Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - FARMERS NATIONAL BANC CORP /OH/ | d262050d8k.htm |

Farmers National Banc Corp.

Canfield, OH

(NASDAQ: FMNB)

Investor Presentation

September 30, 2011

Exhibit 99.1 |

2

Disclosure Statement

Forward-Looking Statements

This

presentation

contains

forward-looking

statements

within

the

meaning

of

the

Private

Securities

Litigation

Reform

Act

of

1995.

Forward-looking

statements

express

management’s

current

expectations,

forecasts

of

future

events

or

long-term-goals

and,

by

their

nature,

are

subject

to

assumptions,

risks

and

uncertainties.

Actual

results

could

differ

materially

from

those

indicated.

Farmers

National

Banc

Corp.

(“Farmers”)

refers

you

to

its

periodic

reports

and

registration

statements

filed

with

the

Securities

and

Exchange

Commission,

including

its

Annual

Report

on

Form

10-K

for

the

year

ended

December

31,

2010

and

Quarterly

Report

on

Form

10-Q

for

the

period

ended

September

30,

2011

which

have

been

filed

with

the

Securities

and

Exchange

Commission

and

are

available

on

Farmers’

website

(www.farmersbankgroup.com)

and

on

the

Securities

and

Exchange

Commission’s

website

(www.sec.gov),

for

additional

discussion

of

these

assumptions,

risks

and

uncertainties.

Forward-looking

statements

are

not

guarantees

of

future

performance

and

should

not

be

relied

upon

as

representing

management’s

views

as

of

any

subsequent

date.

Farmers

undertakes

no

obligation

to

update

forward-looking

statements,

whether

as

a

result

of

new

information,

future

events

or

otherwise,

except

as

may

be

required

by

law.

Use of Non-GAAP Financial Measures

This

presentation

contains

certain

financial

information

determined

by

methods

other

than

in

accordance

with

accounting

principles

generally

accepted

in

the

United

States

(“GAAP”).

These

non-GAAP

financial

measures

include

“Core

Deposits”

and

“Pre-tax,

Pre-

provision

Earnings”.

Farmers

believes

that

these

non-GAAP

financial

measures

provide

both

management

and

investors

a

more

complete

understanding

of

the

Company’s

deposit

profile

and

profitability.

These

non-GAAP

financial

measures

are

supplemental

and

are

not

a

substitute

for

any

analysis

based

on

GAAP

financial

measures.

Because

not

all

companies

use

the

same

calculation

of

“Core

Deposits”

and

“Pre-tax,

Pre-provision

Earnings”,

this

presentation

may

not

be

comparable

to

other

similarly

titled

measures

as

calculated

by other companies. |

3

Sound franchise with many opportunities for growth

Profitable throughout cycle and growing tangible book value per share

Diversified and growing revenue streams

Stable asset quality and strong core deposit franchise

Strong capital position and did not take TARP CPP

Operational excellence and brand development

Seasoned management team with knowledge of the Northeast Ohio

marketplace

Commence trading on NASDAQ effective September 15, 2011 (“FMNB”)

Compelling valuation:

0.78x of tangible book value

4.7x LTM pre-tax pre-provision earnings

Farmers offers a unique and strong platform for growth

Investment Highlights

7.7x LTM EPS

2.68% dividend yield |

4

Founded over 120 years ago

18 branches and 17 ATMs

Approximately 75 -

100 miles from

Cleveland, Pittsburgh & Erie

Branch Map in Mahoning Valley

Erie

Pittsburgh

Youngstown

Akron

Cleveland

Trumbull County

Mahoning

County

Columbiana County

Branch Locations

Trust Locations

Canton |

5

Note: Deposit data as of June 30, 2011

Source: FDIC

Opportunity for growth with approximately 9.5% deposit market share in the Mahoning

Valley Large regional competitors lack focus

Community competitors inwardly focused

Attractive Deposit Franchise –

Deposit Market Share by MSA & County

2011

Rank

Company

Branches

Dep.

($M)

Market

Share

1

Home Savings & Loan Co.

