Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT ON FORM 8-K - Clearwater Paper Corp | d312308d8k.htm |

Clearwater Paper Corporation

Vertical Partners Global Paper & Packaging Conference

March 8, 2012 |

1

Forward-Looking Statements

•

difficulties

with

the

completion

of

our

new

tissue

manufacturing

and

converting

facilities,

including

the

completion

of

our

new

through-air-dried

paper

machine;

•

difficulties with the integration process or the realization of the benefits expected from

our acquisition of Cellu Tissue; •

changes in raw material and energy costs, including changes in the cost and availability of

wood fiber and wood pulp; •

changes in freight costs and disruptions in transportation services;

•

the loss of large customers;

•

customers' product preferences;

•

changes in the United States and international economies;

•

cyclical industry conditions;

•

competitive pricing pressure for the company's products;

•

reliance on a limited number of third-party suppliers of raw materials;

•

an inability to successfully implement our expansion strategies;

•

labor disruptions;

•

unanticipated manufacturing disruptions;

•

changes in general and industry-specific laws and regulations; and

•

unforeseen environmental liabilities or expenditures.

Forward-looking statements contained in this presentation present management’s

views only as of the date of this presentation. We undertake no obligation to publicly update forward-

looking statements, whether as a result of new information, future events or otherwise.

This presentation contains, in addition to historical information, certain

forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including

statements regarding our strategies to grow our business, optimize profitability and build a

high performance culture, the expected delivery and budget relating to our new tissue

machine and converting lines in Shelby, North Carolina, expected future cost savings from

cost synergies relating to our Cellu Tissue acquisition, efficiency projects and reductions to

our cost structure, including our Lean manufacturing program, future growth and market

opportunities, including in the eastern U.S., internal and external pulp purchases and transfers,

internal pulp production and requirements, customer purchases of Private Label tissue,

production capacity of operating divisions, our share repurchase program and the expected

benefit thereof, our capital allocation objectives, our financial priorities such as growing

free cash flow and maintaining modest leverage, estimated annual EBITDA sensitivities, sales

volumes, input costs, and our financial condition and results of operations. Words such as

“anticipate,” “expect,” “intend,” “will,” “plan,” “goals,” “target,” “project,” “believe,” “schedule,”

“estimate,” “may,” and similar expressions are intended to identify such

forward-looking statements. These forward-looking statements are based on management’s current

expectations, estimates, assumptions and projections that are subject to change. Our actual

results of operations may differ materially from those expressed or implied by the forward-

looking statements contained in this presentation. Important factors that could cause or

contribute to such differences include the risk factors described in Item 1A of Part I of our Form

10-K for the year ended December 31, 2011, as well as the following:

|

2

•

We are a company formed in late 2008 with

more than 60 years of operating history

•

A leader in Private Label consumer tissue and

bleached paperboard

•

Focused on producing high quality products that

help our customers build their brands

•

Operate

in

two

segments

of

similar

size

¹

–

Pulp and Paperboard: 43%

–

Consumer Products: 57%

•

Financial overview

–

2011 Net Sales: $1.9 billion

–

2011

Adjusted

EBITDA:

$195.5

million

²

–

5 year average annual Free Cash Flow (FCF)

generation

(2007-2011):

$48.0

million

²

1

Based on net sales for 2011

Introduction to Clearwater Paper

2

See

“Appendix:

Detailed

Financials”

for

the

definition

of

Adjusted

EBITDA

and

Free

Cash

Flow

as

well

as

the

reconciliation to the most comparable GAAP measures |

3

•

Lead Private Label quality

•

Expand geographically

•

Expand retail channel

penetration

Our Strategy

•

Improve sales mix

•

Reduce costs

•

Continue to improve quality

•

Develop common culture

•

Drive for results

•

Attract and retain high

performers

Build a High

Performance

Culture

Optimize

Profitability of

Paperboard

Business

Grow our Tissue

Business |

4

•

Expansion of the Consumer Products Segment:

–

acquisition of Cellu Tissue, and

–

start up of two new converting lines and initiation of construction of our new

TAD paper machine in Shelby, NC

•

Continuing to optimize the pulp and paperboard mills to improve cost

structure •

First U.S. Private Label manufacturer to offer FSC products

•

2-for-1 stock split and $30 million repurchase program in third quarter

2011 •

Sold our sawmill for $30 million in late 2011 to allow the Pulp and Paperboard

Segment to focus on core operations

Accomplishments Since the 2008 Spin-off |

5

•

Complete

new

paper

machine

and

corresponding

converting

lines

in

Shelby,

NC

on time and on budget

•

Expand customer base to align with the expected start up of the paper machine

in fourth quarter 2012

•

Launch Lean Manufacturing program company-wide to reduce costs and

improve efficiencies

•

Achieve $35-$40 million annual run rate cost synergies associated with the

acquisition of Cellu Tissue

2012 Objectives |

6

New Paper Machine |

Shelby Paper Machine –

Our Accomplishments and Goals

•

Remain ON BUDGET with original estimate

of $260-$280 million

•

Remain ON TIME with paper machine

estimated to start up in fourth quarter 2012

•

Manufacture and deliver QUALITY products

•

Remain ON TASK with dedicated project

team to ensure results

7

•

First two converting lines operational

•

Consolidate third-party warehouse to

Shelby

•

Paper machine and remaining

converting lines operational

•

Commence product trials |

Shelby

8 |

Shelby

9 |

Shelby

10 |

11

Cellu Tissue Acquisition |

12

The acquisition of Cellu Tissue has provided us with:

