Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SunCoke Energy, Inc. | d294219d8k.htm |

| EX-99.2 - SUPPLEMENTAL FINANCIAL INFORMATION - SEGMENT REVENUES - SunCoke Energy, Inc. | d294219dex992.htm |

Investor

Presentation February 2012

Exhibit 99.1 |

1

Safe Harbor Statement

Oppenheimer 2nd Annual London 1-1 Investor Conference

Some of the information included in this presentation contains “forward-looking

statements” (as defined in Section 27A of the Securities Act of 1933, as amended and

Section 21E of the Securities Exchange Act of 1934, as amended). Such forward-looking

statements are based on management’s beliefs and assumptions and on information currently available.

Forward-looking statements include the information concerning SunCoke’s possible or assumed

future results of operations, business strategies, financing plans, competitive position,

potential growth opportunities, potential operating performance improvements, effects resulting

from our separation from Sunoco, the effects of competition and the effects of future

legislation or regulations. Forward-looking statements include all statements that are not historical facts and may

be identified by the use of forward-looking terminology such as the words “believe,”

“expect,” “plan,” “intend,” “anticipate,”

“estimate,” “predict,” “potential,” “continue,”

“may,” “will,” “should” or the negative of these terms or similar expressions.

Forward-looking statements involve risks, uncertainties and assumptions. Actual results may differ

materially from those expressed in these forward-looking statements. You should not put

undue reliance on any forward-looking statements.

In accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of

1995, SunCoke has included in its filings with the Securities and Exchange Commission

cautionary language identifying important factors (but not necessarily all the important

factors) that could cause actual results to differ materially from those expressed in any

forward-looking statement made by SunCoke. For more information concerning these factors, see

SunCoke's Securities and Exchange Commission filings. All forward-looking statements

included in this presentation are expressly qualified in their entirety by such cautionary

statements. SunCoke undertakes no obligation to update publicly any forward-looking

statement (or its associated cautionary language) whether as a result of new information or future events or otherwise.

This presentation includes certain non-GAAP financial measures intended to supplement, not

substitute for, comparable GAAP measures. Reconciliations of non-GAAP financial measures to

GAAP financial measures are provided in the Appendix at the end of the presentation. Investors

are urged to consider carefully the comparable GAAP measures and the reconciliations to those

measures provided in the Appendix, or on our website at www.suncoke.com.

|

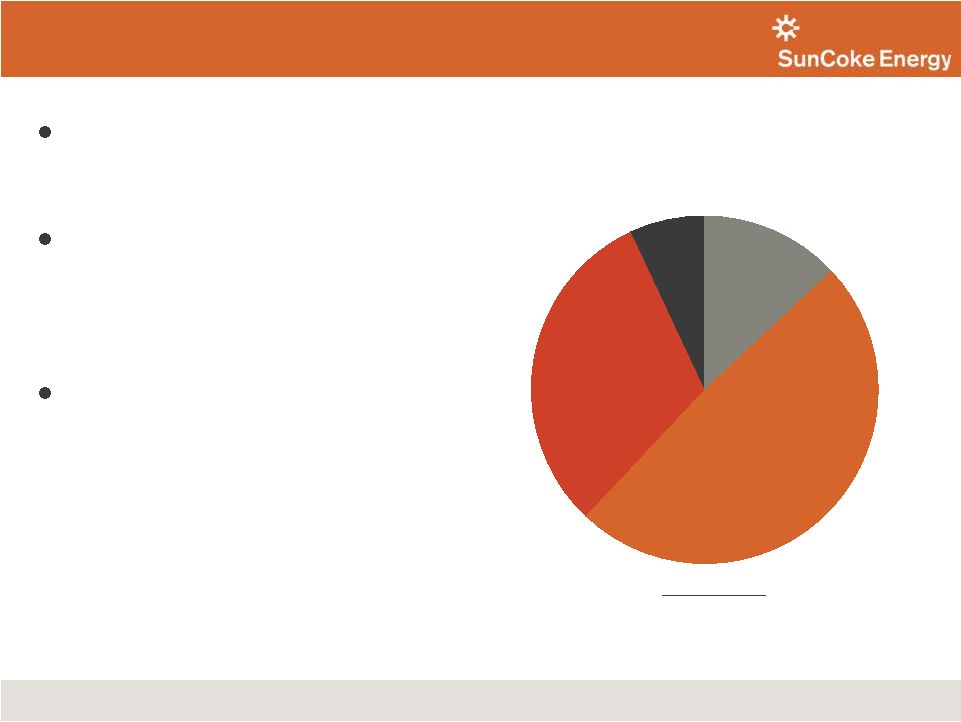

2

Coal

Mining

13%

Jewell

Coke

31%

Int'l Coke

7%

Other Domestic Coke

49%

SunCoke Introduction

2011 Adjusted EBITDA

(1)

(excluding Corporate Segment)

(1) For a definition of Adjusted EBITDA, please see the appendix.

Oppenheimer 2nd Annual London 1-1 Investor Conference

Largest independent producer of

metallurgical coke in Americas with

nearly 50 years experience

~85% of Adjusted EBITDA

(1)

generated

by cokemaking business

-

Secure, long-term take-or-pay

contracts with leading steelmakers

Metallurgical coal mining operations in

Virginia and West Virginia

-

2011 production of approximately

1.4 million tons

-

High quality metallurgical coal

reserves; primarily mid-vol.

