Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Citadel Exploration, Inc. | coil8k.htm |

Citadel Exploration, Inc.

November 9, 2011

2

Forward Looking Statements

This presentation contains forward-looking statements, including without limitation those statements

regarding Citadel’s ability to exploit mining concessions. The statements and discussions contained in this

presentation that are not historical facts constitute forward-looking statements, which can be identified by

the use of forward-looking words such as "believes," "expects," "may," "intends," "anticipates," "plans,"

"estimates" and analogous or similar expressions intended to identify forward-looking statements. Citadel

wishes to caution the reader of this presentation that these forward-looking statements and estimates as

to future performance, estimates as to future valuations and other statements contained herein regarding

matters that are not historical facts, are only predictions, and that actual events or results may differ

materially. Citadel cannot assure or guarantee you that any future results described in this presentation

will be achieved, and actual results could vary materially from those reflected in such forward-looking

statements. We assume no obligation to update any forward-looking statements in order to reflect any

event or circumstance that may arise after the date of this presentation, other than as may be required by

applicable law or regulation.

regarding Citadel’s ability to exploit mining concessions. The statements and discussions contained in this

presentation that are not historical facts constitute forward-looking statements, which can be identified by

the use of forward-looking words such as "believes," "expects," "may," "intends," "anticipates," "plans,"

"estimates" and analogous or similar expressions intended to identify forward-looking statements. Citadel

wishes to caution the reader of this presentation that these forward-looking statements and estimates as

to future performance, estimates as to future valuations and other statements contained herein regarding

matters that are not historical facts, are only predictions, and that actual events or results may differ

materially. Citadel cannot assure or guarantee you that any future results described in this presentation

will be achieved, and actual results could vary materially from those reflected in such forward-looking

statements. We assume no obligation to update any forward-looking statements in order to reflect any

event or circumstance that may arise after the date of this presentation, other than as may be required by

applicable law or regulation.

3

Table of Contents

|

|

Page

|

|

Company Overview

|

4

|

|

Business Strategy

|

14

|

|

Financial Overview

|

17

|

|

Conclusion

|

20

|

4

Investment Highlights

|

Superior

Geographic Focus

|

§ California is in the early stages of an “Oil Renaissance”

§ Premium oil prices - indexed to Brent, approximately $20 over WTI

§ Lack of competition

§ Limited small cap E&P exposure for investors to profit from emerging trend

§ Larger independents entering Basin - drive future M&A and valuation

|

|

Strategic Partnership

|

§ Strategic Partnerships and non operator status

§ Sojitz Joint Venture - brings large corporation knowledge and operating experience

§ Lower cost structure increases economics and shareholder returns

§ Leverage family relationships to gain access to land

|

|

Strong

Oil & Gas Background

|

§ Founded by 4th generation oil family

§ Spent past 40 years generating California prospects

§ Access to unprecedented seismic database accumulated over 40-year period

|

|

Experienced

Management |

§ Over 20 years of E&P experiences across top executives

§ Founder taking zero salary until 1,000 Bblspd goal achieved

§ Compensated entirely via stock ownership and increasing shareholder value

|

5

Experienced Management Team

|

Armen Nahabedian

CEO, President & Director

|

§ Fourth Generation California oil and gas explorer

§ Enlisted in the Marines in 1999 specializing as an infantryman and translator while serving in

operation Iraqi Freedom § Joined his family’s oil business, Nahabedian Exploration Group (NEG) in 2003

§ Became a partner at NEG in 2007 and supervised land acquisition efforts and field operations

|

|

Daniel Szymanski

Chairman of the Board |

§ 20 years of industry experience, including assignments with Tenneco and Chevron and OXY

§ Served as Manager of Business Development at OXY’s headquarters in Los Angeles

§ Since 2008 has been an industry consultant and partner in seismic data firm

§ Bachelors in Geology, University of Wisconsin and Masters in Geophysics from Purdue

|

|

Christopher Whitcomb

Chief Financial Officer

|

§ 10 years of industry experience, CPA with degrees in both Accounting and Business Administration

§ Current CFO of Nahabedian Exploration Group

|

Company Overview

7

Company Overview

§ Company founded in 2011 by 4th generation oil family

§ Spent past 40 years generating California prospects

§ Currently have three drill ready oil projects located in

the San Joaquin and Salinas Basins of California

the San Joaquin and Salinas Basins of California

• Indian

• Landslide

• Rancho Grande (Pastoria Creek)

§ Exposure to 100+ MMBbls of oil

§ Strategic joint venture with Sojitz Corp. to acquire

250,000 gross acres in California

250,000 gross acres in California

§ Leveraging decades of experience in mature basins

utilizing modern technology

utilizing modern technology

Description

Geographic Overview

8

Background - Why California?