Strategic Benefits of Acquisition

•

A national manufacturing footprint that allows greater

operational efficiencies

•

New retail channel opportunities

•

An estimated $15-$20 million in cost synergies in 2012

and an estimated cost synergies annual run rate of $35-

$40 million by the end of 2012 |

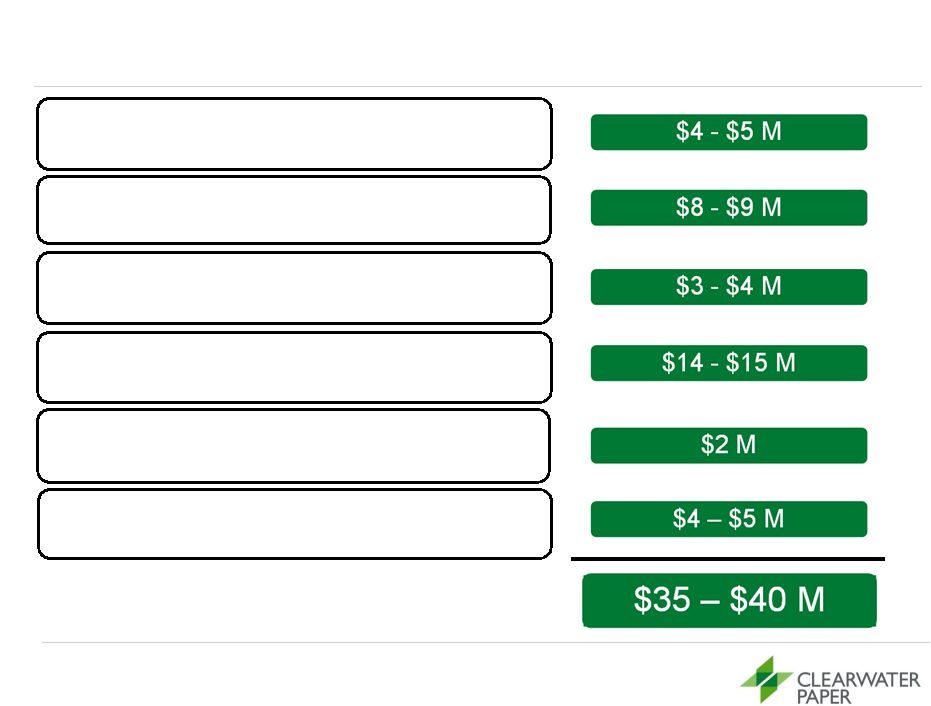

Breakdown

of

Estimated

Annual

Acquisition

Cost

Synergies

1

13

Manufacturing

–

Moving parent rolls to

converted cases

Transportation

–

Product spec changes and

lower miles

Warehousing

–

Closing duplicate facilities

Procurement

–

Purchasing power and

economies of scale

Fiber

–

Increased use of internal pulp

Wages

–

Streamlining processes and

overhead

1

Estimated annual run rate cost synergies of $35-$40 million by the end of

2012 |

14

Consumer Tissue |

15

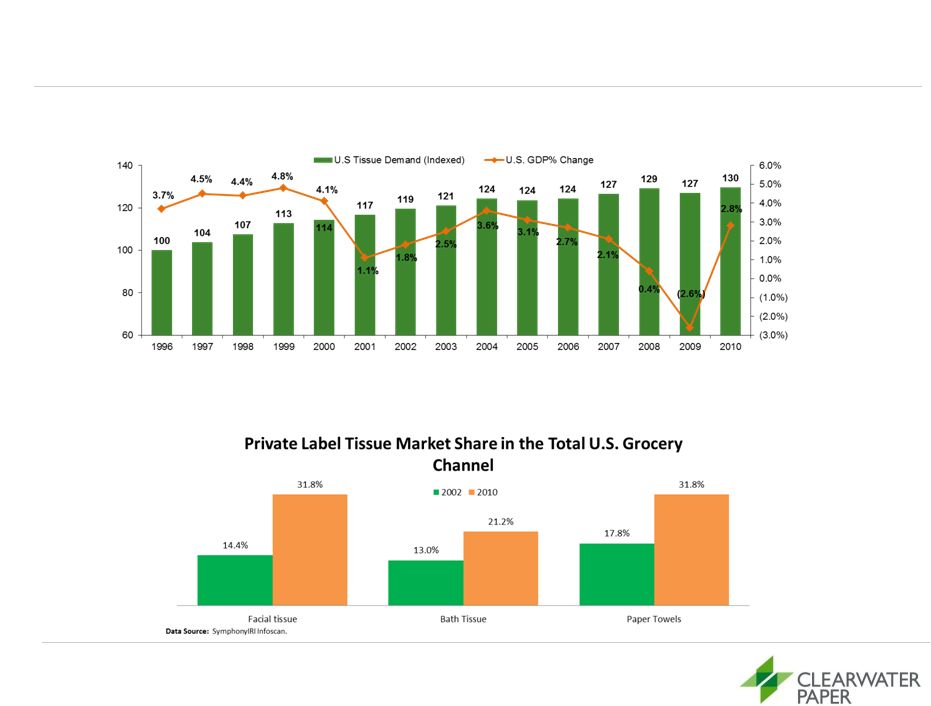

Attractive Industry Characteristics

Within

the

tissue

market,

Private

Label

penetration

has

also

grown

substantially

since

2002

²

The

tissue

market

has

grown

an

average

of

2%

annually

since

1996

¹

Source: RISI and IRI

1 Based on converted short tons

2 Represents market share as a % of sales in U.S. grocery channel

|

16

Therefore they require:

•

National brand-like quality to support high quality store

brands

•

High quality packaging and branding support

•

Complete mix of product offerings to support retailer

assortment objectives

•

Category management support and expertise

•

Experience and execution to deliver a comprehensive

Private Label tissue program

Private Label is a Strategic Focus for Retailers |

Tissue is an Important Category for U.S. Retailers

Segment

% Category (cases)

