Attached files

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 (FEE REQUIRED)

For the fiscal year ended September 30, 2011

o TRANSACTION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 (NO FEE REQUIRED)

For the transaction period from ________ to ________

Commission File number 0-25541

VISUALANT, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

|

91-1948357

|

|

(State or other jurisdiction of incorporation

|

(I.R.S. Employer

|

|

or organization)

|

Identification No.)

|

|

500 Union Street, Suite 406

|

|

|

Seattle, Washington

|

98101

|

|

(Address of principal executive offices)

|

(Zip Code)

|

|

Issuer's telephone number, including area code

|

206-903-1351

|

|

Securities registered pursuant to Section 12 (b) of the Exchange Act:

|

|

|

Common

|

OTCBB

|

|

(Title of each class)

|

(Name of each exchange on which registered)

|

|

Securities registered pursuant to Section 12 (g) of the Exchange Act:

|

|

|

None

|

|

|

(Title of Class)

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o Yes ý No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. o Yes ý No

1

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ý Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ý Yes o No

Indicate by check mark if disclosure of delinquent filers in response to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer

|

o

|

Accelerated filer

|

o

|

Non-accelerated filer

|

o

|

Smaller reporting company

|

ý

|

|

(Do not check if a smaller reporting company)

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes ý No

As of March 31, 2011 (the last business day of our most recently completed second fiscal quarter), based upon the last reported trade on that date, the aggregate market value of the voting and non-voting common equity held by non-affiliates (for this purpose, all outstanding and issued common stock minus stock held by the officers, directors and known holders of 10% or more of the Company’s common stock) was $20,838,190.

As of November 29, 2011, the Company had 53,450,657 shares of common stock issued.

2

|

TABLE OF CONTENTS

|

|

Page

|

||

|

PART 1

|

||

|

ITEM 1.

|

Description of Business

|

4 |

|

ITEM 1A.

|

Risk Factors

|

7 |

|

ITEM 1B

|

Unresolved Staff Comments

|

11 |

|

ITEM 2.

|

Properties

|

11 |

|

ITEM 3.

|

Legal Proceedings

|

11 |

|

ITEM 4.

|

Submission of Matters to Vote of Securities Holders

|

11 |

|

PART II

|

||

|

ITEM 5.

|

Market for Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

13 |

|

ITEM 6.

|

Selected Financial Data

|

14 |

|

ITEM 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

14 |

|

ITEM 7A.

|

Quantitative and Qualitative Disclosures About Market Risk

|

18 |

|

ITEM 8.

|

Financial Statements and Supplementary Data

|

18 |

|

ITEM 9.

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

18 |

|

ITEM 9A.

|

Controls and Procedures

|

18 |

|

ITEM 9B.

|

Other Information

|

19 |

|

PART III

|

||

|

ITEM 10.

|

Directors, Executive Officers and Corporate Governance

|

18 |

|

ITEM 11.

|

Executive Compensation

|

21 |

|

ITEM 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

21 |

|

ITEM 13.

|

Certain Relationships and Related Transactions, and Director Independence

|

21 |

|

ITEM 14.

|

Principal Accounting Fees and Services

|

21 |

|

PART IV

|

||

|

ITEM 15.

|

Exhibits, Financial Statement Schedules

|

21 |

|

SIGNATURES

|

27 |

3

PART I

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS

The following discussion, in addition to the other information contained in this report, should be considered carefully in evaluating us and our prospects. This report (including without limitation the following factors that may affect operating results) contains forward-looking statements (within the meaning of Section 27A of the Securities Act of 1933, as amended ("Securities Act") and Section 21E of the Securities Exchange Act of 1934, as amended ("Exchange Act") regarding us and our business, financial condition, results of operations and prospects. Words such as "expects," "anticipates," "intends," "plans," "believes," "seeks," "estimates" and similar expressions or variations of such words are intended to

identify forward-looking statements, but are not the exclusive means of identifying forward-looking statements in this report. Additionally, statements concerning future matters such as revenue projections, projected profitability, growth strategies, development of new products, enhancements or technologies, possible changes in legislation and other statements regarding matters that are not historical are forward-looking statements.

Forward-looking statements in this report reflect the good faith judgment of our management and the statements are based on facts and factors as we currently know them. Forward-looking statements are subject to risks and uncertainties and actual results and outcomes may differ materially from the results and outcomes discussed in the forward-looking statements. Factors that could cause or contribute to such differences in results and outcomes include, but are not limited to, those discussed below and in "Management's Discussion and Analysis of Financial Condition and Results of Operations" as well as those discussed elsewhere in this report. Readers are urged not to place undue reliance on these forward-looking

statements which speak only as of the date of this report. We undertake no obligation to revise or update any forward-looking statements in order to reflect any event or circumstance that may arise after the date of this report.

ITEM 1. DESCRIPTION OF BUSINESS

THE COMPANY AND OUR BUSINESS

Visualant, Inc. (the “Company” or “Visualant”) was incorporated under the laws of the State of Nevada on October 8, 1998 with authorized common stock of 200,000,000 shares at $0.001 par value. On September 13, 2002, 50,000,000 shares of preferred stock with a par value of $0.001 were authorized by the shareholders. There are no preferred shares issued and the terms have not been determined. Our executive offices are located in Seattle, Washington.

We develop low-cost, high speed, light-based security and quality control solutions for use in homeland security, anti-counterfeiting, forgery/fraud prevention, brand protection ,process control applications, and diagnostics. Our patented and patent-pending technology uses controlled illumination with specific bands of light, to establish a unique spectral signature for both individual and classes of items. When matched against existing databases, these spectral signatures allow precise identification and authentication or diagnostics of any item or substance. This breakthrough optical sensing and data capture technology is called Spectral Pattern Matching (SPM). SPM technology lends itself to

flexible form factors and can be miniaturized, and is easily integrated into a variety of hand-held or fixed mount configurations, and can be a stand-alone device or combined in the same package as a bar-code or biometric scanner.

On September 6, 2011, the Company announced that it was issued US Patent No. 7,996,173, entitled “Method, Apparatus and Article to Facilitate Distributed Evaluation of Objects Using Electromagnetic Energy,” by the United States Office of Patents and Trademarks. Other patent applications remain pending.

Through our wholly owned subsidiary, TransTech Systems, Inc. based in Aurora, Oregon, we provide value added security and authentication solutions to corporate and government security and law enforcement markets throughout the United States.

We closed the acquisition of TransTech of Aurora, OR on June 8, 2010 and recorded the financial results of the acquisition from June 8, 2010 to September 30, 2011 in our most recent financial statements.

TransTech, founded in 1994, is a distributor of access control and authentication systems serving the security and law enforcement markets. With recorded revenues of $10 million in 2009, TransTech has a respected national reputation for outstanding product knowledge, sales and service excellence.

This acquisition is expected to accelerate market entry and penetration through the acquisition of well-operated and positioned distributors of security and authentication systems like TransTech, thus creating a natural distribution channel for products featuring our proprietary SPM technology.

Our strategy for the next 18 to 24 months is to generate substantially increased revenues through the further acquisition of other high quality companies complementary to TransTech, growth of TransTech and the sale and license of SPM products through the TransTech channel of distribution and its strategic relationships.

4

LICENSE AGREEMENT WITH JAVELIN LLC (“Javelin”)

On January 3, 2011, we signed a Commercial License Agreement (“License Agreement”) with Seattle based Javelin for development of environmental diagnostic applications of our SPM technology.