2011 Results:

•Revenue of $1.5 billion

•Adjusted EBITDA

(1)

of $140.5 million |

3

5.9 million tons of capacity with

new Middletown, Ohio facility

-

Six cokemaking facilities; five in

U.S. and one in Brazil

-

More than doubled capacity

since 2005

Proven ability to permit, develop,

construct and start up new

facilities and work internationally

Industry leading environmental

signature: U.S. EPA Maximum

Achievable Control Technology

The Leading Independent Cokemaker

SunCoke

Cokemaking Capacity

(Tons in thousands)

Oppenheimer 2nd Annual London 1-1 Investor Conference

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2004

2005

2006

2007

2008

2009

2010

2011

Jewell Coke

Indiana Harbor

Haverhill I

Vitória

Haverhill II

Granite City

Middletown |

4

SunCoke’s Heat Recovery Oven vs. By-Product Oven

SunCoke’s technology is the industry’s environmental standard and provides many

advantages over the traditional cokemaking process

Oppenheimer 2nd Annual London 1-1 Investor Conference

Pressurization

Negative pressure

Positive pressure

Air Emissions

MACT standard for new

batteries

Potential for emission of hazardous

compounds

Power Generation

Cogenerates power

Power consuming process

Hazardous Inputs

None

Yes

–

sulfuric acid

Volatile Organic Compounds

Complete combustion

No combustion

Solid Wastes

No toxic solid wastes

Process produces toxic waste streams

SunCoke Heat Recovery

Traditional By-Product |

5

SunCoke‘s Value Proposition

Provide an assured supply of coke to steelmakers

Larger, stronger coke for improved blast furnace performance

Demonstrated sustained 30% turndown; higher turndown on temporary basis

High quality coke with cheaper coal blends

Burn loss vs. by-product

Capital preservation and lower capacity cost per ton; particularly relative to

greenfield investment

Stringent U.S. regulatory environment

Power prices and reliability versus value of coke oven gas and by-product

"credits"

High Quality &

Reliable Coke

Supply

Turndown

Flexibility

Coal Flexibility

Capital

Efficiency

and Flexibility

Environmental /

Economic

Trade-offs

Oppenheimer 2nd Annual London 1-1 Investor Conference |

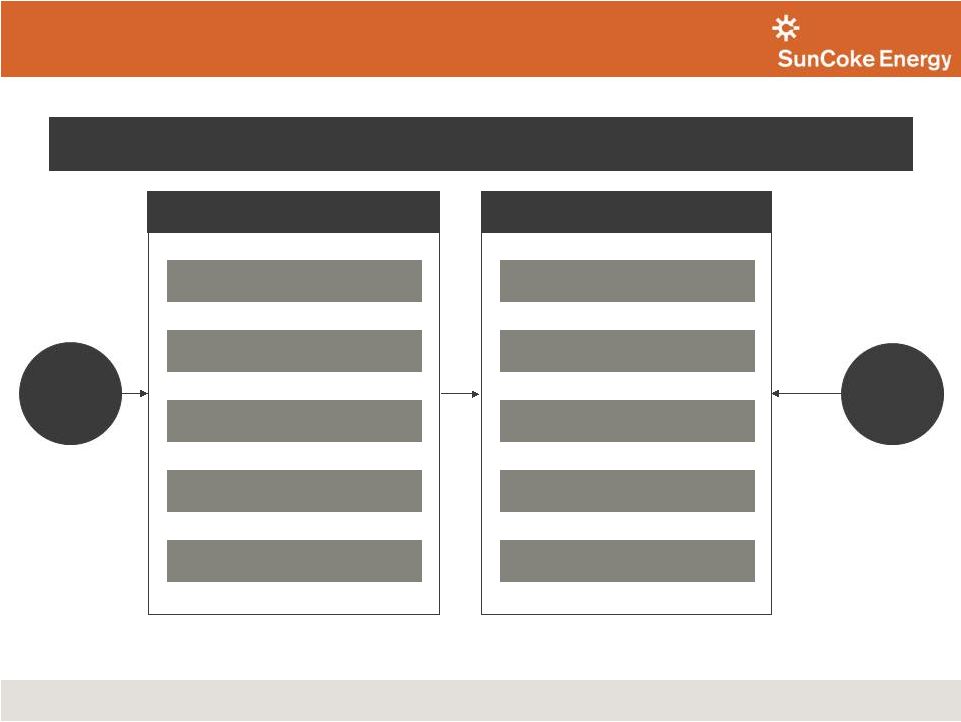

6

SunCoke’s Contract Proposition

Plant

Production

and

Environmental

Compliance

Permits and Approvals

Engineering, Procurement &

Construction

Capital Funding and Ownership

Reliable, High-Quality Coke Supply

Deliver coke to customers through a competitive turnkey solution,

which produces a consistent stream of earnings

Operating Cost Component

(Pass-Through)

Fixed Fee

(Profit and Return on Capital)

Coal Cost Component

(Pass-Through)

Take-Or-Pay

Taxes

and

Transportation

and

Future

Environmental

Costs

(Pass-Through)

Coke fee

Energy fee

Typical Key Coke Sales Agreement

Provisions

What SunCoke Offers

Oppenheimer 2nd Annual London 1-1 Investor Conference

SunCoke

Energy

Customer |

7

Focused Growth Strategy

Expand domestic coal production from current reserves and

improve efficiency of existing mines

We believe

SunCoke

Energy is

uniquely

positioned for

continued

investment and

earnings

growth

Continue to grow our U.S. and Canada cokemaking businesses;

reserving portion of future coke capacity for market sales

Grow international footprint in key growth markets with

immediate focus on India

Growth Initiatives

Oppenheimer 2nd Annual London 1-1 Investor Conference |

8

SunCoke's U.S. and Canada Market Position

Chinese Coke Price vs. Representative SunCoke Price

North American Coke Imports

SunCoke believes it has the opportunity to displace higher cost coke imports

.

SunCoke

Chinese

Q4 2011 Average:

$395

$422

2011 Average:

$387

$431

2008-2010 Average:

$326

$430

(US$/ton)

5.4

3.6

2.5

2.6

2.8

3.6

5.6

1.3

2.4

2.8

2.3

–

1.0

2.0

3.0

4.0

5.0

6.0

2006

2007

2008

2009

2010

2011E

2012E

2013E

2014E

2015E

2021E

SunCoke domestic coke sales volumes

SunCoke weighted-average domestic cokemaking capacity

(Tons in millions)

Source: CRU, The Annual Outlook for Metallurgical Coke 2011.

(1)

Represents SunCoke’s domestic cokemaking capacity weighted by the number of

months each facility operated during that year.

(1)

(1)

Source: Steel Business Briefing, 2012

(1)

Other Domestic Coke sales and other operating revenues divided by tons sold.