Annual Sales

Bath Tissue

53%

$4.2B

Paper Towels

32%

$2.5B

Facial Tissue

10%

$795MM

Paper Napkins

5%

$360MM

Est. Total Category

$7.86B

SOURCE: 52 Week Sales Food, Drug, Mass without Wal-Mart, May 29, 2011,

Symphony IRI 17 |

Private Label Quality is More Important Than Ever Before

18

Mid 60’s to 70’s

2011

•

Private Label has become more brand-like

in quality since the early days of generic

store brand tissue

•

Clearwater Paper manages over 1,300 retail

package SKU’s for its customers |

19

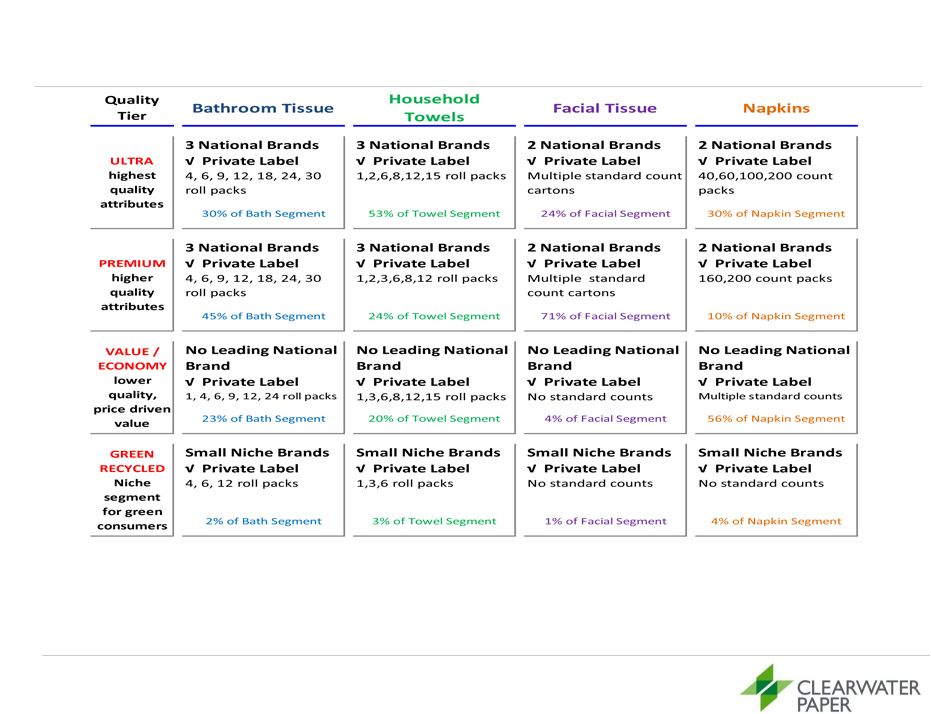

Complex Segmentation Requires Expertise

•

Clearwater Paper is well represented in all segments of the tissue category,

including a leading presence in the value/economy product tier

•

Clearwater Paper is the category leader in providing a full-range of product

tier Private Label offerings nationwide |

20

Clearwater Paper Adds Unique Value Through FSC and

Rainforest Alliance Certification |

21

Paperboard |

22

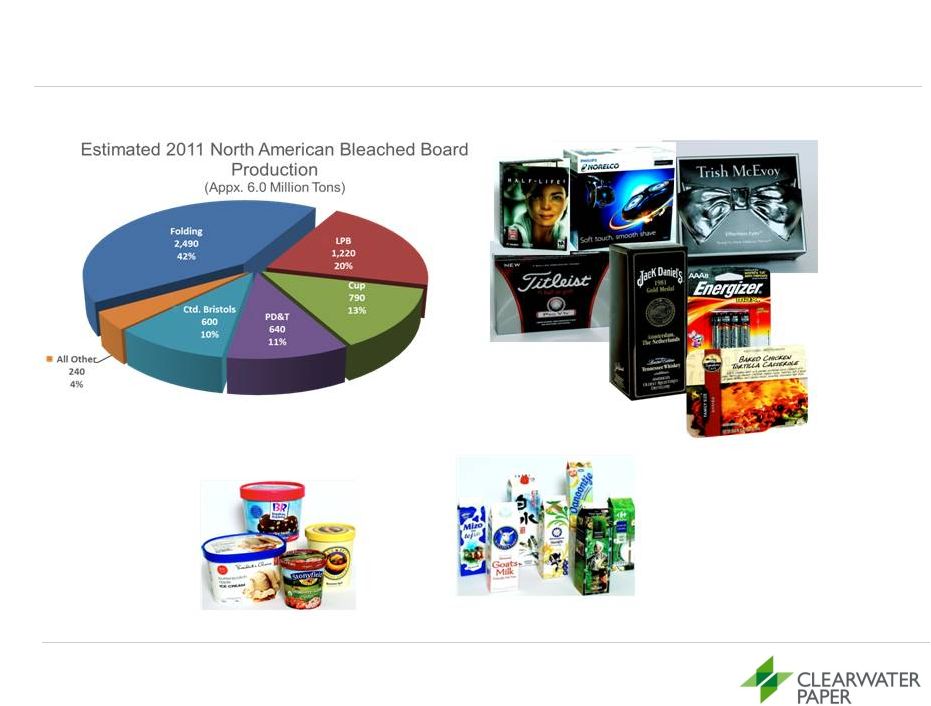

Attractive Industry Characteristics

Source: RISI

1 Top 5 manufacturers in 1998 were International Paper, Westvaco,

Temple-Inland, Georgia-Pacific and Potlatch. Top 5 manufacturers in 2011 were International Paper, MeadWestvaco,

Georgia-Pacific, Evergreen Packaging and Clearwater Paper

2 Based on tons produced

3 Average price per short ton of 16 pt. SBS folding carton C1S

2011 North American Bleached

Paperboard (SBS) Production

Pulp and Paperboard

Capacity

Top 5 Manufacturers

Stable demand for U.S. paperboard products

Demand

Price

1 |

Estimated Industry Mix

23

SOURCE: RISI / Company Websites / Internal Estimates

Cup

Liquid Packaging

Folding/CIS |

24

Efficiency and Optimization

•

Lean manufacturing initiatives focusing on non-capital solutions

for driving out waste and improving quality

•

Sold our sawmill in late 2011 for approximately $30 million and

signed a long-term residual supply agreement

•

Cost reduction projects such as:

•

Lower Columbia reload facility for sawdust to increase fiber

supply

•

Chip screening at Lewiston to improve quality

•

Strong pulp integration –

we internally produced approximately

64% of our pulp requirements in 2011 |

Chip Screening

25 |

26

Financial Overview |

Financial Goals and Priorities

•

Create strong shareholder return

•

Grow free cash flow through strong operating performance

•

Maintain modest leverage in the range of Net Debt/EBITDA of

1x –

4x

•

Deploy capital effectively

•

Focus on appropriate liquidity levels for growth and business

cycles

27 |

28

Our objective is to allocate capital using a dynamic framework to

create strong returns to shareholders

while providing appropriate

liquidity to meet growth objectives and compete effectively.