The License Agreement, which is exclusive for environmental applications, is perpetual and lasts until the Visualant IP expires. It provides for payments of 5% of Javelin’s revenues, a royalty of $15,000 in year one (which was prepaid) and increasing to $47,407 in year five and profit sharing of 25% of license or transfer of technology. Javelin has certain performance milestones by year 2 and 3. The License Agreement can be terminated by Visualant for failure of Javelin to meet the performance milestones and by Javelin with thirty days' notice.

PROPOSED ACQUISITION OF EAGLE TECHNOLOGIES USA (“Eagle”)

On June 27, 2011, we announced that we signed a new Letter of Intent to Eagle Technologies USA (“Eagle”) (www.eagletechnologiesusa.com) of Brea, California.

On September 15, 2011, the Company announced that it had signed an amendment to the Letter of Intent, extending the closing date to December 31, 2011.

Eagle, founded by card industry leaders Greg and Ryan Hawkins and Jeff Fulmer in 2008, has rapidly emerged as a premier provider of blank PVC and polyester composite cards to the identification market. If this acquisition is completed as anticipated, it is hoped that Eagle will provide an immediate additional $1 million in annual revenue to Visualant and is projected to grow to $3 to $4 million in revenues over the next two years as Eagle increases the range and technical sophistication of its product line.

If this acquisition is completed, we will continue with its strategic initiative to consolidate relevant security and authentication assets. At the same time, we will provide Eagle and its management the human and capital resources necessary to rapidly accelerate its growth. Upon the closing of this acquisition, the Eagle team will continue to manage Eagle with full profit and loss responsibility.

CORPORATE INFORMATION

We were incorporated in Nevada on October 8, 1998. Our executive offices are located at 500 Union Street, Suite 406, Seattle, WA 98101. Our telephone number is (206) 903-1351 and its principal website address is located at www.visualant.net. The information on our website is not incorporated as a part of this Form 10-K.

THE COMPANY’S COMMON STOCK

Our common stock trades on the OTCBB Exchange under the symbol “VSUL.OB.”

INDUSTRY OVERVIEW

Visualant’s SPM technology resides in the general marketplace for spectroscopy (measurement of light according to its spectrum) and spectrometry (the measurement of the chemical or atomic components as a function of light reflected or absorbed by them). These analytic tools are typically fragile and expensive often costing tens or hundreds of thousands of dollars. The Visualant SPM technology is flexible, sturdy and has a very low cost.

The Visualant SPM technology can be used to create low cost, ubiquitous analytic devices that can be used in numerous applications in the broad security and authentication market. There is no room for error in security and authentication, hence the industry requires layers of redundancies in order to provide hoped for failsafe security. The security and authentication industry uses numerous tools in its pursuit of security. These include RFID chips and holograms for access control cards, threads and holograms in currency, and other means of marking to thwart counterfeiting. Visualant SPM technology provides a level of redundancy without the addition of any specific

marking. The SPM technology simply sees the colors present and determines the accuracy of those colors against the prescribed standard. In this case, Visualant SPM technology exists in the broad industry of component manufacturers providing solutions for security and authentication.

TransTech, our wholly-owned subsidiary, is a security and authentication distribution company selling products to over 300 dealers in the United States. TransTech’s products include a variety of security and authentication products including printers, access control devices and numerous components. Distribution is fragmented in the security and authentication marketplace. There are large companies, including Scan Source Security, Wynit, Inc. and Plasco ID, who increasingly sell directly to customers via the Internet and smaller regional and national distributors who sell to these same customers and provide value added services and support. Often called value

added resellers or VARs, distributors such as TransTech work hard to maintain their customers through service and support.

5

DEVELOPMENT OF SPM TECHNOLOGY

After years of development, on September 6, 2011, we announced that we were issued US Patent No. 7,996,173, entitled “Method, Apparatus and Article to Facilitate Distributed Evaluation of Objects Using Electromagnetic Energy,” by the United States Office of Patents and Trademarks. This is our first patent covering our SPM technology. We are pursuing an aggressive patent strategy to expand our unique intellectual property. As of November 29, 2011, we had four family patent applications filed with the U.S. Patent Office and one patent pending in Japan.

KEY MARKET PRIORITIES

Currently, our key market priorities are, among other things, as follows to:

|

•

|

Commercialize the Visualant SPM technology and close sales in the United States and Japan.

|

|

•

|

Implement synergies between TransTech acquisition and the Company.

|

|

•

|

Develop license and royalty producing opportunities for the SPM technology outside the core security and authentication marketplace to include medical, agricultural and environmental diagnostics.

|

|

|

•

|

Close the acquisition of Eagle.

|

|

|

•

|

Pursue additional acquisitions which extend the product range and geographic reach of TransTech.

|

|

|

•

|

Develop our patent portfolio by continually extending the reach and application of our intellectual property.

|

|

|

•

|

Pursue grants from governmental and private sources to fund the exploration of new and unique applications of the SPM technology.

|

|

|

•

|

Improve profitability of the Company by increasing sales and managing expenses.

|

|

|

•

|

Enhance our investor relations activities.

|

|

•

|

Acquire growth businesses at discounted prices in our target sectors and markets in conjunction with business partners. We expect to focus on growth opportunities with distressed businesses that require improvements in management, financial processes and liquidity to be successful.

|

PRIMARY RISKS AND UNCERTAINTIES

We are exposed to various risks related to our need for additional financing, the sale of significant numbers of our shares, a volatile market price for our common stock and our merger and acquisition activities. These risks and uncertainties are discussed in more detail below in Part I, Item 1A.

DISTRIBUTION METHODS

Distribution is fragmented in the security and authentication marketplace. There are large companies who increasingly sell directly to customers via the Internet and smaller regional and national distributors who sell to these same customers and provide value added services and support. Often called value added resellers or VARs, distributors such as TransTech work hard to maintain their customer relationships through the provision of outstanding service and support.

The Visualant SPM technology, as focused upon the security and authentication marketplace will provide TransTech with higher margin proprietary products. Visualant will be able to leverage its built-in channel of distribution at TransTech and obtain speed to market advantage. At the same time, where appropriate, Visualant will utilize broad global channels of distribution for its SPM technology. The Company also expects to enter into joint ventures with co-development partners who may have their own channels of distribution.

COMPETITION

We are not aware of any direct competitors using technology with capabilities of the Visualant SPM technology in the security and authentication marketplace. There are several indirect competitors in the form of other methods for determining the authenticity of products and people. These competitive products include the use of RFID chips, holograms, iris scans, fingerprints and other means of determining whether a person or product is authentic. Many companies compete in the security and authentication marketplace with various solutions many of which perform with excellence. We believe that we can provide an accurate, cost effective component which will add value to

customers looking for additional inexpensive redundancies to solve their security and authentication problems.

As discussed above under “Distribution Methods,” TransTech does face direct competition from both OEMs selling directly to end users/customers and from other distributors of both the same products as TransTech distributes and competing products.

6

GEOGRAPHICAL MARKETS

We primarily operate in the U.S. and Japan. The Company is seeking acquisitions in other markets in order to expand its reach to the global marketplace.

EMPLOYEES

As of September 30, 2011 we had thirteen full-time, three part-time employees and four contractors. Most employees were based in Oregon. The Chief Executive Officer and Chief Financial Officer are based out of the Seattle, Washington office.

WEBSITE ACCESS TO UNITED STATES SECURITIES AND EXCHANGE COMMISSION REPORTS

We file annual and quarterly reports, proxy statements and other information with the Securities and Exchange Commission ("SEC"). You may read and copy any document we file at the SEC's Public Reference Room at 100 F Street, N.E., Washington D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the public reference room. The SEC maintains a website at http://www.sec.gov that contains reports, proxy and information statements and other information concerning filers. We also maintain a web site at http://www.visualant.net that provides additional information about our Company and links to documents we file with the SEC. The Company's charters for the Audit Committee, the Compensation

Committee, and the Nominating Committee; and the Code of Conduct & Ethics are also available on our website. The information on our website is not part of this Form 10-K.