Oppenheimer 2nd Annual London 1-1 Investor Conference

$200

$300

$400

$500

$600

$700

Jan-08

Jan-09

Jan-10

Jan-11 |

9

$301

$442

$517

$395

$11

$130

$50

$25

$0

$100

$200

$300

$400

$500

Chinese Coke

Production Costs (1)

Handling/

Transportation

to Chinese Port

Average Export

License/

Tax Cost (40% Tariff)

Chinese Coke Cost

FOB Chinese Port

Transportation to

U.S.

Handling Losses

Net of Breeze Value

Chinese Coke Price

Delivered to U.S.

Q4 '11 SunCoke

Domestic Coke Price

SunCoke's U.S. and Canada Market Position

Source: CRU, The Annual Outlook for Metallurgical Coke 2011;

Company estimates. (1) Chinese Coke Production Costs net of By-Product

Credits; does not include return on capital. ($ per ton of coke)

Oppenheimer 2nd Annual London 1-1 Investor Conference

SunCoke Domestic Coke Pricing vs. Chinese Imports

40%

Tariff |

10

2010 U.S. & Canada Coke Supply

SunCoke’s U.S. and Canada Market Position

Source: CRU, The Annual Outlook for Metallurgical Coke 2011.

Replace aging coke batteries operated by integrated steel producers

Source: CRU, The Annual Outlook for Metallurgical Coke 2011.

Oppenheimer 2nd Annual London 1-1 Investor Conference

12 million tons or 56% of coke capacity at facilities

>30 years old

Integrated

Steel

Producers

60%

SunCoke

18%

DTE

5%

Other Merchant &

Foundry

7%

Imports

10%

Aging Cokemaking Facilities

9

41

28%

28%

SunCoke

U.S. & Canada

(excl SXC)

30-40 years

40+ years

Average Age

% of U.S. & Canada

coke production |

11

19

22

17

19

19

20

12

18

18

19

51

27

40

48

–

10

20

30

40

50

60

2006

2007

2008

2009

2010

2011E

2012E

2013E

2014E

2015E

Blast Furnace Coke Demand

BF/BOF Crude Steel Production

SunCoke's U.S. and Canada Market Position

BF/BOF Crude Steel Production

and Blast Furnace Coke Demand

3

2

Aging battery

replacement

Demand growth with

market recovery

Expected demand

opportunity by

2015

5

2010 Coke Rate:

894 lbs/thm

2015E Coke Rate:

800 lbs/thm

Market Opportunity

Source: CRU, The Annual Outlook for Metallurgical Coke 2011;

Company estimates. In million tons

million tons

Oppenheimer 2nd Annual London 1-1 Investor Conference

•

We

believe

SunCoke

is

positioned

to

capture

significant

share

of

market

opportunity

•

Next U.S. coke plant size anticipated to be up to 1.1 million tons

•

Near-term focus remains on obtaining permits; anticipated in latter half of 2012

•

Will defer seeking customer commitments until further progress on permits achieved in light

of current economic outlook |

12

India –

Macro Outlook

Population growth

•

1.2 billion people today

•

Projected 1.5 billion by 2030

•

Growth equal to the entire U.S.

population

Urbanization

•

Less than 50% urban population

•

Vehicle production 3.6 MM (’11)

vs. 13 MM in NAFTA

•

Lowest steel intensity of BRICs

Economic prosperity

•

Economy expected to grow

6-8% per year

•

Per capital income could triple

Per Capita Crude Steel Use

(2010)

Kg/y

India

58

Brazil

147

United States

292

China

445

World Avg.

221

Source: World Steel Association, 2011.

Significant

Expected

GDP

Growth

Source: CIA World Factbook.

Oppenheimer 2nd Annual London 1-1 Investor Conference

Source: Census.gov, United States Census Bureau - International Data Base, CIA World

Factbook.

|

13

India Opportunity for SunCoke

Oppenheimer 2nd Annual London 1-1 Investor Conference

India

Steel/Coke

Market

Strong market

fundamentals

with good fit

for SunCoke

technology

GROWING STEEL MARKET

•

Projected to be 3rd largest

steel market by 2020

•

Blast furnace to play a

critical role in growth

COKE SUPPLY DEFICIT

•

Importing between 2 and

5 million tons annually

•

Coke capacity investment

lags steel investment

•

3.5 million tons merchant

production or 13% of total

•

17 active merchant coke

producers

•

10% -

20% short power

•

Average wholesale price

>$80 mwh (2x U.S. rate)

ELECTRIC POWER DEFICIT

ACTIVE MERCHANT MARKET

Sources: CRU, The Annual Outlook for Metallurgical Coke 2011, CIA World

Factbook.

|

14

Why is China Important?

Chinese Crude Steel Production and Coke Consumption

Source: CRU, The Annual Outlook for Metallurgical Coke 2011;

Company estimates. In million tons

2011E World Steel Production

2011E World Coke Production

Oppenheimer 2nd Annual London 1-1 Investor Conference

•

Chinese steel market represents 45% of

world production

•

Steel market expected to grow 46%

over the next 10 years producing an

incremental 300+ million tons (more

than 2x entire U.S. market)

•

Integrated steelmaking comprises 90%

of production, driving China to

represent 62% of the world coke

market

•

China’s coke demand expected to grow

approximately 160 million tons in the

next 10 years (equivalent to nearly 7

U.S. markets)

•

Chinese government has targeted

closure of nearly 40 million tons of

older/inefficient coke capacity

Source: CRU, The Annual Outlook for Metallurgical Coke 2011;

Company estimates. Source: CRU, The Annual Outlook for Metallurgical Coke

2011; Company estimates. 290

344

393

493

520

570

339

366

411

439

467

464

966

1,069

732

626

912

855

792

691

552

545

–

150

300

450

600

750

900

1,050

1,200

2006

2007

2008

2009

2010

2011E

2012E

2013E

2014E

2015E

2021E

Chinese Consumption of Coke

Chinese Crude Steel Production

7%

3%

Rest of

World

48%

China

45%

U.S. & Canada

Rest of

World

35%

China

62%

U.S. &

Canada |

15

Coal Expansion

0.35 million tons expected

surface mining

1.15 million tons

expected production from Jewell

underground mines

0.30 million tons HKCC acquisition

Projected 2012 Coal Production

Planned Growth

Current Operations

Underground

Mining

Surface

Mining

Selective

Reserve

Additions

1.80 million tons

(Projected 2012 production; an

estimated increase of approximately

0.4 million tons from 2011E)