Capital Allocation

Return Timeframe

Greenfield

M&A

Stock Repurchase

Debt Pay Down

Pension Payments

Dividend

Capital allocation CLW has deployed

Shorter

Longer

Illustrative of Projects Meeting Return Hurdle Rates

Capital |

Share Repurchase

•

Authorization to repurchase up to $30 million of common stock

•

Purchases help offset share dilution from equity incentive plans

•

During the fourth quarter of 2011 we repurchased 41,700 shares

of outstanding common stock at an average price of $32.30 per

share

•

Through year-end 2011 we had repurchased 333,300 shares at a

total cost of $11.3 million

29 |

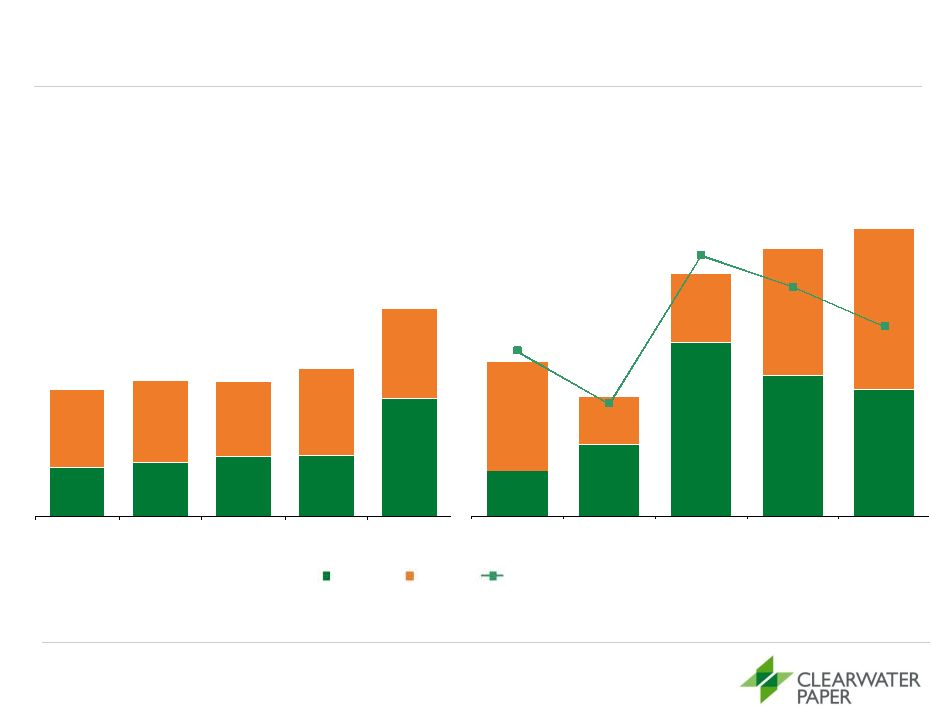

$196

Financial Track Record

$34

$53

$128

$104

$93

$80

$35

$51

$94

$134

8.8%

6.0%

13.9%

12.2%

10.1%

2007

2008

2009

2010

2011

Adjusted

EBITDA

and

Segment

Adjusted

EBITDA

2

5 Yr. Average: $143

$452

$504

$554

$570

$1,092

$731

$751

$696

$803

$836

2007

2008

2009

2010

2011

30

($ in millions)

Net Sales and Segment Net Sales

1

$1,183

$1,255

$1,250

$104

$75

5 Yr. Average: $1,398

$174

$1,373

$167

$1,928

1 Excludes

intersegment

net

sales

and

transfers.

Net

sales

for

2010

for

CPD

includes

four

days

of

Cellu

Tissue

results.

Prior

periods

have

no

Cellu

Tissue

amounts

2 See

Appendix:

“Detailed

Financials”

for

the

definition

of

Adjusted

EBITDA

and

Segment

Adjusted

EBITDA

as

well

as

the

reconciliation

to

the

most

comparable

GAAP

measures

3 Adjusted

EBITDA

margin

percentage

calculated

by

dividing

Adjusted

EBITDA

by

Net

Sales

CPD

Adj. EBITDA Margin %

3

PPD |

Historical Cost Drivers –

Wood Fiber

31

Total Cost

1

:

% of Total

Cost of Sales

2009

2010

2008

$325.4 M

28%

$259.6 M

25%

$304.5 M

26%

1

Excludes intersegment amounts and Cellu Tissue amounts prior to acquisition

•

Wood fiber includes pulp, wood chips, sawdust and saw logs (until the

November 28, 2011 sale of our sawmill)

•

Generally we use a mix of pulp including northern softwood, southern

softwood, northern hardwood, eucalyptus and recycled

•

In 2011, we utilized 95% of our internally generated pulp which represented

approximately 64% of our total pulp needs

2011

$487.6 M

29%

Wood

Fiber |

Historical Cost Drivers –

All Other

32

Total Cost:

% of Total

Cost of Sales

2009

2010

Energy

2008

Total Cost:

% of Total

Cost of Sales

Total

Cost

1

:

% of Total

Cost of Sales

$143.0 M

12%

$114.7 M

10%

$97.3 M

9%

$92.0 M

8%

$123.2 M

10%

$100.3 M

9%

$117.3 M

10%

$ 61.9 M

5%

$70.0 M

7%

$82.4 M

7%

$123.2 M

12%

$132.3 M

11%

Maintenance

& Repairs

Total Cost:

% of Total

Cost of Sales

Chemicals

1

Excludes related labor costs

Transportation

2011

$130.2 M

8%

$148.1 M

9%

$99.8 M

6%

$174.7 M

10% |

33

Estimated Annual Cost Sensitivities

Change

2011

EBITDA

Variable

Units

$/Unit

Units

Purchased Pulp

$/Tonne

$50.00

450,000

+/-

$23

Chips/Sawdust

$/Ton

$5.00

1,750,000

+/-

$9

Transportation

$/Gallon

$1.00

8,820,000

+/-

$9

Chemicals

$/Prod Ton

$5.00

1,300,000

+/-

$7

Natural Gas

$/mmbtu

$0.50

10,400,000

+/-

$5

$0

$5

$10

$15

$20

$25

$30

($ Millions) |

34

($ in millions)

1

See Appendix “Detailed Financials”

for the definition of EBITDA, Adjusted EBITDA and Free Cash Flow as well as a

reconciliation to the most comparable GAAP measures. 2009, 2010 and

2011

amounts

are

Adjusted

EBITDA

and

all

other

periods

represent

EBITDA

2

See Appendix “Detailed Financials”

for supporting schedules

3

We converted gallons previously claimed under the Alternative Fuel Mixture Tax

Credit, or AFMTC, to the Cellulosic Biofuel Producer Credit, or CBPC Free Cash

Flow 2011 free cash flow was impacted by Shelby capital, taxes paid in

connection with our

transition

to

CBPC

³

and

pension

funding

2007

2008

2009

2010

2011

EBITDA/Adjusted

EBITDA

¹

$103.7

$75.4

$174.3

$166.8

$195.5

Capital Expenditures

(20.5)

(21.3)

(19.3)

(46.1)

(134.1)

Cash

Taxes

Paid

²

(14.1)

(5.6)

(41.3)

(28.6)

(43.1)

Cash Net Interest Expense

(13.0)

(13.1)

(15.1)

(15.9)

(43.6)

Working

Capital

Dec

(Inc)

²

37.6

(21.2)

(99.6)

88.5

(85.6)

Other

Cash

Flow

Items

²

(5.7)

6.6

88.2

(44.7)

34.6

Free

Cash

Flow

¹

$88.0

$20.8

$87.2

$120.0

$(76.3) |

35

($ in millions)

Balance Sheet

1

December 31,

December 31,

December 31,

2009

2010

2011

Assets

Current Assets

Cash, Restricted Cash & Short-Term Investments

$190.8

$148.7

$64.2

Receivables, net

94.5

153.3

176.2

Taxes Receivable

101.3

10.4

10.0

Inventories

169.8

228.3

244.1

Prepaid Expenses and Other

15.9

48.8

50.8

Non-Current Assets

Property, Plant & Equipment

364.0

654.5

735.6

Goodwill & Intangibles

-

285.9

279.2

Other

11.2

15.4

11.2

Total Assets

$947.5

$1,545.3

$1,571.3

Liabilities

Current Liabilities

Accounts Payable & Accrued Liabilities

109.8

184.6

144.6

Other

9.9

10.5

9.9

Non-Current Liabilities

Long-Term Debt

148.3

538.3

523.7

Deferred Taxes

-

61.1

69.4

Other Long-Term Liabilities

242.3

210.5

264.3

Accrued Taxes

73.5

72.0

74.5

Total Liabilities

$583.8

$1,077.0

$1,086.4

Total Stockholders' Equity

$363.7

$468.3

$484.9

Total Liabilities & Stockholders' Equity

$947.5

$1,545.3

$1,571.3

Adjusted

EBITDA

to

Interest

Expense,

net

1

11.2X

7.4X

4.4X

0.9

3.2

2.7

Total Debt/Adjusted EBITDA

1

See Appendix “Detailed Financials” for the definition of Adjusted EBITDA as well as a

reconciliation to the most comparable GAAP measure |

36

Appendix:

Detailed Financials |

37

Income Statement

($ in millions)

1

See Appendix for definition of EBITDA and a reconciliation to most comparable GAAP

measure 2007

2008

2009

2010

2011

Net Sales

$1,183.0

$1,255.3

$1,250.1

$1,373.0

$1,928.0

Costs & Expenses

Cost of Sales

1,083.8

1,179.4

1,052.2

1,173.8

1,702.5

Selling, General, & Administrative

46.8

47.4

71.1

100.4

110.0

Income from Canadian Lumber Settlement

-

-

-

-

-

Alternative Fuel Mixture Tax Credit

-

-

170.6

-

-

Income from Operations

$52.4

$28.5

$297.4

$98.8

$115.4

Margin (%)

4.4

%

2.3

%

23.8

%

7.2

%

6.0

%

Depreciation and Amortization

51.3

47.0

47.4

47.7

76.9

EBITDA

1

$103.7

$75.4

$338.6

$146.5

$192.7

Margin (%)

8.8

%

6.0

%

27.1

%

10.7

%

10.0

%

Interest Expense

13.0

13.1

15.5

22.6

44.8

Debt Retirement Costs

-

-

6.2

-

-

Other Expense (Income)

-

-

-

-

(0.3)

Earnings Before Income Taxes

$39.4

$15.3

$275.7

$76.2

$70.9

Income Tax Provision

14.1

5.6

93.2

2.4

31.2

Net Earnings

$25.3

$9.7

$182.5

$73.8

$39.7 |

38

Reconciliation of GAAP to Non-GAAP:

Net Cash from Operating Activities to Free Cash Flow

($ in millions)

