Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - American Water Works Company, Inc. | d284065d8k.htm |

| EX-99.1 - PRESS RELEASE - American Water Works Company, Inc. | d284065dex991.htm |

2012

Earnings Guidance January 18, 2012

Exhibit 99.2 |

January 2012

2

Certain statements in this presentation are forward-looking statements within the

meaning of the safe harbor provisions of the Private Securities Litigation

Reform Act of 1995. These forward-looking statements are predictions based on our current

expectations and assumptions regarding future events and may relate to, among

other things, our future financial performance, including return on

equity performance, our growth and portfolio optimization strategies, our projected capital

expenditures and related funding requirements, our ability to repay debt, our ability

to finance current operations and growth initiatives,

the

impact

of

legal

proceedings

and

potential

fines

and

penalties,

business

process

and

technology

improvement

i

nitiatives, trends in our industry, regulatory or legal developments or rate

adjustments. Actual results could differ materially because of factors such as

decisions of governmental and regulatory bodies, including decisions to raise or lower rates; the

timeliness

of

regulatory

commissions’

actions

concerning

rates;

changes

in

laws,

governmental

regulations

and

policies,

including

environmental,

health

and

water

quality

and

public

utility

regulations

and

policies;

weather

conditions,

patterns

or

events, including drought or abnormally high rainfall; changes in customer demand

for, and patterns of use of, water, such as may

result

from

conservation

efforts;

significant

changes

to

our

business

processes

and

corresponding

technology;

our

ability to appropriately maintain current infrastructure; our ability to obtain

permits and other approvals for projects; changes in our capital requirements;

our ability to control operating expenses and to achieve efficiencies in our operations; our ability

to obtain adequate and cost-effective supplies of chemicals, electricity, fuel,

water and other raw materials that are needed for our operations; our ability

to successfully acquire and integrate water and wastewater systems that are complementary to our

operations and the growth of our business or dispose of assets or lines of business

that are not complementary to our operations and the growth of our business;

cost overruns relating to improvements or the expansion of our operations;

changes in general economic, business and financial market conditions; access to

sufficient capital on satisfactory terms; fluctuations in interest rates;

restrictive covenants in or changes to the credit ratings on our current or future debt that could

increase our financing costs or affect our ability to borrow, make payments on debt

or pay dividends; fluctuations in the value of benefit plan assets and

liabilities that could increase our cost and funding requirements; our ability to utilize our U.S. and

state net operating loss carryforwards; migration of customers into or out of our

service territories; difficulty in obtaining insurance at acceptable rates and

on acceptable terms and conditions; the incurrence of impairment charges ability to retain

and attract qualified employees; and civil disturbance, or terrorist threats or acts

or public apprehension about future disturbances or terrorist threats or

acts. Any forward-looking statements we make, speak only as of the date of

this presentation. Except as required by law, we specifically disclaim any

undertaking or intention to publicly update or revise any forward-looking statements, whether as a

result

of

new

information,

future

events,

changed

circumstances

or

otherwise.

Cautionary Statement Concerning Forward-Looking

Statements |

2011

- What happened

3

January 2012

•Portfolio Optimization

•Divested TX, AWM

•Acquired MO

•Executed Agreements AZ, NM, OH and NY

•Net Utility Plant

•

Invested approximately $900 Million

•Market-Based Operations

•Homeowner Service Contracts reach 880,000

•Improving ROE

•2010 ended at 6.4%

•2011 estimate: 7.2% -

7.4%

•Total Shareholder Returns

•30% at 12/31/2011

•Cash Dividends Increased 5%

•Yield 2.89% at 12/31/11

•Rate Cases Effective in 8 states in 2011

•$158.3 Million

•

Infrastructure Charges awarded of $10.7 Million

•Rate Cases Filed in 10 states

•Decisions Pending in 8 states

•Address Regulatory Lag

•

Declining Usage

•Infrastructure Charges (New Jersey, Illinois)