+

+

=

106 million tons of proven

and probable reserves

Reserve life of 50+ years

Near term focus on increasing

productivity at existing mines;

will defer opening new mines

until 2013

Currently limited to highwall

mining at HKCC

Signed agreement to extract

additional surface tons

Expect 1.2 million tons

over 3 years beginning in

2012

Acquired Harold Keene Coal

Companies in January 2011

Open to opportunistic

additions of coal reserves

Oppenheimer 2nd Annual London 1-1 Investor Conference |

16

Q4 2011 and Full Year 2011 Earnings Overview

Oppenheimer 2nd Annual London 1-1 Investor Conference

•

Q4 2011 and Full Year 2011 missed expectations due to unfavorable

impact of $12.2 million (net of income attributable to noncontrolling

interests) in accounting adjustments at Indiana Harbor

•

Q4 2011 Net Income attributable to shareholders of $8.0 million and

EPS of $0.12 per share

•

Full Year Net Income attributable to shareholders of $60.6 million

and EPS of $0.87 per share

•

Q4 2011 Adjusted EBITDA of $31.4 million and Full Year 2011

Adjusted EBITDA of $140.5 million

•

Executed successful startup of Middletown in late October

•

Continued strong domestic coke plant performance

•

Full Year 2011 Coal Mining Adjusted EBITDA increased $28M over 2010

•

Solid year end liquidity position with cash balance of $128 million and

undrawn revolver

•

Separation from Sunoco, Inc. completed on January 17, 2012

•

Elected three new independent directors to the Board |

17

Q4 2010 to Q4 2011

Adjusted EBITDA

(1)

Bridge

Adjusted EBITDA decrease reflects Indiana Harbor adjustments, higher corporate

costs and Black Lung Liability charge, offset by improved performance in Coal Mining and

the absence of ArcelorMittal legal/settlement costs

($ in millions)

Oppenheimer 2nd Annual London 1-1 Investor Conference

$34.7

$31.4

$10.2

$12.9

($12.2)

($6.5)

($6.0)

($1.7)

Q4 2010

Adjusted

EBITDA

Indiana Harbor

Adjustments

Corporate/Other

(Relocation/

Standalone) (2)

Black Lung

Liability Charge

Coke Segments

(Jewel Coke

Other Domestic Coke/

International)(3)

Net ArcelorMittal

Settlement Impact

Coal Mining (2) (3)

Q4 2011

Adjusted

EBITDA

(1) For a definition of Adjusted EBITDA and reconciliation of Adjusted EBITDA to net

income and operating income, please see the appendix.

(2)

Excludes Black Lung Liability charge

(3)

Jewell Coke includes approximately $0.2 million in favorable coal transfer impact, Coal

Mining includes offsetting $0.2 million unfavorable coal transfer impact.

|

18

Full Year 2010 to 2011

Adjusted EBITDA

(1)

Bridge

Adjusted EBITDA decrease reflects impact of ArcelorMittal settlement and higher corporate

costs,

offset by improved Coal Mining results

($ in millions)

Oppenheimer 2nd Annual London 1-1 Investor Conference

(1) For a definition of Adjusted EBITDA and reconciliation of Adjusted EBITDA to net

income and operating income, please see the appendix.

(2)

Excludes Black Lung Liability charge

(3)

Jewell Coke includes approximately $16.0 million in unfavorable coal transfer impact,

Coal Mining includes offsetting $16.0 million favorable coal transfer impact.

(4)

Excludes Middletown losses

$227.3

$140.5

$31.0

($34.7)

($23.9)

($28.5)

($12.2)

($7.3)

($11.2)

2010

Adjusted

EBITDA

Net ArcelorMittal

Settlement Impact

Corporate/Other

(Relocation/

Standalone Costs)

(2)(4)

Jewell Coke (3)

(ex-settlement)

Indiana Harbor

Adjustments

Other Domestic

Coke

(ex-settlement)(4)

Other

(Black Lung/

Middletown/

International)

Coal Mining (2)(3)

2011

Adjusted

EBITDA |

19

Domestic Coke Financial Summary

(Jewell Coke & Other Domestic Coke)

Domestic Coke Production

Domestic

Coke

Pro

Forma

Adjusted

EBITDA

(1)

,

Pro

Forma

for

ArcelorMittal Settlement and Coal Transfer Price

(Tons in thousands)

($ in millions, except per ton amounts)

Other

Domestic

Coke:

736

Other

Domestic

Coke:

745

Other

Domestic

Coke:

786

915

922

965

(1) For a definition of Pro Forma Adjusted EBITDA and Pro Forma Adjusted EBITDA/Ton

and a reconciliation of Pro Forma Adjusted EBITDA to operating income, please

see the appendix. (2) Other Domestic Coke results for Q4 ‘11 excludes

Middletown loss of approximately $0.4 million. (3) Includes Indiana Harbor

contract billing resolution of $6.0 million and inventory adjustment of $6.2 million,

of which $3.1 million is attributable to Q3 ’11.

