UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2010

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

ROOMLINX, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

|

|

83-0401552

|

|

(State or other jurisdiction of

|

|

(I.R.S. Employer

|

|

incorporation or organization)

|

|

Identification No.)

|

2150 W. 6th Avenue, Unit H, Broomfield, CO 80020

(Address of principal executive offices)

(303) 544-1111

(Registrant’s telephone number)

Securities registered under Section 12(b) of the Act: None

Securities registered under Section 12(g) of the Act:

| (i) Common Stock, $.001 par value per share; and | (ii) Preferred Stock, $.20 par value per share. |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES o NO x

Indicate by check mark if the registrant is not required to file reports pursuant to section 13 or Section 15(d) of the Act. YES o NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES o NO o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this form 10K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer o

Non-accelerated filer o Smaller reporting company x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act.) YES o NO x

The aggregate market value of the registrant’s common shares held by non-affiliates as of June 30, 2010 was $10,863,977 based upon the closing price of these shares as reported on that date. (For purposes of this calculation only, all of the registrant’s directors and executive officers are deemed affiliates of the registrant.)

As of March 29, 2011, the registrant’s issued and outstanding shares were as follows: 5,021,415 shares common stock, 720,000 shares of Class A Preferred Stock.

Documents incorporated by reference: None.

EXPLANATORY NOTE

This amendment is being filed to include the signed audit report. The financial statements themselves did not include any errors.

2

TABLE OF CONTENTS

|

PART I

|

||

|

Item 1.

|

Business

|

3 |

|

Item 1A.

|

Risk Factors

|

13 |

|

Item 1B.

|

Unresolved Staff Comments

|

19 |

|

Item 2.

|

Properties

|

20 |

|

Item 3.

|

Legal Proceedings

|

20 |

|

Item 4.

|

[Reserved]

|

20 |

|

PART II

|

||

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

21 | |

|

Item 6.

|

Selected Financial Data

|

23 |

|

Item 7.

|

Managements Discussion and Analysis of Financial Condition and Results of Operation

|

24 |

|

Item 7A.

|

Quantitative and Qualitative Disclosures About Market Risk

|

33 |

|

Item 8.

|

Financial Statements and Supplementary Data

|

34 |

|

Item 9.

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

62 |

|

Item 9A.

|

Controls and Procedures

|

62 |

|

Item 9B.

|

Other Information

|

63 |

|

PART III

|

||

|

Item 10.

|

Directors, Executive Officers and Corporate Governance

|

64 |

|

Item 11.

|

Executive Compensation

|

68 |

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

71 |

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence

|

73 |

|

Item 14.

|

Principle Accounting Fees and Services

|

75 |

|

PART IV

|

||

|

Item 15.

|

Exhibits, Financial Statement Schedules

|

77 |

| 80 |

3

PART I

ITEM 1. DESCRIPTION OF BUSINESS

General

As used in this Annual report, references to “the Company”, “we”, “our”, “ours”, and “us” refer to Roomlinx, Inc. and consolidated Subsidiaries, unless otherwise indicated.

We prepare our financials in United States dollars and in accordance with generally accepted principles as applied in the United States, referred to U.S. GAAP. In this Annual Report, references to “$” and “dollars” are to United States dollars and “CDN” are to Canadian dollars.

Background

Roomlinx, Inc.

Roomlinx, Inc. was formed in 1998, is incorporated under the laws of the state of Nevada, and has its headquarters at 2150 W 6th Avenue Unit H, Broomfield, CO 80020.

On October 1, 2010, Roomlinx, Inc. acquired 100% of the membership interests of Canadian Communications, LLC and its wholly owned subsidiaries, Cardinal Broadband, LLC, Cardinal Connect, LLC, and Cardinal Hospitality, Ltd. The acquisition of Canadian Communications, LLC also included a 50% joint venture interest in Arista Communications, LLC; Roomlinx, Inc. has maintained this 50% joint venture interest. Subsequent to the acquisition, the assets and liabilities of Canadian Communications, LLC, Cardinal Connect, LLC, and Cardinal Broadband, LLC were transferred to Roomlinx, Inc. Cardinal Broadband became a division of Roomlinx, Inc., and management plans to dissolve the separate entities Canadian Communications, LLC, Cardinal Broadband, LLC, and Cardinal Connect, LLC. Cardinal Hospitality, Ltd. remains a separate and wholly owned subsidiary of Roomlinx, Inc.

Cardinal Broadband, a Division of Roomlinx, Inc.

Cardinal Broadband, LLC was formed in 2005 as a Colorado Limited Liability Company. Pursuant to the acquisition of Canadian Communications, LLC on October 1, 2010, Roomlinx, Inc. became the 100% member of Cardinal Broadband, LLC. Subsequent to the acquisition, Cardinal Broadband became a division of Roomlinx, Inc., and management plans to dissolve the Limited Liability Company in 2011.

Cardinal Hospitality, Ltd.

Cardinal Hospitality, Ltd. was formed in September of 2005, and is incorporated in British Columbia, Canada. Pursuant to the October 1, 2010 acquisition of Canadian Communications, LLC, Roomlinx, Inc. became the sole shareholder of Cardinal Hospitality, Ltd. It remains a separate and wholly owned subsidiary of Roomlinx, Inc.

Arista Communications, LLC.

Arista Communications, LLC is a joint venture between Cardinal Broadband and Wiens Real Estate Ventures, LLC, with each entity having a 50% membership interest.

4

Business

The Company’s primary business is focused on providing in-room media and entertainment solutions along with wired networking solutions and Wireless Fidelity networking solutions, also known as Wi-Fi, for high speed internet access to hotels, resorts, and time share properties. Subsequent to the acquisition of Canadian Communications, LLC, the Company also provides both wired and wireless internet access, satellite television service, and telephone service (both POTS and Voice over Internet Protocol (“VOIP”), to residential and business customers. In addition, the Company now provides Video-on-Demand service to the hotel and timeshare industry throughout Canada, the United States, Mexico, and Aruba. As of December 31, 2010, our current customer base consisted of 253 hospitality properties representing approximately 39,263 hotel rooms served, and 19 residential communities and small businesses, representing an additional 2,100 customers.

Roomlinx, Inc.

Roomlinx’ wired and wireless networking solution offers easy to use access, providing instant and seamless connections for laptop users from anywhere throughout a property, including guest rooms, meeting rooms, back office and public areas, over a high-speed connection. Users on this network have access to home and corporate email accounts and Virtual Private Networks, also known as VPNs. Guests have flexible billing options, choosing from any one of free service, flat rate, time-based usage or unlimited. In addition these users can expand the service to include value-added services such as wireless point of sale, maintenance, check-in and internet telephony services.