ITEM 1A. RISK FACTORS

WE WILL NEED ADDITIONAL FINANCING TO SUPPORT OUR TECHNOLOGY DEVELOPMENT, ACQUIRING OR INVESTING IN NEW BUSINESSES AND ONGOING OPERATIONS.

We had cash of $92,000, a net working capital deficit of approximately $3.2 million and total indebtedness of $2.6 million as of September 30, 2011.

We will need to obtain additional financing to implement the business plan, service our debt repayments and acquire new businesses. There can be no assurance that we will be able to secure funding, or that if such funding is available, the terms or conditions would be acceptable to us. If the Company is unable to obtain additional financing, we may need to restructure our operations, divest all or a portion of our business or file for bankruptcy.

Our recent efforts to generate additional liquidity, including through sales of our common stock, are described in more detail in the financial statement notes set forth in this prospectus.

If we raise additional capital through borrowing or other debt financing, we will incur substantial interest expense. Sales of additional equity securities will dilute on a pro rata basis the percentage ownership of all holders of common stock. When we raise more equity capital in the future, it will result in substantial dilution to our current stockholders.

THE SALE OF A SIGNIFICANT NUMBER OF OUR SHARES OF COMMON STOCK COULD DEPRESS THE PRICE OF OUR COMMON STOCK.

Sales or issuances of a large number of shares of common stock in the public market (including pursuant to the equity line of credit transaction that we entered into with Ascendiant Capital Partners, LLC) or the perception that sales may occur could cause the market price of our common stock to decline. As of November 29, 2011, there were 53.5 million shares of common stock issued and outstanding. The Company recently registered 15,340,361 of shares of common stock for resale, including up to 11,977,714 shares of common stock that may be issued pursuant to warrants or other convertible securities. Since the effective date of the registration statement and as of November 29, 2011, 2,930,777 of the 11,977,714

shares of common stock have been issued pursuant to the convertible securities. Therefore, the amount of shares registered for resale constitutes a significant percentage of the issued and outstanding shares and the sale of all or a portion of these shares could have a negative effect on the market price of our common stock. Significant shares of common stock are held by our principal shareholders, other Company insiders and other large shareholders. As “affiliates” (as defined under Rule 144 of the Securities Act (“Rule 144”)) of the Company, our principal shareholders, other Company insiders and other large shareholders may only sell their shares of common stock in the public market pursuant to an effective registration statement or in compliance with Rule 144.

Some of the present shareholders have acquired shares at prices as low as $0.001 per share, whereas other shareholders have purchased their shares at prices ranging from $0.07 to $0.75 per share.

7

FUTURE ISSUANCE OF COMMON STOCK RELATED TO CONVERTIBLE NOTES PAYABLE MAY HAVE A DILUTING FACTOR ON EXISTING AND FUTURE SHAREHOLDERS.

On May 19, 2011, we entered into a Securities Purchase Agreement (“Agreement”) with Gemini Master Fund, Ltd. and Ascendiant Capital Partners, LLC (“Investors”) pursuant to which the Company issued $1.2 million in principal amount of 10% convertible debentures due May 1, 2012, together with 5-year warrants to purchase 2,400,000 shares of the Company’s common stock. The purchase price for the debentures was 83.3% of the face amount, resulting in the Company receiving $1.0 million, less legal fees, placement agent fees and expenses as set forth below.

We filed a registration statement on Form S-1, which was declared effective on August 29, 2011, to register 15,340,361 of our common stock, including (i) up to 3,600,000 shares of our common stock for Gemini issuable on conversion and 1,800,000 shares of our common stock issuable upon exercise of a warrant issued to Gemini and (ii) up to 1,200,000 shares of our common stock for Ascendiant issuable on conversion and 792,000 shares of our common stock issuable upon exercise of a warrant issued to Ascendiant. Since the effective date of the registration statement, 2,930,777 shares of our common stock have been issued thus far to Gemini on conversion of a portion of the convertible

debentures.

The conversion of the convertible notes payable and the related warrants will likely require us to file an additional registration statement and will likely result in a dilution of the value of the our common shares for all shareholders. Dilution of the value of the common shares will likely result from such sales, which in turn could adversely affect the market price of our common stock.

RISKS ASSOCIATED WITH EQUITY LINE OF CREDIT WITH ASCENDIANT

The Securities Purchase Agreement with Ascendiant will terminate if our common stock is not listed on one of several specified trading markets (which include the OTCBB and Pink Sheets, among others), if we file protection from its creditors or if a Registration Statement on Form S-1 or S-3 is not effective.

If the price or the trading volume of our common stock does not reach certain levels, we will be unable to draw down all or substantially all of our $3,000,000 equity line of credit with Ascendiant.

The maximum draw down amount every 8 trading days under our equity line of credit facility is the lesser of $100,000 or 20% of the total trading volume of our common stock for the 10-trading-day period prior to the draw down multiplied by the volume-weighted average price of our common stock for such period. If our stock price and trading volume decline from at current levels, we will not be able to draw down all $3,000,000 available under the equity line of credit.

If we not able to draw down all $3,000,000 available under the equity line of credit or if the Securities Purchase Agreement is terminated, we may need to restructure our operations, divest all or a portion of our business or file for bankruptcy.

WE MAY ENGAGE IN ACQUISITIONS, MERGERS, STRATEGIC ALLIANCES, JOINT VENTURES AND DIVESTITURES THAT COULD RESULT IN FINANCIAL RESULTS THAT ARE DIFFERENT THAN EXPECTED.

In the normal course of business, we engage in discussions relating to possible acquisitions, equity investments, mergers, strategic alliances, joint ventures and divestitures. Such transactions are accompanied by a number of risks, including:

- Use of significant amounts of cash,

- Potentially dilutive issuances of equity securities on potentially unfavorable terms,

8

- Incurrence of debt on potentially unfavorable terms as well as impairment expenses related to goodwill and amortization expenses related to other intangible assets, and

- The possibility that we may pay too much cash or issue too many of our shares as the purchase price for an acquisition relative to the economic benefits that we ultimately derive from such acquisition.

- The process of integrating any acquisition may create unforeseen operating difficulties and expenditures. The areas where we may face difficulties include:

- Diversion of management time, during the period of negotiation through closing and after closing, from its focus on operating the businesses to issues of integration,

- Decline in employee morale and retention issues resulting from changes in compensation, reporting relationships, future prospects or the direction of the business,

- The need to integrate each Company's accounting, management information, human resource and other administrative systems to permit effective management, and the lack of control if such integration is delayed or not implemented,

- The need to implement controls, procedures and policies appropriate for a public Company that may not have been in place in private companies, prior to acquisition,

- The need to incorporate acquired technology, content or rights into our products and any expenses related to such integration, and

- The need to successfully develop any acquired in-process technology to realize any value capitalized as intangible assets.

From time to time, we have also engaged in discussions with candidates regarding the potential acquisitions of our product lines, technologies and businesses. If a divestiture such as this does occur, we cannot be certain that our business, operating results and financial condition will not be materially and adversely affected. A successful divestiture depends on various factors, including our ability to:

- Effectively transfer liabilities, contracts, facilities and employees to any purchaser,

- Identify and separate the intellectual property to be divested from the intellectual property that we wish to retain,

- Reduce fixed costs previously associated with the divested assets or business, and

- Collect the proceeds from any divestitures.

In addition, if customers of the divested business do not receive the same level of service from the new owners, this may adversely affect our other businesses to the extent that these customers also purchase other products offered by us. All of these efforts require varying levels of management resources, which may divert our attention from other business operations.