7

309.6

$

23.66%

2

Huntington National Bank

12

305.5

$

23.35%

3

PNC Bank National Assn

6

134.9

$

10.31%

4

Farmers National Bank of Canfield

4

123.6

$

9.44%

5

JPMorgan Chase Bank NA

3

90.3

$

6.90%

6

Consumers National Bank

3

85.6

$

6.54%

7

1st National Community Bank

4

85.2

$

6.51%

8

CFBank

2

78.9

$

6.03%

9

Keybank National Assn

1

48.8

$

3.73%

10

RBS Citizens National Assn

1

44.4

$

3.39%

Total For Institutions In Market

45

1,308.3

$

Columbiana - Top 10

2011

Rank

Company

Branches

Dep. ($M)

Market

Share

1

Huntington National Bank

42

1,978.9

$

24.16%

2

Homes Savings & Loan

21

1,241.3

$

15.16%

3

First Place Bank

19

1,188.0

$

14.51%

4

PNC Bank National Assn

23

909.2

$

11.10%

5

Farmers National Bank of Canfield

17

776.4

$

9.48%

6

JPMorgan Chase Bank NA

20

752.1

$

9.18%

7

Cortland Savings & Banking Co.

10

346.5

$

4.23%

8

First NB of Pennsylvania

8

246.2

$

3.01%

9

Keybank National Assn

6

172.2

$

2.10%

10

RBS Citizens National Assn

6

165.4

$

2.02%

Total For Institutions In Market

196

8,189.7

$

Tri-County - Top 10

2011

Rank

Company

Branches

Dep.

($M)

Market

Share

1

Huntington National Bank

17

$1,135.5

27.00%

2

Home Savings & Loan Co.

10

$776.1

18.45%

3

First Place Bank

12

$578.9

13.76%

4

PNC Bank Naitonal Assn

10

$527.1

12.53%

5

Farmers National Bank of Canfield

7

$478.8

11.38%

6

JPMorgan Chase Bank NA

7

$316.5

7.52%

7

First NB of Pennsylvania

5

$168.3

4.00%

8

Keybank National Assn

4

$87.9

2.09%

9

RBS Citizens National Assn

3

$87.1

2.07%

10

Cortland Savings & Banking Co.

2

$26.3

0.63%

Total For Institutions In Market

81

$4,205.8

Mahoning - Top 10

2011

Rank

Company

Branches

Dep.

($M)

Market

Share

1

First Place Bank

7

609.2

$

22.77%

2

Huntington National Bank

13

538.0

$

20.11%

3

JPMorgan Chase Bank NA

10

345.4

$

12.91%

4

Cortland Savings & Banking Co.

8

320.2

$

11.97%

5

PNC Bank National Assn

7

247.2

$

9.24%

6

Farmers National Bank of Canfield

6

174.0

$

6.50%

7

Home Savings & Loan Co.

4

155.6

$

5.81%

8

First NB of Pennsylvania

3

77.8

$

2.91%

9

Home FS&LA of Niles

1

61.5

$

2.30%

10

Middlefield Banking Co.

1

43.7

$

1.63%

Total For Institutions In Market

70

2,675.7

$

Trumbull - Top 10 |

6

Source: Regional Chamber, Youngstown-Warren, Ohio Metropolitan Profile

Valley Leads in Industrial Job Growth in NE Ohio, The Vindicator

Ohio’s Economic Impact Study –

September, 2011

Resources and infrastructure within 100 miles of the Mahoning Valley

Recently the Mahoning Valley has seen several important investments in new business

including:

Steelmaker V&M Star’s $650 million expansion

•

350,000 tons of steel tubing per year for the drilling of shale gas in the U.S.