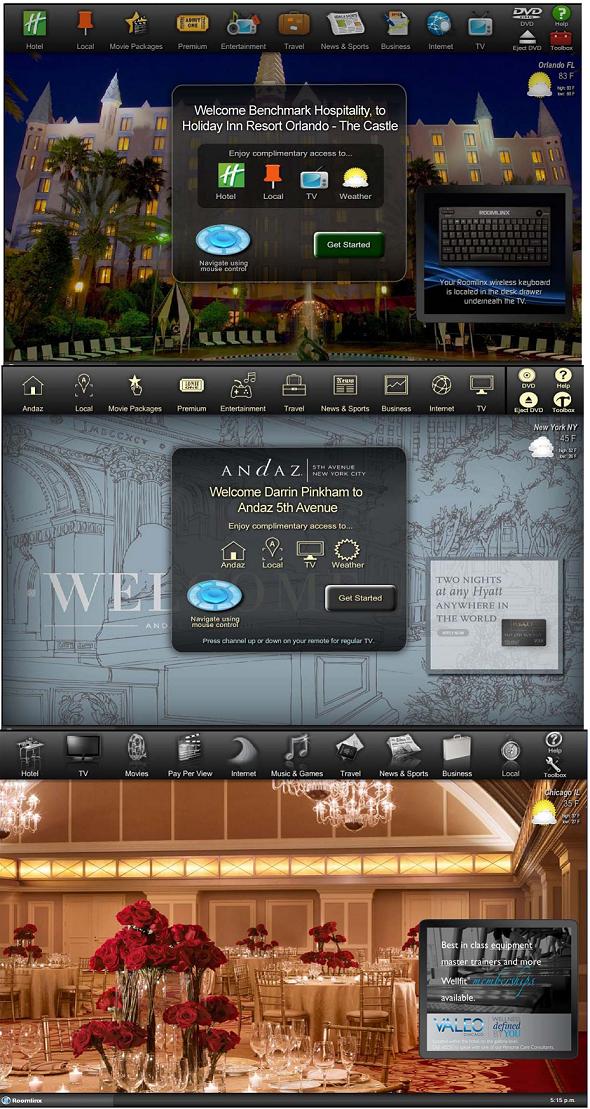

The Roomlinx in-room media and entertainment products include its proprietary Interactive TV platform, internet, and free-to-guest and on-demand programming. Roomlinx provides premium applications for internet-based business and entertainment media to venues serving the visitor-based market such as hotels, resorts, and time share properties. The Interactive TV offering includes a broad range of content and features to satisfy guests while maximizing revenue opportunities for the hotelier. The solution includes movies, international and US television programming, music and news, games, local travel and concierge information, and business productivity tools that include desktop applications, conferencing and printing applications.

The Company generates revenue through:

|

|

1.

|

Ongoing connectivity service and support contracts

|

|

|

2.

|

Network design and installation services

|

|

|

3.

|

Delivery of content and advertising

|

|

|

4.

|

Delivery of business and entertainment applications

|

|

|

5.

|

E-commerce

|

|

|

6.

|

The customization of its software for the in-room media product

|

|

|

7.

|

Delivery of pay-per-view content

|

The following are examples of three different custom user interfaces of the Roomlinx Interactive TV platform in use today:

5

6

Cardinal Broadband, a Division of Roomlinx, Inc.

Cardinal Broadband offers residential and business customers telecommunication services including telephone, satellite television, and wired and wireless internet access. Cardinal Broadband is a Certified Local Exchange Carrier (“CLEC”), and as such has a tariff filed with the Colorado Public Utility Commission that allows it to provide traditional land line services throughout Colorado. Cardinal Broadband offers “bundled” service wherever possible, meaning that they can provide telephone, television, and internet service to the same customer, allowing a single point of contact for customer service and a single invoice for multiple services.

Telephone service is provided through traditional, analog “twisted pair” lines, as well as digital Voice Over Internet Protocol. Analog phone service is typically provided via an Interconnection agreement with Qwest Communications, which allows Cardinal Broadband to resell Qwest service through their wholesale and retail accounts with Qwest. VOIP service is provided at properties where Cardinal Broadband maintains a broadband internet service to the end customer, allowing Cardinal Broadband to provide digital phone service (VOIP) over the same lines as their internet service.

Television service is typically provided via Cardinal Broadband’s agreements with DISH Networks and DirecTv. Most television service to customers is provided via a head-end distribution system, or an L-Band digital distribution system. Television service is offered in high definition whenever possible.

Internet service is provided via both wired and wireless network design. Cardinal Broadband provisions and manages broadband access to their customers through multiple provisioning methods:

|

|

1.

|

Wholesale method where Cardinal Broadband owns and controls the Internet circuit and

|

|

|

2.

|

Resale method where Cardinal Broadband utilizes an affiliated third party to provide the Internet circuit.

|

Cardinal Broadband generates revenue through:

|

|

1)

|

Delivery of telephone service, billed on a monthly basis

|

|

|

2)

|

Delivery of internet access, billed on a monthly basis

|

|

|

3)

|

Delivery of television service, billed by the satellite provider with monthly commissions paid to Cardinal Broadband by the provider

|

|

|

4)

|

Installation and maintenance revenue

|

|

|

5)

|

Management fees for the management of affiliated telecommunication systems

|

Cardinal Hospitality, Ltd.

Cardinal Hospitality, Ltd (“CHL”) supplies video-on-demand services to the hospitality industry. CHL operates systems throughout Canada. CHL, a British Columbia corporation, was formed in 2006 with the acquisition of the proprietary Video-on-Demand (VOD) technology formerly offered through GalaVu Entertainment Networks. CHL also acquired the existing contracts of GalaVu. CHL became a wholly owned subsidiary of Roomlinx with the acquisition of Canadian Communications on October 1, 2010. CHL offers a full selection of video-on-demand services and technology; including first non-theatrical release Hollywood motion pictures, adult, and specialty content.

CHL is based in Halifax, Nova Scotia, and is owned and managed by Roomlinx. CHL is the second largest provider of VOD in Canada, with approximately 5% of the total available rooms and close to 50% of those rooms currently offering VOD.

7

Revenue is generated as follows:

|

|

1)

|

Pay-per-view movies and specialty content.

|

|

|

2)

|

Sales of VOD systems

|

Arista Communications, LLC.

Arista Communications, LLC (“Arista Com”) is a joint venture with the developer of the Arista residential/retail/office development in Broomfield, Colorado, formed to provide telecommunication services to the Arista community. Arista Com provides telephone, television, and internet connectivity to the residents and businesses of the Arista development, including the 1st Bank Center (formally the Broomfield Event Center), an 8,000-seat music and sports venue. Roomlinx owns a 50% membership interest in Arista Com through its Cardinal Broadband division. Cardinal Broadband manages the operations of Arista Com.

Highlights

The highlights and business developments for the year ended December 31, 2010 include the following:

|

v

|

Total revenues increased 84% and gross profit increased 22%.

|

|

v

|

Shareholder equity increased 314%

|

|

v

|

US hospitality revenues increased 62%

|

|

v

|

Foreign hospitality revenues increased 446%

|

|

v

|

Roomlinx was awarded the pilot project for Hyatt Corporation and successfully installed Interactive TV, Satellite HD TV, and a High Speed Internet network into the Andaz on 5th Avenue in New York City.

|

|

v

|

Roomlinx installed their Interactive TV platform into our largest property to date – a 610 room hotel in Chicago.

|

|

v

|

Successfully integrated their Interactive TV platform with ATT’s wired and wireless network at a major luxury brand hotel.

|

|

v

|

Successfully completed the acquisition of Canadian Communications LLC and its wholly owned subsidiaries.

|

|

v

|

Created a Free-To-Guest TV division giving them the ability and expertise to install and support Satellite TV for Hotels and MDUs.

|

|

v

|

Increased their channel sales agents from 23 in 2009 to over 30 by the end of 2010.

|

|

v

|

Rolled out version 2.5 of the Roomlinx Interactive TV platform.

|

Recent Financial Developments

On June 5, 2009, the Company, entered into a $5,000,000 Revolving Credit, Security and Warrant Purchase Agreement (the “Credit Agreement”) with Cenfin LLC, a Delaware limited liability company. On March 11, 2010, the terms of the agreement were amended to increase the credit limit to $25,000,000. On July 30, 2010, with effect as of July 15, 2010, the terms of the agreement were amended to change (1) the interest rate to the Federal Funds Rate plus 5% and (2) the strike price of warrants issued in connection with any draws of the line of credit after the first $5,000,000 of borrowings after July 15, 2010 from $2.00 per share to the fair market value of the Company’s common stock on the date of such draw.