If we do not realize the expected benefits or synergies of any divestiture transaction, our consolidated financial position, results of operations, cash flows and stock price could be negatively impacted.

WE MAY INCUR LOSSES IN THE FUTURE.

We have experienced net losses since inception. There can be no assurance that we will achieve or maintain profitability.

THE MARKET PRICE OF OUR COMMON STOCK MAY BE VOLATILE.

The market price of our common stock has been and is likely in the future to be volatile. Our common stock price may fluctuate in response to factors such as:

|

•

|

Announcements by us regarding liquidity, significant acquisitions, equity investments and divestitures, strategic relationships, addition or loss of significant customers and contracts, capital expenditure commitments, loan, note payable and agreement defaults, loss of our subsidiaries and impairment of assets,

|

|

|

•

|

Issuance of convertible or equity securities for general or merger and acquisition purposes,

|

|

|

•

|

Issuance or repayment of debt, accounts payable or convertible debt for general or merger and acquisition purposes,

|

|

|

•

|

Sale of a significant number of shares of our common stock by shareholders,

|

|

|

•

|

General market and economic conditions,

|

|

|

•

|

Quarterly variations in our operating results,

|

|

|

•

|

Investor relation activities,

|

|

|

•

|

Announcements of technological innovations,

|

9

|

•

|

New product introductions by us or our competitors,

|

|

|

•

|

Competitive activities, and

|

|

|

•

|

Additions or departures of key personnel.

|

These broad market and industry factors may have a material adverse effect on the market price of our common stock, regardless of our actual operating performance. These factors could have a material adverse effect on our business, financial condition and results of operations.

FUTURE ISSUANCE OF STOCK OPTIONS, WARRANTS AND /OR RIGHTS MAY HAVE A DILUTING FACTOR ON EXISTING AND FUTURE SHAREHOLDERS.

The grant and exercise of stock options, warrants or rights to be issued in the future will likely result in a dilution of the value of our common shares for all shareholders. hawse have established a Combined Incentive and Non-Qualified Stock Option Plan and may in the future issue further stock options to officers, directors and consultants which will dilute the interest of the existing and future shareholders. Moreover, we may seek authorization to increase the number of its authorized shares and sell additional securities and/or rights to purchase such securities at any time in the future. Dilution of

the value of the common shares will likely result from such sales, which in turn could adversely affect the market price of our common stock.

OUR CHIEF EXECUTIVE OFFICER HAS SUBSTANTIAL INFLUENCE OVER OUR COMPANY.

As of November 29, 2011, Mr. Erickson and his immediate family members, either directly or indirectly, own or control 5,256,473 shares as of the filing date or approximately 9.8% of our common stock and an additional 3,000,000 shares granted under the Stock Incentive Plan. These Controlling Shareholders have stated in a Schedule 13D that they may be deemed to constitute a “group” for the purposes of Rule 13d-3 under the Exchange Act. Mr. Ronald P. Erickson, our Chief Executive officer, controls each of our Controlling Shareholders.

This group, could cause a change of control of our board of directors, if in combination with another large shareholder elects candidates of their choice to the board at a shareholder meeting, and approve or disapprove any matter requiring stockholder approval, regardless of how our other shareholders may vote. Further, under Nevada law, the group could have a significant influence over our affairs, if in combination with another large shareholder, including the power to cause, delay or prevent a change in control or sale of the Company, which in turn could adversely affect the market price of our common stock.

TRADING IN THE COMPANY’S STOCK MAY BE RESTRICTED BY BLUE SKY ELIGIBILITY AND THE SEC’S PENNY STOCK REGULATIONS.

The SEC has adopted regulations which generally define "penny stock" to be any equity security that has a market price (as defined) less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exceptions. Under the penny stock rules, additional sales practice requirements are imposed on broker-dealers who sell to persons other than established customers and "accredited investors." The term "accredited investor" refers generally to institutions with assets in excess of $5,000,000 or individuals with a net worth in excess of $1,000,000 or annual income exceeding $200,000 or $300,000 jointly with their spouse. The penny stock rules require a

broker-dealer, prior to a transaction in a penny stock not otherwise exempt from the rules, to deliver a standardized risk disclosure document in a form prepared by the SEC which provides information about penny stocks and the nature and level of risks in the penny stock market. The broker-dealer also must provide the customer with current bid and offer quotations for the penny stock, the compensation of the broker-dealer and its salesperson in the transaction, and monthly account statements showing the market value of each penny stock held in the customer's account. The bid and offer quotations, and the broker-dealer and salesperson compensation information, must be given to the customer orally or in writing prior to effecting the transaction and must be given to the customer in writing before or with the customer's confirmation. In addition, the penny

stock rules require that prior to a transaction in a penny stock not otherwise exempt from these rules, the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser's written agreement to the transaction. These disclosure requirements may have the effect of reducing the level of trading activity in the secondary market for the stock that is subject to broker-dealers to trade in the Company’s securities.

The penny stock rules may discourage investor interest in and limit the marketability of, the Company’s common stock.

10

CONFLICT OF INTEREST.

Some of the directors of the Company are also directors and officers of other companies, and conflicts of interest may arise between their duties as directors of the Company and as directors and officers of other companies. These factors could have a material adverse effect on our business, financial condition and results of operations.

WE ARE DEPENDENT ON KEY PERSONNEL.

Our success depends to a significant degree upon the continued contributions of key management and other personnel, some of whom could be difficult to replace. We do not maintain key man life insurance covering certain of our officers. Our success will depend on the performance of our officers, our ability to retain and motivate our officers, our ability to integrate new officers into our operations and the ability of all personnel to work together effectively as a team. Our failure to retain and recruit officers and other key personnel could have a material adverse effect on our business, financial condition and results of operations.

WE HAVE LIMITED INSURANCE.

We have limited director and officer insurance and commercial insurance policies. Any significant claims would have a material adverse effect on our business, financial condition and results of operations.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

ITEM 2. PROPERTIES

Corporate Offices

Our executive office is located at 500 Union Street, Suite 406, Seattle, Washington, USA, 98101. On January 1, 2011, we entered into a lease with a party affiliated with our Chief Executive Officer. We pay $799 per month. The lease is cancellable with ten days' notice.

TransTech Facilities

TransTech leases a total of approximately 9,750 square feet of office and warehouse space for its administrative offices, product inventory and shipping operations, at a monthly rental of $4,292. The lease was extended from March 2011 for an additional five year term at a monthly rental of $4,751. There are two additional five year renewals with a set accelerating increase of 10% per 5 year term. TransTech also leases additional 500 square feet of off-site space at $250 per month from a related party.

ITEM 3. LEGAL PROCEEDINGS

There are no pending legal proceedings against us that are expected to have a material adverse effect on our cash flows, financial condition or results of operations.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

On April 29, 2011, the Company held its 2011 Annual Meeting of Stockholders. The results of the Annual Meeting are set forth below. Each of the matters considered at the meeting was described in detail in the definitive proxy statement on Schedule 14A that the Company filed with the Securities and Exchange Commission on January 31, 2011.