§ Historically dominated by majors

• Chevron - 174,000 Bblspd

• Aera (Shell/Exxon) - 151,000

• OXY - 65,000

• Plains Exploration - 35,000

• Berry Petroleum - 19,000

• Venoco - 6,000

§ Slow to adapt new technology due to “low hanging fruit”

• Perception of difficult working environment benefits

those with local working knowledge

those with local working knowledge

• Misconception regarding onerous environmental

restriction

restriction

o 3,000 wells permitted in 2010

§ Premium oil price

• Mature under utilized infrastructure

o Pipeline capacity exceeding 2 million Bblspd

vs. current production of 630,000 Bblspd

vs. current production of 630,000 Bblspd

• Refining capacity of 2 MMBblspd vs. 630 MBblspd

in production

in production

• Heavy oil currently at $20+ per barrel premium to

NYMEX/WTI prices

NYMEX/WTI prices

§ Conventional targets

• 3D driven exploration

• Implementation of horizontal drilling

• Multi seam completion potential.

• Relatively few wells drilled below 15,000’

§ Unconventional targets

• U.S Geological Survey (USGS) estimates 15 billion

Bbls recoverable from Monterey and Antelope

Shales

Bbls recoverable from Monterey and Antelope

Shales

• Higher oil prices coupled with new technology

unlocking source rock

unlocking source rock

Low Competition

Strong Potential

9

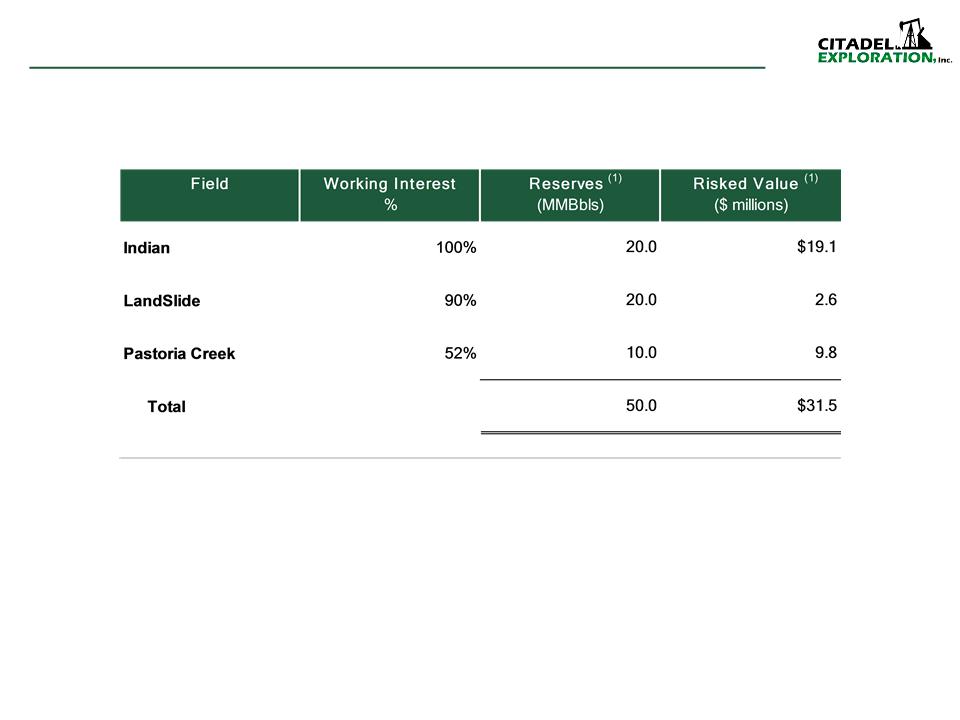

Asset Overview

(1) Based on Company projections.

10

Indian Prospect - Overview

§ Analogous to San Ardo oilfield

• Discovered by Chevron in 1950

• 600 MMBbls recovered

§ Shallow heavy oil - 13 API

• 688 acre lease

• 100% working interest - 79% NRI

• 100 MMBbls of oil in place

• 15 well pilot cyclic steam project

• Expected 20% recovery

§ 2012 CAPEX $3.5 million

§ Proof of concept expected by year-end 2012.