•O&M Efficiency Ratio improvement

•

Expense Management

•Rate Case Effectiveness

•Business Transformation

•On schedule for 2014 completion

Operating

Efficiency

Regulatory

Environment

Growth

Shareholder

Value |

January 2012

4

2012 Range: Solid Growth Powers Earnings Range

from Ongoing Operations of $1.90 -

$2.00

Key Drivers

•

Annual infrastructure

investment of approximately

$900 million

•

Continued improvement in

operating efficiency ratio

toward 5-year goal of 40%

•

Completion of current portfolio

optimization transactions

•

Continued low interest rate

environment

•

Completion of outstanding

rate cases

•

Continued dividend focus

•

No equity offering

2012 Range

$1.90 -

$2.00

•

2011 Range excludes the impact from discontinued operations and the

one-time contribution of appreciated land to a county authority in

Lexington, Kentucky |

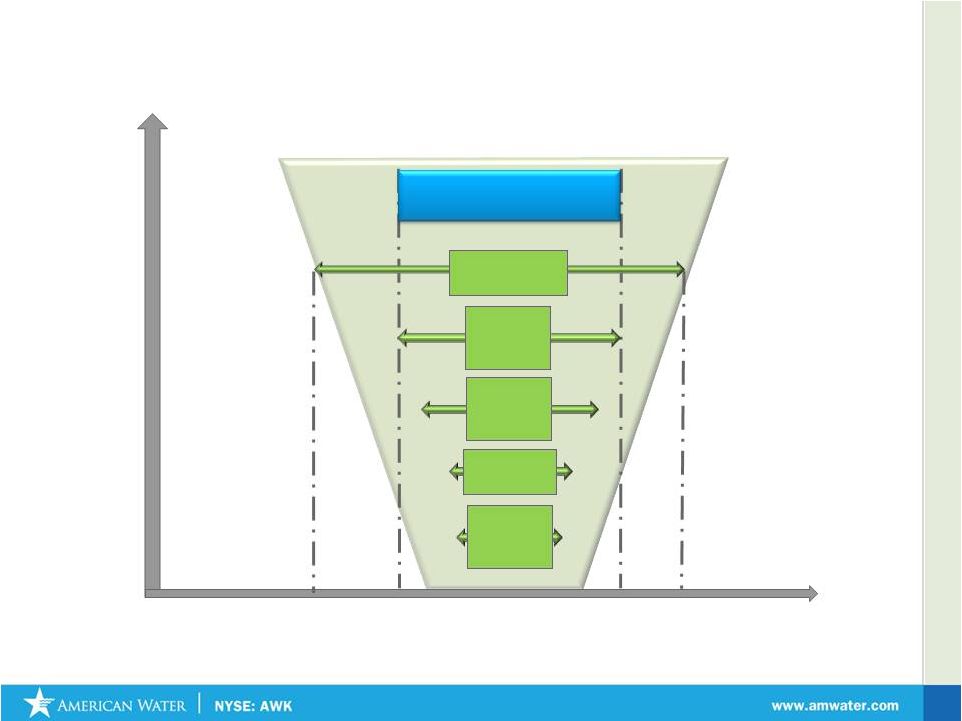

5

* Not to scale

2012 Earnings Per Share Range: Key Factors

Influencing Earnings Range

Interest

Rates

(+/-

1%)

2012 EPS Range

$1.90 -

$2.00

Consumption

(+/-1%)

Fuel &

Power

(+/-

10%)

Chemicals

(+/-

10%)

O&M

Expense

(+/-

1%)

$2.03

$1.87

$1.90

$2.00

January 2012 |

January 2012

6

AWK 2011 Accomplishments

2012 Expectations

Continue Portfolio Optimization Initiative

Finalize transactions in NM, AZ, NY and Ohio

Identify additional valued-added opportunities

Actively Address Regulatory Lag that Impacts

Returns on Investments

Expect to file 4 general rate cases in 2012

Infrastructure Surcharges filings in 4-6 states

Address usage trends via rate case or other filings

Continue Operating Efficiency Improvement

Five-year goal below 40%

Efficient use of our Capital

Invest approximately $900 million to upgrade

infrastructure

Enhance DSIC like mechanisms

Optimize Supply Chain

Increase Earned Regulated Return

Expand

Market

Based

businesses

-

focusing

on

Homeowner Services & Military Contract

Operations

Optimize Municipal Contract Operations Business

Model

Execution of Portfolio Optimization Initiative

Closed MO acquisition, TX sale and sale of

Applied Water Management (AWM)

Filed for regulatory approvals for transactions

in NM, AZ, NY and Ohio

Resolved Rate Cases worth $296.5 MM of

filed Annualized Revenues

Rate cases effective in 8 states generating

approximately $158.3 million in annualized

revenue increases and $10.7 million in

infrastructure surcharges, assuming normal

usage patterns.