11

|

Proposal No 1 -

|

To elect eight nominees to serve on the Board of Directors until the 2012 Annual Meeting of Stockholders.

|

|

Ron Erickson

|

For

|

19,761,279

|

|

Withheld

|

37,375

|

|

|

Brad Sparks

|

For

|

18,751,279

|

|

Withheld

|

1,047,375

|

|

|

Jon Pepper

|

For

|

19,761,279

|

|

Withheld

|

37,375

|

|

|

Dr. Masahiro Kawahata

|

For

|

19,760,274

|

|

Withheld

|

38,380

|

|

|

Marco Hegyi

|

For

|

19,748,779

|

|

Withheld

|

49,875

|

|

|

Yoshitami Arai

|

For

|

19,760,279

|

|

Withheld

|

38,375

|

|

|

James Gingo

|

For

|

19,758,274

|

|

Withheld

|

40,380

|

|

|

Paul Bonderson

|

For

|

19,758,274

|

|

Withheld

|

40,380

|

|

Proposal No. 2 -

|

To adopt the Visualant, Inc. 2011 Stock Incentive Plan.

|

|

For

|

19,498,979

|

|

Against

|

168,445

|

|

Abstain

|

131,230

|

|

Non Vote

|

6,585,817

|

|

Proposal No. 3 -

|

To ratify the appointment of Madsen & Associates CPA’s, Inc. of Murray, Utah as the Company’s independent registered public accounting firm for the fiscal year ending September 30, 2011.

|

|

For

|

25,975,459

|

|

Against

|

165,053

|

|

Abstain

|

243,959

|

|

Non Vote

|

-

|

12

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock trades on OTCBB Exchange under the symbol "VSUL". The following table sets forth the range of the high and low sale prices of the common stock for the periods indicated:

|

Quarter Ended

|

High

|

Low

|

||||||

|

December 31, 2010

|

$ | 0.74 | $ | 0.23 | ||||

|

March 31, 2011

|

$ | 0.70 | $ | 0.33 | ||||

|

June 30, 2011

|

$ | 0.57 | $ | 0.21 | ||||

|

September 30, 2011

|

$ | 0.24 | $ | 0.08 | ||||

|

December 31, 2009

|

$ | 0.17 | $ | 0.04 | ||||

|

March 31, 2010

|

$ | 0.16 | $ | 0.05 | ||||

|

June 30, 2010

|

$ | 0.40 | $ | 0.05 | ||||

|

September 30, 2010

|

$ | 0.40 | $ | 0.14 | ||||

|

December 31, 2008

|

$ | 0.15 | $ | 0.01 | ||||

|

March 31, 2009

|

$ | 0.50 | $ | 0.03 | ||||

|

June 30, 2009

|

$ | 0.20 | $ | 0.05 | ||||

|

September 30, 2009

|

$ | 0.12 | $ | 0.05 | ||||

As of September 30, 2011, the closing price of the Company's common stock was $0.08 per share. As of November 29, 2011, there were 53,450,657 shares of common stock outstanding held by approximately 122 stockholders of record. The number of stockholders, including the beneficial owners' shares through nominee names is approximately 1,300.

DIVIDEND POLICY

We have never paid any cash dividends and intend, for the foreseeable future, to retain any future earnings for the development of our business. Our future dividend policy will be determined by the board of directors on the basis of various factors, including our results of operations, financial condition, capital requirements and investment opportunities.

RECENT SALES OF UNREGISTERED SECURITIES

During the three months ended September 30, 2011, there were no sales of unregistered sales of equity securities.

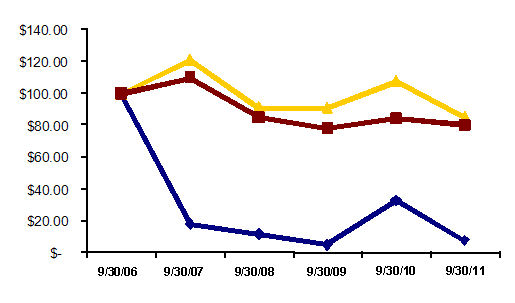

Performance Graph

Comparison of Cumulative Total Return

September 30, 2006-September 30, 2011

Among Visualant, Inc., Russell Microcap- Growth Index Without Dividend and the Russell Microcap Index Without Dividend

13

The above assumes that $100 was invested in the common stock and each index on September 30, 2006. Although the company has not declared a dividend on its common stock, the total return for each index assumes the reinvestment of dividends. Stockholder returns over the periods presented should not be considered indicative of future returns. The foregoing table shall not be deemed incorporated by reference by any general statement incorporating by reference the Form 10-K into any filing under the Securities Act or the Exchange Act, except to the extent the company specifically incorporates this information by reference, and shall not otherwise be deemed filed under the acts.

EQUITY COMPENSATION PLAN INFORMATION

The following table provides information as of September 30, 2011 related to the equity compensation plan in effect at that time.

|

(a)

|

(b)

|

(c)

|

||||||||||

|

Number of securities

|

||||||||||||

|

remaining available

|

||||||||||||

|

Number of securities

|

Weighted-average

|

for future issuance

|

||||||||||

|

to be issued upon

|

exercise price of

|

under equity compensation

|

||||||||||

|

exercise of outstanding

|

outstanding options,

|

plan (excluding securities

|

||||||||||

|

Plan Category

|

options, warrants and rights

|

warrants and rights

|

reflected in column (a))

|

|||||||||

|

Equity compensation plan

|

||||||||||||

|

approved by shareholders

|

6,920,000 | 0.296 | 80,000 | |||||||||

|

Equity compensation plans

|

||||||||||||

|

not approved by shareholders

|

- | - | - | |||||||||

|

Total

|

6,920,000 | 0.296 | 80,000 | |||||||||

ITEM 6. SELECTED FINANCIAL DATA

In the following table, we provide you with our selected consolidated historical financial and other data. We have prepared the consolidated selected financial information using our consolidated financial statements for the years ended September 30, 2011, 2010 and 2009. When you read this selected consolidated historical financial and other data, it is important that you read along with it the historical financial statements and related notes in our consolidated financial statements included in this report, as well as Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

|

Year Ended September 30,

|

||||||||||||||||||||

|

2011

|

2010

|

2009

|

2008

|

2007

|

||||||||||||||||

|

(in thousands, except for per share data)

|

||||||||||||||||||||

|

STATEMENT OF OPERATIONS DATA:

|

||||||||||||||||||||

|

Revenue

|

$ | 9,136 | $ | 2,543 | $ | - | $ | - | $ | - | ||||||||||

|

Net loss

|

(2,396 | ) | (1,147 | ) | (951 | ) | (945 | ) | (1,635 | ) | ||||||||||

|

Net loss applicable to Visualant, Inc. common shareholders

|

(2,410 | ) | (1,149 | ) | (951 | ) | (945 | ) | (1,635 | ) | ||||||||||

|

Net loss per share

|

(0.06 | ) | (0.04 | ) | (0.03 | ) | (0.05 | ) | (0.10 | ) | ||||||||||

|

BALANCE SHEET DATA:

|

||||||||||||||||||||

|

Total assets

|

4,313 | 4,144 | 12 | 2 | 89 | |||||||||||||||

|

Stockholder's deficiency

|

(1,610 | ) | (1,900 | ) | (1,366 | ) | (2,135 | ) | (1,478 | ) | ||||||||||

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Overview

We develop low-cost, high speed, light-based security and quality control solutions for use in homeland security, anti-counterfeiting, forgery/fraud prevention, brand protection ,process control applications, and diagnostics. Our patented and patent-pending technology uses controlled illumination with specific bands of light, to establish a unique spectral signature for both individual and classes of items. When matched against existing databases, these spectral signatures allow precise identification and authentication or diagnostics of any item or substance. This breakthrough optical sensing and data capture technology is called Spectral Pattern Matching (SPM). SPM technology lends itself to

flexible form factors and can be miniaturized, and is easily integrated into a variety of hand-held or fixed mount configurations, and can be a stand-alone device or combined in the same package as a bar-code or biometric scanner.

14

On September 6, 2011, the Company announced that it was issued US Patent No. 7,996,173, entitled “Method, Apparatus and Article to Facilitate Distributed Evaluation of Objects Using Electromagnetic Energy,” by the United States Office of Patents and Trademarks.