•

About 350 jobs will be created once production begins

The

acquisition

of

WCI

Steel

by

OAO

Severstal

–

$327

million

investment

General

Motors

Lordstown

plant

building

the

Chevrolet

Cruze

next

generation

small

car

–

$230

million

investment

Ohio’s Natural Gas and Crude Oil Exploration and Production Industry and the

Emerging Utica Gas Formation

Impact regarding to:

•

Jobs (204,000 created or supported by 2015)

•

Income (Economic Output will increase by over $22 billion by 2015)

Economic Overview of Market Area

6.8 million people

18 Fortune 500 company world headquarters

95 colleges and universities campus locations

2 international airports; 3 regional airports

Lake Erie shipping

Ohio River ports

Northeast Ohio’s manufacturing productivity is on

track to outpace the rest of the nation by 10 percent

as early as 2015, according to a report released by

Team Northeast Ohio.

Youngstown-Warren metro area had the third-highest

job growth in the U.S. in the last 12 months.

Land acquisition, construction and labor costs are

significantly below national averages |

7

•

Performance-driven culture

•

Advancing automation and use of technology

•

Metrics-oriented accountability

•

Scaling organization to support growth

•

Diligent risk management

•

Expand fee-based business

•

Integrate sales efforts

•

Continue to drive name awareness

•

Unification of brand

•

Top graded talent to drive performance growth

•

De novo expansion and strategic acquisitions

•

Customer intimacy/decisions close to customer

•

Identify target markets and customer segments

•

Lead with commercial business/expand wallet share

Acquire Share of

Market/Share of

Customer

Operational

Excellence

Risk Management

Evolve Trust,

Insurance & Financial

Services

Brand Development

Talent

Farmers’

Strategy for Growth |

8

Established and experienced management team with over 173 years of combined

experience, 97 of which has been with Farmers

Experienced Management Team

FMNB

Industry

Previous Experience

John S. Gulas

(53)

President & CEO

3+

27+

Past executive roles with Key Bank, Sky Bank and Wachovia. Prior to Farmers, Mr. Gulas

served as President and CEO of Sky Trust Company and was responsible for a $6.0BN

trust company, a $1.2BN brokerage company and a $1.1BN private bank.

James H. Sisek

(65)

President & CEO of Farmers Trust

15+

36+

President and CEO of the Farmers Trust Company.

Carl D. Culp

(48)

EVP & CFO

22+

26+

25 years of experience in finance and accounting in the banking industry, and is a

Certified Public Accountant.

Mark L. Graham

(56)

SVP & Chief Credit Officer

34+

34+

Has been with Farmers for 33 years and has held a variety of positions within the bank,

all in the credit area.

Kevin J. Helmick

(39)

SVP of Retail Services

16+

16+

Responsible for the management of Farmers National Investments, Farmers Insurance

and all branch sales and operational functions. Mr. Helmick holds an MBA and CFP

designation.

Amber B. Wallace

(45)

SVP & Director of Marketing

3+

3+

Prior to joining the Farmers team, Ms. Wallace served as the Assistant Vice President of

Marketing and Physician Relations at Trumbull Memorial Hospital, where she managed a

$14MM endowment, a $1.5MM marketing budget and all physician contracts.

Mark A. Nicastro

(40)

VP & Director of Human Resources

2+

13+

Brings an MBA and more than 12 years experience in HR Management from both large

multi-national banks and regional community banks, including U.S. Bank and Sky Bank.

Brian Jackson

(42)

VP & Chief Information Officer

2+

18+

More than 17 years experience in the IT field.

Yrs. Of Experience |

9

March 2009 –

opportunistic acquisition of Butler Wick Trust Company, the largest trust

department in the Mahoning Valley

Assets under management have grown approximately 48% since acquisition to $901

million currently From December 31, 2008 through December 31, 2010:

Revenue¹

has grown $16.6 million or 52.9%

Total assets have increased $102.4 million or 11.6%

•

Loans have grown $38.4 million or 7.0%

Total deposits have increased $113.0 million or 17.4%

•

Core deposits²

have grown $113.3 million or 20.6%

Tangible book value per share has grown $0.12 or 2.1%

Fiserv Premier –

core operating system

Flexible system that offers unlimited accounts

Keeps current with compliance and regulatory changes

Offers multiple products and services that integrate into core system (i.e.

