primary material assets are our ownership interests in our subsidiaries and in certain intellectual property rights. Consequently, our earnings derive from our subsidiaries and we depend on accumulated cash flows, distributions, and other inter-affiliate transfers from our subsidiaries. In view of our history of losses, operating costs, and all other risk factors discussed in this Annual Report, we may not be profitable in the future.

Adverse macroeconomic conditions could magnify our customers’ current financial difficulties.

We provide solutions that are resold by our customers – primarily value-added resellers whose customers are end users of our solutions and distributors who sell to other resellers of our solutions. Many of our customers operate on narrow margins and have been adversely affected by current overall economic conditions. Current economic conditions, while improving by some measures, continue to negatively impact demand for our customers’ solutions, reducing their demand for our solutions. Our customers may also face higher financing and operating costs. If current economic conditions do not improve or worsen, we may experience reduced revenue growth or a decrease in revenues and an increase in expenses, particularly in the form of bad debt on the part of our customers. All of these and other macroeconomic factors could have a material adverse effect on demand for our solutions and on our financial condition and operating results.

We are also likely to experience greater pressure to reduce pricing and accept lower margins as we compete for customers subject to similar constraints on their pricing and margins. While our largest customers have been less affected by the current economy, if current adverse economic conditions persist or worsen, those customers could begin to be affected in a similar manner.

In particular, we anticipate that continued sluggishness in the new housing sector will impair sales of our residential alarm monitoring solutions, since customers may purchase our security systems in connection with the purchase of a new residence.. If overall conditions worsen significantly, residential and commercial consumers may also decide to cancel wireless monitoring services in an effort to eliminate expenses viewed as discretionary or non-critical. Similarly, a reversal of the current uptick in vehicle sales would negatively impact sales of our vehicle tracking solutions.

The markets in which we operate are highly competitive, and we may not be able to compete effectively.

We sell our products in intensely competitive markets. Some of our competitors and potential competitors have significantly greater financial, technical, sales and marketing and other resources than we do. Existing or new products and services that provide alternatives to our products and services could materially impact our ability to compete in these markets. As the markets for our products and services continue to develop, additional companies, including companies with significant market presence in the M2M industry, could enter the markets in which we compete and further intensify competition. In addition, we believe price competition could become a more significant competitive factor in the future. As a result, we may not be able to maintain our historic prices and margins, which could adversely affect our business, results of operations and financial condition.

As a further result of such competition, our new solutions could fail to gain market acceptance. Over the past several years, we have introduced a system enabling alarm signals to be transmitted digitally over cellular networks to central

11

monitoring stations; a cellular and GPS-based vehicle tracking solution; a satellite-based mobile asset monitoring and tracking solution; enhanced “back end” services and application development platforms. If these solutions and services, or any of our other existing solutions and services, do not perform as expected, or if our sales fall short of expectations, our business may be adversely affected.

We operate in new and rapidly evolving markets where rapid technological change can quickly make hardware solutions and services, including those that we offer, obsolete.

The markets we operate in are subject to rapid advances in technology, continuously evolving industry standards and regulatory requirements, and ever-shifting customer requirements. The M2M industry, in particular, is currently undergoing profound and rapid technological change. For example, most of the current subscribers we host connect to cellular networks using 2G-based devices. At least one major wireless carrier we utilize has signaled that it intends to fully transition to 3G-based architecture and therefore plans to cease supporting 2G-based devices in the near future. While we are beginning to market, sell, and support 3G-based devices and service, we may not be successful in transitioning all of our 2G-based subscribers to 3G and may lose customers as a result. The introduction of unanticipated new technologies by carriers, or the development of unanticipated new end applications by our customers, could render our current solutions obsolete. In that regard, we must discern current trends and anticipate an uncertain future. We must engage in product development efforts in advance of events that we cannot be sure will happen and time our production cycles and marketing activities accordingly. If our projections are incorrect, or if our product development efforts are not properly directed and timed, or if the demands of the marketplace shift in directions that we failed to anticipate, we may lose market share and revenues as a result. To remain competitive, we continue to support engineering and development efforts intended to bring new hardware solutions and services to the markets that we serve. However, those efforts are capital intensive. If we are unable to adequately fund our engineering and development efforts, we may not be successful in keeping our product line current with advances in technology and evolving customer requirements. Even with adequate funding, our development efforts may not yield any appreciable short-term results and may never result in hardware solutions and services that produce revenues over and above our cumulative development costs or that gain traction in the marketplace, causing us to either lose market share or fail to increase and forego increased sales and revenues as a result.