Through our wholly owned subsidiary, TransTech based in Aurora, Oregon, we provide value added security and authentication solutions to corporate and government security and law enforcement markets throughout the United States.

RESULTS OF OPERATIONS

The following table presents certain consolidated statement of operations information and presentation of that data as a percentage of change from year-to-year.

(dollars in thousands)

|

Year Ended September 30,

|

|||||||||||||||||

|

2011

|

2010

|

$ Variance

|

% Variance

|

||||||||||||||

|

Revenue

|

$ | 9,136 | $ | 2,543 | $ | 6,593 | 259.3 | % | |||||||||

|

Cost of sales

|

7,570 | 2,095 | 5,475 | -261.3 | % | ||||||||||||

|

Gross profit

|

1,566 | 448 | 1,118 | 249.6 | % | ||||||||||||

|

Research and development expenses

|

134 | 91 | 43 | -47.3 | % | ||||||||||||

|

Selling, general and administrative expenses

|

3,691 | 1,378 | 2,313 | -167.9 | % | ||||||||||||

|

Operating loss

|

(2,259 | ) | (1,021 | ) | (1,238 | ) | -121.3 | % | |||||||||

|

Other income (expense):

|

|||||||||||||||||

|

Interest expense

|

(213 | ) | (144 | ) | (69 | ) | -47.9 | % | |||||||||

|

Other income

|

67 | 10 | 57 | 570.0 | % | ||||||||||||

|

Total other expense

|

(146 | ) | (134 | ) | (12 | ) | -9.0 | % | |||||||||

|

Loss before income taxes

|

(2,405 | ) | (1,155 | ) | (1,250 | ) | -108.2 | % | |||||||||

|

Income taxes - current benefit

|

(9 | ) | (8 | ) | (1 | ) | -12.5 | % | |||||||||

|

Net loss

|

(2,396 | ) | (1,147 | ) | (1,249 | ) | -108.9 | % | |||||||||

|

Non-controlling interest

|

14 | 2 | 12 | -600.0 | % | ||||||||||||

|

Net loss attributable to Visualant, Inc. common shareholders

|

$ | (2,410 | ) | $ | (1,149 | ) | $ | (1,261 | ) | -109.7 | % | ||||||

YEAR ENDED SEPTEMBER 30, 2011 COMPARED TO THE YEAR ENDED SEPTEMBER 30, 2010

SALES

Net revenue for the year ended September 30, 2011 increased $6,593,000 to $9,136,000 as compared to $2,543,000 for the year ended September 30, 2010.

We closed the acquisition of TransTech of Aurora, OR on June 8, 2010 and recorded the results from June 8, 2010 to September 30, 2011.

COST OF SALES

Cost of sales for the year ended September 30, 2011 increased $5,475,000 to $7,570,000 as compared to $2,095,000 for the year ended September 30, 2010.

We closed the acquisition of TransTech of Aurora, OR on June 8, 2010 and recorded the results from June 8, 2010 to September 30, 2011.

SELLING, GENERAL AND ADMINISTRATIVE EXPENSE

Selling, general and administrative expenses for the year ended September 30, 2011 increased $2,313,000 to $3,691,000 as compared to $1,378,000 for the year ended September 30, 2010. $1,213,000 of such increase was due to increased employee and independent contractor expenses, amortization of identifiable intangible assets and intellectual property, professional and consulting fees, investor relation, legal, stock option and other general and administrative costs related to the expansion of the Company’s business.

In addition, TransTech selling, general and administrative expenses increased by $1,102,000. We closed the acquisition of TransTech of Aurora, OR on June 8, 2010 and recorded the results from June 8, 2010 to September 30, 2011.

During the year ended September 30, 2011, we recorded non-cash expenses of $1,204,000.

The selling, general and administrative expenses consisted primarily of research and development expenses, employee and independent contractor expenses, overhead, equipment and depreciation, amortization of identifiable intangible assets and intellectual property, professional and consulting fees, investor relation, legal, stock option and other general and administrative costs.

15

OTHER INCOME/EXPENSE

Other expense for the year ended September 30, 2011 was $146,000 as compared to other expense of $134,000 for the year ended September 30, 2010. The expenses for the year ended September 30, 2011 included $213,000 for interest expense, offset by $67,000 in other income.

The 2010 other expense included interest expense of $144,000, offset by other income of $10,000.

NET LOSS

Net loss for the year ended September 30, 2011 was $2,396,000 as compared to a net loss of $1,147,000 for the year ended September 30, 2010 for the reasons discussed above. The net loss included non-cash expenses of $1,204,000 and other business development and investor relation expenditures to expand the business.

RESULTS OF OPERATIONS

The following table presents certain consolidated statement of operations information and presentation of that data as a percentage of change from year-to-year.

(dollars in thousands)

|

Year Ended September 30,

|

|||||||||||||||||

|

2010

|

2009

|

$ Variance

|

% Variance

|

||||||||||||||

|

Revenue

|

$ | 2,543 | $ | - | $ | 2,543 | 100.0 | % | |||||||||

|

Cost of sales

|

2,095 | - | 2,095 | -100.0 | % | ||||||||||||

|

Gross profit

|

448 | - | 448 | 100.0 | % | ||||||||||||

|

Research and development expenses

|

91 | 214 | (123 | ) | 57.5 | % | |||||||||||

|

Selling, general and administrative expenses

|

1,378 | 683 | 695 | -101.8 | % | ||||||||||||

|

Operating loss

|

(1,021 | ) | (897 | ) | (124 | ) | -13.8 | % | |||||||||

|

Other income (expense):

|

|||||||||||||||||

|

Interest expense

|

(144 | ) | (54 | ) | (90 | ) | -166.7 | % | |||||||||

|

Other income

|

10 | - | 10 | 100.0 | % | ||||||||||||

|

Total other expense

|

(134 | ) | (54 | ) | (80 | ) | -148.1 | % | |||||||||

|

Loss before income taxes

|

(1,155 | ) | (951 | ) | (204 | ) | -21.5 | % | |||||||||

|

Income taxes - current benefit

|

(8 | ) | - | (8 | ) | 100.0 | % | ||||||||||

|

Net loss

|

(1,147 | ) | (951 | ) | (196 | ) | -20.6 | % | |||||||||

|

Non-controlling interest

|

2 | - | 2 | -100.0 | % | ||||||||||||

|

Net loss attributable to Visualant, Inc. common shareholders

|

$ | (1,149 | ) | $ | (951 | ) | $ | (198 | ) | -20.8 | % | ||||||

YEAR ENDED SEPTEMBER 30, 2010 COMPARED TO THE YEAR ENDED SEPTEMBER 30, 2009

SALES

Net revenue for the year ended September 30, 2010 increased $2,543,000 to $2,543,000 as compared to $0 for the year ended September 30, 2009.

We closed the acquisition of TransTech of Aurora, OR on June 8, 2010 and recorded the results from June 8, 2010 to September 30, 2010.

COST OF SALES

Cost of sales for the year ended September 30, 2010 increased $2,095,000 to $2,095,000 as compared to $0 for the year ended September 30, 2009.

We closed the acquisition of TransTech of Aurora, OR on June 8, 2010 and recorded the results from June 8, 2010 to September 30, 2010.

EXPENSES

Selling, general and administrative expenses for the year ended September 30, 2010 increased $695,000 to $1,378,000 as compared $682,000 for the year ended September 30, 2009.

16

We closed the acquisition of TransTech of Aurora, OR on June 8, 2010 and recorded the results from June 8, 2010 to September 30, 2010.