861

$48

$36

$19

•

Q4 ‘11 increase over Q4 ‘10 reflects Middletown startup and

improvement at Indiana Harbor

•

Q4 ‘11 performance impacted by Indiana Harbor

accounting adjustments

1,014

Other

Domestic

Coke:

838

$42

$32

(2)

(3)

Oppenheimer 2nd Annual London 1-1 Investor Conference

179

174

177

179

176

282

256

301

314

309

286

266

276

293

289

168

165

168

179

172

68

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Jewell

Indiana Harbor

Haverhill

Granite City

Middletown

Other

Domestic

Coke:

687

$11

$11

$11

$14

$11

$31

$8

$25

$34

$21

$46/ton

$22/ton

$39/ton

$50/ton

$34/ton

$ 0

$ 20

$ 40

$ 60

$ 80

$ 120

$ 140

($5)

$5

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Jewell Coke Segment

Other Domestic Coke Segment

Pro Forma Adjusted EBITDA/ton |

20

2012 Priorities

Oppenheimer 2nd Annual London 1-1 Investor Conference

•

Execute the ramp up of Middletown; expect to reach full production

levels in Q2 2012

•

Achieve targeted coke production volumes of 4.0 to 4.2 million tons

•

Continue permitting work for potential new U.S. plant in anticipation of a

market recovery

•

Implement India entry strategy by completing due diligence and

negotiating definitive agreements

•

Drive improved productivity at existing mines; mining a

projected

1.8 million tons and positioning segment for future expansion |

21

Coal Expansion

Coal prices offer attractive growth and

return on capital in our coal mining business

SunCoke’s Mid-Vol. Coal

Contract Prices

$130

$165

2010

2011

2012E

$170 - $190

2012

Estimates

MV

(2)

HV

Thermal

Total

Sales Tons

(1)

1,550k

150k

150k

1,850k

% Committed

88%

27%

40%

79%

Price of

Committed

Tons (per ton)

$177

$130

$81

$171

Estimated Price Range of Uncommitted Tons (per ton)

High

$170

$120

$80

Low

$150

$100

$60

(1)

Includes approximately 50k of purchased coal.

(2)

Includes approximately 200k of 2011 carryover tonnage at $165.

Oppenheimer 2nd Annual London 1-1 Investor Conference

($ per ton) |

22

$141

$74 -$84

$25 -

$40

$10 -

$15

2011

Adj. EBITDA

Coke

Coal Mining

Corporate

and Other

2012E

Adj. EBITDA

$250 -

$280

$250 -

$280

2012 Adjusted EBITDA

(1)

Outlook

($ in millions)

(1)

For a definition of Adjusted EBITDA, please see the appendix.

(2)

Excluding corporate costs.

•

Middletown

•

Indiana Harbor

improvement

•

Higher prices and

volumes

Oppenheimer 2nd Annual London 1-1 Investor Conference

Estimated

2012

Adjusted

EBITDA

(1)

projected

to

increase

by

$109 to $139 versus 2011;

expect

80%

-

85%

of

2012

Adjusted

EBITDA

(1,

2)