Filed 10 rate proceedings in 2011 requesting

$282.9 million in annualized revenue

Initiated state specific efforts to address

declining usage in all rate cases filed in 2011

Continued Operating Efficiency improvement

Continued improvement in Return on Equity

What We Accomplished in 2011

In 2012 You Can Expect Us To |

January 2012

American Water: Providing Value to Investors

•

The Adjusted 2011 EPS Range, a non-GAAP measure, does not recognize an

approximate 9 cent benefit to earnings per share from the cessation of

depreciation for discontinued operations in Arizona, New Mexico,

Texas and Ohio.

•

CAGR percentages calculated to midpoint of 2012 estimates

•

2008 and 2009 EPS and ROE exclude impairment charges

Earnings Per Share

7

Mid-

range

Return of Equity

8.00%

6.00%

4.00%

2.00%

0.00%

4.12%

4.99%

6.49%

7.2%

7.4%

7.5%

7.9%

2008

2009

2010

2011

Landing

Zone

2012E |

8

January 2012 |

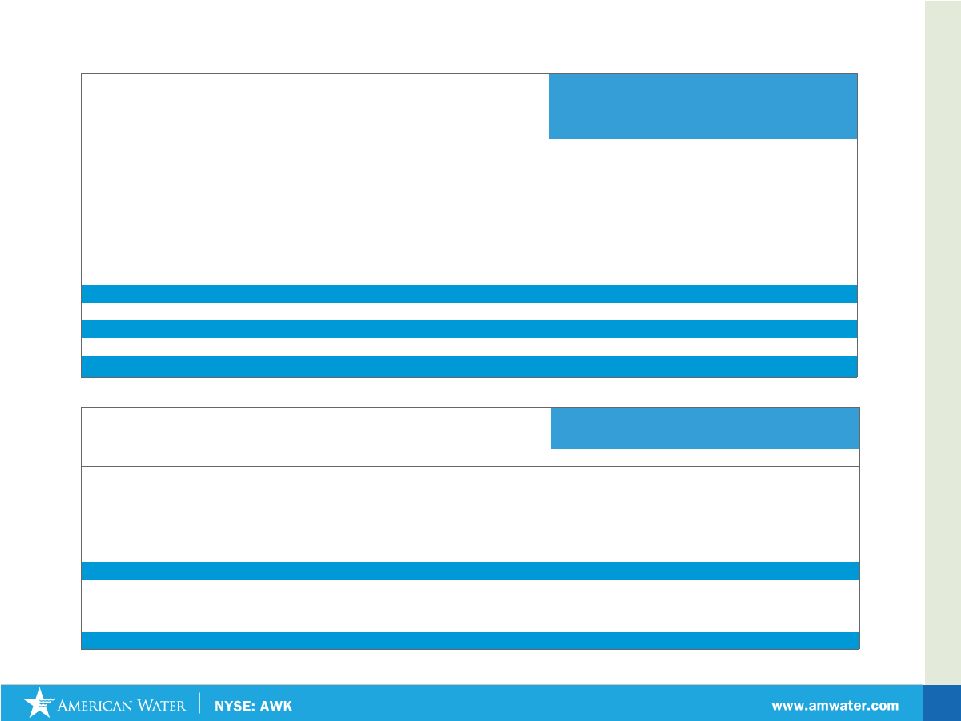

January 2012

Return on Equity Excluding Impairment Charge (A Non-GAAP Unaudited Number)

Historical

($ in thousands )

2008

2009

2010

Net income (Loss) from Continuing Operations

($562,421)

($233,083)

$267,827

Adjustments

Impairment charges

738,475

443,024

0

Adjusted net income excluding impairment charge

$176,054

$209,941

$267,827

Year end stockholders’

equity

$4,102,001

$4,000,859

$4,127,725

Add impairment charge, net of tax

738,475

443,024

0

Adjusted stockholders’

equity excluding impairment charge, net of tax

$4278,055

$4,210,800

$4,127,725

ROE Percentage

4.12%

4.99%

6.49%

9

Net Income (Loss) –

Earnings per Share Excluding Impairment Charge

(A Non-GAAP Unaudited Number)

Historical

($ in thousands, except per share data)

2008

2009

2010

Net income, (Loss)

($562,421)

($233,083)

$267,827

Add: Impairment

750,000

450,000

0

Net income excluding impairment charge before associated tax benefit

187,579

216,917

267,827

Less: Income tax benefit relating to impairment charge

11,525

6,976

0

Adjusted net income excluding impairment charge

$176,054

$209,941

$267,827

Basic earnings per common share excluding impairment charge:

Adjusted net income excluding impairment charge

$1.10

$1.25

$1.53

Diluted earnings per common share excluding impairment charge:

Adjusted net income excluding impairment charge

$1.10

$1.25

$1.53

Reconciliation Tables |