internet banking, ATMs, and GL) One of the top core system providers in the

nation SAN & Virtualization –

data management system

Data Storage: reduces disk space expenditures; allow for better utilization of

disk space Data Backup: consistent backups of all data and replicated at

DR Site

Disaster Recovery: able to recover from disaster in minutes

Overall reduced IT costs

Scalable to various network configurations

¹

Revenue defined as net interest income plus non-interest income;

excludes securities gains / losses;

²

Core

deposits

defined

as

Total

Deposits

–

Jumbo

Deposits

Recent Growth |

10

Butler Wick Trust Company Acquisition

Acquired

from

United

Community

Financial

Corporation

for

cash

on

March

31,

2009

Only locally owned trust company in the Mahoning Valley

Rebranded to Farmers Trust Company

Assets increased approximately 48% since acquisition

Contributed $4.9 million to non-interest income in 2010

Farmers Trust Company |

11

Meaningfully profitable every quarter during this cycle

Always paid quarterly cash dividend

High net interest margin which has expanded every year since 2006

4.10% December 31, 2010

Strong record of profitability

Average ROAA and ROAE from 2006 through 2010 of 0.75% and 8.60%,

respectively

Continue to invest in operations to support ongoing growth, yet maintain a strong

balance sheet

Historical Operating Results |

12

Pre-tax income excluding security gains and losses increased 12% from the third

quarter of 2010.

Investment commissions and trust fees for the third quarter of 2011 increased 63%

and 8%, respectively, from the third quarter of 2010.

Provision for loan losses for the third quarter of 2011 decreased $800 thousand

from the third quarter of 2010.

Annualized net charge-offs to average net loans outstanding improved to 0.43%

at September 30, 2011, compared to 1.31% at September 30, 2010.

Loans 30-89 days delinquent decreased to $3.4 million at September 30, 2011,

compared to $5.9 million at September 30, 2010.

Continued Strong Results –

Overview of Q3 2011 |

13

•

2010 net interest income increased 13%

over prior year period due to increase in

loan balances and lower cost of funds

•

Acquisition of Trust Company increased

non-interest income by 13.8% since first

quarter 2009¹

Growing and Diverse Revenue Stream

Note:

Revenue defined as net interest income plus non-interest income;

Excludes $225K gain on settlement of trust business and $2.7MM net gain on

securities ¹

Calculated as Q4 2010 trust revenue / Q1 2009 total revenue

Net Interest Margin

3.29%

3.33%

3.58%

3.88%

4.10%

3.00%

3.25%

3.50%

3.75%

4.00%

4.25%

4.50%

2006

2007

2008

2009

2010 |

14

Diverse loan mix

No national lending

No sub-prime lending

Farmers’

practice is to lend

primarily within its market area

Less than 1% of loan portfolio is

participations purchased

Less than 2% of loan portfolio is

construction loans

Loan Portfolio Mix

(September 30, 2011)