8

On April 29, 2010, Roomlinx entered into a securities purchase agreement with investors for an aggregate of 250,000 shares of common stock. The shares were purchased at $4.00 per share for an aggregate of $1,000,000.

On May 28, 2010, shareholders approved a reverse stock split of the outstanding shares of common stock, pursuant to which each 100 shares of the Company’s pre-split common stock issued and outstanding was exchanged for one share of the Company’s post-split common stock. After giving effect to the reverse stock split, there were 4,243,982 shares of common stock issued and outstanding. All share and per share amounts presented in this report have been retroactively adjusted to reflect the reverse stock split.

On August 17, 2010, the Company entered into a securities purchase agreement with investors for an aggregate of 187,500 shares of common stock. The shares were purchased at $4.00 per share for an aggregate of $750,000.

On August 30, 2010, Cenfin exercised 170,500 warrants at $2.00 per share, for an aggregate of $341,000, in accordance with the Credit Agreement entered into on June 5, 2009.

On October 1, 2010, Roomlinx, Inc. acquired 100% of the membership interests of Canadian Communications, LLC for aggregate consideration of $500,000 in cash and the issuance of 270,000 shares of Roomlinx’s common stock, of which 79,000 are being held back as security for the sellers’ indemnification obligations. Roomlinx, Canadian Communications, LLC, Peyton Communications, LLC, Garneau Alliance LLC, Peyton Holdings Corporation and Ed Garneau entered into a Unit Purchase Agreement providing for the above described transaction.

During 2010, an aggregate of 391,125 warrants were exercised pursuant to the clauses in securities purchase agreements. The warrants were exercised at various strike prices and resulted in the distribution of an aggregate of 387,400 shares of common stock.

During 2010, the board of directors approved the grant of an aggregate of 77,942 Incentive Stock Options and an aggregate of 6,813 Non-Qualified Stock Options. Such options were issued at various exercise prices, vest at various rates, and expire 7 years from the grant dates.

During 2010, 340,800 warrants were granted pursuant to the clauses in securities purchase agreements. The warrants were issued at various prices, vest at various rates, and expire at various dates.

Our Services

Currently we offer the following services to our customers:

|

|

v

|

site-specific determination of needs and requirements;

|

|

|

v

|

design and installation of the wireless or wired network;

|

|

|

v

|

customized development, design and installation of a media and entertainment system;

|

|

|

v

|

IP-based delivery of on-demand high-definition and standard-definition programming including Hollywood, Adult, and specialty content;

|

|

|

v

|

delivery of television programming via satellite (Direct TV or Dish Networks);

|

|

|

v

|

delivery of an electronic television programming guide (EPG) viewed via the television;

|

|

|

v

|

full maintenance and support of the network and Interactive TV product;

|

|

|

v

|

technical support to assist guests, hotel staff, and residential and business customers, 24 hours a day, 7 days a week, 365 days a year;

|

|

|

v

|

hotel staff and management training;

|

|

|

v

|

marketing assistance and continuous network and system monitoring to ensure high quality of service;

|

|

|

v

|

advertising sales and advertising sales support;

|

|

|

v

|

management of affiliated telecommunications systems.

|

9

Our strategy is to focus our resources on delivering quality communication, information, advertising, and E-commerce services to the hospitality industry and residential/business customers. We plan to aggressively penetrate the hotel, resort, and timeshare verticals through direct sales, channel sales agents, and acquisitions. We plan to continually develop our Interactive TV platform to meet the needs of the ever changing habits of the hotel guest. The networks that we install can supply a hotel with all of the internet requirements to the hotel’s back office, guest rooms, restaurants, lobbies, convention center, and meeting rooms over the internal local area network (LAN). Users access the Internet without any modification to their computer and can walk freely about the premises while still being connected to the network. In our residential system deployments, we offer bundled service (television, telephone, and internet access) to the residents of the particular development.

When we commence service to a new hotel property, we install hardware in the hotel and integrate that hardware into the hotel’s billing server. We give the client hotel property two options in acquiring our high-speed Internet services: the hotel can buy the system and pay us a monthly service fee to maintain technical support (usually on a per room per month basis), or the hotel can lease-to-own the system with a third party, or us, and pay us a monthly service fee. We also obtain fee income by enabling “meeting rooms” for our hotel customers.

We believe that we will continue to increase sales and gross profits by offering our Interactive TV platform to our current wired and wireless internet customer base. Roomlinx’ goal is to be the sole source solution for in-room technology, redefining how the hotel guests access traditional free-to-guest television, contemporary web content, premium, pre-release, and high-definition material, along with business tools and information specific to the property and their stay. We currently deliver this via our user-friendly, streamlined interface displayed on a sleek, flat-panel HD LCD television and powered by our Roomlinx media console. We believe we have truly converged the television and personal computer into one offering in hotel rooms. We also believe we have developed a truly unique and proprietary product in our Interactive TV platform.

Our residential and business telecommunications division, Cardinal Broadband, continues to expand its customer base by adding new residential developments, as well as continuing to market to its current residential properties in order to increase its penetration at those properties.

We seek to deepen penetration within our installed customer base and expand the breadth of our overall customer base by distinguishing our current and future offerings with value-added solutions through increased marketing activities and continued custom, proprietary software development efforts that enhance the Interactive TV platform.

Our Strategy

Our short term strategies include the following:

|

|

v

|

We are seeking to grow the number of rooms installed with our Interactive TV platform

|

|

|

v

|

We are seeking to make our Interactive TV platform our core competency and focus on quality service and highly-profitable opportunities;

|

|

|

v

|

We are seeking to grow the number of rooms under management. We can improve our margins through the recurring revenues that we receive from rooms under management;

|

|

|

v

|

We are seeking to attain preferred vendor status or become a brand standard with premier hotel chains. Our hotel customers include many of the country’s most highly regarded hotel chains. If we are successful in attaining preferred vendor status or becoming a brand standard, we will be able to expand our services to cover the applicable chain’s site map;

|

|

|

v

|

We are seeking to leverage our core competency by expanding the markets we serve beyond the United States and Canada into Central America and the Caribbean.

|

|

|

v

|

We hope to expand the IP-based services and Interactive TV platform that we offer to include:

|

|

|

●

|

IP-based television programming;

|

10

|

|

●

|

Integration with multiple web applications including:

|

|

|

■

|

3D games

|

|

|

■

|

Dining reservations

|

|

|

●

|

Television programming bundles

|

|

|

●

|

Custom integration with the Hotel’s back office applications

|

|

|

●

|

Expanded IP-based advertising through the LCD television and laptop;

|

|

|

●

|

Expanded IP-based E-Commerce through the LCD television and laptop;

|

|

|

●

|

Managed technical services, to provide special technical services to users.

|

|

|

●

|

Growth in our custom software development and professional service revenues

|

|

|

v

|

Through acquisition or organic growth we plan to:

|

|

|

■

|

Increase our media & entertainment base of customers.

|

|

|

■

|

Continue to focus on increasing revenues in our Canadian and other foreign segments.

|

|

|

■

|

Increase our high speed internet base of customers

|

|

|

■

|

Offer additional synergistic technologies or services that allow us to sell more of our Interactive TV platform

|

|

|

■

|

Expand our customer base in the residential and business markets

|

Our longer term strategies include the following:

|

|

v

|

We hope to be able to offer our Interactive TV platform to the consumer market;

|

|

|

v

|

Expansion into the European and Asian hotel industries; and,

|

|

|

v

|

We have begun to consider other infrastructure and value added services to include in our Interactive TV platform.

|

Ultimately, we hope to position ourselves as our customers’ central communications, entertainment and media provider. However, we cannot assure our investors that we will be successful in attaining these goals or that we will not pursue other strategies when opportunities arise. Capital constraints and competition, among other factors, may preclude us from attaining our goals.