We experience long sales cycles for some of our solutions.

Certain of our product offerings are subject to long sales cycles in view of the need for testing of our hardware solutions and services in combination with our customers’ applications and third parties’ technologies, the need for regulatory approvals and export clearances, and the need to resolve other complex operational and technical issues. For example, in the government contracting arena in particular, longer sales cycles are reflective of the fact that government contracts can take months or longer to progress from a “request for proposal” to a finalized contract document pursuant to which we are able to sell a finished product or service. Terms and conditions of sale unique to the government sector may also affect when we are able to recognize revenues. Delays in sales could cause significant variability in our revenue and operating results for any particular period. For that reason, quarter-over-quarter comparisons of our financial results may not always be meaningful.

We face substantial inventory and other asset risk in addition to purchase commitment cancellation risk.

We record a write-down for product and component inventories that have become obsolete or exceed anticipated demand or net realizable value and accrue necessary cancellation fee reserves for orders of excess products and components. We also review our long-lived assets for impairment whenever events or changed circumstances indicate the carrying amount of an asset may not be recoverable. If we determine that impairment has occurred, it records a write-down equal to the amount by which the carrying value of the assets exceeds its fair market value. Although we believe its provisions related to inventory, other assets and purchase commitments are currently adequate, no assurance can be given that we will not incur additional related charges given the rapid and unpredictable pace of product obsolescence in the industries in which we compete. Such charges could materially adversely affect our financial condition and operating results.

We are contractually obligated to provide our manufacturers and network service providers with forecasts of our demand for components of our hardware solutions and network capacity. Specific terms and conditions vary by contract, however, if our forecasts do not result in the production of a quantity of units or network capacity sufficient to meet demand we may be subject to contractual penalties under some of our contracts with our customers. By contrast, overproduction of units based on forecasts that that overestimate demand could result in an accumulation of excess inventory that, under some of our contracts with our customers, would have to be managed at our expense thus adversely impacting our margins.

12

Excess inventory that becomes obsolete or that we are otherwise unable to sell would also be subject to write-offs resulting in adverse affects on our margins. Because our markets are volatile, competitive and subject to rapid technology and price changes, there is a risk that we will forecast incorrectly and order excess or insufficient amounts of components or products, or not fully utilize firm purchase commitments. Our financial condition and operating results could in the future be materially adversely affected by tour ability to manage our inventory levels and respond to short-term shifts in customer demand patterns.

If we achieve our growth goals, we may be unable to manage our resulting expansion.

To the extent that we are successful in implementing our business strategy, we may experience periods of rapid expansion. In order to effectively manage growth, whether organic or through acquisitions, we will need to maintain and improve our operations and effectively train and manage our employees. Our expansion through acquisitions is contingent on successful management of those acquisitions, which will require proper integration of new employees, processes and procedures, and information systems, which can be both difficult and demanding from an operational, managerial, cultural, and human resources perspective. We must also expand the capacity of our sales and distribution networks in order to achieve continued growth in our existing and future markets. The failure to manage growth effectively in any of these areas could have a material adverse effect on our financial condition and operating results.

We are dependent on third party telecommunications service providers and other suppliers, including domestic and international cellular and satellite carriers and hardware manufacturers, the loss of any one of which could adversely impact our ability to supply or service our customers.

Our long-term success depends on our ability to operate, manage, and maintain a reliable and cost effective network, as well as our ability to keep pace with changes in technology. The loss or disruption of key telecommunications infrastructure and key wireless and satellite-based network services supplied to us by carriers in the U.S., Canada, Mexico, Europe, and other locations overseas would unfavorably impact our ability to adequately service our customers. If we experience technical or logistical impediments to our ability to transfer traffic to third party facilities, or if our third party carriers experience technical or logistical difficulties of their own, such as disruptions to their supply chains caused by weather events, natural disasters, or terrorism, and are unable to carry our network

traffic, we may not achieve our revenue goals or otherwise be successful in growing our business. Given our dependence on cellular and satellite telecommunications service providers, risks specific or unique to their technologies, i.e., the loss or malfunction of a cell tower, a satellite, or a satellite ground station, should also be viewed as having the potential to impair our ability to provide services.