Overview of Loan Portfolio

Note: Dollars in thousands |

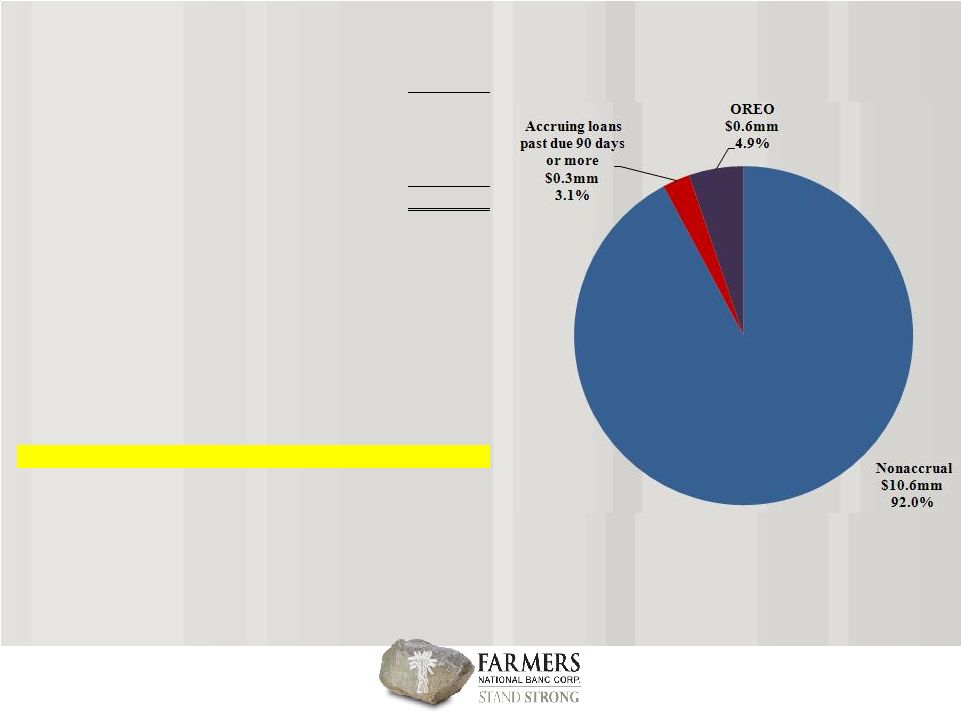

15

Excellent Asset Quality

Note:

Dollars

in

millions;

Asset

quality

ratios

exclude

troubled

debt

restructuring

9/30/2011

Nonaccrual loans

$10.6

Accruing loans past due 90 days or more

0.3

OREO

0.6

Total nonperforming assets (NPAs)

$11.5

Troubled Debt Restructuring (TDR)

$4.0

Loans 30-89 days delinquent

3.4

Gross portfolio loans

568.0

Loans held for sale (HFS)

0.0

Allowance for loan losses (ALL)

11.0

Total Assets

$1,086.4

NPLs & 90 days past due/Gross loans (excl. HFS)

1.92%

NPLs & 90 days past due/Gross loans (incl. HFS)

1.92%

NPAs/Total Assets

1.05%

TDR/Gross loans (excl. HFS)

0.70%

30-89 days delinquent/Gross loans (excl. HFS)

0.60%

ALL/NPLs & 90 days past due

100.92%

ALL/Gross loans (excl. HFS)

1.93% |

Financial Data for the

Period Ended September 30, 2011 Condition and Performance Metrics

Valuation Metrics

LTM

Core

Price/

Core

Price/

Price/

TCE/

LTM

LTM

PTPP ³/

Loans/

Dep/

NPAs/

NPL/

Res./

Res./

Tan.

Dep.

LTM

LTM

Div.

TA

ROAA

NIM

ROAA

Dep.

Tot Dep

Assets

Loans

Loans

NPLs

Book

Prem.

PTPP ³/

EPS

Yield

(%)

(%)

(%)

(%)

(%)

(%)

(%)

(%)

(%)

(%)

(x)

(%)

(x)

(x)

(%)

Peers

Midwest Banks ¹

7.12

0.49

3.57

1.40

81.7

86.3

2.62

3.06

2.05

72.8

0.82

(1.8)

3.9

11.4

1.16

National Banks ²

8.91

1.00

3.91

1.68

74.3

86.6

1.25

1.45

1.60

92.6

1.14

1.8

6.4

10.9

3.18

FMNB.OB

9.94

0.92

4.14

1.69

70.5

88.3

1.06

1.92

1.93

100.7

0.79

(3.2)

4.9

7.8

2.67

16

Relative to Comparable Midwest and National banks, Farmers is attractively

valued Farmers has an Attractive Valuation

Note: Peer data is the median value for the peer group; market data is as of

November 16, 2011; asset quality ratios exclude troubled debt restructurings

¹

Selected Midwest Banks with Assets $800 Million -

$2.0 Billion

²

Selected Capital & Credit Quality Banks with Assets $800 Million -

$2.0 Billion; No TARP; TCE / TA >= 7.0%; NPAs / Assets < 2.5% and Positive

LTM Net Income ³

Last 12 months pre-tax, pre-provision earnings

Source: SNL Financial |