Sales and Marketing

Sales

As of March 30, 2011, our direct sales force consisted of 4 persons and our channel sales program consisted of 1 master sales agent and over 30 sales agents. While we will always require a small in-house team of direct sales representatives, we believe that if we are to grow the scale of our operations, it will be necessary for us to develop a channel sales program utilizing sales agents and re-sellers. As a result, our direct sales are supplemented by strategic alliances with communication marketing companies and communication providers. These organizations already have preferred access to customers, which may give us an advantage in the marketplace. These sales representatives are paid on a commission basis. We provide sales training and packaged marketing materials to our independent representatives in order to obtain optimum installation contracts.

There are four succinct areas of outsource marketing in the hospitality sector that we concentrate our sales efforts on:

|

|

v

|

Hospitality Consultants - This group sells consulting services to hotel ownership and management groups. For the most part, they have strong relationships with the aforementioned groups to provide consulting expertise.

|

|

|

v

|

Independent Communication Sales Representatives, and Representative Organizations – this group sells communication products into the hotel industry. Because they sell multiple lines of communication services to hotels, they have direct contact with the Information Systems director. These services save money for the hotels as well as providing them with additional income to the hotel, and as such they have good access to the decision-maker in this market.

|

11

|

|

v

|

Wholesale Equipment Suppliers, Equipment Installers in the Hospitality Market - This group sells and installs central phone systems - also known as PBX systems - voice mail systems, property management systems and software related services directly into the hotel market. Since these services are directly related to both the income and marketing sides of the hospitality area, we believe that their access to this clientele is very good.

|

|

|

v

|

The Hotel Interconnect Individual or Companies - This group handles the installation and the maintenance for the independent communications sales representative and interconnect companies.

|

Typically, at least one and often all four of the above groups interact with the hotel industry on a daily basis. This provides us with a valuable source of sales and marketing personnel with direct contact into the industry.

Marketing

We typically deploy a marketing mix consisting of grass roots marketing by joining industry specific affiliations such as HTNG (Hotel Technology Next Generation) and AHLA (American Hotel and Lodging Association) direct mail, internet direct response, print ads in periodicals aimed at hospitality industry, and tradeshow sponsorship and support.

Operations

We have built a foundation on which to achieve quality customer service and scalability. We have achieved this by building the internal infrastructure, partnerships, and quality controls to scale quickly and offer quality services within the following areas: system integration, system deployment, software development, project management, and technical support and service.

For our high speed wired and wireless offering we act as a system design and integrator that aggregates the products and services required to install wireless high-speed networks and deploys them through a delivery infrastructure that combines in-house technical and RF (radio frequency) experts with select system integrators in the customer’s area. After installation we seek to manage the network under a long-term contract.

For our proprietary Interactive TV platform we control the development of the product in-house allowing us to have ultimate control of response time to customer requests for product customization and version updates. For installation and support we utilize both certified partners and in-house personnel. We use In-house personnel for project management and pro-active monitoring of our technical components in the field.

For our residential telecommunications offerings, we design and deploy these projects using in-house personnel, as well as occasionally outsourcing installation labor if needed. Ongoing service and support is provided using in-house resources. Television content and bandwidth provisioning is secured through 3rd party providers, such as DISH Network, DirecTv, and Qwest.

12

Competition

Wired and Wireless High-Speed Internet Offering

The market for our high-speed internet (“HSIA”) services has leveled off. Our competitors may use the same products and services in competition with us. With time and capital, it would be possible for competitors to replicate our services and offer similar services at a lower price. We expect that we will compete primarily on the basis of the functionality, breadth, quality and price of our services. Our current and potential competitors include:

- Other wireless high-speed internet access providers, such as iBahn, Guest-Tek, AT&T, and LodgeNet;

- Other internal information technology departments of large companies.

Many of our existing and potential competitors may have greater financial, technical, marketing and distribution resources than we do. Additionally, many of these companies may have greater name recognition and more established relationships with our target customers.

Media and Entertainment

The market for our Interactive TV services is in its infancy. Due to technological advances we believe many of the larger companies will not be able to react quickly in duplicating our offering. The market for free to guest services in the hospitality industry is strong, and we believe it will remain strong for the future due to the demand for HD content. We continue to win customers by being a single source for all of a hotel’s telecommunication needs.

Current competition consists of players offering portions of our offering, such as video on demand, internet access, and free-to-guest programming; these competitors include:

- LodgeNet, SuiteLinq, KoolKonnect, NXTV, World Cinema, and Guest-Tek.

Residential and Business Telecommunications

This market is served by multiple competitors, primarily the Incumbent Local Exchange Carriers (ILECs) (Qwest), the cable company (Comcast), and multiple small independent companies providing individual television, telephone, and internet services. We believe we will continue to gain customers by distinguishing ourselves from our competitors by superior service and competitive pricing. Sometimes we gain a competitive advantage because we are not the ILEC or large cable company, as many customers prefer a company who is not so large and cannot give customized attention to their individual needs.

Many of our existing and potential competitors may have greater financial, technical, marketing and distribution resources than we do. Additionally, many of these companies may have greater name recognition and more established relationships with our target customers.

Research and Development

We seek to continually enhance the features and performance of our existing products and services. In addition, we are continuing to evaluate new products to meet our customers’ expectations of ongoing innovation and enhancements.

Our ability to meet our customers’ expectations depends on a number of factors, including our ability to identify and respond to emerging technological trends in our target markets, develop and maintain competitive products, enhance our existing products by adding features and functionality that differentiate them from those of our competitors and offering products on a timely basis and at competitive prices. Consequently, we have made, and we intend to continue to make, investments in research and development.

13

Patents and Trademarks

We own the registered trademarks of “SuiteSpeed®,” “SmartRoom®,” and “Roomlinx®”. We also have proprietary processes and other trade secrets that we utilize in our business.

Employees

As of March 30, 2011 we had a total of 31 full-time personnel and 2 part-time personnel. None of our employees are covered by a collective bargaining agreement. We believe that our relations with our employees are good.

Environmental Matters

We believe that we are in compliance with all current federal and state environmental laws and currently have no costs associated with compliance with environmental laws or regulations.

Dependence on Key Customers and Suppliers

We are not dependent on any single customer or a few major customers for a material portion of our revenues.

The remote control devices required to utilize our services are currently supplied by a single supplier. The content for our unlimited movie services is currently supplied by a single supplier. Our set top boxes are currently supplied by a single supplier, although we are currently testing set top boxes from additional suppliers. It would require some time in order for us to replace a supplier. Therefore, in the event that the supply of any of these items from any of these suppliers was to be interrupted without sufficient notice, it would have a material adverse impact on us.

ITEM 1A. RISK FACTORS

An investment in our company is very speculative and involves a very high degree of risk. An investment in our company is suitable only for the persons who can afford the loss of their entire investment. Accordingly, investors should carefully consider the following risk factors, as well as other information set forth in this report, in making an investment decision with respect to our securities. We have sought to identify what we believe to be all material risks and uncertainties to our business and ownership of our common stock, but we cannot predict whether, or to what extent, any of such risks or uncertainties may be realized nor can we guarantee that we have identified all possible risks and uncertainties that might arise. Additional risks and uncertainties that we do not currently know about or that we currently believe are immaterial may also harm our business operations. If any of these risks or uncertainties occurs, it could have a material adverse effect on our business.

Risks Relating to Our Business

We Have Only a Limited Operating History, Which Makes It Difficult to Evaluate an Investment in Our Common Stock.