We outsource our hardware manufacture to independent companies and do not have internal manufacturing capabilities to meet the demands of our customers. Any delay, interruption, or termination of our hardware manufacture could harm our ability to provide our solutions to our customers and, consequently, could have a material adverse effect on our business and operations. Our hardware manufacture requires specialized know-how and capabilities possessed by a limited number of enterprises. Consequently, we are reliant on just a few manufacturers. If a key supplier experiences production problems, financial difficulties, or has difficulties with its supply chain as a result of severe weather, a natural disaster, terrorism, or other unforeseen event, we may not be able to obtain enough units to meet demand, which could result in failure to meet our contractual commitments to our customers, further causing us to lose sales and generate less revenue.

We may experience quality problems from time to time, resulting in decreased sales and operating margins and the loss of customers.

While we test our products and services, they may still have errors, defects, or bugs that we find only after commercial production has begun. In the past, we have experienced errors, defects, and bugs in connection with new solutions. Our customers may not make purchases from us, or may make fewer purchases, if they are concerned about such problems. Furthermore, correcting problems could require additional capital expenditures, result in increased design and development costs, and force us to divert resources from other efforts. Failure to remediate problems could result in lost revenue, harm our reputation, and lead to costly warranty or other legal claims against us by our customers, and could have a material adverse impact on our financial condition and operating results. Historically, the time required for us to correct problems has caused delays in product shipments and has resulted in lower than expected revenues.

Interruptions in service or performance problems, no matter what their ultimate cause, could undermine confidence in our services and cause us to lose customers or make it more difficult to attract new customers. In addition, because most of our customers are businesses, any significant interruption in service could result in lost profits or other losses to our customers. It may also be difficult to identify the source of the problem due to the overlay of our network with cellular, and/or satellite networks and our network’s reliance on those other networks. The occurrence of hardware or software errors, regardless of whether such errors are caused by our hardware solutions or services, or our internal facilities, may result in the delay or loss of market acceptance of our solutions, and any necessary revisions may result in significant and additional expenses. Although we attempt to disclaim or limit our liability for hardware, system, and software failures in our agreements with our customers, a court may not enforce a limitation of liability, which could expose us to substantial losses.

13

If our goodwill or amortizable intangible assets become impaired we may be required to record a significant charge to earnings.

Under generally accepted accounting principles, we review our amortizable intangible assets for impairment when events or changes in circumstances indicate the carrying value may not be recoverable. Goodwill is tested for impairment at least annually. Factors that may be considered a change in circumstances, indicating that the carrying value of our goodwill or amortizable intangible assets may not be recoverable, include a decline in stock price and market capitalization, reduced future cash flow estimates, and slower growth rates in our industry. We may be required to record a significant charge in our financial statements during the period in which any impairment of our goodwill or amortizable intangible assets is determined, negatively impacting our results of operations.

A natural disaster, terrorist attack, or other catastrophic event could diminish our ability to provide service and hardware to our customers and our revenues may be impacted by weather patterns and climate change.

Events such as severe storms, tornadoes, earthquakes, floods, solar flares, industrial accidents, and terrorist attacks including, without limitation, the actions of computer hackers, could damage or destroy both our primary and redundant facilities as well as the facilities and operations of third party cellular and satellite carriers and hardware suppliers we are reliant on, which could result in a significant disruption of our operations. Further, in the event of an emergency, the telecommunications networks that we rely upon may become capacity constrained or preempted by governmental authorities. We may also be unable, due to loss of personnel or the inability of personnel to access our

facilities, to provide some services to our customers or maintain all of our operations for a period of time. With respect to our satellite-based mobile asset tracking solution in particular, sales may be influenced by weather patterns and climate change. For example, if government agencies and emergency responders anticipate relatively “mild” weather over one or more storm seasons on account of cyclical weather patterns or long-term climate change, they may buy fewer of our mobile asset tracking units for deployment in support of disaster response operations.

The loss of a few key personnel could have an adverse affect on us in the short-term.