§ Full field development in 2013

• On sight steam facility $25 million

• 100’s of wells

• 1,500 Bblspd production in 2015

Description

Geographic Overview

11

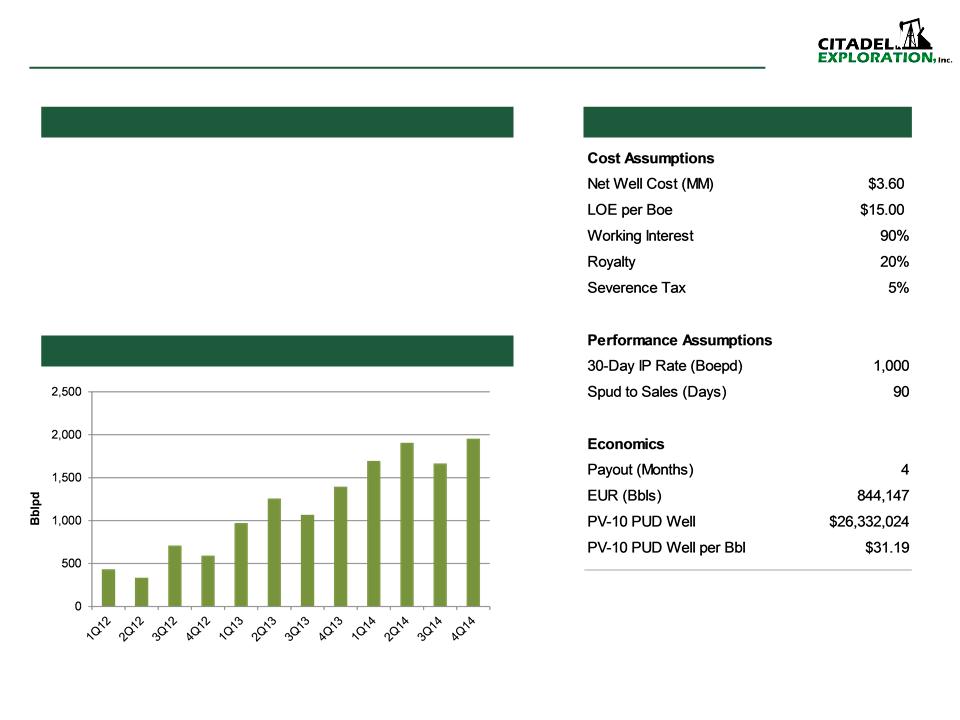

Indian Field - Development Plan

§ 15 wells in year 1 to “prove concept”

§ Build onsite steam facilities in 2013 - $25 million

§ 75 wells per year through 2016

§ Expect production to peak at 2,000 Bblspd in 2016

§ Decline rate: 15%, 10%, 10%

Description

Economics Summary

Production Forecast

12

LandSlide Prospect - Overview

§ Discovered in 1985 by Citadel founder’s father Mark

Nahabedian

Nahabedian

• Stevens Sand at 13,000’

• IP rates of 1,000+ Bblspd

• EUR’s of 500,000 to 2 million Bbls

• Drill and completion costs of $5 million

• 10 wells drilled 17 MMBbls recovered

• Existing infrastructure (OXY Owned/Operated)

underutilized

underutilized

§ Recently acquired adjoining block

• 3D seismic defined objective is up dip from 500,000

Bbl well

Bbl well

• Adjacent to well that recovered 2.7 MMBbls

§ Development and extension potential targeting 20 MMBbls

recoverable

recoverable

§ First well to SPUD December 2011

§ Expect to turn to sales within days of completion using

existing infrastructure

existing infrastructure

§ Target 2nd well from same surface location in 2nd half

2012

2012

Description

Geographic Overview

13

LandSlide Prospect - Development Plan

§ First well to SPUD December 2011

§ 45 days to drill and complete

§ Successful well sets up multi-year drilling campaign.