1

2009

amount

excludes

$170.6

million

of

alternative

fuel

mixture

tax

credits

for

the

period

late

January

through

December

31,

2009

2007

2008

2009

1

2010

2011

Net Cash Provided by Operating

Activities

$108.5

$42.1

$54.2

$185.6

$68.4

Capital Expenditures

(20.5)

(21.3)

(19.3)

(46.1)

(134.1)

Non-cash Net Interest

-

-

0.4

6.7

1.3

Non-cash Net Taxes

-

-

51.9

(26.2)

(11.9)

Free Cash Flow

$88.0

$20.8

$87.2

$120.0

$(76.3) |

39

Free Cash Flow –

Working Capital

($ in millions)

2007

2008

2009

2010

2011

Dec (Inc) in Receivables

$18.8

$(8.8)

$9.5

$(9.9)

$(25.6)

Dec (Inc) in Tax Receivables

-

-

(101.3)

93.8

0.4

Dec (Inc) in Inventories

(8.5)

(14.0)

(16.8)

(3.9)

(18.7)

Dec (Inc) in Prepaid Expenses

0.4

(0.5)

0.1

(5.0)

(0.2)

Inc (Dec) in Taxes Payable

18.1

0.8

(0.8)

-

2.2

Inc (Dec) in Accounts Payable

and Accrued Liabilities

8.9

1.3

9.7

13.5

(43.7)

Working Capital Dec (Inc)

$37.6

$(21.2)

$(99.6)

$88.5

$(85.6) |

40

Free Cash Flow –

Other

($ in millions)

2007

2008

2009

2010

2011

Equity-Based Compensation

Expense

$3.3

$2.3

$5.6

$8.5

$8.1

Employee Benefit Plans

(1.0)

1.1

14.1

15.0

16.9

Funding of Qualified Pension

Plans

-

-

-

(25.1)

(12.5)

Excess Tax Benefit from Share-

based Payment Arrangements

-

-

(0.1)

(0.9)

(0.9)

Change in Non-current Accrued

Taxes

-

-

73.5

(4.3)

2.5

Change in Deferred Taxes

(8.1)

4.9

(4.6)

(15.0)

14.8

Other

0.2

(1.7)

(0.3)

(22.9)

5.7

Other Cash Flow Items

$(5.7)

$6.6

$88.2

$(44.7)

$34.6 |

41

Reconciliation of GAAP to Non-GAAP:

Clearwater Paper EBITDA and Adjusted EBITDA

1

See last page of this Appendix for definitions of EBITDA and Adjusted EBITDA

($ in millions)

2007

2008

2009

2010

2011

Net Earnings

$25.3

$9.7

$182.5

$73.8

$39.7

Income Tax Provision

14.1

5.6

93.2

2.4

31.2

Interest Expense

13.0

13.1

15.5

22.6

44.8

Earnings Before Interest and

Income Taxes

52.4

28.5

291.2

98.8

115.7

Depreciation & Amortization

51.3

47.0

47.4

47.7

76.9

EBITDA

1

$103.7

$75.4

$338.6

$146.5

$192.7

Alternative Fuel Mixture Tax

Credit

-

-

(170.6)

-

-

Debt Retirement Costs

-

-

6.2

-

-

Cellu Tissue Acquisition

Related Expenses

-

-

-

20.3

-

Lewiston, Idaho sawmill sale

related adjustments

-

-

-

-

2.9

Adjusted EBITDA¹

$103.7

$75.4

$174.3

$166.8

$195.5 |

42

Reconciliation of GAAP to Non-GAAP:

Clearwater Paper Segment EBITDA and Segment Adjusted EBITDA

($ in millions)

1

See last page of this Appendix for definitions of Segment EBITDA and Segment

Adjusted EBITDA 2007

2008

2009

2010

2011

Consumer Products

Operating Income

$17.6

$37.3

$112.2

$80.8

$42.8

Depreciation and Amortization

16.3

15.7

16.0

17.0

50.4

Other, net

-

-

-

-

0.1

Segment EBITDA

1

$33.9

$53.0

$128.2

$97.8

$93.3

Cellu Tissue Acquisition

Related Expenses

-

-

-

6.4

-

Segment

Adjusted EBITDA

1

$33.9

$53.0

$128.2

$104.2

$93.3

Pulp & Paperboard

Operating Income

$45.0

$4.4

$201.8

$64.9

$92.8

Depreciation

34.6

30.9

29.9

28.7

26.1

Segment

EBITDA

1

$79.6

$35.3

$231.7

$93.6

$118.9

Alternative Fuel Mixture Tax

Credits

-

-

(170.6)

-

-

Lewiston, Idaho sawmill sale

related adjustments

-

-

-

-

15.4

Segment

Adjusted EBITDA

1

$79.6

$35.3

$51.1

$93.6

$134.3 |

43

Definitions of Non-GAAP Measures

Clearwater Paper Definitions of Non-GAAP Measures

EBITDA

is a non-GAAP measure that Clearwater Paper management uses to evaluate the

cash generating capacity of Clearwater Paper. The most directly comparable

GAAP measure is net earnings. EBITDA, as defined by Clearwater Paper management, is net earnings adjusted for net

interest

expense,

income

taxes,

and

depreciation

and

amortization.

It

should

not

be

considered

as

an

alternative

to

net

earnings

computed under

GAAP.

Adjusted EBITDA

is a non-GAAP measure that Clearwater Paper management defines as EBITDA

adjusted for items that we do not believe are indicative of our core

operating performance, including acquisition related expenses and alternative fuel mixture tax credits. The most directly

comparable GAAP measure is net earnings. It should not be considered as an

alternative to net earnings computed under GAAP. Segment EBITDA

is a non-GAAP measure used by Clearwater Paper management. The most directly

comparable GAAP measure is segment operating

income.

Segment

EBITDA,

as

defined

by

Clearwater

Paper

management, is segment operating income adjusted for segment

depreciation

and

amortization.