Due to the specialized knowledge and skills each of our executive officers and other key employees possesses with respect to the development and maintenance and our operations, the loss of service of any of our officers. Any unplanned turnover could diminish our institutional knowledge base and erode our competitive advantage. We may need to hire additional personnel in the future, and we believe the success of the combined business depends, in large part, upon our ability to attract and retain key employees. The loss of the services of any key employees, the inability to attract or retain qualified personnel in the future, or delays in hiring required personnel could limit our ability to generate revenues and to operate our business.

We may require additional capital to fund further development, and our competitive position could decline if we are unable to obtain additional capital, or access the credit markets.

To address our long-term capital needs, we intend to continue to pursue strategic relationships that would provide resources for the further development of our product candidates. There can be no assurance, however, that these discussions will result in relationships or additional funding. In addition, we may seek to raise capital through the public or private sale of securities, if market conditions are favorable for doing so. If we are successful in raising additional funds through the issuance of equity securities, stockholders will likely experience dilution, or the equity securities may have rights, preferences, or privileges senior to those of the holders of our common stock. If we raise funds through the issuance of debt securities, those securities would have rights, preferences, and privileges senior to those of our common stock.

14

Our Loan and Security Agreement with Silicon Valley Bank, or SVB, contains financial and operating restrictions that may limit our access to credit. If we fail to comply with covenants in the SVB Credit Facility, we may be required to repay any potential indebtedness thereunder, which may have an adverse effect on our liquidity.

In May 2011, we amended our Loan and Security Agreement (the “Agreement”) with SVB to increase the credit facility from $5 million to $10 million, among other changes. Provisions in the Agreement impose restrictions on our ability to, among other things:

• incur additional indebtedness;

•create liens;

•enter into transactions with affiliates;

•transfer assets;

•pay dividends or make distributions on, or repurchase our stock; or

•merge or consolidate.

In addition, we are required to meet certain financial covenants and ratios customary with this type of credit facility. The SVB credit facility also contains other customary covenants. We may not be able to comply with these covenants in the future. Our failure to comply with these covenants may result in the declaration of an event of default and could cause us to be unable to borrow under the SVB credit facility. In addition to preventing additional borrowings under the SVB credit facility, an event of default, if not cured or waived, may result in the acceleration of the maturity of indebtedness outstanding under the SVB credit facility, which would require us to pay all amounts outstanding. If an event of default occurs, we may not be able to cure it within any applicable cure period, if at all. If the maturity of our indebtedness is accelerated, we may not have sufficient funds available for repayment or we may not have the ability to borrow or obtain sufficient funds to replace the accelerated indebtedness on terms acceptable to us, or at all.

We are subject to risks associated with laws, regulations and industry-imposed standards related to fixed and mobile communications devices and associated services.

Laws and regulations related to fixed and mobile communications devices and associated services and end applications are extensive, vary by jurisdiction, and are subject to change. Such changes, could include, without limitation, restrictions on the production, manufacture, distribution, and use of communications devices, restrictions on the ability to port devices and associated services to new carriers’ networks, requirements to make devices and associated services compatible with more than one carrier’s network, or restrictions on end use could, by preventing us from fully serving affected markets, have a material adverse effect on our financial condition and operating results.

In particular, communication devices we sell, or which our customer wish us to support, are subject to regulation or certification by governmental agencies such as the Federal Communications Commission (FCC), industry standardization bodies such as the PCS Type Certification Review Board (PTCRB), and particular carriers for use on their networks. The procedures for obtaining required regulatory approvals and certifications are extensive and time consuming, and can require us to conduct additional testing requirements, makes modifications to our hardware solutions and services, or delay in product launch and shipment dates, which could have a material adverse effect on our financial condition and operating results.

We may be subject to breaches of its information technology systems, which could damage our reputation, vendor, and customer relationships, and our customers’ access to our services.

Our business requires it to use and store customer, employee, and business partner personally identifiable information (PII). This may include names, addresses, phone numbers, email addresses, contact preferences, tax identification numbers, and payment account information. We require user names and passwords in order to access its information technology systems. We also uses encryption and authentication technologies to secure the transmission and storage of data.