We have only a limited operating history on which you can evaluate our business, financial condition and operating results. We face a number of risks encountered by early stage technology companies that participate in new technology markets, including our ability to:

|

●

|

Maintain our engineering and support organizations, as well as our distribution channels;

|

|

|

●

|

Negotiate and maintain favorable usage rates with our vendors;

|

|

●

|

Retain and expand our customer base at profitable rates;

|

|

|

●

|

Recoup our expenses associated with the wireless devices we resell to subscribers;

|

14

|

●

|

Manage expanding operations, including our ability to expand our systems if our subscriber base grows substantially;

|

|

|

●

|

Attract and retain management and technical personnel; and

|

|

●

|

Anticipate and respond to market competition and changes in technologies as they develop and become available.

|

We may not be successful in addressing or mitigating these risks and uncertainties, and if we are not successful our business could be significantly and adversely affected.

Some of Our Supplies Are Provided By One Supplier Each

The remote control devices required to utilize our services are currently supplied by a single supplier. The content for our unlimited movie services is currently supplied by a single supplier. Our set top boxes are currently supplied by a single supplier, although we are currently testing set top boxes from additional suppliers. It would require some time in order for us to replace a supplier. Therefore, in the event that the supply of any of these items from any of these suppliers was to be interrupted without sufficient notice, it would have a material adverse impact on us.

To Generate Increased Revenue We Will Have to Increase Substantially the Number of Our Customers, Which May be Difficult to Accomplish.

Adding new customers will depend to a large extent on the success of our direct and indirect distribution channels and acquisition strategy, and there can be no assurance that these will be successful. Our customers’ experiences may be unsatisfactory to the extent that our service malfunctions or our customer care efforts, including our website and 800 number customer service efforts, do not meet or exceed subscriber expectations. In addition, factors beyond our control, such as technological limitations of the current generation of devices, which may cause our customers’ experiences with our service to not meet their expectations, can adversely affect our revenues.

We May Acquire or Make Investments in Companies or Technologies That Could Cause Loss of Value to Our Stockholders and Disruption of Our Business.

Subject to our capital constraints, we intend to continue to explore opportunities to acquire companies or technologies in the future. Entering into an acquisition entails many risks, any of which could adversely affect our business, including:

|

●

|

Failure to integrate the acquired assets and/or companies with our current business;

|

|

|

●

|

The price we pay may exceed the value we eventually realize;

|

|

●

|

Loss of share value to our existing stockholders as a result of issuing equity securities as part or all of the purchase price;

|

|

|

●

|

Potential loss of key employees from either our current business or the acquired business;

|

|

●

|

Entering into markets in which we have little or no prior experience;

|

|

|

●

|

Diversion of management’s attention from other business concerns;

|

|

●

|

Assumption of unanticipated liabilities related to the acquired assets; and

|

|

|

●

|

The business or technologies we acquire or in which we invest may have limited operating histories, may require substantial working capital, and may be subject to many of the same risks we are.

|

We Have Limited Resources and We May be Unable to Effectively Support Our Operations.

We must continue to develop and expand our systems and operations in order to remain competitive. We expect this thesis to place strain on our managerial, operational and financial resources. We may be unable to develop and expand our systems and operations for one or more of the following reasons:

|

●

|

We may not be able to retain at reasonable compensation rates qualified engineers and other employees necessary to expand our capacity on a timely basis;

|

15

|

●

|

We may not be able to dedicate the capital necessary to effectively develop and expand our systems and operations; and

|

|

●

|

We may not be able to expand our customer service, billing and other related support systems.

|

If we cannot manage our operations effectively, our business and operating results will suffer.

Our Business Prospects Depend in Part on Our Ability to Maintain and Improve Our Services as Well as to Develop New Services.

We believe that our business prospects depend in part on our ability to maintain and improve our current services and to develop new services. Our services will have to achieve market acceptance, maintain technological competitiveness and meet an expanding range of customer requirements. We may experience difficulties that could delay or prevent the successful development, introduction or marketing of new services and service enhancements. Additionally, our new services and service enhancements may not achieve market acceptance.

If We Do Not Respond Effectively and on A Timely Basis to Rapid Technological Change, Our Business Could Suffer.

Our industry is characterized by rapidly changing technologies, industry standards, customer needs and competition, as well as by frequent new product and service introductions. Our services are integrated with the computer systems of our customers. We must respond to technological changes affecting both our customers and suppliers. We may not be successful in developing and marketing, on a timely and cost-effective basis, new services that respond to technological changes, evolving industry standards or changing customer requirements. Our success will depend, in part, on our ability to accomplish all of the following in a timely and cost-effective manner:

|

●

|

Effectively using and integrating new technologies;

|

|

|

●

|

Continuing to develop our technical expertise;

|

|

●

|

Enhancing our engineering and system design services;

|

|

|

|

●

|

Developing services that meet changing customer needs;

|

|

●

|

Advertising and marketing our services; and

|

|

●

|

Influencing and responding to emerging industry standards and other changes.

|

We Depend on Retaining Key Personnel. The Loss of Our Key Employees Could Materially Adversely Affect Our Business.

Due to the technical nature of our services and the dynamic market in which we compete, our performance depends in part on our retaining key employees. Competitors and others may attempt to recruit our employees. A major part of our compensation to our key employees is in the form of stock option grants. A prolonged depression in our stock price could make it difficult for us to retain our employees and recruit additional qualified personnel.

An Interruption in the Supply of Products and Services That We Obtain From Third Parties Could Cause a Decline in Sales of Our Services.

In designing, developing and supporting our services, we rely on many third party providers. These suppliers may experience difficulty in supplying us products or services sufficient to meet our needs or they may terminate or fail to renew contracts for supplying us these products or services on terms we find acceptable. If our liquidity deteriorates, our vendors may tighten our credit, making it more difficult for us to obtain suppliers on terms satisfactory to us. Any significant interruption in the supply of any of these products or services could cause a decline in sales of our services, unless and until we are able to replace the functionality provided by these products and services. We also depend on third parties to deliver and support reliable products, enhance their current products, develop new products on a timely and cost-effective basis and respond to emerging industry standards and other technological changes.

16

We May Face Increased Competition, Which May Negatively Impact Our Prices for Our Services or Cause Us to Lose Business Opportunities.

The market for our services is becoming increasingly competitive. Our competitors may use the same products and services in competition with us. With time and capital, it would be possible for competitors to replicate our services and offer similar services at a lower price. We expect that we will compete primarily on the basis of the functionality, breadth, quality and price of our services. Our current and potential competitors include:

|

●

|

Other wireless high speed internet access providers, such as SDSN, Guest-Tek Wayport, Greentree, Core Communications and StayOnLine;

|

|

|

●

|

Other viable network carriers, such as SBC, Comcast, Sprint and COX Communications; and

|

|

●

|

Other internal information technology departments of large companies.

|

Many of our existing and potential competitors have substantially greater financial, technical, marketing and distribution resources than we do. Additionally, many of these companies have greater name recognition and more established relationships with our target customers. Furthermore, these competitors may be able to adopt more aggressive pricing policies and offer customers more attractive terms than we can. In addition, we have established strategic relationships with many of our potential competitors. In the event such companies decide to compete directly with us, such relationships would likely be terminated, which could have a material adverse effect on our business and reduce our market share or force us to lower prices to unprofitable levels.

We May be Sued by Third Parties For Infringement of Their Proprietary Rights and We May Incur Substantial Defense Costs and Possibly Substantial Royalty Obligations or Lose The Right to Use Technology Important To Our Business.