will

be

generated

by

cokemaking

business |

23

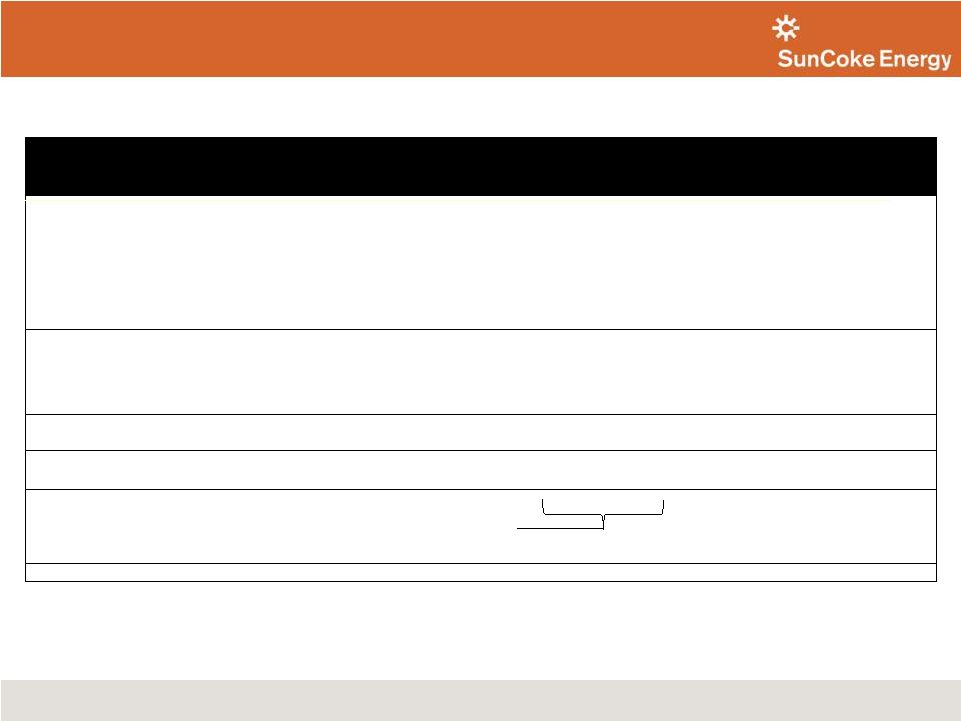

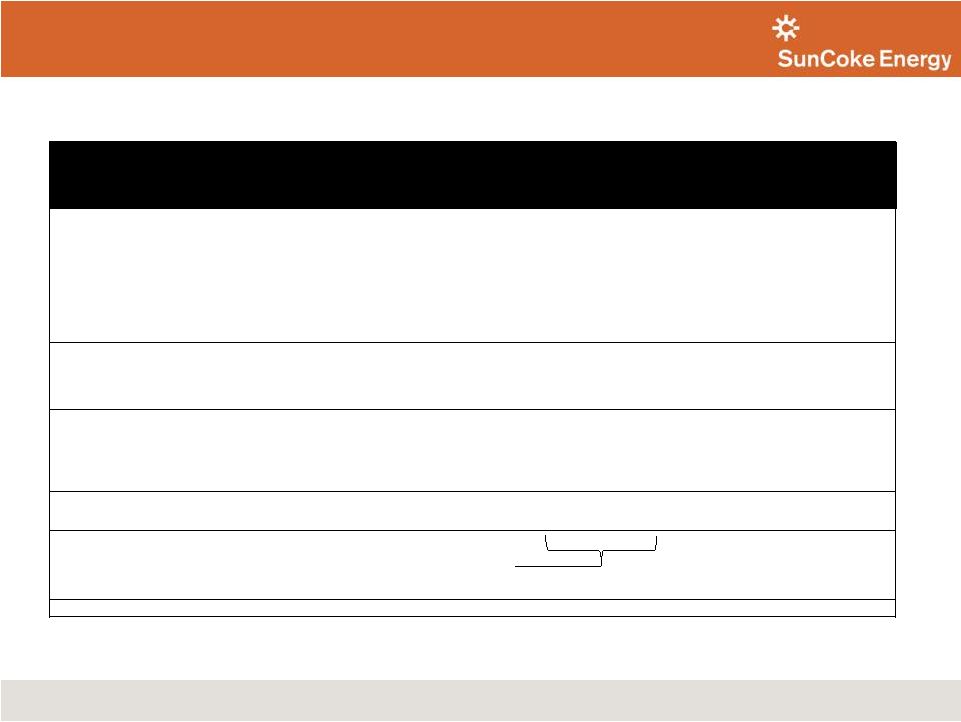

2012 Outlook Summary

Metric

Expected 2012 Outlook

Adjusted EBITDA

(1)

$250 million –

$280 million

Capital Expenditures

& Investments

Approximately $150 million

Free Cash Flow

(2)

$50 million +

Cash Tax Rate

10% –

15%

Effective Tax Rate

20% –

24%

Corporate Costs

$30 million -

$35 million

Coke Production

4.0 -

4.2 million tons

Coal Production

Approximately 1.8 million tons

EPS (at 22% tax rate)

$1.30 -

$1.65

(1) For a definition of Adjusted EBITDA, please see the appendix

(2) For a definition of Free Cash Flow, please see the appendix

Oppenheimer 2nd Annual London 1-1 Investor Conference

|

24

Strategy for Shareholder Value Creation

Oppenheimer 2nd Annual London 1-1 Investor Conference

Operational Excellence

•

Rigorous execution in

existing operations

•

Maintain focus on

safety and environment

•

Deliver returns through

strong, consistent coke

earnings and optimize

coal operations

Grow The Coke Business

•

Domestic

•

Secure permits for

next potential facility

•

Capitalize on aging

domestic capacity,

demand growth and

import displacement

•

International

•

Execute India entry

and pursue follow

on

growth

•

Continue evaluating

China for potential

entry

Potential Structuring

Alternatives

•

Coke MLP

•

Domestic assets well

suited and expected

to qualify

•

Will evaluate in 2012

•

Coal

•

Aggressively manage

the business

•

Optimize value in

near term and

enhance strategic

flexibility

- |

25

Appendix

Oppenheimer 2nd Annual London 1-1 Investor Conference |

26

Adjusted EBITDA

represents earnings before interest, taxes, depreciation, depletion and

amortization (“EBITDA”) adjusted for sales discounts and the

deduction of income attributable to non-controlling interests in our Indiana Harbor cokemaking operations.

EBITDA

reflects

sales

discounts

included

as

a

reduction

in

sales

and

other

operating

revenue.

The

sales

discounts

represent

the

sharing

with

our

customers

of

a

portion

of

nonconventional

fuels

tax

credits,

which

reduce

our

income

tax

expense.

However,

we

believe that our Adjusted EBITDA would be inappropriately penalized if these

discounts were treated as a reduction of EBITDA since they represent sharing

of a tax benefit which is not included in EBITDA. Accordingly, in computing Adjusted EBITDA, we have

added back these sales discounts. Our Adjusted EBITDA also reflects the deduction

of income attributable to noncontrolling interest in our Indiana Harbor

cokemaking operations. EBITDA and Adjusted EBITDA do not represent and should not be considered

alternatives to net income or operating income under United States generally

accepted accounting principles (GAAP) and may not be comparable to other

similarly titled measures of other businesses. Management believes Adjusted EBITDA is an important

measure of the operating performance of the Company’s assets and is indicative

of the Company’s ability to generate cash from operations.

Pro Forma Adjusted EBITDA

represents Adjusted EBITDA adjusted for the ArcelorMittal settlement impact and

coal transfer price impacts. The Jewell Coke and Coal Mining results have

been adjusted to set the internal transfer price to equal the coal component

contract price in Jewell Coke’s coke sales price for coal sales volumes sold

to Jewell Coke under the transfer pricing agreement. Management

believes Pro Forma Adjusted EBITDA provides transparency into the underlying profitability of these respective

segments for the periods presented.

Pro Forma Adjusted EBITDA/Ton

represents Pro Forma Adjusted EBITDA divided by tons sold.

Free Cash Flow

equals cash from operations less cash used in investing activities less cash

distributions to non-controlling interests.

Management

believes

Free

Cash

Flow

information

enhances

an

investor’s

understanding

of

a

business’

ability

to

generate cash. Free Cash Flow does not represent and should not be considered

an alternative to net income or cash flows from operating activities as

determined under GAAP and may not be comparable to other similarly titled measures of other businesses.

Definitions

Oppenheimer 2nd Annual London 1-1 Investor Conference |

27

2012

Low

2012

High

Net Income

$98

$122

Depreciation, Depletion and Amortization

74

72

Total financing costs, net

48

46

Income tax expense (benefit)

25

37

EBITDA

$245

$277

Sales discounts

11

10

Noncontrolling interests

(6)

(7)

Adjusted EBITDA

$250

$280

Estimated EBITDA Reconciliation, $MM

2012E Net Income to Adjusted EBITDA Reconciliation

Oppenheimer 2nd Annual London 1-1 Investor Conference |

28

Estimated Free Cash Flow Reconciliation, $MM

2012E Estimated Free Cash Flow Reconciliation

Oppenheimer 2nd Annual London 1-1 Investor Conference

2012

Cash from (i) operations;

In excess of

204

$

(ii) less investing;

Approx.

(150)

(iii) less payments to minority interest

Approx.