These security measures may be compromised as a result of third-party security breaches, employee error, malfeasance, faulty password management, or other irregularity, and result in persons obtaining unauthorized access to our data or accounts. Third parties may attempt to fraudulently induce employees or customers into disclosing user names, passwords or other sensitive information, which may in turn be used to access our information technology systems. If a computer security breach affects our systems or results in the unauthorized release of PII, tour reputation and brand could be materially damaged and use of our products and services could decrease.

15

We would also be exposed to a risk of loss or litigation and possible liability, which could result in a material adverse effect on our business, results of operations and financial condition.

Our business is subject to a variety of U.S. and international laws, rules, policies and other obligations regarding data protection.

We are subject to federal, state and international laws relating to the collection, use, retention, security and transfer of PII. In many cases, these laws apply not only to third-party transactions, but also to transfers of information between the Company and our subsidiaries, and among the Company, our subsidiaries and other parties with which we have commercial relations. Several jurisdictions have passed new laws in this area, and other jurisdictions are considering imposing additional restrictions. These laws continue to develop and may be inconsistent from jurisdiction to jurisdiction. Complying with emerging and changing international requirements may cause us to incur substantial costs or require us to change its business practices. Noncompliance could result in penalties or significant legal liability.

Our privacy policies and practices concerning the use and disclosure of data are posted on its website and its customer contracts. Any failure by the Company, our suppliers or other parties with whom we do business to comply with our posted privacy policies or with other federal, state or international privacy-related or data protection laws and regulations could result in proceedings against us by governmental entities or others, which could have a material adverse effect on our business, results of operations and financial condition.

The Company is also subject to payment card association rules and obligations under its contracts with payment card processors. Under these rules and obligations, if information is compromised, we could be liable to payment card issuers for the cost of associated expenses and penalties. In addition, if we fail to follow payment card industry security standards, even if no customer information is compromised, we could incur significant fines or experience a significant increase in payment card transaction costs

Changes in domestic tax regulations or unanticipated foreign tax liabilities could affect our results.

The issuance by the Internal Revenue Service and/or state tax authorities of new tax regulations or changes to existing standards and actions by federal, state or local tax agencies and judicial authorities with respect to applying applicable tax laws and regulations could impose costs on us that we are unable to fully recover.

We are doing business in, and are expanding into, foreign tax jurisdictions. We believe that we have complied in all material respects with our obligations to pay taxes in these jurisdictions. If the applicable taxing authorities were to challenge successfully our current tax positions, or if there were changes in the manner in which we conduct our activities, we could become subject to material unanticipated tax liabilities. We may also become subject, prospectively or retrospectively, to additional tax liabilities following changes in tax laws. The application of existing, new or future laws could have adverse effects on our business, prospects and operating results. There have been, and will continue to be, substantial ongoing costs associated with complying with the various indirect tax requirements in the numerous markets in which we conduct or will conduct business.

A portion of our future revenue, in particular the revenue deriving from our sale of satellite-based mobile asset tracking solutions, may be derived from contracts with the U.S. government, state governments, or government contractors Those contracts are subject to uncertain funding.

The funding of government programs is uncertain and, at the federal level, is dependent on continued congressional appropriations and administrative allotment of funds based on an annual budgeting process. We cannot assure you that current levels of congressional funding for programs supporting by our offerings will continue, particularly as result of the Budget Control Act and the mandated substantial automatic spending cuts beginning in 2013 and lasting for 10 years, unless Congress modifies these cuts. In particular, a significant portion of our revenues from the sale of satellite-based tracking solutions through our location-based services division has been derived from sales made by us indirectly as a subcontractor to a prime government contractor that has the direct relationship with the U.S. government. In addition, these cuts could adversely affect the viability of the prime contractor of our program. If the prime contractor loses business with respect to which we serve as a subcontractor, our government business would be hurt. We also maintain a Federal Supply Schedule with the General Services Administration under which we do business directly with the U.S. government. If we, as the prime contractor, were to lose some or all of such business, our revenues derived from the sale of satellite-based tracking solutions would suffer as a result.