The selling, general and administrative expenses consisted primarily of employee and independent contractor expenses, overhead, equipment and depreciation, amortization of identifiable intangible assets and intellectual property, professional and consulting fees, sales and marketing costs, legal, stock option and other general and administrative costs.

OTHER INCOME/EXPENSE

Other expense for the year ended September 30, 2010 was $134,000 as compared to other expense of $54,000 for the year ended September 30, 2009. The expenses for the year ended September 30, 2010 included $144,000 for interest expense.

The 2009 other expense was primarily related to interest expense of $54,000.

NET LOSS

Net loss for the year ended September 30, 2010 was $1,147,000 as compared to a net loss of $951,000 for the year ended September 30, 2009.

LIQUIDITY AND CAPITAL RESOURCES

We had cash of $92,000, a net working capital deficit of approximately $3.2 million and total indebtedness of $2.6 million as of September 30, 2011.

We will need to obtain additional financing to implement the business plan, service our debt repayments and acquire new businesses. There can be no assurance that we will be able to secure funding, or that if such funding is available, whether the terms or conditions would be acceptable to us.

Volatility and disruption of financial markets could affect our access to credit. The current difficult economic market environment is causing contraction in the availability of credit in the marketplace. This could potentially reduce or eliminate the sources of liquidity for the Company.

If the Company is unable to obtain additional financing, we may need to restructure our operations, divest all or a portion of our business or file for bankruptcy.

OPERATING ACTIVITIES

Net cash used by operating activities for the year ended September 30, 2011 was $1.3 million. This amount was primarily related to a net loss of $2.4 million and an increase in accounts receivable and prepaid expenses of $.2 million, offset by depreciation and amortization and other non-cash expenses of $1.2 million and a decrease in inventory of $.2 million.

FINANCING ACTIVITIES

Net cash provided by financing activities for the year ended September 30, 2011 was $1.4 million. This amount was primarily related to proceeds from the sale of common stock of $.9 million and the proceeds from the issuance of convertible debt of $1.3 million, offset by payments on the debt of $.7 million.

Our contractual cash obligations as of September 30, 2011 are summarized in the table below:

|

Less Than

|

Greater Than

|

|||||||||||||||||||

|

Contractual Cash Obligations

|

Total

|

1 Year

|

1-3 Years

|

3-5 Years

|

5 Years

|

|||||||||||||||

|

Operating leases

|

$ | 287,825 | $ | 57,012 | $ | 114,024 | $ | 116,789 | $ | - | ||||||||||

|

Capital lease obligations

|

- | - | - | - | - | |||||||||||||||

|

Notes payable

|

2,551,773 | 1,537,191 | 1,012,261 | 2,321 | - | |||||||||||||||

|

Capital expenditures

|

345,000 | 80,000 | 105,000 | 80,000 | 80,000 | |||||||||||||||

|

Acquisitions

|

650,000 | 300,000 | 350,000 | - | - | |||||||||||||||

| $ | 3,834,598 | $ | 1,974,203 | $ | 1,581,285 | $ | 199,110 | $ | 80,000 | |||||||||||

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The application of GAAP involves the exercise of varying degrees of judgment. On an ongoing basis, we evaluate our estimates and judgments based on historical experience and various other factors that are believed to be reasonable under the circumstances.

17

Actual results may differ from these estimates under different assumptions or conditions. We believe that of our significant accounting policies (see summary of significant accounting policies more fully described in Note 2 to the financial statements set forth in this report), the following policies involve a higher degree of judgment and/or complexity:

INVENTORIES

Inventories consist primarily of printers and consumable supplies, including ribbons and cards, badge accessories, capture devices, and access control components held for resale and are stated at the lower of cost or market on the first-in, first-out (“FIFO”) method. Inventories are considered available for resale when drop shipped and invoiced directly to a customer from a vendor, or when physically received by TransTech at a warehouse location. The company records a provision for excess and obsolete inventory whenever an impairment has been identified. There is no provision for impaired inventory as of September 30, 2011.

REVENUE RECOGNITION

TransTech revenue is derived from products and services. Revenue is considered realized when the services have been provided to the customer, the work has been accepted by the customer and collectability is reasonably assured. Furthermore, if an actual measurement of revenue cannot be determined, we defer all revenue recognition until such time that an actual measurement can be determined. If during the course of a contract management determines that losses are expected to be incurred, such costs are charged to operations in the period such losses are determined. Revenues are deferred when cash has been received from the customer but the revenue has not been earned. The Company recorded deferred revenue of $0 as

of September 30, 2011 and 2010, respectively.

There is no SPM revenue at this time.

STOCK BASED COMPENSATION

The Company has share-based compensation plans under which employees, consultants, suppliers and directors may be granted restricted stock, as well as options to purchase shares of Company common stock at the fair market value at the time of grant. Stock-based compensation cost is measured by the Company at the grant date, based on the fair value of the award, over the requisite service period. For options issued to employees, the Company recognizes stock compensation costs utilizing the fair value methodology over the related period of benefit. Grants of stock options and stock to non-employees and other parties are accounted for in accordance with the ASC 505.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

We have no investments in any market risk sensitive instruments either held for trading purposes or entered into for other than trading purposes.

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

Reference is made to our consolidated financial statements beginning on page F-1 of this report.

ITEM 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

Not applicable.

ITEM 9A. CONTROLS AND PROCEDURES

MANAGEMENT'S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING

a) Evaluation of Disclosure Controls and Procedures

We have adopted and maintain disclosure controls and procedures (as such term is defined in Rules 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934, as amended (the “Exchange Act”)) that are designed to ensure that information required to be disclosed in our reports under the Exchange Act, is recorded, processed, summarized and reported within the time periods required under the SEC’s rules and forms and that the information is gathered and communicated to our management to allow for timely decisions regarding required disclosure.

As required by Rules 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934, our management conducted an evaluation of the effectiveness of the design and operation of our disclosure controls and procedures as of September 30, 2011. Our disclosure controls and procedures are designed to provide reasonable assurance that information required to be disclosed by us in the reports that we file or submit under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms, and our management necessarily was required to apply its judgment in evaluating and

implementing our disclosure controls and procedures. Based upon the evaluation described above, our management concluded that they believe that our disclosure controls and procedures were not effective, as of September 30, 2011, in providing reasonable assurance that information required to be disclosed by us in the reports that we file or submit under the Exchange Act is accumulated and communicated to our management to allow timely decisions regarding required disclosures, and is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms. Management identified the weaknesses discussed below.

18

Identified Material Weakness

A material weakness in our internal control over financial reporting is a control deficiency, or combination of control deficiencies, that results in more than a remote likelihood that a material misstatement of the financial statements will not be prevented or detected. Management identified material weaknesses during its assessment of internal controls over financial reporting as of August 31, 2011:

While we have an audit committee, the financial expert is not independent and attended 50% of the committee meetings. The Company is currently reviewing the financial expert situation.

The effectiveness of our internal control over financial reporting as of September 30, 2011 has not been audited by Madsen Associates, CPA’s Inc., an independent registered public accounting firm, as stated in their report which is included herein.

CHANGES IN INTERNAL CONTROL

There has been no change in our internal control over financial reporting during the quarter ended September 30, 2011 that has materially affected or is likely to materially affect our internal control over financial reporting.

ITEM 9B. OTHER INFORMATION

There were no disclosures of any information required to be filed on Form 8-K during the three months ended September 30, 2011 that were not filed.