(4)

Free Cash Flow

In excess of

50

$ |

29

EBITDA Reconciliation, $MM

Oppenheimer 2nd Annual London 1-1 Investor Conference

For The Year Ended 2011

Domestic Coke Weighted

Average = $36

Jewell

Coke

Other

Domestic Coke

International

Coke

Coal

Mining

Corporate

and Other

Total

Net Income

$58.9

Add: Depreciation, depletion and amortization

58.4

Subtract: Interest Income (Primarily from Affiliates)

(12.9)

3.5

Subtract: Capitalized interest

(9.8)

Add: Interest expense

20.6

Add (Subtract): Income tax expense

7.2

EBITDA

$57.6

$74.8

$13.7

$24.0

($44.2)

$125.8

–

12.9

–

–

–

12.9

–

1.7

–

–

–

1.7

Adjusted EBITDA

$57.6

$89.4

$13.7

$24.0

($44.2)

$140.5

Add (Subtract): Pro Forma coal transfer price impact

(11.5)

–

–

11.5

–

–

Pro Forma Adjusted EBITDA coal transfer price impacts

$46.1

$89.4

$13.7

$35.4

($44.2)

$140.5

Sales Volumes (thousands of tons)

702

3,068

1,442

1,454

–

Pro Forma Adjusted EBITDA per Ton

$66

$29

$10

$24

Operating Income (Loss)

$52.7

$36.1

$13.5

$11.1

($45.9)

$67.5

Add: Depreciation Expense

$4.9

$38.7

$0.2

$12.9

$1.7

$58.4

EBITDA

$57.6

$74.8

$13.7

$24.0

($44.2)

$125.9

Add: Sales discounts provided to customers due to sharing of nonconventional fuels tax credits Add

(Subtract): Net (Income) loss attributable to noncontrolling interests

Add: Interest cost – Affiliate |

30

EBITDA Reconciliation, $MM

Oppenheimer 2nd Annual London 1-1 Investor Conference

For The Three Months Ended December 31, 2011

Domestic Coke Weighted

Average = $32

Jewell Coke

Other

Domestic Coke

International

Coke

Coal

Mining

Corporate

and Other

Total

Net Income

$7.5

Add: Depreciation, depletion and amortization

16.0

Subtract: Interest Income

(0.1)

-

Subtract: Capitalized interest

(4.5)

Add: Interest expense

11.7

Add: Income tax expense

(2.9)

EBITDA

$11.4

$17.6

$10.2

$1.7

($13.2)

$27.7

-

3.2

-

-

-

3.2

-

0.5

-

-

-

0.5

Adjusted EBITDA

$11.4

$21.3

$10.2

$1.7

($13.2)

$31.4

Add (Subtract): coal transfer price impact

(0.8)

0.8

-

Pro Forma Adjusted EBITDA without coal tranfer price impact

$10.6

$21.3

$10.2

$2.5

($13.2)

$31.4

Sales Volumes (thousands of tons)

166

837

295

363

Pro Forma Adjusted EBITDA per Ton

$64

$25

$34

$7

Operating Income (Loss)

$10.2

$7.0

$10.1

($2.0)

($13.6)

$11.8

Depreciation Expense

1.2

10.6

0.1

3.7

0.4

16.0

EBITDA

$11.4

$17.6

$10.2

$1.7

($13.2)

$27.8

Add: Interest cost - affiliates Add: Sales discounts provided to customers due to sharing of nonconventional fuels tax credits

Add (Subtract): net (income) loss attributable to noncontrolling interests

|

31

EBITDA Reconciliation, $MM

For The Three Months Ended September 30, 2011

Oppenheimer 2nd Annual London 1-1 Investor Conference

Domestic Coke Weighted

Average = $50

Net Income

Add: Depreciation, depletion and amortization

Subtract: Interest Income

Subtract: Capitalized interest

Add: Interest expense

Add: Income tax expense

EBITDA

Adjusted EBITDA

Add (Subtract): coal transfer price impact

Pro Forma Adjusted EBITDA without coal tranfer price impact

Sales Volumes (thousands of tons)

Pro Forma Adjusted EBITDA per Ton

Operating Income (Loss)

Depreciation Expense

EBITDA

Jewell

Coke

Other

Domestic Coke

International

Coke

Coal

Mining

Corporate

and Other

Total

$21.7

14.8

(1.3)

0.3

(4.6)

8.9

5.1

$14.3

$34.3

$1.7

$8.8

($14.3)

$44.8

3.3

3.3

(3.4)

(3.4)

$14.3

$34.3

$1.7

$8.8

($14.3)

$44.8

(0.4)

0.4

-

$13.9

$34.3

$1.7

$9.2

($14.3)

$44.8

191

777

373

371

$73

$44

$5

$25

$13.1

$24.5

$1.7

$5.5

($14.6)

$30.1

1.2

9.8

0.1

3.3

0.3

14.8

$14.3

$34.3

$1.7

$8.8

($14.3)

$44.8

Add: Sales discounts provided to customers due to sharing of nonconventional fuels tax credits

Add (Subtract): net (income) loss attributable to noncontrolling interests Add:

Interest

cost

-

affiliates |

32

EBITDA Reconciliation, $MM

For The Three Months Ended June 30, 2011

Oppenheimer 2nd Annual London 1-1 Investor Conference

Domestic Coke Weighted

Average = $39

Jewell

Coke

Other

Domestic Coke

International

Coke

Coal

Mining

Corporate

and Other

Total

Net Income

$24.0

Add: depreciation, depletion and amortization

14.6

Subtract: interest income (primarily from affiliates)

(5.8)

1.7

Subtract: capitalized interest

(0.4)

Add (Subtract): income tax expense (benefit)

$1.9

EBITDA

$12.9

$23.7

$0.8

$9.1

($10.5)

$36.0

Add: sales discounts provided to customers due to sharing of nonconventional fuels

tax credits

3.2

3.2

(1.6)

(1.6)

Adjusted EBITDA

$12.9

$25.3

$0.8

$9.1

($10.5)

$37.6

Add (Subtract): coal transfer price impact

(2.3)

2.3

-

Pro Forma Adjusted EBITDA without coal transfer impact

$10.6

$25.3

$0.8

$11.5

($10.5)

$37.6

Sales Volumes (thousands of tons)

170

757

412

334

Pro Forma Adjusted EBITDA per Ton

$62

$33

$2

$34

Operating Income (Loss)