Any intellectual property claims, with or without merit, could be time consuming and expensive to litigate or settle and could divert management attention from administering our business. A third party asserting infringement claims against us or our customers with respect to our current or future products may materially adversely affect us by, for example, causing us to enter into costly royalty arrangements or forcing us to incur settlement or litigation costs.

Our Quarterly Operating Results are Subject to Significant Fluctuations and, As A Result, Period-To-Period Comparisons of Our Results of Operations are Not Necessarily Meaningful.

|

●

|

The success of our brand building and marketing campaigns;

|

|

|

●

|

Price competition from potential competitors;

|

|

●

|

The amount and timing of operating costs and capital expenditures relating to establishing the Company’s business operations;

|

|

|

●

|

The demand for and market acceptance of our products and services;

|

|

●

|

Changes in the mix of services sold by our competitors;

|

|

|

●

|

Technical difficulties or network downtime affecting communications generally;

|

|

●

|

The ability to meet any increased technological demands of our customers; and

|

|

|

●

|

Economic conditions specific to our industry.

|

Therefore, our operating results for any particular quarter may differ materially from our expectations or those of security analysts and securities traders and may not be indicative of future operating results. The failure to meet expectations may cause the price of our common stock to decline. Since we are susceptible to these fluctuations, the market price of our common stock may be volatile, which can result in significant losses for investors who purchase our common stock prior to a significant decline in our stock price.

17

A Significant Amount of Our Common Stock is Held by a Few Stockholders

As of March 30, 2011, Matthew Hulsizer and Jennifer Just, directly and indirectly, together with certain of their affiliates, held 1,430,022 (or approximately 28.8%) of our outstanding shares of common stock and could, therefore, have a significant influence on us.

Potential Fluctuations In Quarterly Operating Results

Our quarterly operating results may fluctuate significantly in the future as a result of a variety of factors, most of which are outside of our control, including: the demand for our products and services; seasonal trends in purchasing; the amount and timing of capital expenditures and other costs relating to the development of our products and services; price competition or pricing changes in the industry; technical difficulties or system downtime; general economic conditions, and economic conditions specific to the hospitality industry. Our quarterly results may also be significantly impacted by the impact of the accounting treatment of acquisitions, financing transactions or other matters. Due to the foregoing factors, among others, it is likely that our operating results will fall below our expectations or those of investors in some future quarter.

Limitation of Liability and Indemnification of Officers and Directors

Our officers and directors are required to exercise good faith and high integrity in the management of our affairs. Our Articles of Incorporation provides, however, that our officers and directors shall have no personal liability to us or our stockholders for damages for any breach of duty owed to us or our stockholders, unless they breached their duty of loyalty, did not act in good faith, knowingly violated a law, or received an improper personal benefit. Our Articles of Incorporation and By-Laws also provide for the indemnification by us of our officers and directors against any losses or liabilities they may incur by reason of their serving in such capacitates, provided that they do not breach their duty of loyalty, act in good faith, do not knowingly violate a law, and do not received an improper personal benefit. Additionally, we have entered into individual Indemnification Agreements with each of our directors and officers to implement with more specificity the indemnification provisions provided by the Company’s By-Laws and provide, among other things, that to the fullest extent permitted by applicable law, the Company will indemnify such director or officer against any and all losses, expenses and liabilities arising out of such director’s or officer’s service as a director or officer of the Company, as the case may be. The Indemnification Agreements also contain detailed provisions concerning expense advancement and reimbursement.

Disclosure Controls and Procedures and Potential Inability to Make Required Public Filings

As of March 30, 2011, we have 31 full-time employees. Given our limited personnel, we may be unable to maintain effective controls to insure that we are able to make all required public filings in a timely manner. In fact, from December 27, 2005 until May 14, 2009, our Common Stock was removed from listing from the OTC Bulletin Board as a result of our failure to timely make all our required public filings. If we do not make all public filings in a timely manner, our shares of common stock may again be delisted from the OTC Bulletin Board and we could also be subject to regulatory action and/or lawsuits by stockholders.

Risks Relating to Our Common Stock

Resale of Shares Could Adversely Affect the Market Price of Our Common Stock and Our Ability to Raise Additional Equity Capital

The sale or availability for sale, of common stock in the public market pursuant to filed or future prospectuses may adversely affect the prevailing market price of our common stock and may impair our ability to raise additional capital by selling equity or equity-linked securities. The resale of a substantial number of shares of our common stock in the public market could adversely affect the market price for our common stock and make it more difficult for you to sell our shares at times and prices that you feel are appropriate.

18

Articles of Incorporation Grants the Board of Directors the Power to Designate and Issue Additional Shares of Preferred Stock.

Our Articles of Incorporation grants our Board of Directors authority to, without any action by our stockholders, designate and issue, from our authorized capital, shares in such classes or series as it deems appropriate and establish the rights, preferences, and privileges of such shares, including dividends, liquidation and voting rights. The rights of holders of classes or series of preferred stock that may be issued could be superior to the rights of the common stock offered hereby. Our board of directors’ ability to designate and issue shares could impede or deter an unsolicited tender offer or takeover proposal. Further, the issuance of additional shares having preferential rights could adversely affect other rights appurtenant to the shares of common stock offered hereby. Any such issuances will dilute the percentage of ownership interest of our stockholders and may dilute our book value.

Lack of Liquid Trading Market for Common Stock

Although our stock is quoted on the OTC Bulletin Board (the “OTCBB”) under the symbol “RMLX”, the market for our common stock is not liquid as there have been days when our stock did not trade even though it was quoted.

Limited Market Due To Penny Stock

Our stock differs from many stocks, in that it is considered a penny stock. The Securities and Exchange Commission has adopted a number of rules to regulate penny stocks. These rules include, but are not limited to, Rules 3a5l-l, 15g-1, 15g-2, 15g-3, 15g-4, 15g-5, 15g-6 and 15g-7 under the Securities and Exchange Act of 1934, as amended. Because our securities probably constitute penny stock within the meaning of the rules, the rules would apply to our securities and us. The rules may further affect the ability of owners of our stock to sell their securities in any market that may develop for them. There may be a limited market for penny stocks, due to the regulatory burdens on broker-dealers. The market among dealers may not be active. Investors in penny stock often are unable to sell stock back to the dealer that sold them the stock. The mark-ups or commissions charged by the broker-dealers may be greater than any profit a seller may make. Because of large dealer spreads, investors may be unable to sell the stock immediately back to the dealer at the same price the dealer sold the stock to the investor. In some cases, the stock may fall quickly in value. Investors may be unable to reap any profit from any sale of the stock, if they can sell it at all.

Stockholders should be aware that, according to the Securities and Exchange Commission Release No. 34-29093, the market for penny stocks has suffered in recent years from patterns of fraud and abuse. These patterns include: control of the market for the security by one or a few broker-dealers that are often related to the promoter or issuer; manipulation of prices through prearranged matching of purchases and sales and false and misleading press releases; “boiler room” practices involving high pressure sales tactics and unrealistic price projections by inexperienced sales persons; excessive and undisclosed bid-ask differentials and markups by selling broker-dealers; and the wholesale dumping of the same securities by promoters and broker-dealers after prices have been manipulated to a desired level, along with the inevitable collapse of those prices with consequent investor losses.