It

should

not

be

considered

as

an

alternative to segment operating income computed under GAAP.

Segment

Adjusted

EBITDA

is

a

non-GAAP

measure

that

Clearwater

Paper

management

defines

as

Segment

EBITDA adjusted for items that we

do

not

believe

are

indicative

of

the

segment’s

core

operating

performance,

including

alternative

fuel

mixture

tax credits. The most directly

comparable GAAP measure is segment operating income. It should not be

considered as an alternative to segment operating income computed under

GAAP. Free Cash Flow

is a non-GAAP measure that Clearwater Paper management uses to evaluate the

financial performance of Clearwater Paper. The most

directly

comparable

GAAP

measure

is

net

cash

from

operating

activities. Free Cash Flow, as defined by Clearwater Paper management, is

net cash from operating cash flows adjusted for capital expenditures,

non-cash net interest and non-cash taxes. It should not be considered as an

alternative

to

net

cash

from

operating

activities

computed

under

GAAP. |

44

Appendix:

Estimated Pulp Flow and

Synergy Example |

45

Pulp Flows 2011

(MT)

36%

64%

Pulp Sources

Internal

90%

10%

By Division

26%

74%

Recycled/Virgin

Recycled

DIP,

Other

38%

62%

Virgin

Hardwood

•

BEK

Softwood

Consumer Products

Idaho

Pulp and Paperboard

External

450,000 MT

•

NBHK

•

SBHK

•

NBSK

•

NBHK

•

NBSK

•

SBSK

•

SOP, |

Synergy Opportunity Example

Underutilized

large converting winder in Neenah, WI (formerly Cellu Tissue) can more

efficiently produce Away-from-Home products and 1000 count bathroom

tissue Actions:

1.

Relocate a wrapper machine from Elwood, IL (formerly CLW) to Neenah, WI

2.

Reposition an underutilized case packer in Neenah, WI

3.

Redirect the existing 1000 count product from Lewiston, ID (formerly CLW) and

Thomaston, GA (formerly CLU) to Neenah, WI

4.

Increase the production schedule of the existing underutilized large converting

winder in Neenah, WI from 5 to 7 days

Expected Results:

1.

Creates new case capacity in the systems at Neenah, Lewiston and

Thomaston

2.

Reduces freight

3.

Improves paper machine trim

46 |

47

Appendix:

Other Information |

48

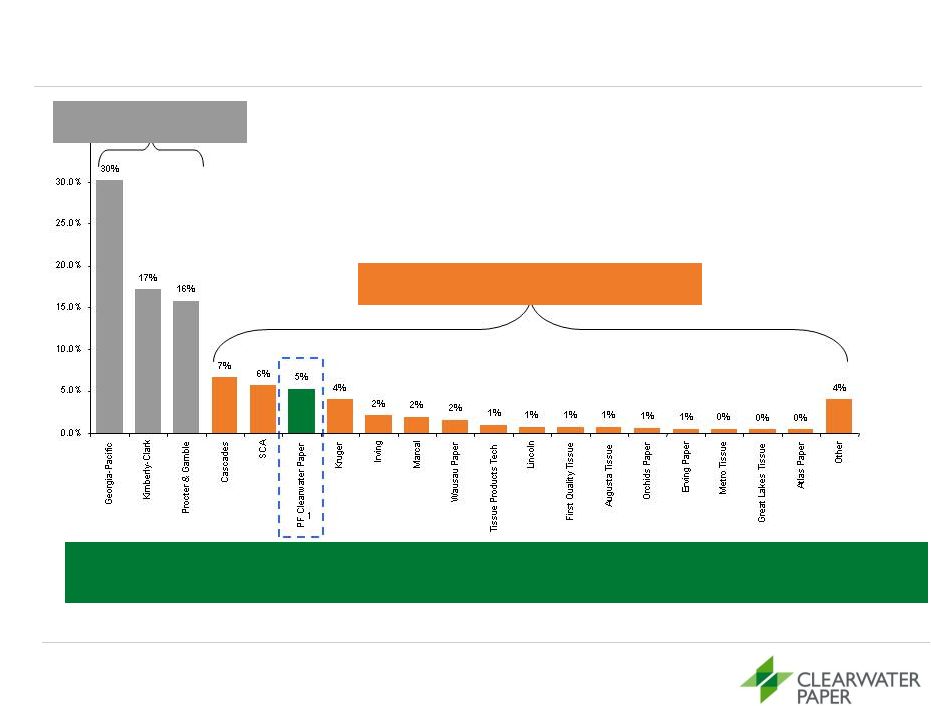

2010 North American Tissue Market by Producer

Remaining Manufacturing Base Highly

Fragmented

Large Brand

Manufacturers

Source: Equity research.

1

Represents Clearwater Paper tissue parent roll capacity combined on a pro

forma basis with Cellu Tissue tissue parent roll production The Combined

Company was the Sixth-Largest Manufacturer in the

North American Tissue Market in 2010 |

1 Clearwater Paper capacities exclude expected tissue parent roll

manufacturing in Shelby, NC of 70,000 tons annual capacity expected to be

operational in 2012

49

National Manufacturing Footprint

Bleached Paperboard

775,000 tons

Tissue Parent Roll

586,000 tons

Tissue Converting

489,000 tons

Pulp

845,000 tons

Clearwater

Paper

Capacities

1

Clearwater Paper Pulp

Clearwater Paper SBS

Clearwater Paper Tissue Converting

Clearwater Paper Tissue Parent Roll

Corporate and administrative

Spokane, WA

Corporate Headquarters

Lewiston, ID

Converting Capacity:

102,000 tons

Lewiston, ID (Pulp)

Capacity: 540,000 tons

Lewiston, ID (SBS)

Capacity:

445,000 tons

Lewiston, ID (Tissue)

Capacity: 189,000 tons

Las Vegas, NV (TAD)

Capacity: 39,000 tons

Las Vegas, NV

Converting Capacity:

51,000 tons

Cypress Bend, AR (Pulp)

Capacity: 305,000 tons

Cypress Bend, AR (SBS)

Capacity: 330,000 tons

Elwood, IL

Converting Capacity:

68,000 tons

Wiggins, MS

Capacity: 59,000 tons

Neenah, WI

Capacity: 85,000 tons

Ladysmith, WI

Capacity: 56,000 tons

Oklahoma City, OK

Converting Capacity:

19,000 tons

East Hartford, CT

Capacity: 36,000 tons

Gouverneur, NY

Capacity: 39,000 tons

Alpharetta, GA

Thomaston, GA

Converting Capacity:

58,000 tons

Long Island, NY

Converting Capacity:

38,000 tons

Shelby, NC (TAD)

Announced Capacity:

70,000 tons

Neenah, WI

Converting

Capacity:

99,000 tons

Menominee, MI

Capacity: 36,000 tons

St. Catharines, ON (TAD)

Capacity: 47,000 tons

Menominee, MI

Converting

Capacity:

27,000 tons

Shelby, NC (TAD)

Converting Capacity:

27,000 tons |

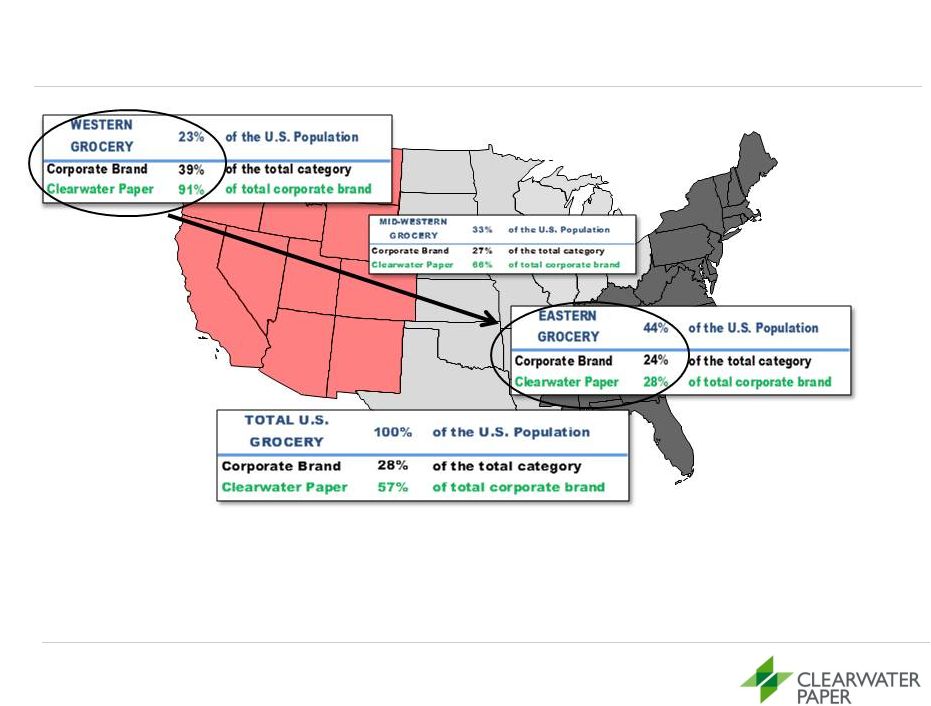

50

Expansion Opportunities

Clearwater Paper has been a strong influence in the development of Private

Label tissue in the Western U.S. An opportunity exists to grow Private

Label category development and company share in the Eastern U.S.

Source: SymphonyIRI InfoScan. 52 Weeks Ending May 29, 2011. Data

excludes Cellu Tissue |

North American Tissue Capacity Change

51

* Estimated

Source: RISI and Other Industry

COMPANY

LOCATION

CONV/TAD

TONS

STARTUP DATE

CHANNEL/BUSINESS/PRODUCTS

Procter and Gamble

Box Elder, UT

TAD

80,000

4th Q, 2012

Retail/Brand/Bounty

First Quality

Anderson, SC

TAD

70,000

3rd Q, 2012

Retail/P.L./BRT

Florelle Tissue

Brownville, NY

CONV

35,000

2nd Q, 2012 *

Retail/P.L./Virgin Fiber

Patriarch Partners

Gorham, NH

CONV

(Overmechanica)

35,000

3rd Q, 2012 *

Retail/P.L.

Kruger

Memphis, TN

TAD

70,000

4th Q, 2012

Retail/Brand/P.L.

Clearwater Paper

Shelby, NC

TAD

70,000

4th Q, 2012

Retail/P.L./BRT & HHT

ST Paper

Franklin, VA

CONV

70,000

1st Q, 2013

Parent Roll Sales/Recycled

South Georgia Tissue

Snelling, SC

CONV

70,000

1st Q, 2013 *

Parent Roll Sales/Recycled

Wausau Paper

Harrodsburg, KY

ATMOS

75,000

1st Q, 2013

AFH/Recycled

COMPANY

LOCATION

CONV/TAD

TONS

STARTUP DATE

CHANNEL/BUSINESS/PRODUCTS

Georgia Pacific

Port Hudson, LA

ETAD

100,000

4th Q, 2012 *

Retail/Brand & P.L./HHT & BRT

SCA

Menasha, WI

ATMOS (PM#3)

70,000

1st Q, 2013

AFH

COMPANY

LOCATION

CONV/TAD

TONS

STARTUP DATE

CHANNEL/BUSINESS/PRODUCTS

Kimberly-Clark

Everett, WA

CONV/UCTAD/DRC

(All 5 PM)

193,000

1st Q, 2012

Retail/AFH/PL-Club/Parent Roll Sales

Kimberly-Clark

Chester, PA

CONV (PM #16)

27,000

1st Q, 2012

Napkin/BRT

REBUILDS

ANNOUNCED SHUTDOWNS

ANNOUNCED NEW PAPER MACHINES |