$11.6

$14.1

$0.8

$6.0

($10.9)

$21.4

Depreciation Expense

1.3

9.6

0.1

3.2

0.4

14.6

EBITDA

$12.9

$23.7

$0.8

$9.1

($10.5)

$36.0

Add (Subtract): net (income) loss attributable to noncontrolling interests Add:

interest cost - affiliate

|

33

EBITDA Reconciliation, $MM

For The Three Months Ended March 31, 2011

Oppenheimer 2nd Annual London 1-1 Investor Conference

Domestic Coke Weighted

Average = $22

Jewell

Coke

Other

Domestic Coke

International

Coke

Coal

Mining

Corporate

and Other

Total

Net Income

$5.7

Add: depreciation, depletion and amortization

13.0

Subtract: interest income (primarily from affiliates)

(5.7)

1.5

Subtract: capitalized interest

(0.3)

Add (Subtract): income tax expense (benefit)

3.1

EBITDA

$19.1

($0.9)

$1.0

$4.3

($6.2)

$17.3

3.1

3.1

6.2

6.2

Adjusted EBITDA

$19.1

$8.4

$1.0

$4.3

($6.2)

$26.6

Add (Subtract): coal transfer price impact

(8.0)

8.0

-

Pro Forma Adjusted EBITDA without coal transfer price impact

$11.1

$8.4

$1.0

$12.3

($6.2)

$26.6

Sales Volumes (thousands of tons)

175

697

362

386

Pro Forma Adjusted EBITDA per Ton

$63

$12

$3

$32

Operating Income (Loss)

$18.0

($9.5)

$0.9

$1.6

($6.7)

$4.3

Depreciation Expense

1.1

8.6

0.1

2.7

0.5

13.0

EBITDA

$19.1

($0.9)

$1.0

$4.3

($6.2)

$17.3

Add: Sales discounts provided to customers due to sharing of nonconventional fuels tax credits Add

(Subtract): net (income) loss attributable to noncontrolling interests

Add: interest cost - affiliate |

34

EBITDA Reconciliation, $MM

For The Year Ended 2010

Oppenheimer 2nd Annual London 1-1 Investor Conference

Domestic Coke Weighted

Average = $46

Jewell

Coke

Other

Domestic Coke

International

Coke

Coal

Mining

Corporate

and Other

Total

Net Income

$146.3

Add: Depreciation, depletion and amortization

$48.2

Subtract: Interest Income (Primarily from Affiliates)

($23.7)

$5.4

Subtract: Capitalized interest

($0.7)

Add (Subtract): Income tax expense

$46.9

EBITDA

$151.5

$73.6

$15.0

($3.6)

($14.1)

$222.4

Add: Sales discounts provided to customers due to sharing of nonconventional fuels tax

credits –

12.0

–

–

–

12.0

–

(7.1)

–

–

–

(7.1)

Adjusted EBITDA

$151.5

$78.5

$15.0

($3.6)

($14.1)

$227.3

Add (Subtract): Pro Forma impact of ArcelorMittal settlement

(69.0)

18.0

–

–

–

(51.0)

Add: Legal and Settlement charges related to ArcelorMittal Settlement and Indiana Harbor

Arbitration 3.6

12.7

–

–

–

16.3

Add (Subtract): Pro Forma coal transfer price impact

(27.6)

–

–

27.6

–

–

Pro Forma Adjusted EBITDA without ArcelorMittal settlement and coal transfer price impacts

$58.5

$109.2

$15.0

$24.0

($14.1)

$192.6

Sales Volumes (thousands of tons)

721

2,917

–

1,277

–

Pro Forma Adjusted EBITDA per Ton

$81

$37

$19

Operating Income (Loss)

$147.1

$38.6

$14.9

($11.3)

($15.1)

$174.2

Add: Depreciation Expense

4.4

35.0

0.1

7.7

1.0

48.2

EBITDA

$151.5

$73.6

$15.0

($3.6)

($14.1)

$222.4

Add (Subtract): Net (Income) loss attributable to noncontrolling interests Add:

interest cost - Affiliate |

35

EBITDA Reconciliation, $MM

For The Three Months Ended December 31, 2010

Oppenheimer 2nd Annual London 1-1 Investor Conference

Domestic Coke Weighted

Average = $46

Jewell

Coke

Other Domestic

Coke

International

Coke

Coal

Mining

Corporate and

Other

Total

Net Income

$15.1

Add: Depreciation, depletion and amortization

12.3

Subtract: Interest Income

(5.7)

1.0

Subtract: Capitalized interest

(0.3)

Add: Interest expense

-

Add: Income tax expense

5.7

EBITDA

$19.6

$6.6

$13.8

($7.8)

($4.1)

$28.1

Add: Sales discounts provided to customers due to sharing of nonconventional fuels tax

credits 3.2

3.2

3.4

3.4

Adjusted EBITDA

19.6

13.2

13.8

(7.8)

(4.1)

34.7

Add (Subtract): pro forma impact of ArcelorMittal settlement

(11.0)

4.9

(6.1)

Add: Legal and Settlement charges related to ArcelorMittal Settlement and Indiana Harbor

Arbitration 3.6

12.7

16.3

Add (Subtract): coal transfer price impact

(1.0)

1.0

-

Pro Forma Adjusted EBITDA without ArcelorMittal settlement and coal tranfer price impact

$11.2

$30.8

$13.8

($6.8)

($4.1)

$44.9

Sales Volumes (thousands of tons)

162

750

321

Pro Forma Adjusted EBITDA per Ton

$69

$41

($21)

Operating Income (Loss)

$18.5

($2.1)

$13.8

($9.8)

($4.6)

$15.8

Depreciation Expense

1.1

8.7

-

2.0

0.5

12.3

EBITDA

$19.6

$6.6

$13.8

($7.8)

($4.1)

$28.1

Add: (Subtract): net (income) loss attributable to noncontrolling interests

Add: interest cost - affiliates |

36

Media releases and SEC filings are available

on our website at www.suncoke.com

Contact Investor Relations for more information: 630-824-1907

Oppenheimer 2nd Annual London 1-1 Investor Conference |