PART III

Except as otherwise disclosed below, the following information required by the Instructions to Form 10-K is incorporated herein by reference from various sections of the Visualant, Inc. Proxy Statement for the annual meeting of shareholders to be held in March 2012, as summarized below:

ITEM 10. DIRECTORS AND EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

"Election of Directors;" "Section 16(a) Beneficial Ownership Reporting Compliance;" "Corporate Governance;" and "Meetings and Committees of the Board of Directors." – see the Visualant, Inc. Proxy Statement for the annual meeting of shareholders to be held in March 2012.

The following table sets forth, as of September 30, 2011, the name, age, and position of each executive officer and director and the tenure in office of each director of the Company.

|

Name

|

Age

|

Positions and Offices Held

|

Since

|

|

Ronald P. Erickson

|

67

|

Chief Executive Officer, Management Director

|

April 24, 2003

|

|

Mark Scott

|

58

|

Chief Financial Officer and Secretary

|

May 1, 2010

|

|

Bradley E. Sparks

|

65

|

Management Director

|

November 10, 2006

|

|

Jon Pepper

|

60

|

Independent Director

|

April 19, 2006

|

|

Dr. Masahiro Kawahata

|

75

|

Independent Director

|

April 19, 2006

|

|

Marco Hegyi

|

53

|

Chairman of the Board, Independent Director

|

February 14, 2008

|

|

Yoshitami Arai

|

80

|

Independent Director

|

October 8, 2008

|

|

James Gingo

|

59

|

Independent Director

|

June 8, 2010

|

|

Paul R. Bonderson Jr.

|

59

|

Independent Director

|

June 8, 2010

|

Business Experience Descriptions

Set forth below is certain biographical information regarding each of the Company's executive officers and directors.

19

Our Management Directors

RONALD P. ERICKSON has been a director and officer of the Company since April 24, 2003. He currently serves as the Company’s Chief Executive Officer and President. He was appointed to the positions of CEO and President on November 10, 2009. Earlier, he was appointed President and Chief Executive Officer of the Company on September 29, 2003, and resigned from this position on August 31, 2004 at which time he was appointed Chairman of the Board. A seasoned executive with more than 30 years of experience in the high technology, telecommunications, micro-computer, and digital media industries, Mr. Erickson was the founder of Visualant. In

addition to his Visualant responsibilities he also serves as Chairman of ivi, Inc. a streaming media company and eCharge Corporation an Internet based transaction processing company. He is formerly Chairman, CEO and Co-Founder of Blue Frog Media, a mobile media and entertainment company; Chairman, CEO and Co-founder of GlobalTel Resources, a provider of telecommunications services; Chairman, Interim President and CEO of Egghead Software, Inc. the large software reseller where he was an original investor; Chairman and CEO of NBI, Inc.; and Co-founder of MicroRim, Inc. the database software developer. Earlier, Mr. Erickson practiced law in Seattle and worked in public policy in Washington, DC and New York, NY. Additionally, Mr. Erickson has been an angel investor and board member of a number of public and private technology companies. In addition to his business activities Mr.

Erickson serves on the Board of Trustees of Central Washington University where he received his BA degree. He also holds a MA from the University of Wyoming and a JD from the University of California, Davis. He is licensed to practice law in the State of Washington and the District of Columbia.

JAMES GINGO has served as a director since June 8, 2010. He is the President and founder of TransTech Systems, Inc. (“TransTech”), since it was founded. TransTech is a distributor of access control and authentication systems serving the security and law enforcement markets. TransTech was acquired by the Company on June 8, 2010 and is a wholly owned subsidiary. James Gingo is a highly regarded industry veteran and one of the early members of the Document Security Alliance, an organization co-founded by the United States Secret Service and concerned industry representatives after the events of 9/11. He sits on the Board of the Security

Industry Association.

BRADLEY E. SPARKS currently serves as a director. On November 12, 2009, Mr. Sparks resigned as the Company’s Chief Executive Officer and President. He held these positions since November 2006. Mr. Sparks currently serves as the Chief Financial Officer for Laredo Oil, Inc. Before joining Visualant in 2006, he served as Chief Financial Officer of WatchGuard Technologies, Inc. from 2005-2006. Previous to WatchGuard, he was the founder and managing director of Sunburst Growth Ventures, LLC, a private investment firm specializing in emerging-growth companies. Earlier, he founded Pointer Communications and served as

Chief Financial Officer for several publicly-held telecommunications companies, including eSpire Communications, Inc., Digex, Inc., Omnipoint Corporation, and WAM!NET. He also served as Vice President and Treasurer of MCI Communications from 1988-1993 and as Vice President and Controller from 1993-1995. Before his tenure at MCI, Mr. Sparks held various financial management positions at Ryder System, Inc. Mr. Sparks also serves on the Board of Directors for iCIMS, a privately--held software company and Comrise China, also a privately—held company. Mr. Sparks graduated from the United States Military Academy at West Point and is a former Army Captain in the Signal Corps. He has an MS in Management from the Sloan School of Management at MIT and is a licensed CPA in Florida.

Our Independent Directors

JON PEPPER has served as an independent director since April 19, 2006. Mr. Pepper is the co-founder of Pepcom [www.pepcom.com], an industry leader at producing press-only technology showcase events around the country. Prior to that Pepper started the DigitalFocus newsletter, a ground-breaking newsletter on digital imaging that went to leading influencers worldwide. Pepper has been closely involved with the high technology revolution since the beginning of the personal computer era. He was formerly a well-regarded journalist and columnist; his work on technology subjects appeared in The New York Times, Fortune, PC Magazine, Men's Journal, Working Woman, PC

Week, Popular Science and many other well-known publications. Pepper was educated at Union College in Schenectady, New York and the Royal Academy of Fine Arts in Copenhagen.

DR. MASAHIRO KAWAHATA has served as an independent director since April 19, 2006. Dr. Kawahata is the former Director of the Fujitsu Research Institute. He is known in Japan as "the father of multimedia" for his work as National Program Director in developing the nationwide fiber optic network. Early in 2005, the U.S. Government officially acknowledged him as "Non-U.S. Scientist of Extraordinary Ability". Dr. Kawahata has taught at Tokai University, is a Consulting Professor at Stanford University, Provost's Distinguished Professor at the University of Southern California and Visiting Professor at the University of Washington. He has served as a Director

of numerous technology companies, and has received several prestigious awards in the United States and Japan.

MARCO HEGYI has served as an independent director since February 14, 2008 and as Chairman of the Board since May 2011. Mr. Hegyi has been a principal with the Chasm Group since 2006, where he combines his expertise in, and passion for helping companies expand their businesses with innovative technologies and collaborative partnership strategies using mobile and wireless platforms, service business models and Internet marketing

programs. Prior to working as a strategic advisor, Mr. Hegyi served as Senior Director, Global Product Management, at Yahoo Search Marketing during 2006. Prior to Yahoo, Mr. Hegyi was at Microsoft leading program management for Microsoft Windows and Office beta releases aimed at software developers from 2001 to 2006. While at Microsoft, he formed new service concepts and created operating programs to extend the depth and breadth of the company’s unparalleled developer eco-system, including managing offshore, outsource teams in China and India, and being the named inventor of a filed Microsoft patent for a business process in service delivery. Mr. Hegyi earned a Bachelor of Science degree in Information and Computer Sciences from the University of California, Irvine, and has completed advanced studies in innovation marketing, advanced management, and strategy at Harvard Business

School, Stanford University, UCLA Anderson Graduate School of Management, and MIT Sloan School of Management.

20

YOSHITAMI ARAI has served as an independent director since October 8, 2008. Mr. Arai brings strategic experience, a broad global business network, and sophisticated business acumen to the board. He has performed in many professional and civic capacities throughout Japan and abroad, and has served as Director and Senior Executive of international organizations including 7-Eleven, Tokyo Hotels, Systems International, Catalina Marketing and Sony.