16

Our operating results may be negatively affected by developments affecting government programs generally, including the following:

|

·

|

changes in government programs that are related to our hardware solutions and services;

|

|

·

|

adoption of new laws or regulations relating to government contracting or changes to existing laws or regulations;

|

|

·

|

changes in political or public support for programs;

|

|

·

|

delays or changes in the government appropriations process; and

|

|

·

|

delays in the payment of invoices by government payment offices and the prime contractors.

|

These developments and other factors could cause governmental agencies to reduce their purchases under existing contracts, to exercise their rights to terminate contracts at-will or to abstain from renewing contracts, any of which would cause our revenue to decline and could otherwise harm our business, financial condition and results of operations. For example, many of the ultimate consumers of our PowerPlay™ hardware and services are elementary and secondary schools that pay for their purchases with funding that they receive through the Schools and Libraries Program (commonly known as the “E-Rate Program”) of the Universal Service Fund, which is administered by the Universal Service Administrative Company (USAC) under the direction of the FCC. Demand for solutions and services under the E-Rate Program is very difficult to predict and changes in the program itself could also affect demand.

Government contracts contain provisions that are unfavorable to us.

Government contracts contain provisions, and are subject to laws and regulations, that give the government rights and remedies not typically found in commercial contracts. These provisions may allow the government to

|

·

|

Terminate existing contracts for convenience, as well as for default;

|

|

·

|

Reduce or modify contracts or subcontracts;

|

|

·

|

Cancel multi-year contracts and related orders if funds for contract performance for any subsequent year become unavailable;

|

|

·

|

Decline to exercise an option to renew a multi-year contract;

|

|

·

|

Claim rights in our hardware solutions and services;

|

|

·

|

Suspend or debar us from doing business with the federal government or with a governmental agency; and

|

|

·

|

Control or prohibit the export of our hardware solutions and services.

|

If the government terminates a contract for convenience, we may recover only our incurred or committed costs, settlement expenses and profit on work completed prior to the termination. If the government terminates a contract for default, we may not recover even those amounts, and instead may be liable for excess costs incurred by the government in procuring undelivered items and services from another source. We may experience performance issues on some of our contracts. We may receive show cause or cure notices under contracts that, if not addressed to the government’s satisfaction, could give the government the right to terminate those contracts for default or to cease procuring our services under those contracts in the future.

Agreements with government agencies may lead to regulatory or other legal action against us including, without limitation, claims against us under the Federal False Claims Act or other federal statutes. These claims could result in substantial fines and other penalties.

We must comply with a complex set of rules and regulations applicable to government contractors and their subcontractors. Failure to comply with an applicable rule or regulation could result in our suspension of doing business with the government or with the prime government contractors that do business with or cause us to incur substantial penalties. Our agreements with the U.S. government are subject to substantial financial penalties under the Civil Monetary Penalties Act and the False Claims Act and, in particular, actions under the False Claims Act’s “whistleblower” provisions. Private enforcement of fraud claims against businesses on behalf of the U.S. government has increased due in large part to amendments to the False Claims Act that encourage private individuals to sue on behalf of the government. These whistleblower suits by private individuals, known as qui tam actions, may be filed by almost anyone, including present and former employees. The False Claims Act statute provides for treble damages and up to $11,000 per claim on the basis of the alleged claims. Prosecutions, investigations or qui tam actions could have a material adverse effect on our liquidity, financial condition and results of operations.

17

Finally, various state false claim and anti-kickback laws also may apply to us. Violation of any of the foregoing statutes can result in criminal and/or civil penalties that could have a material adverse effect our business.

We operate internationally, which subjects us to international regulation and business uncertainties that create additional risk for us.

We have been doing business directly, or via our distributors, in Australia, Canada, Mexico, and Pakistan, and are expanding, directly or via our distributors, into additional countries in Latin America, Europe, the Middle East, and Asia. Accordingly, we or our distributors are subject to additional risks, such as:

|

·

|

a continued international economic downturn;

|

· export control requirements, including restrictions on the export of critical technology;

· restrictions imposed by local laws and regulations;

· restrictions imposed by local product certification requirements;

· currency exchange rate fluctuations;

· generally longer receivable collection periods and difficulty in collecting accounts receivable;

· trade restrictions and changes in tariffs;

· difficulties in repatriating earnings;

· difficulties in staffing and managing international operations; and

· potential insolvency of channel partners.