Furthermore, the penny stock designation may adversely affect the development of any public market for our shares of common stock or, if such a market develops, its continuation. Broker-dealers are required to personally determine whether an investment in penny stock is suitable for customers. Penny stocks are securities (i) with a price of less than five dollars per share; (ii) that are not traded on a “recognized” national exchange; (iii) whose prices are not quoted on the NASDAQ automated quotation system (NASDAQ-listed stocks must still meet requirement (i) above); and (iv) of an issuer with net tangible assets less than $2,000,000 (if the issuer has been in continuous operation for at least three years) or $5,000,000 (if in continuous operation for less than three years), or with average annual revenues of less than $6,000,000 for the last three years. Section 15(g) of the Exchange Act and Rule 15g-2 of the Commission require broker-dealers dealing in penny stocks to provide potential investors with a document disclosing the risks of penny stocks and to obtain a manually signed and dated written receipt of the document before effecting any transaction in a penny stock for the investor’s account. Potential investors in our common stock are urged to obtain and read such disclosure carefully before purchasing any shares that are deemed to be penny stock. Rule 15g-9 of the Commission requires broker-dealers in penny stocks to approve the account of any investor for transactions in such stocks before selling any penny stock to that investor.

19

This procedure requires the broker-dealer to (i) obtain from the investor information concerning his financial situation, investment experience and investment objectives; (ii) reasonably determine, based on that information, that transactions in penny stocks are suitable for the investor and that the investor has sufficient knowledge and experience as to be reasonably capable of evaluating the risks of penny stock transactions; (iii) provide the investor with a written statement setting forth the basis on which the broker-dealer made the determination in (ii) above; and (iv) receive a signed and dated copy of such statement from the investor, confirming that it accurately reflects the investor’s financial situation, investment experience and investment objectives. Compliance with these requirements may make it more difficult for the Company’s stockholders to resell their shares to third parties or to otherwise dispose of them.

The Trading Price Of Our Common Stock May Fluctuate Significantly Due To Factors Beyond Our Control

The trading price of our common stock will be subject to significant fluctuations in response to numerous factors, including:

|

●

|

Variations in anticipated or actual results of operations;

|

|

|

●

|

Announcements of new products or technological innovations by us or our competitors;

|

|

|

●

|

Changes in earnings estimates of operational results by analysts;

|

|

|

●

|

Inability of market makers to combat short positions on the stock;

|

|

|

●

|

Inability of the market to absorb large blocks of stock sold into the market; and

|

|

|

●

|

Comments about us or our markets posted on the Internet.

|

Moreover, the stock market from time to time has experienced extreme price and volume fluctuations, which have particularly affected the market prices for emerging growth companies and which often have been unrelated to the operating performance of the companies. These broad market fluctuations may adversely affect the market price of our common stock. If our stockholders sell substantial amounts of their common stock in the public market, the price of our common stock could fall. These sales also might make it more difficult for us to sell equity or equity related securities in the future at a price we deem appropriate.

We Do Not Intend to Pay Dividends on Our Common Stock.

We have never paid or declared any cash dividends on our common stock and intend to retain any future earnings to finance the development and expansion of our business. We do not anticipate paying any cash dividends on our common stock in the foreseeable future. Unless we pay dividends, our stockholders will not be able to receive a return on their shares of common stock unless they sell them.

Sarbanes-Oxley and Federal Securities Laws Reporting Requirements Can Be Expensive

As a public reporting company, we are subject to the Sarbanes-Oxley Act of 2002, as well as the information and reporting requirements of the Securities Exchange Act of 1934, as amended, and other federal securities laws. The costs of compliance with the Sarbanes-Oxley Act and of preparing and filing annual and quarterly reports, proxy statements and other information with the SEC, and furnishing audited reports to stockholders, are significant and may increase in the future.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

20

ITEM 2. PROPERTY

We lease our principal offices, which are located at 2150 West 6th Avenue, Unit H, Broomfield, CO 80020, consisting of approximately 6,400 square feet.

ITEM 3. LEGAL PROCEEDINGS

From time to time, the Company is a party to litigation, none of which is individually material to the business operations of the Company.

No material legal proceedings to which the Company (or any officer or director of the Company, or any affiliate or owner of record or beneficially of more than five percent of the Common Stock, to management’s knowledge) is party to or to which the property of the Company is subject is pending, and no such material proceeding is known by management of the Company to be contemplated.

ITEM 4. RESERVED

21

PART II

ITEM 5. MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

Our common stock trades on the OTC-Bulletin Board under the symbol “RMLX”. Our Class A Preferred Stock trades on the OTC-Bulletin Board under the symbol “RMLXP”. For the periods indicated, the following table sets forth the high and low bid quotations for our Common Stock and Class A Preferred Stock as reported by the National Quotation Bureau, Inc. The quotations represent inter-dealer quotations without retail mark-up, mark-down or commission and may not necessarily represent actual transactions.

All common shares and share prices reflected in the financial statements and in the discussions below reflect the effect of the 1-for-100 reverse stock split approved on May 28, 2010 and affected on July 29, 2010.

|

SYMBOL

|

TIME PERIOD

|

LOW

|

HIGH

|

||||||

|

RMLX

|

January 1, - March 31, 2009

|

$ | 1.00 | $ | 3.00 | ||||

|

April 1, - June 30, 2009

|

$ | 1.00 | $ | 4.00 | |||||

|

July 1, - September 30, 2009

|

$ | 2.00 | $ | 3.00 | |||||

|

October 1, - December 31, 2009

|

$ | 2.00 | $ | 3.00 | |||||

|

January 1, - March 31, 2010

|

$ | 1.30 | $ | 2.70 | |||||

|

April 1, - June 30, 2010

|

$ | 2.50 | $ | 5.50 | |||||

|

July 1, - September 30, 2010

|

$ | 2.00 | $ | 5.00 | |||||

|

October 1, - December 31, 2010

|

$ | 2.75 | $ | 4.35 | |||||

|

RMLXP

|

January 1 – March 31, 2009

|

$ | 0.04 | $ | 0.04 | ||||

|

April 1 – June 30, 2009

|

$ | 0.04 | $ | 0.05 | |||||

|

July 1 – September 30, 2009

|

$ | 0.05 | $ | 0.05 | |||||

|

October 1, - December 31, 2009

|

$ | 0.05 | $ | 0.05 | |||||

|

January 1, - March 31, 2010

|

$ | 0.05 | $ | 0.05 | |||||

|

April 1, - June 30, 2010

|

$ | 0.07 | $ | 0.15 | |||||

|

July 1, - September 30, 2010

|

$ | 0.07 | $ | 0.07 | |||||

|

October 1, - December 31, 2010

|

$ | 0.10 | $ | 0.10 | |||||

The closing bid for our Common Stock on the OTC-Bulletin Board on March 29, 2011 was $1.45. As of March 29, 2011, 5,021,415 shares of Common Stock were issued and outstanding which were held of record by 277 persons. As of March 29, 2011, 720,000 shares of Class A Preferred Stock were issued and outstanding which were held of record by 2 persons.

The Company has not paid any cash dividends on its stock. During the year ended December 31, 2009, the Company paid dividends of $91,532 on its Series C Preferred Stock through the issuance of 61,022 shares of common stock. No dividends were paid in stock during 2010. The Series C Preferred Stock was converted into 1,000,000 shares of Common Stock on March 31, 2009. There are no restrictions currently in effect which preclude the Company from declaring dividends. However, dividends may not be paid on the common stock while there are accrued but unpaid dividends on the Class A Preferred Stock, which bears a 9% cumulative dividend. As of December 31, 2010 accumulated but unpaid Class A Preferred Stock dividends aggregated $159,240. It is the current intention of the Company to retain any earnings in the foreseeable future to finance the growth and development of its business and not pay dividends on the common stock.