§ Full field potential of 20 MMBbls

§ Decline rate: 30%, 25%, 20%

Description

Economics Summary

Production Forecast

14

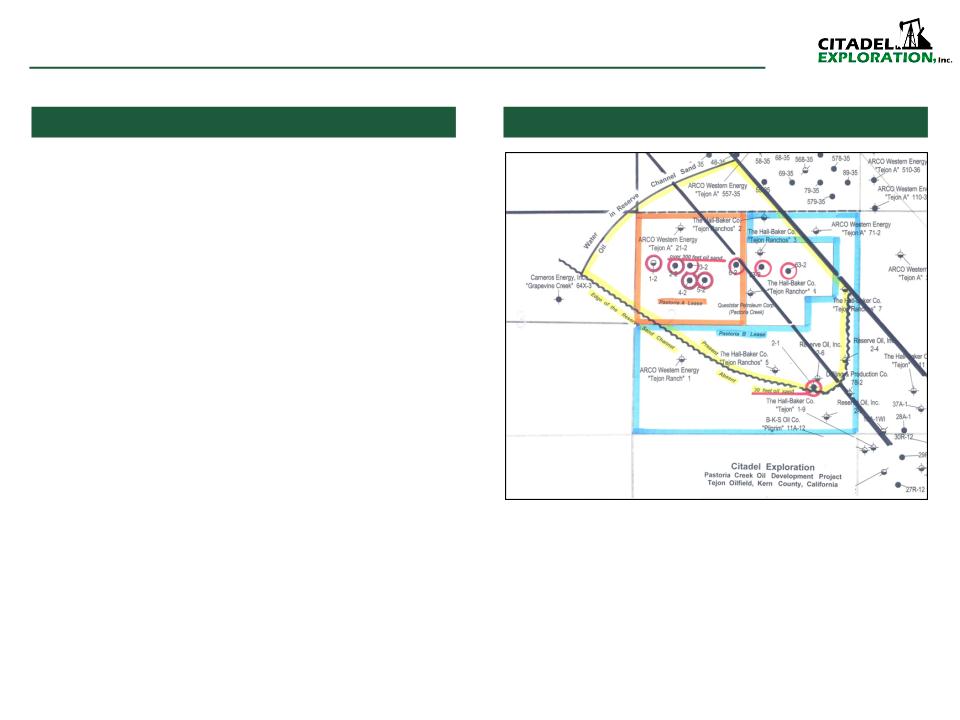

Pastoria Creek Prospect - Overview

§ Pastoria Creek A&B are to be developed in the early

stages of the Sojitz Joint Venture

stages of the Sojitz Joint Venture

§ On largest privately owned contiguous ranch in

California 250,000 acres

California 250,000 acres

§ Acquired 800 gross acres with partner Sojitz 48%

working interest

working interest

§ Defined by 3D seismic

§ Target formation at 3,200 feet

§ Drill and complete costs of $1.5 million

§ Field redevelopment program with up to 12 horizontal

wells and 6 vertical wells

wells and 6 vertical wells

§ Potential to recover 10 MMBbls (gross)

§ OXY currently redeveloping with horizontals in adjacent

fields

fields

Description

Geographic Overview

15

Pastoria Creek Prospect - Development Plan

§ Production forecast for only the first two areas for re-

development

development

§ Combination of horizontal and vertical wells

§ Additional field redevelopment opportunities and field

extensions

extensions

§ Decline rate: 40%, 30%, 25%

Description

Economics Summary

Production Forecast

Business Strategy

17

Sojitz Joint Venture - Overview

§ Sojitz Corporation - a trading company based in Tokyo, Japan

• Operates in construction, forestry, plastics, chemicals, mining, textiles and petroleum

• Formed in 2004 by the merger of Nissho Iwai Corp and Nichimen Corporation

• 2010 revenue of $41.3 billion and net income of $95 million

• Over 17,000 employees and 91 offices abroad

§ Joint Venture - Sojitz pays 90% of land acquisition costs

• Targeting 250,000 acres over next 24 months

§ Citadel has first right of refusal to earn from 25% up to 67.5% on a prospect by prospect basis

• Promoted on industry standard third for quarter basis on exploration well only.

§ Sojitz Operator - allows Citadel to leverage experienced operating team with a successful track record

• Texas Gulf Coast & Gulf of Mexico

18

Sojitz Joint Venture - Rancho Grande

§ 52,000 acres under lease

• Citadel can earn 25% to 67.5% working interest on

a prospect by prospect basis

a prospect by prospect basis

• Pastoria Creek A&B are the 1st fields to be

redeveloped

redeveloped

• Currently permitting 20 exploratory prospects

across acreage block

across acreage block

• 2D and 3D seismic coverage of prospects

• Expect first exploratory drilling in 1Q2012

§ Shallow objectives

• 50+ MMBbls

• 7,000 feet or less

§ Deeperobjectives

• 100+ MMBbls

• Up to 15,000 feet

§ 2012 CAPEX of $2 million

Description

Geographic Overview

Financial Overview

20

Financial Overview

Revenue ($ millions)

EBITDA ($ millions)

Daily Production (Bblspd)

CAPEX ($ millions)

21

Citadel Value Creation

22

Conclusion

|

Superior Geographic Focus

|

|

|

|

Strategic Partnership

|

|

|

|

Strong Oil & Gas Background

|

|

|

|

Experienced Management

|