We have only limited experience in marketing and operating our services in certain international markets. Moreover, we have in some cases experienced and expect to continue to experience in some cases higher costs as a percentage of revenues in connection with establishing and providing services in international markets versus the U.S. In addition, certain international markets may be slower than the U.S. in adopting the outsourced communications solutions and so our operations in international markets may not develop at a rate that supports our level of investments.

Furthermore, because regulatory schemes vary by country, we may also be subject to regulations in foreign countries of which we are not presently aware. If that were to be the case, we could be subject to sanctions by a foreign government that could materially and adversely affect our ability to operate in that country. We cannot assure you that any current regulatory approvals held by us are, or will remain, sufficient in the view of foreign regulatory authorities, or that any additional necessary approvals will be granted on a timely basis or at all, in all jurisdictions in which we wish to operate, or that applicable restrictions in those jurisdictions will not be unduly burdensome. The failure to obtain the authorizations necessary to operate satellites internationally could have a material adverse effect on our ability to generate revenue and our overall competitive position. We, our customers and companies with whom we do business may be required to have authority from each country in which we or they provide services or provide our customers use of our hardware solutions and services. Because regulations in each country are different, we may not be aware if some of our customers and/or companies with which we do business do not hold the requisite licenses and approvals.

Unfavorable results of legal proceedings could materially adversely affect us.

We are subject to various legal proceedings and claims that have arisen out of the ordinary conduct of our business and are not yet resolved and additional claims may arise in the future. Results of legal proceedings cannot be predicted with certainty. Regardless of its merit, litigation may be both time-consuming and disruptive to our operations and cause significant expense and diversion of management attention. In recognition of these considerations, we may enter into material settlements. Should we fail to prevail in certain matters, or should several of these matters be resolved against us in the same reporting period, we may be faced with significant monetary damages or injunctive relief against us that would materially adversely affect a portion of our business and might materially affect our financial condition and operating results.

The loss of intellectual property protection both U.S. and international could have a material adverse effect on our operations.

Our future success and competitive position depend upon our ability to obtain and maintain intellectual property protection, especially with regard to our core business. We cannot be sure that steps taken by us to protect our technology will prevent misappropriation of the technology. Our services are highly dependent upon our technology and the scope and limitations of our proprietary rights therein. If our assertion of proprietary rights is held to be invalid, or if another party’s use of our technology were to occur to any substantial degree, our business, financial condition and results of operations could be materially adversely affected. In order to protect our technology, we rely on a combination of patents, copyrights, and trade secret laws, as well as certain customer licensing agreements, employee and customer confidentiality and non-disclosure agreements, and other similar arrangements. Loss of such protection could compromise any advantage obtained and, therefore, impact our sales, market share, and results. To the extent that our licensees develop inventions or processes independently that may be applicable to our hardware solutions and services, disputes may arise as to the ownership of the proprietary rights to this information. These inventions or processes will not necessarily become our property, but may remain the property of these persons or their full-time employers. We could be required to make payments to the owners of these inventions or processes, in the form of either cash or equity, or a combination of both.

Furthermore, our future or pending patent applications may not be issued with the scope of the claims sought by us, if at all. In addition, others may develop technologies that are similar or superior to our technology, duplicate our technology or design around the patents owned or licensed by us. Effective patent, trademark, copyright, and trade secret protection may be unavailable or limited in foreign countries where we may need protection.

18

We rely on access to third-party patents and intellectual property, and our future results could be materially adversely affected if we are unable to secure such access in the future.

Many of our hardware solutions and services are designed to include third-party intellectual property, and in the future we may need to seek or renew licenses relating to such intellectual property. Although we believe that, based on past experience and industry practice, such licenses generally can be obtained on reasonable terms, there is no assurance that the necessary licenses would be available on acceptable terms or at all. Some licenses we obtain may be nonexclusive and, therefore, our competitors may have access to the same technology licensed to us. If we fail to obtain a required license or are unable to design around a patent, we may be unable to sell some of our hardware solutions and services, and there can be no assurance that we would be able to design and incorporate alternative technologies, without a material adverse effect on our business, financial condition, and results of operations.

Our competitors have or may obtain patents that could restrict our ability to offer our hardware solutions and services, or subject us to additional costs, which could impede our ability to offer our hardware solutions and services and otherwise adversely affect us. We may, from time to time, also be subject to litigation over intellectual property rights or other commercial issues.