22

Recent Sales of Unregistered Securities

On November 24, 2009, 60,000 warrants were granted by Roomlinx to Marilyn Crawford pursuant to an advisory board agreement dated November 24, 2009. Such warrants were issued at an exercise price of $2.30 per share; 30,000 warrant shares were to vest at the rate of 1,250 per month starting on December 31, 2009 and continuing, unless earlier terminated, for a period of 24 months. The remaining 30,000 warrant shares were to vest at the rate of 5,000 shares for each $250,000 in revenue for which the Ms. Crawford is responsible as set forth in the Advisory Board Agreement; the warrants were scheduled to expire three years from the date of issuance. On February 17, 2010, Roomlinx cancelled the advisory board contract with Marilyn Crawford effectively canceling the 56,250 unvested warrants issued in connection with the November 24, 2009 agreement.

On April 12, 2010, the Board of Directors granted 22,440 aggregate incentive stock options to employees of Roomlinx and 6,813 non-incentive stock options to contractors of Roomlinx. These options have an exercise price of $3.10, the fair market value on the grant date, and vest in three equal annual installments on the grant anniversary date. The options expire at the end of the business day on the 7th anniversary of the grant date.

On April 27, 2010, Cenfin LLC exercised 116,000 warrants at $2.00 per share, for an aggregate of $232,000, in accordance with the Credit Agreement entered into on June 5, 2009, as amended March 10, 2010.

On April 29, 2010, Roomlinx issued and sold (i) 225,000 shares of its Common Stock to Verition Multi-Strategy Master Fund Ltd. and (ii) 25,000 shares of its Common Stock to Wilmot Advisors LLC. The shares were purchased at $4.00 per share for an aggregate of $1,000,000.

On May 13, 2010, two individuals each exercised 5,000 warrants at $2.00 per share on a cashless basis resulting in the issuance of 3,040 shares of Common Stock to each of them.

On July 6, 2010, an investor exercised 19,625 warrants at $2.00 per share. The exercise was cashless and resulted in 11,775 shares being issued.

On July 30, 2010, with effect as of July 15, 2010, the Company and Cenfin LLC entered into a Second Amendment to Revolving Credit, Security and Warrant Purchase Agreement (the “Amendment”). The Amendment changed (1) the interest rate under the Credit Agreement to the Federal Funds Rate plus 5% and (2) the strike price of warrants issued in connection with any draws of the line of credit after the first $5,000,000 of borrowings after July 15, 2010 from $2.00 per share to the fair market value of the Company’s common stock on the date of such draw.

On August 2, 2010, warrants to purchase 170,500 shares were granted by Roomlinx to Cenfin LLC pursuant to the terms of the Credit Agreement (as amended on March 10, 2010 and July 15, 2010). Such warrants were issued at an exercise price of $2.00 per share, vesting immediately and expiring three years from the date of issuance.

On August 18, 2010, Roomlinx issued and sold (i) 87,500 shares of its Common Stock to Verition Multi-Strategy Master Fund Ltd., (ii) 67,500 shares of its Common Stock to Wilmot Advisors LLC, (iii) 27,500 shares of its Common Stock to Arceus Partnership, (iv) 2,500 shares of its Common Stock to Ted Hagan and (v) 2,500 shares of its Common Stock to Josh Goldstein. These issuances were at a price of $4.00 per share for an aggregate purchase price of $750,000.

23

On August 30, 2010, Cenfin LLC exercised the 170,500 warrants granted to it on August 2, 2010 at $2.00 per share, for an aggregate of $341,000.

On September 30, 2010, warrants to purchase 75,000 shares were granted by Roomlinx to Cenfin LLC pursuant to the terms of the Credit Agreement (as amended on March 10, 2010 and July 15, 2010). Such warrants were issued at an exercise price of $2.00 per share, vesting immediately and expiring three years from the date of issuance.

On October 1, 2010, Cenfin LLC exercised the 75,000 warrants granted to it on September 30, 2010 at an exercise price of $2.00 per share, for an aggregate of $150,000.

On October 1, 2010, Roomlinx, Inc. acquired 100% of the membership interests of Canadian Communications, LLC for aggregate consideration of $500,000 in cash and the issuance of 270,000 shares of Roomlinx’s common stock, of which 79,000 are being held back as security for the sellers’ indemnification obligations. At the sellers’ direction, and in consideration of releases of indebtedness and other obligations owed by Canadian, on October 1, 2010, Roomlinx issued (i) 48,000 shares of its Common Stock to Peyton Communications, LLC, (ii) 162,000 shares of its Common Stock to Thunderbird Management Limited Partnership, (iii) 18,000 shares of its Common Stock to AEJM Limited Partnership, and (v) 42,000 shares of its Common Stock to Garneau Alliance, LLC

On October 1, 2010, further to an Employment Agreement with Mr. Edouard Garneau, our Chief Financial Officer effective beginning on such date, and pursuant to Roomlinx’s standard stock option award agreement, Mr. Garneau was granted options to purchase 40,000 shares of Roomlinx Common Stock at an exercise price of $4.50 per share, the last publicly reported sales price of a share of Roomlinx Common Stock on such date, vesting equally over a three year period. The options expire at the end of the business day on the 7th anniversary of the grant date.

On November 18, 2010, our Board of Directors approved the grant to Jill Solomon of warrants to purchase 21,000 shares and the grant to Lisa Goodman of warrants to purchase 11,800 shares as compensation for marketing and public relations services rendered. Such warrants were issued at an exercise price of $4.50 per share, vesting immediately and expiring five years from the date of issuance.

On November 18, 2010, our Board of Directors approved the grant to employees under our Long-Term Incentive Plan of an aggregate of 11,000 Incentive Stock Options. Such options were issued at an exercise price of $3.75 per share (the last publicly reported sales price of a share of Roomlinx Common Stock on November 18, 2010) and vest one-third (1/3) on each of the first three anniversaries of the employment date.

On December 20, 2010, warrants to purchase 62,500 shares were granted by Roomlinx to Cenfin LLC pursuant to the terms of the Credit Agreement (as amended on March 10, 2010 and July 15, 2010). Such warrants were issued at an exercise price of $2.00 per share, vesting immediately and expiring three years from the date of issuance.

On March 3, 2011 65,000 warrants were granted, pursuant to the clauses outlined in the Credit Agreement dated June 5, 2009. Such warrants were issued at an exercise price of $2.00 per share and vest immediately; the warrants expire 3 years from the date of issuance.

On March 3, 2011, 62,500 warrants were exercised at $2.00 per share, for an aggregate of $125,000, in accordance with the Credit Agreement entered into on June 5, 2009.

ITEM 6. SELECTED FINANCIAL DATA

Not required.

24

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis should be read together with our consolidated financial statements, the accompanying notes to these financial statements, and the other financial information that appears elsewhere in this Annual Report on Form 10-K or our SEC filings.

GENERAL

Overview

Roomlinx, Inc., a Nevada corporation (“we,” “us” or the “Company”), provides four core products and services:

Wired Networking Solutions and Wireless Fidelity Networking Solutions.

We provide wired networking solutions and wireless fidelity networking solutions, also known as Wi-Fi, for high speed internet access at hotels, resorts, and timeshare locations. The Company installs and creates services that address the productivity and communications needs of hotel, resort, and timeshare guests. We specialize in providing advanced Wi-Fi wireless services such as the wireless standards known as 802.11a/b/g/n/i.

Hotel customers sign long-term service agreements, where we provide the maintenance for the networks, as well as the right to provide value added services over the network.

We derive revenues from the installation of the wired and wireless networks we provide to hotels, resorts, and timeshare properties. We derive additional revenue from the maintenance of these networks. Customers typically pay a one-time fee for the installation of the network and then pay monthly maintenance fees for the upkeep and support of the network.

In-room media and entertainment.

We provide in-room media and entertainment products and services for hotels, resorts, and time share properties. Products and services included within our in-room media and entertainment offering include our proprietary Interactive TV platform, Satellite TV programming, and on-demand movies.